Learning Nested Agent Models in an Information Economy

Abstract

We present our approach to the problem of how an agent, within an economic Multi-Agent System, can determine when it should behave strategically (i.e. learn and use models of other agents), and when it should act as a simple price-taker. We provide a framework for the incremental implementation of modeling capabilities in agents, and a description of the forms of knowledge required. The agents were implemented and different populations simulated in order to learn more about their behavior and the merits of using and learning agent models. Our results show, among other lessons, how savvy buyers can avoid being “cheated” by sellers, how price volatility can be used to quantitatively predict the benefits of deeper models, and how specific types of agent populations influence system behavior.

1 Introduction

In open, multi-agent systems, agents can come and go without any central control or guidance, and thus how and which agents interact with each other will change dynamically. Agents might try to manipulate the interactions to their individual benefits, at the cost of the global efficiency. To avoid this, the protocols and mechanisms that the agents engage in might be constructed to make manipulation irrational [Rosenschein and Zlotkin, 1994], but unfortunately this strategy is only applicable in restricted domains. By situating agents in an economic society, as we do in the University of Michigan Digital Library (UMDL), we can make each agent responsible for making its own decisions about when to buy/sell and who to do business with [Atkins et al., 1996]. A market-based infrastructure, built around computational auction agents, serves to discourage agents from engaging in strategic reasoning to manipulate the system by keeping the competitive pressures high. However, since many instances can arise where imperfections in competition could be exploited, agents might benefit from strategic reasoning, either by manipulating the system or not allowing others to manipulate them. But strategic reasoning requires effort. An agent in an information economy like the UMDL must therefore be capable of strategic reasoning and of determining when it is worthwhile to invest in strategic reasoning rather than letting its welfare rest in the hands of the market mechanism.

In this paper, we present our approach to the problem of how an agent, within an economic MAS, can determine when it should behave strategically, and when it should act as a simple price-taker. More specifically, we let the agent’s strategy consist of learning nested models of the other agents, so the decision it must make refers to which of the models will give it greater gains. We show how, in some circumstances, agents benefit by learning and using models of others, while at other times the extra effort is wasted. Our results point to metrics that can be used to make quantitative predictions as to the benefits obtained from learning and using deeper models.

1.1 Related work

Different research communities have run across the problems that arise from having agents learning in societies of learning agents. The studies of [Shoham and Tennenholtz, 1992], and [Glance, 1993] focus on very simple but numerous agents and emphasize their emergent behavior. [Hu and Wellman, 1996] show that learning agents in an economic domain sometimes converge to globally sub-optimal equilibria. The work on agent-based modeling [Hübler and Pines, 1994, Axelrod, 1984, Epstein and Axtell, 1996] of complex systems studies slightly more complicated agents that are meant as stand-ins for real world agents (e.g. insects, communities, corporations, people).

All these researchers used agents whose learning abilities consist of choosing from among a set of fixed strategies. They do not explicitly consider the fact that the agents inhabit communities of learning agents. That is, their agents do not try to model other agents. We address this issue and try to determine when and which models an agent should keep.

Within the MAS community, some work [Sen, 1996] has focused on how artificial AI-based learning agents would fare in communities of similar agents. For example, [Nadella and Sen, 1997] and [Terabe et al., 1997] show how agents can learn the capabilities of others via repeated interactions, but these agents do not learn to predict what actions other might take. Most of the work in MAS also fails to recognize the possible gains from using explicit agent models to predict agent actions. [Tambe and Rosenbloom, 1996] is an exception and gives another approach for using nested agent models. However, they do not go so far as to try to quantify the advantages of their nested models or show how these could be learned via observations. We believe that our research will bring to the foreground some of the common observations seen in these research areas and help to clarify the implications and utility of learning and using nested agent models.

2 Description of the UMDL

The UMDL project is a large-scale, multidisciplinary effort to design and build a flexible, scalable infrastructure for rendering library services in a digital networked environment. In order to meet these goals, we chose to implement the library as a collection of interacting agents, each specialized to perform a particular task. These agents buy and sell goods/services from each other, within an artificial economy, in an effort to make a profit. Since the UMDL is an open system, which will allow third parties to build and integrate their own agents into the architecture, we treat all agents as purely selfish.

2.1 Implications of the information economy.

Information goods/services, like those provided in the UMDL, are very hard to compartmentalize into equivalence classes that all agents can agree on. For example, if a web search engine service is defined as a good, then all agents providing web search services can be considered as selling the same good. It is likely, however, that a buyer of this good might decide that seller provides better answers than seller . We cannot possibly hope to enumerate the set of reasons an agent might have for preferring one set of answers (and thus one search agent) over another, and we should not try to do so. It should be up to the individual buyers to decide what items belong to the same good category, each buyer clustering items in possibly different ways.

This situation is even more evident when we consider an information economy rooted in some information delivery infrastructure (e.g. the Internet). There are two main characteristics that set this economy apart from a traditional economy.

-

•

There is virtually no cost of reproduction. Once the information is created it can be duplicated virtually for free.

-

•

All agents have virtually direct and free access to all other agents.

If these two characteristics are present in an economy, it is useless to talk about supply and demand, since supply is practically infinite for any particular good and available everywhere. The only way agents can survive in such an economy is by providing value-added services that are tailored to meet their customers’ needs. Each provider will try to differentiate his goods from everyone else’s while each buyer will try to find those suppliers that best meet her value function. We propose to build agents that can achieve these goals by learning models of other agents and making strategic decisions based on these models. These techniques can also be applied, with variable levels of efficacy, to traditional economies.

3 A Simplified Model of the UMDL

In order to capture the main characteristics of the UMDL, and to facilitate the development and testing of agents, we have defined an “abstract” economic model. We define an economic society of agents as one where each agent is either a buyer or a seller of some particular good. The set of buyers is and the set of sellers is . These agents exchange goods by paying some price , where is a finite set. The buyers are capable of assessing the quality of a good received and giving it some value , where is also a finite set.

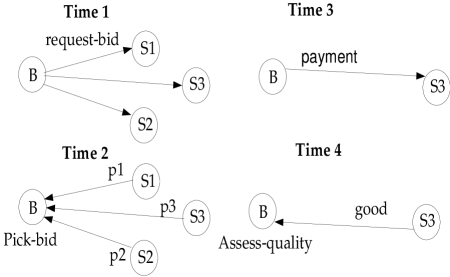

The exchange protocol, seen in Figure 1, works as follows: When a buyer wants to buy a good , she will advertise this fact. Each seller that sells that good will give his bid in the form of a price . The buyer will pick one of these and will pay the seller. All agents will be made aware of this choice along with the prices offered by all the sellers.. The winning seller will then return111In the case of agent/link failure, each agent is free to set its own timeouts and assess the quality of the never-received good accordingly. Bids that are not received in time will, of course, not be considered. the specified good. Note that there is no law that forces the seller to return a good of any particular quality. For example, an agent that sells web search services returns a set of hits as its good. Each buyer of this good might determine its quality based on the time it took for the response to arrive, the number of hits, the relevance of the hits, or any combination of these and/or other features. Therefore, it would usually be impossible to enforce a quality measure that all buyers can agree with.

It is thus up to the buyer to assess the quality of the good received. Each buyer also has a value function for each good that she might wish to buy. The function returns a number that represents the value that assigns to that particular good at that particular price and quality. Each seller , on the other hand, has a cost associated with each good he can produce. Since we assume that costs and payments are expressed in the same units (i.e. money) then, if seller gets paid for good , his profit will be . The buyers, therefore, have the goal of maximizing the value they get for their transactions, while the sellers have the goal of maximizing their profits.

4 Learning recursive models

Agents placed in the economic society we just described will have to learn, typically via trial and error, what actions give them the highest expected reward and under which circumstances. In this section we will present techniques that these agents might use to maximize their rewards.

An important question we wish to answer is: when do agents benefit from having deeper nested models of other agents? It seems intuitive that, ignoring computational costs, the agents with more complete models of others will always do better. We find this to be usually true; however, while there are instances when it is significantly better to have deeper models, there are also instances when the difference is barely noticeable and, instances when its better to ignore deeper models if they are imperfect or provide no useful information. These instances are defined in part by the set of other agents present, their capabilities and preferences, and the dynamics of the system. In order to precisely determine what these instances are, and in the hopes of providing a more general framework for studying the effects of increased agent-modeling capabilities within our economic model, we have defined a set of techniques that our agents can use for learning and using models.

We divide the agents into classes that correspond to their modeling capabilities. The hierarchy we present is inspired by the Recursive Modeling Method [Gmytrasiewicz, 1996], but is function-based rather than matrix-based, and includes learning. We will first describe our agents at the knowledge level, stating only the type of knowledge the agents are either trying to acquire through learning, or already have (i.e. knowledge that was directly implemented by the designers of the agents), and will then explain the details of how this knowledge was implemented.

At the most abstract level, we can say that every agent is trying to learn the oracle decision function , which maps the state of the world into the action that the agent should take in that state. This function will not be fixed throughout the lifetime of the agent because the other agents are also engaged in some kind of learning themselves. The agents that try to directly learn we refer to as 0-level agents, because they have no explicit models of other agents. In fact, they are not aware that there are other agents in the world. Any such agent will learn a decision function where is what agent knows about its external world and is its rational action in that state. For example, a web search agent might look at the going price for web searches, in order to determine how much to charge for its service.

Agents with 1-level models of other agents, on the other hand, are aware that there are other agents out there but have no idea what the “interior” of these agents looks like. They have two kinds of knowledge— a set of functions which capture agent ’s model of each of the other agents (), and which captures ’s knowledge of what action to take given and the collective actions the others will take. We define , where is the number of agents. An agent’s model of others might not be correct; therefore, it is not always true that . The knowledge for all turns out to be easier to learn than the joint action because the set of possible hypotheses is smaller.

Agents with 2-level models are assumed to have deeper knowledge about the other agents; that is, they have knowledge of the form . This knowledge tells them how others determine which action to take. They also know what actions others think others are going to take, i.e. , and (like 1-level modelers) what action they should take given others’ actions, . Again, the is easier to learn that the other two, as long as all agents use the same features to discriminate among the different worlds (i.e. share the same ).

4.1 Populating the knowledge

If the different level agents had to learn all the knowledge then, since the 0-level agents have a lot less knowledge to learn, they would learn it much faster. However, in the economic domain, it is likely that the designer has additional knowledge which could be incorporated into the agents. The agents we built incorporated extra knowledge along these lines.

We decided that 0-level agents would learn all their knowledge by tracking their actions and the rewards they got. These agents, therefore, receive no extra domain knowledge from the designers and learn everything from experience. 1-level agents, on the other hand, have a priori knowledge of what action they should take given the actions that others will take. That is, while they try to learn knowledge of the form by observing the actions others take (i.e. in a form of supervised learning where the other agents act as tutors), they already have knowledge of the form . In our economic domain, it is reasonable to assume that agents have this knowledge since, in fact, this type of knowledge can be easily generated. That is, if I know what all the other sellers are going to bid, and the prices that the buyer is willing to pay, then it is easy for me to determine which price to bid. We must also point out that in this domain, the knowledge cannot be used by a 0-level agent. If this knowledge had said, for instance, that from some state agent will only ever take one of a few possible actions, then this knowledge could have been used to eliminate impossibilities from the knowledge of a 0-level agent. However, this situation never arises in our domain because, as we shall see in the following Sections, the states used by the agents permit the set of reasonable actions to always be equal to the set of all possible actions.

The 2-level agents learn their knowledge from observations of others’ actions, under the already stated assumption that there is common knowledge of the fact that all agents see the actions taken by all. The rest of the knowledge, i.e. and , is built into the 2-level agents a priori. As with 1-level agents, we cannot use the knowledge to add knowledge to a 1-level modeler, because other agents are also free to take any one of the possible actions in any state of the world. There are many reasonable ways to explain how the 2-level agents came to possess the knowledge. It could be, for instance, that the designer assumed that the other designers would build 1-level agents with the same knowledge we just described. This type of recursive thinking (i.e. “they will do just as I did, so I must do one better”), along with the obvious expansion of the knowledge structure, could be used to generate -level agents, but so far we have concentrated only on the first three levels.

| Level | Form of Knowledge | Method of Acquisition |

|---|---|---|

| 0-level | Reinforcement Learning | |

| 1-level | Previously known | |

| Learn from observation | ||

| 2-level | Previously known | |

| Previously known | ||

| Learn from observation. |

The different forms of knowledge, and their form of acquisition, are summarized in Table 1. In the following sections, we talk about each one of these agents in more detail and give some specifics on their implementation. Our current model emphasizes transactions over a single good, so each agent is only a buyer or a seller, but cannot be both.

4.2 Agents with 0-level models

Agents with 0-level models must learn everything they know from observations they make about the environment, and from any rewards they get. In our economic society this means that buyers see the bids they receive and the good received after striking a contract, while sellers see the request for bids and the profit they made (if any). In general, these agents get some input, take an action, then receive some reward. This framework is the same framework used in reinforcement learning, which is why we decided to use a form of reinforcement learning [Sutton, 1988] [Watkins and Dayan, 1992], for implementing learning in our agents.

Both buyers and sellers will use the equations in the next few sections for determining what actions to take. But, with a small probability they will choose to explore, instead of exploit, and will pick their actions at random (except for the fact that sellers never bid below cost). The value of is initially but decreases with time to some empirically chosen, fixed minimum value . That is,

where is some annealing factor.

4.2.1 Buyers with 0-level models.

A buyer will start by requesting bids for a good . She will then receive all bids for good and will pick the seller:

| (1) |

This function implements the buyer’s which, in this case, can be rephrased as . The function returns the value the buyer expects to get if she buys good at a price of . It is learned using a simple form of reinforcement learning, namely:

| (2) |

Here is the learning rate, is the price pays for the good, and is the quality she ascribes to it. The learning rate is initially set to and, like , is decreased until it reaches some fixed minimum value .

4.2.2 Sellers with 0-level models.

When asked for a bid, the seller will provide one whose price is greater than or equal222We could just as easily have said that the price must be strictly greater than the cost. to the cost for producing it (i.e. ). From these prices, he will chose the one with the highest expected profit:

| (3) |

Again, this function encompasses the seller’s knowledge, where we now have that the states are the goods being sold , and the actions are prices offered . The function returns the profit expects to get if he offers good at a price . It is also learned using reinforcement learning, as follows:

| (4) |

where

| (5) |

4.3 Agents with One-level Models

The next step is for an agent to keep one-level models of the other agents. This means that it has no idea of what the interior (i.e. “mental”) processes of the other agents are, but it recognizes the fact that there are other agents out there whose behaviors influence its rewards. The agent, therefore, can only model others by looking at their past behavior and trying to predict, from it, their future actions. The agent also has knowledge, implemented as functions, that tells it what action to take, given a probability distribution over the set of actions that other agents can take. In the actual implementation, as shown below, the knowledge takes into account the fact that the knowledge is constantly being learned and, therefore, is not correct with perfect certainty.

4.3.1 Buyers with one-level models.

A buyer with one-level models can now keep a history of the qualities she ascribes to the goods returned by each seller. She can, in fact, remember the last qualities returned by some seller for some good , and define a probability density function over the qualities returned by (i.e. returns the probability that returns an instance of good that has quality ). This function provides the knowledge. She can use the expected value of this function to calculate which seller she expects will give her the highest expected value.

| (6) | |||||

The is given by the previous function which simply tries to maximize the value the buyer expects to get. The buyer does not need to model other buyers since they do not affect the value she gets.

4.3.2 Sellers with one-level models.

Each seller will try to predict what bid the other sellers will submit (based solely on what they have bid in the past), and what bid the buyer will likely pick. A complete implementation would require the seller to remember past combinations of buyers, bids and results (i.e. who was buying, who bid what, and who won). However, it is unrealistic to expect a seller to remember all this since there are at least possible combinations.

However, the seller’s one-level behavior can be approximated by having him remember the last prices accepted by each buyer for each good , and form a probability density function , which returns the probability that will accept (pick) price for good . The expected value of this function provides the knowledge. Similarly, the seller remembers other sellers’ last bids for good and forms , which gives the probability that will bid for good . The expected value of this function provides the knowledge. The seller can now determine which bid maximizes his expected profits.

| (7) |

Note that this function also does a small amount of approximation by assuming that wins whenever there is a tie333The complete solution would have to consider the probabilities that ties with 1, 2, 3,…other agents. In order to do this we would need to consider all subsets.. The function calculates the best bid by determining, for each possible bid, the product of the profit and the probability that the agent will get that profit. Since the profit for lost bids is , we only need to consider the cases where wins. The probability that will win can then be found by calculating the product of the probabilities that his bid will beat the bids of each of the other sellers. The function approximates the knowledge.

4.4 Agents with Two-level Models

The intentional models we use correspond to the functions used by agents that use one-level models. The agents’ knowledge has again been expanded to take into account the fact that the deeper knowledge is learned and might not be correct. The knowledge is learned from observation, under the assumption that there is common knowledge of the fact that all agents see the bids given by all agents.

4.4.1 Buyers with two-level models.

Since the buyer receives bids from the sellers, there is no need for her to try to out-guess or predict what the sellers will bid. She is also not concerned with what the other buyers are doing since, in our model, there is an effectively infinite supply of goods. The buyers are, therefore, not competing with each other and do not need to keep deeper models of others.

4.4.2 Sellers with two-level models.

A seller will model other sellers as if they were using the one-level models. That is, he thinks they will model others using policy models and make their decisions using the equations presented in Section 4.3.2. He will try to predict their bids and then try to find a bid for himself that the buyer will prefer more than all the bids of the other sellers. His model of the buyer will also be an intentional model. He will model the buyers as though they were implemented as explained in Section 4.3.1. A seller, therefore, assumes that it has the correct intentional models of other agents.

The algorithm he follows is to first use his models of the sellers to predict what bids they will submit. He has a model of the buyer , that tells him which seller she might choose given the set of bids submitted by each seller . The seller uses this model to determine which of his bids will bring him higher profit, by first finding the set of bids he can make that will win:

| (8) |

And from these finding the one with the highest profit:

| (9) |

These functions provide the knowledge.

5 Tests

Since there is no obvious way to analytically determine how different populations of agents would interact and, of greater interest to us, how much better (or worse) the agents with deeper models would fare, we decided to implement a society of the agents described above and ran it to test our hypotheses. In all tests, we had buyers and sellers. The buyers had the same value function , which means that if then the buyers will prefer the seller that offers the higher quality. The quality that they perceived was the same only on average, i.e. any particular good might be thought to have quality that is slightly higher or lower than expected. All sellers had costs equal to the quality they returned in order to support the common sense assumption that quality goods cost more to produce. A set of these buyers and sellers is what we call a population. We tried various populations; within each population we kept constant the agents’ modeling levels, the value assessment functions and the qualities returned. The tests involved a series of such populations, each one with agents of different modeling levels, and/or sellers with different quality/costs. We also set , , and . There were runs done for each population of agents, each run consisting of auctions (i.e. iterations of the protocol). The lessons presented in the next section are based on the averages of these runs.

6 Lessons

From our tests we were able to discern several lessons about the dynamics of different populations of agents. Some of these lead to methods that can be used to make quantitative predictions about agents’ performance, while others make qualitative assessments about the type of behaviors we might expect. We detail these in the next subsections, and summarize them in Table 2.

6.1 Micro versus macro behaviors.

In all tests, we found the behavior for any particular run does not necessarily reflect the average behavior of the system. The prices have a tendency to sometimes reach temporary stable points. These conjectural equilibria, as described in [Hu and Wellman, 1996], are instances when all of the agents’ models are correctly predicting the others’ behavior and, therefore, the agents do not need to change their models or their actions. These conjectural equilibria points are seldom global optima for the agents. If one of our agents finds itself at one of these equilibrium points, since the agent is always exploring with probability , it will in time discover that this point is only a local optima (i.e. it can get more profit selling/buying at a different price) and will change its actions accordingly. Only when the price is an equilibrium price444That is, is an equilibrium price if every seller that can sell at that price (i.e. those whose cost is less than ) does. do we find that the agents continue to forever take the same actions, leaving the price at its equilibrium point.

In order to understand the more significant macro-level behaviors of the system, we present results that are based on the averages from many runs. While these averages seem very stable, and a good first step in learning to understand these systems, in the future we will need to address some of the micro-level issues. We do notice from our data that the micro-level behaviors (e.g. temporary conjectural equilibria, price fluctuations) are much more closely tied, usually in intuitive ways, to the agents’ learning rate and exploration rate . That is, higher rates for both of these lead to more price fluctuations and shorter temporary equilibria.

6.2 0-level buyers and sellers.

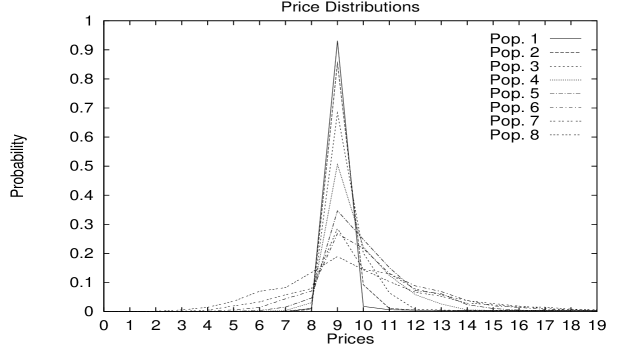

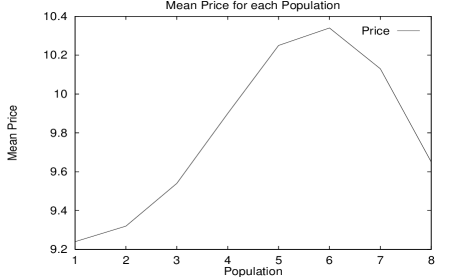

This type of population is equivalent to a “blind” auction, where the agents only see the price and the good, but are prevented from seeing who the seller (or buyer) was. As expected, we found that an equilibrium is reached as long as all the sellers are providing the same quality. This is the case for population 1 in Figure 2. Otherwise, if the sellers offer different quality goods, the price fluctuates as the buyers try to find the price that on the whole returns the best quality, and the sellers try to find the price555Remember, the sellers are constrained to return a fixed quality. They can only change the price they charge. the buyers favor. In these populations, the sellers offering the higher quality, at a higher cost, lose money. Meanwhile, sellers offering lower quality, at a lower cost, earn some extra income by selling their low quality goods to buyers that expect, and are paying for, higher quality. As more sellers start to offer lower quality, we find that the mean price actually increases, evidently because price acts as a signal for quality and the added uncertainty makes the higher prices more likely to give the buyer a higher value. We see this in Figure 2, where population 1 has all sellers returning the same quality while in each successive population more agents offer lower quality. The price distribution for population 1 is concentrated on 9, but for populations 2 through 6 it flattens and shifts to the right, increasing the mean price. It is only by population 7 when it starts to shift back to the left, thus reducing the mean price, as seen in Figure 3. That is, it is only after a significant number of sellers start to offer lower quality that we see the mean price decrease.

6.3 0-level buyers and sellers, plus one 1-level seller.

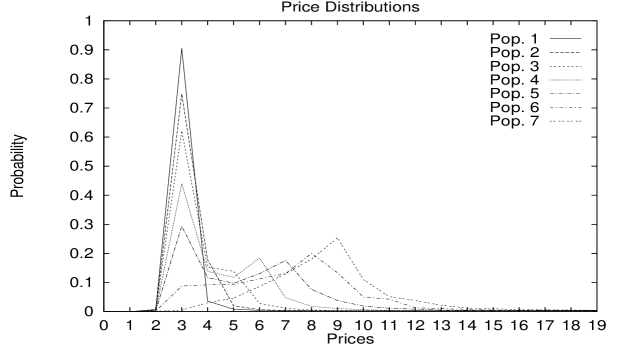

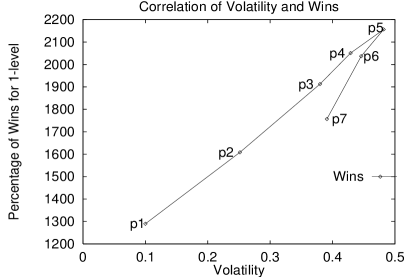

In these population sets we explored the advantages that a 1-level seller has over identical 0-level sellers. The advantage was non-existent when all sellers returned the same quality (i.e. when the prices reached an equilibrium as shown in population 1 in Figure 4), but increased as the sellers started to diverge in the quality they returned. In order to make these findings useful when building agents, we needed a way to make quantitative predictions as to the benefits of keeping 1-level models. It turns out that these benefits can be predicted, not by the population type as we had first guessed, but by the price volatility.

We define volatility as the number of times the price changes from one auction to the next, divided by the total number of auctions. Figure 5 shows the linear relation between volatility and the percentage of times the 1-level seller wins. The two lines correspond to two “types” of volatility. The first line includes populations 1 through 5 (p1-p5). It reflects the case where the buyers’ second-favorite (and possibly, the third, fourth, etc.) equilibrium price is greater than her most preferred price. In these cases the buyers and sellers fight among the two most preferred prices, the sellers pulling towards the higher equilibrium price and the buyers towards the lower one, as shown by the two peaks in populations 4 and 5 in Figure 4. The other line, which includes populations 6 and 7, corresponds to cases where the buyers’ preferred equilibrium price is greater than the runner-ups. In these cases there is no contest between two equilibria. We observe only one peak in the price distribution for these populations.

The slope of these lines can be easily calculated and the resulting function can be used by a seller agent for making a quantitative prediction as to how much he would benefit by switching to 1-level models. That is, he could measure price volatility, multiply it by the appropriate slope, and the resulting number would be the percentage of times he would win. However, for this to work the agent needs to know that all eight buyers and five sellers are 0-level modelers because different types of populations lead to different slopes. Also, slight changes in our learning parameters ( and ) lead to slight changes in the slopes so these would have to be taken into account if the agent is actively changing its parameters.

We also want to make clear a small caveat, which is that the volatility that is correlated to the usefulness of keeping 1-level models is the volatility of the system with the agent already doing 1-level modeling. Fortunately, our experiments show that having one agent change from 0-level to 1-level does not have a great effect on the volatility as long as there are enough (i.e. more than five or so) other sellers.

The reason volatility is such a good predictor is that it serves as an accurate assessment of how dynamic the system is and, in turn, of the complexity of the learning problem faced by the agents. It turns out that the learning problem faced by 1-level agents is “simpler” than the one faced by 0-level modelers. Our 0-level agents use reinforcement learning to learn a good match between world states and the actions they should take. The 1-level agents, on the other hand, can see the actions other agents take and do not need to learn their models through indirect reinforcements. They instead use a form of supervised learning to learn the models of others. Since 1-level agents need fewer interactions to learn a correct model, their models will, in general, be better than those of 0-level agents in direct proportion to the speed with which the target function changes. That is, in a slow-changing world both of them will have time enough to arrive at approximately correct models, while in a fast-changing world only the 1-level agents will have time to arrive at an approximately correct model. This explains why high price volatility is correlated to an increase in the 1-level agent’s performance. However, as we saw, the relative advantages for different volatilities (i.e. the slope in Figure 5) will also depend on the shape of the price distribution and the particular population of agents.

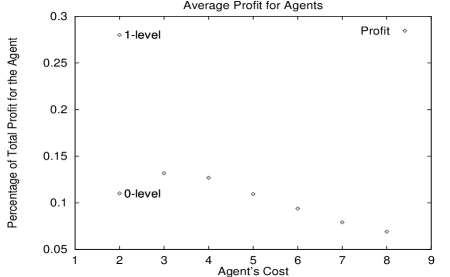

Finally, in all populations where the buyers are 0-level, we saw that it really pays for the sellers to have low costs because this allows them to lower their prices to fit almost any demand. Since the buyers have 0-level models, the sellers with low quality and cost can raise their prices when appropriate, in effect “pretending” to be the high-quality sellers, and make an even more substantial profit. This extra profit comes at the cost of a reduction in the average value that the buyers receive. In other words, the buyers get less value because they are only 0-level agents and are less able to detect the sellers’ deception. In the next Section we will see how this is not true for 1-level buyers.

Of course, the 1-level sellers were more successful at this deception strategy than the 0-level sellers. Figure 6 shows the profit of several agents in a population as a function of their cost. We can see how the 0-level agents’ profit decreases with increasing costs, and how the 1-level agent’s profit is much higher than the 0-level with the same costs. We also notice that, since the 0-level agents are not as successful as the 1-level at taking advantage of their low costs, the first 0-level seller (that returns quality 2) has lower profit than the rest as some of his profit was taken away by the 1-level seller (that returns the same quality).

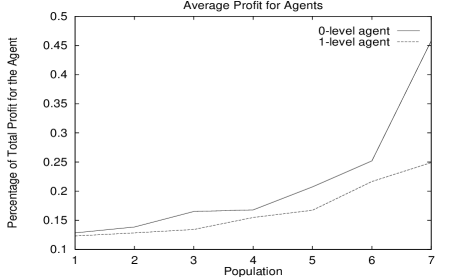

6.4 1-level buyers and 0 and 1-level sellers.

In these populations the buyers have the upper hand. They quickly identify those sellers that provide the highest quality goods and buy exclusively from them. The sellers do not benefit from having deeper models; in fact, Figure 7 shows how the 1-level seller’s profit is less than that of a similar 0-level seller because the 1-level seller tries to charge higher prices than the 0-level seller. The 1-level buyers do not fall for this trick— they know what quality to expect, and buy more from the lower-priced 0-level seller(s). We have here a case of erroneous models— 1-level sellers assume that buyers are 0-level, and since this is not true, their erroneous deductions lead them to make bad decisions. To stay a step ahead, sellers would need to be 2-level in this case.

In Figure 7, the first population has all sellers returning a quality of 8 while by population 7 they are returning qualities of , respectively, with the 1-level always returning quality of 8. We notice that the difference in profits between the 0-level and the 1-level increases with successive populations. This is explained by the fact that in the first population all seven 0-level sellers are returning the same quality, while by population 7 only the 0-level pictured (i.e. the first one) is still returning quality 8. This means that his competition, in the form of other 0-level sellers returning the same quality, decreases for successive populations. Meanwhile, in all populations there is only one 1-level seller who has no competition from other 1-level sellers. To summarize, the 0-level seller’s profit is always higher than the similar 1-level seller’s, and the difference increases as there are fewer other competing 0-level sellers who offer the same quality.

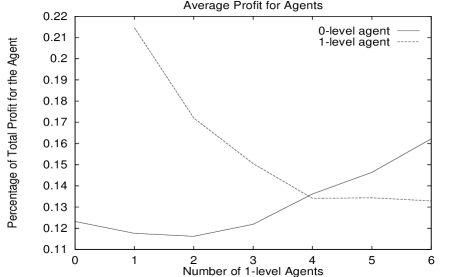

6.5 1-level buyers and several 1-level sellers.

We have shown how 1-level sellers do better, on average, than 0-level sellers when faced with 0-level buyers, but this is not true anymore if too many 0-level sellers decide to become 1-level. Figure 8 shows how the profits of a 1-level seller decrease as he is joined by other 1-level sellers. In this Figure the sellers are returning qualities of . Initially they are all 0-level, then one of the sellers with quality 2 becomes 1-level (he is the seller shown in the Figure), then another one and so on…until there is only one 0-level seller with quality two. Then the seller with quality three becomes 1-level and, finally the seller with quality four becomes 1-level. At this point we have six 1-level sellers and one 0-level seller. We can see that with more than four 1-level sellers the 0-level seller is actually making more profit than the similar 1-level seller. The 1-level seller’s profit decreases because, as more sellers change from 0 to 1-level, they are competing directly with him since they are offering the same quality and are the same level. Notice that the 1-level seller’s curve flattens after four 1-level sellers are present in the population. The reason is that the next sellers to change over to 1-level return qualities of 3 and 4, respectively, so that they do not compete directly with the seller pictured. His profits, therefore, do not keep decreasing.

For this test, and other similar tests, we had to use a population of sellers that produce different qualities because, as explained in Section 6.3, if they had returned the same quality then an equilibrium would have been reached which would prevent the 1-level sellers from making a significantly greater profit than the 0-level sellers.

6.6 1-level buyers and 1 and 2-level sellers.

Assuming that the 2-level seller has perfect models of the other agents, we find that he wins an overwhelming percentage of the time. This is true, surprisingly enough, even when some of the 1-level sellers offer slightly higher quality goods. However, when the quality difference becomes too great (i.e. greater than 1), the buyers finally start to buy from the high quality 1-level sellers. This case is very similar to the ones with 0-level buyers and 0 and 1-level sellers and we can start to discern a recurring pattern. In this case, however, it is much more computationally expensive to maintain 2-level models. On the other hand, since these 2-level models are perfect, they are better predictors than the 1-level, which explains why the 2-level seller wins much more than the 1-level seller from Section 6.3.

7 Conclusions

| Buyers | Sellers | Lessons |

|---|---|---|

| 0-level | 0-level | Equilibrium reached only when all sellers offer |

| the same quality. Otherwise, we get oscillations. | ||

| Mean price increases when quality offered decreases. | ||

| 0-level | Any | Sellers have big incentives to lower quality/cost. |

| 0-level | 0-level and | 1-level seller beats others. |

| one 1-level | Quantitative advantage of being 1-level predicted by | |

| volatility and price distribution. | ||

| 0-level | 0-level and | 1-level sellers do better, as long as there |

| many 1-level | are not too many of them. | |

| 1-level | 0-level and | Buyers have upper hand. They buy from the most |

| one 1-level | preferred seller. | |

| 1-level sellers are usually at a disadvantage. | ||

| 1-level | 1-level and | Since 2-level has perfect models, it wins an |

| one 2-level | overwhelming percentage of time, except | |

| when it offers a rather lower quality. |

We have presented a framework for the development of agents with incremental modeling/learning capabilities, in an economic society of agents. These agents were built, and the execution of different agent populations leads us to the discovery of the lessons summarized in Table 2. The discovery of volatility and price distributions as predictors of the benefits of deeper models will be very useful as guides for deciding how much modeling capability to build into an agent. This decision could either be done prior to development or, given enough information, it could be done at runtime. We are also encouraged by the fact that increasing the agents’ capabilities changes the system in ways that we can recognize from our everyday economic experience.

Some of the agent structures shown in this paper are already being implemented into the UMDL [Atkins et al., 1996]. We have a basic economic infrastructure that allows agents to engage in commerce, and the agents use customizable heuristics for determining their strategic behavior. We are working on incorporating the more advanced modeling capabilities into our agents in order to enable more interesting strategic behaviors.

Our results showed how sellers with deeper models fare better, in general, even when they produce less valuable goods. This means that we should expect those types of agents to, eventually, be added into the UMDL666If not by us, then by a profit-conscious third party.. Fortunately, this advantage is diminished by having buyers keep deeper models. We expect that there will be a level at which the gains and costs associated with keeping deeper models balance out for each agent. Our hope is to provide a mechanism for agents to dynamically determine this cutoff and constantly adjust their behavior to maximize their expected profits given the current system behavior. The lessons in this paper are a significant step in this direction. We have seen that one needs to look at price volatility and at the modeling levels of the other agents to determine what modeling level will give the highest profits. We have also learned how buyers and sellers of different levels and offering different qualities lead to different system dynamics which, in turn, dictate whether the learning of nested models is useful or not.

We are considering the expansion of the model with the possible additions of agents that can both buy and sell, and sellers that can return different quality goods. Allowing sellers to change the quality returned to fit the buyer will make them more competitive against 1-level buyers. We are also continuing tests on many different types of agent populations in the hopes of getting a better understanding of how well different agents fare in the different populations.

In the long run, another offshoot of this research could be a better characterization of the types of environments and how they allow/inhibit “cheating” behavior in different agent populations. That is, we saw how, in our economic model, agents are sometimes rewarded for behavior that does not seem to be good for the community as a whole (e.g. when some of the sellers raised their price while lowering the quality they offered). The rewards, we are finding, start to diminish as the other agents become “smarter”. We can intuit that the agents in these systems will eventually settle on some level of nesting that balances their costs of keeping nested models with their gains from taking better actions [Kauffman, 1994]. It would be very useful to characterize the environments, agent populations, and types of “equilibria” that these might lead to, especially as interest in multi-agent systems grows.

References

- [Akerlof, 1970] Akerlof, G. A. (1970). The market for ‘lemons’: Quality uncertainty and the market mechanism. The Quaterly Journal of Economics, pages 488–500.

- [Atkins et al., 1996] Atkins, D. E., Birmingham, W. P., Durfee, E. H., Glover, E. J., Mullen, T., Rundensteiner, E. A., Soloway, E., Vidal, J. M., Wallace, R., and Wellman, M. P. (1996). Toward inquiry-based education through interacting software agents. IEEE Computer.

- [Axelrod, 1984] Axelrod, R. M. (1984). The Evolution of Cooperation. Basic Books.

- [Durfee et al., 1994] Durfee, E. H., Gmytrasiewicz, P. J., and Rosenschein, J. S. (1994). The utility of embedded communications and the emergence of protocols. In Proceedings of the 13th International Distributed Artificial Intelligence Workshop.

- [Epstein and Axtell, 1996] Epstein, J. M. and Axtell, R. L. (1996). Growing Artifical Societies: Social Science from the Bottom Up. Brookings Institution.

- [Glance, 1993] Glance, N. S. (1993). Dynamics with Expectations. PhD thesis, Stanford University.

- [Gmytrasiewicz, 1996] Gmytrasiewicz, P. J. (1996). On reasoning about other agents. In Wooldridge, M., Müller, J. P., and Tambe, M., editors, Intelligent Agents Volume II, Lecture Notes in Artificial Intelligence, pages 143–155. Springer-Verlag.

- [Hu and Wellman, 1996] Hu, J. and Wellman, M. P. (1996). Self-fulfilling bias in multiagent learning. In Proceedings of the Second International Conference on Multi-Agent Systems, pages 118–125.

- [Hübler and Pines, 1994] Hübler, A. and Pines, D. (1994). Complexity: Methaphors, Models and Reality, chapter Prediction and Adaptation in an Evolving Chaotic Environment, pages 343–379. Addison Wesley.

- [Kauffman, 1994] Kauffman, S. A. (1994). Complexity: Models, Metaphors and Reality, chapter Whispers from Carnot: The Origins of Order and Principles of Adaptation in Complex Nonequilibrium Systems, pages 83–136. Addison Wesley.

- [Mullen and Wellman, 1996] Mullen, T. and Wellman, M. P. (1996). Some issues in the design of market-oriented agents. In Wooldridge, M., Müller, J. P., and Tambe, M., editors, Intelligent Agents Volume II, Lecture Notes in Artificial Intelligence, pages 283–298. Springer-Verlag.

- [Nadella and Sen, 1997] Nadella, R. and Sen, S. (1997). Correlating internal parameters and external performance. In Weiß, G., editor, Distributed Artificial Intelligence Meets Machine Learning, pages 137–150. Springer.

- [Rosenschein and Zlotkin, 1994] Rosenschein, J. S. and Zlotkin, G. (1994). Rules of Encounter. The MIT Press, Cambridge, Massachusetts.

- [Russell, 1995] Russell, S. (1995). Rationality and intelligence. In Proceedings of the 14th International Joint Conference on Artificial Intelligence, pages 950–957.

- [Sen, 1996] Sen, S., editor (1996). Working Notes for the AAAI Symposium on Adaptation, Co-evolution and Learning in Multiagent Systems.

- [Shoham and Tennenholtz, 1992] Shoham, Y. and Tennenholtz, M. (1992). Emergent conventions in multi-agent systems. In Proceedings of Knowledge Representation.

- [Sutton, 1988] Sutton, R. S. (1988). Learning to predict by the methods of temporal differences. Machine Learning, 3:9–44.

- [Tambe and Rosenbloom, 1996] Tambe, M. and Rosenbloom, P. S. (1996). Architectures for agents that track other agents in multi-agent worlds. In Wooldridge, M., Müller, J. P., and Tambe, M., editors, Intelligent Agents Volume II, Lecture Notes in Artificial Intelligence, pages 156–170. Springer-Verlag.

- [Terabe et al., 1997] Terabe, M., Wasio, T., Katai, O., and Sawaragi, T. (1997). A study of organizational learning in multi-agent systems. In Weiß, G., editor, Distributed Artificial Intelligence Meets Machine Learning, pages 168–179. Springer.

- [Vidal and Durfee, 1996a] Vidal, J. M. and Durfee, E. H. (1996a). The impact of nested agent models in an information economy. In Proceedings of the Second International Conference on Multi-Agent Systems, pages 377–384. http://jmvidal.ece.sc.edu/papers/amumdl/.

- [Vidal and Durfee, 1996b] Vidal, J. M. and Durfee, E. H. (1996b). Using recursive agent models effectively. In Wooldridge, M., Müller, J. P., and Tambe, M., editors, Intelligent Agents Volume II, Lecture Notes in Artificial Intelligence, pages 171–196. Springer-Verlag. http://jmvidal.ece.sc.edu/papers/lr-rmm2/.

- [Watkins and Dayan, 1992] Watkins, C. J. and Dayan, P. (1992). Q-learning. Machine Learning, 8:279–292.