Akihiko Inoue and Yumiharu Nakano

Department of Mathematics

Faculty of Science

Hokkaido University

Sapporo 060-0810

Japan

inoue@math.sci.hokudai.ac.jpDivision of Mathematical Sciences for Social Systems

Graduate School of Engineering Science

Osaka University

Toyonaka 560-8531, Japan

y-nakano@sigmath.es.osaka-u.ac.jp

(Date: May 5, 2006)

Abstract.

We consider a financial market model driven by an -valued

Gaussian process with stationary increments which is different from Brownian

motion. This driving noise process consists of independent components, and

each component has memory described by two parameters.

For this market model, we explicitly solve optimal investment problems.

These include (i) Merton’s portfolio optimization problem;

(ii) the maximization of growth rate of expected utility of wealth over

the infinite horizon;

(iii) the maximization of the large deviation probability

that the wealth grows at a higher rate than a given benchmark.

The estimation of paremeters is also considered.

Key words and phrases:

Optimal investment, long term investment, processes with memory,

processes with stationary increments, Riccati equations, large deviations

1. Introduction

In this paper we study optimal investment problems for a financial market

model with memory. This market model consists of risky

and one riskless assets. The price of the riskless

asset is denoted by and that of the th risky asset by .

We put , where denotes the transpose of a

matrix . The dynamics of the -valued process

are described by the stochastic differential

equation

(1.1)

while those of by the ordinary differential equation

(1.2)

where the coefficients , , and

are continuous deterministic functions on

and the initial prices are positive constants.

We assume that the volatility matrix

is nonsingular for .

The major feature of the model is the -valued

driving noise process which has memory.

We define the th component by the autoregressive type equation

(1.3)

where , , is an

-valued standard Brownian motion defined on a complete

probability

space , the derivatives and

are in the random distribution sense, and ’s and ’s are

constants such that

(1.4)

(cf. Anh and Inoue [1]).

Equivalently, we may define by the moving-average type

representation

(1.5)

(see [1, Examples 2.12 and 2.14]).

The components , , are Gaussian processes with

stationary increments

that are independent of each other. Each has short

memory that is described by the two parameters and .

In the special case ,

reduces to the Brownian motion .

Driving noise processes with short or long memory of this kind

are considered in [1], Anh et al. [2] and

Inoue et al. [20], for the case .

We define

where is the -null subsets of .

This filtration is the underlying

information structure of the market model .

From (1.5), we can easily show that

is a semimartingale with respect to

(cf. [1, Section 3]).

In particular, we can interpret the stochastic differential equation

(1.1) in the usual sense. In actual calculations, however, we need

explicit semimartingale representations of .

It should be noticed that (1.5) is not a semimartingale

representation of (except in the special case ).

For, involves the information of with

and vice versa.

The following two kinds of semimartingale representations of

are obtained in [2, Example 5.3] and [20, Theorem 2.1],

respectively:

(1.6)

(1.7)

where, for , is

the so-called innovation process, i.e., an

-valued standard Brownian motion such that

Notice that ’s are independent of each other.

The point of (1.6) and (1.7) is that

the deterministic kernels and are

given explicitly by

(1.8)

(1.9)

with

(1.10)

We have the equalities

(1.11)

Many authors consider financial market models in which the standard driving

noise, that is, Brownian motion, is replaced by a different one, such as

fractional Brownian motion, so that the model can capture

memory effect.

To name some related contributions, let us mention here

Comte and Renault [7, 8], Rogers [30], Heyde [16],

Willinger et al. [32], Barndorff-Nielsen and Shephard [5],

Barndorff-Nielsen et al. [4], Hu and Øksendal [18],

Hu et al. [19], Elliott and van der Hoek [9], and

Heyde and Leonenko [17].

In most of these references, driving noise processes are assumed to have

stationary increments since this is a natural requirement of

simplicity.

Among such models, the above model driven by which is

a Gaussian process with stationary increments is possibly

the simplest one. One advantage of is that, by the

semimartingale representations (1.6) and (1.7) of ,

it admits explicit calculations in problems such as those

considered in

this paper. Another advantageous feature of the model is

that, assuming ,

real constants, we can easily estimate the characteristic parameters

, and from stock price data.

We consider this parameter estimation in Appendix C.

For the market model , we consider an agent who

has initial endowment and invests

dollars in the th risky asset for

and dollars in

the riskless asset at each time , where denotes the agent’s

wealth at time . The wealth process is governed by the

stochastic differential equation

(1.12)

Here, we choose the self-financing strategy

from the admissible class

for the finite time horizon of length ,

where denotes the Euclidean norm of .

If the time horizon is infinite, we choose from the class

Let and .

In this paper, we consider the following three optimal investment

problems for the model :

(P1)

(P2)

(P3)

The goal of Problem P1 is to maximize the expected utility of

wealth at the end of the finite horizon.

This classical optimal investment problem dates back to Merton [25].

We refer to Karatzas and

Shreve [21] and references therein for work on this and related problems.

In Hu et al. [19], this problem is solved

for a Black–Scholes type model driven by fractional Brownian motion.

In Section 2, assuming for ,

we explicitly solve this problem for the model .

Our approach is based on a Cameron–Martin

type formula which we prove in Appendix A. This formula holds under the

assumption that a relevant Riccati type equation has a solution, and the key

step of our arguments is to show the existence of such a solution

(Lemma 2.1).

The aim of Problem P2 is to maximize the growth rate of

expected utility of wealth over the infinite horizon.

This problem is studied by Bielecki and Pliska

[6], and subsequently by other authors under various settings,

including Fleming and Sheu [11, 12], Kuroda and Nagai [22],

Pham [28, 29], Nagai and Peng [27], Hata and Iida [13],

and Hata and Sekine [14, 15].

In Section 3, we solve Problem P2 for the model by

verifying that a

candidate of optimal strategy suggested by the solution to Problem P1

is actually optimal. In so doing,

existence results on solutions to

Riccati type equations (Lemmas 2.1 and 3.5)

play a key role as in Problem P1.

The result of Nagai and Peng [27] on the

asymptotic behavior of solutions to Riccati equations,

which we review in Appendix B, is also an essential ingredient in

our arguments.

The purpose of Problem P3 is to maximize the large deviation probability that

the wealth grows at a higher rate than

the given benchmark .

This problem is studied by Pham

[28, 29], in which a significant result, that is, a duality relation

between Problems P2 and P3, is established.

Subsequently, this problem is studied by Hata and Iida

[13] and Hata and Sekine [14, 15] under different settings.

In Section 4, we solve Problem P3 for the market

model . In the approach of [28, 29],

one needs an explicit expression of .

Since our solution to Problem P2 is explicit, we can solve Problem

P3 for using this approach.

As in [28, 29], our solution to Problem 3 is given in the form of a

sequence of nearly optimal strategies.

For with certain constant ,

an optimal strategy, rather than such a nearly optimal sequence,

is obtained by ergodic arguments.

2. Optimal investment over the finite horizon

In this section, we consider the finite horizon optimization

problem P1 for the market model .

Throughout this section, we assume

and

By (1.1), (1.2), (1.6), and (1.12),

the wealth process evolves according to

whence, by the Itô formula, we have, for ,

(2.4)

We define an -valued process by

Since is a continuous Gaussian

process, the process is a -martingale

(see, e.g., Example 3(a) in Liptser and Shiryayev [23, Section 6.2]).

We define the -valued process by

where is the

conjugate exponent of , i.e.,

Notice that (resp. ) if

(resp. ).

In view of Theorem 7.6 in Karatzas and Shreve [21, Chapter 3],

to solve Problem P1, we only have to derive a stochastic integral

representation for .

We define an -valued -martingale by

Then, by Bayes’ rule, we have

for , where stands for the expectation with respect to

the probability measure on such that

.

Thus

(2.5)

We are to apply Theorem A.1 in Appendix A to (2.5).

By (1.11), the dynamics of are described by

the -dimensional stochastic differential equation

(2.6)

where ,

, and

with ’s as in (1.10).

Write for

. Then is an -valued standard Brownian

motion under . By (2.6), the process evolves

according to

(2.7)

where ,

with

(2.8)

(2.9)

By Theorem A.1 in Appendix A, we are led to consider

the following one-dimensional backward Riccati equations:

for

(2.10)

The following lemma, especially (iii), is crucial in our arguments.

If , then

(2.10) has a unique nonnegative solution .

(iii)

If and , then

(2.10) has a unique solution such that

for .

Proof.

(i) If , then (2.10) is linear,

whence it has a unique solution.

(ii) If , then , so that,

by the well-known result on Riccati

equations (see, e.g., Fleming and Rishel [10, Theorem 5.2] and

Liptser and Shiryayev [23, Theorem 10.2]),

(2.10) has a unique nonnegative solution.

(iii) When and , write

(2.11)

Then the equation for becomes

(2.12)

where

Since and , we see that

We write as

which is positive since .

Thus , so that

(2.12) has a unique nonnegative solution .

The desired solution to (2.10)

is given by .

∎

In what follows, we write for the unique solution to

(2.10) in the sense of Lemma 2.1.

Then satisfies

the backward matrix Riccati equation

(2.13)

where denotes the unit matrix.

For , let be the solution to the

following one-dimensional linear equation:

(2.14)

Then satisfies

the matrix equation

(2.15)

We put, for and ,

(2.16)

where

(2.17)

We are now ready to give the desired representation for .

The equality (2.19) follows from this.

A straightforward calculation based on (2.20), (2.6) and

the Itô formula gives ,

where is as in (2.18).

Thus the proposition follows.

∎

Recall that we have assumed and

(2.14). Here is the solution to Problem P1.

Theorem 2.3.

For , the strategy

defined by

(2.21)

is the unique optimal strategy for Problem P1.

The value function in (P1) is given by

(2.22)

Proof.

By Theorem 7.6 in Karatzas and Shreve [21, Chapter 3],

the unique optimal strategy for Problem P1 is given by

which, by (2.18), is equal to . Thus

the first assertion follows. By the same theorem in

[21],

.

This and (2.19) give (2.22).

∎

Remark 2.4.

We can regard , which is the only

random term on the right-hand side of (2.21),

as representing the memory effect.

To illustrate this point, suppose that is

a constant matrix.

Then, by (C.2) in Appendix C, we can express , whence ,

in terms of the past prices , , of the risky assets.

Regarding (2.1), we assume this to ensure the existence of

solution to (2.10) for .

Under the weaker assumption (1.4),

we could show by a different argument that, for ,

(2.10) has a solution

if , where

is defined by

From this, we see that

the same result as Theorem 2.3 holds under (1.4) if

, , where

.

However, we did not succeed in extending the result to the

most general case , .

Such an extension, if possible, would lead us to the solution of

Problem P3 under (1.4) (see Remark 3.8).

3. Optimal investment over the infinite horizon

In this section, we consider the infinite horizon optimization problem P2

for the financial market model .

Throughout this section, we assume (2.1) and the following two

conditions:

(3.1)

(3.2)

Here recall from

(2.2). In the main result of this section (Theorem 3.4),

we will also assume

, , where

(3.3)

with

(3.4)

Notice that .

To give the solution to Problem P2, we take the following steps:

(i)

For the value function in (P1), we calculate

the following limit explicitly:

we conclude that is an optimal strategy for Problem P2 and that

the optimal growth rate in (P2) is given by

.

Let and be its conjugate

exponent as in Section 2.

For , recall from (2.9).

We have , where

Notice that . We consider the equation

(3.8)

When , we write

for the unique solution of this linear

equation. If , then

so that we may write for the larger solution to the quadratic

equation (3.8). Let

Then .

As in Section 2,

we write for the unique solution to

(2.10) in the sense of Lemma 2.1.

Recall from (2.17).

The next proposition provides the necessary results on the asymptotic

behavior of .

Proposition 3.1.

Let , , and

. Then

(i)

is bounded in .

(ii)

.

(iii)

For such that ,

Proof.

If , then and for ,

so that the assertions follow from Theorem B.3 in Appendix B.

We assume .

Since

the function converges to exponentially fast as .

Hence the coefficients of the equation (2.10) converge to

their counterparts in (3.8) exponentially fast, too.

If , then the desired

assertions follow from Theorem B.1 in Appendix B

(due to Nagai and Peng [27]).

Suppose .

Let , and be as in (2.11).

Since and is bounded

from below in , so is

. To show that

is bounded from above in ,

we consider the solution to the linear equation

Since and

we have in . However,

as ,

so that is bounded from above in , whence

so is . The desired

assertions now follow from Theorem B.2 in Appendix B.

∎

where denotes the expectation with respect to

the probability measure on such that

.

Step 2. We continue the calculation of .

We are about to apply Theorem A.1 in Appendix A to (3.17).

Write for .

Then is an -valued standard Brownian motion under

. By (2.6), the process evolves according to

the -dimensional stochastic differential equation

(3.18)

where

,

with

For , let be the unique solution

to the one-dimensional backward Riccati equation

(3.19)

in the sense of Lemma 3.5 below, and

let be the solution to the

one-dimensional linear equation

(3.20)

Then, from (3.17)–(3.20) and Theorem A.1, we obtain

(3.21)

where, for and ,

Step 3. We compute the limit

in (3.6). Let .

Write

Then converges to , as , exponentially fast.

Now

which implies

(3.22)

Thus we may write for the larger (resp. unique) solution of

the following equation when (resp. ):

(3.23)

From (3.22), we also see that .

Let be the solution to

If and , then (3.19) has

a unique nonnegative solution .

(iii)

If and , then

(3.19) has a unique solution such that

for , where

is the solution to (2.10) in the sense

of Lemma 2.1 (iii).

Proof.

(i) When , (3.19) is linear, whence it

has a unique solution.

(ii) For and , we put

.

Since and ,

the larger solution to satisfies

if and only if

. However,

this is equivalent to . Thus, if

and , then or

, so that the Riccati equation

(3.19) has a unique nonnegative solution.

(iii) Suppose and .

For the solution to (2.10) in the sense of

Lemma 2.1 (iii), we consider

with . Since and

,

this Riccati equation has a unique nonnegative solution.

Thus the assertion follows.

∎

Proposition 3.6.

Let , , and

. Let be the unique solution to

(3.19) in the sense of Lemma 3.5,

and let be the larger (resp. unique) solution to

(3.23) when (resp. ).

Then

(i)

is bounded in .

(ii)

.

(iii)

For such that

,

Proof.

We assume and . Since

in and

is bounded from below

by Proposition 3.1, so is .

Let be the solution to the linear equation

By (3.22),

as ,

so that is bounded from above in .

Since and

we have, as in the proof of Proposition 3.1,

in . Thus is also bounded from

above in . Combining, is bounded in .

The rest of the proof is similar to that of Proposition

3.1, whence we omit it.

∎

Proposition 3.7.

Let , , and

. Let and be the solutions to

(3.20) and (3.24), respectively. Then

(i)

is bounded in .

(ii)

.

(iii)

For

such that ,

The proof of Proposition 3.7

is similar to that of Proposition 3.2; so

we omit it.

Remark 3.8.

We note that the proof of Lemma 3.5 (iii) is still valid

under (1.4) if there were a solution to

(2.10). This implies that, to prove an analogue of

Theorem 3.4 with , which is relevant to Problem P3,

for (1.4), one may show

the existence of such when . We did not succeed in

such an extension to Lemma 2.1 (iii) (see Remark 2.6).

4. Large deviations probability control

In this section, we study the large deviations probability control problem

P3 for the market model .

Throughout this section, we assume (2.1), (3.1),

(3.2) and

(4.1)

either or

.

For and ,

let be the growth rate defined by

We have .

Following Pham [28, 29],

we consider the optimal logarithmic moment generating function

For , we denote by the optimal

strategy in (3.14).

Recall from (P3).

From Theorem 3.4, Proposition 4.1,

and Pham [28, Theorem 3.1], we immediately obtain

the following solution to Problem P3:

Theorem 4.3.

We have

Moreover, if is such that

, then,

for , the sequence of strategies

is nearly optimal in the sense that

Remark 4.4.

Theorem 3.1 in Pham [28] is stated for a

model different from but the arguments there are

so general that we can prove Theorem 4.3 in the same way.

We turn to the problem of deriving an optimal strategy,

rather than a nearly optimal sequence, for the problem (P3)

when .

We define by

From Theorem 10.1 in Karatzas and Shreve [21, Chapter 3],

we see that

is the log-optimal or growth optimal strategy in

the sense that

We also find that a.s. for

.

Appendix A A Cameron–Martin type formula

In this appendix, we prove a generalization of the Cameron–Martin formula that we need in the proofs of Proposition 2.2 and

Theorem 3.4. We refer to Myers [26] for earlier work.

Let and let be the set of

real matrices.

We say that is symmetric if is a

symmetric matrix for all .

Let be the underlying

complete probability space equipped with filtration

satisfying

the usual conditions.

We assume that the -valued process

satisfies the -dimensional stochastic differential equation

where is an -valued standard -Brownian

motion and all the coefficients and

are deterministic, bounded measurable functions.

Theorem A.1.

Let and be

deterministic, bounded measurable functions. We assume that

is symmetric.

We also assume that there exists a bounded symmetric function

satisfying

the backward matrix Riccati equation

(A.1)

Let be the solution to the linear equation

(A.2)

Then,

for ,

Proof.

We put for .

Then, by the Itô formula,

Therefore,

is equal to

Since is a continuous Gaussian process, the process

is a martingale (cf. Example 3(a) in [23, Section 6.2]). Thus

Combining, we obtain the theorem.

∎

Appendix B Asymptotics for a solution to Riccati equation

Here we summarize the results on the asymptotics for

a solution to Riccati or linear equation that we need

in Section 3.

For ,

we consider the one-dimensional backward Riccati equation

(B.1)

where

(B.2)

for ,

(B.3)

for ,

(B.4)

for , converges to

exponentially fast as ,

(B.5)

and .

By (B.5), we may write for the larger solution to

the quadratic equation

For , write for the solution to

(B.7). Let be the solution of the linear equation

. Then

(i)

is bounded in .

(ii)

.

(iii)

For such that ,

Appendix C Parameter estimation

In this appendix, we use the special case of our model

in which ’s are constants, i.e.,

We explain how we can statistically estimate

the parameters , and

from stock price data.

This problem, for the univariate case , is discussed in

[3, 20]. Here we are interested in the multivariate case .

As for the expected rates of return ,

there is as usual a structural difficulty

in the statistical estimation of them

(cf. Luenberger [24, Chapter 8]),

whence we do not discuss it here.

(cf. [1], Examples 4.3 and 4.5). Notice that .

From (1.6) or (1.7)

and the Itô formula, the solution to

(1.1) is given by

(C.2)

for . Since has stationary increments, we may define

where cov denotes the covariance with respect to the

physical probability measure .

By (C.1) and (C.2), we see that

Suppose that we are given data consisting of closing prices of assets

observed at

a time interval of consecutive trading days.

For and ,

we denote by the price of the th asset

on the th day. Notice that here the time unit is the day.

Pick , and, for ,

define by

For , we consider the estimator

(C.3)

of ,

where .

The number 252, which is the average number of trading days in one

year,

converts the return into that per annum, while the number 100

gives the return in percentage.

We estimate the values of the parameters

, and by nonlinear least squares.

More precisely, we search for the values of them such that the following

least squares error is minimized:

We show numerical results obtained from the following daily stock

prices from September 18, 1995, through September 16, 2005:

Here we use closing prices adjusted for dividends and splits, which are

available at Yahoo! Finance [33],

rather than actually observed closing prices.

In this example, we have

The estimated values of the parameters are as follows:

Using the signed square root

,

we write

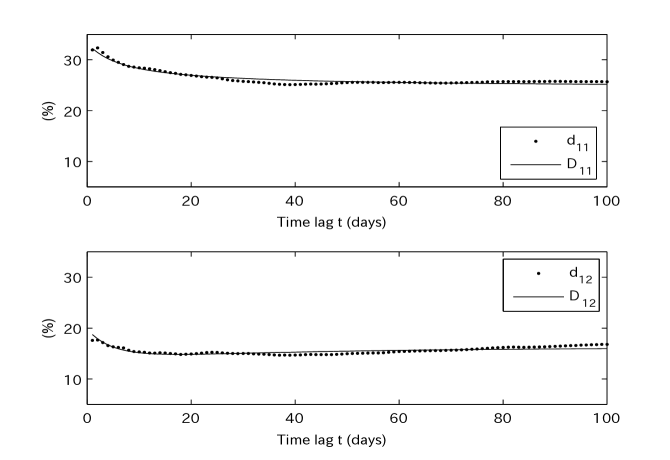

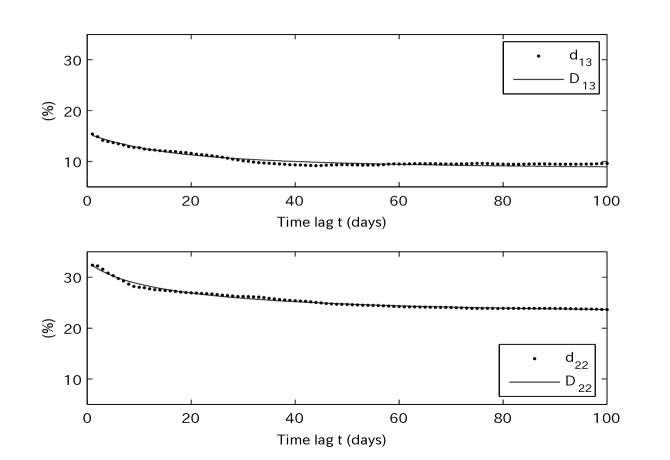

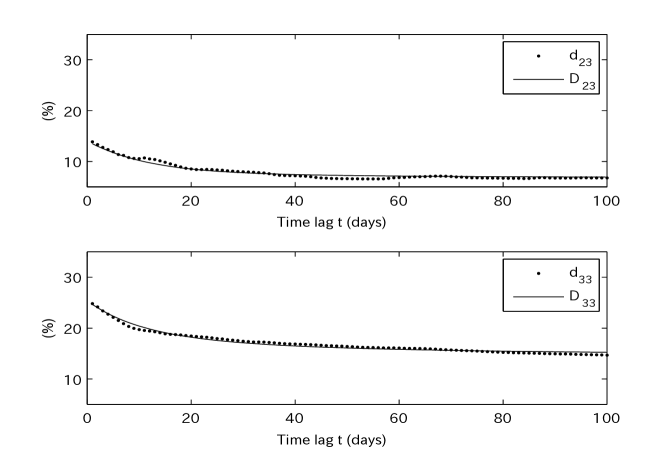

In Figures C.1–C.3, the dotted lines are

the graphs of ’s, while the corresponding solid lines represent

those of ’s that are obtained by using the nonlinear least

squares above. We see that the fitted functions

simultaneously approximate the corresponding sample values

well for this data set.

We have repeated this procedure for various data sets and

obtained reasonably good fits in most cases.

Figure C.1. vs. fitted and vs. fitted

.Figure C.2. vs. fitted and vs. fitted

.Figure C.3. vs. fitted and vs. fitted

.

Acknowledgements. We express our gratitude to Jun Sekine who suggested the use of a

Cameron–Martin type formula in the proof of Theorem 2.3.

The work of the second author was partially supported by a Research

Fellowship of the Japan Society for the Promotion of Science for

Young Scientists.

References

[1]V. Anh and A. Inoue.

Financial markets with memory I: Dynamic models.

Stoch. Anal. Appl., 23:275–300, 2005.

[2]V. Anh, A. Inoue and Y. Kasahara.

Financial markets with memory II: Innovation processes and expected

utility maximization.

Stoch. Anal. Appl., 23:301–328, 2005.

[3]V. Anh, A. Inoue and C. Pesee.

Incorporation of memory into the Black–Scholes–Merton theory and

estimation of volatility. Preprint.

[4]O. E. Barndorff-Nielsen, E. Nicalato and N. Shephard.

Some recent developments in stochastic volatility modelling.

Quant. Finance, 2:11–23, 2002.

[5]O. E. Barndorff-Nielsen and N. Shephard.

Non-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in

financial economics.

J. Roy. Statist. Soc. Ser. B, 63:167–241, 2001.

[6]T. R. Bielecki and S. R. Pliska.

Risk sensitive dynamic asset management.

Appl. Math. Optim., 39:337–360, 1999.

[7]F. Comte and E. Renault.

Long memory continuous-time models.

J. Econometrics, 73:101–149, 1996.

[8]F. Comte and E. Renault.

Long memory in continuous-time stochastic volatility models.

Math. Finance, 8:291–323, 1998.

[9]R. J. Elliott and J. van der Hoek.

A general fractional white noise theory and applications to finance.

Math. Finance, 13:301–330, 2003.

[10]W. H. Fleming and R. W. Rishel.

Deterministic and Stochastic Optimal Control.

Springer-Verlag, New York, 1975.

[11]W. H. Fleming and S. J. Sheu.

Risk-sensitive control and an optimal investment model.

Math. Finance, 10:197–213, 2000.

[12]W. H. Fleming and S. J. Sheu.

Risk-sensitive control and an optimal investment model (II).

Ann. Appl. Probab., 12:730–767, 2000.

[13]H. Hata and Y. Iida.

A risk-sensitive stochastic control approach to an optimal

investment problem with partial information.

Preprint.

[14]H. Hata and J. Sekine.

Solving long term optimal investment problems with Cox-Ingersoll-Ross

interest rates. Adv. Math. Econ., 8:231–255, 2006.

[15]H. Hata and J. Sekine.

Solving a large deviations control problem with a nonlinear factor

model. Preprint.

[16]C. C. Heyde.

A risky asset model with strong dependence through fractal activity time.

J. Appl. Prob., 36:1234–1239, 1999.

[17]C. C. Heyde and N. N. Leonenko.

Student processes.

Adv. in Appl. Probab., 37:342–365, 2005.

[18]Y. Hu and B. Øksendal.

Fractional white noise calculus and applications to finance.

Infin. Dimens. Anal. Quantum Probab. Relat. Top., 6:1–32, 2003.

[19]Y. Hu, B. Øksendal, and A. Sulem.

Optimal consumption and portfolio in a Black-Scholes market driven by

fractional Brownian motion.

Infin. Dimens. Anal. Quantum Probab. Relat. Top.,

6:519–536, 2003.

[20]A. Inoue, Y. Nakano and V. Anh.

Linear filtering of systems with memory and application to finance.

J. Appl. Math. Stoch. Anal., 2006, in press.

[21]I. Karatzas and S. E. Shreve.

Methods of mathematical finance.

Springer-Verlag, New York, 1998.

[22]K. Kuroda and H. Nagai.

Risk sensitive portfolio optimization on infinite time horizon.

Stoch. Stoch. Rep., 73:309–331, 2002.

[23]R. S. Liptser and A. N. Shiryayev.

Statistics of random processes. I. General theory, 2nd ed.

Springer-Verlag, New York, 2001.

[24]D. G. Luenberger, Investment science, Oxford University Press,

Oxford, 1998.

[25]R. Merton.

Optimal consumption and portfolio rules in a continuous time model.

J. Econom. Theory, 3:373–413, 1971.

[26]L. E. Myers.

Survival functions induced by stochastic covariance processes.

J. Appl. Prob., 18:523–529, 1981.

[27]H. Nagai and S. Peng.

Risk-sensitive dynamic portfolio optimization with partial

information on infinite time horizon.

Ann. Appl. Probab., 12:173–195, 2002.

[28]H. Pham.

A large deviations approach to optimal long term investment.

Finance Stoch., 7:169–195, 2003.

[29]H. Pham.

A risk-sensitive control dual approach to a large deviations

control problem.

Systems Control Lett., 49:295–309, 2003.

[30]L. C. G. Rogers.

Arbitrage with fractional Brownian motion.

Math. Finance, 7:95–105, 1997.

[31]L. C. G. Rogers and D. Williams.

Diffusions, Markov processes and Martingales, Vol. 2, 2nd ed.

Cambridge university press, Cambridge, 2000.

[32]W. Willinger, M. S. Taqqu, and V. Teverovsky.

Stock market prices and long-range dependence.

Finance Stoch., 3:1–13, 1999.

[33]Yahoo! Inc. Yahoo! Finance,

http://finance.yahoo.com/.