The Wick theorem for non-Gaussian distributions

and its application for noise filtering

of correlated -Exponentialy distributed random variables

Przemysław Repetowicz and Peter Richmond

Department of Physics, Trinity College Dublin 2, Ireland

Abstract

We derive the Wick theorem for the -Exponential distribution.

We use the theorem to derive a numerical algorithm for

finding parameters of the correlation matrix of q-Exponentialy

distributed random variables given empirical spectral moments of the time series.

-Exponential distributions (-Exponentials defined in the next section)

are used[1] in modeling distributions of stocks.

The -Exponentials possess two desirable features namely

exhibit power law tails in the high end of the distribution and tend toward a Gaussian

when . These facts provide enough motivation

to derive a variant of a Wick theorem for linear combinations

of independent identically distributed (iid) -Exponentials

(correlated -Exponentials).

Recent growth of interest in applications of physics to economics

and to the theory of finance (econophysics) yields the Wick theorem useful

for the following purposes:

1.

Deriving exact relations between spectra of eigenvalues of

financial covariance matrices related to -exponentially distributed time series

and of estimators of covariance matrices. This will be a generalization of

existing exact relations [8] for Gaussian distributed time series.

2.

Deriving algorithms [6] for optimizing a portfolio

(minimizing the variance and/or the higher moments of a portfolio

subject to a presumed return from a portfolio) of stocks whose time series are -exponentially

distributed.

3.

Verifying empirical findings [5] regarding a very fast time decay

of the autocorrelation function in time series and regarding a power-law time dependence

of the autocorrelation function of the volatility; investigating many point correlations

in financial time series.

2 The Wick theorem

The objective of this section is to derive the Fourier transform

of correlated -Exponentially distributed variables.

A random variable is -Exponentially distributed,

() if

and the probability density function (pdf)

of reads:

(1)

where ,

and .

The pdf (1) has (equation (20.52) in [1])

is a continuous superposition of Gaussians and has a following

integral representation:

(2)

where and

and the integral runs over

the -dimensional space with:

(3)

We define correlated -Exponentials as linear combinations of iid -Exponentials.

Therefore the joint pdf of correlated

-Exponentials

(4)

where , and are iid,

reads:

(5)

(6)

Here we call

a rotation tensor.

We take and we calculate the Fourier transform

.

It reads:

(8)

where we introduced

(a correlation tensor)

that is related to the rotation tensor

and to a diagonal tensor

.

The transposition T operation is defined as

.

This means that:

(9)

The last integral on the right hand side in (8)

is evaluated by “completing to a square” and it reads:

In (15) we expressed the integral over

in radial coordinates

.

Now we differentiate (14) times

with respect to variables

and evaluate the result at . We get:

(20)

where the sum in (20) runs over all -permutations

that are composed exclusively of cycles

for of lengths two.

Since the functions are symmetric with respect to exchanging

the above and lower pairs

and multiplication is commutative the whole of terms in the sum in (20)

decomposes into distinct terms

who occur times each.

In this way the factor in the denominator in

(20) cancels out.

In (20) we used the definition (9)

of the correlation tensor and we introduced new indices and

Since the average over in (20)

consists in performing integrals of the kind

it is readily seen that the result

(20) is expressed via a number

that depends on the sequence and that

is equal to the multiplicity of the pair in that sequence:

(21)

3 Covariances their estimators and noise filtering

In this section we discuss

definitions of averages over ensembles of stochastic variables

(resolvents) whose properties may be compared to measured properties

of financial time series.

Definition 3.1.

The resolvent function is a complex function such that:

(22)

where is a representation of the delta function.

The function is used for finding the density of eigenvalues

of the covariance

where

(23)

and the average is over the random ensemble . We have:

(24)

(25)

Lemma 3.2.

The resolvent function

has

.

Here res denotes a residue.

Proof 3.3.

The function can be expanded in a Laurent series around .

This means that

(26)

where the function is analytic.

We need to prove that

for .

We consider at first the non-analytic term in (26).

(27)

where the above equality in (27) is straightforward

and the lower equality is derived by means of the Cauchy integral theorem.

Now we analyse the analytic term. For we compute

(28)

where the last equality in (28) follows from the application

of the Cauchy integral theorem to a contour consisting of four

intervals , ,

and .

From the last expression on the right hand side in (28)

we see that the imaginary part of that integral is

and hence disappears when .

This fact and (27) suffices to finish the proof.

The class of functions becomes narrowed down subject to the following

condition:

Lemma 3.4.

The resolvent function ,

if and only if

(29)

The necessity follows in a straightforward manner from substituting

into (29).

To prove the sufficiency we take , multiply both sides

of (29) by and sum over .

Since the left hand side is the Taylor expansion of around

and the right hand side form a geometric series we obtain a functional equation:

where in (32) we have iterated the equation (31)

and we used the fact that . Finally in (33) we summed

a geometric series and completed the proof.

4 Computation of the expansion of the resolvent

We calculate a function

(34)

where the average is performed over random variables

that are correlated in

and in time and is a resolvent function.

The function is termed the resolvent.

For the purpose of the calculation we fix ,

we project the joint pdf

onto Gaussians Normal(0,)

using the integral representation (2),

average over the Gaussians and obtain

(35)

Note that the two-point correlation function (35) does not

factorize into functions depending on times and on only.

It factorises for if the rotation tensor

factorises, ie .

For generic value of , however, correlations in and in time are coupled with each other.

In the following we sum over repeated indices (use Einstein’s summation convention).

The N-type indices and the T-type indices (running from one to N and to T)

are denoted by Latin and by Greek letters respectively.

We expand the resolvent function in a series around . We get:

(40)

In (40) we introduced two new N-type indices

and ; in (40) we expanded the -th power

and we introduced

indices together with .

In (40) we inserted T-type Kronecker delta functions between the

ordered pairs and N-type delta functions between the pairs .

This resulted in introducing indices and indices

.

Finally in (40) we made use of the Wick theorem (20)

(the sum over runs over all -permutations composed

entirely of cycles of length two),

of Lemmas 3.1 and 3.2 and we eliminated the index .

Note that the sum over contains terms each containing

variable indices and

and two fixed indices and .

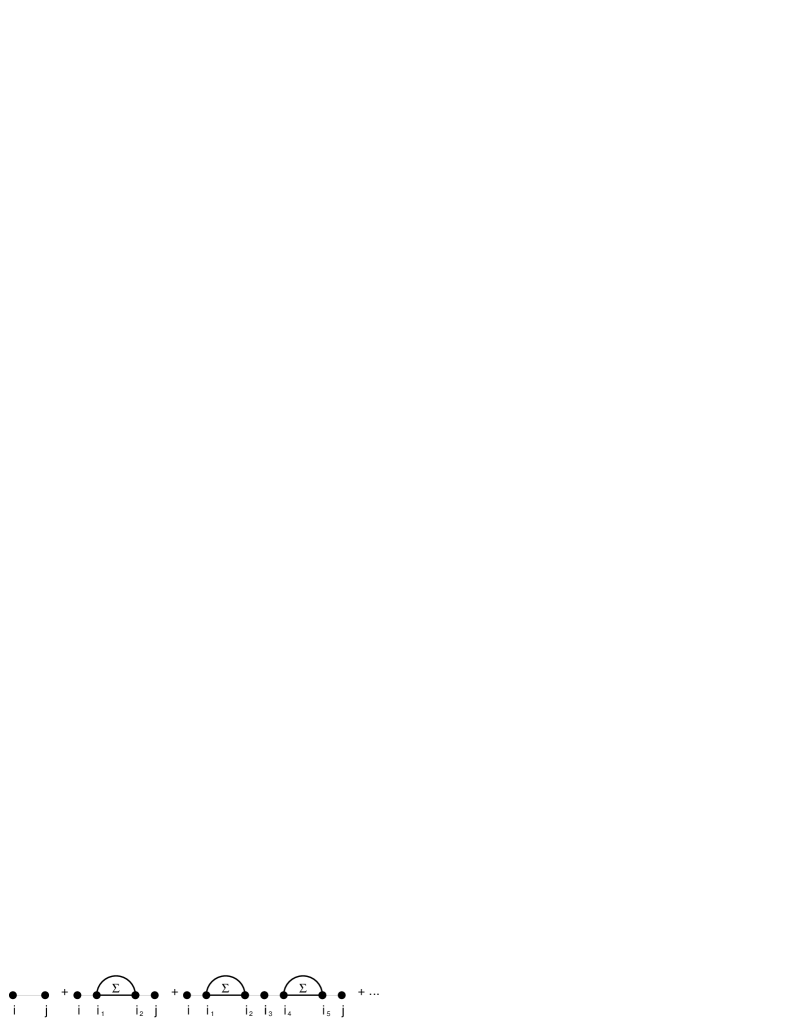

Now we construct a pictorial representation (Feynmann diagrams)

[2, 3, 4, 7] of terms in the sum

(40) according to a following recipe.

The indices are denoted by bullets ,

and the indices are denoted by open circles .

The factors in the product on the right hand side in (40)

are assigned to graphs as follows:

Factor

Graph

In this way the sum (40) can be represented as a sum over graphs

that are constructed from building blocks (4)

in such a way that for every node, except for the nodes and (external nodes),

there are exactly two edges abutting at it (this follows from the Einstein’s

summation convention).

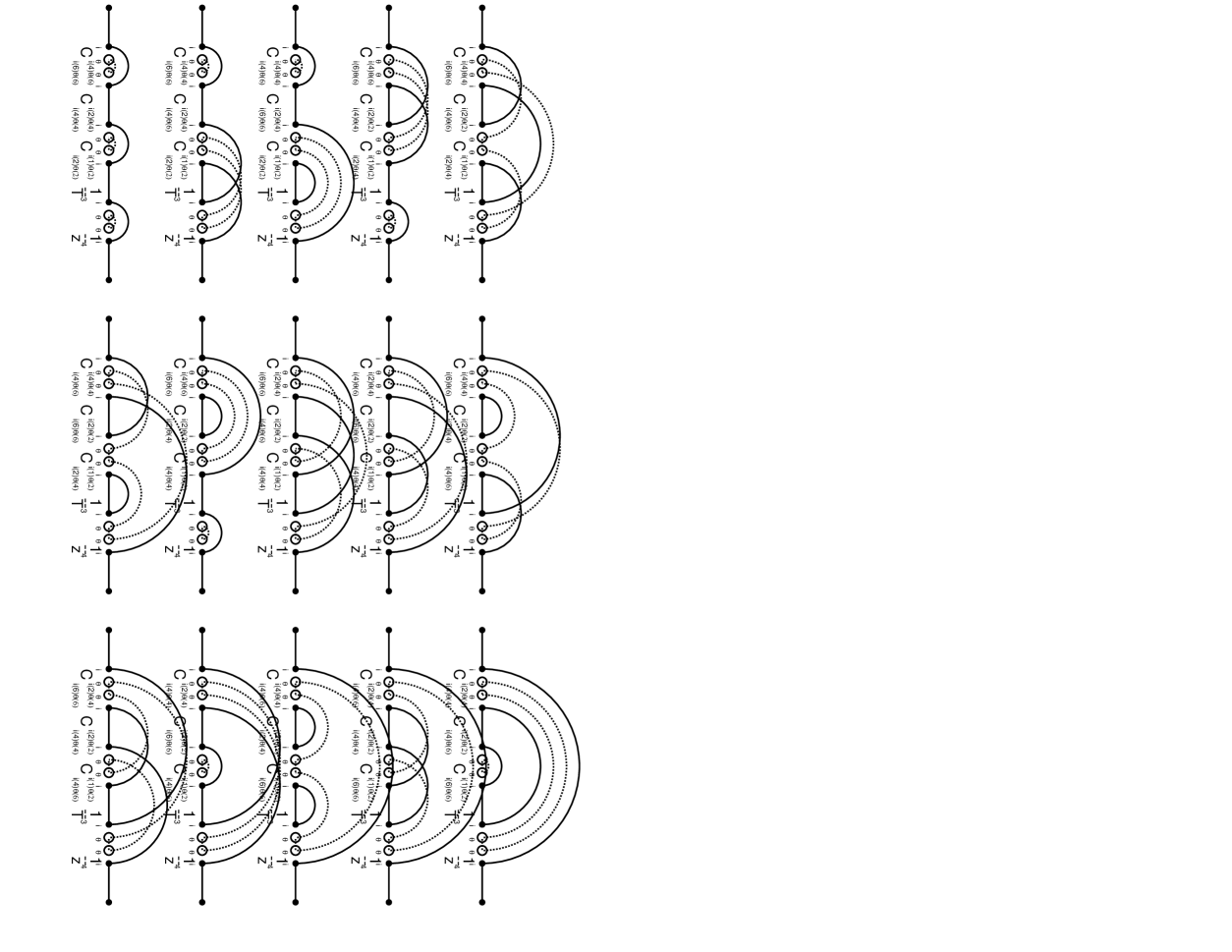

All graphs contributing to the second and to the third order of the expansion

are listed, together with their weights, in Figs. 3 and

4.

Each graph consists of a number of closed solid, a number of closed dashed loops

and of a solid line that starts at index and ends at .

Since a closed loop corresponds to a contraction

(setting two indices of the tensor equal and summing over them)

of a tensor

that is constructed by multiplying the weights of the edges of the graph,

the weight of the closed loop is proportional to and to

for solid and a dashed closed loops respectively.

In other words the weight of a closed solid (dashed) loop

is equal to a trace of a or () matrix

and thus proportional to or ().

In the following we assume that is fixed

and investigate the expansion (40)

in the limit .

Only such graphs contribute to the expansion whose number of loops

(either dashed or solid) is equal to the order of the expansion (planar graphs).

Graphs that consist of intersecting lines, like the second graph from the top

in Fig.3 are negligible in the limit

since their weight is inverse proportional to a certain power of .

We define one-line irreducible graphs as

graphs that cannot be split into two distinct graphs by cutting

a certain edge. The usefulness of this definition follows from the fact

that the weight of a graph

(the term in the sum (40) for fixed and fixed )

factorizes

into a product of weights corresponding to one-line irreducible components.

Note that this would not be the case if the weight depended explicitly

on (e.g. the function satisfied Lemma 3.1 but not Lemma 3.2)

or if it depended on some function of indices or ).

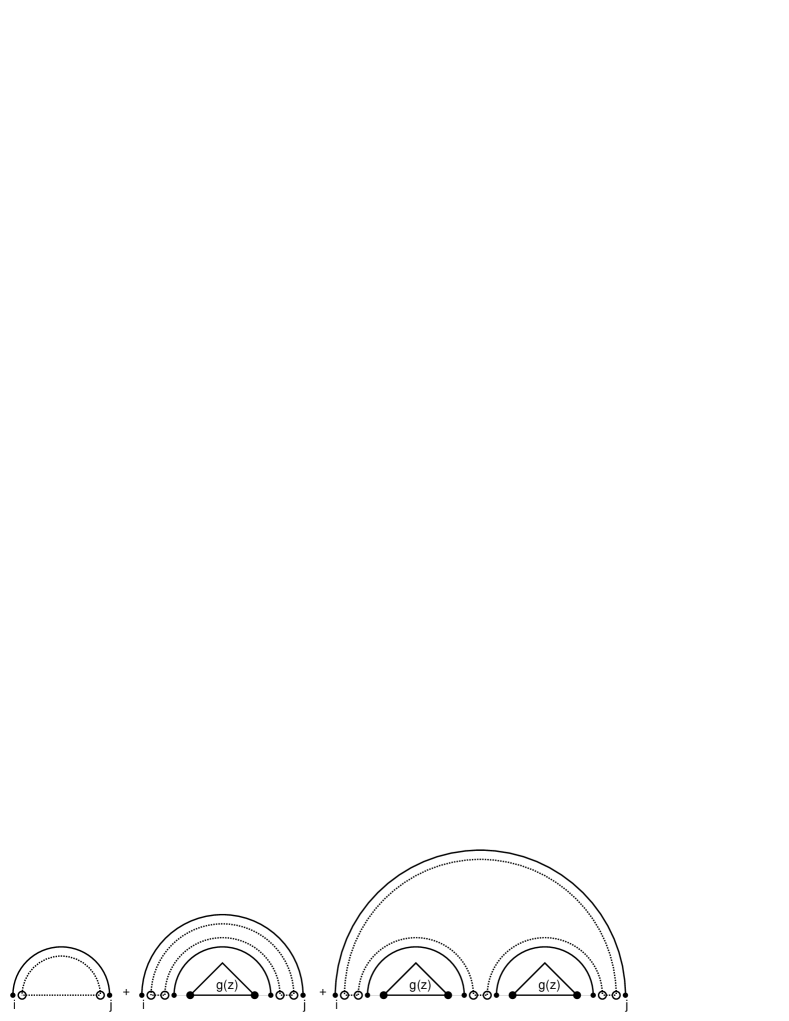

Denoting by

the sum of weights of all one-line irreducible

graphs (self-energy)

with external nodes and we realize from (40)

and from Fig.1 that the resolvent is a sum of a geometric

series in self-energy:

Figure 1: Computation of the resolvent as a geometric sum of self-energy graphs.

(41)

This result is quite general,

ie it holds also if non-planar graphs are taken into account.

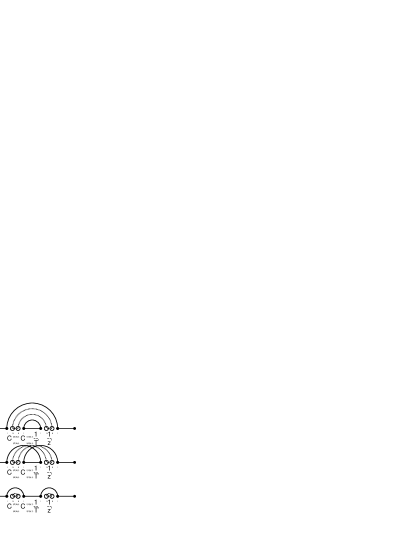

However, the self-energy can only be calculated in the case when non-planar

graphs are neglected as we see in Fig.2 and in equation (42).

(42)

where .

Denoting and we write the result in a compact way:

(43)

(44)

and we make following comments:

1.

The results (43) and (44)

are to be understood as follows. We fix

and for a given rotation tensor and

we compute the correlation tensor from

(9), we insert the self-energy

from equation (44) into (43)

and we iterate the result until convergence,

in the expansion in to a given order,

is obtained. Then we average the result over

according to the rule (15). Since the weight in (15)

factorises and the resolvent as a function of

is a polynomial of inverse powers of the weighting can be done analytically.

2.

The correlation tensor is not a tensor product

of - and time - dependent matrices (does not factorize)

(as noted in the paragraph under equation (35))

even if the rotation tensor factorises.

3.

The result (44) is only valid in the limit . For finite values of there will be corrections proportional to

inverse powers of , corrections resulting from non-planar graphs (see Figs.3 and 4).

Figure 2: Calculation of the self energy as a geometric sum of the resolvent contributions.

5 The direct and inverse problems and the moment expansion of the resolvent

The purpose of this section is to make connection between quantities that are measured

from financial time series, namely estimators of correlations

(definition (23)),

and between the underlying rotation tensor and

the variance of the q-Exponential distribution.

We define spectral moments of the estimator of correlations

as traces of powers of the estimator:

(45)

for .

Having done that we readily see from the definition of the resolvent

(34)

that the trace of the resolvent

is a generating function of the spectral moments

Following the terminology from [8] we define two problems

the direct and the indirect one.

The direct problem consists in computing the spectral moments

from the rotation tensor and the variance .

The indirect problem, which is more interesting from the point of view

of applications in quantitative finance, is defined as determining the

correlation tensor and the variance from the sole knowledge of the spectral moments.

To what extent it is possible,

what additional assumptions about the structure of the tensor have to be made before

deriving a numerical algorithm and

what is the error estimate in the algorithm will be discussed in future work.

5.1 Finding the resolvent

We solve equations (43) and (44)

for

according to the recipe in point (1) at the end of section 4

and obtain following results:

Order The resolvent 0(46)1(47)2(48)3(50)

Comparing the coefficients of the expansion (50)

in powers of with the spectral moments of the estimator of the correlations

we obtain a set of non-linear equations that relate certain contractions of the

correlation tensor to the spectral moments.

If we assumed that the correlation tensor factorized, which is not the case as we discussed

in point (1) in section 4, then we would have obtained equations (34)

from [8], equations that relate the spectral moments to moments

of the underlying correlation matrices both in and in time.

In our case the relations are averaged over and will be related to some

contractions of the rotation tensor .

Before proceeding further we note that the relations solve the direct problem

but they do not provide enough information to solve the indirect problem.

6 Conclusions

We have derived a variant of the Wick theorem

that expresses the many-point correlation function of -Exponentialy distributed

random variables through two-point correlation functions.

This theorem will be used for solving the indirect problem

in quantitative finance, ie for determining the

correlations of time series from the knowledge of the spectral moments of the estimator of covariance.

7 Acknowledgments

We thank Hagen Kleinert

www.physik.fu-berlin.de/kleinert for suggesting this problem and for discussions.

Figure 3: All diagrams of the second order that contribute to the expansion of the resolvent and their weights.

Figure 4: The same as in Fig. 3 but for diagrams of third order.

References

[1]

Kleinert H,

Student or Tsallis Distribution,

in: Path Integrals in Quantum Mechanics, Statistics, Polymer Physics, and Financial Markets,

World Scientific Publishing Co., Singapore

3rd edition (alpha version), pp. 1375-1380, (2002)

[2] Hooft G ’t,

A planar diagram theory for strong interactions

Nuclear Physics B, B 72, n 3, p 461-73, (1974)

[3] Kleinert H and Schulte-Frohlinde V,

Feynman Diagramms, in:

Critical Properties of Phi4̂-Theories,

World Scientific, Singapore, pp. 41–51, (2001)

[4] Burda Z, Goerlich A, Jarosz A anf Jurkiewicz J,

Signal and Noise in Correlation Matrix,

preprint cond-mat/0305627

[5] Mantegna R N, Stanley E H,

An Introduction to Econophysics. Correlations and Complexity in Finance,

Cambridge University Press (2000)

[6] Sornette D, Simonetti P and Andersen J V,

-Field Theory for Portfolio Optimization:

“Fat Tails” and non-linear Correlations,

Physics Reports 335 (2000) 19-92

[7] Sengupta A M, Mitra P P,

Distributions of Singular Values of some Random Matrices,

preprint cond-mat/9709283;

Phys. Rev. E 60 (1999), 3389

[8] Burda Z, Jurkiewicz J,

Spectral Moments of Correlated Wishart Matrices,

preprint cond-mat/0405263

![[Uncaptioned image]](/html/math-ph/0411020/assets/x1.png)

![[Uncaptioned image]](/html/math-ph/0411020/assets/x2.png)

![[Uncaptioned image]](/html/math-ph/0411020/assets/x3.png)