Estimated Correlation Matrices and Portfolio Optimization

Szilárd Pafka1,2 and Imre Kondor1,3

1Department of Physics of Complex Systems, Eötvös

University

Pázmány P. sétány 1/a, H–1117 Budapest, Hungary

2Risk Management Department, CIB Bank

Medve u. 4–14., H–1027 Budapest, Hungary

3Institute for Advanced Studies, Collegium Budapest

Szentháromság u. 2., H–1014 Budapest, Hungary

April, 2003

Abstract

Financial correlations play a central role in financial theory and also in many practical applications. From theoretical point of view, the key interest is in a proper description of the structure and dynamics of correlations. From practical point of view, the emphasis is on the ability of the developed models to provide the adequate input for the numerous portfolio and risk management procedures used in the financial industry. This is crucial, since it has been long argued that correlation matrices determined from financial series contain a relatively large amount of noise and, in addition, most of the portfolio and risk management techniques used in practice can be quite sensitive to the inputs. In this paper we introduce a model (simulation)-based approach which can be used for a systematic investigation of the effect of the different sources of noise in financial correlations in the portfolio and risk management context. To illustrate the usefulness of this framework, we develop several toy models for the structure of correlations and, by considering the finiteness of the time series as the only source of noise, we compare the performance of several correlation matrix estimators introduced in the academic literature and which have since gained also a wide practical use. Based on this experience, we believe that our simulation-based approach can also be useful for the systematic investigation of several other problems of much interest in finance.

PACS: 87.23.Ge; 05.45.Tp; 05.40.–a

Keywords: financial correlation matrices, estimation error, random matrix theory, noise filtering, portfolio optimization, capital allocation, risk management

E-mail: syl@complex.elte.hu (S. Pafka), kondor@colbud.hu (I. Kondor)

1 Introduction

Correlation matrices of financial returns play a crucial role in several branches of modern finance such as investment theory, capital allocation and risk management. For example, financial correlation matrices are the key input parameters to Markowitz’s classical portfolio optimization problem [1], which aims at providing a recipe for the selection of a portfolio of assets such that risk (quantified by the standard deviation of the portfolio’s return) is minimized for a given level of expected return. For any practical use of the theory it would therefore be necessary to have reliable estimates for the correlations of returns (of the assets making up the portfolio), which are usually obtained from historical return series data. However, if one estimates a correlation matrix from time series of length each, since is usually bound by practical reasons, one inevitably introduces estimation error, which for large can become so overwhelming that the whole applicability of the theory may become questionable.

This difficulty has been well known by economists for a long time (see e.g. [2] and the numerous references therein). Several aspects of the effect of noise (in the correlation matrices determined from empirical data) on the classical portfolio selection problem has been investigated e.g. in refs. [3]. One way to cope with the problem of noise is to impose some structure on the correlation matrix, which may certainly introduce some bias in the estimation, but by reducing effectively the dimensionality of the problem, could be in fact expected to improve the overall performance of the estimation. The best-known such structure is that imposed by the single-index (or market) model, which has gained a large interest in the academic literature (see e.g. [2] for an overview and references) and has also become widely used in the financial industry (the coefficient ”beta”, relating the returns of an asset to the returns of the corresponding wide market index, has long become common talk in the financial community). On economic or statistical grounds, several other correlation structures have been experimented with in the academic literature and financial industry, for example multi-index models, grouping by industry sectors, macroeconomic factor models, models based on principal component analysis etc. Several studies (see e.g. refs. [4]) attempt to compare the performance of these correlation estimation procedures as input providers for the portfolio selection problem, although all these studies have been somewhat restricted to the use of given specific empirical samples. More recently, other procedures to impose some structure on correlations (e.g. Bayesian shrinkage estimators) or bounds directly on the portfolio weights (e.g. no short selling) has been explored, see e.g. refs. [5]. The general conclusion of all these studies is that reducing the dimensionality of the problem by imposing some structure on the correlation matrix may be of great help for the selection of portfolios with better risk–return characteristics.

The problem of estimation noise in financial correlation matrices has been put into a new light by [6, 7, 8] from the point of view of random matrix theory. These studies have shown that empirical correlation matrices deduced from financial return series contain such a high amount of noise that, apart from a few large eigenvalues and the corresponding eigenvectors, their structure can essentially be regarded as random. In [7], e.g., it is reported that about 94% of the spectrum of correlation matrices determined from return series of the S&P 500 stocks can be fitted by that of a random matrix. Furthermore, two subsequent studies [9, 10] have shown that the risk–return characteristics of optimized portfolios could be improved if prior to optimization one filtered out the lower part of the eigenvalue spectrum of the correlation matrix in an attempt to remove (at least partially) the noise, a procedure similar to principal component analysis. Other approaches inspired from physics and that are aimed to be useful in extracting information from noisy correlation data have been introduced in [11, 12]. It is important to note that all the above studies have used (given) empirical datasets, which in addition to the noise due to the finite length of the time series, contain also several other sources of error (caused by non-stationarity, market microstructure etc.).

The motivation of our previous study [13] came from this context. In order to get rid of these additional sources of errors, we based our analysis on data artificially generated from some toy models. This procedure offers a major advantage in that the ”true” parameters of the underlying stochastic process, hence also the correlation matrix is exactly known. The key observation of [13] is that the effect of noise strongly depends on the ratio , where is the size of the portfolio while is the length of the available time series. Moreover, in the limit , but the suboptimality of the portfolio optimized using the ”noisy” correlation matrix (with respect to the portfolio obtained using the ”true” matrix) is exactly. Therefore, since the length of the time series is limited in any practical application, any bound one would like to impose on the effect of noise translates, in fact, into a constraint on the portfolio size .

The aim of this paper is (besides to extend the analysis of the previous study) to introduce a model (simulation)-based approach that can be generally used for the systematic investigation of correlations in financial markets and for the study of the effect of different sources of noise on the numerous procedures based on correlation matrices extracted from financial data. As an illustration of the usefulness of this approach, we introduce several toy models aimed to progressively incorporate the relevant features of real-life financial correlations and, in the world of these models, we study the effect of noise (in this case only due to the estimation error caused by the finiteness of surrogate time series generated by the models) on the classical portfolio optimization problem. More precisely, we compare the performance of different correlation matrix ”estimation” methods (e.g. the filtering procedure introduced in [9, 10]) in providing inputs for the selection of portfolios with optimal risk–return characteristics. The approach is in fact very common in physics, where one starts with some bare model and progressively adds finer and finer elements, while studying the behavior of the ”world” embodied by the model by comparing it to the real-life (experimental) results. We strongly believe that our model-based approach can be useful for the systematic study of several other problems in which financial correlation matrices play a crucial role.

2 Results and Discussion

We keep to consider the following simplified version of the classical portfolio optimization problem introduced in [13]: the portfolio variance is minimized under the budget constraint , where denotes the weight of asset in the portfolio and the covariance matrix of returns. This simplified form provides the most convenient laboratory for testing the effect of noise in correlations, since it eliminates the additional uncertainty arising from the determination of several other parameters that appear in more complex formulations. The weights of the optimal portfolio in this simple case are:

| (1) |

Starting from a given ”true” covariance matrix () we generate surrogate time series (of finite length ), , with and the Cholesky decomposition of the matrix . In this way we obtain ”return series” that have a distribution characterized by the ”true” covariance matrix . Similar to real-life situations (where the true covariance matrix is not known) we calculate different ”estimates” for the covariance matrix based on several competing procedures and then use these estimates in our portfolio optimization. Finally, we compare the performance of these procedures using metrics related to the risk (standard deviation) of the ”optimal” portfolios constructed based on the corresponding estimates. The main advantage of this simulation-based approach is that the ”true” covariance matrix can be incorporated in the evaluation, which is certainly much cleaner than using, as in empirical studies, some proxy for it (which in turn introduces an additional source of noise).

In our previous study [13] we have used a very simple structure (”model”) for (namely the identity matrix) and we have studied the effect of noise when the ”estimated” matrix is the sample (or historical) covariance matrix. In this paper we introduce several other ”models” (proposals for the structure of ) which are intended to incorporate progressively the most relevant characteristics of real-life financial correlations (the models are given in terms of the corresponding correlation matrix ):

-

1.

”Single-index”, ”market” or ”average correlation” model. The correlation matrix has 1 in the diagonal and given () off-diagonal (all correlations the same, hence the name of ”average correlation” model). The eigenstructure of such a matrix is formed of one large111, which for the usual values of the parameters is large compared to . eigenvalue with corresponding eigenvector in the direction of and a -fold degenerated eigenvalue subspace orthogonal on the subspace of the first eigenvector. The eigenspace of the large eigenvalue can be thought of as describing correlations with a broad ”index” composed of all stocks (the ”market”), hence the name of ”single-index” or ”market” model. This model is motivated by the similar salient feature of stock market correlations found by numerous research studies (see e.g. [2] for references).

-

2.

”Market+sectors” model. A very simple structure intended to incorporate this more debated222See e.g. refs. [14]. feature of real-life financial correlations can be based on a correlation matrix composed of blocks (with 1 in the diagonal and off-diagonal) and outside the blocks ( and integer). In this model there is still a strong influence of the ”market” but stocks from the same block (”industrial sector”) display additional common correlations. On the other hand, the eigenspectrum of such a matrix333The eigenstructure is formed of a large eigenvalue , a -fold degenerated subspace corresponding to medium-size eigenvalues and a -fold degenerated subspace with eigenvalues . is closer to the eigenspectrum of real-life financial correlation matrices as described e.g. in [10]. This correlation structure also fits better with the findings of [11, 12], which using a hierarchial tree approach found also that stocks tend to be coupled according to their belonging to industrial sectors.

-

3.

”Semi-empirical” (bootstrapped) model. Starting from a large set of empirical financial data444The same dataset as in [13] has been used. We thank again J.-P. Bouchaud and L. Laloux for making their data [7, 9] available to us. for each portfolio size , we select randomly (bootstrap) time series from the set of empirical return data and an covariance matrix is calculated using the full length of the available series. This matrix is then used as in the simulations (to generate the surrogate data). In order to examine the sensitivity of our results with respect to the choice of the time series, we repeat several times the simulations (with different bootstrapped empirical series) and we compare the results. The correlation structure of this model is hoped to be the closest to real-world financial correlations, although the disadvantage of it is, similar to empirical studies, that it is based on a given set of empirical data which might be representative in certain situations but it is still not fully general.

In the framework of each of the models introduced above, we investigate the performance of three alternative choices for the ”estimated” covariance matrix :

-

1.

Sample (historical) covariance matrix.

-

2.

”Single-index” covariance matrix, i.e. the matrix obtained from the sample covariance matrix by a simplified filtering procedure similar to the one described below, but considering only the largest eigenvalue (and the corresponding eigenvector), which is believed to correspond to a broad market index covering all stocks, see e.g. [10].

-

3.

Filtered covariance matrix using the procedure based on random matrix theory [9, 10]. For this, one starts with the sample correlation matrix and keeps only the eigenvalues and the corresponding eigenvectors reflecting deviations from random matrix theory predictions (those outside the random matrix noise-band) and then constructs a ”cleaned” correlation matrix such that the trace of the matrix is preserved. The intuition behind this procedure is that deviations from random matrix theory predictions should correspond to ”information” and describe genuine correlations in the system while the eigenstates corresponding to random matrix theory predictions should be manifestations of purely random ”noise”. The filtered covariance matrix is then obtained from the filtered correlation matrix and sample standard deviations. This procedure is very much reminiscent of principal component analysis, although classical multivariate analysis gives generally no hints about how many components (factors) to include in the matrix constructed using the principal components (see e.g. [15]). The filtering procedure based on random matrix theory can therefore be thought of as a theoretically sound indication for the number of principal components to be included in the analysis.

To study the effect of noise on the portfolio optimization problem we use metrics based on the following quantities:

-

1.

, the ”true” risk of the optimal portfolio without noise, where denotes the solution to the optimization problem with ;

-

2.

, the ”true” risk of the optimal portfolio determined in the case of noise, where denotes the solution to the optimization problem with ;

- 3.

- 4.

To facilitate the comparison, we calculate the ratios of the square roots of the three latter quantities to the first one, and denote these by and , respectively. That is and represent the ”true”, the ”predicted” resp. the ”realized” risk, expressed in units of the ”true” risk in the absence of noise. In other words, describes directly the ability of a given estimation procedure to provide the correct input for portfolio optimization, describes the bias one makes if then uses the estimated matrix for the calculation of the risk of the optimal portfolio, while is the risk measured if one waits in time and uses the information from the new series for risk measurement (see also [13]).

We start with presenting the simulation results when the series have been generated using the ”market” model (for ). Since the main feature of the correlation structure (one outstanding large eigenvalue) is, at least for the parameter values used in our simulations, preserved also in the correlation matrix obtained from the generated series (), the results for the filtering based on the largest eigenvalue and on random matrix theory are in fact the same. Therefore, we proceed with comparing the performance of the historical and filtered estimation procedures for different values of the model parameters , and using the evaluation metrics , , and . A summary of our simulation results is presented in Table 1.

| 0.2 | 200 | 300 | 1.5 | 1.77 | 1.11 | 0.56 | 0.78 | 1.77 | 1.13 | 3.16 | 1.46 |

| 0.2 | 1000 | 1500 | 1.5 | 1.73 | 1.12 | 0.59 | 0.78 | 1.71 | 1.11 | 2.96 | 1.42 |

| 0.6 | 1000 | 1500 | 1.5 | 1.75 | 1.11 | 0.58 | 0.77 | 1.75 | 1.12 | 3.01 | 1.45 |

| 0.2 | 1000 | 2000 | 2 | 1.42 | 1.11 | 0.71 | 0.82 | 1.43 | 1.11 | 2.00 | 1.35 |

| 0.2 | 1000 | 5000 | 5 | 1.11 | 1.07 | 0.89 | 0.91 | 1.12 | 1.07 | 1.26 | 1.18 |

| 0.2 | 1000 | 500 | 0.5 | - | 1.12 | - | 0.57 | - | 1.12 | - | 1.92 |

It turns out that, for sufficiently large and , the value of the ’s depends strongly only on (and, interestingly, does not seem to depend on ). This can be seen also from the results presented in Table 1 (the variation in the first 3 rows is in fact within the usual standard deviation bounds). This is not very surprising as concerning the results for the historical matrix, which has been studied in our previous paper [13]. The strong dependence on seems to be valid, however, also when the filtered matrix is used. One important difference to note is, however, the significant improvement in the risk characteristics of the optimal portfolio when the filtering procedure is used for estimation, e.g. for instead of obtaining a portfolio with risk more than 40% larger than the trully optimal one (see ), using the filtering procedure one can get portfolios with risk only 10% larger. Furthermore, as it can also be seen from the table, using the filtered matrix one can obtain portfolios close to the optimal one even for when the sample (historical) matrix is singular and not at all appropriate for being used in the optimization. This improvement in performance is not difficult to understand, since with the filtering procedure one implicitly incorporates into the ”estimation” the additional information about the structure of the correlation matrix. Note also that for all parameter values is very close to , therefore the risk measured in the second ”period” seems to be a good proxy for the ”true” risk of the optimal portfolio.

| 0.2 | 0.4 | 25 | 200 | 300 | 1.71 | 1.27 | 1.13 | 0.58 | 0.77 | 0.76 | 2.93 | 1.65 | 1.47 |

| 0.2 | 0.4 | 25 | 1000 | 1500 | 1.75 | 1.28 | 1.13 | 0.58 | 0.77 | 0.76 | 3.07 | 1.63 | 1.46 |

| 0.2 | 0.6 | 25 | 1000 | 1500 | 1.74 | 1.64 | 1.13 | 0.59 | 0.78 | 0.76 | 2.94 | 2.09 | 1.47 |

| 0.4 | 0.6 | 25 | 1000 | 1500 | 1.73 | 1.36 | 1.13 | 0.58 | 0.77 | 0.76 | 2.96 | 1.77 | 1.49 |

| 0.2 | 0.4 | 50 | 1000 | 1500 | 1.71 | 1.42 | 1.12 | 0.58 | 0.77 | 0.77 | 2.96 | 1.84 | 1.46 |

| 0.2 | 0.4 | 25 | 1000 | 2000 | 1.42 | 1.24 | 1.12 | 0.70 | 0.82 | 0.81 | 1.99 | 1.50 | 1.37 |

| 0.2 | 0.4 | 25 | 1000 | 5000 | 1.11 | 1.16 | 1.07 | 0.89 | 0.91 | 0.90 | 1.24 | 1.27 | 1.17 |

| 0.2 | 0.4 | 25 | 1000 | 500 | - | 1.24 | 1.19 | - | 0.58 | 0.55 | - | 2.14 | 2.17 |

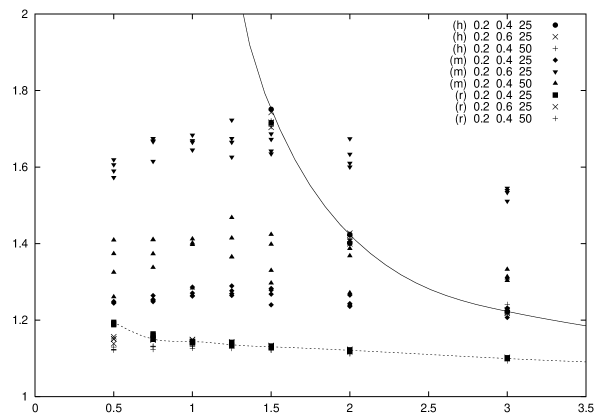

We next present the results when the series are generated with the ”market+sectors” model, for different values of the parameters , , , and . Our results are summarized in Table 2. The values for ’s have been again very close to and therefore have been left out from the table. We have found that the value of the ’s in the case of the historical and random matrix theory-based estimators, again, depends strongly on and not on the value of the other parameters, while this is not true for the estimator based on the largest eigenvalue only. This is illustrated in Fig. 1, where in the case of the three estimators is represented as a function of for different value of the parameters , , , and . The dependence of for the ”single-index” estimator on the parameters , and can be easily understood, since either the increase of or , or the decrease of can be thought of as the increase in the relative strength of ”inter-sector” correlations (relative to the overall correlation corresponding to the ”market”) and therefore an estimator taking into account only the ”market” component of correlations (and ignoring the ”sector” component) is of course expected to perform worse is this case. Another important point to note is that, in most cases, the random matrix theory based filtering outperforms the single-index estimator which in turn outperforms the historical estimator. Moreover, the first two estimators can be used even when the latter one provides a singular matrix totally inappropriate for input to the portfolio optimization (for ).

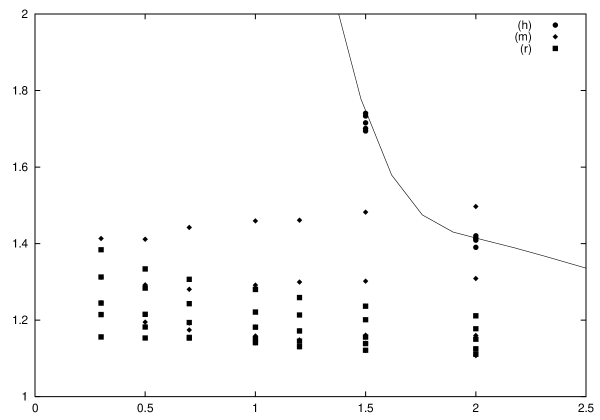

Finally, we analyze the performance of the three correlation matrix estimators in the case of the ”semi-empirical” model for (the matrix is bootstrapped from the empirical matrix of a given large set of financial series). More precisely, for each value of the parameter , we select at random series from the available dataset and we calculate the historical matrix which is then used as in our simulations555Since most of the values for the length of the time series used in our simulations is small compared to the lengths of the original dataset from which is computed, the noise due to the ”measurement error” of can be hoped to be small compared to the noise (deliberately) introduced by the finiteness of .. Our results are summarized in Table 3 (the values for ’s have been again left out of the table.) In this case, the ’s for the two filtering matrix estimations do not depend so strongly on , some dependence on (and ) can also be observed (see Fig. 2). It can be said again that, in general, the filtering procedures outperform significantly the historical matrix estimation, with the filtering based on the random matrix theory approach performing the best.

| 200 | 300 | 1.5 | 1.70 | 1.30 | 1.20 | 0.58 | 0.78 | 0.83 | 3.03 | 1.67 | 1.44 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 300 | 450 | 1.5 | 1.74 | 1.48 | 1.24 | 0.58 | 0.76 | 0.84 | 2.99 | 1.94 | 1.45 |

| 300 | 600 | 2 | 1.41 | 1.50 | 1.21 | 0.71 | 0.77 | 0.90 | 2.02 | 1.95 | 1.35 |

| 300 | 1500 | 2 | 1.12 | 1.53 | 1.15 | 0.89 | 0.80 | 0.96 | 1.26 | 1.92 | 1.21 |

| 300 | 150 | 0.5 | - | 1.41 | 1.33 | - | 0.76 | 0.73 | - | 2.02 | 1.85 |

In conclusion, our simulation study provides a more general argument for the usefulness of techniques for ”massageing” empirical correlation matrices before using them as inputs for portfolio optimization as suggested e.g. by [4, 5, 9, 10]. Furthermore, it re-emphasizes the fruitfulness of the random matrix theory-based filtering procedure for portfolio selection applications.

There are several possibilities to extend the analysis of this paper. One main direction would be to develop ”models” that incorporate more subtle features of real-life financial correlations. For example, an important feature of real financial series that has been neglected is non-stationarity. Incorporating the dynamics of correlations into the model could result into a more realistic description of correlations. For example, models such as ARCH/GARCH and its numerous variants (see e.g. [16] for an overview) have been found to be fruitful in describing the dynamics of changing volatility (and also of correlations in the multivariate setting). On the other hand, estimation techniques based on similar rationales (for example RiskMetrics [17]) have been widely utilized by financial practitioners. These estimation procedures run into the dimensionality problem typically already for or 5, but fortunately the principal component/factor approach has proved here also useful [18]. A simple way to take account of non-stationarity in our ”estimation” would be to use exponential weighting of observations in the calculation of the correlation matrix (in the spirit of RiskMetrics) and then apply the filtering to this matrix. Of course, this should be preceded by the derivation of the corresponding formulae for the noise band of matrices with this new structure. Another way to extend the analysis of this study is to use the model (simulation)-based approach for evaluating the performance of several other correlation matrix estimators introduced in the literature or used in practice.

The implications of successful noise filtering in correlation matrices used for portfolio optimization are enormous. Correlation matrices are not only at the heart of modern finance and investment theory, but also appear in most practical risk management and asset allocation procedures used in the financial industry. In particular, most implementations of practical risk–return portfolio optimization or benchmark tracking (minimization of risk with respect to a given benchmark) involve either correlation matrices or ”scenarios” usually generated using correlation matrices, see e.g. [19]. A short overview on the techniques used by practitioners for reducing noise and estimation error in correlation matrices can be found in [20]. The filtering procedure based on random matrix theory fits well into this package and can prove very useful for reducing estimation error and its consequences. On the other hand, from purely academic point of view, understanding the structure and dynamics of correlations in financial markets is still of central interest in finance and related fields, therefore any study that makes it possible to reveal finer and finer bits of the structure of these correlations can be of great importance.

3 Conclusion

In this paper we introduced a model (simulation)-based approach which can be used for a systematic investigation of the effect of different sources of noise in correlation matrices determined from financial return series. To show the usefulness of this approach we developed several toy models for the structure of financial correlations and, by considering only the noise arising from the finite length of the model-generated time series, we analyzed the performance of several correlation matrix estimation procedures in a simple portfolio optimization context.

The results of this study can be extended in very numerous ways, some of which are briefly given next. First, by developing models that incorporate finer and finer elements of the structure of financial correlations, the relevance of the results can be increased further. For example, allowing for some dynamics (non-stationarity) in correlations could make it possible to analyze the effect of noise due to non-stationarity or due to the estimation error of the parameters of some dynamic models on the portfolio optimization problem. Second, the analysis could be extended to several other correlation estimation procedures introduced in the literature, e.g. trully single-index model (with betas), multi-index models, different factor estimation procedures, Bayesian-estimators etc. (see for example [4, 5, 19, 20]). The models (simulations) could also be used for studying the performance of several other techniques for the extraction of correlation information such as the hierarchial tree methods of [11, 12]. Third, our model-based approach can be used also in a more complex optimization framework, e.g. in that of the classical mean–variance efficient frontier rather than just in the simple global optimization framework used in this paper. Last, but not least, the approach could be used also for the study of different other more general ”correlation” measures if instead of the portfolio standard deviation some other more sophisticated risk measure (e.g. Conditional Value-at-Risk) is used.

Acknowledgements

This work has been supported by the Hungarian National Science Found OTKA, Grant No. T 034835.

References

- [1] H. Markowitz, J. Finance 7, 91 (1952); H. Markowitz, Portfolio Selection: Efficient Diversification of Investments (J. Wiley and Sons, New York, 1959).

- [2] E. J. Elton and M. J. Gruber, Modern Portfolio Theory and Investment Analysis (J. Wiley and Sons, New York, 1995).

- [3] G. Frankfurter, H. Phillips and J. Seagle, J. Fin. Quant. Anal. 6, 1251 (1971); J. Dickinson, J. Fin. Quant. Anal. 9, 447 (1974); J. Jobson and B. Korkie, J. Am. Stat. Assoc. 75, 544 (1980); R. Michaud, Fin. Anal. Journal 45, 31 (1989); V. Chopra and W. T. Ziemba, J. Portf. Managem. 19, 6 (1993).

- [4] E. J. Elton and M. J. Gruber, J. Finance 28, 1203 (1973); E. J. Elton, M. J. Gruber and T. Urich, J. Finance 33, 1375 (1978); C. Eun and B. Resnick, J. Finance 39, 1311 (1984); L. Chan, J. Karceski and J. Lakonishok, Rev. Fin. Stud. 12, 937 (1999); N. Amenc and L. Martellini, J. Altern. Inv. 5, 7 (2002); C. Bengtsson and L. Holst, Lund University working paper (2002).

- [5] P. Jorion, J. Fin. Quant. Anal. 21, 544 (1986); V. Chopra, C. Hensel and A. Turner, Managem. Sci. 39, 845 (1993); O. Ledoit and M. Wolf, J. Empir. Fin., forthcoming (2003); R. Jagannathan and T. Ma, NBER working paper No. 8922 (2002).

- [6] G. Galluccio, J.-P. Bouchaud and M. Potters, Physica A 259, 449 (1998).

- [7] L. Laloux, P. Cizeau, J.-P. Bouchaud and M. Potters, Phys. Rev. Lett. 83, 1467 (1999); L. Laloux, P. Cizeau, J.-P. Bouchaud and M. Potters, Risk 12, No. 3, 69 (1999).

- [8] V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral and H. E. Stanley, Phys. Rev. Lett. 83, 1471 (1999).

- [9] L. Laloux, P. Cizeau, J.-P. Bouchaud and M. Potters, Int. J. Theor. Appl. Finance 3, 391 (2000).

- [10] V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, T. Guhr and H. E. Stanley, e-print cond-mat/0108023; B. Rosenow, V. Plerou, P. Gopikrishnan and H. E. Stanley, e-print cond-mat/0111537.

- [11] G. Bonanno, F. Lillo and R. N. Mantegna, Physica A 299, 16 (2001), e-print cond-mat/0104369.

- [12] L. Kullmann, J. Kertesz and R. N. Mantegna, Physica A 287, 412 (2000); J. P. Onnela, A. Chakraborti, K. Kaski and J. Kertesz, e-print cond-mat/0208131.

- [13] S. Pafka and I. Kondor, Physica A 319, 487 (2003), e-print cond-mat/0205119.

- [14] B. King, J. Business 39, 139 (1966); S. Meyers, J. Finance 28, 695 (1973); J. Farrell, J. Business 47, 186 (1974); M. Livingston, J. Finance 32, 861 (1977).

- [15] W. R. Krzanowski, Principles of Multivariate Analysis, (Clarendon Press, Oxford, 1998).

- [16] T. Bollerslev, R. Engle and D. Nelson, ”ARCH Models” in Handbook of Econometrics, Vol. IV, ed. by R. Engle (North Holland, Amsterdam, 1994).

- [17] J. P. Morgan and Reuters, RiskMetrics – Technical Document (New York, 1996).

- [18] R. Engle, V. Ng and M. Rotschild, J. Econometrics 45, 213 (1990); C. Alexander, ”Orthogonal GARCH” in Mastering Risk, Vol. 2, ed. by C. Alexander (FT–Prentice Hall, 2001).

- [19] Barra, portfolio optimization documentation, www.barra.com; Algorithmics, scenario and risk–reward optimization documentation, www.algorithmics.com; R. Litterman and K. Winkelmann, Goldman Sachs Risk Management Series paper (1998); APT, portfolio optimization documentation, www.apt.com.

- [20] D. diBartolomeo, ”Risk of Equity Securities and Portfolios”, Northfield Information Services Inc. paper, www.northinfo.com.