Stochastic Storage Models and Noise-Induced Phase Transitions

Published online 13 January 2007)

Abstract

The most frequently used in physical application diffusive (based on the Fokker-Planck equation) model leans upon the assumption of small jumps of a macroscopic variable for each given realization of the stochastic process. This imposes restrictions on the description of the phase transition problem where the system is to overcome some finite potential barrier, or systems with finite size where the fluctuations are comparable with the size of a system. We suggest a complementary stochastic description of physical systems based on the mathematical stochastic storage model with basic notions of random input and output into a system. It reproduces statistical distributions typical for noise-induced phase transitions (e.g. Verhulst model) for the simplest (up to linear) forms of the escape function. We consider a generalization of the stochastic model based on the series development of the kinetic potential. On the contrast to Gaussian processes in which the development in series over a small parameter characterizing the jump value is assumed [Stratonovich R.L., Nonlinear Nonequilibrium Thermodynamics, Springer Series in Synergetics, vol.59, Springer Verlag, 1994], we propose a series expansion directly suitable for storage models and introduce the kinetic potential generalizing them.

pacs:

05.70.LnNonequilibrium and irreversible thermodynamics and 05.40.-aFluctuation phenomena, random processes, noise, and Brownian motion and 05.10.GgStochastic analysis methods (Fokker-Planck, Langevin etc)1 Introduction

One of the aspects of modelling the behaviour of a complex physical system consists in introducing a random process capable of describing its essential properties. The most common (and in practice almost unique) class of stochastic processes where reliable results can be obtained is the class of Markov processes. Said processes in their turn can be subdivided into different families. The most widespread is the model of diffusion process with Gaussian noise superimposing on the macroscopic dynamics. The Poisson random processes (or ”shot noise”) present a second bench point Horst together with the former subclass covering the most common physical situations. In the present paper we bring into consideration the stochastic storage models based on essentially non-Gaussian noise and treat them as a complementary alternative to the diffusion approximation (that is to the Gaussian white noise). We consider the phase transitions in such models which resemble the noise-induced phase transitions Horst .

The class of stochastic storage models Prabhu ; Brock presents a rather developed area of the stochastic theory. As opposed to the common diffusion model Horst ; Risken it contains as essential part such physical prerequisites: (i) limitation of the positive semispace of states, (ii) the jumps of a random physical process which need not be considered small; (iii) essentially non-zero thermodynamic flux explicitely specified by the process of random input.

The following material allows to conjecture that said models provide more handy facilities of describing the noise-induced phase transitions than diffusion ones Horst . One of the reasons in favour of this is the fact that typical probability distributions there are not Gaussian but rather exponential and gamma-distributions which are characteristic for, e.g., Tsallis statistics. The approach of the present work is invoked to extend the range of applicability of such models. Attempts have already been made to apply them to the kinetics of aerosol coagulation Ryazanov:1990 , to the problems of probabilistic safety assessment methodology Ryazanov:1995 etc, and to relate these processes to the Gibbs statistics and general theory of dynamic systems Ryazanov:1993 . One more possible application of the storage models consists in the possibility of naturally introducing the concept of the lifetime of a system (the random time of existence of a given hierarchical level) Prabhu ; Ryazanov:1993 ; Ryazanov:2006 ; Chechkin:2005:1 . It was shown Ryazanov:1993 that the ambiguity of macroscopic behaviour of a complex system and the existence of concurring evolution branches can be in principle related to the finiteness or infiniteness of its average lifetime.

It is worth mentioning now that (at least) the simplest cases of storage models do not require special probabilistic techniques, and corresponding kinetic equations are treatable by means of the Laplace (or Fourier) transform. Up to now such models have not gained much recognition in physical problems. We believe them to be rather promising especially in the approaches based on modelling the kinetics of an open system, where the input and release rates could be set from the physical background. In the present work we do not intend to cover the variety of physical situations akin to the storage models. Having discussed the form of the stationary distributions for a set of input and release functions (Sect.2) and their relation to noise-induced phase transitions we reconsider the formalism of the kinetic potential and fluctuation-dissipation relations (FDR) (Sect.3) and then pass to the problem of reconstructing the underlying stochastic process from the available macroscopic data (Sect.4). The material of Sect.4 also considers the possibility of generalizing the classical storage schemes to cover more realistic physical situations. The concluding Section gives an example of an application in the context of a practical problem of modelling a nuclear fission process.

2 Storage model as prototype to phase transition class models

Stochastic storage models (dam models) belong to a class of models well known in the mathematical theory of random processes Prabhu ; Brock . They bear a close relation to the queuing theory and continous-time random walk (CTRW) schemes Feller:2 . The visualization object for understanding the physical ground of such a model is a reservoir (water pool), the water supply to which is performed in a random fashion. The random value describing the bulk amount in a storage is controlled by the stochastic equation:

| (1) |

Here is the (random) input function; is the function of output (release rate). Usually deterministic functions are considered. In the simplest case it is constant:

| (2) |

The storage model (1) is defined over non-negative values , and the output from an empty system is set to be zero (2). Therefore the release rate from (1) is written as a discontinuous function

| (3) |

More complicated input functions can be brought into consideration. Analytical solutions are easy to find for escape rates up to linear Prabhu ; Brock

| (4) |

As to the random process describing the input into the system, it can be specified within various classes of processes. For our purposes a partial case will be of special interest, namely, that of Lévy processes with independent increments Prabhu ; Feller:2 . It can be completely described by its Laplace transform:

| (5) |

where means averaging. The function is expressed as

| (6) |

with

| (7) |

The function and parameters (7) have a transparent physical meaning clear from the visualized water pool picture of the model. Namely, describes the intensity of Poisson random jumps (time moments when there is some input into the pool), and is the distribution function (scaled to unity) of the water amount per one jump with average value . Thus, is the probability distribution of a generalized Poisson process Feller:2 (for a “pure” Poisson process there were ). For illustrative purposes the typical choice

| (8) |

will be considered. In this case the function (6) has the form

| (9) |

The parameter gives the average rate of input into a system representing thus an essentially non-zero thermodynamic flow. The basic property of the stochastic process under consideration is thus the violation of the detailed balance (absence of the symmetry of the left- and rightwards jumps). This intrinsic characteristics makes them a candidate for the systems essentially deviating from the equilibrium (locating beyond the ”thermodynamic branch” Horst ). From this point of view the thermodynamic equilibrium of a storage model is achieved only in the degenerate case , that is for a system which occupies only the state (of course, the equilibrium heat fluctuations are thus neglected).

Another property of the model consists in the finiteness of jumps, on the contrast to the custom scheme of Gaussian Markov processes with continuous trajectories. Therefore such models can be believed to be more adequate in describing the systems with fluctuations which can no more be considered small (for example, systems of small size). We recover however the continuous-walk scheme setting , and keeping finite. In this case the input is performed with an infinite intensity of jumps of infinitely small size, that is the system is driven by a Wiener-like noise process with positive increments; if we limit the release rate with linear terms (4) the process for the random variable then turns to that of Ornstein-Uhlenbeck Risken ; Vankampen ; Gard , and the storage model presents its natural generalization. More specifically, one can introduce the smallness parameter [in equilibrium situations with Gaussian noise it would equal to ; generally accounts for the environment and noise levels in a system and can be related to the parameter in the stationary distribution ] such that

| (10) |

from where the Gaussian case is recovered assuming ; the exponent in the characteristic function (5) acquires now the form of the Gaussian processes with drift.

It is instructive from the very outset to trace the relation of the present models to the stochastic noise introduced by the Lévy flights as well as to the processes encountered in the CTRW. The non-Gaussian stable laws are described by means of the characteristic function of their transition probabilities in the form Chechkin:2005:1 ; Feller:2 ; Metzler ; Chechkin:2005:2 ; Chechkin:2003 ; Chechkin:2002 ; Sokolov:2003 ; Uchaikin ; Zolotarev ; Jespersen with the Lévy index , the case recovering the Gaussian law. The generalized central limit theorem states that the sum of independent random variables with equal distributions converges to a stable law with some value of depending on the asymptotic behaviour of the individual probability distributions Feller:2 ; Uchaikin . In the case of the storage model the characteristic function from (6) [where instead of there enters after an appropriate analytical continuation in the complex plane] comes in place of . The finiteness of indicates that the trajectories of the storage process are discontinuous in time. It is understandable that if the functions from (6-7) have a finite dispersion, the sum of many storage jumps will converge to the Gaussian law with . From the physical picture of the dam model, as well as from the analytical expressions like (5) we can see that the storage models present a class of models where a mimic of the long-range flights is effectively introduced, likewise in the Lévy flights, but the nonlocality is achieved by virtue of the finiteness of allowed jumps. Indeed, the trajectories of the centered process present a saw-like lines with irregular distribution of the jump sizes. Only in the limit of big times and scales it can be viewed as a Wiener process with the variance with . On shorter time scales the behaviour of the process models the features akin to the superdiffusion (to the positive semiaxis), and, on the contrary, a completely degenerated ”subdiffusion” to the left since the jumps to the left are forbidden. In this context the function presents an effectively varying Lévy index which ranges from the superdiffusive region () to negative meaning suppression of the diffusion. The variable Lévy index for diffusion processes is encountered in the models of distributed-order fractional diffusion equations (see. e.g. Chechkin:2002 ). Actually, it is possible to bring into consideration from the outset the input fuctions pertaining to the “basins of attraction” of other stable distributions with Lévy indices . The storage schemes in which the functions themselves are stable Lévy distributions with power-like assymptotics are considered in Brock .

The CTRW processes Feller:2 ; Metzler ; Sokolov:2003 are characterized by the joint distribution of the waiting times and jumps of the variable. The stochastic noise in the storage models is a narrow subclass of CTRW where the waiting times and jump distributions are factorized, and the waiting time distribution is taken in a single possible form ensuring the Markov character of the process Uchaikin . This suggests a simple generalization to a non-Markovian case. Namely, assuming the storage input moments to be distributed by an arbitrary law instead of used we arrive at generalized CTRW schemes yielding semi-Markovian processes which can be applied for introducing the memory effects into a system.

The solution to the models (1-5) can be found either with the sophisticated apparatus of the mathematical storage theory Prabhu ; Brock or directly by solving the appropriate kinetic equation (see Sect.3,5). A considerable simplification in the latter case is achieved in the Fourier space where up-to linear release rates yield differential equations of the first order (the situation is similar to the systems with Lévy flights which are usually treated in the Fourier space; note also the analogy to the method of the ”Poisson representation” in the chemical reactions problems Gard ).

For the constant escape rate (2) all characteristics of the time evolution of the model are obtained in the closed form Prabhu . We mention just for reference for :

where , the same as in (6) and satisfies a functional equation

| (11) |

However the feature of interest now is the stationary behaviour of the models of the class (1). Even for continuous functions and the stationary distributions besides the continuous part can have an atom at zero, that is

| (12) |

where is a probability distribution scaled to , and . The integral equation for from Brock reads as:

| (13) |

with the measure . For the exponential shape of the input function (8) for which the equation (13) can be solved for arbitrary release functions ( is found from the normalization condition):

| (14) |

The condition of the existence of the stationary distributions for arbitrary input and release functions from Brock is the existence of some such that

| (15) |

Similarly the expression for can be written for the general case Brock . There is a simple relation

between the weight of the zero atom and the average lifetime (averaged random time of attaining the zero level starting from a point ). The presence of the non-zero indicates at the existence of idle periods where no elements are present in a system. Such periods can be characteristic for systems of the small size (in which the values of fluctuations of a macrovariable are comparable to their averages) Ryazanov:2006 and must influence essentially the statistical properties of a system, for example, they impose limitations on the maximal correlation time.

The behaviour of the models (1) admits a pronounced property of nonequilibrium phase transitions (change in the character of the stationary distribution) which occur when one increases the value of the average thermodynamic flow (parameter ). The phase transition points can be explored by investigating the extrema of the stationary distribution (cf. the analysis of noise-induced phase transitions in Horst ), that is for the case of (14) – from the condition . For example, for the model with constant escape rate we get two types of solutions: converging solution for small input rates and the pool overflow (no stationary solution exists) if the average input per time unit exceeds the output rate. The criterium for the phase transition (15) in this case reads simply as . If , no stationary distributions are possible. For the stationary distribution possesses additionally an atom at with the weight . Explicitly for (8) and the stationary distribution for is:

| (16) |

Consider now the exit function and the input in the form (8). This storage system does not have an atom at zero, and the stationary probability distribution exists for all input rates – there is no overflow in the system:

| (17) |

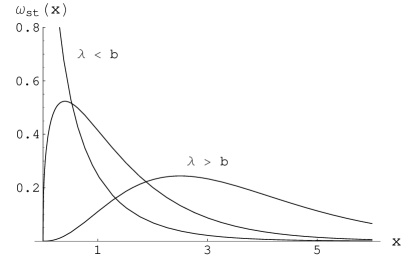

() is gamma-function). The phase transition is the modal change of the distribution function, which occurs at , where the distribution changes its character from the exponential to Gauss-like with a maximum at (Figure 1). This peculiarity of the stationary distribution can be interpreted as a non-equilibrium phase transition induced by external fluctuations. Such transitions are typical Horst ; Hongler for the multiplicative type of noise. They do not have their deterministic analogue and are entirely conditioned by the external noise. The phase transition at manifests in the emerging of the nonzero maximum of the distribution function although all momenta of the distribution change continuously. As in the Verhulst model Horst the phase transition at coincides with a point in which , where is the dispersion, is the first moment of the distribution. With the choice of the input function in the form the stationary distribution is

( is Bessel function). The behaviour of the distribution is qualitatively the same as on Fig.1 with the phase transition point at as well. In both cases we have the phase transitions which are caused by an additive noise (which does not depend on the system variable). The existence of phase transitions for the additive noise is closely related to the long-range character of the distribution function of the noise and such transitions were discovered in systems with, e.g. Lévy type of additive noise Chechkin:2005:1 ; Chechkin:2005:2 where the structural noise-induced phase transitions are conditioned by the trade-off between the long-range character of the flights and the relaxation processes in the model. Analogous conclusions for other types of superdiffusive noises are also drawn in Jespersen ; Hongler etc. We can thus state that the effective long-rangeness in the storage models leads to similar effects causing the modal changes of the distribution function which can be interpreted as a nonequilibrium noise-induced phase transition.

More complicated example is the rate function and the input rate (8). In this case

( is incomplete gamma-function). It combines two previously considered models: there is an atom at with weight and there is the phase transition at critical where the distribution switches from exponential to Gaussian-like. This critical value is . If , it coincides with that for the model , and if - with the results of model (17).

For a realistic release function , () corresponding to, for example, the nonlinear voltage-current characteristics, the solution to (13) for exponential input (8) (expression (14)) yields [in this case, like for the linear model , ]:

(we consider the case only because natural restrictions on the drift coefficient impose Brock ). The phase transition points can be explored from the custom analysis of the value of the corresponding cubic determinant . The number of phase transitions varies from one () to three at depending on the relations between , , and . This latter example can be compared to the nonequilibrium regimes found in the quartic potential well driven by an additive Lévy-type noise Chechkin:2005:2 ; Chechkin:2003 ; as in the above systems the additional criticality is achieved due to a long-range character of the additive noise.

The distribution functions and phase transitions in this class of models are common to various physical systems. Relative simplicity in mathematical treatment allows us to propose them as a handy tool for modelling physical phenomena of stochastic nature. We will show that this class of models based on the Poisson noise presents a prototype for stochastic modelling complementary to the commonly considered Gaussian noise. This latter, as the simplest case of phenomenologically introduced stochasticity, became in fact the most recognized way of introducing noise, and various enhancements of stochastic description meant merely an extension of the Langevin source of a Gaussian nature introducing the small parameter of jumps value (see later in the Section 4). The use of the Poisson noise, starting from the storage model as its basic case, allows an extension to more complicated cases as some regular development series in a small parameter as well. In contrast to the Gaussian scheme, it does not require at the very beginning the smallness of jumps thus it is able of describing more adequately a wide class of physical phenomena where this assumption does not have its physical justification. As an example we mentioned a thermodynamic system of a small size, where the random value is the number of particles. The Gaussian assumptions are valid only for large size (in comparison to the rates of input or output) of a system, when the diffusion approximation can be used. The smaller is the system, the worse is the description in terms of minor random jumps (basic for Gaussian scheme), and, vice versa, more reliable becomes the description based on the Poisson character of a random process.

3 Fluctuation-dissipation relations and formalism of the kinetic potential

This section is a brief reminder of the formalism of the kinetic potential Stratonovich which is appropriate for presenting the properties of a Markovian random process in a compact form.

The primary concept of the Markov process is the transition probability for a random value to jump from the initial state at the time moment into state at , that is the probability . The idea of Markovian behaviour imposes obvious restriction on the values , so that they possess a superposition property , ; in other words, form a continuous semigroup in time (the reverse element of this group for dissipative processes is not defined), so that all characteristics of a system can be derived from the infinitesimal generators of the group. In normal language, we bring into consideration the probabilities per time unit (). To characterize this function it is useful to consider its moments which are called “kinetic coefficients”:

| (18) |

The stationarity of the Markov process assumes that are time-independent. The kinetic equation for the distribution function of the process reads as Risken ; Vankampen ; Stratonovich

| (19) | |||

The kinetic potential is defined as the generating function of the kinetic coefficients Stratonovich :

| (20) |

Thus the kinetic coefficients can be expressed as

| (22) |

In (22) the notation means the order of the differentiation operations: they should follow all actions with the multiplication by as it is seen from (19).

An example of the kinetic potential for the simplest and most utilized stochastic process is

| (23) |

With the choice , , the corresponding kinetic equation is then the Fokker-Planck equation for the Orstein-Uhlenbeck process Risken ; Vankampen which describes a system with linear relaxation towards the stationary solution in the Gaussian form

Note that the kinetic potential for a process driven by a Lévy flight noise has thus the generic form and assumes the kinetic equation of the formally fractional order which is not reduced to the series in (19); one uses instead its plausible generalization which can be encountered elsewhere (e.g., Metzler ; Sokolov:2003 ; Uchaikin ; Zolotarev ; Jespersen etc).

As another example we write down the form of the kinetic potential for the class of storage models of Section 2. The kinetic potential through the transition probabilities of a Markov process is written as

| (24) |

where . Inserting there the Laplace transform of the random value from (1), we obtain Ryazanov:1993 , for an elementary derivation see Appendix:

It is handy to introduce another generating function called the “image” of the kinetic potential Stratonovich . Namely, let be the stationary solution of the kinetic equation (19). The image of the kinetic potential is defined as

| (26) |

or, in the notation of the transition probabilities,

| (27) | |||

The series of over :

| (28) |

defines new coefficients being the image of :

| (29) |

We note by passing that the variable in (26) or (29), presenting merely a variable over which the Laplace transform of the process variables is performed, can be also understood as a (fictive or real) thermodynamic force. This interpretation is clarified when we look at the “pseudo-distribution” where stands for an amendment to the free energy of a system Stratonovich .

The reconstruction of a stochastic random process assumes that knowing macroscopic information about system we make plausible assumptions as to the fluctuating terms of the kinetic equation, that is we try to construct the matrix of the transition probabilities in any of equivalent representations (18), (20) or (26) leaning upon some macroscopic information about the random process. As the latter, we can understand the following two objects: 1) the stationary distribution , and 2) “macroscopic” equations of motion which are usually identified with the time evolution of the first momenta of and hence the kinetic coefficient (in the case of the sharp probability distribution where one can identify the ”macroscopic variable” at all). For example, for the storage model scheme the problem is inverse to that considered in Section 2: knowing the macroscopic relaxation law and the shape of the stationary distribution we then try to reconstruct the input function . The relaxation law is given by the balance of the averaged input and release rate (in the present class of storage models the input rate is -independent, the generalization is considered further). Then, given one can set into correspondence to it the input function yielding a given distribution :

| (30) |

The relations between said objects and the remaining part of the stochastic information contained in the process are called fluctuation-dissipation relations (FDR). These relations express the property of time reversibility of the transition probabilities (detailed balance). In the representation of the image of kinetic potential (26), (27) they are written in the most elegant fashion Stratonovich :

| (31) |

where according to the parity of the variable. The particular case of the FDR in the form (31) at represents the “stationary” FDR

| (32) |

The FDR in the form (32) hold for any system in the stationary state with no assumption about the detailed balance, that is the system needs not to be in the equilibrium state. Indeed, it is easy to check that (32) is just an another notation of the equation for the stationary distribution (see Appendix).

4 Reconstruction of the random process

The problem of reconstructing a random process in the notations of the preceding section is formulated as a set of algebraic equations for a function . Thus, given functions and we must find which identically satisfies the relation (31) (for the system in equilibrium) or (32) (for the stationary system with no assumption about the thermal equilibrium and detailed balance). The problem, of course, has many solutions since those conditions do not define the function uniquely. There exists the “FDR-indeterminable information” which hence should be borrowed from some additional criteria to be imposed on the equations in order to close the problem, which means confining ourselves within some class of the stochastic processes. The kinetic potential representation allows us to elucidate clearly the nature of the approximations made.

4.1 “Gaussian” scheme

The standard reconstruction procedure considers the possibility of setting the “FDR-indeterminable” functions negligibly small, that is introducing a small parameter over which the kinetic potential can be developed in series Vankampen ; Stratonovich . Thus the generalization of the “bare Gaussian” model showed in the example above (23) is achieved. In the series

successive coefficients decrease progressively as . This relation can be expressed introducing the family of kinetic potentials labelled by the large parameter Stratonovich (compare with (10))

| (33) |

This is a common approximation for a random process consisting in the fact that its jumps are small. If we keep only two terms and , the second coefficient for one variable can be restored from FDR exactly. As an example, we write the kinetic potential reconstructed up to 4-th order (from the formula (31) applying development in the powers of ):

where the coefficient is arbitrary (indeterminable from FDR). The first term describes the base variant corresponding to (23).

4.2 “Storage” scheme

The assumption of small jumps leads to the possibility to neglect the higher order kinetic coefficients , constructing a stochastic process by the “Gaussian” scheme (G-scheme). We suggest an alternative approach which can be regarded as complementary to the G-scheme and does not require the assumption of the small jumps. Like G-scheme, it has its basic variant which is well treatable mathematically.

We assume now that the kinetic coefficients are expandable into series over the variable :

| (34) |

Possibility of truncating these series implies that in (34) contain a small parameter which decreases them progressively with the growth of the number : for . In the coefficient determining the macroscopic evolution we however keep the macroscopic part whose development on does not depend on : .

The image of the kinetic potential thus turns out to be a development into series

| (35) |

here

and are defined through coefficients in (34):

The series (35) can be considered as a development on the base which is a natural base of the problem following from the peculiarities of its stationary distribution. The coefficient at has the same meaning as the function from (6) and truncating (35) up to it reproduces the storage scheme of Sec.2. This is a generalization referring to the multiplicative noise processes instead of (1) with the characteristics function of the noise instead of (5).

From the equation applying it to (35) we obtain the reconstructed scheme for a random process (“S-scheme”):

| (36) | |||

Keeping in mind that the coefficient is supposed to be known the last expression can be rewritten as

| (37) |

The coefficients at are dissipative-indeterminable. They are given by

5 Conclusion. An example of possible application

Both schemes sketched above - that is the common G-scheme and suggested complementary S-scheme of the stochastic reconstruction both lean upon two basic stochastic models which use respectively the assumption of Gaussian and Poissonian nature of the random noise. They both apply the series development of the kinetic potential on a small parameter. Keeping infinite series leads to identical results in both cases. However, in real physical problems we use to truncate the expansion series keeping small finite number of terms. According to the physical situation and to the nature of the random noise either one, or another scheme would give a more reliable convergence.

Consider now an example of the storage model with the linear release rate (4) and generalized input which is now -dependent (Sect.4.2). Find the solution of the simplest linear dependence of the input function on with the kinetic potential (20) set as

| (38) |

The first two terms in (38) describe the usual storage model with linear release, and the last term is the amendment to the input function proportional to (cf. (34-35)). The parameter controls the intensity of this additional input. The equation for the Laplace transform of the stationary distribution is , where the differentiation refers only to the function . Its solution for in (38) is

| (39) |

For illustration specify now the input functions as

| (40) |

which correspond to the exponential distribution functions of input jumps (6,8) . Then

| (41) |

Comparing to the solution of the storage model shows that the additional term leads to an effective decrease of the parameter . The stationary probability distribution is given by the gamma-distribution function

The stationary solution exists if , otherwise the system undergoes the phase transition with the system overflow likewise for the model with constant release rate. If there are two phase transitions (increasing ), first of which is that of the model (17) (Fig.1) and the second is the system overflow at . If the overflow occurs earlier than the condition meets and qualitatively the behaviour of the system is similar to that of constant release rate (2), with the transition condition instead of former .

Now let us sketch an example of application of the generalized storage scheme for the problem of neutron fission process. Set the generating function in (38) in the following form

here is the generating function of the neutron number distribution per one elementary fission act ( for a discrete variable); are probabilities of emerging secondary neutrons (discrete analogue of the function in (6)); is the fission intensity (probability of a fission act per time unit), with average neutron velocity and macroscopic fission cross section Zweifel ; further, , is the average neutron lifetime till the absorbtion or escape Zweifel . Let us set and assume that the function accounts for the external neutron source with intensity (the smallness parameter in (34) now describes the relation of the intensities of fission and external source events). This probabilistic model is essentially the same as in the example of the generalized storage scheme (38) sketched above. From (22),(38)

that is we arrive at the equation for the

distribution function of the prompt neutrons in the diffusion

single-velocity approximation. The macroscopic equation for the

averages

is

Zweifel and coincides with that obtainable apriori from the stochastic storage model. The neutron reproduction factor is defined as Zweifel , where is the average number of secondary neutrons per one fission act. The expression for the generalized storage model phase transition corresponds to the reactor criticality condition . Extending probabilistic schemes in (38) beyond the toy model considered here and introducing vector (multi-component) stochastic processes allows for taking into account the delayed neutrons, as well as various feedbacks and controlling mechanisms.

6 Appendix. Derivation of the relations (25) and (32)

Here we sketch the elementary derivations of the expressions in the text describing the kinetic potential of the storage model (expr. (25)) and that of the stationary FDR through the image of the kinetic potential (expr.(32)). The more rigorous and generalizing derivations can be searched elsewhere, resp. Prabhu ; Brock ; Ryazanov:1993 ; Stratonovich .

6.1 Kinetic potential of the storage model

From (1) and (24) using the fact that the input rate is a random process independent on (to simplify notations we set the initial moment ):

Then, using (5) and taking ,

The last term of this expression gives in the limit provided that the intensity of jumps is finite which is the case of the considered class of Poisson processes.

6.2 Stationary FDR

We limit ourselves to the nonequilibrium FDR relation only. For a general case of the detailed balance, as well as for the generalization to non-Markov processes, the reader is referred, e.g., to the book Stratonovich .

The stationary Fokker-Planck equation is written as

| (42) |

Perform over (42) the operation . Use the relation

for some which can be verified with recursive integrations by parts (the terms with full derivation vanish at ; if the space of states is a semiaxis as in the storage models, the integration including the atom in is assumed). Then,

| (43) |

References

- (1) W. Horsthemke, R. Lefever, Noise-Induced Transitions. Theory and Applications in Physics, Chemistry, and Biology (Springer Verlag, Berlin, 1984)

- (2) N.U. Prabhu, Stochastic storage processes (Springer Verlag, Berlin, 1980)

- (3) P.J. Brockwell, S.I. Resnick, R.L. Tweedie, Adv. Appl. Prob. 14, 392 (1982)

- (4) H. Risken, The Fokker-Planck Equation (Springer, Berlin, 1984)

- (5) V.V. Ryazanov, in Aerosols: Sciense, Indystry, Health and Environment, 1 band (Pergamon Press, Kyoto, 1990), p.142; V.V. Ryazanov, S.G. Shpyrko, Journal of Aerosol Science, 28, 647 (1997); ibid. 28, 624 (1997)

- (6) V.V. Ryazanov, S.G. Shpyrko, in Proc. Int. Conf. on Probabilistic Safety Assessment Methodology and Applications. PSA’95, Seoul, 1995 (Atomic Energy Research Institute, Seoul, Korea, 1995), v.1, p.121

- (7) V.V. Ryazanov, Ukr.Phys.J. 38, 615 (1993)

- (8) V.V.Ryazanov, S.Shpyrko, Cond.Matt.Phys., 9, 71 (2006).

- (9) A.V.Chechkin et al, Europhys.Lett. 72, 348 (2005); J.Phys.A:Math.Gen. 36, L537 (2003)

- (10) W. Feller, An Introduction to Probability Theory and its Applications, vol.2, (John Wiley & sons, Inc., New York, 1971)

- (11) N.G. Van Kampen, Stochastic Processes in Physics and Chemistry (North-Holland Personal Library, 1992)

- (12) C.W. Gardiner, Handbook of Stochastic Methods for Physics, Chemistry and the Natural Sciences, Springer Series in Synergetics, Vol. 13, 3rd edn. (Springer Verlag, Berlin, 2004)

- (13) R.Metzler,J.Klafter, Phys.Rep.339,1 (2000)

- (14) A.V.Chechkin,V.Yu.Gonchar, J.Klafter, R.Metzler, Phys.Rev. 72 E, 010101 (R) (2005)

- (15) A.V.Chechkin et al, Phys.Rev. 67 E, 010102(R) (2003).

- (16) A.V.Chechkin, R.Gorenflo, I.M.Sokolov, Phys.Rev. 66 E, 046129 (2002)

- (17) I.M.Sokolov, R.Metzler, Phys.Rev. 67 E, 010101(R) (2003).

- (18) V.V.Uchaikin, Uspekhi fizicheskih nauk 173, 847 (2003) [Physics - Uspekhi, 46, 821 (2003)].

- (19) V.M.Zolotarev, One-Dimensional Stable Distributions, AMS, Providence, RI, 1986.

- (20) S.Jespersen, R.Metzler, and H.S.Fogedby, Phys.Rev. 59 E, 2736 (1999)

- (21) M.-O.Hongler, R.Filliger, P.Blanchard, Physica A 370, 301 (2006)

- (22) R.L. Stratonovich, Nonlinear Nonequilibrium Thermodynamics, Springer Series in Synergetics, vol. 59 (Springer Verlag, Berlin, 1994)

- (23) P.F. Zweifel, Reactor Physics (McGraw-Hill, New York, 1973)