Stochastic Volatility in a Quantitative Model of Stock Market Returns

Professor David S. Brée

Abstract

Standard quantitative models of the stock market predict a log-normal distribution for stock returns (Bachelier 1900, Osborne 1959), but it is recognised (Fama 1965) that empirical data, in comparison with a Gaussian, exhibit leptokurtosis (it has more probability mass in its tails and centre) and fat tails (probabilities of extreme events are underestimated). Different attempts to explain this departure from normality have coexisted. In particular, since one of the strong assumptions of the Gaussian model concerns the volatility, considered finite and constant, the new models were built on a non finite (Mandelbrot 1963) or non constant (Cox, Ingersoll and Ross 1985) volatility.

We investigate in this thesis a very recent model (Dragulescu et al. 2002) based on a Brownian motion process for the returns, and a stochastic mean-reverting process for the volatility. In this model, the forward Kolmogorov equation that governs the time evolution of returns is solved analytically. We test this new theory against different stock indexes (Dow Jones Industrial Average, Standard and Poor’s and Footsie), over different periods (from 20 to 105 years). Our aim is to compare this model with the classical Gaussian and with a simple Neural Network, used as a benchmark.

We perform the usual statistical tests on the kurtosis and tails of the expected distributions, paying particular attention to the outliers. As claimed by the authors, the new model outperforms the Gaussian for any time lag, but is artificially too complex for medium and low frequencies, where the Gaussian is preferable. Moreover this model is still rejected for high frequencies, at a 0.05 level of significance, due to the kurtosis, incorrectly handled.

Acknowledgements

I would like to express my thanks and appreciation to my supervisor, Professor David S. Brée, for his valuable advice and guidance, and my gratitude to Reader Nathan L. Joseph from the Accounting and Finance Department of the University of Manchester, for his continuous support and assistance.

I would also like to thank Robert Woolfson (Ph.D. Student) for his help and enlightening comments and Bin Yang (M.Sc. Student) for his patience and skills as a team worker.

I feel a deep sense of gratitude for my father and mother, Hubert and Gina, who formed part of my vision and taught me the good things that really matter in life. I am grateful for my brother, Vincent, for rendering me the sense and the value of brotherhood.

Finally, the chain of my gratitude would be definitely incomplete if I would forget to thank my fellows in Manchester, Laure, Bruno, Fabrice, Vivek, Matthias, Arnaud, ToLiS, Darko and Tom, and more generally my very close friends, Guillaume, Jerôme, Max and Hugues.

Without the help of all these people none of the current work would have been feasible.

Dedication

A Paul,

Qui vit désormais à travers nous

Chapter 1 Introduction

1.1 A two century old paradigm

Many attempts have been made, since the first agreement to trade on the NYSE in 1792, to model the stock market’s behaviour. Understanding the patterns that govern this heart of the capitalism is more than challenging, it is a crusade. But so far, can anybody claim to have found out the rules enabling them to predict tomorrow’s move for instance? And do these rules even exist? Actually, the efficient markets theory states that market prices reflect the knowledge and expectations of all investors. As a consequence, this theory predicts, according to E. Fama [Fam65], that the market would react quickly to such a discovery and these patterns would be modified instantly. Contrary to natural laws that govern physics, laws of the market adjust themselves to new discoveries.

Anyhow, financial and scientific communities persist in building new models, not only because we are eager to understand, but mainly because predicting tomorrow’s move is not the only way to make money. Where the study of Fundamentals or Technical Analysis are broadly used by traders on the market floor, Quantitative Finance tries to evaluate risk and hence price options using statistical models of the market.

1.2 Aims

We will present in this thesis the theory underlying most of these models, the Theory of Random Walks. Then we will discuss the different hypotheses that have been proposed, in the Bachelier-Osborne and Mandelbrot models, concerning a major parameter, the standard deviation. This parameter is crucial since it represents the volatility of the market, and is used for instance in Value-at-Risk. After having confronted these models with empirical data, we will see that the structure of the market implies neither a constant standard deviation, as thought initially, nor an infinite standard deviation: the Probability Density Function (PDF) of the log-returns exhibits fat tails and kurtosis (peakedness or flatness compared to a Gaussian), with finite standard deviation.

Then we will focus on one of these models, published very recently by A. A. Dragulescu and V. M. Yakovenko, from the University of Maryland. Their paper [DY], “Probability distribution of returns with stochastic volatility” introduces a new model for volatility of stock market indexes. The proposed probability density function of stock returns seems to fit empirical data much better than previous models. We will double-check their results and propose a methodology to test their model against empirical data.

But first, let’s have a look at the different models of the market. Some are used by traders to try to predict tomorrow’s move, others by derivative traders to price options or by risk managers to set the global policy of an Investment Bank, for instance.

1.3 Usual Stock Market Prediction Methods

On market floors, two radically different types of traders usually coexist: fundamentalists and chartists. Fundamentalists believe that the stock price of a company reflects its intrinsic value. This intrinsic value depends on the present and forecast economic situation of the company (its “fundamentals”), and is mainly influenced by any new piece of information about these fundamentals. The problem is to evaluate this intrinsic value.

On the other hand, chartists only analyse historical data (the “charts”) of the stock, mainly the historical price, but other indicators as well, such as traded volumes, volatility, past resistance and support thresholds, etc. They try hard to find out hidden patterns that replicate over days, weeks, month or years, according to their speculative or investment needs. The assumption is that the market should have a short/long term memory, so we could use the past to predict the future. But here, the efficient market hypothesis asserts that all information which can be learned from technical analysis of stock prices is already reflected in those prices. According to this hypothesis, past stock prices may be useful to estimate the parameters of the distribution of future returns, but they do not provide information which permits an investor to outperform the market.

1.4 Quantitative Methods

Broadly speaking, none of those stock traders (fundamentalists or chartists) daily use the quantitative models we are describing in this thesis. But these models are used on the floor by derivative traders and in risk divisions of investment banks to elaborate the global trading policy of the bank, the risk aversion, the over-night limits of individual traders, etc.

Now the reader won’t be surprised to learn that quantitative models are neither fundamentalists nor chartists. They are much more deeply involved with maths. In fact, the theory underlying most of these models, called the “Theory of Random Walks”, claims that successive price changes () or price returns () are independent, identically distributed random variables. This i.i.d. hypothesis has been studied by E. Fama in 1965 [Fam65] and is still discussed today. We will discuss the independence of successive price changes in Chapter 2, but at the moment we will study different models that make this very strong assumption.

Under this assumption of i.i.d. price returns, many models have been developed, but two of them are used commonly nowadays. The first and most common one, called the Bachelier-Osborne model and elaborated in 1959, states that price returns have a constant finite volatility over a given period of time (“time lag ”), e.g. one day, one week, one month, etc. This theory results in a log-normal distribution for price returns and a volatility proportional to the square root of the time lag, i.e. the weekly volatility will be about times higher than the daily one. But it is now known that price returns do not follow a Gaussian distribution, since they exhibit kurtosis and fat tails: dramatic draw downs and spectacular jumps arise far more often than predicted by a Normal distribution. Hence, the idea of infinite volatility appeared. It was introduced by Mandelbrot in 1963 and leads to stable Pareto-Levy distributions that can exhibit fat tails. Unfortunately, the hypothesis of infinite volatility supposes that the variance increases indefinitely with sample size, which is not verified by empirical data. Variance first increases then reaches a bound [CB00].

1.5 Conclusion

For centuries, practitioner’s have tried to model and predict the financial markets, using diverse techniques such as fundamental study or technical analysis. With the rapid growth of statistics and stochastic calculus fifty years ago, new quantitative methods were born that seem to be able to handle the complexity of the stock market.

The main model, Bachelier-Osborne, will be detailed in Chapter 2. We will see that it suffers mainly from two imperfections, high kurtosis and fat tails, that still remain to be explained. A. Dragulescu and V. Yakovenko published in March 2002 an improvement of this model, based on a stochastic finite volatility, that seems to fit the data perfectly. We will analyse this model in Chapter 3 and test it in Chapter 4.

But first, let us present the basis of most of stock returns models, the Theory of Random Walks.

Chapter 2 The Theory of Random Walks

2.1 Introduction

The Theory of Random Walks has been used for the last 35 years by the main statistical models of the stock markets. It was first introduced by Bachelier in his 1900 dissertation written in Paris, ”Théorie de la Spéculation” (and in his subsequent work, esp. 1906, 1913), in which he anticipated much of what was to become standard fare in financial theory: the random walk of financial market prices, Brownian motion and martingales (all before both Einstein and Wiener!). His innovativeness, however, was not appreciated by his professors or contemporaries. His dissertation received poor marks from his teachers and, consequently blackballed, he quickly dropped into the shadows of the academic underground. After a series of minor posts, he ended up obscurely teaching in Besancon for much of the rest of his life. Virtually nothing else is known of this pioneer - his work being largely ignored until the 1960s when Osborne introduced his model based on Bachelier’s work.

A random walk is a random process consisting of a sequence of discrete steps of fixed length totally independent one from another. For instance, the random thermal perturbations in a liquid are responsible for a random walk phenomenon known as Brownian motion, and the collisions of molecules in a gas are a random walk responsible for diffusion.

Applied to our problem, this theory is founded on two strong hypothesis: price returns are independent (tomorrow’s price return does not depend on today’s or on any other price return) and identically distributed (they all follow the same distribution). This is called the i.i.d. hypothesis.

Throughout this thesis, we will use these notations

| price change | price return | log return |

|---|---|---|

| where | log is the natural logarithm |

|---|---|

| is the close price of the security at time | |

| is the close price of the security at time | |

| is the time lag |

For instance, if the close price of the studied index is 106 today and was 105 yesterday, the daily (time lag = 1) values are

| price change | price return | log return |

|---|---|---|

By “day”, we mean trading day, since all of our datasets are composed of trading days only: week-ends and bank holidays have been removed. By “time lag”, we mean the number of days between two points used to compute a log return. If our initial dataset is composed of 1000 close prices, then for a time lag of five days, we will take one point every five to compute the log returns. As a consequence, our final dataset will will be composed of log returns only. Nevertheless, we can begin by the first, the second, the third, the fourth or the fifth close price, so that finally, we can use five different datasets of 200 log returns. This will allow us to give, for any computation, the average value and an estimate of the variance of the result, which will give greater robustness to our statistical tests.

We will usually use the log return, mainly for two reasons:

-

1.

financially, it corresponds to the continuously compounded return of the asset S;111If is the continuously compounded return of an asset S, then the value of S at time t is = for t [0,T]

-

2.

numerically, it has the advantage of guaranteeing the positivity of the price.

Obviously, any hypothesis about the independence and identical distribution of price changes is directly applicable to price returns and log returns.

According to the theory of random walks, the price change series is a collection of random variables having the property that, given the present, the future is conditionally independent of the past. In other words,

or, formulated directly in terms of price at time t

To sum up, in such a process without memory, the last realisation contains all of the information. This process is known as a Markov process.

Before we go more deeply in the mathematics of the theory of random walks, and study the main statistical model of stock market behaviour, the Bachelier-Osborne model, let us discuss the i.i.d. hypothesis itself.

2.2 Independence of price returns

As said before, all of the assumptions about price returns can be applied to price changes and log returns. Since we will not consider the mathematical aspect of the theory in this paragraph, we will prefer to use the price returns, simpler to tackle and often discussed in the financial press in terms of percentage of variation.

The hypothesis of independent price returns is extremely important - and controversial - since it underlies all of the theory of random walks, and so all of the models developed around it. E. Fama discussed abundantly this hypothesis in his paper ”The Behavior of Stock-Market Prices” [Fam65] and states that the independence of price returns is the result of a noisy price mechanism. By noise, one should understand the psychology of different traders and the uncertainty or disagreement about the intrinsic value of the security, which depends on new information arrived or about to arrive. If successive bits of new information arise independently across time and if noise or uncertainty concerning intrinsic value does not tend to follow any consistent pattern, then successive price returns in a common stock will be independent.

A third and crucial condition for independence of price returns is the existence of ”superior traders”, viz. traders who will detect abnormalities on stock prices - departure of the security price from its intrinsic value - and will correct them by buying (resp. selling) the security if it is underestimated (resp. overestimated). If there are enough such traders, then the price will tend to stabilise around its intrinsic value, reducing risks of bubbles or crashes.

In the light of the recent scandals about the conflicts of interests of financial analysts working for the largest Investment Banks that participated in the creation of the speculative bubble around the ”new economy”, it is legitimate to wonder if this last condition enunciated by Fama is still respected, and then if the hypothesis of independent price returns still holds. But this problem is out of the scope of this thesis, and from now on we will make the assumption that the hypothesis underlying the Random Walk are respected: price returns will be considered independent and identically distributed.

Let us have a look now at the classical statistical model of the stock market, the Geometric Brownian Motion.

2.3 Bachelier-Osborne Model

The basic theory, known as the Bachelier-Osborne model, states that the stock index prices follows a Geometric Brownian Motion (GBM). The description ”Brownian motion” comes from the fact that the same process describes the physical motion of a particle subject to random shocks, a phenomenon first noted by the British physicist Brown in 1828, observing irregular movement of pollen suspended in water. The first mathematically rigorous construction of Brownian motion was carried out by Wiener in 1923. This theory is based on Markov Processes, Wiener processes and Itô processes, which are detailed in Appendix A. We summarise here the basic idea of the GBM.

Let the price be a non negative stochastic process.

And the log return

The idea, first introduced by Bachelier [Bac00], even if he used a Brownian motion and not a geometric Brownian motion, is that for a given time lag t, the log return is the sum of a large number of i.i.d. random variables

Then if we assume that the distribution followed by the has finite moments, and specially finite variance, then the Central Limit Theorem states directly that must follow a Normal distribution. Osborne formalised this in 1959 using the following equation, called Geometric Brownian Motion, for the stock price

| (2.1) |

where and are two constants called the drift and the volatility, and W is a standard Wiener process.222See Appendix A. The increments of W, , are normally distributed with and

We will demonstrate that obeys a simple Brownian motion with an instantaneous expectation and an instantaneous volatility .

We start from 2.1 and apply Itô’s lemma to the following function

We obtain

| (2.2) | |||||

Besides

| (2.3) | |||||

| where | |

|---|---|

| and |

| (2.4) | |||||

From 2.4, we see that follows a simple Brownian motion. If , then is governed by the following equation:

| (2.5) |

Log returns follow a simple Brownian motion, and are then normally distributed. Indeed, 2.5 admits the solution

| (2.6) |

Or formulated differently

| (2.7) |

This model is known as the Bachelier-Osborne model, and predicts a log-normal distribution for the price .

2.4 Departure from normality

According to the GBM model, stock prices should be log-normally distributed, i.e. stock log-returns should be normally distributed:

Nevertheless, it is now well known that log returns exhibit two specific kinds of departure from a Gaussian: kurtosis and fat tails. A high kurtosis means that the model distribution is more peaked than a Gaussian around the mean. Fat tails mean that crashes and huge increases appear far more often than predicted by the normal law. Let us consider the probability density function (PDF) of log returns for the different datasets we have:

-

•

DJIA1982: Dow Jones Industrial Average from January 04, 1982 to December 31, 2001

-

•

DJIA1988: Dow Jones Industrial Average from January 04, 1988 to December 31, 2001

-

•

DJIA1930: Dow Jones Industrial Average from January 02, 1930 to December 31, 2001

-

•

DJIA1896: Dow Jones Industrial Average from May 26, 1896 to December 31, 2001

-

•

SP1965: Standard and Poor’s 500 from January 04, 1965 to December 31, 2001

-

•

FTSE1984: FTSE100 from January 04, 1984 to December 31, 2001

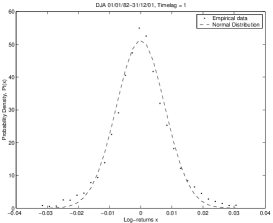

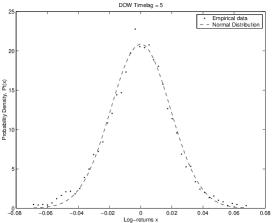

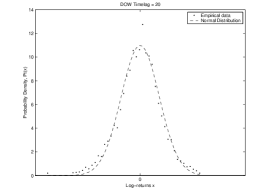

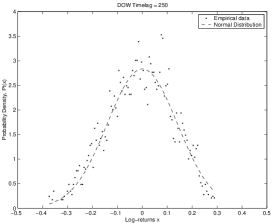

We will perform a few tests to exhibit more precisely the kurtosis and fat tails. These tests will be reproduced later on Dragulescu’s model. Before we perform our tests, let us have a look at a few examples of PDFs: we plot the PDFs for different time lags ( trading days) against a Normal distribution based on the sample mean and variance.

|

|

|

|

The issue is whether the Normal distribution fits empirical data sufficiently well, or whether the model should be rejected.

2.4.1 Measure of kurtosis: Jarque-Bera Test

If log returns really follow a Normal distribution, then we are expecting a null value for the Fisher kurtosis.333See Appendix B, Section “Kurtosis” Kurtosis is a measure of whether the data are peaked or flat relative to a normal distribution. That is, data sets with high kurtosis tend to have a distinct peak near the mean, decline rather rapidly, and have heavy tails. We compute the kurtosis for each dataset, and for different time lags. As explained above, we can give an estimate of the standard deviation (indicated into parenthesis) of the kurtosis for time lags superior to 1, because we compute the kurtosis on many different datasets, or “paths”. Are results are presented in Tables 2.1, 2.2, and 2.3.

| time lag | DJIA1982 | DJIA1988 | ||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

| time lag | DJIA1896 | DJIA 1930 | ||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

| time lag | SP1965 | FTSE1984 | ||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

We can clearly see that for every dataset, empirical log returns exhibit high kurtosis for high frequencies (time lag = 1 and 5 days) and medium frequencies (time lag = 20, 40 and 80 days), and small (for the largest datasets only, DJIA1896 and DJIA1930) or no kurtosis for low frequencies (time lag = 200 and 250 days). But the standard deviation is very high compared with the mean value, which means that some paths exhibit very high kurtosis whereas others exhibit very little. For instance, let us have a look at the five paths of the 5 days time lag returns of the DJIA1982. Results are shown in Table 2.4.

| path | kurtosis | |||||||||||||||

|

|

The kurtosis goes from 3.99 to 38.20, with a mean and standard deviation of 16.87 and 16.20 respectively. Only two paths out of five exhibit very high kurtosis, which is enough to have a high mean, but the large standard deviation must remind us of the important heterogeneity of the different paths.

On average, the probability mass of empirical log returns is leptokurtic444See appendix B, Section “Measures of kurtosis” for high frequencies. This departure from normality should enable us to reject the normal hypothesis.

To verify, we perform a Jarque-Bera test, which tests the goodness-of-fit to a normal distribution, according to the skewness and kurtosis.555See Appendix B, Section “Jarque-Bera Goodness-of-Fit Test” It tests a composite hypothesis, which means that the parameters of the tested distribution, viz. the mean and variance of the normal distribution, can be derived from the empirical data, and do not need to be known in advance. For each path, the output of the test is 0 if we do not reject the null hypothesis (viz the normal hypothesis) at a significance level , and 1 if we reject it. We give in Table 2.5 the average of the tests. For instance, for a time lag of 80 days, we perform the Jarque-Bera test 80 times, on 80 different log returns datasets. An average value of 0.9 means that the test rejected the null hypothesis 90% of the time, i.e. 72 out of 80 datasets.

| time lag | DJIA1988 | DJIA1982 | DJIA1930 | DJIA 1892 | SP1965 | FTSE1984 |

|---|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 |

| 20 | 0.65 | 1 | 1 | 1 | 1 | 1 |

| 40 | 0.625 | 1 | 1 | 1 | 1 | 0.975 |

| 80 | 0.2375 | 0.9 | 1 | 1 | 0.5375 | 0.8 |

| 100 | 0.08 | 0.6 | 1 | 1 | 0.23 | 0.54 |

| 200 | 0 | 0 | 1 | 0.97 | 0.01 | 0 |

| 250 | 0 | 0 | 1 | 0.964 | 0.064 | 0 |

For each dataset, for high frequencies, the normal hypothesis is systematically rejected. For low frequencies, except for the largest datasets (DJIA1896 and DJIA1930), which exhibit small kurtosis, the normal distribution cannot be rejected. The conclusion is not straightforward for middle frequencies.

2.4.2 Fat tails: Normal Probability Plot and Lilliefors Test

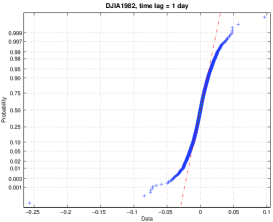

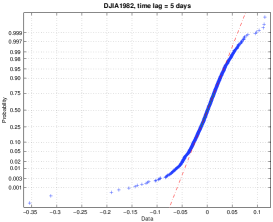

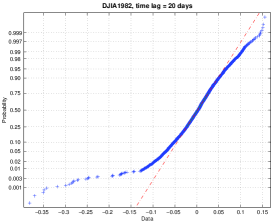

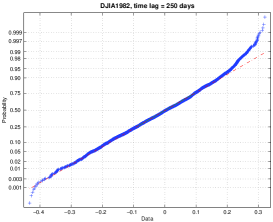

The other important departure from Normality consist of fat tails, that could be exhibited by performing a probability plot. This time, we do not perform a test on each dataset and each time lag, since a few examples should be enough. We select the first dataset, the Dow Jones Industrial Average, from January 04, 1982, to December 31, 2001 and draw the Normal Probability Plot on the log returns. The results are presented in Figure 2.2.

|

|

|

|

We can make the following conclusions from the above plot:

-

1.

The normal probability plot shows a non-linear pattern;

-

2.

The normal distribution is not a good model for these data.

For data with short (less variance than expected in a normal distribution) or long (more variance than expected in a normal distribution) tails relative to the normal distribution, the non-linearity of the normal probability plot shows up in two ways. First, the middle of the data shows an S-like pattern. This is common for both short and long tails. Second, the first few and the last few points show a marked departure from the reference fitted line. For short tails, the first few points show increasing departure from the fitted line above the line and last few points show increasing departure from the fitted line below the line ( days). For long tails, this pattern is reversed ( days).

In this case, we can reasonably conclude that the normal distribution does not provide an adequate fit for this dataset, for high frequencies. To confirm this, we perform a Lilliefors Goodness-of-Fit Test.

Lilliefors tests the goodness of fit to a normal distribution. It is derivated from the Kolmogorov-Smirnof test, with the difference that it tests a composite hypothesis and not a simple hypothesis.666See Appendix B, Section “Lilliefors Goodness-of-Fit Test” The difference with the Jarque-Bera test is that this one is based on the maximum departure of the empirical distribution from the normal distribution, so this test will tend to reject the null hypothesis in the presence of kurtosis and fat tails. We perform this test for each index and each dataset. For each path, the output of the test is 0 if we do not reject the null hypothesis (viz the normal hypothesis) at a significance level , and 1 if we reject it. We give in Table 2.6 the average of the tests. For instance, for a time lag of 80 days, we perform the Lilliefors test 80 times, on 80 different log returns datasets. An average value of 0.1875 means that we rejected the null hypothesis times out of 80.

| time lag | DJIA1988 | DJIA1982 | DJIA1930 | DJIA1896 | SP1965 | FTSE1984 |

|---|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 |

| 20 | 0.4 | 0.85 | 1 | 1 | 0.8 | 0.65 |

| 40 | 0.075 | 0.725 | 1 | 1 | 0.675 | 0.425 |

| 80 | 0.025 | 0.1875 | 1 | 1 | 0.0625 | 0.1625 |

| 100 | 0 | 0.06 | 1 | 1 | 0.03 | 0.08 |

| 200 | 0.035 | 0.04 | 0.61 | 0.41 | 0.1 | 0.035 |

| 250 | 0.02 | 0.024 | 0.532 | 0.376 | 0.064 | 0.112 |

The Lilliefors test rejects the normal hypothesis for high frequencies, but not for low frequencies. Again, for large datasets, the normal hypothesis is more often rejected, even for low frequencies. We believe rejection comes from the fact that kurtosis and fat tails are due to outliers, events that are expected to happen once in a century by the Bachelier-Osborne model, but that occur far more often. Even if these events happen more often, they are still rare enough to be absent from some too small datasets, specially for low frequencies where the number of points in each dataset is very low. This issue is not investigated in this thesis, and remains to be resolved.

2.5 Conclusion

We have described in this chapter the theory underlying most of statistical models of the stock market, the Random Walk Theory. The first model to use this theory was Bachelier-Osborne model (1959), that predicts a normal distribution for log returns. Even though this model remains widely used, specially by Black and Scholes in their famous model for option pricing, the empirical data show a clear departure from normality for high frequencies ( and days): the observed distribution is leptokurtic and exhibits fat tails. For low frequencies ( and days), the normal hypothesis cannot be rejected. The conclusion is not straightforward for medium frequencies ( and days).

Since 1959, some attempts have been done to produce a better model for log returns (stable Pareto-Levy distributions [Fam65], exponentially truncated power law, etc.), a model that would particularly fit the kurtosis and fat tails of the empirical distribution. But so far, all of them suffered from strong criticisms. We investigate in next chapter a recent model, proposed by Dragulescu et al. in 2002, based on a stochastic mean-reverting process for the volatility.

Chapter 3 Dragulescu’s model

3.1 Introduction

Mainly because of kurtosis and fat tails, we have to figure out better models for stock market returns than the Gaussian. Above all, the normal distribution fails to describe the most important phenomena: draw downs and bubbles, that occur far more often than expected, as shown by the fat tails.

Hence, we have to review some hypothesis that result in the classic Gaussian model, in order to improve upon it. Many models exist that try to explain or produce fat tails. The main assumptions of the Gaussian model concern (1) the independence of log-returns and (2) the finite constant volatility. If we assume that log-returns are really independent and identically distributed, then only a non constant or non finite volatility could explain the departure from normality observed in the empirical data.

In the Gaussian hypothesis, the instantaneous volatility takes the form of , where is a finite constant and is the security price at time t. Some models, e.g. stable Paretian distributions ([Fam65]), consider the volatility as infinite and produce fat tails as in empirical data. Nevertheless, the assumption of infinite volatility does not appear to be relevant, since the volatility does not grow indefinitely with the sample size. Another innovation is to consider a finite stochastic volatility. This class of models has been introduced by Hull and White. We are studying here one of these models, proposed by A. Dragulescu and A. Yakovenko. We will reproduce their results following their methodology, make a few critical comments on the way they trim the data, and propose a methodology to test their model against the empirical distribution of log returns.

3.2 Mean-reverting stochastic volatility

This model starts from a geometric Brownian motion stochastic differential equation for the price

| (3.1) |

where is a standard Wiener

Then instead of having a constant volatility as in the Bachelier-Osborne model, the authors assume the variance obeys the following mean-reverting stochastic differential equation

| (3.4) |

| where | |

|---|---|

| is the long time mean of | |

| is the rate of relaxation to this mean | |

| is a constant parameter called the variance noise | |

| is another standard Wiener process, | |

| not necessarily correlated with |

This model for the variance has been proposed first by Cox, Ingersoll and Ross [CIR85] in an attempt to price options, known as the CIR model.

3.3 Forward Kolmogorov

The authors solve the forward Kolmogorov (also called Fokker-Planck) equation that governs the time evolution of the joint probability of having the log return and the variance for the time lag , given the initial value of the variance

| (3.5) | |||||

They introduce a Fourier transform to solve analytically this equation, and obtain the following expression for the probability distribution of centred log-returns x for a time lag t:

| (3.6) |

with

| (3.7) |

| where | |

|---|---|

| is the correlation coefficient between the two Wieners and | |

| , , and are the parameters of the model |

Eqn. 3.6 is the central result of their model. It gives, for a given time lag , the expected probability density of centred log returns x. An asymptotic analysis111See [DY] Part VI of shows that it predicts a Gaussian distribution for small values of , and exponential, time dependent tails for large values of .

To confront their model with observed log returns, they train the four parameters of the model, , , and , to fit the empirical index (DOW JONES from January 04, 1982 to December 31, 2002) by minimising the following square-mean deviation error

for all available values of log returns x, and time lag and days,

where is the empirical probability mass

In their model, the authors set the correlation coefficient to zero, since (i) their trained parameter is almost null () and (ii) they do not observe any difference, in the fitting of empirical data, between taking or . Hence, they reduce the complexity of their model.

Minimising the deviation of the log instead of the absolute difference forces the parameters to fit the fat tails instead of the middle of the distribution, where the probability mass is very high.

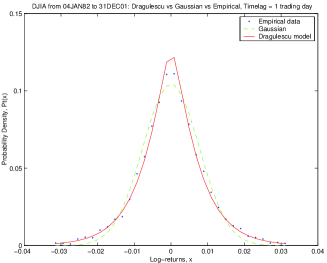

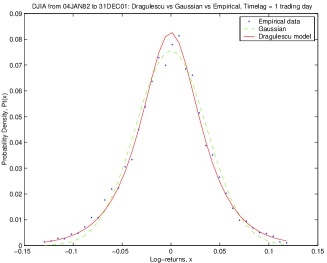

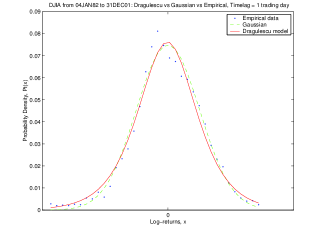

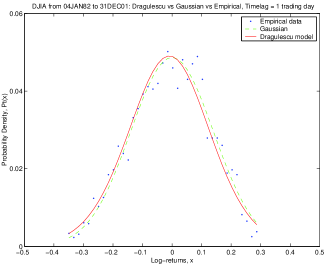

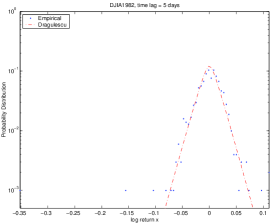

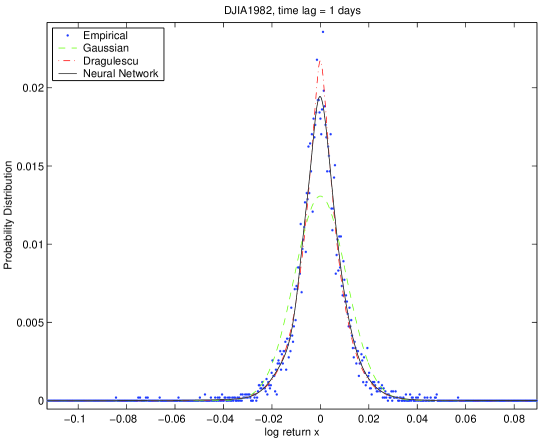

The results are shown in figure 3.1.

|

|

|

|

Apparently, their model (plain line) fits the empirical data (dots) far better than the Gaussian (dash line), specially if we look at the fat tails.

3.4 Conclusion

In his attempt to improve the classical Bachelier-Osborne model, which does not handle the kurtosis and the fat tails of the empirical probability mass, Dragulescu and Yakovenko started from a geometrical Brownian motion for the stock price , assumed a mean-reverting stochastic process for the variance , and solved analytically the forward Kolmogorov equation that governs the joint probability of this two-dimensional stochastic process. Then, by integrating over the variance, they derived the probability density of log returns for a given time lag .

Once the four parameters of the model are trained, the resulting distribution seems to fit the empirical data far better than the Normal. We explain in Chapter 4 the methodology we used to obtain these results. Then we replicate these results on different datasets (different indexes) and perform some statistical tests to measure the goodness-of-fit of this model.

Chapter 4 Experiments

4.1 Introduction

Our aim is to replicate Dragulescu and Yakovenko results and to see if they are reproducible on other datasets, with different time periods and/or different indexes. The model is supposed to fit any stock index, provided we set the value of the four parameters correctly. We will test their model itself and some assumptions such as the ergodicity of the dataset. First, we use exactly the same methodology as described in the paper, and see that strange points appear on our results. By clarifying the origin of these points directly with Dragulescu and Yakovenko, we make a few critical comments concerning the way they reuse and trim the data, and propose our own methodology based on the conservation of all the data (specially outliers, that occur during crashes and form fat tails). As a benchmark, we test this model against the classical Gaussian model and against a simple Neural Network.

4.2 Datasets

Our datasets will be, first, the Dow Jones Industrial Average (DJIA) for different time periods: the period used in Dragulescu and Yakovenko paper (from January 04, 1982 to December 31, 2001), the period after the 1987 crash (from January 04, 1988 to December 31, 2001), after the 1929 crash (from January 02, 1930 to December 31, 2001) and finally since 1896 (from May 26, 1896 to December 31, 2001) to get the largest dataset possible. Indeed, we need a very large dataset to compute distributions for important time lags such as 250 days (we take one point out of 250). Thanks to these datasets, we will test the robustness of our potential patterns according to different periods. In particular, we will focus on the impact the presence of a crash in the dataset can have on the model.

Moreover, we will use other indexes to test these patterns against other markets: the Standard and Poor’s 500 from January 04, 1965 to December 31, 2001, and the FTSE100 from January 02, 1984, to December 31, 2001.

We download the data from YAHOO ([YF]) and ECONOMY.COM ([Eco]) for the Dow Jones and Standard and Poor’s 500 and from Datastream for the FTSE100.

By “day”, we mean trading day, since all of our datasets are composed of trading days only: week-ends and bank holidays have been removed. By “time lag”, we mean the number of trading days between two points used to compute a log return. If our initial dataset is composed of 1000 close prices, then for a time lag of five days, we will take one point every five to compute the log returns. As a consequence, our final dataset will will be composed of log returns only. Nevertheless, we can begin by the first, the second, the third, the fourth or the fifth close price, so that, finally, we use five different datasets of 200 log returns. This allows us to give, for any computation, the average value and an estimate of the variance of the result, which will give more robustness to our statistical tests.

4.3 Methodology

We first describe and follow strictly the methodology proposed in their paper by Dragulescu et al., in order to reproduce their results. This methodology suffers from imperfections, specially because (i) they re-use the data and (ii) they trim the data during the pre-processing step. This leads us to propose our own methodology.

4.3.1 Reusing the data

Introduction

For a given index I at a given period, let us say the Dow Jones Industrial Average from January 04, 1982, to December 31, 2001, and a given time lag , let us say days, the raw close price dataset closePrice is composed of n close prices, here . When Dragulescu and Yakovenko compute the log returns dataset logReturns starting from closePrice, they obtain the following time series:

where

In our example, we would have

Thus, they obtain a single dataset of log returns. We believe this way of computing the log returns time series is unfair, because it “re-uses” the data. Indeed, let us assume that a crash occurs at time . Then they will take into account this specific event times exactly in their dataset in log returns .

This way to derive, from a raw close price time series of points, a single log returns time series of points, is strictly equivalent, in terms of shape parameters of the final distribution (sample mean and sample standard deviation ), to deriving 111where denotes the nearest integer less than or equal to A log returns time series composed of log returns, and averaging them into a single time series .

with

where

To put it in a nutshell, we derive m log returns time series of cardinality , called “paths”, instead of a single log return time series of cardinality . Then we average these paths to obtain a final log return time series , of cardinality . Obviously, we have:

-

•

-

•

The fact that Dragulescu and Yakovenko re-use the data is then justifiable only if all of the paths are equivalent, viz. only if we assume that the system is ergodic.222“A collection of systems forms an ergodic ensemble if the modes of behaviour found in any one system from time to time resemble its behaviour at other temporal periods and if the behaviour of any other system when chosen at random also is like the one system. We do not require identical performance, only quite similar time averages and number averages. (If you cannot tell one youth from another or one adult from another, they belong to an ergodic ensemble.) In an ergodic population, any single individual is representative of the entire population. The salient characteristics of this individual are essentially identical with any other member of the group”, [MW]

First test of ergodicity

There is a simple way to test the ergodicity of the dataset: for each time lag, we compute the sample mean and the sample standard deviation of each path . If the system is really ergodic, then we expect these shape parameters to be almost constant from one path to the other. In other words, their variance should be almost null. To compare things that are comparable, instead of giving the variance alone, we give the standard deviation (square root of the variance) of the parameter divided by its mean, which gives us a “variation rate”. Results are presented in Tables 4.1 and 4.2 for DJIA1982 and DJIA1896 respectively.

| time lag | % variation on | % variation on | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

| time lag | % variation on | % variation on | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

There is no variance, and then no variation, for a time lag of one day, since we have only one single log returns time series.

The variation rate is low for very large datasets like the Dow Jones Industrial Average from 1896 to 2001; it is always inferior to 5.5 %. However, for relatively small datasets (DJIA 1982, DJIA1988), the variation rate can reach 11.5 %, and even 17 % for DJIA1988. This comes from the fact the distribution of an average tends to be normal (CLT333See Appendix B, Section “Central Limit Theorem”) when the sample size increases, with variance decreasing proportionally to . The more points we have, the less the variation rate, whatever the initial distribution.

Second test of ergodicity

Given that this test is not conclusive, we perform a Kruskal-Wallis Test, which is a nonparametric version of the One-Way Analysis of Variance (“ANOVA”).444Se Appendix B, Section “ANOVA Test” The purpose of a one-way analysis of variance is to find out whether data from several datasets have a common mean. The assumption behind this test is that the measurements come from a continuous distribution, but not necessarily a normal distribution.555Se Appendix B, Section “Kruskal-Wallis Test” If the p-value is near zero, this casts doubt on the null hypothesis and suggests that at least one sample mean is significantly different than the other sample means.

| time lag | Chi-Square | df | p-value | ||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

| time lag | Chi-Square | df | p-value | ||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

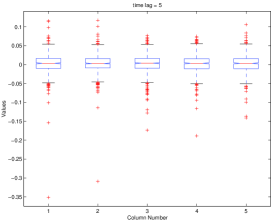

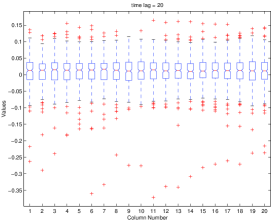

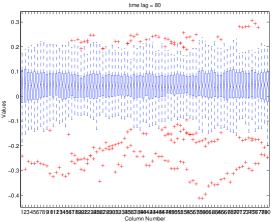

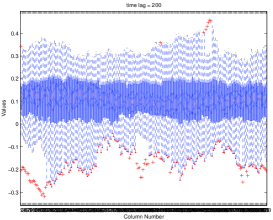

The results, presented in Tables 4.3 and 4.4, clearly demonstrate that there is no significant difference between the means of all the different paths, whatever the frequency. Indeed, the p-value is always very high. This tends to support the hypothesis that all the paths are equivalent. But if we have a look at the variance now (which is the core of Dragulescu and Yakovenko model), we see that it changes dramatically from a path to another. To show this, we plot in Figure 4.1 the Box Plot of the different paths.666Box Plots are composed of different elements: • The lower and upper lines of the “box” are the 25th and 75th percentiles of the sample • The distance between the top and bottom of the box is the interquartile range • The line in the middle of the box is the sample median. If the median is not centred in the box, that is an indication of skewness • The “whiskers” are lines extending above and below the box. They show the extent of the rest of the sample (unless there are outliers). Assuming no outliers, the maximum of the sample is the top of the upper whisker. The minimum of the sample is the bottom of the lower whisker. By default, an outlier is a value that is more than 1.5 times the interquartile range away from the top or bottom of the box • The plus sign at the top of the plot is an indication of an outlier in the data. This point may be the result of a data entry error, a poor measurement or a change in the system that generated the data

|

|

|

|

We can clearly see that the different paths are not equivalent, even if they almost have the same mean. The number of outliers for instance vary dramatically from one path to another, as indicated by the number of red crosses outside the “whiskers”. We have to indicate that this variance in the volatility of the log returns has no specific relation with the well documented “seasonal effect”, since our paths are not based on calendar days but on trading days. For instance, the five paths obtained for a 5-days time lag are not composed of log returns from Mondays to Mondays, Tuesdays to Tuesdays, etc., but on consecutive trading days. Nevertheless, in the financial literature, analysts usually use realisations (called “paths” in this thesis) that do not reuse the data, because they are interested in investment strategies on a daily, weekly, monthly, etc., basis. They do not average the paths to get a final very large dataset, as Dragulescu and Yakovenko did.

Conclusion

For technical reasons (paths are different from each other, the system is not ergodic) and practical reasons (financial analysts do not do that), we think Dragulescu and Yakovenko should not reuse the data, which is equivalent to averaging the mean and the variance of each data. As a consequence, in our subsequent tests, we will present our results without reusing the data.

4.3.2 Pre-processing the data

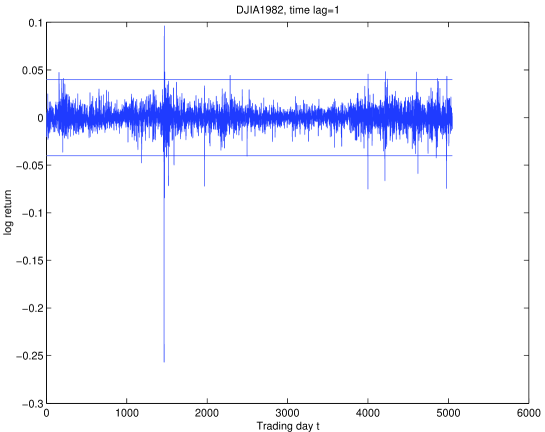

We perform all of our tests for different time lags: 1, 5, 20, 40, 80, 100, 200, and 250 days. For a given time lag and a given dataset D, we compute all of the log-return series . If the price dataset contains n points (each point is the daily close price of the index considered), then we obtain log-returns. Dragulescu and Yakovenko trimmed the log returns, rejecting any value out of the boundaries presented in Table 4.5.777This step is not mentioned in Dragulescu’s paper. Before applying this trimming method, strange points used to appear in our results. Then we contacted the authors who informed us of trimming of the log returns, using those boundaries for the Dow Jones Industrial Average from January 04, 1982, to December 31, 2001 (“DJIA1982”).

| time lag | trimming boundaries | ||||||||||||||||

|

|

We visualise in Figure 4.2 the effect of trimming the data: all of the log returns outside the boundaries, represented here by the two horizontal lines, were trimmed by the authors.

We believe this way of trimming the data is unfair, because it removes information from the dataset. Given that the model is supposed to outperform the Bachelier-Osborne model, and specially to fit the kurtosis and the fat tails, removing extreme values (that belong to the fat tails, and produce kurtosis) is counter-productive. Even the normal distribution could fit the data quite well in these conditions. To prove this, we perform the Jarque-Bera and Lillifors tests against the normal distribution, but using the trimmed data.

| time lag | DJIA1982 | DJIA1988 | DJIA1896 | DJIA 1930 | SP1965 | FTSE1984 |

|---|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 0.6 |

| 20 | 0 | 0.1 | 1 | 1 | 0.5 | 0.1 |

| 40 | 0.175 | 0.375 | 0.225 | 0.575 | 0.175 | 0 |

| 80 | 0 | 0.0125 | 0 | 0.025 | 0 | 0 |

| 100 | 0 | 0.05 | 0 | 0 | 0 | 0 |

| 200 | 0 | 0 | 0 | 0 | 0 | 0 |

| 250 | 0 | 0 | 0 | 0 | 0 | 0 |

| time lag | DJIA1982 | DJIA1988 | DJIA1896 | DJIA 1930 | SP1965 | FTSE1984 |

| 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 0.8 |

| 20 | 0.1 | 0.35 | 1 | 0.9 | 0.35 | 0.1 |

| 40 | 0.05 | 0.025 | 0.3 | 0.525 | 0.125 | 0.05 |

| 80 | 0.0375 | 0.025 | 0.075 | 0.1375 | 0 | 0 |

| 100 | 0 | 0 | 0.09 | 0.04 | 0.03 | 0.01 |

| 200 | 0.025 | 0.035 | 0.01 | 0 | 0.065 | 0.04 |

| 250 | 0.032 | 0.02 | 0.016 | 0 | 0.02 | 0.108 |

Results in Tables 4.6 and 4.7, compared with the same test on untrimmed data (Tables 2.5 and 2.6) clearly show that trimming the data, as Dragulescu and Yakovenko do, rejects the normal hypothesis only for higher frequencies. This time the tests do not reject the normal hypothesis for medium frequencies as they did without trimming.

For this reason, we decided to perform our statistical tests without trimming the data.

4.3.3 Distributions

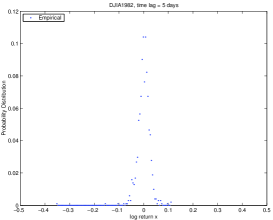

To obtain the empirical distribution, we partition the log-returns into equal sized bins of length ( ). Then we count the number of log-returns per bin, called occupation number and remove the bins for which occupation number is lower than a critical value of five. We initially choose the number of bins so that we globally remove less than one percent of the log-returns. This filtering technique is supposed to get rid of the outliers, viz. infrequent events. Thus, we obtain the frequency repartition of log-returns, also called in this paper the empirical probability density function, empPDF.

In order to exhibit fat tails and kurtosis, we fit a Gaussian to the empPDF, by estimating the sample mean and sample standard deviation of the set of log-returns . We obtain the sample mean and the sample standard deviation and plot the Gaussian normPDF.

After having observed the departure from normality, we build the new model. We train the four parameters of Dragulescu and Yakovenko model by minimising the mean-square deviation , and compute the PDF, draguPDF for different time lags.

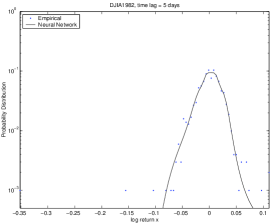

Finally, we build and train a Neural Network to fit empPDF as precisely as possible. A very simple structure is enough for this first approach. We will use this NN, nnPDF, later in our tests as a benchmark.

We can now perform goodness-of-fit tests, measures of kurtosis and measures of fat tails on different models (Gaussian, Neural Network and Dragulescu).

Empirical Distribution

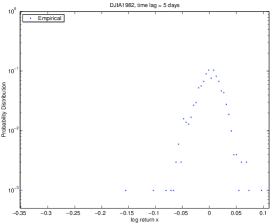

All we have to do to obtain the empirical pdf empPDF is to divide each occupation number by the bin size and the total number of observations, once bins with less than five log-returns have been removed. Then we centre the result (we subtract the sample mean to the x axis) to obtain the final probability density function empPDF. We plot in Figure 4.3 the probability mass obtained. Since the log returns are almost normal, at least according to the classical Bachelier-Osborne model, we prefer plotting the PDFs on a semi-logarithmic graph. Thus, the slopes of the probability mass should look like straight lines. This has also the advantage of focusing on the tails, since on a normal plot any discrepancy in the tails looks negligible compared to the discrepancies in the middle of the distribution, that form the kurtosis.

|

|

On the semi-log plot, a close look at the tails, specially on the left side, exhibits a series of points aligned horizontally. These events happened once, and constitute a kind of long tail. Indeed, the probability mass (or empirical probability density) is bounded, and the inferior limit is simply where an event is a specific log return in the time series. We will see that our models are all unbounded: they cannot predict those extremely isolated events. We will have to pay attention to these long tails in our tests, and not confuse them with the fat tails.

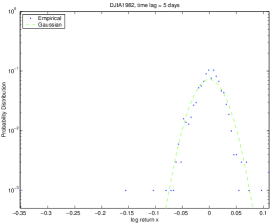

Gaussian Distribution

In order to exhibit fat tails and kurtosis, we compute the sample mean and standard deviation of the log-returns data, and generate a normal distribution normPDF with these parameters. We stress here that as we do not have any prior knowledge of the mean and variance of the Gaussian, we have to derive them from the empirical log returns. This will have an impact later in our statistical tests, since we will have to test a composite hypothesis instead of a simple hypothesis, usually easier to deal with.

The Gaussian seems to fit the empirical distribution quite well, but a simple look at the graph, even if it is often useful, cannot be used as a strong evidence. We need statistical tests to measure the goodness-of-fit of the model, as we will see later in this Chapter.

Dragulescu’s Distribution

We can now compute the distribution expected by Dragulescu’s model, draguPDF. First, we have to set the value of the four parameters of the model. To do so, we minimise the mean-square deviation between the model and the empirical data. Once we have these values, we can generate draguPDF by integrating between finite bounds the expression given in the model. Using finite instead of infinite bounds does not seem to modify the results, provided the bound is large enough.

Neural Network Distribution

Even if draguPDF is supposed to fit empPDF better than normPDF, we want to compare it with the best fit possible, the one obtained with a Neural Network. This Neural Network must be as simple as possible, but should fit the main characteristics of the empirical time series, fat tail and kurtosis. Th structure chosen was the following: it is a feed-forward back-propagation network, with a five node hidden layer and a single node output layer. The transfer functions are respectively and , where and . The back-propagation function used is , a network training function that updates the weight and bias values according to Levenberg-Marquardt optimisation. It minimises a combination of squared errors and weights and then determines the correct combination so as to produce a network which generalises well. The process is called Bayesian regularisation. This structure appears to be a good trade-off between the complexity and the goodness of fit.

We prefer not to complicate the structure, in order to have meaningful statistical tests: indeed, a model with many parameters will obviously manage to fit the data, but the goodness-of-fit will be very poor.888See Chapter 4, Section “ Statistic”

4.4 Comparison of the models

Now that we have obtained different models, we can compare them. Our aim is to verify if the Dragulescu and Yakovenko model fits the empirical data better than the classical Gaussian. The Neural Network is used as a benchmark. We perform the following tests without re-using or trimming the data.

For each dataset D and for each time lag , we obtain a set of distributions: the empirical distribution empPDF computed from the empirical log-returns, the normal distribution normPDF fitted on the empirical log-returns, Dragulescu and Yakovenko distribution fitted on empPDF and finally the neural network distribution nnPDF fitted on empPDF.

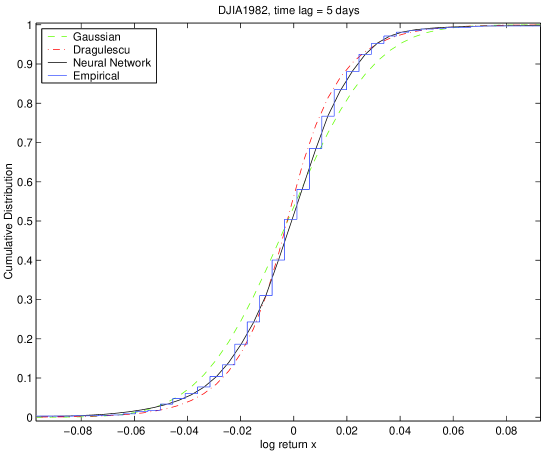

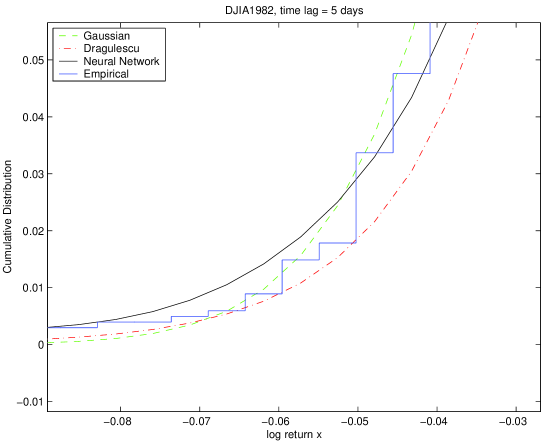

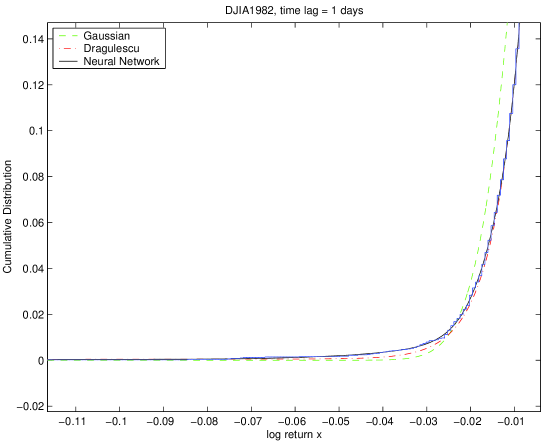

The first thing to do when comparing different models is to have a close look at the empirical and expected cumulative distributions. Even if it can be misleading sometimes, this usually gives a good overview of the possible discrepancies between the theoretical and observed data. We plot in Figure 4.7 the expected and observed cumulative distributions for the index DJIA1982 and a 5 days time lag. It seems that Dragulescu and Yakovenko curve fits the empirical distribution a bit better than the Gaussian, specially if we look at the tails in Figure 4.8. Even if it has a very simple structure, the Neural Network seems to be the best model, except in the law tail.

To test the goodness-of-fit of our models, we will first use the Kolmogorov-Smirnov Statistic. Mainly because this test poorly handles the fat tails and because it can only test a simple hypothesis, we will then perform a goodness-of-fit test on equal expected frequency bins. Finally, we will use generated random data to focus on the kurtosis of the different models and then study the outliers that compose the fat and long tails.

4.4.1 Kolmogorov-Smirnov Statistic

Introduction

Dragulescu and Yakovenko claim that their model fits the empirical data of DJIA1982 better than the Gaussian for any time lag. To check that, we use the Kolmogorov-Smirnov Statistic,999See Appendix B, Section “Kolmogorov-Smirnov Goodness-of-Fit Test” based on the maximal discrepancy between the expected and the observed cumulative distributions, for any log return x. We perform this test on the DJIA1982 index, for different time lags. This statistic is suitable for testing only a simple hypothesis, for instance a Gaussian with known and , but not a composite hypothesis (a class of Gaussians, or a Gaussian with and derivated from the tested sample dataset itself). Unfortunately, whatever the model, we always derive the parameters ( and for normPDF, , , and for draguPDF, the weights and biases for nnPDF) from the initial dataset.

By performing this test with parameters derived from the dataset, we expect the statistic to be large enough to reject the simple hypothesis, and a fortiori the composite hypothesis ([Bre75]). But if the value of is small enough to accept the simple hypothesis, it does not mean that we can accept the composite hypothesis.

Methodology

For each time lag, we compute the log returns dataset, and we divide it into paths. For each path and each model, we build the empirical cumulative density function empCDF and the expected CDF modelCDF (normCDF, draguCDF or nnCDF), and we compute the KS-statistic . We present in Tables 4.8, 4.9 and 4.10 the mean and standard deviation of over the different paths, and the associated p-value101010The p-value is the probability of observing the given sample result under the assumption that the null hypothesis (the tested model) is true. If the p-value is less than the level of significance , then you reject the null hypothesis. For example, if and the p-value is 0.03, then you reject the null hypothesis. The converse is not true. If the p-value is greater than , you have insufficient evidence to reject the null hypothesis. interval .

Results

| time lag | p-value | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

| time lag | p-value | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

| time lag | p-value | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

First, we observe an important variance, over the different paths, in the statistic : the standard deviation is not negligible in comparison with the mean . It is another evidence that the paths are not equivalent. We had observed a similar phenomenon on empirical data111111See Chapter 2, “Measure of kurtosis: Jarque-Bera Test” when computing their kurtosis. It comes from the high heterogeneity of the dataset, which makes our tests less robust. But any test performed on this heterogeneous dataset would suffer from the same issue. Even though this apparent lack of consistency prevents us from drawing any strong and global conclusion, the knowledge of the mean and standard deviation provides us with a fair overview of the statistic .

On plots, Dragulescu and Yakovenko model seems to fit the empirical cumulative distribution better than the Gaussian. But in fact, on average, both models are rejected for high frequencies (for days) at the 0.01 level of significance. Even the Neural Network is rejected for a one day time lag. This rejection of the three models may come from the fact that this test is based on the maximum discrepancy between the empirical and the theoretical cumulative distributions, for any x. To pass this test, a model must fit the observed data sufficiently well everywhere, i.e. in the tails (problem of fat tails) and in the middle (problem of high kurtosis for high frequencies) of the distribution. We will test the kurtosis and the tails of the models separately later in this Chapter.

We point out that even if Dragulescu and Yakovenko model is rejected for a one day time lag, the statistic is smaller than the Gaussian one (0.109 vs 0.131), which is an indication that the model fits the data a bit better. For other time lags, the p-value are equivalent: both models are systematically rejected for 5 days (), sometimes rejected for 20 days (, but ) and never rejected for higher frequencies (). For medium and low frequencies, the fact that the simple hypothesis is not rejected does not guarantee that the composite hypothesis can be accepted.

Conclusion

The Kolmogorov-Smirnov Goodness-of-Fit Test rejects both the Gaussian and Dragulescu and Yakovenko model for high frequencies ( days). For medium and low frequencies, we cannot conclude because of the theoretical limits of this test. To go on investigating, we need a more powerful statistical test that can be used even if the parameters of the model are derived from the tested dataset itself. The statistic is suitable in those conditions.

4.4.2 Statistic

Introduction

The Goodness-of-Git Test, based on binned data, is a powerful statistical tool to test if an empirical distribution comes from a given distribution.121212See Appendix B, Section “Chi-Square Goodness-of-Fit Test” Contrary to the Kolmogorov-Smirnov test, it is designed to evaluate a composite hypothesis, i.e. the parameters of the model can be derivated from the empirical dataset tested. This test is a good trade-off between the goodness-of-fit of a model (the better fit, the smaller the statistic) and its complexity (the more complex, the larger number of parameters ). Indeed, even if a model fits the empirical data very well, a too large complexity may penalise its p-value, so that it still can be rejected.

Finally, to be meaningful, this test must be performed using relatively large bins, and a critical value of 5 expected observations per bin is regarded as a minimum.

Methodology

If we perform this test with equal size bins, then the fats tails will be trimmed (there are less than 5 expected log returns per bin in tails) and will not participate in the value of the statistic, making the the test inaccurate. Instead, we split the log return axis into equal expected frequency bins, so that all of the log returns participate in the value of the statistic. We use an expected frequency of 5 log returns per bin.

Unfortunately, this test cannot be performed for large time lags, because of the lack of data. Indeed, in the DJIA1982 index for instance, we have initially around 5000 close prices, which means that for a time lag of 250 days, each path will have only about 20 log returns. In those conditions, because of the critical value of 5 log returns per bin, we will have finally only 4 bins, which is too small to perform a relevant test.

Results

We present our results of the Goodness-of-Fit Test in Tables 4.11, 4.12 and 4.13. The degree of freedom is given by , where is the number of parameters of the model ( for the Gaussian, for Dragulescu and Yakovenko model, and for the Neural Networks if we count the weights and the biases). For large time lags, becomes smaller and smaller because decreases, as explained above.

| time lag | df | p-value | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

| time lag | df | p-value | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

| time lag | df | p-value | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

Concerning the Neural Network, we cannot perform this test for time lags higher than 40 days, or else the degree of freedom decreases to zero. This is due to the relatively high number of parameters (). With a structure even more complicated, we could not have performed the test at all, except for high frequencies.

First we notice that the Neural Network’s statistic is slightly smaller than Dragulescu’s one, itself smaller than the Gaussian’s one, for all paths with a time lag from to days. It means that the Neural Networks fits empirical data better than Dragulescu model, which itself is better than the Gaussian. But there is a price to pay, in terms of complexity: due to too many parameters (and then a lower degree of freedom), the p-value of the Neural Networks and Dragulescu model are not systematically higher than the p-value of the Gaussian. And it is precisely the p-value that is used to accept or reject a model, not directly the statistic.

If we look at the p-value in detail, we observe that

-

•

For , the three models are rejected at a 0.05 level of significance

-

•

For , only the Neural Network is systematically accepted. The Gaussian and Dragulescu model are only accepted in the best situation ()

-

•

For , the three models are accepted and Dragulescu model is better than the Neural Network and the Gaussian

-

•

For and , Dragulescu model is still accepted, but its p-value is smaller than the one of the Gaussian

Conclusion

Thanks to the Goodness-of-Fit Test, we can assert that Dragulescu and Yakovenko model fits empirical data slightly better than the Gaussian, for high and medium frequencies. Nevertheless, both models are rejected for high frequencies ( days), at a 0.05 level of significance. In this sense, these results are consistent with the Kolmogorov-Smirnov Goodness-of-Fit Test.

We also observe a clear shift in the goodness-of-fit of the models around days: the probability of accepting the Gaussian becomes larger than the probability to accept Dragulescu model (and even the Neural Network) due to the lower complexity of the Normal model (two parameters instead of four and eleven respectively).

To put it in a nutshell, using a complex model, such as the Dragulescu model or a Neural Network, is only worth for days. For lower frequencies ( days), the Gaussian is preferable because it is simpler. Given that for these frequencies, we had observed neither fat tails nor kurtosis in the empirical datasets, the Gaussian represents the best trade-off between goodness-of-fit and complexity.

4.4.3 Measure of kurtosis

Introduction

As attested by Figures 4.7 and 4.8 and by the results of the Goodness-of-Fit Test, the Dragulescu and Yakovenko model fits their empirical data slightly better than the Gaussian, for any time lag. Nevertheless, both models are rejected for high frequencies, characterised by prominent fat tails and high kurtosis, as exposed in Section 2. Hence, we should try to find out if the models are rejected mainly because of fat tails, kurtosis, or both. First, let us have a look at the kurtosis, as it is easy to test. We will concentrate on the tails in the next Section.

Methodology

We perform our tests on the DJIA1982 index, without reusing or trimming the data. For each time lag, we compute the log returns dataset, and we divide it into paths. For each path , we start by computing the observed kurtosis, exactly as we did in Chapter 2. Then, for each model, we build the PDF (empPDF, normPDF, draguPDF or nnPDF, where empPDF is the empirical PDF), and use it to generate random data, i.e. plausible log returns time series. More precisely, we generate random datasets of elements, where is the number of log returns in the initial paths from which we derivated the model distribution. Finally, we compute the kurtosis of these time series and obtain, for each path , a mean value and a standard deviation over the simulations.

We already know that the empirical data exhibit kurtosis mainly for days, and that even for those time lags, they do not exhibit kurtosis consistently for each path131313See Chapter 2, Section “Measure of kurtosis: Jarque-Bera Test”. As a consequence, we expect a good model to produce kurtosis only when the empirical data does. For each path, we give in Tables 4.14 and 4.15 the average kurtosis , and its standard deviation , produced by the simulations.

Results

| observed | from empPDF | from normPDF | from draguPDF | from nnPDF |

|---|---|---|---|---|

| 69.27 | 22.21 20.48 | -0.01 0.07 | 107.69 16.66 | 30.55 24.9964 |

| observed | from empPDF | from normPDF | from draguPDF | from nnPDF | ||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

The variance in the kurtosis is extremely important, for observed data and for generated random data. Because the aim of this thesis is to compare a model with observed data, the analysis of the origin itself of this variance is out of our scope. Actually, we are only interested here in the capacity of different models to reproduce or not a high kurtosis, when it is exhibited by observed data.

As expected, the Gaussian never exhibits kurtosis, since by definition the kurtosis is a departure from normality. Moreover, the simulated time series generated from the empirical PDF empPDF and the Neural Network nnPDF exhibit high kurtosis in accordance with observed data, even if their kurtosis is in general smaller ( for , and for ).

To the opposite, random data generated from draguPDF exhibit a very high kurtosis for a one day time lag, even higher than expected (), as attested by the high peakedness of the distribution in Figure 4.9. Moreover, for a five day time lag, this model clearly fails to produce kurtosis, whatever the path, as shown by column (4) of Table 4.15.

This could explain why Dragulescu and Yakovenko model is rejected by both the Kolmogorov-Smirnov and the goodness-of-fit tests for high frequencies, whereas the Neural Network, for instance, is not rejected for a five day time lag.

Conclusion

Our conclusion is that the Dragulescu and Yakovenko model does not handle correctly the kurtosis: it exhibits too high kurtosis for a one day time lag, and not enough for a five day time lag. In this sens, although it is better than the Gaussian because at least, it can produce some kurtosis, this model is still rejected for high frequencies. In terms of plot, it is generated by a too large probability mass in the centre and in the tails of the distribution, which is translated by an important peakedness and by fat tails. We will focus on the fat tails in next Section.

4.4.4 Measure of the fat tails

Introduction

Fat tails are very difficult to handle, because they correspond to exceptional events, statistically not significant, but terribly important for stock markets. Indeed, they are caused by crashes and bubbles that happen far more often than predicted by the Gaussian. By trimming the data, Dragulescu and Yakovenko removed some of them, which explains why their plots look so smooth. Using equal expected frequency bins in the goodness-of-fit test was the only way to keep them. We will investigate in this Section these extreme events and try to capture them as precisely as possible.

Methodology

In 1962, E. Fama defended Mandelbrot’s stable-Paretians against the Gaussian specially because stable-Paretians could produce fat tails. He was the first to exhibit clearly those fat tails, and used a simple test (among others) to do so. The idea is to count the number of outliers, viz. the number of log returns outside , and . If the log returns really followed a normal distribution, then the number of outliers should be respectively and , where is the total number of log returns in the given path. If we compare this expected value with the real number of outliers for normPDF, then we should capture the fat tails. In Tables 4.16, 4.17 and 4.18, we indicate, for a given level of deviation () , the expected number of outliers if the log returns were normally distributed in Column (2) and the observed (regarding normPDF) number of outliers in Column (3). For instance, for a one day time lag, if the log returns followed a normal distribution, we would expect around 13.63 out of 5049 log returns outside the boundaries . We observed, however, 50 outliers (i.e. observations outside three standard deviations of normPDF). It indicates that the Gaussian dramatically underestimates the number of outliers.

Results

| time lag | expected | observed in normPDF | ||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

| time lag | expected | observed in normPDF | ||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

| time lag | expected | observed in normPDF | ||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

In Table 4.16, the real number of outliers is systematically inferior to the expected number: it means that we don’t have fat tails at a level of . In fact the tails are not fatter than expected by a Gaussian. But for high frequencies ( days), fat tails appear at a level of () and (). For medium frequencies, the expected number of outliers is inferior to one, and the real is around one or two: these log returns correspond to extremely rare events, that appear very far from the mean (more than 4 standard deviations!); we classify them as long tails.

To summarise, for high frequencies, the Gaussian exhibits fat tails outside and long tails after . Fat tails correspond to crashes (bubbles) and occur far more often than predicted, whereas long tails correspond to exceptional huge crashes (resp. huge bubbles). For medium frequencies, the Gaussian exhibits long tails at , but no fat tails. Finally, for low frequencies, the Gaussian exhibits neither fat nor long tails.

Unfortunately, the tails are not as easy to isolate statistically for the other models, Dragulescu and the Neural Network. Nevertheless, given that both these models outperform the Gaussian, we expect them to fit the tails a bit better. We can verify that by a mere observation of the plots, for instance the left tails (that corresponds to crashes) of the CDFs of the different models, in Figure 4.10.

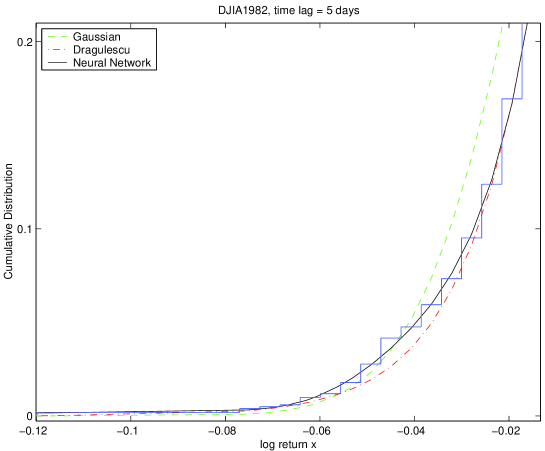

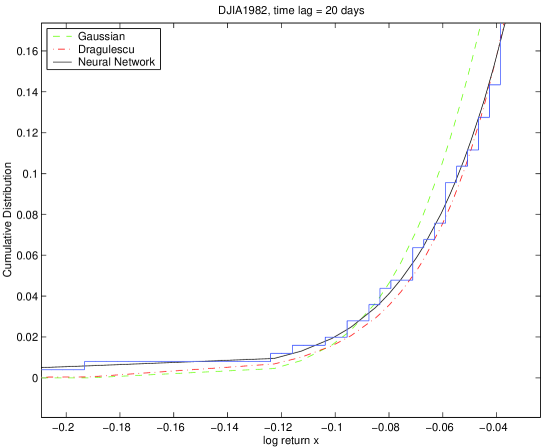

We clearly see on this plot the poor fit of the Gaussian, the slightly better fit of the Dragulescu and Yakovenko model, and the very good fit of the Neural Network. But we have to keep in mind that the complexity of those models is greater as well, which explains why the Gaussian is a still preferable for medium and low frequencies. For five days, this phenomenon still subsists, but is less prominent (4.11). Finally, by a way of comparison, we plot the same figure for medium frequencies ( days), where all of the models are accepted(4.12). We can see that gradually, the difference of fit between the Dragulescu and Yakovenko distribution and the Gaussian becomes smaller and smaller.

4.5 Conclusion