Detecting long and short memory via spectral methods

Abstract

We study the properties of memory of a financial time series adopting two different methods of analysis, the detrended fluctuation analysis (DFA) and the analysis of the power spectrum (PSA). The methods are applied on three time series: one of high-frequency returns, one of shuffled returns and one of absolute values of returns. We prove that both DFA and PSA give results in line with those obtained with standard econometrics measures of correlation.

keywords:

serial correlation, high-frequency data, DFA, power spectrum, short memory, long memory.url]http://people.unt.edu/sb0269 ††thanks: The author would like to thank Prof. R. Renò for research assistance and proofreading, and the Welch foundation for financial support through grant no. B-1577

1 Introduction

The analysis of financial time series has become an important field of application for

physicists. A special role plays the analysis of serial correlation in the

time series, as it gives useful insight to the price formation

mechanism. The study of serial correlation is not new, both in Econometrics

and Econophysics. The presence of serial correlation in the time series of

log-returns is forbidden by the efficient market hypothesis in its weak form,

see [1]. At daily level the presence of these fluctuations has been

found in several markets and interpreted in the rational framework, with non-synchronous

trading [2] or institutional factors [3], or invoking behavioral

factors [4].

The number of works on serial correlation with intraday and

high-frequency data is, at our knowledge, very limited due mainly to

the presence of microstructure effects in the time series that make difficult

a direct analysis of the problem. Recent examples are

Refs. [5] on the Italian futures index, [6] on the

exchange rates and [7] on the Indian market. In this paper we show how the adoption of popular

methods of statistical data analysis to infer about the presence of serial

correlations at intraday level, can be meaningful interpreted at the light of econometrics

measures, if the microstructure of the market is correctly taken into

account. Particularly, we adopt a simple analysis of the power spectrum

(PSA) associated with the signal, and the famous Detrended Fluctuation Analysis (DFA)

method.

The paper is organized as follows: Sections 2 and 3

introduce the statistical instruments used, the data set is described

in Section 4, Section 5 shows the methodology that we

employ and discuss the results at the light of

recent works on the same topic, while Section 6 concludes.

2 Power spectrum analysis

Let be a stochastic process, we define the power spectrum as the square modulus of the Fourier transform of the signal, namely:

| (1) |

The power spectrum is linked to the autocorrelation function of the signal by the Wiener-Khintchine theorem, namely by the following equation:

| (2) |

which admits the following inverse relation:

| (3) |

In absence of correlations, the correlation function is peaked and the power spectrum is flat (white noise). If on the contrary there is serial correlation, this does not hold anymore and therefore we observe a decay in the power spectrum with the frequency as follows:

| (4) |

By monitoring the decay of we can infer about the memory properties of the time series under study. To perform the PSA we use a fast Fourier transform algorithm.

3 Detrended Fluctuation Analysis

The method of DFA has been widely adopted in the literature, starting from the

analysis of DNA sequences [8] to financial time

series [9], from ecological applications [10] to nuclear

reactions related problems [11]. It consists on the evaluation of the scaling properties of the locally

detrended standard deviation of the time series. We shall now briefly introduce

the algorithm.

Let again , () be a stochastic process. The method consists on the

following steps:

-

•

build the integrated time series where is the mean value of the signal;

-

•

divide the new sequence in non-overlapping subsequences of length ;

-

•

evaluate the local trend of each subsequence, ;

-

•

evaluate the summation of the differences between the integrated time series and the local trend in the time window , and take its standard deviation, t. i. the quantity:

(5)

The modified standard deviation so built has the following scaling property:

| (6) |

If the process is a white noise and there no autocorrelation; if , then there is significant autocorrelation in the time series. In the next Section we shall describe the data set we use for the analysis of this paper.

4 Data set description

The data set at our disposal consists of all the transactions taken from the

Italian futures on the stock index S&PMIB, named FIB30, in the period from

January 2000 to December 2002. We use only the

next-to-expiration contracts. The data are evenly spaced according to a

previous interpolation procedure at a time lag of minute. The spacing has the effect of getting rid of

microstructure effects that can spoil the analysis, see Ref. [5]

for a complete discussion. We have trading days, for a total of

transactions. After the spacing procedure, we have

minute returns per day. The same data set has been also used in recent

publications, see Refs. [12, 13].

In the next Section we shall see how the analysis

is performed.

5 Methodology and results

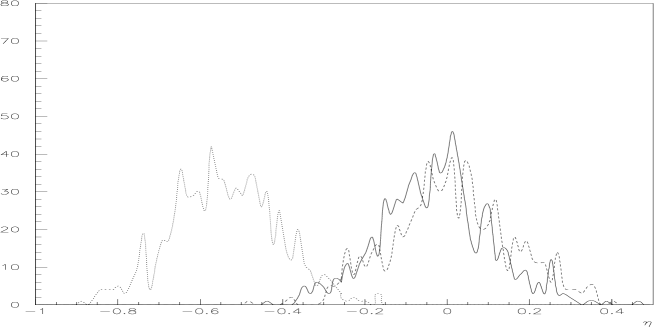

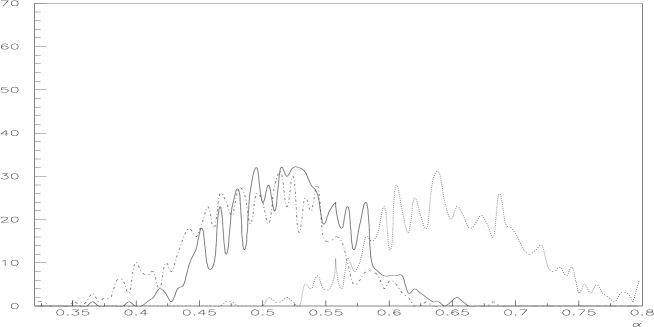

In this Section we describe the methodology that we use to evaluate the memory properties of the time series. We apply the methods introduced in the previous Sections to three time series: one made of high-frequency returns, whose memory properties are unknown, one obtained by shuffling the returns and therefore without memory, and one of absolute returns, which are known to be long range autocorrelated. We repeat the procedure for every day of our data set and build the distribution of the coefficients obtained from the PSA and the DFA. We then plot the three distributions and compare them to infer the memory characteristics of the original time series. The results are in Figs. 1 and 2.

It is evident from the Figures that both the methods agree in detecting no

memory in the time series of shuffled returns: both distributions are centered

around the expected value, that is for PSA and for DFA. We note that the standard

deviation of the distributions is a reliable measure of the statistical

uncertainty of the coefficient. Moreover the results of the two methods when

applied to the time series of absolute returns are, as expected, compatible with

the hypothesis of long memory of this time series. When applied to the time

series of real returns, both DFA and PSA suggest the presence of short memory

effects in the time series, being the distributions of coefficients between

the other two.

In order to properly address the results we refer again to Ref. [5], where the

authors were able to prove, adopting only econometric indicators, the presence of

short memory in the time series of returns.

Our study therefore suggests that the

adoption of DFA and PSA is effective in the evaluation of short and long term memory in

financial time series.

6 Concluding remarks

In this paper we prove that an effective relation exists between what is expected adopting scaling method of analysis, as DFA, spectral methods, as PSA, and econometric indicators, as in Ref. [5] in the evaluation of intraday serial correlations in high-frequency financial time series. As far as our knowledge is concern this study is the first to highlight this equivalence on high-frequency data. We think that might be interesting to extend the analysis on more liquid markets, as the US stock market, and we plan to address this problem in the future.

References

- [1] E. Fama, Journal of Finance, 25, 383-417 (2003).

- [2] A. W. Lo and A. C. MacKinlay, Journal of Econometrics 45, 181-211 (1990).

- [3] J. Boudoukh, M. Richardson, and R. Whitelaw, Review of Financial Studies 7(3), 539-573 (1994).

- [4] D. Cutler, J. Poterba, and L. Summers, Rev. of Econ. Studies 58, 529-546 (1991).

- [5] S. Bianco and R. Renò, Journal of Futures Market, 26, 61-84 (2006); Proc. of Spie, vol. 5848, 318-322 (2005).

- [6] A. Low and J. Muthuswany, in Forecasting Financial Markets: Exchange Rates, Interest rates and Asset Management, C. Dunis ed., 3-32, John Wiley & Sons (1996).

- [7] S. Thomas and T. Patnaik, unpublished work, 2003.

- [8] C.-K. Peng, S.V. Buldyrev, S. Havlin, M. Simons, H.E. Stanley, and A.L Goldberg, Phys. Rev. E, 49(2):1685-1689 (1994).

- [9] J. A. O. Matos, S. M. A. Gama, H. J Ruskin, and J. A. M. S. Duarte, Physica A, 342 665-676 (2004).

- [10] L. Telesca, R. Lasaponara, and A. Lanorte, Physica A, 361, 699-706 (2005).

- [11] J. Alvarez-Ramirez, G. Espinosa-Paredes, and A. Vazquez, Physica A, 351 227-240 (2005).

- [12] R. Rizza and R. Renò, Physica A, 322, 620-628 (2003).

- [13] M. Pasquale and R. Renò, Physica A, 346, 518-528 (2005).