Ehrenfest Model with Large Jumps in Finance

Abstract

Changes (returns) in stock index prices and exchange rates for currencies are argued, based on empirical data, to obey a stable distribution with characteristic exponent for short sampling intervals and a Gaussian distribution for long sampling intervals. In order to explain this phenomenon, an Ehrenfest model with large jumps (ELJ) is introduced to explain the empirical density function of price changes for both short and long sampling intervals.

keywords:

Lévy stable process; Ehrenfest model; FinancePACS:

02.50.-r; 05.45.Tp; 89.65.Gh1 Introduction

This paper introduces a simple stochastic model, an Ehrenfest model with large jumps (ELJ), to explain the observed fact that the density function of price change fits well to a symmetrical Lévy stable distribution near the central part of the density function, while it has a truncated tail far from the center [7]. The proposed model also explains that it is close to a Gaussian distribution for long sampling intervals.

Changes in stock prices and exchange rates for currencies are one of the best examples to which the random walk concept is applicable [5]. We have seen a lot of work of related topics since the work of L. Bachelier in 1900. In financial theory such as the argument on the Black-Scholes model, the distribution of (logarithmic) stock returns is assumed to be Gaussian. It seems that this assumption is well accepted for a long sampling interval of empirical data, namely those for sampling intervals of several days, a week or longer.

In the case of a short sampling interval of empirical data, i.e. those for sampling intervals of several seconds, minutes or hours, the price returns are not distributed according to a Gaussian law [2]. The value of for the empirical density function of the S&P500 index estimated for short sampling intervals indicates that the density function follows a stable law () [7, 8].

The price changes are therefore said to be distributed according to a stable law with a characteristic exponent for short sampling intervals, and a Gaussian distribution () for long sampling intervals [3].

2 Ehrenfest model with large jumps

The Ehrenfest model [1, 4] envisages two boxes and , with particles distributed in these boxes. A particle is chosen at random and moved from one box to the other and the same procedure is repeated.

We consider a generalized Ehrenfest model in which steps of the Ehrenfest model take place with probability at each step, where and is a normalization constant defined by:

For simplicity, is fixed to be 1 in the following discussion. This generalized model becomes identical to the original Ehrenfest model in the limit .

Suppose that initially there are () particles in box , after repeating the above procedure times, there are particles in box . The probability of this event calculated in case of the original Ehrenfest model [6] can be described as:

| (1) |

where

With the duration of each step for the original Ehrenfest model defined as , consider a particle moving along the -axis in such a way that at the time it is located at . In the diffusion limit:

we have

where

| (2) |

We denote the particle number in the box after steps as , and define the changes as:

where denotes the step interval. Using the above , we define the empirical density as:

| (3) |

where and denotes the Kronecker delta.

Using Eq. (1), the probability density function of the changes for the proposed model is expressed as:

| (4) | |||||

where = 0,1,2,…. Using the diffusion approximation, the above equation can be approximated by Eq. (6).

Assuming that the initial density function is given by a Gaussian density function , the probability density function of the change in the original Ehrenfest model, obtained from the diffusion approximation (2), is given by:

| (5) | |||||

where is the Dirac delta function. The variance of the change is given by:

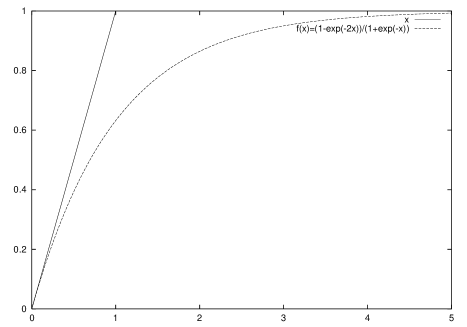

Figure 1 shows the behavior of the function:

From this figure, we find that when both and are sufficiently large, the difference remains small, even if and are very different.

The time series of the ELJ is interpreted as a time series chosen randomly from that of the original Ehrenfest model. Using Eq. (5), the probability density function of the ELJ is approximated as:

| (6) | |||||

and the variance as:

| (7) | |||||

When is large, the density of ELJ in Eq. (6) will be approximately given by:

with

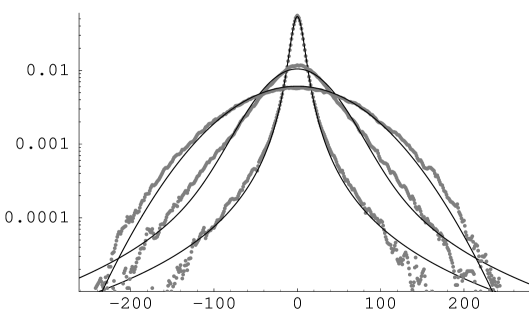

where of the summation is an integer satisfying the condition . From the above equation, we find that the density of the proposed model decays in proportion to toward the end of the tail as seen in Fig. 3 (a), whereas in Fig. 3 (b), the tail decays in proportion to to mid-way when is small.

The Lévy stable symmetrical density function is given by:

| (8) |

for the characteristic exponent ( ) and positive scale factor . This reduces to a Gaussian density function when = 2. The Lévy stable density is characterized by a fat tail and kurtosis, is consistent with empirical data, and satisfies a scaling law. It is one of the most natural generalization of the Gaussian distribution which is stable with respect to convolution.

From Eq. (6), we find the reason that the stable density function is chosen for the best fitting density function of the proposed model for shorter by the maximum likelihood method that we will explain later. The large coefficient of in the exponential function gives a sharper peak at the origin, in contrast, the small coefficient of affords a flatter peak, broadening the density function. Therefore, the density function given by the sum of these two types of terms with dissimilar coefficients has a fatter tail than the Gaussian density function.

When is sufficiently large, the density function on proposed model becomes the sum of the Gaussian density functions of almost the same shape. Therefore, the density function in the proposed model is given by the Gaussian density function for longer sampling intervals.

The proposed model well describes the changes in the stock indices such as the S&P500, TOPIX and currency exchange rates. Let each particle in the box represent a buy stance dealer and each particle in the box represent a sell stance dealer. These dealers will get a lot of information from a newspaper, television, radio, business reports etc. on business conditions, weather reports, governmental decisions etc. and their view will be changed from buy to sell or from sell to buy on the basis of such information. These changes will generate a change in the stock price or the exchange rate. We assume that a change in the dealer’s mind directly causes a change in the price so that is interpreted as the price.

As the information is spatially and temporally distributed, and any piece of information may have a different impact on the dealers, the price will sometimes change drastically within minutes, or sometimes only slightly over hours. The difference between the progress of time in the ELJ and in the original Ehrenfest model describes this phenomenon. The parameters and might thus represent the dealers’ (price change) sensitivity and frequency of information.

3 Maximum likelihood method

The maximum likelihood method [9] is employed to estimate parameters of the model. It is assume that a joint density function of the random variable is given, where the parameter specifies the density function. If the random variables are mutually independent, then the joint probability density function of is given as the product of the individual density functions of . Thus we have

Taking the logarithm on the right-hand side yields the log likelihood:

For the present case, the log likelihood is expressed as:

The maximum likelihood estimate of the parameters of the model is obtained by maximizing this quantity.

4 Numerical simulation

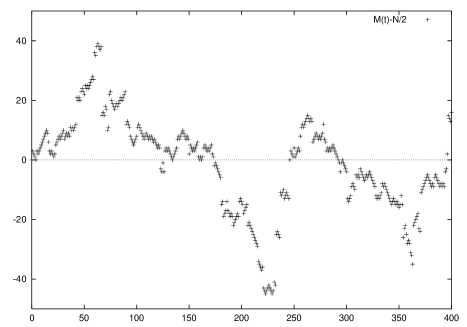

The results of a numerical simulation of the trajectory of is shown in Fig. 2, where , , and . Big jumps that do not exist in the original Ehrenfest model are observed in the proposed model. Because of these big jumps, the empirical density of the new model is a better fit to a stable distribution (), whereas the empirical density is given by a Gaussian distribution in the original Ehrenfest model.

(a)

(b)

In Fig. 3, the empirical density is shown for different time intervals 64, 512. These results were obtained for a sequence of about one million steps of the ELJ. The density obtained by simulation using the proposed model is well described by a symmetrical Lévy stable density function (8).

The parameters and of Eq. (8) estimated using the maximum likelihood method for different time intervals are shown in Table 1. In the model, increase to with increasing for different values of and , as can be clearly understood from Table 1. Here we used the results of numerical simulation and considered the numerical values for and for several values on , or in Table 1. However, the probability density function of the proposed model can be approximately given by Eq. (6).

| 16 | 32 | 64 | 128 | 256 | 512 | 1024 | ||

|---|---|---|---|---|---|---|---|---|

| 1.386 | 1.529 | 1.763 | 1.958 | 2.0 | 2.0 | 2.0 | ||

| 22.81 | 72.81 | 335.0 | 1285 | 2138 | 2418 | 2528 | ||

| 1.758 | 1.956 | 2.0 | 2.0 | 2.0 | 2.0 | 2.0 | ||

| 45.69 | 139.2 | 219.8 | 247.1 | 249.7 | 250.3 | 350.2 | ||

| 1.719 | 1.756 | 1.804 | 1.859 | 1.932 | 1.988 | 2.0 | ||

| 18.05 | 39.28 | 90.47 | 213.6 | 524.9 | 1155 | 1825 | ||

| 1.713 | 1.748 | 1.796 | 1.871 | 1.949 | 2.0 | 2.0 | ||

| 15.80 | 34.18 | 7813 | 196.6 | 493.7 | 1080 | 1685 |

Consider a density function given by a combination of an infinite number of Gaussian density functions:

| (9) |

It is easy to confirm from the knowledge of domains of attraction [4] that the density function of the above equation belongs to the domain of attraction of the symmetrical Lévy stable density with characteristic exponent given by:

| (10) |

The density functions given by Eqs. (6) and (9) are identical under a first order approximation in the limit and . Therefore, the symmetrical Lévy stable density with characteristic exponent given by Eq. (10) fits the density function (6) well as far as the central part of the density function of the ELJ is concerned.

5 Exchange rate

In ordered to discuss the empirical density function, we should redefine the empirical density function as a continuance version. Price changes (returns) are defined by:

where is the price at time and is a time interval. The empirical density function is then defined by:

where is the Dirac delta function and takes , = 1, 2,…,.

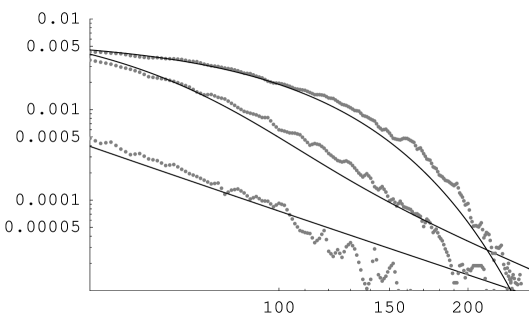

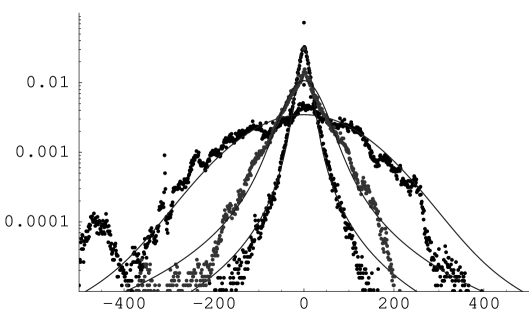

The empirical density of the exchange rate between the US dollar and the Japanese yen over one year (Jan. ’94-Dec. ’94) [10] is shown in Fig. 4, along with the estimated stable density functions. This figure shows that the empirical density is close to the stable distribution with a characteristic exponent for short sampling intervals and a Gaussian distribution for long sampling intervals. Table 2 shows the maximum log likelihood estimate of and . When the sampling interval is small, the return is distributed according to a stable law with characteristic exponent . In addition, becomes larger with expansion of the sampling interval and approaches 2. Similar results were obtained for German stocks [3].

(sen)

| 1.436 | 1.451 | 1.441 | 1.483 | 1.588 | 1.666 | 1.840 | 1.900 | |

| 13.84 | 24.86 | 38.95 | 75.46 | 184.5 | 431.75 | 1743 | 4276 |

6 Concluding remarks

This paper introduced a simple stochastic model (ELJ) to understand that the observed density function of the price change is approximately given by a truncated symmetrical Lévy stable distribution for short sampling intervals and a Gaussian distribution for long sampling intervals.

The elastic potential of the Ehrenfest model makes the tail of the density function decay rapider than that of the Lévy stable density. The empirical density function of the price change should not have an infinitely long heavy tail. Thus, the empirical density function given by Eq. (6) seems to be reasonable.

Acknowledgement

The author would like to thank Professors Y. Itoh, G. Kitagwa, T. Ozaki, M. Taiji and Y. Tamura for helpful suggestions and comments.

References

- [1] Aoki, M. (1996) New Approaches to Macroeconomic Modeling (Cambridge University Press, New York).

- [2] Barndorff-Nielsen, O. E. and Shephard N., J. R. Statist. Soc. B 63, 167 (2001).

- [3] Eberlein, E. and Keller, U., Bernoulli, 1, 281-299 (1995).

- [4] Feller, W., An Introduction to Probability Theory and Its Applications II, 2nd ed. (John Wiley & Son, New York,1973).

- [5] Hull, J. C., Options, Futures, & Other Derivatives, 4th ed. (Prentice-Hall International, Inc., London, 2000).

- [6] Kac, M., Amer. Math. Monthly 54, 369 (1947).

- [7] Mantegna, Rosario N. and Stanley, H. Eugene, Nature 376 46 (1995).

- [8] Mantegna, Rosario N. and Stanley, H. Eugene, J. Stat. Phys. 89 469 (1997).

- [9] Sakamoto, Y., Ishiguro, M. and Kitagawa, G.: Akaike Information Criterion Statistics (Kluwer Academic Publishers, Tokyo, 1986).

- [10] Data were purchased from Olsen & Associate.