Abstract

We introduce a simple stochastic dynamics for game theory. It assumes “local” rationality in the sense that any player climbs the gradient of his utility function in the presence of a stochastic force which represents deviation from rationality in the form of a “heat bath”. We focus on particular games of a large number of players with a global interaction which is typical of economic systems. The stable states of this dynamics coincide with the Nash equilibria of game theory. We study the gaussian fluctuations around these equilibria and establish that fluctuations around competitive equilibria increase with the number of players. In other words, competitive equilibria are characterized by very broad and uneven distributions among players. We also develop a small noise expansion which allows to compute a “free energy” functional. In particular we discuss the problem of equilibrium selection when more than one equilibrium state is present.

1 Introduction

The economic world is a complex many-body dynamical system whose fluctuation phenomena has recently attracted much attention in the physicists community [1, 2, 3, 4, 5]. The identification, in economics and finance, of phenomena (such as scaling and multiscaling) which also occur in physical systems (such as critical phase transitions and turbulence) suggests that some of the knowledge and techniques developed in physics to understand fluctuation phenomena, might also be useful to understand fluctuations in economics and finance.

Fluctuation phenomena in physics depend on the nature of the equilibrium state. The starting point to understand fluctuations in economics is then a theory for economic equilibria. Game Theory[6] is the natural candidate: it describes the interaction among players’ strategies and, assuming rationality, it identifies the possible game equilibria, named after Nash[7].

It is important to stress at this point that we shall deal mainly with economics and not with finance. Finance is, loosely speaking, a dynamical system out of equilibrium, where players gamble (speculate) on future market’s fluctuations (see ref. [5] for a model). In an economic system, instead, the assumption of rational behavior is more realistic. However perfect rationality is utopistic in real life. Deviations from rationality, which can arise from human errors, from limited or incomplete information or from random events, are practically unavoidable. Put differently one can say that, in real life, reducing human errors or the impact of random events costs time and money. Infinite precision is impossible if not at infinite costs. The analysis of the effects of “irrationality” becomes then an important issue to understand how game theoretical predictions can be modified in realistic situations.

We shall address this issue for a “thermodynamic” economic system: a system with many degrees of freedom (players). The random events discussed above have then the same qualitative nature of thermal fluctuations in statistical mechanics. One can indeed think that, in a thermodynamic system, each degree of freedom pursues the minimization of the (global) energy in the presence of random shocks due to thermal fluctuations. In the same manner we shall assume that in a macro-economic system, each agent pursues the maximization of his utility, under the effect of random shocks. In this perspective, Nash equilibria become analogs of ground states in statistical mechanics and deviations from rationality can be introduced in exactly the same way as temperature is introduced in statistical mechanics. In particular, there are several dynamical ways, depending on the nature of the problem, to model temperature in statistical mechanics. This leads us to a natural definition of stochastic dynamics in game theory.

In this work, which is an extension of a previous paper [8], we shall follow these lines, using the Langevin approach. We shall address the issue of fluctuations around Nash equilibria and the effects of deviations from rationality in some specific games with a large number of players. We shall focus on games where each of the players can control a continuous variable or “strategy” . He is endowed of a utility function which depends on his strategy as well as on that of other players . In the model, each player continuously adjusts his variable in order to maximize his utility. He also faces stochastic shocks which affect his actions and, as a result, the variable becomes a continuous time stochastic process. The stochastic force acting on a player is similar to that arising from an “heat bath” at finite temperature in statistical mechanics. The dynamics allows for a comparison with equilibrium dynamics in statistical mechanics, which we find a useful paradigm to discuss the results. In this comparison negative utility plays the role of an energy and the effects of fluctuations can be compared to entropic effects in statistical mechanics. The main difference between the two dynamics is that, while in statistical mechanics each degree of freedom evolve to minimize a global (free) energy, in game theory each degree of freedom maximizes his own (part of the total) utility.

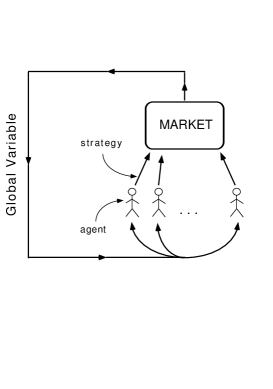

We shall focus on a particular class of games with a global interaction. By this we mean that the utility of each player depends on others’ players strategies only through an aggregate or global quantity , whose value is determined by all of them. This peculiar interaction, shown schematically in figure 1, reflects the nature of economic laws such as the law of demand and supply.

Nash equilibria are stationary points of the dynamics. When we include fluctuations we find that two main equilibria exist: i) non-competitive equilibria, where each player’s equilibrium strategy is determine by its interaction with the rules of the game and ii) competitive equilibria, which result from the the aggressive competition of each player with all the others. For example, we shall discuss a game where the introduction of taxes determines both a non-competitive and a competitive equilibria. In the former it will be the balance between profit and loss due to taxes, which is important for each player. In the other, competitive equilibrium, taxes are negligible and the balance leading to equilibrium is only due to the competition among all players.

The main results that we shall find are:

-

1.

Competitive Nash equilibria are usually affected by very large fluctuations which increase with the number of players. Competition leads to broad distributions and large inequalities in an economic system. This is reminiscent of Pareto Law of distribution of incomes[9]. We shall find that inequalities increase with the number of players.

-

2.

Competitive equilibria are also characterized by large relaxation times which are proportional to , and by a negative correlation between players’ strategies. This means that two players tend to have opposite fluctuations around the Nash equilibrium.

-

3.

At odd with statistical mechanics, where fluctuations always increase the system’s energy, we shall find that in a game theoretical system, under particular conditions, fluctuations increase the utility (i.e. decrease the “energy”).

-

4.

We can, in principle, compute the stationary state distribution in strategy space. This allows to solve, for example, the problem of equilibrium selection in games where more than one Nash equilibrium exists.

-

5.

Fluctuations, in general, displace Nash equilibria and in some cases, for strong enough randomness, a Nash equilibrium can also disappear.

-

6.

Our approach also suggests that time-scales for the transition from one Nash equilibrium to another one are proportional to , where is a “free energy barrier” and is the noise strength.

The paper is organized as follows. The next section reviews game theory and discusses some simple game. We also discuss briefly evolutionary game theory and its differences with our approach. Section 4 introduces the class of models we shall analyze. The following section discusses gaussian fluctuations around Nash equilibria. Then we develop a general approach to the stationary state probability distribution in strategy space. The main results are illustrated with simple examples. In the final section we summarize the results, we draw some conclusions and comment on possible further extensions.

2 Game theory and evolution

An economic system consists of a large number of interacting agents. In the game theoretical setting, each agent has a spectrum of strategies parametrized by an index . Each player is also endowed of a utility or payoff function which depends on the strategy he plays as well as on that played by all other players. With the notation , we can conveniently write . are also called pure strategy as opposed to mixed strategies , in which strategy is played with probability by player . Under mixed strategies, the strategies used by the players are independent random variables. Independence is justified in one stage games, which are played just once and each player has to decide his strategy simultaneously, without information about what others will do.

Game theory, in its simplest setting, assumes that the payoff functions are common knowledge and that each player behaves rationally. Rationality is also common knowledge, which means that each player knows all other players are rational (these are so-called complete information games). Game theory aims at predicting the possible stable states of the system, which are called Nash Equilibria [7]. The strategies are a Nash Equilibrium (NE) if each player’s utility, for fixed opponents’ strategies , is a maximum for , i.e. , . The NE strategies are such that no player has incentives to change his strategy, since any change would cause a utility loss. Nash showed[7] that any game has at least one Nash equilibrium in the space of mixed strategies.

2.1 The Cournot Game and the Tragedy of the Commons

The concept of NE is best illustrated by a simple example, originally introduced by Cournot in 1838 [10]: 2 firms produce quantities and respectively, of a homogeneous product. The market-clearing price of the product depends, through the law of demand-and-offer, on the total quantity produced: . The larger the smaller is. The model assumes that the cost of producing a quantity is and . The firms choose their strategies (i.e. ) with the goal to maximize their profit. We can then define the payoff function as . The problem is to find assuming that both firms behave rationally. One way to do this is by means of the concept of best response. The best response of a player to the opponents strategies , is the strategy which maximizes . In the Cournot game, the best response of firm to any given strategy of firm is obtained by maximizing with respect to with fixed , i.e. . Firm , knowing that behaves rationally (i.e. that it will play whatever is) will choose which maximizes . It is important to stress that operationally this means

i.e. the maximum of must be found at fixed . This leads to . This simple example shows that rationality, and the assumption of other’s rationality, plays a crucial role in the concept of Nash equilibrium[7]. It is easy to generalize this game to firms. Let us set, for convenience, and . Then , where is the average of . The calculations generalizes straightforwardly and we find [8] a NE at and a per player payoff . This celebrated example, is also known as the Tragedy of the commons[11]. In this formulation of the problem, the utility depends on a common resource which, at the NE, is almost totally depleted by the aggressive behavior of players. As a result each player receives a very small payoff. This is an example of a competitive NE where the strategies of players are not limited because of a direct loss in utility, but because the global resource is almost exhausted by the aggressive, competitive behavior of players.

2.2 Repeated Games and Evolutionary Game Theory

This setting generalizes to repeated games, where different stage games are played a finite or an infinite number of times. In repeated games a strategy must describe the action the player has to do at each stage. Also the single stage utility is generally replaced by an utility which accounts for many stages, usually with a discount factor (i.e. an exponential weight function for future utility). All these things make the analysis much more complex than in single stage games.

A game posses, in general, several NE’s, and this raises the question of which of them is more relevant. In order to answer this question, several definitions of stability have been proposed [12, 13, 14]. The most successful approach to stability has been that of evolutionary game theory[15, 12]. This considers a game with mixed strategies as a game played by a population of players playing pure strategies with random opponents.

This idea has attracted much interests in the community of theoretical population biologists, which have translated this idea into a mathematical model: the so called replicator dynamics[16]. Though several versions of this dynamics have been proposed [16, 12], in its simplest form, it assumes that the individuals playing a given strategy reproduce at a rate proportional to their utility. Stochastic fluctuations, in the population dynamical setting of replicator dynamics, have also been considered in refs. [17].

There are some points that are worth to point out in evolutionary game theory. The first is that its application has been mostly limited to two players games. Indeed its generalization to contexts with players is technically very complex[12]. The second is that rationality is not assumed. Players are on the contrary rather dull: they just keep playing the game the way their ancestors did. Rational NE results from the selective evolution of replicator dynamics. Finally we note that replicator dynamics assumes that the strategies are independently chosen by each player111The joint distribution of the strategies factorizes into the single players distribution functions .. It also assumes that is independent of for .

In contrast with these observations, our goal is to study a simple realistic dynamics for an players game with “almost” rational players. We shall do this weakening the assumption of perfect rationality with the introduction of a “thermal” noise. Therefore will become a continuous time stochastic process. We shall therefore pursue quite different purposes and use totally different techniques than those of evolutionary game dynamics.

3 The Langevin approach

Focusing on a class of models with a continuum spectrum of strategies , we recently proposed [8] a Langevin dynamics of the form

| (1) |

Where the stochastic term models deviation from perfect rationality. We take gaussian with and

| (2) |

Eq. (1) is a model dynamics which contains both the deterministic efforts each player exerts to increase his payoff and the effects of random events. The deterministic part assumes “local rationality” of the agents: each agent knows which is the direction in which his utility increases. In other words, it assumes that each agent knows the utility function as a function of in a small neighborhood of . Note that this weakens the assumption of perfect rationality, according to which each player knows the function for any and any , .

The stochastic term , represents all hindrances which prevent a rational behavior. These may be internal, i.e. affect only one player (e.g. illness), or external if they affect equally all players (e.g. earthquake). This suggests that is composed of two components, , where the ’s are independent gaussian forces. This motivates our choice

| (3) |

for the correlation of . Here is the strength of the stochastic force acting on player , whereas is that for events which affect all players in the same way.

Clearly, since NE are defined as the set of for which the equations

| (4) |

are simultaneously satisfied, for , NE are stationary points of the dynamics. Equation (1) is also very appealing since, comparing eq. (1) with model A dynamics[18], it allows for an analogy with statistical mechanics. The main difference with statistical mechanics is that in game theory each degree of freedom (player’s strategy) maximizes a different function (player’s utility) whereas in statistical mechanics each degree of freedom minimizes the same function (energy or Hamiltonian). Also, at odd with statistical mechanics, the interactions among strategies need not be symmetric: players’ goals may be in conflict with one another.

In this analogy, NE are analogs of zero temperature (meta) stable states. The Langevin approach includes “thermal” fluctuations in game theory, and this allows to analyze stability of NE through the study of fluctuations. It also gives a “free energy” measure, which enables to distinguish the real “ground state” from “meta-stable” states. Indeed in an ideal slow cooling down where , analogous to simulated annealing, only the state with the smallest “free energy” is selected independently of the initial conditions. This contrasts with the evolutionary approach, where the final state is uniquely determined by the initial conditions. The Fokker-Planck equation associated to eq. (1) provides a description of the game at the level of the distribution of . At odd with replicator dynamics (which also involves the distribution functions of the ), this does not assumes that the are independent. As we shall see, correlations indeed arise.

4 The model

Many complex systems in economics have a very peculiar form of interaction (see figure 1). In a stock market, for example, each agent guesses whether to buy or to sell a stock, looking at the stock’s price fluctuations. These fluctuations are in their turn produced by the cumulative effect of the actions of all the agents in the market, through some form of demand-offer law [5]. Each player interacts with a signal, which in its turn is determined by the collective effect of all players. A further example is the above mentioned Cournot model, where firms produce the same good, and the market clearing price is determined by the ratio between the aggregate production and the demand.

Focusing on this kind of interactions, we consider in the following situations where the payoff function for player is

| (5) |

In other words, the payoff for player depends on for only through the aggregate quantity . The -players Cournot game, is of this form with , and has been discussed at length in ref. [8].

Because of the symmetry of the interaction, the NE are symmetric: for all , and satisfies the equation

| (6) |

where we defined, for convenience,

A NE must not only be an extremum of , it must also be a maximum with respect to at fixed opponents’ strategies . This requires

| (7) |

It is worth to emphasize that eq. (6,7) are necessary but not sufficient for to be a NE. Indeed a NE must be globally stable, which means that must have a global minimum at .

5 Fluctuations around a Nash equilibrium

Let be a NE for our model. Without loss of generality we can set by a linear transformation . We shall also set . We can then investigate the small gaussian fluctuations around the NE resulting from the Langevin dynamics (1). Expanding the deterministic part to leading order, we arrive at the equation

| (8) |

where

Stability requires that all the eigenvalues of the matrix must be positive. These are given by the equation

| (9) |

A graphic inspection of the solutions of these equations, shows that if

| (10) |

then all eigenvalues are positive. Note that, in terms of and the local stability condition (7) reads . For this is clearly satisfied if the conditions (10) are met.

Equation (8) is a multivariate Ornstein-Uhlenbeck process [19]. Fluctuations around the NE are described by the matrix of correlations. This is the solution of the set of linear equations , where and is the matrix of the noise correlation given in eq. (3)[19]. Introducing the vector , this matrix equation can be reduced to

| (11) | |||||

| (12) |

Here we have introduced the notation for averages over the ensemble of players. Note that is the correlation between the variable and the global variable .

Qualitatively there are two different cases according to whether the are broadly distributed or not. We shall first focus on the second case, when the average value of is much larger than the fluctuations around it: . With a redefinition of the scale of , we set, for simplicity, . In the limit and , the values of are densely distributed in a small interval of size . In each interval , we can define an average value of , and , which we denote by , and . This allows for a systematic expansion in powers of .

For , one easily finds

| (13) |

Note that , which means that each variable tends to fluctuate in phase with . We can also compute an ensemble average of the correlation, which for reads

| (14) |

The common stochastic force, as it could be expected, gives a positive contribution to the correlation, and for large enough, the correlation always turns positive.

With respect to the dynamics in the stationary state, correlation functions decay exponentially

The correlation time of the leading exponential behavior is given by the minimum eigenvalue in eq. (9).

It is finally possible to compute the average utility

| (15) |

where all derivatives of are evaluated at . Note that in view of our choice this expression yields the deviation of the average utility from a completely rational behavior. As we shall see it is possible that fluctuations increase the average utility. The last term in eq. (15) is the average of the utility at the Nash equilibrium in presence of fluctuations:

This would be the utility of a player which maintains the NE strategy even in presence of fluctuations. It is interesting to note that it is possible that . Loosely speaking this means that in a game with random deviations from rationality players who are affected by the randomness may receive a higher payoff (on average) than those which behave rationally (). The condition for this to happen is

| (16) |

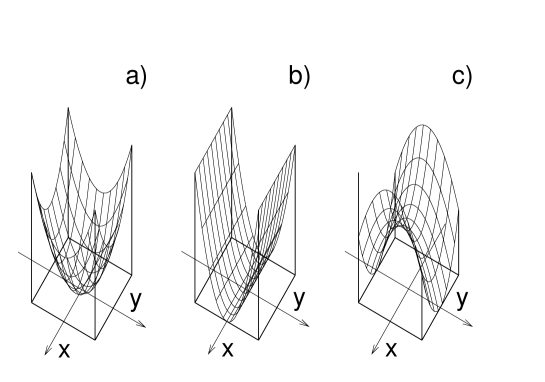

Let us now discuss these findings. As expected the fluctuations of grow with and . There are three qualitatively different cases, as shown in figure 2:

- a)

-

when and are all finite and positive. The point lies well inside the domain defined by eq. (10). As a result we have a normal behavior with small fluctuation. Fluctuations increase the average utility and a rational behavior is generally more rewarding.

- b)

-

, and are finite and positive. Then is small and, from eq. (13), we see that fluctuations are proportional to . This, in view of the explicit factor in front of in eq. (11), is a general feature which holds also for broadly distributed . The condition obtains for example for utilities of the form , which describes e.g. the tragedy of the commons problem[11, 8]. We shall discuss in more detail this class of models in the next paragraph. Generally is typical of competitive equilibria. Indeed it means that each player does not feel the effects of a change in his directly. Rather it feels it indirectly through the reaction of other players, or better through the effects this change has on the global variable . Large fluctuations are a result of the fact that the dependence of on is weak. Competitive equilibria are also characterized by negatively correlated variables for small enough: . Large fluctuations come together with large relaxation times. Indeed eigenvalues are proportional to , so that for all of them are small, yielding large relaxation times . Finally the average utility is decreased.

- c)

-

. Also in this case large fluctuations occur since . The divergence of the terms proportional to suggests that the mode with stronger fluctuations is associated with . For small the smallest eigenvalue is small. This results in a large correlation time . At odd with the case b), only one eigenvalue is small in this case, the others being . The (right) eigenvector associated with this eigenvalue is nearly constant. The slow mode characterized by large fluctuations is then associated with . Note that also is large and positive, which means that fluctuate in phase thus yielding a large fluctuation of their sum. Finally fluctuations may decrease the average utility in this case. Furthermore if player behaves rationally () he receives a smaller payoff .

These results can be extended to higher order in . The idea is to assume that are distributed around according to a gaussian density with standard deviation . We shall limit our discussion to the first term here. Taking the average of eq. (12), multiplied by over this distribution and taking the leading order in , gives

These equations give interesting informations. For example implies that the fluctuations experienced by a player are smaller the faster his dynamics (i.e. the larger his rate constant ). This is what one naturally expects and it occurs when . On the other hand, if grows sufficiently fast with , one has . This suggests that generally the fluctuations of a variable grow with and decrease with . The same kind of information can be obtained for the correlation . The case yields a compact expression:

This says that correlations are weaker for faster variables, unless grows fast enough with . We shall not discuss the case , which leads to less transparent formulas.

The case of broadly distributed needs a more detailed knowledge of the parameters. However we expect that the results obtained by the small disorder expansion above qualitatively describe the system. Note that eq. (11) suggests that diverges as . In a large system of players with broadly distributed , the smallest can be vanishingly small as . For example, in a system where the are distributed with a density for , one expects that the smallest , in the population of players, is . In this case some player can have fluctuations growing with . It is worth to stress, however that such a distribution of implies a power law distribution of characteristic times , which might not be realistic.

5.1 An example

Let us illustrate these findings with simple examples. An example with an utility of the form has been discussed in detail elsewhere [8]. The main point raised by this example is that of the emergence of large fluctuations. Here we shall describe a second example:

The utility function above describes a classical game where each player has to throw a number with the aim of guessing a fraction of the average of all players’ guesses. This clearly has only one NE , . can also be assumed as a local approximation of a more complex utility around one of its Nash equilibria.

With the choice , the parameters are and . The stability condition requires that , which is intuitive because if players where told to guess a number larger than the mean everybody would tend to overshoot and . On the contrary with every player has to be careful: he must play a number which is smaller than the one played by the others. In the extreme case he has to try to do the opposite of what the majority does. Let us discuss only the results for . It is straightforward to find

Note that, for , has the same sign of . For , a player attempts to guess the fluctuation of others and as a result it tends to make fluctuations in the same direction as the others. On the other hand, for a negative correlation arises.

The average utility is whereas the condition (16), after some algebra, reads:

In order for this condition to hold at least one of the two terms must be negative. For , it becomes “favorable” to follow the random force for

In other words, if the global component of the stochastic force is strong enough, it is not convenient to play the NE strategy .

This behavior can be qualitatively explained as follows: Each player has to try to follow as closely as possible the global variable . The latter evolves under a stochastic force of strength . The random force acting on each player has a component of strength along . If this component is large enough, each player can guess correctly whether the mean will move left or right and so it becomes favorable to follow the stochastic force.

For the condition holds with . This region is also characterized by large correlated fluctuations (note that ). Even in the absence of a global stochastic force, the dynamics leads to a state where the are highly correlated. In such a state, the strategy is less rewarding than the average.

For there are no values of and for which the condition (16) is satisfied.

6 Probability distribution in strategy space

In this section we shall extend the analysis of our model to study the full probability distribution in the stationary state. A complete treatment is not possible in general. We shall restrict attention to the case

In view of our discussion of the previous section, means that all players have the same characteristic time-scale. Qualitatively, we expect that the results below apply also in case of narrowly distributed time-scales.

Our equation is

| (17) |

It is useful to introduce the variables

| (18) | |||||

| (19) |

The transformation is orthonormal, which implies the useful identity

| (20) |

The same transformation, applied to the noise term leads to a stochastic force in the equation for which has a correlation

| (21) |

which is diagonal. The common stochastic force acts on only. For convenience, instead of , we shall use the variable . The noise appearing in the equation for has a strength .

6.1 Linear utility

Let us first consider the model

which allows for a full solution for the stationary state distribution of . A situation described by this kind of utility function [11, 8] is a system where firms produce a quantity of a homogeneous product. Then is the difference between the market clearing price of one unit of product and the production cost of one unit. We assume that it depends only on the aggregate production (the production cost per unit is a constant). The payoff of firm is then proportional to its production. In realistic situations is an increasing function. One expects e.g. that because of competition, the price of a product decreases with the total quantity produced, in view of the law of demand and offer.

The NE is defined by . Note that the payoff per player

is positive and proportional to .

The orthonormal transformation , yields

| (22) | |||||

| (23) |

The equation for does not involve other variables and can be directly solved yielding the distribution . The equations for depend only on . Treating as a parameter, one can find the conditional distribution of : . The full distribution is then

Back transforming to the variables , yields the solution. Eq. (23) describes a “particle” in a potential with thermal fluctuations and can be solved using standard techniques[19]:

| (24) |

with a normalization factor. The equation for similarly gives

| (25) |

where here normalization requires . Using the equation (20), one can easily find the full distribution of :

where .

Some implications of this result have already been discussed in ref. [8]. In particular it was observed that if one finds fluctuations of order and large relaxation times . We note furthermore that vanishes as . For , which corresponds in any case to an “unphysical” situation222For example, in the firms problem, means that the price increases if the production is increased., we must set . Note that eqs. (22, 23) imply that if the system is “prepared” at in a state with , in the early stages of the dynamics, the deviations increase exponentially. This is clearly a highly non-equilibrium situation.

The average utility, to order is given by

| (26) |

If , then the effect of fluctuation will be that of increasing the average utility (note that, in the notations of the previous section, ). An example, which allows for simple expressions, is . Since we need to restrict the range of to in order for (otherwise would flow to ). The NE is at and its existence requires . The payoff per player at the NE, to leading order in , is . With gaussian fluctuations, we find:

For fluctuations increase the average utility, an effect related to the asymmetry of the function around .

The average instead, has no corrections to order . As we shall see this does not hold in general. It does neither hold when the function changes rapidly close to the NE, a situation which cannot be described in the gaussian approximation. Consider for example, the game of the tragedy of the commons, where the utility function is much steeper when negative payoff arise: for and for and . This represents a situation where each player is very scared of receiving negative payoffs. Clearly, as far as the NE is concerned, no change occurs: The NE is always the same, dangerously close to the edge of negative utilities. In the presence of fluctuations, however, the distribution of is very asymmetric on the two sides of the NE. For it drops off much more quickly than for . As a result the NE is shifted by an amount of order towards safer values of . We see then that fluctuations can induce a more cautious behavior.

The most general model which allows for a complete solution, with the above technique, is with . The term changes only the distribution of by a factor proportional to , whereas the term also affects the distribution of . A simple realization of this model, with , is the one where players cooperate to increase each other’s utility: (). Of course means anti-cooperation, i.e. each player tries to maximize his utility as well as to minimize that of others. With , one easily finds that the NE is at and the payoff per player is . A high degree of cooperation, leads to a finite utility per player. On the contrary fluctuations always remain large . For , as discussed in [8], fluctuations diverge even though the average utility remains finite. Clearly anti-cooperation decreases the utility. However for fluctuations give a positive contribution to the utility. Fluctuations increase the average utility in over-competitive systems (those in which each player main efforts are devoted to decrease other players’ payoffs).

6.2 The general case

The general case does not allow for a full solution. It is however possible to compute the stationary state distribution to leading order in . We assume that

| (27) |

While this is surely satisfied close to a NE (when all are close to ), it might not hold in non-equilibrium situations or when rare events such as large fluctuations occur.

The equation for , derived from eq. (17), contains terms with or . Expanding in powers of and , we find, to leading order

where is still gaussian uncorrelated noise, in view of the orthonormality of the transformation (see eq. 21). This equation is valid to , since we neglected terms proportional to which are of order in view of eq. (27). Using eq. (21), one easily finds:

| (28) |

where we used the notation for the average of the quantity conditional to the value assumed by a second variable. Note that the requirement , implies . This condition, which generalizes the condition in the previous paragraph, restricts the range of possible values of .

Let us now move to the equation for . Expanding the right hand side of the equation for to second order in , we find

where . In view of eq. (20), we have . Taking the average over conditional to the value of in this equation, we substitute with . This results in the equation

where we suppressed the dependence on of .

The steady state distribution of is then given by , where the “temperature” is , and the “free energy” is given by:

| (29) |

It is useful, for the following discussion, to split into a independent part and into a dependent one:

and

The relation is reminiscent of a free energy in equilibrium statistical mechanics, which is a useful paradigm to discuss our system.

6.3 Discussion and applications

It is worth to stress that the function is not simply related to the utility. This contrast with equilibrium statistical mechanics where the probability of a state is directly related to his energy.

The “entropic” term results from the inclusion of the fluctuations of the variables . Usually, in statistical mechanics, one finds that the larger the fluctuations in a state the larger the entropy is. We shall see in the following that this does not hold for our system: can be larger for “ordered” states than for states with wild fluctuations.

Fluctuations displace the NE (defined as the minima of ) of a quantity of order :

Note that stability requires that the denominator be positive.

The analysis of any particular case goes as follows. First one needs to determine the range of where our approach can be applied. This is given by the condition which ensures that is finite. Outside this range, the behavior cannot be described perturbatively in (i.e. the gaussian approximation for the variables is no longer valid). Secondly find all solutions of eq. (6), , which are the candidates for NE’s. Each solution to this equation must then be checked for stability. If eqs. (10) are verified, the equilibrium is stable. Finally for each stable equilibrium one can evaluate its free energy from eq. (29). This gives the statistical weight of each state in the stationary regime. The state with the smallest is the one with a larger statistical weight and it dominates in the limit .

In ref. [8] we discussed the case

| (30) |

of a quadratic utility both in and . This is an interesting case, both because such an utility function can be motivated [8] and because the system possesses two NE’s. As a rough motivation, we can go back to the firms problem with , and argue that their utility may not exactly equal their net gain since this is then subject to taxes. If taxes do not grow linearly with the income (as is usually the case) we need to add a further term to the utility. The simplest choice leads to the above form of .

Let us go through the above passages for this example: Eq. (6) has one only solution for which is at

| (31) |

which is stable . For two other solutions appear at

| (32) |

of which only is stable. These two NE’s have a quite different nature. The NE at is a competitive NE since and it is characterized by a small payoff per player and by large fluctuations . The NE at is Pareto dominant333The NE with largest utility is called Pareto dominant equilibrium in game theory. since it has a finite and positive utility. Also fluctuations are finite, as , at . At this NE the action of players is limited by the increase of the non-linear term due to “taxes”.

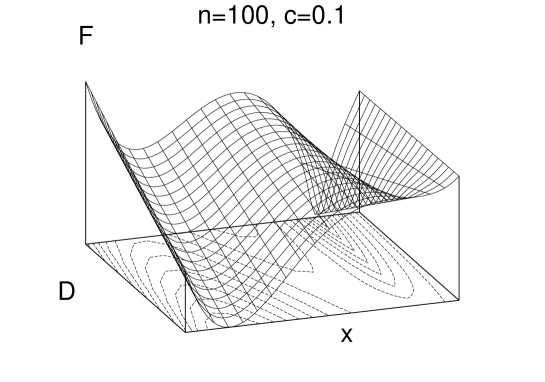

The function is readily computed. Setting, for convenience , we find

and

The function is plotted in figure 3 for as a function of . The “entropic” contribution, is of order . This is a consequence of the fact that in this model. Since , fluctuations in increase the probability of the state . Indeed for large enough , figure 3 shows that the state at has a higher probability. Therefore fluctuations in this case decrease the probability of the Pareto dominant NE. Note also that, as and , for , which implies that the probability to find the system in the Pareto dominant NE tends to . This example shows that the system does not always choose the state of maximum utility. In addition, when one stable state can become unstable. In our example, for higher values of or the state at which is a minimum of is no more a minimum of .

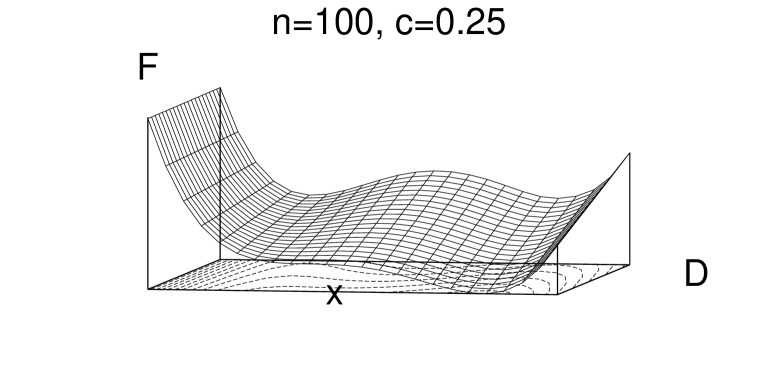

In this system, however, entropic effects are “accidentally” small because . If one adds a higher order term the situation changes. Consider indeed

| (33) |

For this has the same stable equilibria as before444For the system is unstable and for , becomes unstable and two new equilibria appear.. The picture, in the limit , is qualitatively the same apart from the entropy, which now is finite since . Note that , and . Therefore the effects of fluctuations are opposite to the ones discussed above. Indeed , which means that the stochastic force favours, in this case, the Pareto dominant NE over the state . Contrary to our intuition from statistical mechanics, it is the “ordered” state which has a larger contribution from the stochastic term. This is shown in figure 4, which shows in particular that fluctuations lead to a new minimum of : This meta-stable state is a precursor of the NE at . This example shows that the identification of with an entropy can be misleading.

Direct numerical simulations of the Langevin equation gives results in good agreement with this picture for small values of . The higher order terms in the expansion seem to enhance the behavior discussed above for the two particular models.

For a particle in a random potential subject to a stochastic force of strength , the transition times from one metastable state to the other are of the order of where labels the state of departure. The generalization of this result to our case, predicts relaxation times that, for diverge in the “thermodynamic” limit . This behavior is reminiscent of a first order phase transition in statistical mechanics. It is worth to remind, however, that the transition from one state to the other is a far from equilibrium process, whereas we derived eq. (29) within an approximation which is valid to order close to the equilibria (see eq. 27). For this reason we performed numerical simulations of the above bi-stable systems. Even though a systematic quantitative computation of transition times was too demanding, we definitely found that numerical simulations are in qualitative agreement with the picture emerging from the approximation.

7 Conclusions

We have introduced a simple stochastic dynamics for game theory. This assumes “local” rationality since any player tries to climb the gradient of his utility function. This deterministic process is affected by a stochastic force which represents deviation from rationality in the form of a “heat bath”. We focused on particular games with a global interaction which is typical of socio-economic systems: each player’s utility depends on his strategy as well as on a global quantity. The stable states of this dynamics coincide with the NE. We studied the gaussian fluctuations around these NE and established that competitive equilibria are characterized by large fluctuations which grow with the number of players. Large fluctuations imply great inequalities in the distribution of utility among players. Uneven distribution of goods is, unfortunately, very common in the economic world. Our analysis suggests that this is related to the competitive nature of the Nash equilibrium. Players competing for a common resource have broadly distributed utilities whereas players whose strategy is bounded by a direct utility loss (as in the tragedy of commons with taxes) have more or less the same payoffs. Fluctuations usually decrease the utility of players, but cases where the contrary holds are also possible. Finally we studied the general case in a small noise limit. We found that, depending on the particular, game, fluctuations can either increase or decrease the dominance of a Pareto dominant state and that new metastable states can occur.

This approach can naturally be extended to games with a discrete strategy space. For these, the Langevin dynamics can be replaced by e.g. Metropolis dynamics where each player tries to minimize his own cost function.

Fluctuations and deviation from rationality are inevitable in the real world. Reducing their strength costs time and money. This suggests a generalization of our work where is considered as a parameter in the strategy space. If one then assumes that players have “local” rationality so that the best thing they can do is to climb their utility gradient, one is left with a system where the strategy of each player consists in the choice of the strength of the fluctuations and the rate at which they climb the potential. In terms of these parameters we can define a generalized utility function

| (34) |

where the first term is the average utility discussed in the body of the paper. The second term is instead related to the cost of achieving a noise reduction to strength and a rate of convergence . In general we expect to be a decreasing function of . Furthermore infinite precision most likely requires an infinite cost. A possible candidate for is the entropy . In general we found that the average utility decreases with increasing . In these cases Nash equilibria, in the strategy space will occur for . In the particular cases where we found that increases with , a large noise strength will be preferred to a more rational behavior. This new approach would provide a more realistic description of real systems of interacting players.

This work was partly supported by the Swiss National Foundation under grant 20-46918.96

References

- [1] Anderson, P.W., K. Arrow, D. Pines, (1988), The Economy as an evolving complex system, Redwood city, Addison-Wesley Co.

- [2] Mandelbrot, B.B., (1963) J. of Business, 36, 394; Mantegna, R.N. and H.E. Stanley, (1995), Nature, 376, 46; Levy, M., H. Levy and S. Solomon, (1995), J. Physique I 5, 1087; Galluccio, S., G. Caldarelli, M. Marsili and Y.-C. Zhang, (1997) Physica A, 245, 423.

- [3] Ghashghaie, S. et al., (1996) Nature, 381, 767.

- [4] Bak, P. , M. Paczuski and M. Shubik, (1996) preprint cond-mat/9609144 (Submitted to the Journal of Mathematical Economics).

- [5] Caldarelli, G., M. Marsili and Y.-C. Zhang, (1997) Europhys. Lett. 40, 479.

- [6] Fudenberg D. and J. Tirole, (1991), Game Theory, The MIT Press.

- [7] Nash, J., (1950), Proc. Nat. Acad. Sci. 36, 48.

- [8] Marsili, M. and Y.-C. Zhang, (1997), Physica A, 245, 181.

- [9] Pareto, V. (1965), Ecrits sur la courbe de la répartition de la richesse, ed. G. Busino (Droz, Genéve).

- [10] Cournot, A. (1897) Researches into the Mathematical Principles of the Theory of Wealth, Ed. N. Bacon, New York Macmillan.

- [11] Hardin, G. (1968), Science 162, 1243.

- [12] Weibull, J.W., (1995), Evolutionary Game Theory, The MIT Press, (Cambridge, Massachusetts; London, UK.

- [13] Selten, R., (1975) Int. J. of Game Th. 4 25, studied the robustness of a NE with respect to players’ trembling hands. Trembling hand means that players are unable to play exactly pure strategies: any strategy is played with a probability that cannot be less than a small number . If a NE, in spite of this, does not change dramatically, then it is said to be perfect.

- [14] Wu, W., and J. Jiang, (1962), Sci. Sinica 11, 1307, investigated robustness of a NE with respect to small random perturbations in the payoff functions[14].

- [15] Maynard Smith, J. and G. R. Price, Nature, 246, 15 (1973); see also Maynard Smith, J. Evolution and the theory of Games, Cambridge Univ. Press (Cambridge, 1982).

- [16] Taylor, P., and L. Jonker, (1978), Math. Biosc. 40, 145; for a review, see J. Hofbauer and K. Sigmund, The Theory of Evolution and Dynamical Systems, Cambridge Univ. Press (Cambridge, 1988).

- [17] Foster, D., and P. Young, (1990), Theor. Pop. Biol. 38, 219; D. Fudenberg and C. Harris, J. Econ. Theory, 57, 420 (1992).

- [18] Hohenberg, P.C., and B. I. Halperin, (1977), Rev. Mod. Phys. 49, 435.

- [19] Gardiner, C. W., (1985), Handbook of Stochastic Methods, second edition, p. 124 (Springer-Verlag).