Technical Report IDSIA-15-03

Bayesian Treatment of Incomplete Discrete Data applied to Mutual

Information and

Feature Selection††thanks: This work was supported in parts by the NSF grants 2000-61847.00

and 2100-067961.02.

Abstract

Given the joint chances of a pair of random variables one can compute quantities of interest, like the mutual information. The Bayesian treatment of unknown chances involves computing, from a second order prior distribution and the data likelihood, a posterior distribution of the chances. A common treatment of incomplete data is to assume ignorability and determine the chances by the expectation maximization (EM) algorithm. The two different methods above are well established but typically separated. This paper joins the two approaches in the case of Dirichlet priors, and derives efficient approximations for the mean, mode and the (co)variance of the chances and the mutual information. Furthermore, we prove the unimodality of the posterior distribution, whence the important property of convergence of EM to the global maximum in the chosen framework. These results are applied to the problem of selecting features for incremental learning and naive Bayes classification. A fast filter based on the distribution of mutual information is shown to outperform the traditional filter based on empirical mutual information on a number of incomplete real data sets.

Keywords

Incomplete data, Bayesian statistics, expectation maximization, global optimization, Mutual Information, Cross Entropy, Dirichlet distribution, Second order distribution, Credible intervals, expectation and variance of mutual information, missing data, Robust feature selection, Filter approach, naive Bayes classifier.

1 Introduction

Let be the joint chances of a pair of random variables (,). Many statistical quantities can be computes if is known; for instance the mutual information used for measuring the stochastic dependency of and . The usual procedure in the common case of unknown chances is to use the empirical probabilities as if they were precisely known chances. This is not always suitable: The point estimate does not carry information about the reliability of the estimate. Samples may be incomplete in the sense that in some samples the variable or may not be observed.

The Bayesian solution to is to use a (second order) prior distribution over the chances themselves, which takes account of uncertainty about . From the prior and the likelihood of data one can compute the posterior . The traditional solution to is to assume that the data are missing at random [LR87]. A (local) maximum likelihood estimate for can then be obtained by the expectation-maximization (EM) algorithm [CF74].

In this work we present a full Bayesian treatment of incomplete discrete data with Dirichlet prior and apply the results to feature selection. This work is a natural continuation of [ZH02], which focused on the case of complete data and, by working out a special case, provided encouraging evidence for the extension of the proposed approach to incomplete data. Here we develop that framework by creating a very general method for incomplete discrete data, providing the complete mathematical derivations, as well as experiments on incomplete real data sets. In particular, Section 2 derives expressions (in leading order in ) for . In the important case (for feature selection) of missingness in one component of only, we give closed form expressions for the mode, mean and covariance of . In the general missingness case we get a self-consistency equation which coincides with the EM algorithm, that is known to converge to a local maximum. We show that is actually unimodal, which implies that in fact EM always converges to the global maximum. We use the results to derive in Section 3 closed-form leading order expressions of the distribution of mutual information . In case of complete data, the mean and variance of have been approximated numerically in [Kle99] and analytically in [Hut02]. The results are then applied to feature selection in Section 4. A popular filter approach discards features of low empirical mutual information [Lew92, BL97, CHH+02]. We compare this filter to the two filters (introduced in [ZH02] for complete data and tested empirically in this case) that use credible intervals based on to robustly estimate mutual information. The filters are empirically tested in Section 5 by coupling them with the naive Bayes classifier [DHS01] to incrementally learn from and classify incomplete data. On five real data sets that we used, one of the two proposed filters consistently outperforms the traditional filter.

2 Posterior Distribution for Incomplete Data

2.1 Missing data

Consider two discrete random variables, class and feature111The mathematical development is independent of the interpretation as class and feature, but it is convenient to use this terminology already here. taking values in and , respectively, and an i.i.d. random process with samples drawn with joint probability . In practice one often has to deal with incomplete information. For instance, observed instances often consist of several features plus class label, but some features may not be observed, i.e. if is a class label and is a feature, from the pair only is observed. We extend the contingency table to include , which counts the number of instances in which only the class is observed (= number of instances). Similarly, counts the number of instances, where the class label is missing. We make the common assumption that the missing-data mechanism is ignorable (missing at random and distinct) [LR87], i.e. the probability distribution of class labels of instances with missing feature is assumed to coincide with the marginal . Similarly, given an instance with missing class label, the probability of the feature being is assumed to be .

2.2 Maximum likelihood estimate of

The likelihood of a specific data set of size with contingency table given , hence, is . Assuming a uniform , Bayes’ rule leads to the posterior222Most (but not all) non-informative priors for also lead to a Dirichlet posterior distribution with interpretation , where are the number of samples , and comprises prior information ( for the uniform prior, for Jeffreys’ prior, for Haldane’s prior, for Perks’ prior, and other numbers in case of specific prior knowledge [GCSR95]). Furthermore, in leading order in , any Dirichlet prior with leads to the same results, hence we can simply assume a uniform prior. The reason for the is that must be constrained to the probability simplex .

| (1) |

where the normalization is chosen such that . With missing features and classes there is no exact closed form expression for .

In the following, we restrict ourselves to a discussion of leading-order (in ) expressions, which are as accurate as one can specify one’s prior knowledge [Hut02]. In leading order, the mean coincides with the mode of (=the maximum likelihood estimate) of . The log-likelihood function is

where we have replaced the function by a Lagrange multiplier to take into account the restriction . The maximum is at . Multiplying this by and summing over and we obtain . The maximum likelihood estimate is, hence, given by

| (2) |

This is a non-linear equation in , which, in general, has no closed form solution. Nevertheless (2) can be used to approximate . Eq. (2) coincides with the popular expectation-maximization (EM) algorithm [CF74] if one inserts a first estimate into the r.h.s. of (2) and then uses the resulting l.h.s. as a new estimate, etc.

2.3 Unimodality of

The Hessian matrix of and the second derivative in direction of the dimensional column vector are

This shows that is a convex function of , hence has a single (possibly degenerate) global maximum. is strictly convex if for all , since in this case333Note that is not sufficient, since for is possible. Actually .. This implies a unique global maximum, which is attained in the interior of the probability simplex. Since EM is known to converge to a local maximum, this shows, that in fact EM always converges to the global maximum.

2.4 Covariance of

With

| (3) |

and we can represent the posterior to leading order as an dimensional Gaussian:

| (4) |

The easiest way to compute the covariance (and other quantities) is to also represent the -function as a narrow Gaussian of width . Inserting into (4), where for all (hence ), leads to a full -dimensional Gaussian with kernel , . The covariance of a Gaussian with kernel is . Using the Sherman-Morrison formula [PFTV92, p73] and we get

| (5) |

where denotes up to terms of order . Singular are easily avoided by choosing a prior such that for all . may be inverted exactly or iteratively, the latter by a trivial inversion of the diagonal part and by treating as a perturbation.

2.5 Missing features only, no missing classes

In the case of missing features only (no missing classes), i.e. for , closed form expressions for can be obtained. If we sum (2) over we get with . Inserting into the r.h.s. of (2) and solving w.r.t. we get the explicit expression

| (6) |

Furthermore, it can easily be verified (by multiplication) that has inverse . With the abbreviations

| (7) |

we get and . Inserting everything into (5) we get

| (8) |

2.6 Expressions for the general case

The contribution from unlabeled classes can be interpreted as a rank modification of in the case of no missing classes. One can use Woodbury’s formula [PFTV92, p75] with , , and to reduce the inversion of the matrix to the inversion of only a single -dimensional matrix. The result (which may be inserted into (5)) can be written in the form

| (9) |

3 Distribution of Mutual Information

3.1 Mutual information

An important measure of the stochastic dependence of and is the mutual information

The point estimate for is . In the Bayesian approach one takes the posterior (1) from which the posterior probability density of the mutual information can, in principle, be computed:444 denotes the mutual information for the specific chances , whereas in the context above is just some non-negative real number. will also denote the mutual information random variable in the expectation and variance . Expectations are always w.r.t. to the posterior distribution .

| (10) |

The distribution restricts the integral to for which . For large sample size, , is strongly peaked around the mode and gets strongly peaked around the frequency estimate . The (central) moments of are of special interest. The mean

| (11) |

coincides in leading order with the point estimate, where has been computed in Section 2. Together with the variance (computed below) we can approximate (10) by a Gaussian666For the central limit theorem ensures convergence of to a Gaussian. Using a Beta distribution instead of (12), which also converges to a Gaussian, has slight advantages over (12) [ZH02].

| (12) |

In a previous work we derived higher order central moments (skewness and kurtosis) and higher order (in ) approximations in the case of complete data [Hut02].

3.2 Variance of

The leading order variance of the mutual information has been related777 was defined in [Hut02] as the mean whereas has been defined in this work as the ML estimate. Furthermore the Dirichlet priors differ. Since to leading order both definitions of coincide, the prior does not matter, and the expression is also valid for incomplete data case, the use of (13) in this work is permitted. in [Hut02] to the covariance of :

| (13) |

Inserting (8) for the covariance into (13) we get for the variance of the mutual information in leading order in in the case of missing features only, the following expression:

| (14) |

A closed form expression for also exists. Symmetric expressions for missing classes only (no missing features) can be obtained. Note that for the complete case , we have , , , , , and , consistent with [Hut02] (where and are defined and the accuracy is discussed).

There is at least one reason for minutely having inserted all expressions into each other and introducing quite a number definitions. In the so presented form all expressions involve at most a double sum. Hence, the overall computation time of the mean and variance is in the case of missing features only.

3.3 Expression for the general case

The result for the covariance (5) can be inserted into (13) to obtain the variance of the mutual information to leading order.

Inserting (9) and rearranging terms appropriately we can compute Var[] in time plus the time to compute the matrix and time to invert it, plus the time for determining , where is the number of iterations of EM. Of course, one can and should always choose . Note that these expressions converge for to the exact values. The fraction of data with missing feature or class needs not to be small.

4 Feature Selection

Feature selection is a basic step in the process of building classifiers [BL97]. We consider the well-known filter (F) that computes the empirical mutual information between features and the class, and discards features with for some threshold [Lew92]. This is an easy and effective approach that has gained popularity with time.

We compare F to the two filters introduced in [ZH02] for the case of complete data, and extended here to the more general case. The backward filter (BF) discards a feature if its value of mutual information with the class is less than or equal to with high probability (discard if ). The forward filter (FF) includes a feature if the mutual information is greater than with high probability (include if ). BF is a conservative filter, because it will only discard features after observing substantial evidence supporting their irrelevance. FF instead will tend to use fewer features, i.e. only those for which there is substantial evidence about them being useful in predicting the class.

For the subsequent classification task we use the naive Bayes classifier [DH73], which is often a good classification model. Despite its simplifying assumptions (see [DP97]), it often competes successfully with much more complex classifiers, such as C4.5 [Qui93]. Our experiments focus on the incremental use of the naive Bayes classifier, a natural learning process when the data are available sequentially: the data set is read instance by instance; each time, the chosen filter selects a subset of features that the naive Bayes uses to classify the new instance; the naive Bayes then updates its knowledge by taking into consideration the new instance and its actual class. Note that for increasing sizes of the learning set the filters converge to the same behavior, since the variance of tends to zero (see [ZH02] for details).

For each filter, we are interested in experimentally evaluating two quantities: for each instance of the data set, the average number of correct predictions (namely, the prediction accuracy) of the naive Bayes classifier up to such instance; and the average number of features used. By these quantities we can compare the filters and judge their effectiveness.

The implementation details for the following experiments include: using the Gaussian approximation (12) to the distribution of mutual information with the mean (11) using (6), and the variance (14) using (7) and (3); using natural logarithms everywhere; and setting the level of the posterior probability to , and the threshold to 0.003 as discussed in [ZH02].

5 Experimental Analysis

Table 1 lists five data sets together with the experimental results. These are real data sets on a number of different domains.

| Name | #feat. | #inst. | #m.v. | maj.class | FF | F | BF |

|---|---|---|---|---|---|---|---|

| Audiology | 69 | 226 | 317 | 0.212 | 64.3 | 68.0 | 68.7 |

| Crx | 15 | 690 | 67 | 0.555 | 9.7 | 12.6 | 13.8 |

| Horse-colic | 18 | 368 | 1281 | 0.630 | 11.8 | 16.1 | 17.4 |

| Hypothyroidloss | 23 | 3163 | 1980 | 0.952 | 4.3 | 8.3 | 13.2 |

| Soybean-large | 35 | 683 | 2337 | 0.135 | 34.2 | 35 | 35 |

The data sets presenting non-nominal features have been pre-discretized by MLC++ [KJL+94], default options (i.e., the common entropy based discretization). This step may remove some features judging them as irrelevant, so the number of features in the table refers to the data sets after the possible discretization. The instances have been randomly sorted before starting the experiments.

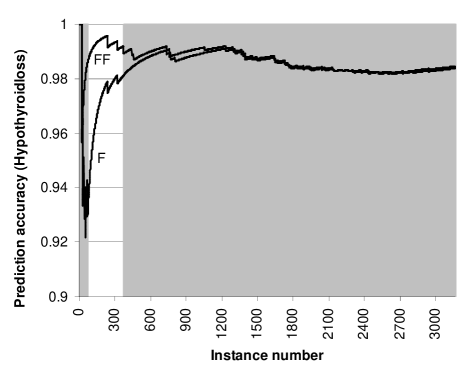

The last three columns of Table 1 show that FF selects lower (i.e. better) number of features than the commonly used filter F, which in turn, selects lower number of features than the filter BF. We used the two-tails paired t test at level 0.05 to compare the prediction accuracies of the naive Bayes with different filters, in the first instances of the data set, for each . On four data sets out of five, both the differences between FF and F, and the differences between F and BF, were never statistically significant, despite the different number of used features, as indicated in Table 1. The reduction can be very pronounced, as for the Hypothyroidloss data set. This is also the only data set for which the prediction accuracies of F and FF are significantly different, in favor of the latter. This is displayed in Figure 1. Similar (even stronger) results have been found for 10 complete data sets analyzed in [ZH02].

The most prominent evidence from the experiments is the better performance of FF versus the traditional filter F. In the following we look at FF from another perspective to exemplify and explain its behavior. FF includes a feature if , according to its definition. Let us assume that FF is realized by means of the Gaussian (as in the experiments above), and let us choose . The condition becomes , or, in an approximate way, , given that is the first-order approximation of (cf. (11)). We can regard as a new threshold . Under this interpretation, we see that FF is approximately equal to using the filter F with the bigger threshold . This interpretation makes it also clearer why FF can be better suited than F for sequential learning tasks. In sequential learning, decreases as new units are read; this makes to be a self-adapting threshold that adjusts the level of caution (in including features) as more units are read. In the limit, is equal to . This characteristic of self-adaptation, which is absent in F, seems to be decisive to the success of FF.

6 Conclusions

We addressed the problem of the reliability of empirical estimates for the chances and the mutual information in the case of incomplete discrete data. We used the Bayesian framework to derive reliable and quickly computable approximations for the mean, mode and the (co)variance of and under the posterior distribution . We showed that is unimodal, which implies that EM always converges to the global maximum. The results allowed us to efficiently determine credible intervals for with incomplete data. Applications are manifold, e.g. to robustly infer classification trees or Bayesian networks. As far as feature selection is concerned, we empirically showed that the forward filter, which includes a feature if the mutual information is greater than with high probability, outperforms the popular filter based on empirical mutual information in sequential learning tasks. This result for incomplete data is obtained jointly with the naive Bayes classifier. More broadly speaking, obtaining the distribution of mutual information when data are incomplete may form a basis on which reliable and effective uncertain models can be developed.

References

- [BL97] A. L. Blum and P. Langley. Selection of relevant features and examples in machine learning. Artificial Intelligence, 97(1–2):245–271, 1997. Special issue on relevance.

- [CF74] T. T. Chen and S. E. Fienberg. Two-dimensional contingency tables with both completely and partially cross-classified data. Biometrics, 32:133–144, 1974.

- [CHH+02] J. Cheng, C. Hatzis, H. Hayashi, M. Krogel, S. Morishita, D. Page, and J. Sese. KDD cup 2001 report. ACM SIGKDD Explorations, 3(2), 2002.

- [DH73] R. O. Duda and P. E. Hart. Pattern classification and scene analysis. Wiley, New York, 1973.

- [DHS01] R. O. Duda, P. E. Hart, and D. G. Stork. Pattern classification. Wiley, 2001. 2nd edition.

- [DP97] P. Domingos and M. Pazzani. On the optimality of the simple Bayesian classifier under zero-one loss. Machine Learning, 29(2/3):103–130, 1997.

- [GCSR95] A. Gelman, J. B. Carlin, H. S. Stern, and D. B. Rubin. Bayesian Data Analysis. Chapman, 1995.

- [Hut02] M. Hutter. Distribution of mutual information. In T. G. Dietterich, S. Becker, and Z. Ghahramani, editors, Advances in Neural Information Processing Systems 14, pages 399–406, Cambridge, MA, 2002. MIT Press.

- [KJL+94] R. Kohavi, G. John, R. Long, D. Manley, and K. Pfleger. MLC++: a machine learning library in C++. In Tools with Artificial Intelligence, pages 740–743. IEEE Computer Society Press, 1994.

- [Kle99] G. D. Kleiter. The posterior probability of Bayes nets with strong dependences. Soft Computing, 3:162–173, 1999.

- [Lew92] D. D. Lewis. Feature selection and feature extraction for text categorization. In Proc. of Speech and Natural Language Workshop, pages 212–217, San Francisco, 1992. Morgan Kaufmann.

- [LR87] R. J. A. Little and D. B. Rubin. Statistical Analysis with Missing Data. John-Wiley, New York, 1987.

- [MA95] P. M. Murphy and D. W. Aha. UCI repository of machine learning databases, 1995. http://www.sgi.com/Technology/mlc/db/.

- [PFTV92] W. H. Press, B. P. Flannery, S. A. Teukolsky, and W. T. Vetterling. Numerical Recipes in C: The Art of Scientific Computing. Cambridge University Press, Cambridge, second edition, 1992.

- [Qui93] J. R. Quinlan. C4.5: Programs for Machine Learning. Morgan Kaufmann, San Mateo, 1993.

- [ZH02] M. Zaffalon and M. Hutter. Robust feature selection by mutual information distributions. In A. Darwiche and N. Friedman, editors, Proceedings of the 18th International Conference on Uncertainty in Artificial Intelligence (UAI-2002), pages 577–584, San Francisco, CA., 2002. Morgan Kaufmann.