On the top eigenvalue of heavy-tailed random matrices

Abstract

We study the statistics of the largest eigenvalue of random matrices with iid entries of variance , but with power-law tails . When , converges to with Tracy-Widom fluctuations of order , but with large finite corrections. When , is of order and is governed by Fréchet statistics. The marginal case provides a new class of limiting distribution that we compute explicitly. We extend these results to sample covariance matrices, and show that extreme events may cause the largest eigenvalue to significantly exceed the Marčenko-Pastur edge.

One of the most exciting recent result in mathematical physics is the Tracy-Widom distribution of the top eigenvalue of large random matrices TW . In itself, this result is remarkable since it constitutes one of the rare exactly soluble case in extreme value statistics for strongly correlated random variables (the eigenvalues of a random matrix), generalizing in a non trivial way the well known Gumbel-Fisher-Tippett, Weibull and Fréchet cases Galambos . But the truly amazing circumstance is that the very same distribution appears in a host of physically important problems Spohn : crystal shapes, exclusion processes Satya , sequence matching, directed polymers in random media, etc. The last case can in fact be considered, thanks to the mapping onto the Tracy-Widom problem, as an exactly soluble disordered system in finite dimensions, for which not only the scaling exponents but the full distribution of the ground state energy can be completely characterized Johansson .

As for many limit theorems, the Tracy-Widom result is in fact expected to hold for a broad class of random matrices. The precise characterisation of this class, as well as the extension of the Tracy-Widom result for other classes, is a subject of intense activity Sosh1 ; BBAP . It is already known that for symmetric matrices with iid entries of variance , such that all moments are finite, the Tracy-Widom result holds asymptotically Sosh1 . The case where the distribution of entries decays as a power-law (possibly multiplying a slow function) is expected to fall in a different universality class, at least when is small enough. In the case where the variance of entries diverge, it is known that even the eigenvalue spectrum of is no longer the Wigner semi-circle but itself acquires power-law tail , bequeathed from the tails of the matrix entries CB ; Burda . Correspondingly, the largest eigenvalues are described by Fréchet statistics Sosh2 . What happens when is in the range , such that the eigenvalue spectrum still converges CB , for large , to the Wigner semi-circle? The aim of this letter is to discuss this problem in details. We find that as soon as , the Tracy-Widom result holds asymptotically, albeit with large finite size corrections that we compute. For , the largest eigenvalues are still ruled by Fréchet statistics. The marginal case provides a new class of limiting distribution that we compute explicitly. We then extend these results to the case of sample covariance Wishart matrices, for which power-law tailed elements are extremely common, for example in financial applications book . Finally, the relation with directed polymers in the presence of power-law disorder is shortly addressed.

We start by considering real symmetric matrices with iid elements of variance equal to , and such that the distribution has a tail decaying as:

| (1) |

where the tail amplitude insures that ’s are of order . As soon as , the density of eigenvalues converges to the Wigner semi-circle on the interval , meaning that the probability to find an eigenvalue beyond goes to zero when . However, this does not necessarily mean that the largest eigenvalue tends to – we will see below that this is only true when . In order to understand the statistics of the largest eigenvalues, we need first to study the following auxiliary problem. Consider an random matrix with iid elements , such that its eigenvalue spectrum is, for large , the Wigner semi-circle. Now, we perturb this matrix by adding a certain amount to a given pair of matrix elements, say : and . What can one say about the spectrum of this new matrix? There are several ways to solve this problem: self-consistent perturbation theory (that we use below), free convolution methods Verdu or the replica method; the last two methods in principle require some specific properties of matrix , for example that has Gaussian entries. However, the three methods give the same results for large , as can be understood from general diagrammatic considerations (see e.g. Zee ). Self-consistent perturbation theory is rather straightforward and can be easily extended to other cases, such as Wishart matrices (see below). We write down the eigenvalue equations as:

| (2) |

while for , neglecting compared to :

| (3) |

and similarly for . We look for a special solution such that is of order unity, whereas all other ’s are of order . We assume (as will be self-consistently checked) that in the large limit the terms and both converge to , where is a constant to be determined. As a consequence, from Eq. (3), up to small corrections. One can now solve equation (2) to obtain:

| (4) |

where and are the eigenvalues and the eigenvectors of the matrix obtained from removing the rows and the columns and . Using this expression, we can compute . Up to terms negligible in the large limit one finds:

| (5) |

where is, by assumption, the Wigner semicircle. Performing the integral over , the above self-consistency assumption finally leads to . This equation for only has a solution when , in which case and the corresponding eigenvalue of the perturbed matrix is with , which is therefore expelled from the Wigner sea (see BBAP for a similar mechanism in the case of sample covariance matrices, and Peche for Hermitian random matrices). Note that these eigenvalues come in pairs, with , corresponding to . When , one the other hand, no such eigenvalue exist, our assumption that there exists a localised eigenvector sensitive to the presence of breaks down, and the edge of the spectrum remains in this case. One can in fact compute and characterize completely the corresponding localised eigenvector. Using Eq. (4) and imposing the normalisation condition one finds:

| (6) |

showing that for large , as expected, the eigenvector completely localises on and , whereas when , it “dissolves” over all sites – for the perturbation is not strong enough to induce condensation. Eq. (6) enables one to compute various participation ratios of the eigenvectors, for example .

The above computation shows that adding any entry strictly less than unity (in absolute value) to a Wigner matrix does not affect the statistics of its largest eigenvalue. There is in fact a stronger theorem, due to S. Péché Peche , showing that the addition of any matrix of rank , , with its largest eigenvalue less that unity, leaves unchanged the statistics of the largest eigenvalue of a random Hermitian matrix. The mechanism leading to such a result is very similar to the one above; the largest eigenvalue of the resulting matrix is when , and otherwise.

We can now come back to our initial problem, and define the matrix by removing all elements of that are (in absolute value) larger than , where is finite, but as large as we wish. It is clear that all the moments of are now finite; therefore the largest eigenvalue of has a Tracy-Widom distribution of width around Sosh1 ; TW . The number of ‘large’ entries that we have removed is, using Eq. (1), with . Now, we should add back the entries that we have left out, starting by all those between and . Naively, each one of them leaves unchanged: one can dress with all entries less that and still keep the largest eigenvalue Tracy-Widom. If the number of such elements was (with ), the Péché theorem would insure that this is true. Unfortunately, this number is rather , but all added entries are iid and randomly scattered over the matrix, and the Wigner semi-circle is preserved at each step. It is thus natural to conjecture that provided all these entries are strictly below unity, the largest eigenvalue remains Tracy-Widom. We have checked this numerically for different values of (see Fig. 1).

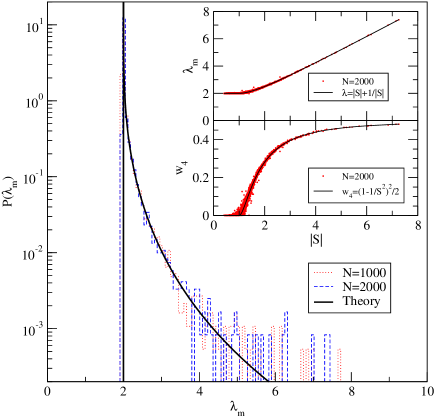

We are now left with entries . From Eq. (1), their number is . In the case , it is clear that this number tends to zero when . With probability close to unity for large , no entry is larger than one, in which case the largest eigenvalue is Tracy-Widom. With small probability, the largest element of exceeds one; its distribution is and the corresponding largest eigenvalue, using the above analysis, is . For and large but finite , we therefore expect that the distribution of the largest eigenvalue of is Tracy-Widom, but with a power-law tail of index that very slowly disappears when . Our numerical results are in full agreement with this expectation (see Fig. 1). When , on the other hand, the number of large entries increases with . However, when is larger than , such as to insure that the eigenvalue spectrum still converges to the Wigner semi-circle, the number of row or columns where two such large entries appear still tends to zero, as . Therefore, the above analysis still holds: for each large element exceeding unity, one eigenvalue will pop out of the Wigner sea. Even if the eigenvalue density tends to zero outside of the interval when , the number of eigenvalues exceeding (in absolute value) grows as . The largest entries are well known to be given by a Poisson point process with Fréchet intensity Sosh2 ; the order of magnitude of the th largest entry is which diverges with , such that in this regime the eigenvectors become strictly localized (). The largest eigenvalues are then equal to the largest entries and are themselves given by a Poisson point process with Fréchet intensity, as proven by Soshnikov in the case Sosh2 . His result therefore holds in the whole range . Finally, the marginal case is easy to understand from the above discussion. The number of entries exceeding one remains of order unity as ; the distribution of the largest entry is Fréchet with -independent parameters:

| (7) |

The probability that exceeds is , in which case ; otherwise, with probability , . This characterizes entirely the asymptotic distribution of the largest eigenvalue in the marginal case : it is a mixture of a -peak at and a transformed Fréchet distribution. Note that this asymptotic distribution is non-universal since it depends explicitly on the tail amplitude . Our argument also predicts the structure of the eigenvector when is finite, see Eq. (6). Again, all these results are convincingly borne out by numerical simulations, see Fig. 2. The statistics of the second, third, etc. eigenvalues could be understood along the same lines.

We now turn to the case of sample covariance matrices, important in many different contexts. The ‘benchmark’ spectrum of sample covariance matrix for iid Gaussian random variables is well known, and given by the Marčenko-Pastur distribution MP . Here again, the spectrum has a well defined upper edge, and the distribution of the largest eigenvalue is Tracy-Widom (see e.g. BBAP ). What happens if the random variables have heavy tails? More precisely, we consider times series of length each, denoted , where and . The have zero mean and unit variance, but may have power-law tails with exponent . For example, daily stock returns are believed to have heavy tails with an exponent in the range book . The empirical covariance matrix is defined as:

| (8) |

When the time series are independent, and for and both diverging with a fixed ratio , the eigenvalues of are distributed in the interval . When at fixed , all eigenvalues tend to unity, as they should since the empirical covariance matrix converges to its theoretical value, the identity matrix. When and are large but finite, the largest eigenvalue of is, for Gaussian returns, a distance away from the Marčenko-Pastur edge, with Tracy-Widom fluctuations. When returns are accidentally large, this may cause spurious apparent correlations and substantial overestimation of the largest eigenvalue of . Let us be more specific and assume, as above, that one particular return, say , is exceptionaly large, equal to . A generalisation of the above self-consistent perturbation theory, or free convolution methods, shows that whenever , the largest eigenvalue remains stuck at , whereas when , the largest eigenvalue becomes:

| (9) |

This result again enables us to understand the statistics of as a function of the tail exponent . For times series of iid random variables, of length each, the largest element is of order . For , this is much smaller than and, exactly as above, we expect the largest eigenvalue of to be Tracy-Widom, with possibly large finite size corrections Burda2 . For , large ‘spikes’ in the time series dominate the top eigenvalues, which are of order and distributed according to a Fréchet distribution of index . For applications to financial data, reasonable numbers for intraday data are , and , leading to , compared to the Marčenko-Pastur edge located at . This shows that the effect can indeed lead to anomalously large eigenvalues with no information content. In the marginal case , as above, has a finite probability to be equal to the Marčenko-Pastur value, and with the complementary probability it is distributed according to a transformed Fréchet distribution of index , with a and independent scale. The structure of the corresponding eigenvectors can also be investigated and is again found to be partly localized when . Finally, we expect similar results to hold for the Random Singular Value problem studied in Augusta , where rectangular matrices corresponding to cross correlations between different sets of time series are considered.

As mentioned in the introduction, the Tracy-Widom distribution for the largest eigenvalue of complex sample covariance matrices has deep links with the directed polymer problem in (1+1) dimension Johansson . A naive guess would therefore be that the universality class of the ground state energy changes whenever the disorder of the directed polymer problem has fat tails with an exponent . This is in fact not correct, at least in the version of the directed polymer problem where each site carries a random iid energy. In this case, simple Flory type arguments Zhang suggest that the universality class in fact changes as soon as . More precisely, the energy fluctuations should scale as and by Tracy-Widom for , and as for with a new type of limiting distribution (the case corresponds to a complete stretching of the polymer and was recently solved in Hamley ). We have conducted new numerical simulations of this problem which indeed confirm that for , the ground state energy scales as with Tracy-Widom fluctuations, while for the above Flory prediction seems correct. The distribution of ground state energy can be fitted by a geometric convolution of Fréchet distributions: , different from the pure Fréchet distributed reported above for the largest eigenvalue for . Following BBAP , the correct mapping should in fact be onto a directed polymer with power-law columnar disorder. We leave this for further detailed investigations.

In summary, we have analyzed the statistics of the largest eigenvalue of heavy tailed random matrices. We have shown that as soon as the entries have finite fourth-moment, the largest eigenvalue has Tracy-Widom fluctuations, whereas if the fourth-moment is infinite, the largest eigenvalue diverges with the size of the matrix and has Fréchet fluctuations. In the marginal case where the fourth-moment only diverges logarithmically, the distribution is a non-universal mixture of a delta peak and a modified Fréchet law. The structure of the associated eigenvector evolves from being completely delocalized in the Tracy-Widom case, to partially or totally localized in the Fréchet case. We have shown that similar results holds for sample covariance matrices, and that extreme events may cause the largest empirical eigenvalue to significantly exceed the Marčenko-Pastur edge.

Acknowledgments - We thank Gerard Ben Arous and Sandrine Péché for important discussions. GB is partially supported by the European Community’s Human Potential Program contracts HPRN-CT-2002-00307 (DYGLAGEMEM).

References

- (1) C.A. Tracy and H. Widom, Level spacing distributions and the Airy kernel, Comm. Math. Phys., 159, 33 (1994)

- (2) J. Galambos, The Asymptotic Theory of Extreme Order Statistics, Malabar, FL: Krieger (1987)

- (3) for a review, see: H. Spohn, Exact solutions for KPZ-type growth processes, random matrices, and equilibrium shapes of crystals, cond-mat/0512011

- (4) S. Majumdar, S. Neachaev, Exact asymptotic results for the Bernoulli matching model of sequence alignment, Phys. Rev. E 72, 020901(R) (2005)

- (5) K. Johansson. Shape fluctuations and random matrices, Comm. Math. Phys. 209 437 (2000).

- (6) A. Soshnikov. Universality at the edge of the spectrum in Wigner random matrices, Comm. Math. Phys., 207 697 (1999).

- (7) J. Baik, G. Ben Arous, S. Péché, Phase transition of the largest eigenvalue for non-null complex sample covariance matrices, Ann. Probab. 33 1643 (2005)

- (8) P. Cizeau and J.P. Bouchaud, Theory of Lévy Matrices, Phys. Rev. E50 1810 (1994)

- (9) Z. Burda, J. Jurkiewicz, M. A. Nowak, G. Papp and I. Zahed, Random Lévy Matrices Revisited, cond-mat/0602087.

- (10) A. Soshnikov. Poisson statistics for the largest eigenvalues of Wigner random matrices with heavy tails, Elect. Comm. in Probab. 9, 82 (2004)

- (11) J.-P. Bouchaud and M. Potters, Theory of Financial Risk and Derivative Pricing, Cambridge University Press (2003); M. Potters, J.-P. Bouchaud and L. Laloux, Financial Applications of Random Matrix Theory: Old laces and new pieces, Acta Physica Polonica B, 36 2767 (2005)

- (12) for a review, see, e.g.: A. Tulino, S. Verdù, Random Matrix Theory and Wireless Communications, Foundations and Trends in Communication and Information Theory, 1, 1-182 (2004).

- (13) A. Zee, Law of addition in random matrix theory Nucl. Phys. B474, 726 (1996)

- (14) D. Féral, S. Péché, The largest eigenvalue of rank one deformation of large Wigner matrices, math.PR/0605624. S. Péché, The largest eigenvalue of small rank perturbations of Hermitian random matrices, Probab. Theory Relat. Fields 134, 127 (2006)

- (15) M. Prähofer, H. Spohn, Exact scaling functions for one-dimensional stationary KPZ growth, J. Stat. Phys. 115 (1-2), 255-279 (2004).

- (16) V. A. Marčenko and L. A. Pastur, Distribution of eigenvalues for some sets of random matrices, Math. USSR-Sb, 1, 457-483 (1967)

- (17) For a case where the asymptotic eigenvalue spectrum develpos fat tails, see: Z. Burda, T. Gorlich, B. Waclaw, Spectral properties of empirical covariance matrices for data with power-lawtails, physics/0603186

- (18) J.-P. Bouchaud, L. Laloux, M. A. Miceli, M. Potters, Large dimension forecasting models and random singular value spectra, Eur. Phys. J. B (2006).

- (19) Y. C. Zhang, Growth anomaly and its implications, Physica A170, 1 (1990)

- (20) B. Hambly, J. B. Martin, Heavy tails in last-passage percolation, math.PR/0604189.