Local Search Techniques for Constrained Portfolio Selection Problems

Abstract

We consider the problem of selecting a portfolio of assets that provides the investor a suitable balance of expected return and risk. With respect to the seminal mean-variance model of Markowitz, we consider additional constraints on the cardinality of the portfolio and on the quantity of individual shares. Such constraints better capture the real-world trading system, but make the problem more difficult to be solved with exact methods.

We explore the use of local search techniques, mainly tabu search, for the portfolio selection problem. We compare and combine previous work on portfolio selection that makes use of the local search approach and we propose new algorithms that combine different neighborhood relations. In addition, we show how the use of randomization and of a simple form of adaptiveness simplifies the setting of a large number of critical parameters. Finally, we show how our techniques perform on public benchmarks.

Keywords: Portfolio optimization, Mean-Variance portfolio selection, local search, tabu search

1 Introduction

The portfolio selection problem consists in selecting a portfolio of assets (or securities) that provides the investor a given expected return and minimizes the risk. One of the main contributions on this problem is the seminal work by ? (?), who introduced the so-called mean-variance model, which takes the variance of the portfolio as the measure of risk. According to Markowitz, the portfolio selection problem can be formulated as an optimization problem over real-valued variables with a quadratic objective function and linear constraints (see [Markowitz] for an introductory presentation).

The basic Markowitz’ model has been modified in the recent literature in various directions. First, ? (?) propose a linear versions of the objective function, so as to make the problem easier to be solved using available software tools, such as the simplex method. On the other hand, with the aim of better capturing the intuitive notion of risk, ? (?) and ? (?) studied more complex objective functions, based on the notions of skewness and semi-variance, respectively. Furthermore, several new constraints have been proposed, in order to make the basic formulation more adherent to the real world trading mechanisms.

Among others, there are constraints on the maximal cardinality of the portfolio [Chang et al., Bienstock] and on the minimum size of trading lots [Mansini and Speranza]. Finally, ? (?) and ? (?) consider multi-period portfolio evolution with transaction costs.

In this paper we consider the basic objective function introduced by Markowitz, and we take into account two important additional constraints, namely the cardinality constraint and the quantity constraint, which limit the number of assets and the minimal and maximal shares of each individual asset in the portfolio, respectively.

The use of local search techniques for the portfolio selection problem has been proposed by ? (?) and ? (?). In this paper, we depart from the above two works, and we try to improve their techniques in various ways. First, we propose a broader set of possible neighborhood relations and search techniques. Second, we provide a deeper analysis on the effects of the parameter settings and employ adaptive evolution schemes for the parameters. Finally, we show how the interleaving of different neighborhood relations and different search techniques can improve the overall performances.

We test our techniques on the benchmarks proposed by ?, which come from real stock markets.

The paper is organized as follows. Section 2 introduces the portfolio selection problem and its variants. Section 3 recalls the basic concepts of local search. Section 4 illustrates our application of local search techniques to the portfolio selection problem. Section 5 show our experimental results. Section 6 discusses related work. Finally, Section 7 proposes future work and draws some conclusions.

2 Portfolio Selection Problems

We introduce the portfolio select problem in stages. In Section 2.1, we present the basic unconstrained version of Markowitz. In Section 2.2, we introduce the specific constraints of our formulation. Other constraints considered in the literature but not in this work are mentioned in Section 2.3.

2.1 Basic formulation

Given is a set of assets, . Each asset has associated a real-valued expected return (per period) , and each pair of assets has a real-valued covariance . The matrix is symmetric and each diagonal element represents the variance of asset . A positive value represents the desired expected return.

A portfolio is a set of real values such that each represents the fraction invested in the asset . The value represents the variance of the portfolio, and it is considered as the measure of the risk associated with the portfolio. Consequently, the problem is to minimize the overall variance, still ensuring the expected return . The formulation of the basic (unconstrained) problem is thus the following [Markowitz].

| (1) | |||||

| (2) | |||||

| (3) |

This is a quadratic programming problem, and nowadays it can be solved optimally using available tools111For example, an online portfolio selection solver is available at http://www-fp.mcs.anl.gov/otc/Guide/CaseStudies/port/ despite the NP-completeness of the underlying decision problem.

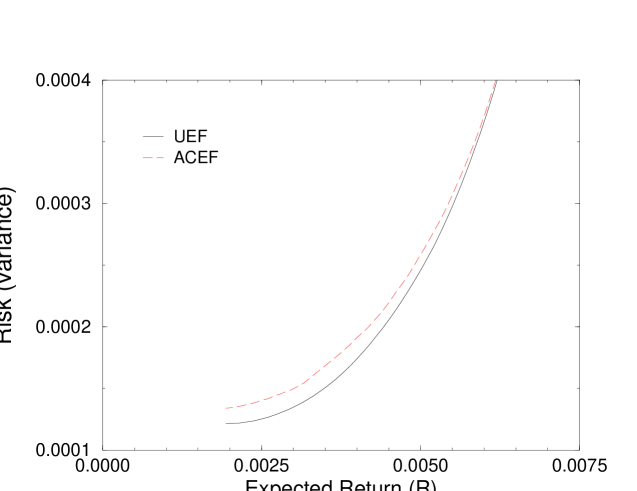

By solving the problem as a function of , we obtain the so-called unconstrained efficiency frontier (UEF), that gives for each expected return the minimum associated risk. The UEF for one of the benchmark problems of ? (?) is provided in Figure 1 (solid line).

2.2 Additional constraints

In our formulation, we consider the following two additional constraint types:

- Cardinality constraint:

-

The number of assets that compose the portfolio is limited. That is, a value is given such that the number of ’s for which is at most .

- Quantity constraints:

-

The quantity of each asset that is included in the portfolio is limited within a given interval. Specifically, a minimum and a maximum for each asset are given, and we impose that either or .

These two constraint types can be modeled by adding binary variables and the following constraints.

| (4) | |||||

| (5) | |||||

| (6) |

The variable equals to if asset is included in the portfolio, otherwise. The resulting problem is now a mixed integer programming problem, and is it much harder to be solved using conventional techniques.

We call CEF the analogous of the UEF for the constrained problem. Given that we do not solve the problem with an exact method, we do not actually compute the CEF, but what we call the ACEF (approximate constrained efficiency frontier). Figure 1 shows the ACEF (dashed line) we computed for the same instance for the values , (for ), and .

Notice that when the return is high, the distance to UEF is very small because typically large quantities of a few assets are used, and thus Constraints (4) and (5) don’t come into play.

In particular, in the instance of Figure 1 the number of assets in the ACEF is below 10 for .

2.3 Variants of the problem

In this section, we briefly discuss other variants of the portfolio selection problem and different constraint types not taken into account in this work.

- Transaction lots:

-

? (?) consider the constraint stating that assets can be traded only in indivisible lots of fixed size. In this case, the problem must be formulated in terms of integer-valued variables —as opposed to real-valued ones— that represent, for each asset, the number of purchased lots, instead of the real-valued ones.

Given that assets are normally composed by units, this constraint is certainly meaningful; its practical importance however depends on the ratio between the size of the minimum trading lots and the size of the shares involved in the portfolio.

- Linear risk:

-

? (?) propose to replace the objective function based on the variance with a linear risk function based on absolute deviation. This simplified model is easier to deal with due to the absence of the quadratic term. According to the authors, it provided results as accurate as in the basic model. The effectiveness of the linear objective function, though, has been criticized by ? (?).

- Semi-variance:

-

? (?) propose a different version of the objective function based on semi-variance rather than on variance. Semi-variance is a concept similar to variance, except that it takes into account only downward deviations rather than upward and downward ones. In fact, as Markowitz (?, Cap. 9) first noted, an objective function based on variance has the drawback that it considers very high and very low returns equally undesirable. The use of semi-variance instead tends to eliminate very low returns, without worrying about the distribution of positive returns.

- Skewness:

-

A more complex objective function is considered by Konno and coworkers [Konno et al., Konno and Suzuki], who introduce a third-order quantity called skewness. Skewness is represented by means of an matrix, and contributes to the objective function with a cubic term. The authors also propose an algorithm to solve the resulting problem.

- Multi-period optimization:

-

Most of the literature refers to a one-period trade in which the investor has initially no asset shares. In the perspective of a longer run, however the investor at each round has to decide in which assets to invest, based also on the assets that he/she already holds. ? (?) considers the case of the presence of an initial portfolio and the notion of transaction costs. The transaction costs must be subtracted from the expected return, and thus the number of atomic sell or buy operations must be taken into account.

3 Local Search

Local search is a family of general-purpose techniques for search and optimization problems. Local search techniques are non-exhaustive in the sense that they do not guarantee to find a feasible (or optimal) solution, but they search non-systematically until a specific stop criterion is satisfied.

3.1 Local Search Basics

Given an instance of a problem , we associate a search space with it. Each element corresponds to a potential solution of , and is called a state of . An element that corresponds to a solution that satisfies all constraints of is called a feasible state of . Local search relies on a function , depending on the structure of , which assigns to each its neighborhood . Each is called a neighbor of .

A local search algorithm starts from an initial state , which can be obtained with some other technique or generated randomly, and enters a loop that navigates the search space, stepping from one state to one of its neighbors . The neighborhood is usually composed by the states that are obtained by some local change (called move) from the current one.

We call the state reached after the stop condition has been met. We write to mean that is obtained from applying the move .

Local search techniques differ from each other according to the strategy they use both to select the move in each state and to stop the search. In all techniques, the search is driven by a cost function that estimates the quality of the state.

For search problems, the cost function generally accounts for the number of violated constraints, and thus the search is guided by the aim of minimizing and reaching the value for it. For optimization problems, also takes into account the objective function of the problem. We call the first state such that for all encountered in the search started in . Depending on the search technique, may or may not coincide necessarily with .

In conclusions, local search consists in defining a search space and a neighborhood relation, creating an initial state , and moving from to according to the chosen strategy.

The most common local search techniques are hill climbing (HC), simulated annealing (SA), and tabu search (TS). We describe in more details TS which is the technique that gave best results for our application.

3.2 Tabu Search

Tabu search is a modern local search technique that has been successfully applied in many real-life problems. A full description of TS is out of the scope of this paper (see, e.g., ?, ?). We now describe the formulation of the technique which has been used in this work.

At each state , TS explores exhaustively the current neighborhood . Among the elements in , the one that gives the minimum value of the cost function becomes the new current state , independently of the fact whether is less or greater than .

Such a choice allows the algorithm to escape from local minima, but creates the risk of cycling among a set of states. In order to prevent cycling, the so-called tabu list is used, which determines the forbidden moves. This list stores the most recently accepted moves. The inverses of the moves in the list are forbidden.

The simplest way to run the tabu list is as a queue of fixed size . That is, when a new move is added to the list, the oldest one is discarded. We employ a more general mechanism which assigns to each move that enters the list a random number of moves, between two values and (where and are parameters of the method), that it should be kept in the tabu list. When its tabu period is expired, a move is removed from the list. This way the size on the list is not fixed, but varies dynamically between and .

There is also a mechanism that overrides the tabu status: If a move gives a “large” improvement of the cost function, then its tabu status is dropped and the resulting state is acceptable as the new current one. More precisely, we define an aspiration function that, for each value of the objective function, returns another value for it, which represents the value that the algorithm “aspires” to reach from . Given a current state , the cost function , and a neighbor state obtained through the move , if then can be accepted as , even if is a tabu move.

The stop criterion is based on the so-called idle iterations: the search terminates when it reaches a given number of iterations elapsed from the last improvement of the current best state.

3.3 Composite local search

One of the attractive properties of the local search framework is that different techniques can be combined and alternated to give rise to complex algorithms.

In particular, we explore what we call the token-ring strategy, which is a simple mechanism for combining different local search techniques and/or different neighborhood relations. Given an initial state and a set of basic local search techniques , that we call runners, the token-ring search makes circularly a run of each , always starting from the best solution found by the previous runner (or if ).

The full token-ring run stops when it performs a fixed number of rounds without an improvement by any of the solvers, whereas the component runners stop according to their specific criteria.

The effectiveness of token-ring search for runners has been stressed by several authors (see ?, ?). In particular, when one of the two runners, say , is not used with the aim of improving the cost function, but rather for diversifying the search region, this idea falls under the name of iterated local search (see, e.g., ?, ?). In this case the run with is normally called the mutation operator or the kick move.

For example, we used the alternation of a TS using a small neighborhood with HC using a larger neighborhood for the high-school timetabling problem [Schaerf].

4 Portfolio Selection by Local Search

In order to apply local search techniques to portfolio selection we need to define the search space, the neighborhood structures, the cost function, and the selection rule for the initial state.

4.1 Search space and neighborhood relations

For representing a state, we make use of two sequences and such that and is the fraction of in the portfolio. All assets have the fraction implicitly set to . With respect to the mathematical formulation, having corresponds to setting to 1.

We enforce that the length of the sequence is such that , that the sum of equals , and that for all elements in . Therefore, all elements of the search space satisfy Constraints (2), (3), (4), and (5). Constraint (1) instead is not always satisfied and it is included in the cost function as explained below.

Given that the problem variables are continuous, the definition of the neighborhood relations refers to the notion of the step of a move , which is a real-valued parameter , with , that determines the quantity of the move. Given a step , we define the following three neighborhood relations: Other relations have been investigated, but did not provide valuable results.

- idR

-

([i]ncrease, [d]ecrease, [R]eplace):

- Description:

-

The quantity of a chosen asset is increased or decreased. All other shares are changed accordingly so as to maintain the feasibility of the portfolio. If the share of the asset falls below the minimum it is replaced by a new one.

- Attributes:

-

with , ,

- Preconditions:

-

and

- Effects:

-

If then , otherwise . All values are renormalized so as to maintain the property that ’s add up to 1. We renormalize and not to ensure that no asset rather then can fall below the minimum.

- Special cases:

-

If and , then is deleted from and is inserted with . If and , then is set to .

- Reference:

-

Revised version of ? (?).

- idID

-

([i]ncrease, [d]ecrease, [I]nsert, [D]elete):

- Description:

-

Similar to idR, except that the deleted asset is not replaced and insertions of new assets are also considered.

- Attributes:

-

with ,

- Preconditions:

-

If or then . If then .

- Effects:

-

If then ; if then ; if then is inserted into . The portfolio is repaired as explained above for idR.

- Special cases:

-

If and , then is deleted from , and it is not replaced. If and , then is set to .

- TID

-

([T]ransfer, [I]nsert, [D]elete):

- Description:

-

A part of the share is transferred from one asset to another one. The transfer can go also toward an asset not in the portfolio, which is then inserted. If one asset falls below the minimum it is deleted.

- Attributes:

-

with ,

- Preconditions:

-

- Effects:

-

The share of asset is decreased by and is increased by the same quantity. If than it is inserted in with the quantity .

- Special cases:

-

The quantity transferred is larger than in the following two cases: If after the decrease of we have that then also the remaining part of is transferred to . If and then the quantity transferred is set to .

- Reference:

-

Extended version of ? (?).

Intuitively, idR and idID increase (or decrease) the quantity of a single asset, whereas TID trasfers a given amount from one asset to another one.

Notice that idR moves never change the number of assets in the portfolio, and thus the search space is not connected under idR. Therefore, the use of idR for the solution of the problem is limited. The relation idID in fact is a variant of idR that overcomes this drawback.

Notice also that under all three relations the size of the neighborhood is not fixed, w.r.t. the size of , but it depends on the state. In particular, it depends on the number of assets that would fall below the minimum in case of a move that reduces the quantity of that asset. For example, for idR, the size is linear, , if no asset is such that , but becomes quadratic, , if all assets are in such conditions.

We now define the inverse relations, which determines which moves are tabu. Our definitions are the following: For idR and idID, the inverse of is any move with the same first asset and different arrow. For TID, it is the move with the two assets exchanged.

4.2 Cost function and initial state

Recalling that all constraints but Constraint (1) are automatically satisfied by all elements of the search space, the cost function is composed by the objective function and the degree of violation of Constraint (1). Specifically, we define two components, and , which take into account the constraint and the objective function, respectively. The overall cost function is a linear combination of them: .

In order to ensure that a feasible solution is found, is (initially) set to a much larger value than . However, during the search, is let to vary according to the so-called shifting penalty mechanism (see, e.g., ?, ?): If for consecutive iterations Constraint (1) is satisfied, is divided by a factor randomly chosen between 1.5 and 2. Conversely, if it is violated for consecutive iterations, the corresponding weight is multiplied by a random factor in the same range (where and are parameters of the algorithm).

Notice that given a state and a move the evaluation of the cost change associated to , i.e. is computationally quite expensive for both idR and idID, due to the fact that changes the fraction of all assets in . The computation of the cost is instead much cheaper for TID.

The initial state is selected as the best among random portfolios with assets. However, experiments show that the results are insensitive to .

4.3 Local search techniques

We implemented all the three basic techniques, namely HC, SA, and TS, for all neighborhood relations. HC, which performs only improving and sideways moves, is implemented both using a random move selection and searching for the best move at each iteration (steepest descent). SA, which for the sake of brevity is not described in this paper, is implemented in the “standard” way described in [Johnson et al.]. TS is implemented as described in Section 3.2 using a tabu list of variable size and the shifting penalty mechanism.

We also implemented several token-ring procedures. The main idea is to use one technique , with a large step , in conjunction with another one , with a smaller step. The technique guarantees diversification, whereas provides a “finer-grain” intensification.

The step is not kept fixed for the entire run, but it is allowed to vary according to a random distribution. Specifically, we introduce a further parameter and for each iteration the step is selected with equal distribution in the interval and .

Due to its limited exploration capabilities, idR is used only for . Other combinations, of two or three techniques, have also been tested as described in the experimental results.

4.4 Benchmarks and experimental setting

We experiment our techniques on 5 instances taken from real stock markets.222Available at the URL http://mscmga.ms.ai.ac.uk/jeb/orlib/portfolio.html We solve each instance for 100 equally distributed values for the expected return .

We set the constraint parameters exactly as ? (?): and for , and for all instances.

Given that the constraint problem has never been solved exactly, we cannot provide an absolute evaluation of our results. We measure the quality of our solutions in average percentage loss w.r.t. the UEF (available from the web site). We also refer to the ACEF, which we obtain by getting, for each point, the best solution found by the set of all runs using all techniques. The ACEF has been computed using a very large set of long runs, and reasonably provides a good approximation of the optimal solution of the constrained problem.

Table 1 illustrates, for all instances, the original market, the average variance of UEF (multiplied by for convenience), and the percentage average of the difference between ACEF and UEF.

| No. | Origin | assets | UEF | % Diff |

|---|---|---|---|---|

| 1 | Hong Kong | 31 | 1.55936 | 0.00344745 |

| 2 | Germany | 85 | 0.412213 | 2.53845 |

| 3 | UK | 89 | 0.454259 | 1.92711 |

| 4 | USA | 98 | 0.502038 | 4.69426 |

| 5 | Japan | 225 | 0.458285 | 0.204786 |

Notice that the problem for which the discrepancy between UEF and ACEF is highest is no. 4 (with 4.69%). For this reason we illustrate our results for no. 4, in which the differences are more tangible.

Except for no. 1, all other instances give qualitatively similar results and they require almost the same parameter settings. Instance no. 1 instead, whose size is considerably smaller than the others, shows peculiar behaviors and requires completely different settings. Specifically, it requires shorter tabu list and much smaller steps.

5 Experimental Results

The code is written in C++ with the compiler gcc (version 2.96), and makes use of the local search library EasyLocal++ [Di Gaspero and Schaerf]. It runs on a 300MHz Pentium II using Linux.

In the following experiments, we run 4 trials for every point. For each parameter setting, we therefore run 2000 trials (4 trials 100 points 5 instances). Except for the first point of the UEF, in one of the four trials the initial state is not random, but it is the final state of the previous solved point of the UEF. The number of iterations is chosen in such a way that each single trial takes approximately 2 seconds (on a 300MHz Pentium II, using the C++ compiler egcs-2.91.66), and therefore each test runs for approximately an hour.

We experimented with 20 different values of the step . Regarding the step variability , preliminary experiments show that the best value is , which means the step varies between and . In all the following experiments, is either set to (fixed step) or is set to (random step).

Regarding the parameters related to the shifting penalty mechanism, the experiments show that the performances are quite insensitive to their variations as far as they are in a given interval. Therefore, we set such parameters to fixed values throughout all our experiments (, ).

5.1 Single solvers

The first set of experiments regards a comparison of algorithms using the three neighborhood relations idID, idR, and TID in isolation. Given that the search space is not connected under idR, the relation idR is run for initial states of all sizes from to (it is therefore granted a much longer running time). For the other two, idID and TID, we start always with an initial state of assets.

Table 2 shows the best results for TS for both fixed and random steps, and the corresponding step values. For TS, the tabu list length is 10-25, and the maximum number of idle iterations is set to 1000.

The table shows also the best performance of HC and SA for TID and idID. For the sake of fairness, we must say that the parameter setting of SA has not been investigated enough.

The results in Table 2 show that TS works much better than the others, and TID works better than idR and idID. They also show that the randomization of the step improves the results significantly.

| Fixed Step | Random Step | ||||

|---|---|---|---|---|---|

| Tech. | Nhb | step | % Diff | base step | % Diff |

| TS | idID | 0.5 | 6.31568 | 0.4 | 5.60209 |

| TS | TID | 0.5 | 5.42842 | 0.3 | 4.85423 |

| TS | idR | 0.4 | 5.4743 | 0.4 | 5.4621 |

| SA | TID | 0.4 | 53.7006 | 0.4 | 56.5798 |

| SA | idID | 0.2 | 118.698 | 0.5 | 113.735 |

| HC | TID | 0.2 | 29.2577 | 0.2 | 29.039 |

| HC | idID | 0.2 | 41.4734 | 0.1 | 41.0438 |

5.2 Composite solvers

Table 3 shows the best results for token-ring with various combinations of two or three neighborhoods all using TS and random steps. Notice that we consider as token-ring solver also the interleaving of the same technique with different steps.

| Runner 1 | Runner 2 | Runner 3 | ||||

|---|---|---|---|---|---|---|

| Nbh | Step | Nbh | Step | Nbh | Step | % Diff |

| TID | 0.4 | TID | 0.05 | - | - | 4.70872 |

| TID | 0.4 | TID | 0.04 | TID | 0.004 | 4.70866 |

| TID | 0.4 | idR | 0.05 | - | - | 4.70804 |

| TID | 0.4 | idR | 0.05 | TID | 0.01 | 4.71221 |

| idID | 0.4 | idID | 0.04 | - | - | 5.06909 |

| idID | 0.3 | idID | 0.03 | idID | 0.003 | 4.99406 |

| idID | 0.4 | idR | 0.05 | - | - | 4.99206 |

| idID | 0.4 | idR | 0.04 | idID | 0.004 | 5.16368 |

The table shows that the best results are obtained using the combination of TID and idR, but TID with different steps performs almost as good. This results are very close to the ACEF (4.69426%), which is obtained using also much longer runs (24 hours each).

In conclusion, the best results (around 4.7%) are obtained by token ring solvers with random steps. Further experiments show that the most critical parameter is the size of the step of , which must be in the range [0.3, 0.6]. They also show that using alternation of fixed steps the best result obtained is 4.84883.

5.3 Effects of constraints on the results

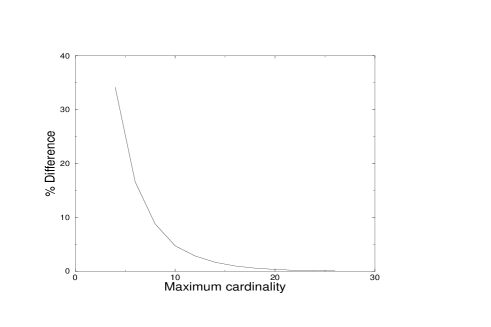

We conclude with a set of experiments that highlights the role played by constraints 4 and 5 on the problem. Figure 2 shows the best results for instance no. 4 for different values of the maximum number of assets ( and are fixed to the values and ).

The results show that the effect of the constraint decreases quite steeply when increasing . The effect is negligible for .

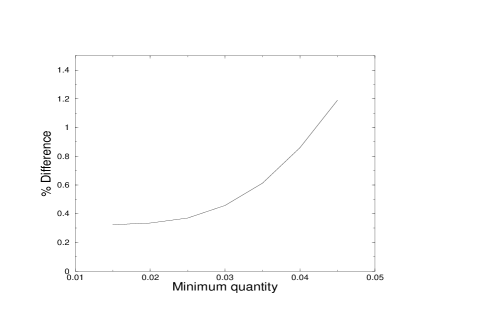

Figure 3, instead, shows how the quality of the portfolio decreases while increasing the minimum quantity (). In order to focus on the minimum quantity constraint, we use a high value for the maximum cardinality () so as to make the effect of the corresponding cardinality constraint less visible.

We don’t show the results for different values of because the constraint on maximum quantity is less important from the practical point of view.

6 Related Work

This problem has been previously considered by ? (?), who implemented three solvers based on TS, SA, and genetic algorithms (GA). Their experimental results suggest that GA and SA work better than TS. Even though the TS procedure is not completely explained in the paper, we believe that this “defeat” of TS in favor of SA and GA is due to the fact that their version of TS is not sufficiently optimized.

The neighborhood relation used by ? is a variant of idR. The difference stems from the fact that in their case a move is represented by only the pair and the replacing asset is not considered part of , but it is randomly generated whenever necessary. This definition makes incomplete the exploration of the full neighborhood because the quality of a move may depends of the randomly generated . In our work, instead, all possible replaces are analyzed. In addition, the application of a move is non-deterministic, and therefore it is not clear which is the definition of the inverse of , and the definition of the tabu mechanism. Finally, with respect to our version, their TS misses the following important features: shifting penalty mechanism, random step (they use the fixed value ), and variable-size tabu list.

Even though ? solve the same problem instances, a fair comparison between their and our results is not possible for two reasons:

First, they formulate Constraint (4) with the equality sign, i.e. , rather than as an inequality. As the authors themselves admit, constraining the solution to an exact number of assets in the portfolio is not meaningful by itself, but it is a tool to solve the inequality case. They claim that the solution of the problem with the inequality can be found solving their problem for all values from to . Unfortunately, though, they provide results only for the problem with equality.

Second, they do not solve a different instance for each value of , but (following ?, ?), they reformulate the problem without Constraint (1) and with the following objective function: . The problem is then solved for different values of . The quality of each solution is measured not based on the risk difference w.r.t. the UEF for the same return , but using a metric that takes into account the distance to both axis. The disadvantage of this approach is that they obtain the solution for a set of values for which are not an homogeneously distributed. Therefore their quality cannot be measured objectively, but it depends on how much they cluster toward the region in which the influence of Constraints (4) and (5) is less or more strong. In addition, these sets of points are not provided, and thus the results are not reproducible and not comparable.

? (?) considers the unconstrained problem therefore his results are not comparable. He introduces the TID neighborhood which turned out to be the most effective. Although, the definition of ? is different because he considers only transfers and no insertions and deletions. This is because, for the unconstrained problem, all assets can be present in the portfolio at any quantity, and therefore there is no need of inserting and deleting. The introduction of insert and delete moves is our way to adapt his (successful) idea to the constrained case.

Rolland makes use of a tabu list of fixed length equal to , thus linearly related to the number of assets. He alternates the fixed step value 0.01 with the fixed value 0.001, shifting every 100 moves. Our experiments confirm the need for two (and no more than two) step values, but they show that those values are too small for the constrained case. In addition, for the constrained problem, randomization works better than alternating two fixed values.

7 Conclusions and Future Work

We compared and combined different neighborhood relations and local search strategies to solve a version of the portfolio selection problem which involves a mixed-integer quadratic problem. Rather than exploring all techniques in the same depth, we focussed on TS that turned out to be the most promising from the beginning.

This work shows also how adaptive adjustments and randomization could help in reducing the burden of parameter setting. For example, the choice of the step parameter turned out to be particularly critical.

We solved public benchmark problems, but unfortunately no comparison with other results is possible at this stage.

In the future, we plan to adapt the current algorithms to different versions of the portfolio selection problem, both discrete and continuous, and to related problems. Possible hybridization of local search with other search paradigms, such as genetic algorithms, will also be investigated.

Acknowledgements

I thank T.-J. Chang and E. Rolland for answering all questions about their work, and K. R. Apt and M. Cadoli for comments on earlier drafts of this paper.

References

- [Bienstock] Daniel Bienstock. Computational study of a family of mixed-integer quadratic programming problems. Mathematical Programming, 74:121–140, 1996.

- [Chang et al.] T.-J. Chang, N. Meade, J. E. Beasley, and Y. M. Sharaiha. Heuristics for cardinality constrained portfolio optimisation. Computers and Operational Research, 27:1271–1302, 2000.

- [Di Gaspero and Schaerf] Luca Di Gaspero and Andrea Schaerf. EasyLocal++: An object-oriented framework for flexible design of local search algorithms. Technical Report UDMI/13/2000/RR, Dipartimento di Matematica e Informatica, Università di Udine, 2000. Available at http://www.diegm.uniud.it/~aschaerf/projects/local++.

- [Gendreau et al.] M. Gendreau, A. Hertz, and G. Laporte. A tabu search heuristic for the vehicle routing problem. Management Science, 40(10):1276–1290, 1994.

- [Glover and Laguna] Fred Glover and Manuel Laguna. Tabu search. Kluwer Academic Publishers, 1997.

- [Glover et al.] F. Glover, J. M. Mulvey, and K. Hoyland. Solving dynamic stochastic control problems in finance using tabu search with variable scaling. In I. H. Osman and J. P. Kelly, editors, Meta-Heuristics: Theory & Applications, pages 429–448. Kluwer Academic Publishers, 1996.

- [Johnson et al.] D. S. Johnson, C. R. Aragon, L. A. McGeoch, and C. Schevon. Optimization by simulated annealing: an experimental evaluation; part I, graph partitioning. Operations Research, 37(6):865–892, 1989.

- [Konno and Suzuki] Hiroshi Konno and Ken-ichi Suzuki. A mean-variance-skewness portfolio optimization model. Journal of the Operations Research Society of Japan, 38(2):173–187, 1995.

- [Konno and Yamazaki] Hiroshi Konno and Hiroaki Yamazaki. Mean-absolute deviation portfolio optimization model and its applications to Tokio stock market. Management Science, 37(5):519–531, 1991.

- [Konno et al.] Hiroshi Konno, Hiroshi Shirakawa, and Hiroaki Yamazaki. A mean-absolute deviation-skewness portfolio optimization model. Annals of Operations Research, 45:205–220, 1993.

- [Mansini and Speranza] Renata Mansini and Maria Grazia Speranza. Heuristic algorithms for the portfolio selection problem with minimum transaction lots. European Journal of Operational Research, 114:219–233, 1999.

- [Markowitz et al.] Harry Markowitz, Peter Todd, Ganlin Xu, and Yuji Yamane. Computation of mean-semivariance efficient sets by the critical line algorithm. Annals of Operations Research, 45:307–317, 1993.

- [Markowitz] Harry Markowitz. Portfolio selection. Journal of Finance, 7(1):77–91, 1952.

- [Markowitz] Harry Markowitz. Portfolio selection, efficient diversification of investments. John Wiley & Sons, 1959.

- [Perold] Andre F. Perold. Large-scale portfolio optimization. Management Science, 30(10):1143–1160, 1984.

- [Rolland] Erik Rolland. A tabu search method for constrained real-number search: applications to portfolio selection. Technical report, Dept. of accounting & management information systems. Ohio State University, Columbus. U.S.A., 1997.

- [Schaerf] Andrea Schaerf. Local search techniques for large high-school timetabling problems. IEEE Transactions on Systems, Man, and Cybernetics, 29(4):368–377, 1999.

- [Simaan] Yusif Simaan. Estimation risk in portfolio selection: the mean variance model versus the mean absolute deviation model. Management Science, 43(10):1437–1446, 1997.

- [Stützle] Thomas Stützle. Iterated local search for the quadratic assignment problem. Technical Report AIDA-99-03, FG Intellektik, TU Darmstadt, 1998.

- [Yoshimoto] Atsushi Yoshimoto. The mean-variance approach to portfolio optimization subject to transaction costs. Journal of the Operations Research Society of Japan, 39(1):99–117, 1996.