Towards Understanding the Predictability of Stock Markets from the Perspective of Computational Complexity††thanks: A preliminary version will appear in Proceedings of the 12th Annual ACM-SIAM Symposium on Discrete Algorithms, 2001.

Abstract

This paper initiates a study into the century-old issue of market predictability from the perspective of computational complexity. We develop a simple agent-based model for a stock market where the agents are traders equipped with simple trading strategies, and their trades together determine the stock prices. Computer simulations show that a basic case of this model is already capable of generating price graphs which are visually similar to the recent price movements of high tech stocks. In the general model, we prove that if there are a large number of traders but they employ a relatively small number of strategies, then there is a polynomial-time algorithm for predicting future price movements with high accuracy. On the other hand, if the number of strategies is large, market prediction becomes complete in two new computational complexity classes CPP and BCPP, where . These computational completeness results open up a novel possibility that the price graph of an actual stock could be sufficiently deterministic for various prediction goals but appear random to all polynomial-time prediction algorithms.

1 Introduction

The issue of market predictability has been debated for more than a century (see [7] for earlier papers and [17, 12, 5, 15] for more recent viewpoints). In 1900, the pioneering work “Theory of Speculation” of Louis Bachelier used Brownian motion to analyze the stochastic properties of security prices [7]. Since then, Brownian motion and its variants have become textbook tools for modeling financial assets. Relatively recently, the radically different methodology of Mandelbrot used fractals to approximate price graphs deterministically [18]. In this paper, we initiate a study into this long-running issue from the perspective of computational complexity.

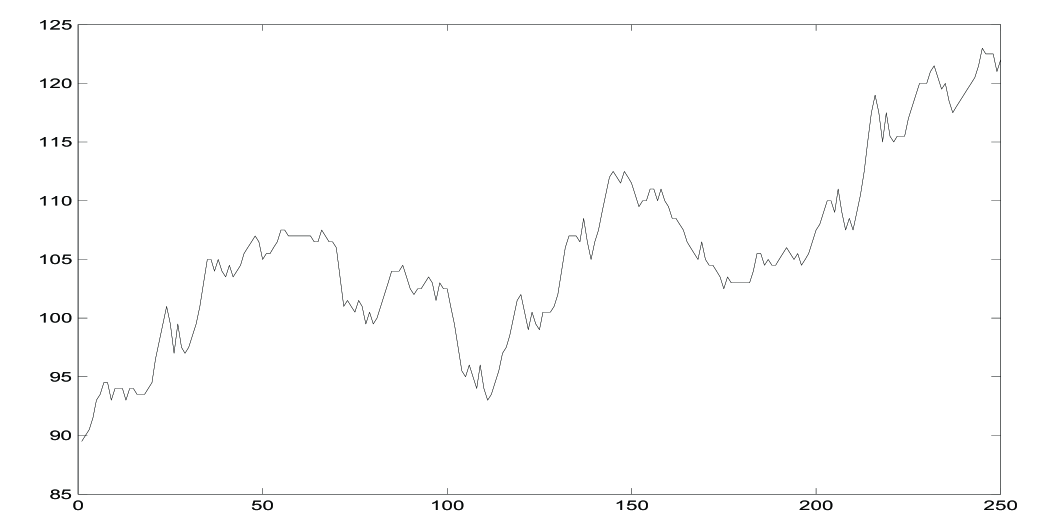

We develop a simple agent-based model for a stock market [8, 16]. The agents are traders equipped with simple trading strategies, and their trades together determine the stock prices. We first consider a basic case of this model where there are only two strategies, namely, momentum and contrarian strategies. The choice of this base model and thus our general model is justified at two levels: (1) Experimental and empirical studies in the finance literature [1, 6, 9, 10, 14, 6, 4, 11] show that a large number of traders primarily follow these two strategies. (2) Our own simulation results show that despite its simplicity, the base model is capable of generating price graphs which are visually similar to the recent price movements of high tech stocks (Figures 1 and 2).

With these justifications, we then consider the issue of market predictability in the general model. We prove that if there are a large number of traders but they employ a relatively small number of strategies, then there is a polynomial-time algorithm to predict future price movements with high accuracy (Theorem 5). On the other hand, if there are also a large number of strategies, then the problem of predicting future prices becomes computationally very hard. To describe this hardness, we define two new computational complexity classes called CPP and BCPP (Definitions 8 and 9). We show that some market prediction problems are complete for these two classes (Theorems 16 and 17) and that .

These computational completeness results open up the possibility that the price graph of an actual stock could be sufficiently deterministic for various prediction purposes but appear random to all polynomial-time prediction algorithms. This is in contrast to the most popular academic belief that the future price of a stock cannot be predicted from its historical prices because the latter are statistically random and contain no information. This new viewpoint also differs from the fractal-based methodology in that the price graph of a stock could be a fractal but the fractal might not be computable in polynomial time. The findings in this paper can by no means settle the debate on market predictability. Our goal is only that this alternative approach could provide new insights to the predictability issue in a systematic manner. In particular, it could provide a general framework to investigate the many documented technical trading rules [20] and to generate novel and significant interdisciplinary research problems for computer science and finance.

2 A Basic Market Model

In this section, we present a very simple market model, called the deterministic-switching MC (DSMC) model. The letter M stands for a momentum strategy, and the letter C for a contrarian strategy. These two strategies and the model itself are defined in Section 2.1. Some computer simulations for this model are reported in Section 2.2.

Intuitively, these strategies are heuristics (“rules of thumb”) used by traders in the absence of reliable asset valuation models. As discussed in [11], a momentum trader may observe a sequence of “up” trades (price increments) and execute a buy trade in the anticipation that she will not be one of the last buyers, knowing very well that the asset is overpriced. Similarly, she may see some “down” trades (price decrements) and then make a sell trade in the hope that there will be more sellers after her. In contrast, after detecting a number of “up” (respectively, down) trades, a contrarian trader may submit a sell (respectively, buy) trade, anticipating a price reversal.

Both experimental and empirical studies have shown that traders look at past price dynamics to form their expectations of future prices, and a large number of them primarily follow momentum or contrarian strategies [1, 6, 9, 10]. In addition, the traders may switch between these two diametrically opposite strategies. Momentum and contrarian strategies are dominant in the behavior of professional market timers as well [14]. The use of momentum and contrarian strategies sometimes signifies gambling tendencies among traders [6]. In fact, a market model with momentum and contrarian traders can also be interpreted as a market with noise traders and rational traders, where the noise traders essentially follow a momentum strategy while the rational traders attempt to exploit the noise traders by following a contrarian strategy [4, 11].

2.1 Defining the DSMC Model

In the DSMC model, there is only one stock traded in the market. The model is completely specified by three integer parameters , and a real parameter as follows.

There are traders in the market, and each trader’s strategy set consists of momentum and contrarian strategies. At the beginning of day 1 of the investment period, each trader randomly chooses her initial strategy from and an integer with equal probability, where is the maximum strategy switching period. This is the only source of randomness in the DSMC model; from this point onwards, there is no random choice.

Rule 1

(Deterministic Strategy Switching Rule) For days , there is no trading. Each trader starts trading from day using her initial strategy. Trader uses the same strategy for days and switches it at the beginning of every days.

The next rule defines the two strategies with respect to a given memory size , which is the same for all traders.

Rule 2

(Trading Rule) At the beginning of day , observe the stock prices of days . For , count the number of days when ; and the number of days when . The -day trend is defied as . Then, if respectively, , the momentum strategy buys (respectively, sells) one share of the stock at the market price determined by Rule 3 below. In contrast, the contrarian strategy sells (respectively, buys) one share of the stock.

For instance, suppose that , and investor picks her initial strategy and at the beginning of day 1. She then observes the prices of days 1, 2, 3, which are, say, . At the beginning of day 4, she issues a market order to buy one share of the stock. The orders issued by the traders on day 4 together determine the price of day 4 as specified by Rule 3. Suppose that the price of day 4 is , then investor issues another market buy order at the beginning of day 5. Since her is 2, at the beginning of day 6, she switches her strategy from to .

Rule 3

(Price Adjustment Rule) The prices for days are given. On day , let and be the total numbers of buys and sells, respectively. Then, the price on day is determined by the following equation:

where is the unit of price change.

2.2 Computer Simulation on the DSMC Model

We have conducted some computer simulations of the DSMC model to test whether it can generate realistic price graphs. Because we had to examine the graphs visually, our time constraints limited the number of these simulations to only about six hundred. For a large fraction of them, we set , , and the initial prices in the range of to . We then focused on testing the effect of memory size [19]. Two main findings are as follows:

-

•

For , the price graphs were not visually real.

- •

These two statements are based on our subjective impressions and limited simulations. To further understand the DSMC model, it would be useful to automate statistical analysis on the price graphs generated by this model and compare them with real stock prices.

3 A General Market Model

In this section, we define a market model, called the AS model, where the word AS stands for arbitrary strategies. It can be verified in a straightforward manner that the DSMC model is a special case of the AS model.

In the AS model, there is only one stock traded in the market. The model is completely specified as follows with five parameters: (1) the number of traders, (2) a unit of price change, (3) a set of strategies, (4) a price adjustment rule (Equation 1 or 2 below), and (5) a joint distribution of the population variables .

Rule 4

(Market Initialization) There are traders in the market. At the beginning of day 1 of the investment period, each trader randomly chooses her initial strategy from . Let be the number of traders who choose . Then, each is a random variable, which is the only source of randomness in the model. (Unlike the DSMC model, because the allowable generality of , the AS model does not need strategy switching.)

Different joint distributions of the variables lead to different specific models and prediction problems. In Section 4.2, we consider joint distributions that tend to Gaussian in the limit as the number of traders becomes large. In Section 4.3, we consider the case where the variables are independent, and each is or with equal probability.

Rule 5

(Trading Strategies) There is no trading on day . At the beginning of day , a trader observes the historical prices and reacts by issuing a market order to buy one share of the stock, hold (i.e., do nothing), or sell one share according her strategy. Formally, a strategy is a collection of functions , where each maps to (buy), (hold), or (sell).

The price of day is determined at the end of the day by the day’s market orders using Rule 6. Since the traders choose their strategies randomly, the sequence is a stochastic process. We write for the probability space induced by all possible sequences [13]. Then, we think of each function as a random variable on .

We distinguish between strategies that react to price movements and those that ignore them.

-

•

is an active strategy if the functions may or may not be constant functions. An active trader is one with an active strategy.

-

•

is a passive strategy if the functions all are constant functions. A passive trader is one with a passive strategy.

Rule 6

(Price Adjustment) The price is given. At the end of day , the price is determined by the day’s market orders to buy or sell from the traders. We consider two simple rules:

With the proportional increment (PI) rule,

| (1) |

where is the unit of price change. Thus we can observe directly the net difference between the number of buyers and sellers on day .

With the fixed increment (FI) rule,

| (2) |

In this case, the market moves up or down depending on whether the majority of traders are buying or selling, but the amount by which it moves is fixed at .

For notational brevity, an AS+FI model refers to an AS model with the fixed increment rule, and an AS+PI model refers to an AS model with the proportional increment rule.

In reality, the price tends to move up if there are more buy orders than sell orders; similarly, the price tends to move down if there are more sell orders than buy orders. The FI rule is meant to model the sign but not the magnitude of the slope of this correlation, while the PI rule attempts to model both. Clearly, there can be many other increment rules, which this paper leaves for future research.

4 Predicting the Market

Informally, the market prediction problem at the beginning of day is defined as follows:

-

•

The data consists of (1) the five parameters of an AS-model, i.e., , , , , and a price adjustment rule, and (2) a price history .

-

•

The goal is to predict the price by estimating the conditional probabilities , , and .

Note that is symmetric to and . Thus, from this point onwards, our discussion focuses on estimating .

From an algorithmic perspective, we sometimes assume that the price adjustment rule and the joint distribution of the variables are fixed, and that the input to the algorithm is , , a description of , and the price history. This allows different algorithms for different model families as well as side-steps the issue of how to represent the possibly very complicated joint distribution of the variables as part of the input. As for the description of , we only need for each instead of the whole , and the description of these functions can simplified by restricting their domains to consist of the price sequences consistent with the given price history.

4.1 Markets as Systems of Linear Constraints

In the AS+FI model with parameters and , a price sequence and can yield a set of linear inequalities in the population variables as follows. If the price changes on day , we have

| (3) |

If the price does not change, we have instead the equation

| (4) |

Furthermore, any assignment of the variables that satisfies either inequality is feasible with respect to the corresponding price movement on day . In both cases, is computable from the price sequence . The same statements hold for days . Therefore, given and , we can extract from and a set of linear constraints on the variables . The converse holds similarly. We formalize these two observations in Lemmas 1 and 2 below.

Lemma 1

In the AS+FI model with parameters and , given and a price sequence , there are matrices and with coefficients in , columns each, and rows in total. The rows of (respectively, ) correspond to the days when (respectively, ). Furthermore. the column vectors consistent with and are exactly those that satisfy and . The matrices and can be computed in time , where is an upper bound on the time to compute a single from over all and .

Lemma 2

In the AS+FI model with parameters and , given a system of linear inequalities , where and have coefficients in with columns each, and rows in total, there exist a set of strategies corresponding to the columns of and , and a -day price sequence with the latter days corresponding to the rows of and . Furthermore, the values of the population variables are feasible with respect to the price movement on day if and only if column vector satisfies the -th constraint in and . Also, and a description of can be computed in time.

In the AS+PI model we obtain only equations, of the form:

| (5) |

In this case there is a direct correspondence between market data and systems of linear equations. We formalize this correspondence in Lemmas 3 and 4 below.

Lemma 3

In the AS+PI model with parameters and , given and a price sequence , there is a matrix with coefficients in , columns, and rows, and a column vector of length , such that the column vectors consistent with and are exactly those that satisfy . The coefficients of and can be computed in time , where is an upper bound on the time to compute a single from over all and .

Proof: Follows immediately from Equation 5.

Lemma 4

In the AS+PI model with parameters and , given a system of linear equations , where is a matrix with coefficients in , there exist a set of strategies corresponding to the columns of , and a -day price sequence with the last days corresponding to the rows of . Furthermore, the values of the population variables are feasible with respect to the price movement on day if and only if column vector satisfies the -th constraint in . Also, and a description of can be computed in time.

Proof: Follows immediately from Equation 5.

4.2 An Easy Case for Market Prediction: Many Traders but Few Strategies

In Section 4.2.1, we show that if an AS+FI market has far more traders than strategies, then it takes polynomial time to estimate the probability that the next day’s price will rise. In Section 4.2.2, we discuss why the same analysis technique does not work for an AS+PI market.

4.2.1 Predicting an AS+FI Market

For the sake of emphasizing the dependence on , let be the probability that event occurs when there are traders in the market.

This section makes the following assumptions:

-

E1

The input to the market prediction problem is simply a price history . The output is .

-

E2

The market follows the AS+FI model.

-

E3

is fixed. The values over all are computable from the input in total time polynomial in .

-

E4

Each of the traders independently chooses a random strategy from with fixed probability , where .

The parameter is irrelevant.

Notice that the column vector is the sum of independent identically-distributed vector-valued random variables with a center at . We recenter and rescale to . Then, by the Central Limit Theorem (see, e.g., [3, Theorem 29.5]), as , converges weakly to a normal distribution centered at the -dimensional vector . In Theorem 5 below, we rely on this fact to estimate the probability that the market rises for price histories that occur with nonzero probability.

Theorem 5

Assume that . Then there is a fully polynomial-time approximation scheme for estimating from . The time complexity of the scheme is polynomial in the length of the price history, the inverse of the relative error bound , and the inverse of the failure probability .

Remark. We omit the explicit dependency of the running time in and in order to concentrate on the main point that market prediction is easy with this section’s four assumptions. The parameters and are constant under the assumptions.

Proof: We use Lemma 1 to convert the price history and the strategy set into a system of linear constraints and , with the next day’s price change determined by for some . Since the values are computable in time polynomial in , this conversion takes time polynomial in .

Then, . Since , the constraints in must be vacuous; in other words, for each with , the corresponding constraint in is . Therefore, . Furthermore, since both and are constant with respect to ,

| (6) |

So to compute the desired , we compute and as follows.

To avoid the degeneracy caused by , we work with instead of by replacing with and making related changes. Let , which is the center of . As is true for , as , the vector converges weakly to a normal distribution centered at the -dimensional point . Under the assumption that each is nonzero, the distribution of is full-dimensional (within its restricted -dimensional space), as in the limit the variance of each coordinate is nonzero conditioned on the values of the other coordinates, which implies that the smallest subspace containing the distribution must contain all axes. We can calculate the covariance matrix of directly from the , as it is equal to the covariance matrix for a single trader: on the diagonal, ; and for off-diagonal elements, . Given , has density for some constant , and we can evaluate this density in time given , which is time under our assumption that is fixed.

Let be the -th constraint of , i.e., . Let denote the constraint . Let .

We next convert the constraints of on into constraints on . First of all, notice that . So if and only if . The term may not be constant. In such a case, as , the hyper plane bounding the half space keeps moving away from the origin, which presents some technical complication. To remove this problem, we analyze the term in three cases. If , then since is the center of , as , converges to . In other words, is infeasible with probability in the limit. Then, since , such cannot exist in . Similarly, if , then and is vacuous. The interesting constraints are those for which ; in this case, by algebra, if and only if . Thus, let be the matrix formed by these constraints; can be computed in time. Then, since is constant with respect to , . Similarly, converges to (1) , (2) , or (3) for case (1) , case (2) , or case (3) , respectively.

Therefore, by Equation 6, equals for case (1) and equals for case (2). Case (3) requires further computation.

| (7) |

The numerator and denominator of the ratio in Equation 7 are both integrals of the distribution of in the limit over the bodies of possibly infinite convex polytopes. To deal with the possible infiniteness of the convex bodies and , notice that the density drops exponentially. So we can truncate the regions of integration to some finite radius around the -dimensional origin with only exponentially small loss of precision. Finally, since the distribution of in the limit is normal, by applying the Applegate-Kannan integration algorithm for log-concave distributions [2] to the numerator and denominator separately, we can approximate within the desired time complexity.

4.2.2 Remarks on Predicting an AS+PI Market

The probability estimation technique based on taking to does not appear to be applicable to the AS+PI model for the following reasons.

First of all, by Lemma 3, the input price history induces a system of linear equations . If any equation in is not equivalent to or , then .

A natural attempt to overcome this seemingly technical difficulty would be to (1) solve to choose a maximal set of independent variables and (2) evaluate in the probability space induced by this set. Still, a single constraint such as with for all and for some forces in the new probability space. This is due to the fact that is constant with respect to .

A further attempt would be to evaluate by directly working with the probability space induced by . This also does not work because we show below that the market prediction problem can be reduced to the case where taking a limit in has no effect on the distribution of the strategy counts. Suppose that we are given a market which follows the assumptions E1, E3, and E4 of Section 4.2.1 except that this market uses the PI rule and has traders. We construct a new market with any traders with the following modifications:

-

1.

The price history is extended with an extra day into , where for . Each strategy is extended into a new strategy where (1) on day , , (2) on day , always buys, and (3) on day , . Thus, .

-

2.

Add a passive strategy that always holds.

-

3.

Let for and .

Note that since , traders choose the passive strategy . Also, the new market and the new price history can accommodate any traders. Note that because of the constraint , the probability distribution of conditioned on in the new market for each is identical to the probability distribution of conditioned on in the original market with . Furthermore, . So we have obtained the desired reduction.

Consequently, we are left with a situation where the number of active strategies may be comparable to the number of traders. Such a market turns out to be very hard to predict, as shown next in Section 4.3.

4.3 A Hard Case for Market Prediction: Many Strategies

Section 4.2 shows that predicting an AS+FI market is easy (i.e., takes polynomial time) when the number of traders vastly exceeds the number of strategies. In this section, we consider the case where every trader may have a distinct strategy, and show that predicting an AS+FI or AS+PI market becomes very hard indeed.

We now define two decision-problem versions of market prediction. Both versions make the following assumption:

-

•

Each is independently either or with equal probability.

The bounded market prediction problem is:

-

•

Input: a set of passive strategies and a price history spanning days such that the probability that the market rises on day conditioned on the price history is either (1) greater than or (2) less than .

-

•

Question: Which case is it, case (1) or case (2)?

The unbounded market prediction problem is:

-

•

Input: a set of passive strategies and a price history spanning days.

-

•

Question: Is the probability that the market rises on day conditioned on the price history greater than 1/2 (without the usual term)?

The unbounded market prediction problem has less financial payoff than the bounded one due to different probability thresholds. For each of these two problems, there are in effect two versions, depending on which price increment rule is used; however, both versions turn out to be equally hard. These two problems can be analyzed by similar techniques, and our discussion below focuses on the bounded market prediction problem with a hardness theorem for the unbounded market prediction problem in Section 4.3.4.

We show in Section 4.3.1 how to construct passive strategies and price histories such that solving bounded market prediction is equivalent to estimating the probability that a Boolean circuit outputs on a random input conditioned on a second circuit outputting . In Section 4.3.2, we show that this problem is hard for and complete for a class that lies between and PP. Thus bounded market prediction is not merely NP-hard, but cannot be solved in the polynomial-time hierarchy at all unless the hierarchy collapses to a finite level.

4.3.1 Reductions from Circuits to Markets

Lemma 6 converts a circuit into a system of linear inequalities, while Lemma 7 converts a system of linear inequalities into a system of linear equations. These systems can then be converted into AS+FI and AS+PI market models using Lemmas 2 and 4, respectively.

Note that the restriction in Lemma 6 to circuits consisting of -input NOR gates is not an obstacle to representing arbitrary combinatorial circuits (with constant blow-up), as -input NOR gates are universal.

Lemma 6

For any -input Boolean circuit consisting of 2-input NOR gates, there exists a system of linear constraints in unknowns and a length column vector with the following properties:

-

1.

Both and have coefficients in that can be computed in time .

-

2.

Any - vector has a unique - extension satisfying .

-

3.

If , then if and only if .

Proof: Let represent the output of the -th NOR gate, where . Without loss of generality we assume that gate is the output gate.

The variables and are dummies to allow for a zero right-hand-side in ; our first two constraints are and .

Suppose gate has inputs and . The NOR operation is implemented by the following three linear inequalities:

The first two constraints ensure that the output is never if an input is , while the last requires that the output is if both inputs are ; the constraints are thus satisfied if and only if . Using the dummy variables, the first two constraints are written as

Let be the system obtained by combining all of these inequalities. Then for each , determines for all . The vector is chosen so that .

One might suspect that the fixed increment rule’s ability to hide the exact values of the left-hand side of each constraint is critical to disguise the inner workings of the circuit. However, by adding slack variables we can translate the inequalities into equations, allowing the use of a proportional increment rule without revealing extra information.

Lemma 7

Let be a system of linear inequalities in variables where has coefficients in . Then there is a system of linear equations in variables with the following properties:

-

1.

has coefficients in that can be computed in time .

-

2.

There is a bijection between the - solutions to and the - solutions to , such that for whenever .

Proof: For each , let be the constraint . To turn these inequalities into equations, we add slack variables to soak up any excess over , with some additional care taken to ensure that there is a unique assignment to the slack variables for each setting of the variables .

We will use the following - variables, which we think of as alternate names for through :

| Variables | Purpose | Indices | Count |

|---|---|---|---|

| original variables | n | ||

| constant | none | 1 | |

| slack variables for | |||

| slack variables for |

| Name | Equation | Purpose | Indices | Count |

|---|---|---|---|---|

| set | none | 1 | ||

| represent | ||||

| require | , |

Observe that for each , can take on any integer value between and , and that for any fixed value of , the constraints uniquely determine the values of and for all . So each constraint permits to take on precisely the same values to that does, and each uniquely determines and thus the assignment of all and .

4.3.2 Conditional Probability Complexity Classes

Suppose that we take a polynomial-time probabilistic Turing machine, fix its inputs, and use the usual Cook’s Theorem construction to turn it into a circuit whose inputs are the random bits used during its computation. Then, we can feed the resulting circuit to Lemmas 6 and 2 to obtain an AS+FI market model in which there is exactly one assignment of population variables for each set of random bits, and the price rises on the last day if and only if the output of the Turing machine is . By applying Lemma 7 to the intermediate system of linear inequalities, we can similarly convert a circuit to an AS+PI model. It follows that bounded market prediction is BPP-hard for either model. But with some cleverness, we can exploit the conditioning on past history to show that bounded market prediction is in fact much harder than this. We do so in Section 4.3.3, after a brief detour through computational complexity in this section.

We proceed to define some new counting classes based on conditional probabilities. One of these, BCPP, has the useful feature that bounded market prediction is BCPP-complete. We will use this fact to relate the complexity of bounded market prediction to more traditional complexity classes.

The usual counting classes of complexity theory (PP, BPP, R, ZPP, , etc.) are defined in terms of counting the relative numbers of accepting and rejecting states of a nondeterministic Turing machine. We will define a new family of counting classes by adding a third decision state that does not count for the purposes of determining acceptance or rejection.

A noncommittal Turing machine is a nondeterministic Turing machine with three decision states: accept, reject, and abstain. We represent a noncommittal Turing machine as a deterministic Turing machine which takes a polynomial number of random bits in addition to its input; each assignment of the random bits gives a distinct computation path. A computation path is accepting/rejecting/abstaining if it ends in an accept/reject/abstain state, respectively. We often write , , or as shorthand for the output of an accepting, rejecting, or abstaining path.

Conditional versions of the usual counting classes are obtained by carrying over their definitions from standard nondeterministic Turing machines to noncommittal Turing machines, with some care in handling the case of no accepting or rejecting paths. We can still think of these modified classes as corresponding to probabilistic machines, but now the probabilities we are interested in are conditioned on not abstaining.

Definition 8

The conditional probabilistic polynomial-time class (CPP) consists of those languages for which there exists a polynomial-time noncommittal Turing machine such that if and only if the number of accepting paths when is run with input exceeds the number of rejecting paths.

Definition 9

The bounded conditional probabilistic polynomial-time class (BCPP) consists of those languages for which there exists a constant and a polynomial-time noncommittal Turing machine such that (1) implies that a fraction of at least of the total number of accepting and rejecting paths are accepting and (2) implies that a fraction of at least of the total number of accepting and rejecting paths are rejecting.

Definition 10

The conditional randomized polynomial-time class (CR) consists of those languages for which there exists a constant and a polynomial-time noncommittal Turing machine such that (1) implies that a fraction of at least of the total number of accepting and rejecting paths are accepting, and (2) implies that there are no accepting paths.

As we show in Theorems 11 and 12, CPP and CR turn out to be the same as the unconditional classes PP and NP, respectively.

Theorem 11

.

Proof: First of all, because a PP machine is a CPP machine that happens not to have any abstaining paths. For the inverse direction, represent each abstaining path of a CPP machine by a pair consisting of one accepting and one rejecting path, and each accepting or rejecting path by two accepting or rejecting paths. Then the resulting PP machine accepts if and only if the CPP machine does.

Theorem 12

.

Proof: To show , replace each rejecting path of an NP machine with an abstaining path in a CR machine. For the inverse direction, replace each abstaining path of the CR machine with a rejecting path in the NP machine.

BCPP appears to be a more interesting class. Since it is clearly a subset of CPP, we have:

Corollary 13

.

Proof: Immediate from Theorem 11 and the definition of BCPP and CPP.

On the other hand, BCPP appears to be much stronger than the analogous non-conditional class BPP. For example, it is straightforward to show that . Use the representation of an NP-machine as a deterministic machine that takes some polynomial number of “hint” bits in addition to its input, and replace these hint bits with random bits . In addition, supply another random bits , which will be used to amplify the conditional probability of accepting paths. Now let accept if accepts; reject if rejects and ; and abstain if rejects and . Then if has any accepting path on input , has at least accepting paths and at most rejecting paths, for an exponentially large probability of accepting— since we have amplified the small number of accepting paths so that they overwhelm the few rejectors. Alternatively, if never accepts, neither does .

By repeating this sort of amplification of “good” paths, we can in fact simulate queries of an NP-oracle, as stated in the following theorem.

Theorem 14

.

Proof: Let be a deterministic implementation a machine, where and each supplies a witness for the -th oracle query. We will show that the language accepted by is in BCPP.

To simplify the presentation, we assume that each oracle query is a Boolean formula with a fixed number of variables, where is polynomial in , and that is an assignment for those variables. We assume that consists of a sequence of functions for generating oracle queries, a set of verifiers for verifying the witnesses , and a combining function that produces the output from the input and the outputs of the . Each function takes as input the input and the outputs of through . sees the output of and the input . sees the input and the outputs of through . The output of the combined machine is the output of any computation path where is chosen so that whenever such an exists. In other words, we demand that be a satisfying assignment when possible, and ignore those paths where satisfiable queries are issued but satisfying assignments are not supplied.

We will represent with a noncommittal machine , where each is a random bit-vector replacing the corresponding , and is an extra supply of random bits used to amplify the good computation paths to overwhelm the bad ones. This amplification process is a little complicated, because it is not enough to amplify paths that find good witnesses to particular queries; it may be that a bad witness for an earlier query causes some to issue a different query from the correct one. So we must amplify a path that finds a witness to query enough to overwhelm not only the exponentially many invalid witnesses to query , but also the exponentially many valid witnesses that might be returned to instances queries through based on an incorrect answer to query .

Let be the vector of outputs of . For each , we define an amplification exponent as follows:

We will write for the coefficient ; these coefficients are chosen to make Equation 8 work below.

Now let whenever for all , where is the output of through in the computation of . If for some , . The effect of the bits is to set the weight of each non-abstaining path to .

Clearly can be computed in polynomial time as long as is polynomial. The number of bits needed is the maximum value of , which is . For this to be polynomial, we need .

A good path is precisely one for which each is the correct output of the NP-oracle. A bad path is one in which one or more of the values is incorrect. We will match bad paths with good paths, and show that the weight of each good path is much larger than the total weight of all bad paths mapped to it.

Identify each path with the sequence that generates it. Let generate some bad path. Let be the first point at which is an invalid witness to a satisfiable query. Then there is a good path such that for . Furthermore, if and are the vectors of verifier outputs for and , then not only is for , but also while since the only false verifier outputs are false negatives.

The maximum value for is obtained if for ; so we have

Now

| (8) |

so . But the ratio between the weight of and its corresponding good path is then at most . Since there are only paths altogether, there are fewer than bad paths; thus, the ratio between the total weight of all bad paths mapped to and the weight of is less than . Summing over all good paths shows that the total weight of all bad paths is less than half the total weight of all good paths, so at least of all non-abstaining paths are good. It follows that, conditioned on not abstaining, accepts with probability greater than if accepts, and accepts with probability less than if rejects. Hence .

An interesting open question is where exactly BCPP lies between and PP. It is conceivable that by cleverly exploiting the power of conditioning to amplify low-probability events one could show . However, we will content ourselves with the much easier result of showing that the usual amplification technique for BPP also applies to BCPP.

Theorem 15

If , then there exists a noncommittal Turing machine such that the probability that accepts conditioned on not abstaining is at least if and at most if , where and is any function of the form for some constant .

Proof: Let membership in be computed by . Assume (the case is symmetric). Consider independent executions of with input ; call the random variables representing their outputs . Because the executions are independent, for any - vector of values . So conditioning on no abstentions, has a binomial distribution with , and Chernoff bounds imply is exponentially small in . Since is constant and we can make polynomially large in , the result follows.

4.3.3 Bounded Market Prediction Is BCPP-complete

In Section 4.3.2, we have defined the complexity class BCPP and have shown that it contains the powerful class . In this section, we show that bounded market prediction is complete for BCPP. In a sense, this result says that market prediction is a universal prediction problem: if we can predict a market, we can predict any event conditioned on past history as long as we can sample from an underlying discrete probability space whose size is at most exponential.

It also says that bounded market prediction is very hard. That is, using Theorems 15 and 14, even if the next day’s price is determined with all but an exponentially small probability, it cannot be solved in the polynomial-time hierarchy unless the hierarchy collapses to a finite level.

Theorem 16

The bounded market prediction problem is complete for BCPP, in either the AS+FI or the AS+PI model.

Proof: First we show that bounded market prediction is a member of BCPP. Given a market, construct a noncommittal Turing machine whose input is the price history and strategies, and whose random inputs supply the settings for the population variables . Let abstain if the price history is inconsistent with the input and population variables; depending on the model, this is either a matter of checking the linear inequalities produced by Lemma 1 or the equations produced by Lemma 3. Otherwise, accepts if the market rises and rejects if the market falls on the next day. The probability that accepts thus equals the probability that the market rises: either more than or less than . Since the problem is to distinguish between these two cases, solves the problem within the definition of a BCPP-machine.

In the other direction, we reduce from any BCPP-language . Suppose is accepted by some BCPP-machine . We will translate and its input into a bounded market prediction problem. First use Theorem 15 to amplify the conditional probability that accepts to either more than or less than as bounded market prediction demands. Then convert into two polynomial-size circuits, one computing

and the other computing

Without loss of generality we may assume that and are built from NOR gates. Applying Lemma 6 to each yields two sets of constraints and and column vectors and such that if and only if and if and only if , where satisfies the previous linear constraints and is the initial prefix of consisting of variables not introduced by the construction of Lemma 6. We also have from Lemma 6 that there is a one-to-one correspondence between assignments of and assignments of satisfying the constraints, so probabilities are not affected by this transformation.

Now use Lemma 2 to construct a market model in which , , and are enforced by the strategies and price history, and determines the price change on the next day of trading. Thus the consistent settings of the variables are precisely those corresponding to settings of for which , or, in other words, those yielding computation paths that do not abstain. The market rises when , or when accepts. So if we can predict whether the market rises or falls with conditional probability at least , we can predict the likely output of . It follows that bounded market prediction for the AS+FI model is BCPP-hard.

To show the similar result for the AS+PI model, use Lemma 7 to convert the constraints , into a system of linear equations , and then proceed as before, using Lemma 4 to convert this system to a price history and letting determine the price change (and thus the sign of the price change) on the next day of trading.

4.3.4 Unbounded Market Prediction is CPP-complete

The unbounded market prediction problem seems harder because the probability threshold in question is with no bound in contrast to the thresholds and for the bounded market prediction problem. The following theorem reflects this intuition. However, since we do not know whether BCPP is distinct from PP, we do not know whether unbounded prediction is strictly harder.

Theorem 17

The unbounded market prediction problem is complete for , in either the AS+FI or the AS+PI model.

Proof: Similar to the proof of Theorem 16.

5 Future Research Directions

There are many problems left open in this paper. Below we briefly discuss some general directions for further research.

We have reported a number of simulation and theoretical results for the AS model. As for empirical analysis, it would be of interest to fit actual market data to the model. We can then use the estimated parameters to (1) test whether the model has any predicative power and (2) test the effectiveness of new or known trading algorithms. This direction may require carefully choosing “realistic” strategies for . Besides the momentum and contrarian strategies, there are some popular ones which are worth considering, such as those based on support levels. Investment newsletters could be a useful source of such strategies.

The AS model is an idealized one. We have chosen such simplicity as a matter of research methodology. It is relatively easy to design highly complicated models which can generate very complex market behavior. A more challenging and interesting task is to design the simplest possible model which can generate the desired market characteristics. For instance, a significant research direction would be to find the simplest model in which market prediction is computationally hard. On the other hand, it would be of great interest to find the most general models in which market prediction takes only polynomial time. For this goal, we can consider injecting more realism into the model by introducing resource-bounded learning (the generality of is equivalent to unbounded learning), variable memory size, transaction costs, buying power, limit orders, short sell, options, etc.

Acknowledgments

This work originated with David Fischer’s senior project in 1999, advised by Ming-Yang Kao. David would like to thank his father and role model, Professor Michael Fischer, for teaching, mentoring, and inspiring him throughout college.

References

- [1] P. B. Andreassen and S. Krause. Judgemental extrapolation and the salience of change. Journal of Forecasting, 9(4):347–372, 1990.

- [2] D. Applegate and R. Kannan. Sampling and integration of near log-concave functions. In Proceedings of the 23rd Annual ACM Symposium on Theory of Computing, pages 156–163, 1991.

- [3] P. Billingsley. Probability and Measure. John Wiley and Sons, second edition, 1986.

- [4] F. Black. Noise. Journal of Finance, 41(3):529–543, 1986.

- [5] J. Y. Campbell, A. W. Lo, and A. C. MacKinlay. The Econometrics of Financial Markets. Princeton University Press, Princeton, NJ, 1997.

- [6] R. G. Clarke and M. Statman. Bullish or bearish? Financial Analysts Journal, May/June:63–72, 1998.

- [7] P. A. Cootner. The Random Character of Stock Market Prices. MIT Press, Cambridge, MA, 1964.

- [8] R. H. Day and W. H. Huang. Bulls, bears, and market sheep. Journal of Economic Behavior and Organization, 14:299–330, 1990.

- [9] W. DeBondt. What do economists know about the stock market? Journal of Portfolio Management, Winter:84–91, 1991.

- [10] W. DeBondt. Betting on trends: Intuitive forecasts of financial risk and return. International Journal of Forecasting, 9:355–371, 1993.

- [11] J. B. DeLong, A. Shleifer, L. H. Summers, and R. J. Waldmann. Noise trader risk in financial markets. Journal of Political Economy, 98(4):703–738, 1990.

- [12] E. Fama. Effieicnt capital markets: II. Journal of Finance, 46:1575–1618, 1991.

- [13] I. Karatzas and S. E. Shreve. Methods of Mathematical Finance, volume 39 of Applications of Mathematics. Springer Verlag, New York, NY, 1998.

- [14] A. Kumar. Behavior of momentum following and contrarian market timers. Working Paper 99-01, International Center for Finance, School of Management, Yale University, Jan. 1999.

- [15] A. W. Lo and A. C. MacKinlay. A Non-Random Walk Down the Wall Street. Princeton University Press, Princeton, NJ, 1999.

- [16] T. Lux. The socio-economic dynamics of speculative markets: Interacting agents, chaos, and the fat tails of return distributions. Journal of Economic Behavior and Organization, 33:143–165, 1998.

- [17] B. G. Malkiel. A Random Walk down Wall Street. Norton, New York, NY, 1990.

- [18] B. B. Mandelbrot. Fractals and scaling in finance. Springer-Verlag, New York, 1997. Discontinuity, concentration, risk, Selecta Volume E, with a foreword by R. E. Gomory.

- [19] S. Mullainathan. A memory based model of bounded rationality. Working paper, Department of Economics, MIT, Apr. 1998.

- [20] R. Sullivan, A. Timmermann, and H. White. Data-snooping, technical trading rules and the bootstrap. Journal of Finance, 54:1647–1692, 1999.