Fraudulent agents in an artificial financial market

Abstract

The problem of insider trading and other illegal practices in financial markets is an important issue in the field of financial regulatory policies. Market control bodies, such as the US SEC or the Italian CONSOB [1], regularly perform statistical analyses on security prices in order to unveil clues of fraudulent behaviour within the market. Fraudulent behaviour is connected to the more general problem of information asymmetries, which had already been addressed in the field of experimental economics (see, for instance, refs. [2, 3, 4]). Recently, interesting conclusions were drawn thanks to a computer-simulated market where agents had different pieces of information about the future dividend cash flow of exchanged securities [5]. Here, by means of an agent-based artificial market: the Genoa Artificial Stock Market (GASM) [6, 7], the more specific problem of fraudulent behaviour in a financial market is studied. A simplified model of fraudulent behaviour is implemented and the action of fraudulent agents on the statistical properties of simulated prices and the agent wealth distribution is investigated.

1 Introduction

Laws and regulations define fraudulent behaviour in a financial market. Among the many possible instances of fraud, we will focus our attention on insider trading [1, 8]. It must be stressed that the enforcement of insider trading laws took place mainly in the 1990s, as a consequence of advances in the economic theory as well as in the empirical analysis of financial markets. Actually, many papers have been devoted to insider trading: a recent review by Bainbridge, quoted by Bhattacharia and Daouk, lists 261 papers [8]. In the past, various arguments were presented against the introduction and enforcement of insider trading laws. For instance, it has been pointed out that exploiting insider information is the only way to compensate managers. It has been also argued that the insider pushes the stock price faster towards a value, which better reflects the fundamental value of the company. Although the problem of evaluating the social and economical effects of insider trading can only be assessed by means of accurate empirical studies, there are several difficulties to be overcome, mainly due to the fact that several pieces of information on insider trading are confidential. However, after an empirical analysis of stock markets in 103 countries, Bhattacharya and Daouk were able to conclude that enforcement of insider trading laws reduces the cost of equity by about 5% [8].

In European countries where insider-trading laws are enforced, the scope of the law includes any security listed on a stock exchange, but also face-to-face transactions may be taken into account. The inside information is defined as non-public and price sensitive. Among the enforced subjects there are institutional insiders, other primary insiders and tippees. Some forbidden behaviours are: trading on own account, trading on behalf of third parties and communicating the information to third parties. There may be penal, civil and administrative sanctions, including imprisonment and fines. Fines are computed in relation to the disgorgement: the economic value of the insider information.

There are several methods to compute the disgorgement. The US Security Exchange Commission uses a procedure, which is based on the Event Study Analysis in order to evaluate the return percentage variation caused by the insider information. This is called potential econometric disgorgement. To avoid some pitfalls of the US method, the Italian body (CONSOB) has developed a new probabilistic approach, which will be discussed below.

Insider trading is an instance of information asymmetry in a financial market, which was discussed at length in the literature [2, 3, 9, 10, 11, 12]. Recently, it has been addressed by means of an artificial market [4]. With artificial markets, it is possible to study the effect of information asymmetries in a well-defined and controlled environment.

In this paper, we present a simplified model of insider trading in the Genoa Artificial Stock Market (GASM). The paper is organised as follows. Section 2 is devoted to the methodology of probabilistic disgorgement and to clarify the procedure used here to compute disgorgement in the artificial market. In section 3, the results of the GASM simulations are presented and discussed. Finally, in section 4, the reader can find the main conclusions and the direction for future work on insider trading in artificial financial markets.

2 An alternative path to probabilistic disgorgement

As mentioned in the Introduction, the Italian market regulation authority (CONSOB) has recently developed a new approach to unveil the economic value of the information exploited by each insider. CONSOB has called this procedure potential probabilistic disgorgement [1]. The (simplified) procedure consists of the following steps.

At first, two time-horizons are defined, and . The former corresponds to the period in which the insider will build his/her position on the stock; the latter is defined by the day in which the insider information is published and the first, the second or the n-th day after. The number of days considered is related to the liquidity of the stock under investigation and, in a standard insider-trading scheme, it coincides with the instant in which the insider closes his/her position.

The second step rests on two hypotheses. The first one is that the insider cannot control the price dynamics before the occurrence of the event and the second one is that he/she will create a long (short) position, if the event information will induce an increase (decrease) of the stock price. In other words, the insider predicts that the preferential information will move the market more in the period than it moved in the period . Therefore, the parameters of a geometric Brownian motion representing the time evolution of the stock in the period are estimated, by using daily data.

Finally, on this basis, an oscillation band for the price of the stock under study in the time-period is defined by fixing a significance level. The difference between the actual stock price after the insider information is revealed and this band represents the disgorgement.

A slight but important modification in computing the potential probabilistic disgorgement would be replacing the geometric Brownian motion with a process that better represents the leptokurtic behaviour of the return probability density estimate. To this purpose, there are various possible choices. An interesting possibility would be using truncated L vy walks la Koponen [13] or their generalisation proposed by Boyarchenko and Levendorskii [14]. Here, however, as we use an artificial market, we can directly simulate the behaviour of the same market, with and without the action of the insider. Therefore, in the next section, we shall directly evaluate the impact of insider-trading activities.

3 GASM model for insider trading

3.1 Brief description of the artificial market

We modelled the behavior of an insider trader in the framework of the Genoa Artificial Stock Market (GASM). In the market, random traders buy and sell a risky asset in exchange of cash. The decision-making process of each random trader is constrained by the limited financial resources and influenced by the volatility of the market. The resulting price process is characterized by reversion to the mean and exhibits fat-tailed distributions of returns and volatility clustering [15]. The average price (equilibrium price) is given by the ratio of the total amount of cash present in the system and the number of shares of the traded stock. In a closed market, i.e. no cash or shares inflow or outflow in the system, the long-run price average is constant. An increase of the global amount of cash in the system causes an equal increase of the long-run mean value.

3.2 A model of insider trading

The price process exhibits a mean-reverting behavior around the equilibrium price; thus a fundamentalist trading strategy with fundamental price equal to the equilibrium price would be profitable [16]. As price sensitive event, the injection of liquidity in the market has been chosen, simulating the action of a central bank. Being the equilibrium price equal to the ratio between the total amount of cash and share number, liquidity injection yields a new higher equilibrium price. A fundamentalist agent, who knows in advance the date of this event, should be able to take profit of this piece of insider information.

We consider a number of different simulations with the following features:

-

•

random traders and 1 insider fundamentalist trader operate in the market; at each time step, each random trader issues orders with probability ;

-

•

at the beginning of the simulation (), each random trader receives the same amount of liquidity and number of shares , while the insider is given liquidity and zero number of shares ;

-

•

the initial value of the stock price is set at the equilibrium price:

in order to quickly reach the equilibrium state characterized by fluctuations around the equilibrium price;

-

•

background trading is realized by the action of random traders, who issue random buy and sell orders with no information on the timing and magnitude of liquidity injection;

-

•

at a given time the global amount of cash is increased by 10% and the new cash is distributed to agents proportionally to the fraction of the total wealth (cash+number of shares) they own. Thus the equilibrium price increases by 10%:

Indeed, for , the equilibrium price is given by eq. (1);

-

•

the insider knows the timing and magnitude of the injection of liquidity in advance; let denote this advance;

-

•

the insider is inactive for and acts as a fundamentalist trader with the new appropriate fundamental value, , for . This means that in this time period, the insider tries to convert all the cash into stocks. For , the insider issues sell orders if the stock price is greater than the fundamental value , otherwise he/she keeps its position.

As a final remark, the period discussed in Section 2 corresponds to when the insider builds his/her position, whereas, the periods in which he/she leaves the market corresponds to .

4 Simulations

As already mentioned, the number of random traders operating in the simulations is 10,000. The probability of activation is . The initial amount of liquidity is units, whereas the initial share number of the risky stock is . As for the insider, his/her activity is characterized by two parameters: initial liquidity, , and advance, . The chosen values for are:

The chosen values for the advance are: 20, 40, 60, 80, 100 time steps. For each value of and , 25 independent realizations have been simulated, for a total of 750 simulations. Each simulation lasts 2,000 time steps, which in the framework of GASM can be considered as trading days. The insider event occurs at days.

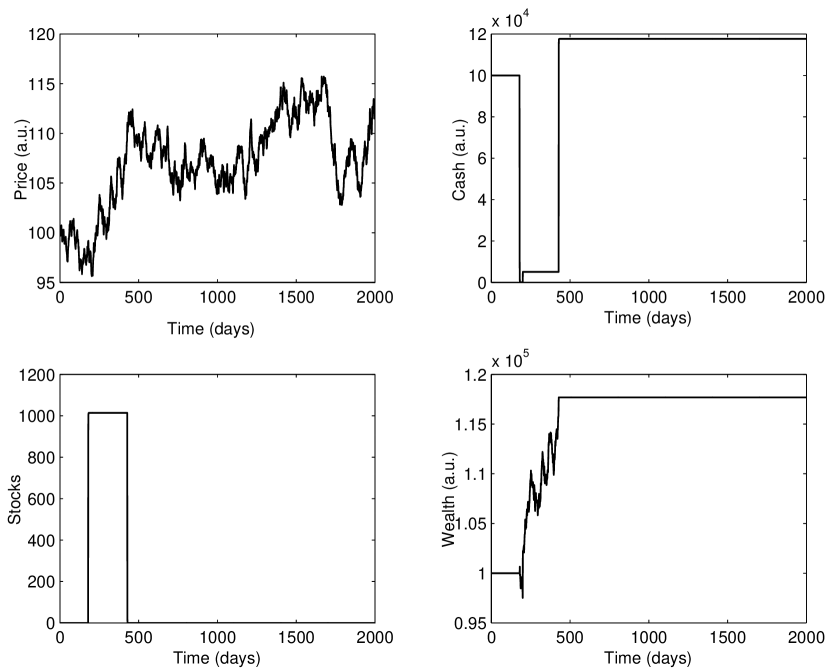

In Figure 1, results of a typical simulation are shown. In this particular case, and days. The left-upper plot displays the price variation as a function of time. The effect of the liquidity injection at time days is evident: after the injection, the average price increases towards 110 units and then fluctuates around this value. The right-upper plot shows the insider cash as a function of time. Essentially, the insider starts with 100,000 units of cash and ends with nearly 120,000 units, with a return of about 20 %. In a few days after day , the insider converts all his/her cash into shares. At day , he/she receives the additional amount of cash like all the random traders. Finally, when the price becomes greater than the new fundamental value (110 units), he/she starts issuing sell orders and succeeds in getting rid of the shares in a few days. The behavior of the insider can be appreciated also in the two bottom plots, where his/her number of shares (left) and his/her total wealth (right) are presented.

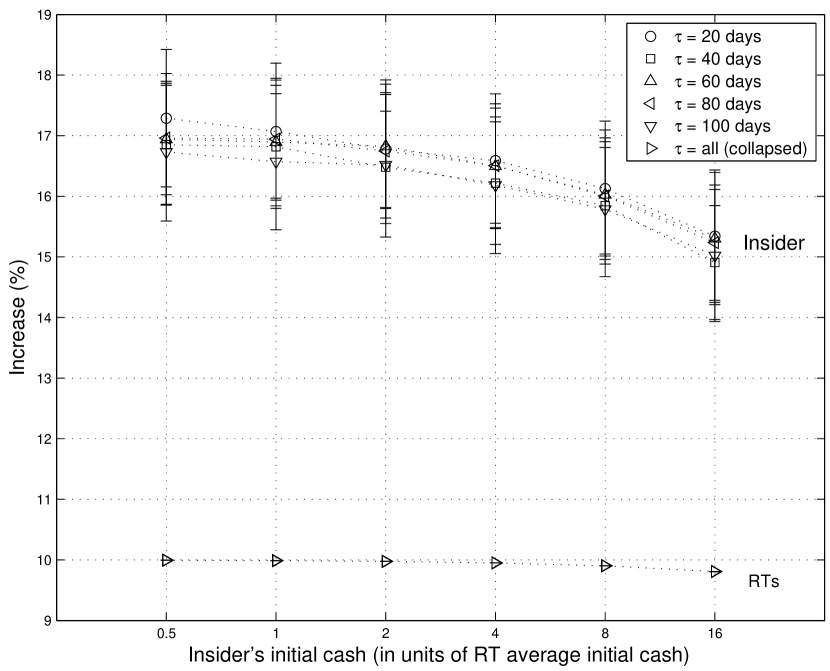

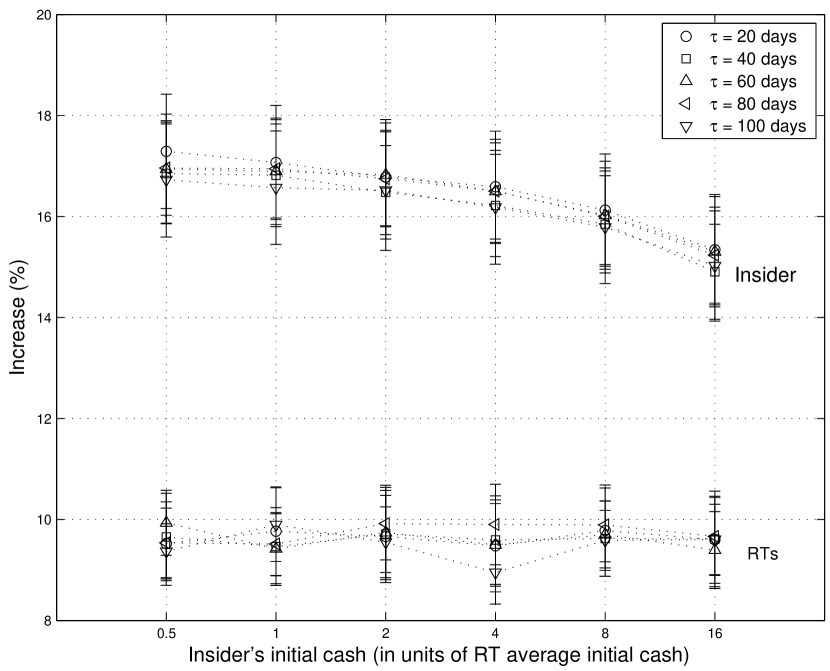

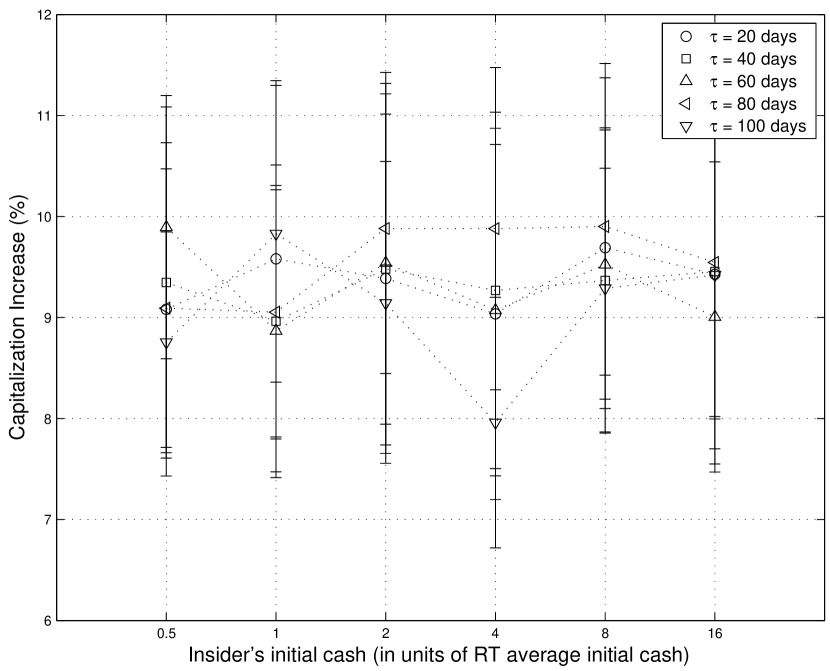

In order to compare the gain of the insider with the average performance of random traders, Figures 2, 3 and 4 present the random-trader percentage increase in aggregate cash, capitalization and wealth, respectively, as a function of insider cash and advance. The percentage increase is computed between day 2,000 (the end of the simulation) and day (the day before the insider entering into the market). The error-bar half-width corresponds to two standard errors.

In Figure 2, random-trader aggregate cash return is compared with the gain of the insider. In Figure 3, the insider gain is compared with the aggregate wealth return of random traders. No definite trend appears as a function of insider advance, but the insider average gain systematically decreases with increasing initial cash. The reason is that the insider influences more and more the stock price when his/her initial cash grows. In fact, he/she tries to convert his/her cash into shares as soon as possible, and issues buy orders that are larger the richer he/she is. Large buy orders can imply a price increase. If the stock price is higher, the number of shares he/she can buy for a given amount of cash is lower. In other words, if he/she influences the stock price, letting it increase, it becomes no longer true that with a double amount of cash, he/she is able to buy a double amount of shares. The decrease in average cash return of random traders is due to the mechanism of cash distribution within the insider event. When the wealth of the insider is large enough, random traders receive less new cash in aggregate (see Sec. 3.2). In Figure 4, the market capitalization return is shown between day 2,000 and day . No systematic effect due to insider activity appears. For this reason, also the aggregate wealth return of random traders in Figure 3 does not show any systematic dependence on insider parameters.

5 Discussion and conclusion

In this paper, a simple model of insider trading in an artificial market has been presented. Quasi zero-intelligence random traders are acting on a closed market providing a sort of thermal bath implying price fluctuations. A fundamentalist insider gets the information of cash inflow occurring on a future day. He/she tries to exploit this piece of information by using a fundamental strategy. It turns out that the insider is able to earn significantly more money than random traders. Due to the simple strategy implemented, the excess gain of the insider decreases when his/her initial endowment of cash is larger. The simulations presented above show that the Genoa Artificial Stock Market (GASM) can be used to study instances of fraudulent behaviour in financial markets. Future work could focus on the effect of insiders in a market with heterogeneous agents as well as different price formation mechanisms (clearing house vs book, …).

References

- [1] M. Minenna, “Insider trading, abnormal return and preferential information: supervising through a probabilistic model,” CONSOB,” Quaderni di Finanza, 2001.

- [2] C. R. Plott and S. Sunder, “Efficiency of experimental security markets with insider information: an application of rational-expectations models,” J Polit Econ, vol. 90, no. 4, pp. 663–698, August 1982.

- [3] R. Forsythe and R. Lundholm, “Information aggregation in an experimental market,” Econometrica, vol. 58, no. 2, pp. 309–347, March 1990.

- [4] J. Huber, M. Kirchler, and M. Sutter, “On the marginal benefits of additional information in markets with heterogenously informed actors - an experimental study,” University of Innsbruck, Tech. Rep., 2003.

- [5] T. Chan, “Artificial markets and intelligent agents,” Ph.D. dissertation, Massachusetts Intitute of Technology, 2001.

- [6] S. Cincotti, S. M. Focardi, M. Marchesi, and M. Raberto, “Who wins? study of long-run trader survival in an artificial stock market,” Physica A, vol. 324, no. 1-2, pp. 227–233, June 2003.

- [7] M. Marchesi, S. Cincotti, S. M. Focardi, and M. Raberto, The Genoa artificial stock market: microstructure and simulation, ser. Lecture notes in economics and mathematical systems. Springer, February 2003, vol. 521, pp. 277–289.

- [8] U. Bhattacharya and H. Daouk, “The world price of insider trading,” J Financ, vol. 57, no. 1, pp. 75–108, February 2002.

- [9] G. A. Akerlof, “The market for “lemons”: quality uncertainty and the amrket mechanism,” Quarterly Journal of Economics, vol. 84, no. 3, pp. 488–500, August 1970.

- [10] E. F. Fama, “Efficient capital markets: A review of theory and empirical work,” J Financ, vol. 25, pp. 383–417, 1970.

- [11] S. J. Grossman and J. E. Stiglitz, “On the impossibility of informationally efficient markets,” Am Econ Rev, vol. 79, no. 3, pp. 393–408, June 1980.

- [12] E. F. Fama, “Efficient capital markets II,” J Financ, vol. 46, pp. 1575–1617, 1991.

- [13] I. Koponen, “Analytical approach to the problem of convergence of truncated lévy flights towards the gaussian stochastic process,” Phys Rev E, vol. 52, no. 1, pp. 1197–1199, July 1995.

- [14] S. Boyarchenko and S. Levendorskii, “Options pricing for truncated lévy processes,” International Journal of Theoretical and Applied Finance, vol. 3, no. 3, pp. 549–552, 2000.

- [15] M. Raberto, S. Cincotti, S. M. Focardi, and M. Marchesi, “Agent-based simulation of a financial market,” Physica A, vol. 219, pp. 319–327, October 2001.

- [16] ——, “Traders’ long-run wealth in an artificial financial market,” Computational Economics, 2003, (in press).