Apparent multifractality

in financial time series

http://www.science-finance.fr

∗ Service de Physique de l’État Condensé, Centre d’études de Saclay,

Orme des Merisiers, 91191 Gif-sur-Yvette cedex, FRANCE

)

Abstract

We present a exactly soluble model for financial time series that mimics the long range volatility correlations known to be present in financial data. Although our model is ‘monofractal’ by construction, it shows apparent multiscaling as a result of a slow crossover phenomenon on finite time scales. Our results suggest that it might be hard to distinguish apparent and true multifractal behavior in financial data. Our model also leads to a new family of stable laws for sums of correlated random variables.

Many time series exhibit interesting scaling properties. This means that if denotes the time series, the probability distribution of the variations , rescaled by a lag-dependent factor , can be written as:

| (1) |

where is a time independent scaling function. For example, if is constructed by summing independent identically distributed random variables with finite variance, one has and for large . Note that often the ‘time’ is actually a space coordinate, as it is the case in the analysis of turbulent velocity fields (where is the fluid velocity) [1], or fracture surfaces (where is the height of the profile) [2]. Equation (1) implies that all moments of that are finite, scale similarly:

| (2) |

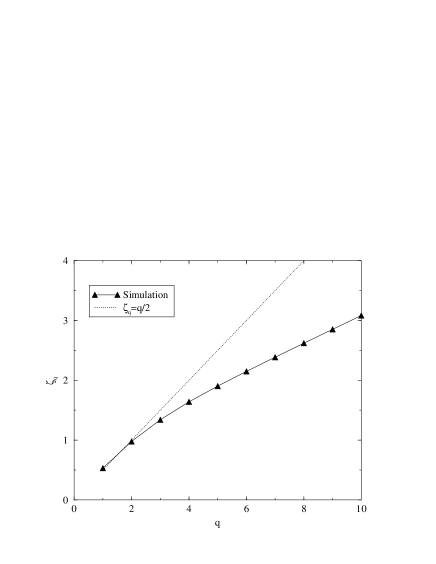

where is a q-dependent number. Very often, behaves as a simple power-law: . In this case of a monofractal process, one therefore has, , with .

This is however not the only possibility, and in some cases, one can observe multifractal scaling, in the sense that , with . Such a possibility has been advocated for turbulent velocity fields [3, 4, 5, 6] and, more recently, for financial time series [7, 8, 9, 10]. In the case of turbulence, there is strong theoretical evidence in favor of such a multifractal behavior [1, 4]. One can actually analytically derive a non trivial function within a simple (‘passive scalar’) model, which is thought to retain some essential features of real turbulence [11]. The situation is much less clear in the case of financial markets, where the only evidence is based on the empirical analysis of the moments of several time series (typically currencies or stock indices). The idea of multiplicative cascades, which is at the heart of the arguments in favor of multiscaling in turbulence, is not easily applicable to price time series (see, however, [12]).

In this note, we study to which extent empirical studies on multiscaling behavior in finance are sensitive to crossover behavior that results in apparent multiscaling, even though the studied process is a monofractal. To that end we present a soluble model that is based on the study of financial time series. In the model, the ‘volatility’ (or the variance) of the elementary price increments is a random variable with long range correlations, which have been shown to be present in financial time series [12, 13, 14, 15, 16]. The model is an exact monofractal, but nevertheless it leads to an apparent multiscaling behavior [17, 18]. As we argue below, one finds effective exponents due to a very long crossover effect, which leads to a systematic negative correction to the true asymptotic behavior . The correction grows with and results thereby in a nontrivial functional form of . The numerical simulation of such a model, which mimics quite well the observed behavior of real prices, accurately reproduces the published data in favor of multiscaling in financial markets.

The model that we propose is also interesting in its own right. As a function of the strength of the correlations, we find a transition between a simple Gaussian behavior for the scaling function (together with the usual scaling for ) for weak correlations, to a new family of stable laws (with a non trivial scaling of ) for strong enough correlations. This adds to the very few cases where the limit distribution for sums of correlated random variables is exactly known.

Our model is the following: we consider that the time series is built by summing random variables:

| (3) |

where is a microscopic time scale. The elementary increments are assumed to be given by the product of two independent random variables, a ‘sign’ and an amplitude : . The are furthermore assumed to be independent Gaussian random variables of variance unity. therefore is the (random) variance of the elementary increments. We choose the ’s to be Gaussian random variables of zero mean [19], with a correlation function given by . All moments of are therefore finite, and the even ones given by .

The correlation function will be chosen to be a power law for large arguments: . From several studies of financial markets, one knows that the variance of the price increments is indeed also random, with a very slowly decaying time correlation function:

| (4) |

where the exponent is found to be on the order of – for different markets [13, 14, 15, 16, 12]. The important point here is that .

More precisely, we will use the following explicit representation of the ’s:

| (5) |

where the ’s are independent complex Gaussian variables of unit variance. In the large limit, the resulting correlation function is well defined and decays, for large , as a power-law with while tends to [20].

We now turn to the calculation of the cumulants of of , as given by Eq. (3). We will show that these cumulants scale anomalously with as soon as (for ).

After making a gauge transform , one finds [21]:

The Gaussian integrals can be easily performed, and leads to the following expression for the characteristic function :

| (7) |

where the bold characters is used for matrices, and where are the eigenvalues of the matrix . From the very construction of the ’s, one finds that , each of which is twofold degenerate.

Expanding in powers of leads to the cumulants of . All odd order cumulants are zero, while even order cumulants are given by:

| (8) |

Let us first analyze the case . In the large limit, the sum over is convergent when and leads to cumulants which do not scale as :

| (9) |

while for one finds exactly . The normalized cumulants therefore behave as for and vanish for . This means that the distribution of indeed tends to a Gaussian for large . However, the approach to the Gaussian is slower than for sums of independent random variables. In particular, the kurtosis of decays anomalously, as , for . For larger values of (i.e. when the volatility correlations are weaker), one recovers the usual scaling of the kurtosis as that holds for independent increments. Such an anomalous decay of the kurtosis with time was first reported for financial time series in [18, 15].

The important outcome of the above calculation is that the moments of the distribution are not simple power-laws, but sums of power laws with similar exponents. For example:

| (10) |

| (11) |

where the ’s are some coefficients. If is small, these sums of power-laws can be fitted on many decades with an effective exponent such that . The exponent is less than , and more and more so as increases. However, the true asymptotic behavior predicted by our model is . In fact, Eqs. (10) and (11) show that our model (and possibly also real financial data) is better characterized by the cumulants than by the moments.

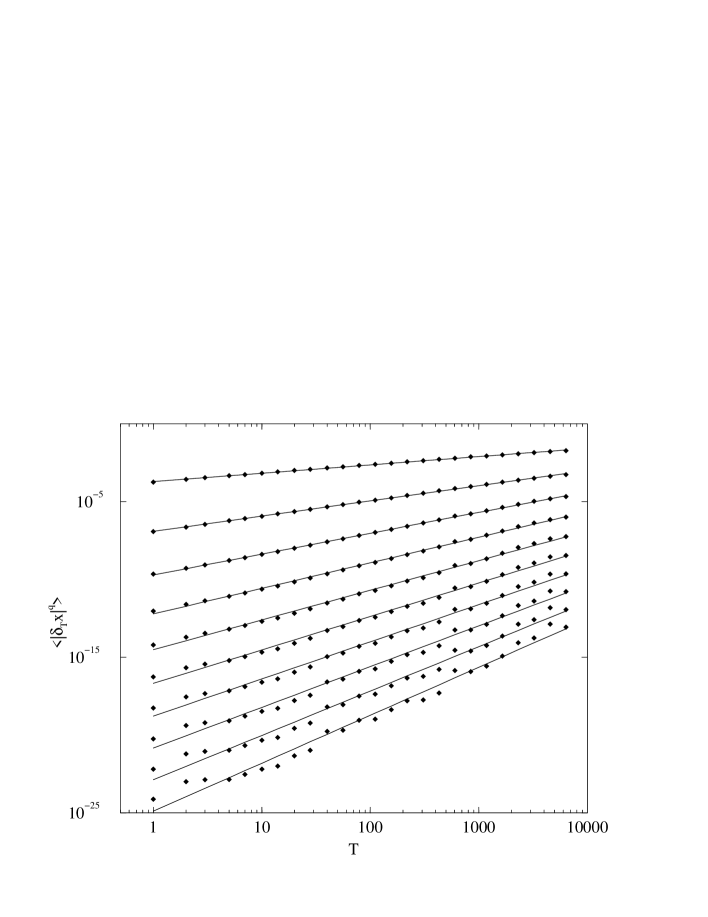

In order to illustrate this point numerically, we have generated a surrogate time series in a way closely related to the above model. Instead of writing , we have chosen to take . This leads to a more realistic time series as compared with real data from financial markets, without changing the crucial feature of the above model, i.e. the very slow decay of the volatility correlations. In particular, the distribution of the volatility has a positively skewed, log-normal shape. The length of our surrogate time series was taken to be comparable to those analyzed previously. The moments are plotted as a function of for different , for the choice (see Fig. 1). The interval of was chosen to be , again comparable to the region investigated in previous studies [7, 8, 9, 10]. The power law fits are extremely good, and lead to a function bending downwards as increases, shown in Fig. 2. For our choice of parameters, the numerical values of actually match precisely those reported in [10]. We have also checked that the same model, but without volatility correlations, leads very precisely to .

We now turn to the case . This corresponds to a non stationary process for the volatility, which typically grows with as . More precisely, from Eq. (5), one can show that . In this case, after changing variables to and , one finds that the asymptotic distribution of has a characteristic function given by:

| (12) |

(we have set , which amounts to a change of scale in .).

The above result means that after rescaling by a factor , the sum of (strongly) correlated random variables converges to a non-Gaussian distribution , obtained as the Fourier transform of the exponential of given by Eq. (12). Since the expansion of is regular for , all the moments of are finite. From the leading singularity of around , one obtains the asymptotic behavior of for large arguments as:

| (13) |

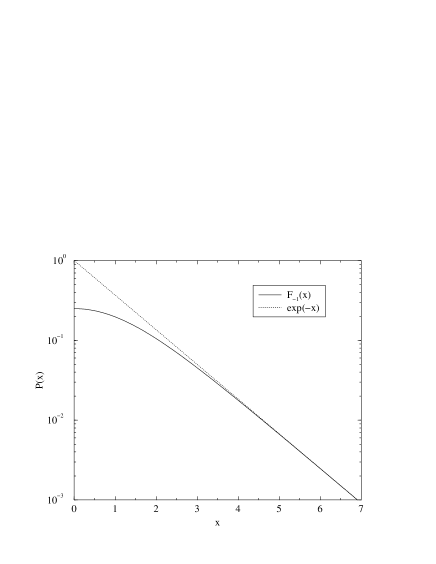

In the special case where , corresponding to a ‘volatility random walk’, the sum in (12) can be explicitly performed, and leads to:

| (14) |

This distribution is shown in Fig. 3, together with the predicted asymptotic behavior (dotted line). The kurtosis of this distribution is equal to . Interestingly, has a shape similar to hyperbolic distributions [22] with exponential tails which have been proposed in a financial context (see [18]). The appearance of such laws might thus be related to the existence of long-ranged correlations in the volatility.

In summary, the purpose of this paper was to show, on an exactly soluble ‘stochastic volatility’ model, that an apparent multiscaling behavior can appear as a result of very long transient effects, induced by the long range nature of the volatility correlations. This model is inspired by real price time series, and leads to an effective exponent spectrum in close correspondence that reported in recent papers on the subject. We therefore suspect that indications of mutlifractal behavior found in financial data might be misleading, as they could be caused by crossover effects that do not correspond to the true asymptotic behavior. To check more carefully for crossover effects, it might be helpful to analyze not only the moments but also the cumulants in empirical studies. We also have, en passant, found a new family of stable laws for sums of correlated random variables in the case where the volatility correlation is growing with time. It would be very interesting to characterize the attraction basin of these new stable laws.

Acknowledgements

We thank M. E. Brachet, P. Cizeau, L. Laloux and A. Matacz for enlightening discussions.

References

- [1] U. Frisch, Turbulence: The Legacy of A. Kolmogorov, Cambridge University Press (1997).

- [2] E. Bouchaud, J. Phys Cond. Mat. 9 4319 (1997)

- [3] B. Mandelbrot, J. Fluid. Mech. 62 331 (1974)

- [4] U. Frisch, P.L. Sulem, M. Nelkin, J. Fluid. Mech. 87, 719 (1978), U. Frisch, G. Parisi, in Turbulence and Predictability, M. Ghil, R. Benzi, G. Parisi (Edts.), North Holland (1985), p. 84.

- [5] For experimental studies, see: B. Castaing, Y. Gagne, E. Hopfinger, Physica D 46 177 (1990); R. Benzi, S. Ciliberto, C. Baudet, R. Tripiccione, F. Massaioli, S. Succi, Phys. Rev. E 48 R 29 (1993); F. Argoul, A. Arnéodo, G. Grasseau, Y. Gagne, E. Hopfinger, U. Frisch, Nature 338 52 (1989); A. Arnéodo, E. Bacry, J.-F. Muzy, Physica A 213 232 (1995) and refs. therein.

- [6] J.M. Tchéou, M.E. Brachet, F. Belin, P. Tabeling, H. Willaime, Physica D 129, (1999) 93-114

- [7] S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, Y. Dodge, Nature 381 767 (1996)

- [8] A. Fisher, L. Calvet, B.B. Mandelbrot, ‘Multifractality of DEM/$ rates’, Cowles Foundation Discussion Paper 1165; B.B. Mandelbrot, Fractals and Scaling in Finance, Springer (1997); B.B. Mandelbrot, Scientific American, Feb. (1999).

- [9] F. Schmitt, D. Schertzer, S. Lovejoy, ‘Turbulent fluctuations in Financial Markets: A multifractal approach’, preprint (1998).

- [10] M.-E. Brachet, E. Taflin, J.M. Tchéou, ‘Scaling transformation and probability distributions for financial time series’, e-print cond-mat/9905169

- [11] M. Chertkov, G. Falkovich, V. Lebedev, Phys. Rev. Lett. 76 3707 (1996) and refs. therein.

- [12] A. Arnéodo, J.-F. Muzy, D. Sornette, E.P.J. B 2, 277 (1998)

- [13] M. M. Dacorogna, U. A. Müller, R. J. Nagler, R. B. Olsen and O. V. Pictet, J. Inter. Money and Finance 12, 413 (1993); D. M. Guillaume, M. M. Dacorogna, R. D. Davé, U. A. Müller, R. B. Olsen and O. V. Pictet, Finance and Stochastics , 1 95 (1997).

- [14] Z. Ding, C. W. J. Granger and R. F. Engle, J. Empirical Finance 1, 83 (1993).

- [15] R. Cont, M. Potters, J.-P. Bouchaud, “Scaling in stock market data: stable laws and beyond” in Scale invariance and beyond, B. Dubrulle, F. Graner, D. Sornette (Edts.), EDP Sciences (1997); M. Potters, R. Cont, J.-P. Bouchaud, Europhys. Lett. 41, 239 (1998).

- [16] Y. Liu, P. Cizeau, M. Meyer, C.-K. Peng, H. E. Stanley, Physica A245 437 (1997), P. Cizeau, Y. Liu, M. Meyer, C.-K. Peng, H. E. Stanley, Physica A245 441 (1997).

- [17] J.-P. Bouchaud, Physica A 263 415 (1999)

- [18] J.-P. Bouchaud and M. Potters, Theory of Financial Risk, (Aléa-Saclay, Eyrolles, Paris, 1997), available at http://www.science-finance.fr

- [19] One could also choose a non zero mean value for and not take the absolute value. This would still lead to an soluble model.

- [20] The (time-domain) correlation function defined by this construction explicitly depends on the number of variables in the sum . This is not a problem when , since when is large, this correlation function is equal to a well-defined -independent limit plus sub-leading correction which can be safely neglected. Therefore, any subpart of the series of size such that will behave, as a function of , as the whole sum.

- [21] We could have considered the case where the can take two values . The model considered would then be tantamount to the Ising model in one dimension with long-ranged correlations.

- [22] E. Eberlein, U. Keller, Bernoulli, 1, 281 (1995). Hyperbolic distributions are such that , which interpolate between a Gaussian and a symmetric exponential.