Benford’s Law, Values of -Functions and the Problem

Abstract.

We show the leading digits of a variety of systems satisfying certain conditions follow Benford’s Law. For each system proving this involves two main ingredients. One is a structure theorem of the limiting distribution, specific to the system. The other is a general technique of applying Poisson Summation to the limiting distribution. We show the distribution of values of -functions near the central line and (in some sense) the iterates of the Problem are Benford.

Key words and phrases:

Benford’s Law, Poisson Summation, -Function, , Equidistribution, Irrationality Type2000 Mathematics Subject Classification:

11K06, 60A10, 11B83, 11M06 (primary), 60F05, 11J86, 60J65, 46F12 (secondary).1. Introduction

While looking through tables of logarithms in the late 1800s, Newcomb [New] noticed a surprising fact: certain pages were significantly more worn than others. People were referencing numbers whose logarithm started with 1 more frequently than other digits. In 1938 Benford [Ben] observed the same digit bias in a wide variety of phenomenon.

Instead of observing one-ninth (about 11%) of entries having a leading digit of 1, as one would expect if the digits were equally likely, over 30% of the entries had leading digit 1, and about 70% had leading digit less than 5. Since and , one may speculate that the probability of observing a digit less than is , meaning that the probability of seeing a particular digit is . This logarithmic phenomenon became known as Benford’s Law after his paper containing extensive empirical evidence of this distribution in diverse data sets gained popularity. See [Hi1] for a description and history, [Hi2, BBH] for some recent results, and page 255 of [Knu] for connections between Benford’s law and rounding errors in computer calculations.

In [BBH] it was proved that many dynamical systems are Benford, including most power, exponential and rational functions, linearly-dominated systems, and non-autonomous dynamical systems. This adds to the ever-growing family of systems known or believed to satisfy Benford’s Law, such as physical constants, stock market indices, tax returns, sums and products of random variables, the factorial function and Fibonacci numbers, just to name a few.

We introduce two new additions to the family, the Riemann zeta function (and other -functions) and the Problem (and other -Maps), though we prove the theorems in sufficient generality to include other systems. Roughly, the distribution of digits of values of -functions near the critical line and the ratio of observed versus predicted values of iterates of the Map tend to Benford’s Law. For exact statements of the results, see Theorem 4.4 and Corollary 4.5 for -functions and Theorem 5.3 for the Problem. While the best error terms just miss proving Benford behavior for -functions on the critical line, we show that the values of the characteristic polynomials of unitary matrices are Benford in Appendix A; as these characteristic polynomials are believed to model the values of -function, this and our theoretical results naturally lead to the conjecture that values of -functions on the critical line are Benford.

A standard method of proving Benford behavior is to show the logarithms of the values become equidistributed modulo 1; Benford behavior then follows by exponentiation. There are two needed inputs. For both systems the main term of the distribution of the logarithms is a Gaussian, which can be shown to be equidistributed modulo by Poisson summation. The second ingredient is to control the errors in the convergence of the distribution of the logarithms to Gaussians. For -functions this is accomplished by Hejhal’s refinement of the error terms (his result follows from an analysis of high moments of integrals of ), and for the Problem it involves an analysis of the discrepancy of the sequence (which follows from is of finite type; see below).

The reader should be aware that the standard notations from number theory and probability theory sometimes conflict (for example, is used to denote the real part of a point in the complex plane as well as the standard deviation of a distribution); we try and follow common custom as much as possible. We denote the Fourier transform (or characteristic function) of by . Recall means as , and or means there is some constant such that for all sufficiently large, . Our proof of the Benford behavior of the problem uses the (irrationality) type of to control the errors; a number is of type if is the supremum of all with

| (1.1) |

By Roth’s theorem, every algebraic irrational is of type . See for example [HS, Ro] for more details.

2. Benford’s Law

To study leading digits, we use the mantissa function, a generalization of scientific notation. Fix a base and for a real number define the mantissa function, , from the unique representation of by

| (2.1) |

We extend the domain of mantissa to all of via

| (2.2) |

We study the mantissa of many different types of processes (discrete, continuous and mixed), and it is convenient to be able to use the same language for all. Take an ordered total space , for example or , and a (weak notion of) measure on such as the counting measure or Lebesgue measure. For a subset and an element , denote by the truncated set. We define the probability of via density in :

Definition 2.1.

, provided the limit exists.

For and the counting measure, , while if and is Lebesgue measure then . In Appendix A we extend our notion of probability to a slightly more general setting, but this will do for now.

For a sequence of real numbers indexed by , , and a fixed , consider the pre-image of mantissa, ; we abbreviate this by .

Definition 2.2.

A sequence is said to be Benford (base ) if for all ,

| (2.3) |

Definition 2.2 is applicable to the values of a function , and we say is Benford base if

| (2.4) |

We describe an equivalent condition for Benford behavior which is based on equidistribution. Recall

Definition 2.3.

A set is equidistributed modulo if for any we have

| (2.5) |

The following two statements are immediate:

Lemma 2.4.

if and only if the mantissa of and are the same, base .

Lemma 2.5.

if and only if has mantissa in .

The following result is a standard way to prove Benford behavior:

Theorem 2.6.

Let , so pointwise , and set . Then is equidistributed modulo 1 if and only if is Benford base .

Proof.

By Lemma 2.5, the set is the same as the set . Hence is equidistributed modulo 1 if and only if

| (2.6) |

if and only if is Benford base . ∎

Theorem 2.6 reduces investigations of Benford’s Law to equidistribution modulo , which we analyze below.

Remark 2.7.

The limit in Definition 2.1, often called the natural density, will exist for the sets in which we are interested, but need not exist in general. For example, if is the set of positive integers with first digit , then oscillates between its of and its of . One can study such sets by using instead the analytic density

| (2.7) |

where is the Riemann Zeta Function (see §4). A straightforward argument using analytic density gives Benford-type probabilities. In particular, Bombieri (see [Se], page 76) has noted that the analytic density of primes with first digit is , and this can easily be generalized to Benford behavior for any first digit.

3. Poisson Summation and Equidistribution modulo

We investigate systems converging to a system with associated logarithmic processes . For example, take some function and let . Then are truncations of , with log-process . When there is no ambiguity we drop the dependence on and write just for .

Let be a fixed probability density with cumulative distribution function . In our applications the probability densities of are approximately a spread version of such as . There is, however, an error term, and the log-process has a cumulative distribution function given by

| (3.1) | |||||

where is an error term. Our goal is to show that, under certain conditions, the error term is negligible and spreads to make equidistributed modulo as . This will imply that is Benford base .

In our investigations we need the density , cumulative distribution function and errors to satisfy certain conditions in order to control the error terms.

Definition 3.1 (Benford-good).

Systems with cumulative distribution functions are Benford-good if the satisfy (3.1), the probability density satisfies sufficient conditions for Poisson Summation (), and there is a monotone increasing function with such that and satisfy

Condition 1.

Small tails:

| (3.2) |

Condition 2.

Rapid decay of the characteristic function:

| (3.3) |

Condition 3.

Small truncated translated error:

| (3.4) |

for all .

In all our applications will be a Gaussian, in which case the Poisson Summation Formula holds. See for example [Da] (pages 14 and 63).

Condition 1 asserts that essentially all of the mass lies in . In applications will be the standard deviation, and this will follow from Central Limit type convergence.

Condition 2 is quite weak, and is satisfied in most cases of interest. For example, if is differentiable and is integrable (as is the case if is the Gaussian density), then , which suffices to show .

Condition 3 is the most difficult to prove for a system, and to our knowledge has not previously been analyzed in full detail. It is well known (see [Fe]) that there are some processes (for example, Bernoulli trials) with standard deviation of size where the best attainable estimate is . Errors this large lead to .

We now see why these conditions suffice. For , let denote the probability that . To prove becomes equidistributed modulo , we must show that . We would like to argue as follows:

| (3.5) | |||||

While the main term can be handled by a straightforward application of Poisson Summation, the best pointwise bounds for the error term are not summable over all . This is why Condition 1 is necessary, so that we may restrict the summation.

Theorem 3.2.

Assume log-processes are Benford-good. Then , where is equidistributed modulo 1.

Proof.

As the Fourier transform converts translation to multiplication, if then a straightforward calculation shows that for any fixed . Our assumptions on allow us to apply Poisson Summation to , and we find

| (3.6) |

Let . By Condition 1 and (3.1),

| (3.7) | |||||

By Condition 3, ; as is integrable we may return the sum to all at a cost of . The interchange of summation and integration below is justified from the decay properties of . To see this, simply insert absolute values in the arguments. Therefore using (3.6),

| (3.8) | |||||

As is a probability density, , and by Condition 2 the sum in (3.8) is . Therefore

| (3.9) |

which completes the proof. ∎

As an immediate consequence, we have:

Theorem 3.3.

Let (the truncation of ) have corresponding log-process . Assume the are Benford-good. Then is Benford base .

An immediate application of Theorem 3.3 is to processes where the distribution of the logarithms is exactly a spreading Gaussian (i.e., there are no errors to sum). We describe such a situation below.

Recall a Brownian motion (or Wiener process) is a continuous process with independent, normally distributed increments. So if is a Brownian motion, then is a random variable having the Gaussian distribution with mean zero and variance , and is independent of the random variable provided .

A standard realization of Brownian motion is as the scaled limit of a random walk. Let be independent Bernoulli trials (taking the values and with equal probability) and let denote the partial sum. Then the normalized process

| (3.10) |

(extended to a continuous process by linear interpolation) converges as to the Wiener process. See [Bi] or Chapter 2.4 of [KaSh] for further details.

A geometric Brownian motion is simply a process such that the process is a Brownian motion. It was known to Benford that stock market indices empirically demonstrated this digit bias, and for almost as long these indices have been modelled by geometric Brownian motion. Thus Theorem 3.3 implies the well-known observation that

Corollary 3.4.

A geometric Brownian motion is Benford.

4. Values of -Functions

Consider the Riemann Zeta function

| (4.1) |

Initially defined for , has a meromorphic continuation to all of . More generally, one can study an -function

| (4.2) |

where the coefficients have arithmetic significance. Common examples include Dirichlet -functions (where for a Dirichlet character ) and elliptic curve -functions (where is related to the number of points on the elliptic curve modulo ).

All the -functions we study satisfy (after suitable renormalization) a functional equation relating their value at to their value at . The region is called the critical strip, and the critical line. The behavior of -functions in the critical strip, especially on the critical line, is of great interest in number theory. The Generalized (or, as some prefer, Grand) Riemann Hypothesis, GRH, asserts that the zeros of any “nice” -function are on the critical line. The location of the zeros of is intimately connected with the error estimates in the Prime Number Theorem. The Riemann Zeta function can be expressed as the moment of the maximum of a Brownian Excursion, and the distribution of the zeros (respectively, values) of -functions is believed to be connected to that of eigenvalues (respectively, values of characteristic polynomials) of random matrix ensembles. See [BPY, Con, KaSa, KeSn] for excellent surveys.

We investigate the leading digits of -functions near the critical line, and show that the distribution of the digits of their absolute values is Benford (see Theorem 4.4 for the precise statement). The starting point of our investigations of values of the Riemann zeta function along the critical line is the log-normal law (see [Lau, Sel1]):

| (4.3) |

Thus the density of values of for are well approximated by a Gaussian with mean zero and standard deviation

| (4.4) |

Such results are often used to investigate small values of and gaps between zeros. As such, the known error terms are too crude for our purposes. In particular, one has (trivially modifying (4.21) of [Hej] or (8) of [Iv]) that

| (4.5) |

The main term is Gaussian with increasing variance, precisely what we require for equidistribution modulo 1. The error term, however, is too large for pointwise evaluation (as we have of the order intervals ).

Better pointwise error estimates are obtained for many -functions in [Hej]. These estimates are good enough for us to see Benford behavior as near the line . Explicitly, consider an -function (or a linear combination of -functions, though for simplicity of exposition we confine ourselves to the case of one -function) satisfying

Definition 4.1 (Good -Function).

We say an -function is good if it satisfies the following properties:

-

(1)

Euler product:

(4.6) -

(2)

has a meromorphic continuation to , is of finite order, and has at most finitely many poles (all on the line ).

-

(3)

Functional equation:

(4.7) where and

(4.8) with and .

-

(4)

For some , , we have

(4.9) -

(5)

The are (Ramanujan-Petersson) tempered: .

-

(6)

If is the number of zeros of with and , then for some we have

(4.10)

Remark 4.2.

There are many families of -functions which satisfy the above six conditions. The last two are the most difficult conditions to verify, as in all cases where these are known the first four conditions can be shown to be satisfied. The last two conditions are established for many -functions (for example, see [Sel1] for and [Luo] for holomorphic Hecke cuspidal forms of full level and even weight ; see Chapter 10 [IK] for more on the subject), and is an immediate consequence of GRH.

We quote a version of the log-normal law with better error terms (see (4.20) from [Hej] with a trivial change of variables in the Gaussian integral); for the convenience of the reader we list where the various parameters in Hejhal’s result are defined. The error terms will be pointwise summable, and allow us to prove Benford behavior.

Theorem 4.3 (Hejhal).

Let be a good -function as in Definition 4.1, and

For our purposes, a satisfactory choice is to take and . Then and

| (4.13) | |||||

We now show, in a certain sense, the values of are Benford. While any modest cancellation would yield the following result on the critical line, due to our error terms for each interval we must stay slightly to the right of .

Theorem 4.4.

Let be a good -function as in Definition 4.1; for example we may take . If the GRH and Ramanujan conjectures hold we may take any cuspidal automorphic -function; see also Remark 4.2. Fix a . For each , let . Then

| (4.14) |

Thus the values of the -function satisfy Benford’s Law in the limit (with the limit taken as described above) for any base .

Proof.

We first prove the claim for base , and then comment on the changes needed for a general base . Unfortunately the notation from number theory slightly conflicts with the standard notation from probability theory of §3. By Theorem 2.6, it suffices to show that

| (4.15) |

Let be the variance of the Gaussian in (4.3), which tends to infinity with . The standard deviation is thus , and corresponds to what we called in §3. Let be the standard normal (mean zero, variance one; plays the role of from §3 – as it is standard to denote -functions by , we use here and in §5), and set . Note is the density of a normal with mean zero and variance . By (4.3) we have

| (4.16) |

where . We must show the logarithms of the absolute values of the -function are Benford-good. As is a Gaussian it satisfies the conditions for the Poisson Summation Formula, and the log-process satisfies (3.1). Thus to apply Theorem 3.3 it suffices to show , and satisfy Conditions 1 through 3 for some monotone increasing function with . We take .

Condition 1 is immediately verified. To show we use (4.3) to conclude the contribution from the error is , and then note that the integral of the Gaussian with standard deviation past is small (as is the density of the standard normal, this integral is dominated by

| (4.17) |

which is ). Identical arguments show . As we are integrating a sizable distance past the standard deviation, it is easy to see that the contribution from the Gaussian is small. We do not need the full strength of the bounds in (4.3); the bounds from (4.5) suffice to control the errors.

Condition 2 follows from the trivial fact that is integrable. We now show Condition 3 holds. Here the bounds from (4.5) just fail. Using those bounds and summing over would yield an error of size . We instead use (4.3), and find for that

| (4.18) | |||||

because , and .

As all the conditions of Theorem 3.2 are satisfied, we can conclude that

| (4.19) |

We have shown that tending to infinity in this manner, the distribution corresponding to converges to being equidistributed modulo , which by Theorem 3.3 implies the values of are Benford base (as always, along the specified path converging to the critical line).

For a general base , note . The effect of changing base is that converges to a Gaussian with mean zero and variance (instead of mean zero and variance ). The argument now proceeds as before. ∎

Corollary 4.5.

Theorem 4.4 is valid if instead of intervals we consider intervals .

Proof.

Let . We consider the intervals and

| (4.20) |

We may ignore as it has length . For each interval , , we use (4.3) and argue as before. We may keep the same values of as before. and change, which implies changes; however, the leading term of is still , and again leads to negligible contributions. As there are only intervals, we may safely add all the errors. ∎

Remark 4.6.

If we stay a fixed distance off the critical line, we do not expect Benford behavior. This is because for a fixed , for we have a distribution function such that

| (4.21) |

Unlike the log-normal law (4.5), where the variance increases with , note here there is no increasing variance for fixed (though of course the variance depends on ); see [BJ, JW] for proofs. Thus to see Benford behavior it is essential that as increases our distance to the critical line decreases.

For investigations on the critical line, one can easily show Benford’s Law holds for a truncation of the series expansion of , where the truncation depends on the height . See (4.12) of [Hej] for the relevant version of the log-normal law (which has a significantly better error term than (4.3)). Similarly, one can prove statements along these lines for the real and imaginary parts of -functions.

Numerical investigations also support the conjectured Benford behavior. In Figure 1 we plot the percent of first digits of versus the Benford probabilities for , , and note the Benford behavior quickly sets in. Of course, we believe that this is strong evidence for Benford behavior exactly on the critical line, but as they stand, our error terms are too big and our cancellation too small to demonstrate this statement.

It is believed that values of characteristic polynomials of random matrix ensembles model values of -functions on the critical line. In Theorem A.2 of Appendix A we show that the digit distribution of the values of these characteristic polynomials converge to the Benford probabilities (as the size of the matrices tend to infinity), providing additional support for the conjecture that -functions are Benford on the critical line.

5. The Problem

People working on the Syracuse-Kakutani-Hasse-Ulam-Hailstorm-Collatz--Problem (there have been a few) often refer to two striking anecdotes. One is Erdös’ comment that “Mathematics is not yet ready for such problems.” The other is Kakutani’s communication to Lagarias: “For about a month everybody at Yale worked on it, with no result. A similar phenomenon happened when I mentioned it at the University of Chicago. A joke was made that this problem was part of a conspiracy to slow down mathematical research in the U.S.” Coxeter has offered $50 for its solution, Erdös $500, and Thwaites, £1000. The problem has been connected to holomorphic solutions to functional equations, a Fatou set having no wandering domain, Diophantine approximation of , the distribution of , ergodic theory on , undecidable algorithms, and geometric Brownian motion, to name a few (see [Lag1, Lag2]). We now relate the -Problem to Benford’s Law.

5.1. The Structure Theorem

If is a positive odd integer then is even, so we can find an integer such that , i.e. so that

| (5.1) |

is also odd. In this way, we get the -Map

| (5.2) |

We call the value of that arises in the definition of the -value of . Notice that is odd and relatively prime to , so the natural domain for iterating is the set of positive integers prime to and . Write , where is the set of possible congruence classes modulo 6. The total space is , not or , and the measure is the appropriate counting measure.

For every integer with , computers have verified that enough iterations of the -Map eventually send to the unique fixed point, 1. The natural conjecture asks if the same statement holds for all :

Conjecture 5.1 (-Conjecture).

For every , there is an integer such that .

Suppose we apply a total of times, calling and , . For each there is a -value, say , such that

| (5.3) |

We store this information in an ordered -tuple , called the -path of . Let denote the map sending to its -path,

| (5.4) |

The natural question is whether given an -tuple of positive integers , there is an integer whose -path is precisely this -tuple. If so, we would like to classify the set of all such . In other words, we want to study the inverse map .

The answer is given by the Structure Theorem, proved in [KonSi]: for each -tuple , not only does there exist an having this -path, but this path is enjoyed by two full arithmetic progressions, , and we can solve explicitly for and . In fact, , and (so the progressions are full; we do not miss any terms at the beginning). Moreover, the two progressions fall into the two possible equivalence classes modulo 6; i.e., . The structure theorem is the key ingredient in analyzing the limiting distributions. These will satisfy the conditions of our main theorem (Theorem 3.3), and yield Benford’s Law.

Recall (Definition 2.1) that we define the probability of a subset by

| (5.5) |

provided the limit exists. We say a random variable has geometric distribution with parameter (for brevity, geometrically distributed) if for . A consequence of the structure theorem is that

| (5.6) |

Both the expectation and variance of a geometrically distributed random variable is . For a seed let be the th iterate. A natural quantity to investigate is , where is the expected value of .

Theorem 5.2 ([KonSi]).

The -values are independent geometrically distributed random variables. Further, for any

| (5.7) |

where is the sum of geometrically distributed (with parameter ) i.i.d.r.v. By the Central Limit Theorem, the right hand side converges to a Gaussian integral as . The paths are also independent, and so the -Paths are those of a geometric Brownian motion with drift .

We remind the reader that a Brownian motion (and hence a geometric Brownian motion) can be realized as the limit of a random walk; the same phenomenon occurs here. The drift corresponds to the fact that the expected value is , rather than just .

It is worth remarking that a consequence of the drift being (which is negative) is that it is natural to expect that typical trajectories return to the origin. This statement extends completely to -Maps discussed in Appendix B. Theorem 5.2 is immediately applicable to investigations in base two (which is uninteresting as all first digits are 1). To study the Problem in base , one simply multiplies by , as . This replaces with or .

5.2. A Tale of Two Limits

The -system, , is probably not Benford for any starting seed as we expect all of the terms to eventually be 1. If we stop the sequence after hitting 1 and consider the proportion of terms having a given leading digit , this is a rational number, whereas is not. Of course, this rational number should be close to , but it is difficult to quantify this proximity since it is easy to find arbitrarily large numbers decaying to 1 after even one iteration of the -map.

One sense in which Benford behavior can be proved is the same as the sense in which -paths are those of a geometric Brownian motion. We use the structure theorem to prove

Theorem 5.3.

Let be any real number such that is irrational of type ; for example, one may take any integer which is not a perfect power of (see (1.1) for a definition of type and Theorem B.1 for a proof of the irrationality type of such integers). Then for any ,

| (5.8) |

As is the expected value of , this implies the distribution of the ratio of the actual versus predicted value after iterates obeys Benford’s Law (base ). If for some integer , in the limit takes on the values with equal probability, leading to a non-Benford digit bias depending only on .

Notice that since probability is defined through density, this is really two highly non-interchangeable limits:

| (5.9) |

Though this is completely natural, it is worth remarking for the sake of precision. Of course, a good starting seed (one with a long life-span) should give a close approximation of Benford behavior, just as it will also be a generic Brownian sample path; this is supported by numerical investigations (see §5.4).

Let be independent geometrically distributed random variables with , , and , . Let . Let , . We know the distribution of is the same as that of . The proof is complicated by the fact that the sum of geometrically distributed random variables itself has a binomial distribution, supported on the integers. This gives a lattice distribution for which we cannot obtain sufficient bounds on the error, even by performing an Edgeworth expansion and estimating the rate of convergence in the Central Limit Theorem. The problem is that the error in missing a lattice point is of size , and we need to sum terms (for some ). We are able to surmount this obstacle by an error analysis of the rate of convergence to equidistribution of .

5.3. Proof of Theorem 5.3

To prove Theorem 5.3 we first collect some needed results. The proof is similar in spirit to Theorem 3.3, with the needed results playing a similar role as the three conditions; however, the discreteness of the problem leads to some interesting technical complications, and it is easier to give a similar but independent proof than to adjust notation and show Conditions 1 through 3 are satisfied.

In the statements below, is an arbitrary sub-interval of . By the Central Limit Theorem, the distribution of (although it only takes integer values) is approximately a Gaussian with standard deviation of size . Let and set . Let

| (5.10) |

and be an irrational number of type (see (1.1)). Soundararajan informed us that one does not need to be of finite type for our applications. For integer , if then it is at least , and one obtains instead of in (5.15); the advantage of using finite type is we obtain sharper estimates on the rate of convergence, as well as being able to handle non-integral bases .

Let denote the density of the standard normal:

| (5.11) |

We collect some results needed for the proof of Theorem 5.3:

-

•

From the Central Limit Theorem (see [Fe], Chapter XV): For any ,

(5.12) We may write as for some monotone increasing which tends to infinity. We use this to approximate the probability of . For future use, choose any monotone tending to infinity such that , and . As with , if is sufficiently small then such an exists.

-

•

Let . Then

(5.13) In practice this implies that for the we must study, there is negligible variation in the Gaussian for .

- •

-

•

For any , letting we have

(5.15) The quantification of the equidistribution of is the key ingredient in proving Benford behavior base (with ). The rate of equidistribution, given the finiteness of the irrationality type of , follows from the Erdös-Turan Theorem. As this is the key argument in our analysis, we provide a sketch of the proof in Appendix B; see Theorem 3.3 on page 124 of [KN] for complete details (while the proof given only applies for , a trivial translation yields the claim for any ).

Proof of Theorem 5.3.

We must show that as , for any ,

| (5.16) |

tends to . We have

| (5.17) | |||||

The second sum in (5.17) is bounded by

| (5.18) |

By the Central Limit Theorem, (5.18) is . Alternatively, using the techniques below (with ), one can show , which implies (5.18) is . As we are not summing (5.18), it is okay to have an error here of size (and errors of approximately this size arise if we add or subtract a lattice point). Therefore

| (5.19) | |||||

The proof is completed by showing the above is . Consider an interval . By (5.15), the number of such that is , . By (5.12), the probability of each such is . We now use (• ‣ 5.3) to bound the error from evaluating all the at and find

| (5.20) |

summing over all gives . This gives four sums, which we must show are .

The sums over of the first and fourth pieces of (5.3) are handled by Poisson Summation. We have for the first piece that

| (5.21) |

As , the second sum in (5.3) is bounded by

| (5.22) |

Using (5.14) with gives

| (5.23) | |||||

as the final sum over is bounded by a geometric series and with . Thus the first piece from (5.3) gives .

As the Gaussian is a monotone function (for or ), a similar argument shows the sum over of the fourth piece of (5.3) contributes . It is here that we use is a very special equidistributed sequence modulo , namely it is of the form . This allows us to control the discrepancy (how many give ).

We must now sum over the second and third pieces of (5.3). For the second piece, we have

| (5.24) |

As and with , we have

| (5.25) |

Recall we chose and such that . Therefore

| (5.26) |

As we chose such that , the sum in (5.24) is

| (5.27) |

proving the second piece in (5.3) is negligible.

We are left with the sum over of the third piece in (5.3). Its contribution is

| (5.28) |

Collecting the evaluations of the sums of the four pieces in (5.3), we see that

| (5.29) |

which completes the proof of Theorem 5.3 if (and thus proves Benford behavior base because, by Theorem B.1, has finite irrationality type).

Consider now the case when . As takes on integer values, the possible values modulo 1 for are . An identical argument shows each of these values is equally likely; by determining which intervals they lie in, one can determine the (non-Benford) digit bias in this case. See also §5.4. ∎

5.4. Numerical Investigations

Theorem 5.3 implies that the first digit of

will not be Benford

in a base . As takes on integer values, is equally likely to be any of

. We considered seeds

congruent to 1 modulo 6, starting at . We can

rapidly analyze the behavior of such large numbers by representing

each number as an array and then performing the required

operations (multiplication by , addition by and division by

) digit by digit. Taking , we analyzed the first digits

for and . We

have (theoretical predictions in parentheses)

| First | |||||||

|---|---|---|---|---|---|---|---|

| Digit | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| Base | 50.2% (50.0%) | 49.8% (50.0%) | 0% | N/A | N/A | N/A | N/A |

| Base | 33.1% (33.3%) | 33.6% (33.3%) | 0% | 33.3% (33.3%) | 0% | 0% | 0% |

In base 16, we only observe digits 1, 2, 4 and 8; all should occur

of the time; we observe them with frequencies and . In base 10, we observe

| First Digit | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| Observed | 29.8% | 17.9% | 12.1% | 10.0% | 8.5% | 9.8% | 2.4% | 8.7% | 0.9% |

| Benford | 30.1% | 17.6% | 12.5% | 9.7% | 7.9% | 6.7% | 5.8% | 5.1% | 4.6% |

The difficulty in performing these experiments is that our theory is that of two limits, and then . We want to choose large seeds (at least large enough so that after applications of the map we haven’t hit ); however, that requires us to examine (at least on a log scale) a large number of . Taking larger starting values (say of the order ) makes it impractical to study enough consecutive seeds. In these cases, to approximate the limit as it is best to choose seeds from a variety of starting values and average.

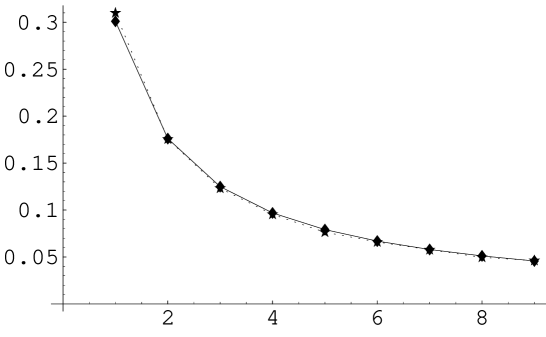

While we cannot yet prove that the iterates of a generic fixed seed are Benford, we expect this to be so. The table below records the percent of first digits equal to base for a 100,000 random digit number under the map (as the map involves simple digit operations, we may represent numbers as arrays, and the computations are quite fast). We performed two experiments: in the first we removed the highest power of in each iteration ( iterates), while in the second we had for odd and for even ( iterates). In both, the observed probabilities are extremely close to the Benford predictions (for each digit, the corresponding -statistics range from about to ).

| First | Benford | ||||

|---|---|---|---|---|---|

| Digit | Probability | Removing 2 | -statistic | Not Removing | -statistic |

| 1 | 0.3010 | 0.3021 | 2.00 | 0.3012 | 0.63 |

| 2 | 0.1761 | 0.1752 | -2.10 | 0.1763 | 0.98 |

| 3 | 0.1249 | 0.1242 | -1.97 | 0.1248 | -0.69 |

| 4 | 0.0969 | 0.0967 | -0.50 | 0.0967 | -1.14 |

| 5 | 0.0792 | 0.0792 | 0.03 | 0.0792 | -0.06 |

| 6 | 0.0670 | 0.0671 | 0.56 | 0.0667 | -1.32 |

| 7 | 0.0580 | 0.0582 | 0.68 | 0.0581 | 0.89 |

| 8 | 0.0512 | 0.0513 | 0.79 | 0.0510 | -0.77 |

| 9 | 0.0458 | 0.0460 | 0.99 | 0.0459 | 1.02 |

We calculated the values for both experiments: it is in the first () and in the second ( for odd and otherwise). As for degrees of freedom, corresponds to a value of , and corresponds to , we do not reject the null hypothesis and our experiments support the claim that the iterates of both maps obey Benford’s law.

6. Conclusion and Future Work

The idea of using Poisson Summation to show certain systems are Benford is not new (see for example [Pin] or page 63 of [Fe]); the difficulty is in bounding the error terms. Our purpose here is to codify a certain natural set of conditions where the Poisson Summation can be executed, and show that interesting systems do satisfy these conditions; a natural future project is to determine additional systems that can be so analyzed. One of the original goals of the project was to prove that the first digits of the terms in the Problem are Benford. While the techniques of this paper are close to handling this, the structure theorem at our disposal makes the natural quantity to investigate (although numerical investigations strongly support the claim that for any generic seed, the iterates of the map are Benford); however, we have not fully exploited the structure theorem and the geometric Brownian motion, and hope to return to analyzing the first digit of at a later time. Similarly, additional analysis of the error terms in the expansions and integrations of -functions may lead to proving Benford behavior on the critical line, and not just near it, although our results on values of -functions near the critical line as well as the digits of values of characteristic polynomials of random matrix ensembles support the conjectured Benford behavior.

Acknowledgements

We thank Arno Berger, Ted Hill, Ioannis Karatzas, Jeff Lagarias, James Mailhot, Jeff Miller, Michael Rosen, Yakov Sinai and Kannan Soundararajan for many enlightening conversations, Dean Eiger and Stewart Minteer for running some of the calculations, Klaus Schuerger for pointing out some typos in an earlier draft, and the referee for many valuable comments (especially suggesting we study characteristic polynomials of unitary matrices). Both authors would also like to thank the 2003 Hawaii International Conference on Statistics and The Ohio State University for their hospitality, where much of this work was written up.

Appendix A Values of Characteristic Polynomials

Consider the random matrix ensemble of unitary matrices (with eigenvalues ) with respect to Haar measure; the probability density of is

| (A.1) |

Let

| (A.2) |

be the characteristic polynomial of . The values of characteristic polynomials have been shown to be a good model for the values of -functions. Of interest to us are the results in [KeSn], where an analogue of the log-normal law of -functions (Theorem 4.3) is shown for random matrix ensembles: as the average of the absolute value of the characteristic polynomials of unitary matrices is Gaussian. Specifically, let be the probability density for averaged with respect to Haar measure (Equation (36) of [KeSn]), and set

| (A.3) |

Here is the variance, and by Equation (11) of [KeSn] satisfies

| (A.4) |

Equation (53) of [KeSn] (and the comment immediately after it) yield

Theorem A.1 (Keating-Snaith).

With as above,

| (A.5) |

In terms of , from (A.3) we immediately deduce that

| (A.6) |

note the pointwise errors are of size one over the square of the variance. It is easy to show the conditions of Theorem 3.2 are satisfied. These errors are significantly smaller than the number theory analogues, in part due to the additional averaging (the formulas here are for averages with respect to Haar measure, whereas in number theory we studied one specific -function). We thus have

Theorem A.2.

As , the distribution of digits of the absolute values of the characteristic polynomials of unitary matrices (with respect to Haar measure) converges to the Benford probabilities.

Proof.

Remark A.3.

While we believe the distribution of digits of -functions on the critical line is Benford, our results (Theorem 4.4 and Corollary 4.5) apply to values just off the critical line. Theorem A.2 may thus be interpreted as providing additional support to the conjectured Benford behavior of -functions on the critical line.

Remark A.4.

In our earlier investigations of Benford behavior, we used either the counting measure (first terms of a sequence) or Lebesgue measure (values of the function at arguments ), with . We have an extra averaging here. We are not looking at the characteristic polynomials of a sequence of unitary matrices (where is ). Instead for each we use Haar measure on unitary matrices to average the values of the characteristic polynomials, and then send . The averaged characteristic polynomials play an analogous role to our -functions from before.

Appendix B Irrationality type of and Equidistribution

Theorem B.1.

Let be a positive integer not of the form for an integer . Then is of finite type.

Proof.

By (1.1), we must show for some finite that

| (B.1) |

As

| (B.2) |

it suffices to show . This follows immediately from Theorem 2 of [Ba], which implies that if and are algebraic integers of heights at most and , then if , , where is the degree of the extension of generated by the and , , and . We take to be maximum of and . (As stated we need ; we replace with ). In our case , , . As is not a power of , unless . In particular,

| (B.3) |

For we may take (though almost surely a lower number would suffice). ∎

We show the connection between the irrationality type of and equidistribution of ; see Theorem 3.3 on page 124 of [KN] for complete details. Define the discrepancy of a sequence () by

| (B.4) |

The Erdös-Turan Theorem (see [KN], page 112) states that there exists a such that for all ,

| (B.5) |

If , then the sum on above is bounded by , where is the distance from to the nearest integer. If is of finite type, this leads to . For of type , this sum is of size , and the claimed equidistribution rate follows from taking .

Appendix C -Maps

The Benford behavior of also occurs in -Maps, defined as follows. Consider positive coprime integers and , with , and a periodic function satisfying:

-

(1)

,

-

(2)

,

-

(3)

.

The map is defined by the formula

| (C.1) |

where is uniquely chosen so that the result is not divisible by . Property (2) of guarantees . The natural domain of this map is the set of positive integers not divisible by and . Let be the set of integers between and that divide neither nor , so we can write . The size of can easily be calculated: . In the same way as before, we have -paths, which are the values of that appear in iterations of , and we again denote them by .

The Problem corresponds to , , and , the Problem corresponds to , , and , the Problem corresponds to , , and , and so on. Similar to Theorem 5.2, one can show

Theorem C.1 ([KonSi]).

The -Paths are those of a geometric Brownian motion with drift .

We expect paths to decay for negative drift and escape to infinity for positive drift. All results on Benford’s Law for the -Problem, in particular Theorem 5.3, generalize trivially to all -Maps, with the (irrationality) type of the generalization of the (irrationality) type of ; note Theorem B.1 is easily modified to analyze .

References

- [BPY] P. Baine, J. Pitman and M. Yor, Probability Laws Related to the Jacobi Theta and Riemann Zeta Functions, and Brownian Excursions, Bulletin of the AMS, Vol 38, Number 4, June 2001, 435-465.

- [Ba] A. Baker, The Theory of Linear Forms in Logarithms, Transcendence Theory: Advances and Applications (editors A. Baker and D. W. Masser), Academic Press, 1977.

- [Ben] F. Benford, The law of anomalous numbers, Proceedings of the American Philosophical Society 78 (1938), 551-572.

- [BBH] A. Berger, Leonid A. Bunimovich and T. Hill, One-dimensional dynamical systems and Benford’s Law, Trans. Amer. Math. Soc. 357 (2005), no. 1, 197-219.

- [Bi] P. Billingsley, Prime numbers and Brownian motion, Amer. Math. Monthly 80 (1973), 1099-1115.

- [BJ] H. Bohr and B. Jessen, On the distribution of the values of the Riemann zeta-function, Amer. J. Math. 58 (1936), 35-44.

- [Con] J. B. Conrey, The Riemann Hypothesis, Notices of the AMS, March 2003, 341-353.

- [Da] H. Davenport, Multiplicative Number Theory, nd edition, Graduate Texts in Mathematics 74, Springer-Verlag, New York, , revised by H. Montgomery.

- [Dia] P. Diaconis, The distribution of leading digits and uniform distribution mod 1, Ann. Probab. 5 (1979), 72-81.

- [Fe] W. Feller, An Introduction to Probability Theory and its Applications, Vol. II, second edition, John Wiley & Sons, Inc., 1971.

- [Hej] D. Hejhal, On a result of Selberg concerning zeros of linear combinations of -functions, International Math. Res. Notices 11 (2000), 551-557.

- [Hi1] T. Hill, The first-digit phenomenon, American Scientists 86 (1996), 358-363.

- [Hi2] T. Hill, A statistical derivation of the significant-digit law, Statistical Science 10 (1996), 354-363.

- [HS] M. Hindry and J. Silverman, Diophantine geometry: An introduction, Graduate Texts in Mathematics 201, Springer, New York, .

- [IK] H. Iwaniec and E. Kowalski, Analytic Number Theory, AMS, Providence, RI, 2004.

- [Iv] A. Ivić, On small values of the Riemann Zeta-Function on the critical line and gaps between zeros, Lietuvos Matematikos Rinkinys 42 (2002), 31-45.

- [JW] B. Jessen and A. Winter, Distribution functions and the Riemann zeta function, Transactions of the AMS 38 (1935), 48-88.

- [KaSh] I. Karatzas and S. E. Shreve, Brownian Motion and Stochastic Calculus, Graduate Texts in Mathematics 113, Springer 1991.

- [KaSa] N. Katz and P. Sarnak, Zeros of zeta functions and symmetries, Bull. AMS 36 (1999), 1-26.

- [KeSn] J. P. Keating and N. C. Snaith, Random matrix theory and , Comm. Math. Phys. 214 (2000), no. 1, 57-89.

- [KonSi] A. Kontorovich and Ya. G. Sinai, Structure theorem for -maps, Bull. Braz. Math. Soc. (N.S.) 33 (2002), no. 2, 213-224.

- [Knu] D. Knuth, The Art of Computer Programming, Volume 2: Seminumerical Algorithms, Addison-Wesley, third edition, 1997.

- [KN] L. Kuipers and H. Niederreiter, Uniform Distribution of Sequences, John Wiley & Sons, 1974.

- [Lag1] J. Lagarias, The Problem and its Generalizations, Organic mathematics (Burnaby, BC, 1995), 305-334, CMS Conf. Proc., 20, Amer. Math. Soc., Providence, RI, 1997.

- [Lag2] J. Lagarias, The 3x+1 problem: An annotated bibliography, http://arxiv.org/abs/math/0309224.

- [Lau] A. Laurinikas, Limit Theorems for the Riemann zeta-function on the critical line II, Lietuvos Mat. Rinkinys 27 (1987), 489-500.

- [Luo] W. Luo, Zeros of Hecke L-functions associated with cusp forms, Acta Arith. 71 (1995), no. 2, 139-158.

- [New] S. Newcomb, Note on the frequency of use of the different digits in natural numbers, Amer. J. Math. 4 (1881), 39-40.

- [Pin] R. Pinkham, On the Distribution of First Significant Digits, The Annals of Mathematical Statistics 32, no. 4 (1961), 1223-1230.

- [Ro] K. Roth, Rational approximations to algebraic numbers, Mathematika 2 (1955), 1-20.

- [Sel1] A. Selberg, Contributions to the theory of the Riemann zeta-function, Arch. Math. Naturvid. 48 (1946), no. 5, 89-155.

- [Sel2] A. Selberg, Old and new conjectures and results about a class of Dirichlet series, in Proceedngs of the Amalfi Conference on Analytic Number Theory, (eds. E. Bombierie et al.), Universit di Salerno, Salerno 1992, 367-385.

- [Se] J. P. Serre, A Course in Arithmetic, Springer-Verlag, 1996.

- [Sin] Ya. G. Sinai, Statistical problem, Comm. Pure Appl. Math. 56 (2003), no. 7, 1016-1028.