Positive forward rates in the maximum smoothness framework

Abstract

In this article we present a non-linear dynamic programming algorithm for the computation of forward rates within the maximum smoothness framework. The algorithm implements the forward rate positivity constraint for a one-parametric family of smoothness measures and it handles price spreads in the constraining dataset. We investigate the outcome of the algorithm using the Swedish Bond market showing examples where the absence of the positive constraint leads to negative interest rates. Furthermore we investigate the predictive accuracy of the algorithm as we move along the family of smoothness measures. Among other things we observe that the inclusion of spreads not only improves the smoothness of forward curves but also significantly reduces the predictive error.

May 2003

1 Introduction

Within the financial industry forward rate curves play a central role in fixed-income derivative pricing and risk management. Notwithstanding, such curves are not empirical or directly measurable objects but rather useful abstract concepts from where observed prices can be derived. Moreover, given a finite set of market prices, we can construct in general an infinite number of compatible forward rate curves111We assume here that prices do not allow for arbitrage. If this is not the case the compatibility condition has to be relaxed.. To avoid such ambiguity several approaches have been proposed in the literature trying to capture a “reasonable” or “natural” functional form within the set of compatible possibilities.

In historical order the first kind of methods proposed to solve this problem make use of the so-called parametric approach. In this approach a particular functional form for the forward rate curve is assumed leaving a certain number of free parameters to be fixed from the calculation of a given set of quoted prices. An extensive literature exists advocating for this approach. We can cite as examples the works of McCulloc [1], Vasicek and Fong [2], Chambers, Carleton and Waldman [3], Shea [4], Nelson and Siegel [5] and more recently the works of Svensson [6], Fisher, Nychka and Zervos [7] and Waggoner [8]. In most of these works we notice the privileged role played by polynomial and exponential splines as the preferred functional forms for the forward rate curves.

The second kind of methods has been termed in the literature as non-parametric or maximum-smoothness approach. Here instead of advocating for an a priori functional form for the forward rate a given measure of smoothness is chosen and then the forward rate curve is obtained as the one maximizing this measure subject to the constraints imposed by market prices. Examples where these methods have been investigated include the works of Adams and Van Deventer [9], Delbaen and Lorimier [10], Kian Guan Lim, Qin Xiao et al [11, 12], Frishling and Yamamura [13] and Yekutieli [14]. In these works three different smoothing measures have been proposed. We also have the works of Forsgren [15] and Kwon [16] that generalize these methodologies and clarify the connection between splines and certain smoothness measures. Finally we point out the work of Wets, Bianchi and Yang [17] that can be located somewhere in-between both approaches since here the number of functional parameters is finite (albeit arbitrarily large) and the functional behavior is restricted to a subfamily of curves.

The purpose of this article is two-fold: Firstly we want to present an efficient maximum-smoothing algorithm that handles the presence of spreads and implements the positivity constraint. Secondly we want to investigate the predictive power of a linear combination of two quadratic measures, namely the one proposed by Delbaen et al. and Frishling et al. [10, 13] and the one by Adams and van Deventer [9]. Here it is worth remarking that once the compatibility with market prices is fulfilled the only guiding principle that should be taken as definition of “reasonable” or “natural” is the predictive power and not other ad-hoc criteria.

In this article we will only use as constraining data coupon bearing bonds. The inclusion of treasury bills, zero coupon bonds or bill futures is straightforward and amounts to adding the corresponding linear constraints. Since our objective in this article is focusing on an algorithm dealing with non-linear constraints and inequality constraints (spreads and positivity constraint) we have not included such data.

With these objectives in mind we organize the article as follows:

In section 2 we present the objective function that we will use throughout the article and we establish the basic notation. In this section we present a sketch of the complete algorithm leaving the details for the appendices. In section 3 we present the results of the article including examples where the absence of the positivity constraint or the adequate spreads leads to negative rates. Here we present also a study of the predictive power of the one-parametric family of smoothness measures that include as extreme cases the measures used by Delbaen et al., Frishling et al. and Adams and Van Deventer. Finally in section 4 we present the conclusions.

2 The algorithm

A bond, , is an instrument that gives future coupons, , at time stages and a final payment, 222By final payment we mean the complete last cash flow of bond , typically that includes a principal plus a last coupon.. The bond price, , can be determined from the discrete forward rate curve, , as follows

| (1) |

where is the length of the time period between time stage and (in our implementation we have used day).

The objective function, or smoothing measure333Note that since we do not include a global minus sign we have to perform a minimization and not a maximization. With this sign, that is the one used in the literature, “rugosity” measure would be a more appropriate name., is defined as a linear combination of the one used by Delbaen et al. and Frishling et al. (DF) [10, 13] and the one used by Adams and Van Deventer (AD) [9]

| (2) |

The first term in Eq.(2) (DF) is a discrete approximation of the integral of the square of the first derivative of and the second term (AD) is a discrete approximation of the integral of the square of the second derivative of . This objective function is to be minimized subject to the consistency constraints

| (3) | ||||

| (4) |

where is to be determined along with and where we have used the definitions

| (5) |

with the respective bid and ask prices of bond ()444Note that this optimization problem is non-convex and therefore several local minima may exist.. Note that the equality constraint given by Eq.(3) is just Eq.(1) rewritten taking logarithms and using the definitions (5). Eq.(4) introduces two inequality constraints. The first one is the positivity constraint over the forward rate curve and the second one is the requirement that the single price given by Eq.(1) must lie in-between the bid and ask prices.

We define the spread of bond as the quantity . We take the largest time to maturity in Eq.(2) equal to the largest time to maturity in the constraining dataset, namely

The constraints reflecting bond prices (1) have been rewritten in a way such that they become linear when no coupons are present ( for a zero–coupon bond ). Constraints given by Eqs.(3) and (4) are moved to the objective function defining

| (6) |

with the Lagrange multipliers and the logarithmic barriers with parameters and (in the solution procedure we take , ). The use of log barriers to deal with inequality constraints is a standard methodology in interior point methods for optimization problems [18]. An explanation of this methodology adapted to our problem is given in appendix A. Briefly the minimization algorithm is structured as follows:

| step 0: | ||||

| step 1: | ||||

| step 2: | ||||

| step 3: | ||||

| (7) |

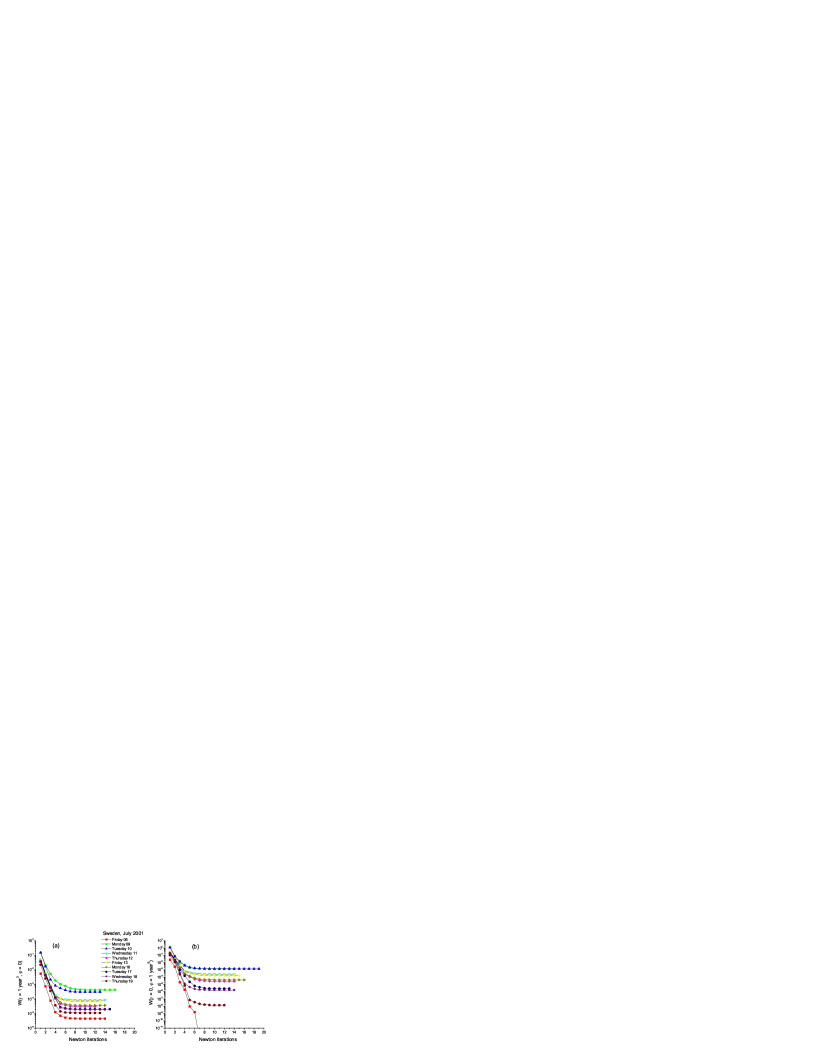

Computing times involved in step 2 are summarized in subsection B.1. The solution typically stabilizes in approximately 6 iterations as can be seen in Fig.(1). On a Pentium 4, 2.4 Ghz computer the algorithm coded in C++ takes around 1/4 sec. to compute a forward rate curve like any of the ones seen in Fig.(2).

3 Consistency and predictability

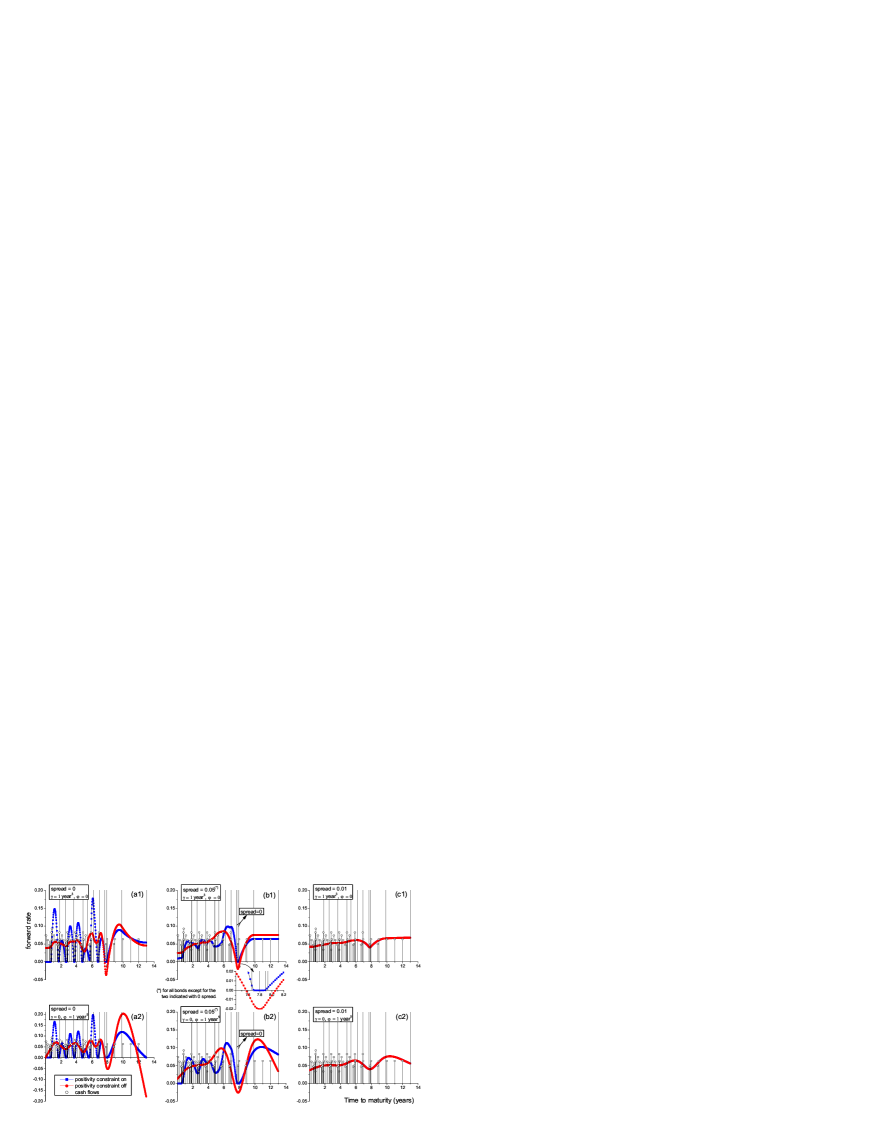

In this section we present some examples of the behavior of algorithm (7) and we investigate the predictive power of the resulting forward rate curves. In Fig.(2) we present a series of forward rate curves calculated using DF and AD smoothing measures. There we can see that for both measures the resulting curves share some similar traits like the positions of most peaks and dips. Clear differences between both sets of curves are found at their end-points and in their behavior in the presence of high spreads. In the set of curves obtained from the DF measure we have vanishing first derivative at the end-points and curves that tend to constants for high spreads. For the AD measure we have vanishing second and third derivatives at end-points [16] and curves for high enough spreads given by straight lines. From the financial point of view these features are, in principle, just different aesthetic possibilities. In order to choose a particular measure the guiding principles should be, in the first place, the fulfillment of the consistency constraints given by Eqs.(3-4) and after this is guaranteed the predictive performance.

Let us start now with the analysis of consistency. As can be found in [16] if we do not consider the positivity constraint the local minima of objective (2) are given by exponential splines with exponents or polynomial splines of order 2 or 4 when or are respectively zero. The main problem with these exponential or polynomial splines is that there is no warranty that they fulfill the positivity constraint. Negative rates are not admissible in the absence of arbitrage opportunities and the risk of obtaining this unwanted feature is illustrated in Fig.(3). In this figure we have concentrated on the Swedish bond data on Monday, July 09, 2001. There we have tested three spread patterns for both DF and AD measures with and without the positivity constraint. From these plots it is evident that the inclusion of spreads in the calculation of the forward rates is a necessary ingredient that can have a major impact in the resulting functional behavior.

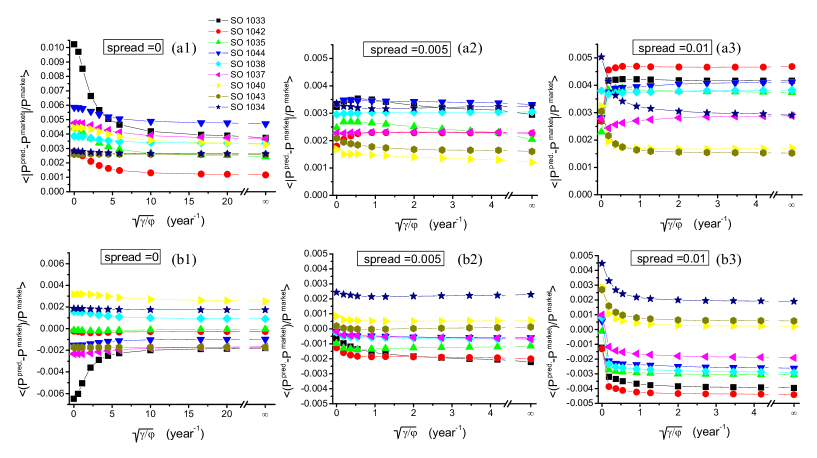

Once we have an algorithm that insures the consistency of forward rates we can concentrate on the predictive accuracy of different measures. However, before starting the analysis of this issue let us make a brief digression to comment a point regarding measure (2). If we want to have both and different from zero and we want to compare the effects of each term it is important to realize that DF and AD measures scale differently under changes of time units. In other words, and have different units. A practical way to define their units is to consider the objective as an adimensional quantity. By doing so and remembering that has units of inverse time, it is immediate to obtain that has units of time3 and units of time5. The importance of keeping this in mind becomes apparent in results like the ones presented in Figs.(4) and (5).

Figs.(4) and (5) summarize our results regarding the predictive accuracy of the algorithm as a function There it is clear that the characteristic time span where DF and AD compete is not the day or the century, but clearly the year. To construct these figures we have calculated the forward rate curves for different values of when one bond is removed from the constraining dataset. The price of this missing bond is used afterwards as a benchmark to test the accuracy of the resulting curves. Since we are interested in the statistical performance we have done such comparison for 335 consecutive trading days starting on Wednesday, November 08, 2000 and ending on Thursday, March 07, 2002.

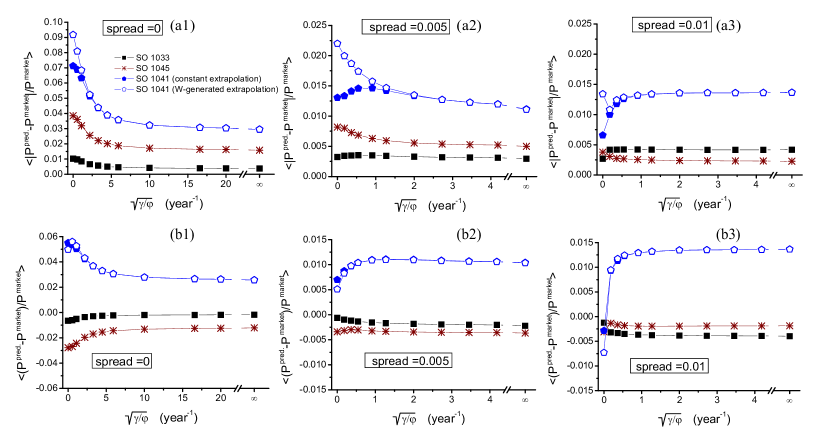

We are also interested in studying the impact of spreads in the constraining dataset over the predictive accuracy. Therefore we present our results for three spread patterns, namely constant spreads of 0%, 0.5% and 1% in the constraining dataset. Fig.(4) concentrates on the predictive accuracy for the first 9 bonds of Table (2) and Fig.(5) presents the same analysis for the remaining 2 bonds of Table (2). These last 2 bonds are the ones with the larger maturities in the complete dataset. In particular for the last one with the largest maturity we have to decide upon the methodology to extrapolate the forward curve outside the range of the constraining dataset555By the range of the constraining dataset we mean the range in time to maturity that goes from present to the last maturity within the dataset.. Therefore in Fig.(5) we present the prediction accuracy using constant extrapolation from the last maturity in the constraining dataset and “-generated” extrapolation that consists in utilizing the -optimal forward rate curve even outside the range of the constraining dataset.

4 Results and conclusions

In this article we have presented a non-linear dynamic programming algorithm designed for the calculation of positive definite forward rate curves using data with or without spreads. We have included multiple details of the algorithm aiming at practitioners not familiar with the techniques of dynamic programming. We have illustrated the results of this algorithms using the Swedish bond data for a one-parametric family of smoothness measures.

The results and conclusions are the following:

-

•

The proposed algorithm calculates forward rate curves in real time and admits, without time or complexity penalizations, the use of any non-linear local objective function. Since it also handles non-linear constraints it is possible to include within the constraining dataset any derivative products with prices bearing some dependence on forward rates.

-

•

This is the first algorithm proposed in the literature that implements the positivity constraint in the maximum smoothness framework. To the knowledge of the authors the only other work that implements such constraint outside this framework is the one of Wets et al. [17]. The proposal in [17] has the advantage of using simple linear programming but do not consider the presence of spreads minimizing instead the sum over the modulus of the difference between calculated prices and market prices.

-

•

For the objective functions and constraining datasets like the ones we have used or more generally for the ones studied in [16] the algorithm proposed in that reference offers better computing times at the expense of ignoring the positivity constraint. Essentially the complexity in [16] is and in ours is where is the number of time steps and the number of constraints. For that reason, when this class of objective functions and constraining datasets are used, a well coded algorithm might try first the proposal in [16] (improving its treatment of the spreads using e.g. log-barriers) and later, only if the result is not positive definite, use our approach.

-

•

Since the optimization problem we are solving is non-convex we can not discard the presence of several local minima (this is independent of the presence of the positivity constraint [16]). However, we have tested our algorithm starting from different seeds and in all cases we have arrived at the same minima. These tests included hundreds of searches with initial log-prices given by (with a flat random variable) and initial forward rates given by several constant and oscillating functions. With this comment we only want to convey our practical experience and by no means we intend to say that we have exhaustively explored the presence or absence of local minima.

-

•

It is clear that one way to avoid negative rates is just by increasing spreads by hand. The advantage of using real spreads at a given moment is that one can be sure of being consistent with market prices. If one observes in Fig.(3) the large forward rate variations taking place for different spread patterns no doubts should remain about the relevance of a careful treatment of this issue.

-

•

From Fig.(5) we conclude that the inclusion of spreads can remarkably improve the accuracy of resulting forward curves in the prediction of market prices of long maturing bonds. In [16] it was pointed out that the inclusion of spreads notably improved the smoothness of the forward curve. To the knowledge of the authors this is the first time it is shown that their presence also improves the prediction accuracy. For that reason we believe that spreads should be considered even when the market data does not provide such information. In that case the approach should consist in using a cross validation technique to asses the optimal spread minimizing an error criterion based in the prediction of market prices (for cross validation methods see for example [20, 21]). One possibility is using the well know “leave-one-out” cross-validation to select the optimal spread much in the spirit suggested by Figs.(4) and (5). Given a constraining set of products, the method actually consists in obtaining forward rate curves for a given spread, each curve leaving out one of the constraining products (bonds in our case) but using only the omitted products to compute an error criterion like Thus we obtain a quantitative criterion to select an optimal level of spread666This technique is stated here only to illustrate the existence of an optimal non vanishing level of spread whenever no real spreads are provided by the market. We do not intend to provide an efficient procedure to find this level.. For example for our dataset and our family of models (measures) it can be conjectured from Figs.(4) and (5) that this optimal level of spread is typically around 0.5%.

- •

Acknowledgements

J. M. acknowledges the financial support from Tekniska Högskolan, Inst. för Fysik och Mätteknik, Linköping University, thanks J. Shaw (Barclays) for calling his attention to ref. [17], F. Delbaen for ref. [10] and J. M. Eroles (HSBC) for proof reading the manuscript. J. M. would also like to thank Dr. Per Olov Lindberg for the hospitality during his stay at the Division of Optimization; Linköping University. The authors would like to thank the referees for their helpful comments on the manuscript.

Appendix A. Newton steps

Since the objective function in Eq.(6) is a non-quadratic function of , we will use an iterative quadratic approximation (Newton steps) to find its minima. We start with feasible seeds and fulfilling inequality constraints (4) and we set up initial log-barriers coefficients and For newton iteration number we define

| (8) |

with The hat over and indicate that at each step , and are the minima of the quadratic approximation and may not fulfill the inequality constraints (4). To assure constraints (4) are fulfilled a final redefinition is necessary after each Newton step. This redefinition is explained in appendix C. Expanding up to second order in and we write

| (9) |

where collects all terms not depending on , or . We will use square brackets around Newton step indices and parenthesis around dynamic programming ones. Let us now work-out the matrices involved in the quadratic approximation. From Eqs.(2) and (9) we immediately obtain

and defining

| (10) | ||||

| (11) | ||||

| (12) |

we have

Thus defining

from above expansions and Eq.(9) we immediately obtain

Appendix B. Dynamic Programming for a quadratic objective

Given positive definite symmetric matrices and and the -vector and -vector , we want to minimize the objective function

subject to the set of constraints

| (13) |

thus defining a new objective function

For any we define

where e.g. , for diagonal, tridiagonal matrices respectively. When and then can be solved efficiently with dynamic programming. To set up the notation and for those readers not familiar with dynamic programming let us here briefly explain the basics of this well known method [19]. We start defining

| (14) |

where satisfies

| (15) |

For we use the inductive hypothesis

| (16) |

where and . The final step of this backwards process consists in obtaining and satisfying

| (17) |

From Eqs.(15) and (16) we obtain

| (18) |

and plugging Eq.(18) into Eq.(14) we obtain

hence obtaining

| (19) | ||||

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) |

where

Now from Eq.(17) we obtain

or

| (25) |

and using Eq.(22) we obtain

Finally from and Eq.(25) we obtain and then using Eqs.(18) and (19-21) we obtain moving forward in the index.

B.1 Computing times of a dynamic programming iteration

The time necessary to compute all is proportional to

To calculate the inverse of , that is a symmetric matrix, we require a computing time proportional to

All and require, respectively, computing times proportional to

Finally the calculation of requires a computing time proportional to

In the forward rate calculation typically we have (in Eq.(2) we have ) and therefore the maximum delay would be given by

Appendix C. Fulfilling inequalities and updating log-barriers

The Newton step obtained from Eq.(8) may not fulfill the inequality constraints (4). To satisfy such constraints we search for a in the interval such that

| (26) |

In order to do this we first determine the maximum in the interval satisfying Eq.(26). That is, given the sets of points

we have

and then we take

with (in our implementation we have taken that is a standard election in the optimization literature). Once we have we define

| (27) |

where and are positive small values guaranteeing that matrices and are positive definite and is a monotonically decreasing function satisfying . In our implementation we have taken of the form

| (28) |

with , . The value of controls how fast barriers are reduced. In our implementation we have found that adequate values for range . The value of controls the non-linearity of . We have found that the simple linear response provides good performance albeit convergence time is not significantly affected for in the range

In this way we iterate the algorithm times until a given termination criterion is met. Defining

we have chosen the following termination criterion

| (29) |

In our implementation we have taken

| (30) |

Obviously there is considerable latitude to change the heuristic values assigned to the above parameters. Let us finish this appendix making some comments regarding their robustness.

is there to guarantee a minimum number of iterations so as to have and well defined and to avoid premature termination in the improbable case where the other criteria incorrectly suggest convergence. For this purpose is enough to take .

serves as a maximum limit to secure termination even if convergence is not achieved and therefore an alarm should be provided whenever . From our experience we observe that is more than enough to take

sets our precision to consider a given forward rate curve as a straight line. The order of magnitude of should be taken much lower than the typical order of magnitude of the observed optimal The value of the optimal depends not only on the constraining data but also on and We have adopted the practise of spanning the range year-1 taking year3, year5 and the range year taking year3, year5. With this convention we have found reasonable to take for the full range

sets the maximum variation of between newton steps that is accepted before termination. Note that in (29) to have () is a necessary but not sufficient condition for termination. Therefore sending has no major impact and is equivalent to rely only on the error and the barrier coefficients as indicators of convergence. On the contrary excessively reducing can generate unnecessary iterations. We have tested that for values satisfying we do not have any drastic increase in convergence time.

controls the error in the constraints and is the most important parameter in (29). A too large value of reduces the accuracy of the result and a too small value can give rise to unnecessary iterations. We have observed acceptable results for in the range

and control the maximum allowed values for the logarithmic barriers implementing the positivity and spread constraints respectively. Large values for these parameters can make log barriers to have a residual influence in the feasible region. Acceptable values of these maximum weights range in and As explained above keeping parameters and positive guarantees that matrices and are positive definite which in turn is sufficient to guarantee the existence of an optimal solution in each iteration. Hence and should be chosen as small as possible without interfering with the numerical stability of the algorithm. Using double precision in our program we have found the values given in (29) as a good compromise.

Finally and are the initial values for the log barriers coefficients. Taking very large values for and increases the convergence time because we need more time to reduce the barriers. Taking too small values for and also increases the convergence time because time is wasted exploring unfeasible solutions. Moreover, we have observed that convergence and stability is improved if the contributions to the objective of the two barrier terms are kept balanced. This is achieved setting (see Eqs.(11) and (12)) and using the same updating factor for and (see Eq.(27)). Keeping we have found that the time of convergence is stable for in the range

Appendix D. Bond tables

In this work we have used the following data tables and conventions.

| DateBond (SO) | 1033 | 1042 | 1035 | 1044 | 1038 | 1037 | 1040 | 1043 | 1034 | 1045 | 1041 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Friday 06 | 4.86 | 4.92 | 5.06 | 5.15 | 5.26 | 5.27 | 5.355 | 5.4 | 5.395 | 5.46 | 5.655 |

| Monday 09 | 4.905 | 4.965 | 5.11 | 5.2 | 5.05 | 5.325 | 5.4 | 5.455 | 5.23 | 5.51 | 5.7 |

| Tuesday 10 | 4.885 | 4.945 | 5.095 | 5.185 | 4.93 | 5.295 | 5.395 | 5.435 | 5.24 | 5.495 | 5.68 |

| Wednesday 11 | 4.865 | 4.92 | 5.06 | 5.15 | 4.93 | 5.275 | 5.355 | 5.41 | 5.415 | 5.465 | 5.65 |

| Thursday 12 | 4.835 | 4.885 | 5.025 | 5.125 | 4.93 | 5.25 | 5.355 | 5.405 | 5.405 | 5.465 | 5.66 |

| Friday 13 | 4.84 | 4.89 | 5.045 | 5.145 | 4.93 | 5.27 | 5.38 | 5.43 | 5.43 | 5.495 | 5.69 |

| Monday 16 | 4.825 | 4.87 | 5.035 | 5.13 | 4.93 | 5.25 | 5.36 | 5.415 | 5.41 | 5.475 | 5.66 |

| Tuesday 17 | 4.805 | 4.85 | 5.015 | 5.11 | 4.93 | 5.23 | 5.34 | 5.395 | 5.395 | 5.455 | 5.64 |

| Wednesday 18 | 4.8 | 4.86 | 5.005 | 5.1 | 4.93 | 5.22 | 5.335 | 5.38 | 5.395 | 5.445 | 5.64 |

| Thursday 19 | 4.77 | 4.83 | 4.97 | 5.06 | 4.93 | 5.165 | 5.27 | 5.34 | 5.34 | 5.39 | 5.585 |

The price of the bond is calculated using the formula

| (31) |

where is the nominal amount (SEK 40 millions for all bonds in Table 1), is the coupon rate (given in Table 2), is the total number of remaining coupons (each paid at time ), is the quoted rate given in Table 1 and is a time difference between and the settlement day. This time difference is calculated according to the ISMA 30E/360 convention defined as follows: given two dates and , their ISMA 30E/360 time difference is given by

| Bond | ||

|---|---|---|

| SO 1033 | 05/05/2003 | 10.25 |

| SO 1042 | 15/01/2004 | 5 |

| SO 1035 | 09/02/2005 | 6 |

| SO 1044 | 20/04/2006 | 3.5 |

| SO 1038 | 25/10/2006 | 6.5 |

| SO 1037 | 15/08/2007 | 8 |

| SO 1040 | 05/05/2008 | 6.5 |

| SO 1043 | 28/01/2009 | 5 |

| SO 1034 | 20/04/2009 | 9 |

| SO 1045 | 15/03/2011 | 5.25 |

| SO 1041 | 05/05/2014 | 6.75 |

References

- [1] McCulloch, J. H., Measuring the term structure of interest rates, Journal of Business, 44, 19-31, 1971. McCulloch, J. H., The Tax-Adjusted Yield Curve, Journal of Finance, 30, 811-830, 1975.

- [2] Vasicek, O. A. and Fong, H. G. Term structure modeling using exponential splines, Journal of Finance, 37(2), 329-348, 1982.

- [3] Chambers, D., Carleton, W. and Waldman, D., A New Approach to Estimation of the Term Structure of Interest Rates, Journal of Financial and Quantitative Analysis 19(3), 223-269, 1984.

- [4] Shea, G., Interest Rate Term Structure Estimation with Exponential Splines: A Note, Journal of Finance, 40, 319-325, 1985.

- [5] Nelson, C. and Siegel, A., Parsimonious Modeling of Yield Curves, Journal of Business 60, 473-489, 1987.

- [6] Svensson, L. O., Estimating and Interpreting Forward Interest Rates: Sweden 1992-1994. Technical Report Discussion Paper Number 1051, Centre for Economic Policy Research, October 1994.

- [7] Fisher, M., Nychka D. and Zervos D., Fitting the term structure of interest rates with smoothing splines, FEDS 95-1, Federal Reserve Board, Washington DC. 1994.

- [8] Waggoner D. F., Spline Methods for Extracting Interest Rates Curves from Coupon Bond Prices, Working Paper 97-10, Federal Reserve Bank of Atlanta, November 1997.

- [9] Adams, K. and van Deventer, D., Fitting Yield Curves and Smooth Forward Rate Curves with Maximum Smoothness, Journal of Fixed Income, V4, 53-62, June 1994.

- [10] Delbaen F., Lorimier S. Estimation of the yield curve and the forward rate curve starting from a finite number of observations. - In: Insurance: mathematics and economics, 11:4, 249-258 1992.

- [11] Kian Guan Lim and Qin Xiao, Computing Maximum Smoothness Forward Rate Curves, Statistics and Computing, Kluwer Academic Publishers, Vol.12, pp. 275-279, ISSN 0960-3174, 2002.

- [12] Kian Guan Lim, Qin Xiao, and Jimmy Ang, Estimating Forward Rate Curve in Pricing Interest Rate Derivatives, Derivatives Use,Trading & Regulation, an International Journal of the Futures and Options Association UK, Vol. 6 No.4, pp. 299-305, 2001.

- [13] Frishling V. and Yamamura, J., Fitting a Smooth Forward Rate Curve to Coupon Instruments, Journal of Fixed Income, V6 12, 97-103, 1996.

- [14] Yekutieli, I., With bond Stripping, the Curve’s the Thing, Bloomberg Magazine 8(3), 84-90, 1999.

- [15] Forsgren A., A note on maximum-smoothness approximation of forward interest rate, Report TRITA-MAT-1998-OS3, Department of Mathematics, Royal Institute of Technology, 1998.

- [16] Kwon, Oh Kang, A general framework for the construction and the smoothing of forward rate curves. QFRG, University of Technology, Sydney. http://www.business.uts.edu.au/finance/qfr/cfrg_papers.html, March 2002.

- [17] Wets, Roger J. B., Bianchi, Stephen W. and Yang, Liming, Serious Zero-Curves, EpiSolutions Inc., http://www.episolutionsinc.com/html/downloads/SeriousZC.pdf, January 2002.

- [18] see for example: J. Nocedal and S. J. Wright. Numerical Optimization. Springer Verlag, 1999.

- [19] see for example: Bertsekas, Dimitri P., Dynamic Programming and Optimal Control: Vol.1, 2nd Edition, Athena Scientific, 2000.

- [20] Weiss, S.M. and Kulikowski, C.A., Computer Systems That Learn, Morgan Kaufmann, 1991.

- [21] Stone, M., Asymptotics for and against cross-validation, Biometrika, 64, 29-35, 1977.