On the Origin of Power-Law Fluctuations in Stock Prices

Abstract

We respond to the issues discussed by Farmer and Lillo (FL) related to our proposed approach to understanding the origin of power-law distributions in stock price fluctuations. First, we extend our previous analysis to 1000 US stocks and perform a new estimation of market impact that accounts for splitting of large orders and potential autocorrelations in the trade flow. Our new analysis shows clearly that price impact and volume are related by a square-root functional form of market impact for large volumes, in contrast to the claim of FL that this relationship increases as a power law with a smaller exponent. Since large orders are usually executed by splitting into smaller size trades, procedures used by FL give a downward bias for this power law exponent. Second, FL analyze 3 stocks traded on the London Stock Exchange, and solely on this basis they claim that the distribution of transaction volumes do not have a power-law tail for the London Stock Exchange. We perform new empirical analysis on transaction data for the 262 largest stocks listed in the London Stock Exchange, and find that the distribution of volume decays as a power-law with an exponent — in sharp contrast to FL’s claim that the distribution of transaction volume does not have a power-law tail. Our exponent estimate of is consistent with our previous results from the New York and Paris Stock Exchanges. We conclude that the available empirical evidence is consistent with our hypothesis on the origin of power-law fluctuations in stock prices.

pacs:

05.45.Tp, 89.90.+n, 05.40.-a, 05.40.FbWe recently proposed a testable theory for the origin of the empirically-observed power-law distributions of financial market variables such as stock returns, volumes, and frequency of trades Gabaix03 . Our theory explains the power-law exponent of the distribution of returns by deriving a square-root functional form for market impact (“square-root law”) that relates price impact and order size. Our previous empirical analysis gave results that support the square-root law of market impact.

Farmer and Lillo (FL) Farmer03 raise some issues related to the empirical validity of the theory proposed in Ref. Gabaix03 . Their discussion is based on the following arguments:

-

1.

FL claim that the price impact function grows slower than a square-root law. Interestingly, FL’s empirical analysis does find a power-law relationship for market impact with exponent for volumes smaller than a threshold, consistent with the square-root form of market impact in our theory. However, for large volumes FL claims [for the New York Stock Exchange (NYSE)] and [based on analyzing 3 stocks in the London Stock Exchange (LSE)]. FL do not compute error-bars for for large volumes, but claim that, from a visual comparison, (square-root law) is inconsistent with the data.

-

2.

FL argue that the empirical analysis that we presented in support of the square-root functional form of market impact Farmer03 is “invalidated” by the “long-memory nature of order flow.”

-

3.

FL analyze the volume distribution of 3 stocks from the London Stock Exchange and claim that the volume distribution does not follow a power-law. Consequently, FL conclude that volume fluctuations do not determine the power-law tail of returns.

We first outline our responses to these criticisms and then present our detailed response with results of our new analysis.

-

1.

FL find for large volumes from analyzing the average value of return for a trade for a given trade size. FL’s procedure for estimating price impact is flawed since large orders are usually executed by splitting into smaller size trades, so the procedure used by FL gives a downward bias for the power law exponent defined in our theory Gabaix03 ; Gabaix04 , giving rise to an apparent exponent value smaller than the correct value . In fact FL’s procedure gives for large volumes—precisely the domain in which we expect the order-splitting effect to be dominant—and therefore a downward bias for .

-

2.

Although we present new estimators to address this point, we believe FL’s argument to be incorrect since long-memory in order flow clearly does not imply the same for returns, so FL’s criticisms about our estimation procedure do not seem relevent. To address a potential problem of long memory in order flow, we draw from a new estimator for measuring market impact Plerou04 and extend our previous analysis to the 1000 largest NYSE stocks. Our new estimation confirms that the market impact function does behave as a square-root function of the volume.

-

3.

We analyze 262 largest stocks listed in the London Stock Exchange. Our analysis of volume distribution for these 262 stocks shows that the distribution of volume decays as a power-law with an exponent in agreement with our previous results for the NYSE and the Paris Bourse. In fact our analysis of the volume distribution for the same stocks analyzed by FL shows a clear power-law behavior with exponent — in contrast to FL’s claim.

Define as the price of the stock after trade ,

| (1) |

as the return concomitant to trade , so the return over a fixed time interval is

| (2) |

where is the number of trades in . Let be the number of shares traded in trade so

| (3) |

is the total volume in interval . We define the trade imbalance

| (4) |

where indicates a buyer-initiated trade and denotes a seller initiated trade. We denote by the size of a large order, which can be executed in several trades.

1. Measuring market impact

Let be the change in price caused by a large order of size , all else remaining the same. Our theoretical approachGabaix03 derives a power-law functional form for the market impact function noteimpactfn ,

| (5) |

We hypothesized and supported the hypothesis by empirical analysis.

Our hypothesis Eq. (5) pertains to , the total impact in price of a large order of size . In practice, as outlined in Ref. Gabaix03 , large orders are executed by splitting into orders of smaller size which are observed in the trade time series as the trade size . The empirical analysis of Refs. Farmer03 and Lillo03 refer to the relationship local price change and not the price impact that we are interested in. The true market impact function is indeed notoriously difficult to measure since the information about the unsplit order size is usually proprietary and not available, neither in our data nor in the data analyzed by FL.

FL claim that the price impact function grows more slowly than a square-root function for large volumes. The basis for their claim is the analysis presented in Ref. Lillo03 that with for small and for larger . While indeed grows less rapidly than a square-root, as reported in Ref. Plerou02 , neither quantifies price impact of large trades, nor does it contradict our theory and empirical results Gabaix03 . This is because a trade by trade analysis of leads to a biased measurement of full price impact and the exponent , since it does not take into account the splitting of trades Gabaix03 ; Gabaix04 .

Consider an example. Suppose that a large fund wants to buy a large number of shares of a stock whose price is $100. The fund’s dealer may offer this large volume for a price of $101. Before this transaction, however, the dealer must buy the shares. The dealer will often do that progressively in many steps, say 10 in this example. In the first step, the dealer will buy shares, and the price will go say, from $100 to $100.1, and in the second the price will go from $100.1 to $100.2. After some time elapses, the price will have gone to $101 in increments of $0.1. At this stage, the dealer has his required number of shares, and hands them over to the fund manager at a price of $101. The true price impact here is 1%, since the price has gone from $100 to $101. But in any given transaction, the price has moved by no more than $0.1. So Ref. Farmer03 would find an “apparent” price impact of no more than $0.1, i.e. 0.1% of the price. Since as the transaction is executed the price of the stocks goes from $100 to $101, the true price impact is 1%. As a result the procedure of FL will measure a value 10 times smaller than the true value. This downward bias explains why FL find in Fig. 2 a maximum impact of 0.1%—a very small price impact. Other evidence in economics Chan95 ; Keim97 finds impacts that are up to 40 times larger than that of FL’s analysis. Likewise our evidence pertains to large impacts, captured by Fig. 2 of our paper which shows on the vertical axis values of equal up to times the variance , i.e., values of return up to standard deviations.

We can quantify the bias in the above example. Suppose that a trade of size is split into (10 in our example) trades of equal size , with . Then the apparent impact incurred by each trade (0.1 in our example) will be (1/10 in our example) of the total price impact (1% in our example), i.e. . So a power law fit of vs , such as the one presented in Fig. 2 of FL, will give with footnoteBetaLessThan1

The “trade by trade” measurement of the price impact, as performed by Ref. Farmer03 ; Lillo03 , leads to a biased measurement of the exponent of the true price impact.

It is to address this bias that we examine in Ref. Gabaix03 . As is well established empirically, the sign of returns is unpredictable in the short term, so the reasoning in Ref. Gabaix04 shows that will not be biased notetmp .

Our analysis Gabaix03 was presented with data for the 116 most actively traded stocks. To check if the result of for large volumes presented in Refs. Farmer03 and Lillo03 could arise from increasing the size of the database, we now extend our analysis to the 1000 largest stocks in our database for the 2-yr period 1994-95. Figure 1(a) confirms that as predicted by our theory.

![[Uncaptioned image]](/html/cond-mat/0403067/assets/x1.png)

![[Uncaptioned image]](/html/cond-mat/0403067/assets/x2.png)

2. Robustness of estimation against long-memory of order flow

FL argue that the empirical analysis that we presented in support of the square-root functional form of market impact is “invalidated” by the “long-memory nature of order flow”. FL’s argument is based entirely on the assumption that returns due to each transaction can be written as where for a buy trade and for a sell trade. Under this assumption, FL then argue that our estimator is affected by the long-range correlations in the trade signs Farmer03 ; Bouchaud04 . FL give some numerical evidence for this potential effect for small to moderate volumes.

![[Uncaptioned image]](/html/cond-mat/0403067/assets/x4.png)

![[Uncaptioned image]](/html/cond-mat/0403067/assets/x5.png)

All of the tests shown by FL are for a fictitious return constructed on a trade-by-trade basis as . FL’s argument and the tests shown in Fig. 1 of FL are for the fictitious return. In reality, return can certainly not be expressed as , with being the trade indicator. Indeed, if this were true, returns themselves would be long-range correlated—a possibility long known to be at odds with empirical data. Since the sign of the return and that of the trade sign are clearly not equal, FL’s argument about our estimation procedure being affected by the long-memory nature of the trade sign () is incorrect (See Ref. Bouchaud04 on a related point).

![[Uncaptioned image]](/html/cond-mat/0403067/assets/x6.png)

Although FL’s argument is incorrect, to address the more general concern that the autocorrelations of the trade signs might bias our analysis, we draw from a forthcoming paper Plerou04 , which performs the following analysis footnoteSplitMatters . For each intervl define as the size of the largest trade. In our theory, if the largest trade is large, it will have a the major influence on the value of return, so that one will have . Hence gives us a diagnostic value of the behavior of the largest trade, independently of a potential collective behavior. We detail this in Ref. Plerou04 . We compute and find [Fig. 1(b)].

| (6) |

In addition to the above, to ensure that our estimation is robust to varying number of trades in a fixed , we have computed for fixed number of trades instead. Figure 1(c) shows that for over trades.

We would like to emphasize that in Fig. 1 we consider very large trades that are up to 70 times the first moment of volume. They correspond to returns of up to 14 standard deviations of returns. This confirms that we study very large trades and returns—the ones that are relevant for the study of power law fluctuations, while in contrast FL’s analysis does not systematically treat large trades.

We conclude that the procedure used in Ref. Farmer03 has a downward bias of the price impact of large trades. When we perform more appropriate analysis, we confirm that the . This corroborates our hypothesis Gabaix03 ; Gabaix04 that large fluctuations in volume cause large fluctuations of prices.

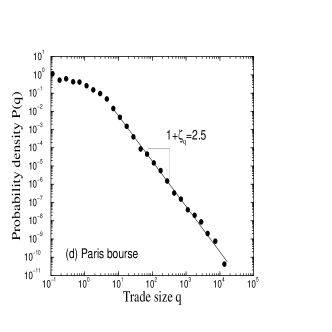

3. Half-cubic power-law distribution of volumes

The last claim of FL pertains to the very nature of the volume distribution. They present the results of their analysis of three stocks in the London Stock Exchange and claim their analysis shows no evidence for a power-law distribution.

We analyze the same database which records all trades for all stocks listed in the London Stock Exchange. From this database, we first examine one stock – Vodafone, VOD — which is analyzed by FL. For this stock, we compute the volume distribution and find clear evidence for a power-law decay [Fig. 2(a)]

| (7) |

with exponent , in agreement with our previous results for the NYSE and the Paris Bourse Gopi00 ; Gabaix03 , but in sharp contrast to the FL results who claim a thin-tailed distribution for the same data.

For the 10 largest stocks in our sample, Fig. 2(b) shows that is consistent with the same power-law of —consistent with our earlier finding for the NYSE Gopi00 . We extend our analysis to the 265 largest LSE stocks and find similar results [Fig. 2(c)].

To test the universal nature of this distribution, we analyze data for 30 largest stocks listed in the Paris Bourse and find that is consistent with the a power-law with almost identical exponents [Fig. 2(d)].

In summary, the analysis of Ref. Farmer03 pertains to small to moderate trades. FL’s estimation is biased for large trades, so FL can detect only very small price impacts, less than 0.1%. When we use our more general procedure and study significantly larger data, we confirm our initial finding of a square root price impact function. We conclude that the available evidence is consistent with our hypothesis Gabaix03 ; Gabaix04 that large fluctuations the volume traded by large market participants may contribute significantly to the large fluctuations in stock prices Plerou04 .

Acknowledgments. We thank the NSF’s economics program for financial support, and Joel Hasbrouck, Carl Hopman, Gideon Saar, Jeff Wurgler and especially Gilles Zumbach for helpful conversations and help with obtaining the data analyzed.

Note added in press: After our initial submission, it has become clear that FL’s claim of a non-power-law distribution of trade sizes [2] for the LSE stocks is based on incomplete data. FL’s analysis excludes the upstairs market blockTrades trades which contain the largest trades in the LSE. In contrast, our result of a 3/2 power-law exponent for the volume distribution is based on data containing all trades (both the upstairs and the downstairs market trades) in the LSE. By excluding the large trades in the upstairs market, FL set an artificial truncation at large volume, so FL’s finding of a non-power-law distribution of volume is merely a trivial artifact of incomplete data. Although FL claim in their note added that “it has been shown that large price fluctuations in the NYSE (including the upstairs market) and the electronic portion of the LSE are driven by fluctuations in liquidity” their new analysis and findings are tainted by the same problems as in their present comment: (i) incompleteness (absence of the upstairs market trades) of the data analyzed and (ii) they do not take into account the splitting of large orders.

Gabaix et al. Gabaix03 ; Gabaix04 and FL Farmer03 discuss two distinct possibilities respectively: (i) large price changes arise from large trades and (ii) large price changes arise from fluctuations in liquidity Plerou02 ; Plerou00 . While we believe that both mechanisms play a role in determining the statistics of price changes, our empirical findings support the possibility that the specific power-law form of the return distribution arises from large trades.

References

- (1) Gabaix, X., Gopikrishnan, P., Plerou, V. & Stanley, H.E. A theory of power law distributions in financial market fluctuations. Nature 423, 267-70 (2003).

- (2) Farmer, J.D., Lillo, F. “On the origins of power laws in financial markets.” Quantitative Fin., this issue, (2004).

- (3) Plerou, V., Gopikrishnan, P., Gabaix, X. & Stanley, H. E. On the relation between very large trades and very large price movements. Manuscript (2004).

- (4) Lillo, F., Farmer, J.D. & Mantegna, R.N. Master curve for price-impact function. Nature 421, 129-130 (2003).

- (5) Gabaix, X., Gopikrishnan, P., Plerou, V. & Stanley, H.E. A theory of large movements in stock market activity. Manuscript.

- (6) The inequality below holds if . There is wide agreement that should be no greater than . This is because the power law exponent of returns and the power law exponent of volumes satisfy Gabaix03 , so that the empirical values imply .

- (7) We are detailing the foundations of this analysis in Ref. Plerou04 . The specifics of the split matter in principle. In Ref. Gabaix03 we present a theory of power law splitting in which the size of the largest chunk, , is proportinal to the size of the entire order, .

- (8) As in Ref. Gabaix03 , we interpret to mean that there exist a slowly varying function such that for large , . A function is called slowly varying when for all , . Typical slowly varying functions are , or logarithmic corrections: , where and are constants.

- (9) Our theory is one of large trades. The evidence presented in Ref. Farmer03 pertains to small to moderate size trades. It follows a long tradition pioneered by Ref. Hasbrouck91 (see also Plerou02 ; Bouchaud04 ), and may be fine for small to moderate trades. The issue of splitting may be less important for those trades, but it is almost certainly crucial for large ones (e.g., trades bigger than 5 to 10 times the average trade size). This is why the trade by trade measurement has a downward bias for large trade, which is avoided when we take .

- (10) Hasbrouck, J. Measuring the information content of stock trades. J. Fin. 46, 179–207 (1991).

- (11) Chan, L. & Lakonishok, J. The behavior of stock prices around institutional trades. J. Fin. 50, 1147–1174 (1995).

- (12) Keim, D. & Madhavan, A. Transactions costs and investment style An inter-exchange analysis of institutional equity trades. J. Fin. Econ. 46, 265–292 (1997).

- (13) Gopikrishnan, P., Plerou, V., Gabaix, X. & Stanley, H. E. Statistical Properties of Share Volume Traded in Financial Markets, Phys. Rev. E 62, R4493-R4496 (2000).

- (14) Plerou, V., Gopikrishnan, P., Gabaix, X. & Stanley, H. E. Quantifying stock price response to demand fluctuations. Phys. Rev. E 66, 027104 (2002).

- (15) Bouchaud, J.P., Gefen, Y., Potters, M. & Matthieu, M. Fluctuations and response in financial markets: the subtle nature of ’random’ price impact. Quantitative Fin. (2004).

- (16) Large trades tend to be executed in the “upstairs” market by bilateral arrangements than through the order book.

- (17) Plerou, Vasiliki, Parameswaran Gopikrishnan, Luis Amaral, Xavier Gabaix, and H. Eugene Stanley “Economic Fluctuations and Anomalous Diffusion”, Phys. Rev. E (Rapid Comm.) 62, R3023-3026 (2000).