Real payoffs and virtual trading in agent based market models

Abstract

The $-Game was recently introduced as an extension of the Minority Game. In this paper we compare this model with the well know Minority Game and the Majority Game models. Due to the inter-temporal nature of the market payoff, we introduce a two step transaction with single and mixed group of interacting traders. When the population is composed of two different group of $-traders, they show an anti-imitative behavior. However, when they interact with minority or majority players the $-population imitates the usual behavior of these players. Finally we discuss how these models contribute to clarify the market mechanism.

keywords:

$-Game, Minority Game, Majority Game, Round-trip transaction and Mixed Models.PACS:

02.50.le, 87.23.ge, 89.65.sand

1 Introduction

The Minority Game (MG) [1]has addressed many issues to understand complex systems with special emphasis on modelling market mechanism. Although the Minority Game is a very simple model, it contains the main ingredients to reproduce a rich behavior such as that observed in financial market [2]. These features arise from relatively simple rules used to define the interaction of agents. In particular the MG assumes that market interaction is such that it pays to be in the minority. This assumption was recently challenged by Andersen and Sornette [3] who derived a different market payoff considering the profits of round-trip transactions (buy/sell or sell/buy). A round-trip requires at least 2 transactions and hence the market payoff depends on the price at two different times, i.e. on the action of traders at different times. The traders in the model introduced by Andersen and Sornette, called $-Game model, use this market payoff to judge the performance of their strategies. This leads to a market behavior which is very different from that of the Minority Game. In particular traders using the correct market payoff are found to perform better than those who base their behavior on the MG payoff. This models was analyzed also by Jefferies and Johnson [4, 5], that discuss different aspects of market models.

A key observation is that, in the $-game the real market payoff is assessed on the basis of virtual trading: round trip transactions are used to evaluate trading strategy, but they are not actually implemented by traders. For example, if an agent bought some shares of asset at time , she/he will consider the virtual payoff of selling these shares at the current price at time , without actually selling it. Using virtual trades to asses market payoff might be a realistic behavioral assumption. Irrespective of this, a key issue is to understand what are the consequences of this assumption on the collective behavior of the market. More precisely, how does market’s behavior differs if agents use virtual or real trades to asses market payoffs?

The naïve arguments which suggests that the difference is very small, contends that prices depend very weakly on a particular trader’s transaction. Whether a transaction was really carried out or not should not affect much the aggregate behavior. These type of arguments are known to be problematic in heterogeneous agent market models, and indeed fail both in the majority [11] and in the minority game [12] as well as in other asset market models [13]. In other words, while the impact of each trader may be small on the aggregate, the effect of all traders neglecting their impact can be dramatic.

We shall come to a quite similar conclusion, namely that virtual or real trading makes a difference in market’s behavior. More precisely, we show that when agents use round-trip transactions both in the definition of market payoff and in their actual behavior we recover a behavior which is similar to that of the MG. Indeed round-trip transactions induces anti-correlations in market returns and Ref. [6] show that market payoff reduces to those assumed in the MG when the market returns are anti-correlated.

In order to do this we need to introduce slightly more complex models based on two times: decision making consists on a round-trip action where the agents decide to buy or sell at time and do the opposite (sell or buy) at time , then they evaluate the result in the next time step. In addition to this we also aim to studying the interaction between different types of traders, using the minority, majority or $-Game payoff.

The paper is organized as follows: in section 2 we derived the market payoff following Ref. [3, 6] and we discuss the key observable. Then we analyze single time models in section 3 and then we move to two times models in section 4. Homogeneous populations and mixed populations are studied. Finally we give some concluding remarks in section 5.

2 Market Payoff

Now we will derive the minority and the majority mechanism from the market’s dynamics. A single step in the Minority Game model could be split in three stages. First of all, at time the agent submits an order (buy or sell) that is going to be useful in computing the aggregate value , at time . At time the agents update their experience simply by evaluating the success of their action. Focusing on one agent , we can assert that if he/she contributes with 1$ to the market demand and if he/she contributes with for the supply where is the price of the cost transaction. The total demand and supply are given by and units of assets respectively. Then following the paper [6], let’s fix the price in such a way that the demand matches the supply, i.e.,

| (1) |

Let’s discuss how the market payoff is defined. To reward someone for their decisions we need to wait at least two successive transactions. For example, if one buys a stock for the price only later, at time when the price will be , we are able to know if buying was profitable. So the market payoff has an inter-temporal nature which depends at least on two prices. We can consider for agent the capital , which quantifies the agent wealth at each time step. This quantity depends on the the amount of money and asset which she/he owns at time , and the current price .

Suppose the agent decides to buy stocks at price , so the position changes to and . Alternatively, if the decision was to sell stocks, so and . In a compact way, we can express the same result as

| (2) | |||||

| (3) |

After a simple algebra we obtain the capital increment,

| (4) |

which means that there is no gain from a single transaction apart from capital gain. Then gain is due to a price changing. Now consider that . This results in:

| (5) | |||||

| (6) |

The capital will be update by

| (7) |

where

| (8) |

are constants of order 1 if .

Note that in Eq. (7) the first term corresponds to the capital gain. From the second term we derive the payoff update

| (9) |

as proposed by Andersen, et.al [3]. Previously, Giardina, et. al [18] proposed a quite similar payoff function on their models. Ref. [6] observes that, at time the agent doesn’t know the excess demand . However he/she may resort to the expectation given by the operator to evaluate the best decision to make on time . Assuming that

| (10) |

where linearity is assumed for the sake of simplicity, the expected payoffs increment of agent is

| (11) |

The stationary state can only occur when the expectation is consistently validated by the dynamics as show in [6], i.e., when

| (12) |

for all . If the agent believes that the price fluctuates around some equilibrium (fundamental) values . This trader is called fundamentalist and as we can see in the Eq. (11) she/he plays as a Minority Game player for whom the payoff is

| (13) |

On the contrary, if the agent believes that the price is following a trend, a movement will likely be followed by fluctuations of the same sign, i.e, . These agents, called chartists, play like in a Majority Game () and the payoff is just

| (14) |

Whether -Game is approximate by Minority Game or Majority Game depends on the sign of . We shall use the superscript in the following to differentiate the results found in the different models.

3 Single Time Models

In this section we will discuss three agent models that simulate different trader’s behaviors and interactions in the stock exchange market. The set up are the same for all models, differing only by the payoff function that ranks their strategies. In a generic description, consider odd agents that buy or sell stocks, goods, currencies, etc…, to profit from the market price fluctuation. Suppose is a discrete time. Each trader is endowed by S quenched strategies randomly generated at the beginning. To each strategy each trader attaches a score which she/he updates in the course of time. At each time , she/he undertakes the action recommended by the highest scored strategy . The action taken by agent also depend on the value of a public information variable. After that, all these orders are collected to compose the excess demand . Finally all agents update all the payoff function according to Eq. (9), (13) or (14) respectively for $-Game, Minority Game or Majority Game. The information is updated according to the outcome of the market:

| (15) |

Note that never occur when N is odd. In this way encodes in its binary representation the signs of the last outcomes of the market. Graphically Eq. (15) describes a processes on the so called de-Bruijn graph. This is a directed graph of nodes with directed links from nodes to nodes and [7].

To fix notation, we denote a temporal average of a given time dependent quantity as

| (16) |

If we decompose this quantity into a conditional average on histories, we rewrite as

| (17) |

Finally the average on the realization is denoted by

| (18) |

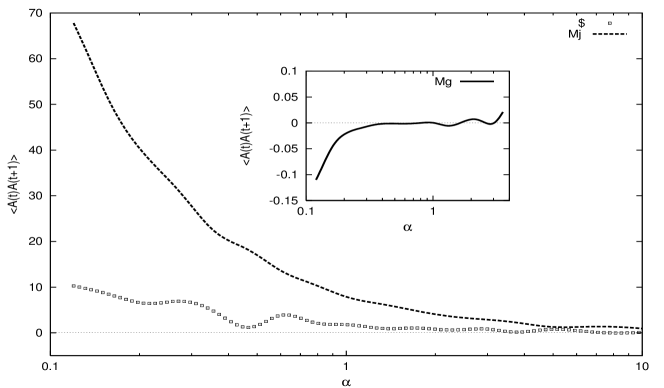

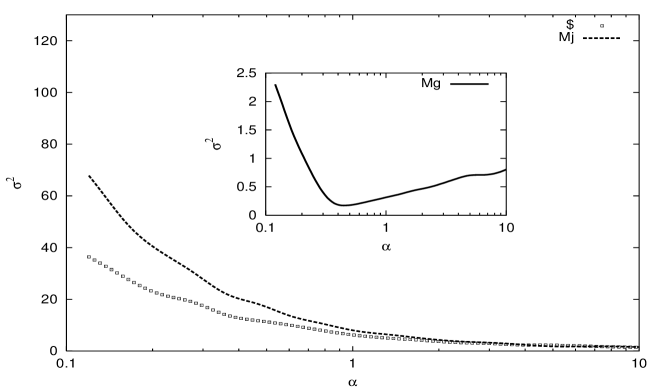

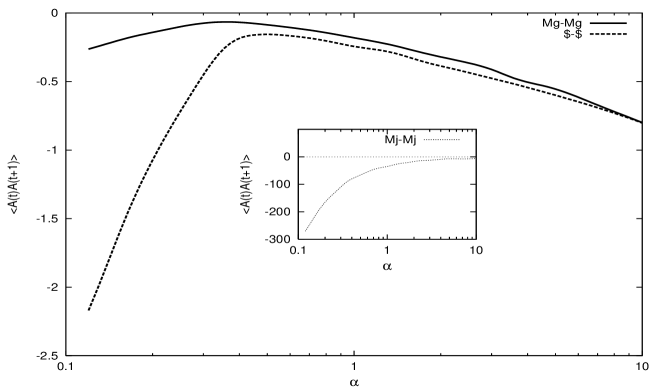

where is the number of realization. The main free parameter to study the stationary state of the system is (see [8]). Let us now analyze the behavior of the different models. The autocorrelation is the key to explain the others quantities for single models and to understand the trader behavior. In the Fig. 1 the autocorrelation of the global action for the Minority Game is plotted as a function of for memory . All runs were equilibrated for times steps and run for 30000 times steps. We fix attention to the case of agents with strategies. For the Minority Game the autocorrelation is zero for much large than the critical point and the global performance is similar to the random game. This happens because the number of players is small compared with the amount of information available in the market (for a discussion of Minority Game behavior see Ref. [8]. Increasing the number of traders, globally they start to exploit the information and coordinate their action until the occurrence of a phase transition. Intrinsically minority players have a non imitative behavior, thus the autocorrelation becomes negative below the critical point. Conversely, the majority players are trend follower and they induce a positive autocorrelation in , see Fig. 1. What can we expect for -Game? Fig. 1 shows that the $-Game is characterized by a positive autocorrelation . Hence we expect(see Eq. (12)) that the $-Game behaves in a way which is similar to the Majority Game. Fig. 2 supports this conclusion by comparing, for the different models, the behavior of given by

| (19) |

If you consider that persist to be positive for some period. All those strategies that is playing with will be reinforce due to the payoff . Conversely, all those strategies with will be weakened. The collective tendency of the traders is to reach a regime where they play with the same strategy. It is very similar to what happens for MJ-Model (for more details discussion of this models, see Ref. [11]). The $-players persist to be in a majority group keeping the same strategy for long. The Fig. 3, exhibits these results clearly by reporting the self-overlap given by:

| (20) |

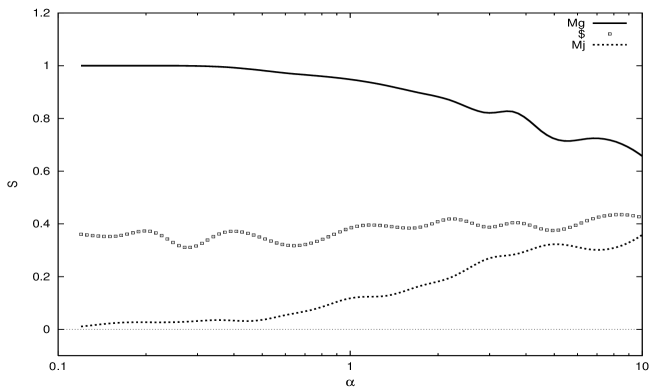

This is a measure of the average fluctuation in the strategy choice. The strategies are labelled by , thus when it means that the players are frozen, i.e they always use the same strategy. This is what we observe in the MJ-Model. Fig. 3 shows that this happens also in $-Game-Model showing that it is modelling a similar market mechanism. On the contrary in the Minority Game we observe which means that the players are changing the strategies frequently. As a consequence of this, the returns in the Minority Game are not predictable. This is measured by the quantity called predictability which is computed as

| (21) |

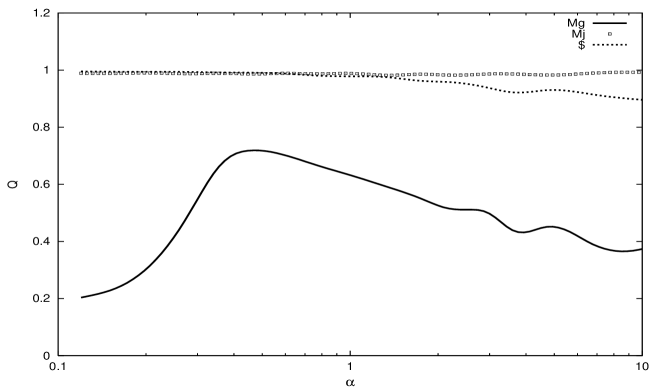

where is the probability that . In Fig. 5 we observe that the predictability is zero when starts to decrease. It is known that for the Minority Game the existence of a phase transition for and the region where is called symmetric phase [10]. Observe that implies for all . In this regime is not possible to predict the minority group based on the public information , this property is known by economist as no arbitrage. For the other models (MJ and $-Game) for all value of , that results from the fact that for some value of . Of course, when the strategy of the agents are frozen the game become predictable.

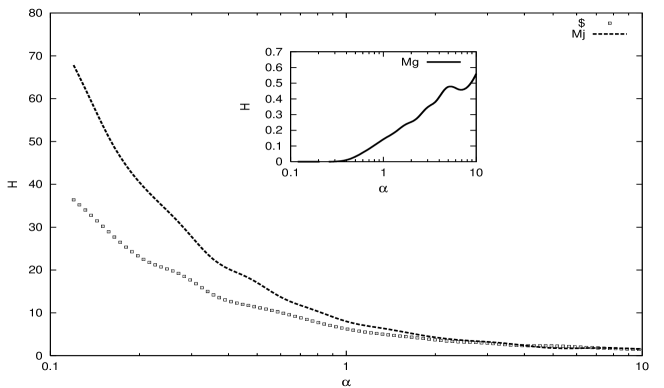

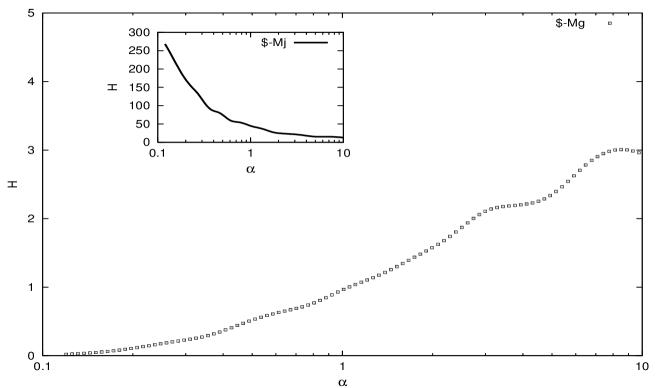

In Fig. 4, we examine the entropy for all these models given by

| (22) |

Note that was normalized to be in the interval . This quantity help us to analyze the dynamics of information in the De-Bruijn graph. The MG dynamics visits all nodes in the graph more or less uniformly. Hence and is closed to one. In both the Majority Game and the $-Game we find that is smaller, this means that only few vertices are visited. The $-Game and MJ have a dynamics restricted to some subgraph, i.e., only a subset of vertices are visited in the stationary regime, resulting in a small value of the entropy .

4 Two Times Models

Let us consider now the models whose dynamics takes place over two time steps. Any particular agent first decides which action to take (buy/sell) at time – according to his/her currently best strategy – then takes the opposite action at time and finally evaluates the results according to Eq. (9), (13) or (14) depending on whether he/she behaves according to the $, minority or majority game respectively. If all agents behave synchronously, we just have that and it is clear that the $-Game payoffs become exactly identical to MG payoffs. Therefore the $-Game becomes identical with the MG.

The non-trivial case is when agents act non-synchronously. This means that we can classify agents into two groups, one of which takes decisions on even times and evaluates the outcome on odd times and the other which does the opposite. Our previous argument suggests that when one group is much larger than the other, then and the game’s behavior becomes that of the MG. For this reason, we consider extreme case of equally sized groups.

More precisely, we divide the set of agents into two sets and of agents111Now is even. Concerning Eq. (15) when we set or at random, with equal probability., and postulate that, at time , group takes a fresh decision whereas the group reacts, i.e. takes an action which is just the opposite of the one they undertook in the previous time step.

The interaction takes place again through the total excess demand which has now two contributions from the two groups:

| (23) |

where we introduced a different notation for the contribution () of the acting group and for that () of the reacting one.

We will first considering how agents using the different scoring rules (9, 13) and (14) behave when they interact among themselves. Then we shall study the behavior of $-players when they are put in interaction with minority or majority players in a mixed population.

4.1 Single population

We analyze the situation where each agent in each of the two different groups of traders is endowed with a set of strategies which are randomly drawn at the beginning.

The numerical analysis reveals that i) the behavior of a pure population of either minority or majority players is equivalent to that observed for a single times models ii) the behavior of the $-Game is similar to that of the MG.

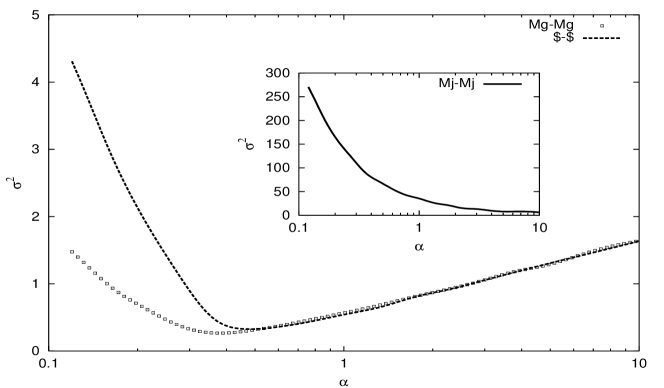

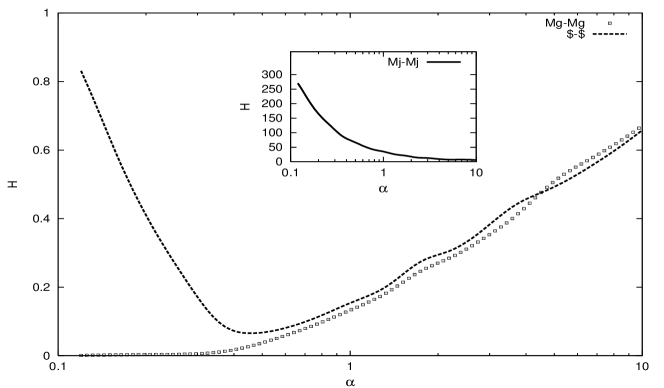

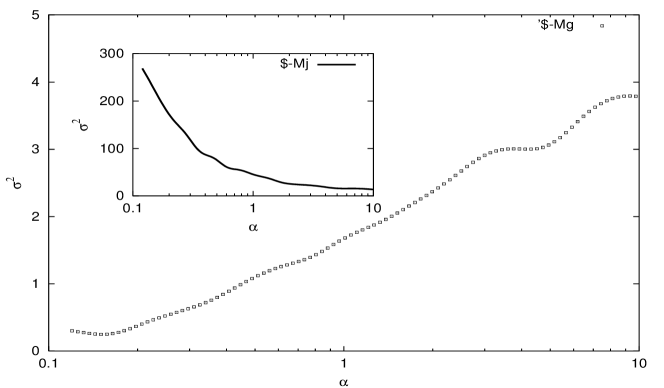

For example, the volatility shows (see Fig. 7) the typical minimum for the MG whereas it steadily increases as decreases in the case of majority players. In Fig 8 we see that most players get frozen () for MJ while the choice of the strategies remains fickle () for minority players, in agreement with the behavior of the corresponding single time models. In the case of $-players, both quantities ( and ) show a behavior similar to that of the MG. The same is true for the entropy , as shown in Fig. 9.

Indeed, for all models analyzed here, the autocorrelation of is negative, as shown in Fig 6. This is a consequence of the alternating behavior of agents. In fact the main contribution is due to the term (notice that has the same behavior as ).

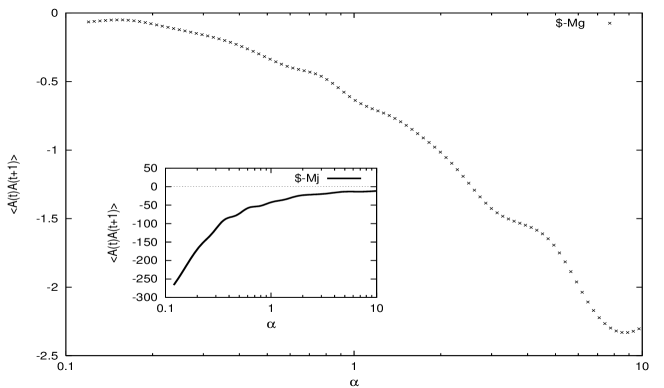

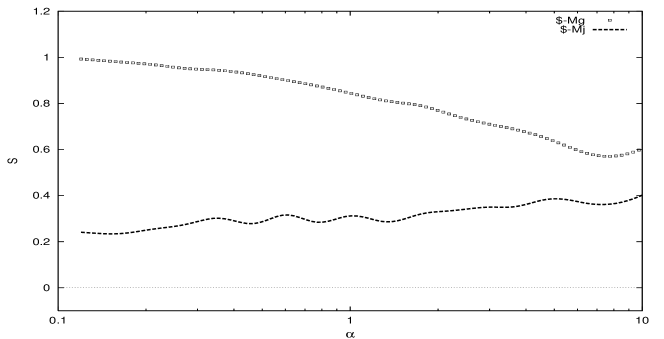

The only difference between $-Game and MG appears in the behavior of . Fig. 10 shows that vanishes when in a population of minority players (because ) whereas increases for majority players (and ). This is in line with the behavior of single time models. The behavior of for the $-Game closely matches that of the MG for but it diverges from it when . This is a consequence of the fact that while , (with ) in the MG, we find that and are uncorrelated in the $-Game. It is remarkable that when the process of Eq. (15) is replaced by random draw, as in Ref. [14], the predictability of the two models coincides. This is because then for all when is small.

4.2 Mixed population

In order to test further the behavior of $-game players, let us consider how they interact with minority or majority players in a mixed population. Specifically we split each of the two groups in two equal sizes (now is a multiple of ). Here and label the type of players in the sub-group. So for example denotes the case where a population of $-players interacts with a population of minority players. Again the interaction is on two times, but now we have two contributions to and from the two sub-populations.

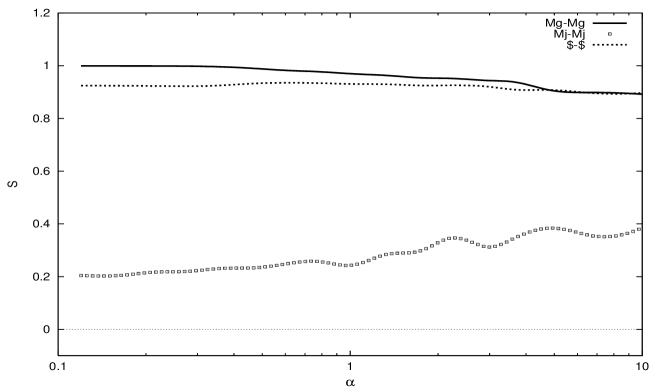

We have studied interaction of $-players with minority or majority players (i.e. and or ). The mixed Minority-Majority model was studied by De Martino, et.al [9]. We found that the autocorrelation is always negative in both cases (see Fig. 11). In the case , we find again that the autocorrelation is proportional to . However contrary to the single population case, we find that when decreases the volatility decreases (at least down to , see of Fig. 12). On the contrary increases as decreases when $-players interact with majority players (see inset of Fig. 12). This suggests that collective behavior is dominated by the sub-population of minority or majority players. This is confirmed by the behavior of in Fig. 13, even though it appears that the presence of $-players removes the phase transition (or shifts it at least to ). This is more clearly evident in the behavior of in the inset of Fig. 15. When interacting with majority type players, $-players also get frozen (). But also the presence of $-players makes minority players much less fickle (). Hence $-players increase the efficiency of coordination of the minority players.

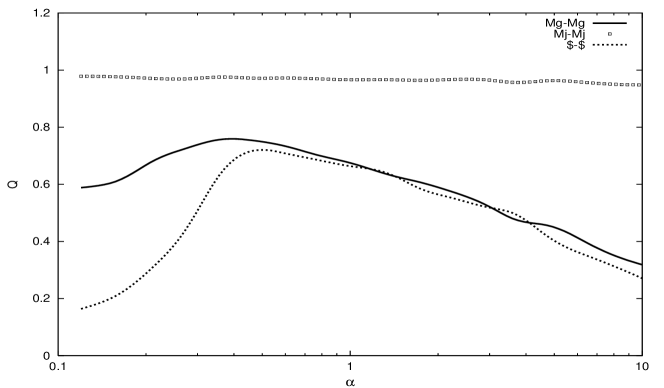

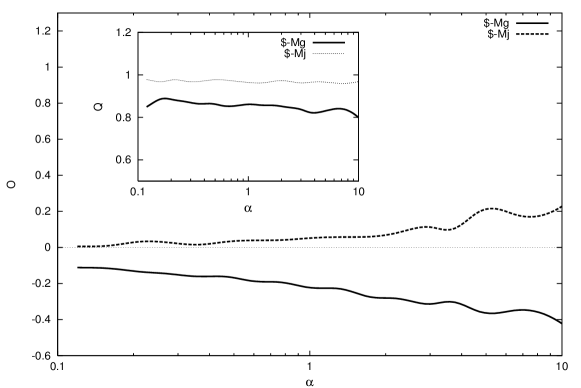

In order to compare the performance of agents of different types, we give the same set of strategies to the two sub-groups and . In particular we define the overlap

| (24) |

between types and . When () the two types of agents behave exactly in the same (opposite) way, whereas implies that agents of the two types behave in an uncorrelated way. Fig. 15 shows that $-players behave in a way which is more or less uncorrelated with majority players. On the contrary they display an anti-imitative behavior when interacting with minority players. It seems indeed reasonable that when minority game type of interaction prevails, as shown by the fact that the autocorrelation of is negative (see Fig. 11), two agents with the same strategies would benefit from playing in different ways.

Therefore we conclude that on one hand the collective behavior of a mixed population “imitates” the behavior of the population with which the $-player sub-population is interacting with. But at the microscopic level, the behavior of $-players tend to be loosely or negatively correlated with that of players of the other type.

5 Conclusions

The $-Game model reproduces the main statistical features observed for Majority Game whenever we consider a single times transaction. The $-traders freeze on the best strategy since the payoff reinforces an imitative behavior as seen from the positive autocorrelation of the excess of demand . When we take into account the inter-temporal nature of the transaction, we force all traders to react after all the transactions. To do so, we proposed a model where two populations interact over two time steps, taking decisions at different moments, out of phase. For two interacting homogeneous populations we saw that, when traders are all of minority or majority type, the same behavior as in single time models obtains. A population of $-traders shows an anti-imitative trend in the choices of strategies behaving as Minority Game players. Whatever the type of traders, the autocorrelation function of the excess demand turns out to be negative implying that the market interaction is similar to that of the minority game.

Also in the mixed composed population, the market interaction is of minority type, as shown by the autocorrelation of the excess demand. The collective behavior with $-traders interacting with a population of minority or majority traders is similar to that of the latter population.

In conclusion, we find that the $-Game model exhibits a set of new features and it poses several new and challenging questions.

References

- [1] D. Challet, Y.-C. Zhang, Emergence of cooperation and organization in an evolutionary Game, Physica A 246 (1997) 407–418.

- [2] Web site with a nice collection of papers and preprints on Econophysics: http://www.unifr.ch/econophysics.

- [3] J. V. Andersen and D. Sornette, The $-Game,Eur. Phys. J. B 31, 141-145 (2003).

- [4] P. Jefferies and N. F. Johnson, Designing agent-based market model,cond-mat/0207523.

- [5] N. F. Johnson, P. Jefferies and P. M. Hui , Financial Market Complexity, Oxford University Press, 2003.

- [6] M. Marsili, Market mechanism and expectation in minority and majority Games, PhysA 299 (2001) 93–103.

- [7] http://www.scs.carleton.ca/ dquesnel/papers/debruijn/paper.html This is a nice introdution of De Bruijn graph.

- [8] R. Savit et al., Adaptive Competition, Market Efficiency, Phase Transitions, PRL, 82(10), 2203 (1999).

- [9] A. De Martino, I. Giardina and G. Mosetti , Statistical mechanics of the mixed majority-minority Game with random external cond-mat/0305625.

- [10] D. Challet, Y. C. Zhang, On the minority Game: analytical and numerical studies, Physica A 256 (1998) 514–532.

- [11] P. Kozlowski and M. Marsili, Statistical Mechanics of Majority Game, J. Phys. A 36 11725 (2003).

- [12] D. Challet, M. Marsili, and R. Zecchina, Phys. Rev. Lett. 84, 1824 (2000); M. Marsili, D. Challet, and R. Zecchina, Physica A 280, 522 (2000).

- [13] J. Berg et al, Statistical mechanics of asset markets with private information Quant. Fin. 1 203-211 (2001).

- [14] A. Cavagna, Irrelevance of memory in the Minority Game, Phys. Rev. E 59, R3783 (1999).

- [15] Y.-C. Zhang, Modeling market mechanism with evolutionary Games, Europhys. News 29 (1998) 51.

- [16] D. Challet, M. Marsili, Y.-C. Zhang, Stylized facts of financial markets and market crashes in minority Games, Physica A 294 (2001) 514–524.

- [17] T. Lux, M. Marchesi, Scaling and criticality in a stochastic multi-agent model of financial market, Nature 397 (1999) 498–500.

- [18] I. Giardina, J.-P. Bouchaud, M. Mezard, Microscopic models for long ranged volatility correlations, Physica A 299 (2001) 28–39.

- [19] H. S. Stanley, R. N. Mantegna, An introduction to econophysics: correlations and complexity in finance, Cambridge University Press, Cambridge, 2000.

- [20] P. Jefferies, M. L. Hart, P. M. Hui, N. F. Johnson, From market Games to real-world markets, Eur. Phys. J. B 20 (2001) 493–501.