Comparison of Field Theory Models of Interest Rates with Market Data

Abstract

We calibrate and test various variants of field theory models of the interest rate with data from eurodollars futures. Models based on psychological factors are seen to provide the best fit to the market. We make a model independent determination of the volatility function of the forward rates from market data.

1 Introduction

In this paper, we compare field theory models of interest rate models with market data, and propose certain modified models inspired from theoretical considerations and observed facts about the interest rates. The theoretical framework for all these models is Baaquie’s formulation [1], [2] of forward rates as a two dimensional quantum field theory. The Baaquie model is a generalization of the Heath-Jarrow-Morton (HJM) model; the key feature of the field theory model is that the forward rates are imperfectly correlated in the maturity direction , and which is specified by a rigidity parameter . The models we study are the following: (a) forward rates with constant rigidity [1], (b) forward rates with the variation of the spot rate constrained by a new parameter [3], and two new models proposed in this paper, namely (c) forward rates with maturity dependent rigidity , and lastly (d) forward rates with non-trivial dependence on maturity specified by an aribitrary function .

We first briefly review Baaquie’s field theory model and review the market data used in this study. We then test the field theory model, introduce two variants and test them as well. We find that the correlation structure can be explained by a relatively straightforward two parameter model which also has a useful theoretical interpretation.

2 The HJM model

2.1 Definition of the model

In the HJM- model the forward rates are given by

| (1) |

where are independent Wiener processes. We can also write this as

| (2) |

where represent independent white noises. The action functional, is

| (3) |

We can use this action to calculate the generating functional which is

| (4) | |||||

3 Field theory model with constant rigidity

We now review Baaquie’s field theory model presented in [1] with constant rigidity. Baaquie proposed that the forward rates being driven by white noise processes in (2) be replaced by considering the forward rates itself to be a quantum field. To simplify notation, we write the evolution equation in terms of the velocity quantum field , and which yields

| (5) |

or

| (6) |

The main extension to HJM is that depends on as well as unlike which only depends on .

While we can put in many fields , we will see that the extra generality brought into the process due to the extra argument will make one field sufficient. Hence, in future, we will drop the subscript for .

Baaquie further proposed that the field has the free (Gaussian) free field action functional

| (7) |

with Neumann boundary conditions imposed at and . This makes the action equivalent (after an integration by parts where the surface term vanishes) to

| (8) |

This action has the partition function

| (9) |

with

| (10) |

where and . We can calculate expectations and correlations using this partition function. Note that due to the boundary conditions imposed, the inverse of the differential operator actually depends only the difference . The above action represents a Gaussian random field with covariance structure . In [1], a different form was found as the boundary conditions used were Dirichlet with the endpoints integrated over. This boundary condition is in fact equivalent to the Neumann condition which leads to the much simpler propagator above. In the limit which we will usually take, the propagator takes the simple form where and stand for and respectively.

When , this model should go over to the HJM model. This is indeed seen to be the case as it is seen that . The extra factor of is irrelevant as it is due to the freedom we have in scaling and . The we use for the different models are only comparable after is normalized111This freedom exists since we can always make the transformation and without affecting any result. On normalization, the propagator for both the HJM model and field theory model in the limit is one showing that the two models are equivalent in this limit.

The basic model with constant rigidity can be generalized in many different ways. The generalization to positive valued forward rates, and to models with stochastic volatility are studied in [2]. In this paper we generalize the free field model to more complex dependence of and on the maturity direction .

4 The Market Data used for the Study

We used the Eurodollar futures data for the following study. A Eurodollars futures contract is represents a deposit of US$1,000,000 for three months at some time in the future. Currently, futures contracts for deposits upto ten years into the future are actively traded. Significant historical data for contracts on deposits upto seven years into the future are available. If one makes the reasonable approximation that is linear for between contract times, one can use this data as a direct measure of the forward rates.

Further, the straightforward simplification that the Eurodollar futures prices directly reflect the forward rate was done, an assumption previously used in the literature [4]. This is a reasonable assumption as the forward rates are small enough that the difference between the logarithmic measure of the forward rate used in theory and the arithmetic rates used in the market are insignificant. We also attempted to analyse Treasury bond tick data from the GovPx database but we found it impossible to obtain forward rates accurate enough for our purposes. The main reason for this is that while we were able to obtain reasonably accurate yields for a few maturities, the differentiation required to get the forward rates from the yields introduced too many inaccuracies. This is somewhat unfortunate since Treasury bonds represent risk free instruments while a small credit risk exists for Eurodollar deposits.

For the following analysis, we used the closing prices for the Eurodollar futures contracts in the 1990s. This is exactly the same data as used by Bouchaud [4] as well as Baaquie and Srikant [5]. In Bouchaud [4], the spread of the forward rates and the eigenfuctions of its changes in time are analyzed. For our purposes, we found it more useful to look at the scaled multivariate cumulants of the changes in forward rates for different maturity times.

5 Assumptions behind the tests of the models

The main assumption that has to be made for all the tests of the models is that of time translation invariance. In other words, we have to assume that is actually only dependent on and not explicitly on . We also assume that the propagator has no explicit time dependence which is possible in principle. It is reasonable and conceptually economical to assume that different times in the future are equivalent. Further, carrying out any meaningful analysis while these quantities are subject to changes in time is impossible.

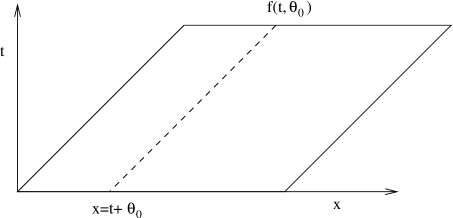

Another important assumption that has to be made is that the forward rate curve is reasonably smooth at small intervals at any given point in time. This assumption is very difficult to test in any meaningful sense given the relative paucity of data as forward rate data is available only at 3 month intervals (which is what necessitates this assumption in the first place). However, the assumption is a reasonable one to make as one would intuitively expect that the forward rate, say three years into the future would not be too different from that three years and one month into the future. In fact, we will show later that there seems to be strong evidence of very long term correlations in the movements of the forward rate. This seems to make the smoothness assumption reasonable as nearby forward rates tend to move together (except possibly at points very close to the current time). This assumption is required as the forward rate data is provided for constant maturity which we have been denoting by while we want data for constant , as shown in figure 1. With this assumption, we can get the data by simple linear interpolation. The loss in accuracy due to this linear interpolation is not all that serious if , the time interval of between specifications of the forward rates is small as the random changes which we are interested in will be much larger than the introduced errors. This same procedure was used in Matacz and Bouchaud [4] as well as Baaquie and Srikant [5].

6 The Correlation Structure of the Forward Rates

A very interesting quantity to look at in the analysis of forward rates is the correlation (or scaled covariance) among their changes for different . Specifically we are interested in the correlation between and , where . Using a free (Gaussian) quantum field theory model, this quantity should be equal to

| (11) |

To a reasonable degree of accuracy, we can ignore the first order expectations such as as they are much smaller than the second order expectations if is small. For an of one day, the error is completely negligible especially given the other approximations. We will do so for the rest of the chapter. If we have a model for the propagator , we have a prediction for this correlation structure. Alternatively, we can use the correlation structure to fit free parameters in .

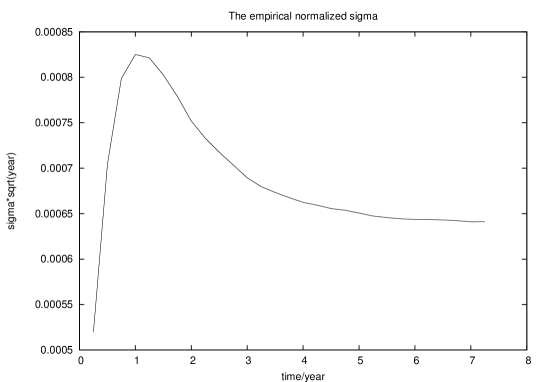

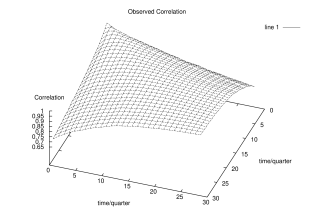

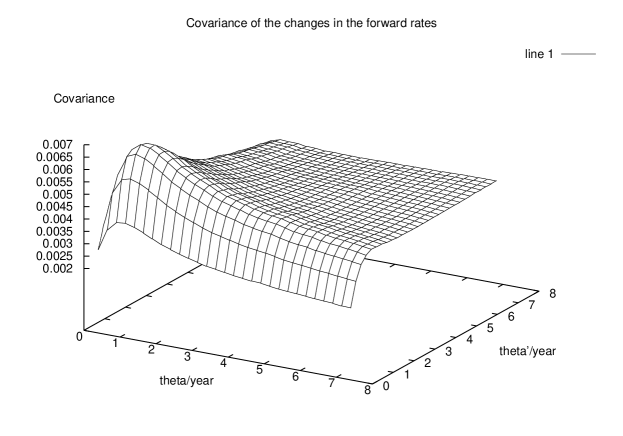

It should be noted that for free (Gaussian) quantum fields the correlation is independent of , so no assumption of its form has to be made. This is the reason why we used the scaled covariance rather than the covariance itself to perform the study. It is equivalent to fixing the inherent freedom in the quantities and to make . The reduction in the freedom of also allows us to directly estimate it from data since we have if . This is shown in figure 2. Further, the correlation between innovations in the forward curve is given exactly by . The correlation structure in the market estimated from the Eurodollar futures data is shown in figure 3. The structure is fairly stable in the sense that the correlation structure for different sections of the data are reasonably similar.

Since the propagator is always symmetric, it will be convenient to calculate only for the different models where and for purposes of comparison.

For the one factor HJM model, this correlation structure is constant as all the changes in the forward rates are perfectly correlated. In other words, . For the two factor HJM model, the predicted correlation structure is given by

| (12) |

We see that this correlation structure depends on a function of . Hence, a whole function has to be fitted from the correlation structure, something which is quite infeasible. The covariance might be a better quantity to test the two factor HJM model as the prediction of the covariance has a simpler form

| (13) |

We still need to specify a functional form for and as it is not possible to estimate entire functions from data. The usual specification of and inspired by the assumption that the spot rate follows a Markov process is easily seen to be unable to explain many features of the covariance in figure 5 such as the peak at one year or the sharp reduction in the covariance as the maturity goes to zero. We can straightaway conclude that the one factor HJM model is insufficient to characterize the data while the two factor HJM model provides us with too much freedom as we can put in an entire arbitrary function to explain the correlation structure. If we try to reduce the freedom by theoretical considerations, we are again unable to explain the data.

We will see that the field theory model with constant rigidity, while explaining some features of the correlation, does not predict the correlation very well. Hence, we consider generalizations to the constant rigidity model.

7 Analysis of Field Theory Model with Constant Rigidity

We have analysed this model in detail in the previous section. We have seen that the model describes the innovations in the forward rates in terms of a Gaussian random field whose structure is defined by the action in (7). For convenience, we repeat the action below in terms of the variables and

| (14) |

To obtain the predicted correlation structure from the propagator (10), we have to take the limit and obtain

| (15) |

The predicted correlation structure for this model can be found from this form of the propagator by normalization and from (11) is given by

| (16) |

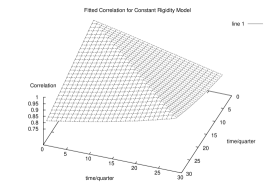

when the limit is taken. To estimate the parameter from market data, we use the Levenberg-Marquardt method from Press et al [6] to fit the parameters to the observed correlation structure graphed in figure 3. The fitting was done by minimizing the square of the error. The overall correlation was fitted by year. To obtain the error bounds, the data was split into 346 data sets of 500 contiguous days of data each and the estimation done for each of the sets. The 90% confidence interval for this data set is . Note that the confidence interval is asymmetric from the overall best fit due to the nonlinear dependence of the correlation (16) on . The root mean square for the correlation for the best fit value is 4.23% which shows that the model’s prediction for the correlation structure is not very good. The main problem as can be seen from a comparison between the prediction for the best fit in figure 6 and the actuall correlation structure in figure 3 is that the prediction is largely independent of the actual value of and largely determined by which is not the case in reality. The correlation rapidly increases as increases in reality.

8 Field Theory with Constrained Spot Rate

One clear fact we notice from the covariance of the innovations in the forward rates in figure 5 is that the covariance falls rapidly as . This observation leads one to a model [3] where is constrained to follow a normal distribution with variance . The mean of can be fixed at any value but will cause a corresponding change in which makes the mean value irrelevant. For calculational purposes it is easiest to assume that it remains at zero. This constraint can be implemented by modification of the action to

| (17) |

where is the action specified in (14). The propagator for this model is given by

| (18) |

After normalizing, we see that the prediction for the correlation structure is given by

| (19) |

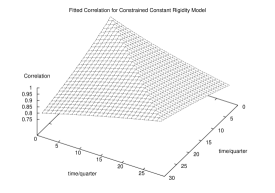

We can see that the free parameters are and . Further, it will be seen that it is easier to consider the ratio as it is dimensionless. The results of the Levenberg-Marquardt method showed that the fitted value of and were very small, of the order of /year for and for both being very unstable but the ratio was stable with a value in the range with an overall best fit of . The most reasonable explanation for this behaviour is that the ratio determines the behaviour of (19) for small and it is this region of parameter space that gives a correlation structure closest to the empirically observed one. We see from the fitted propagator in figure 7 that the behaviour at large is slightly better when the constraint is put in. The root mean square error was 3.35% which again means the fit was not very good though significantly better than if the constraint was not applied. It must be recognized that the constraint introduces one extra free parameter which should improve the best fit. Hence, we see that this model, while again performing better than HJM, is still not very accurate. While the results are not very good, they do represent a reasonable first approximation and are still significantly better than the one factor HJM model.

9 Field Theory Model with Maturity Dependent Rigidity

Another way to get a correlation structure that depends directly on the values of and in a significant way and not only on their difference is to make a function of . This has a direct physical meaning as it means that if we imagine the forward rate curve as a string, its rigidity is increasing as maturity increases making the for larger more strongly correlated if decreases as a function of . We choose the function as it declines to zero as becomes large as is expected from the observed covariance in figure 5, contains the constant case as a limit and is solvable. The action is given by

| (20) |

This is still a quadratic action and can be put into a quadratic form by performing integration by parts and setting the boundary term to zero since we are assuming Neumann boundary conditions. The inverse (Greens function) of the quadratic operator or the propagator for this action is found to be

| (21) |

where and where we have put the bound on the variable explicitly. The reason for this is that the limits have to be taken carefully in order to compare this model to the HJM in the limit and to the constant rigidity field theory model when .

Let us first consider the limit . First, we note

| (22) |

Therefore, we have

| (23) |

Similarly , and . Putting all these limits into (21) and performing some straightforward simplifications, we see that (21) becomes equal (10) in the limit . In the taking of this limit, we did not have any trouble with . However, for the HJM limit, we will see that the limit has to be taken only after the limit has been taken.

Let us now consider the limit . In this limit . Hence, only one term in (21) survive as all the others are multiplied by . This surviving term can be evaluated

| (24) |

The terms and obviously go to one in this limit and so were not included in the calculation above. This result can be seen to be equivalent to the HJM propagator after normalization. If the limit is taken first, then the propagator becomes

| (25) |

which exhibits a dependence in the limit . Hence, this cannot be made equivalent to HJM if the limits are taken in the wrong order. This problem is not present in the constant rigidity model.

For comparison with market data, we still take the limit as the model is then still directly related to the field theory model. The predicted correlation structure for this model is then given by

| (26) |

We fitted the parameters and to the correlation structure observed in the market in a similar manner as for the field theory model and obtained the results and . The root mean square error in the correlation was 3.35%. On performing the error analysis for the parameters, it is found that is very unstable but always very small (less than ) while the 90% confidence interval for is (0.099, 0.149). The relatively high value for seems to show that the falloff of the rigidity paramater is fairly rapid. The error is reduced from 4.23% to 3.35% but an extra parameter has had to be added and the model has become considerably more complicated due to the freedom of the form of the rigidity parameter . Further, we seem to be in the region of very small which does not behave well in the HJM limit. In fact, the correlation structure in this limit is given by

| (27) |

Due to the very small value of for the fitted function, this is a very good approximation for the fit. The obtained fit for the correlation function can be seen in figure 8.

The limited improvement, the relatively complicated form of the correlation and the near zero problem prompted us to consider a different way of approaching the problem which presented a much more satisfactory solution. This model is described in the next section

10 Field Theory Model with

To see where we might make an improvement, we notice that the predicted correlation structure with the field theory model is largely defined by the term which means that the correlation does not depend explicitly on the times and 222There is another term of the form but this has only a small effect on the correlation structure. However, we see immediately from figure 3 that the correlation increases significantly as we increase and . This is intuitively reasonable as market participants are likely to treat the difference between ten and fifteen years into the future quite differently from the difference between now and five years. Far out into the future, we would expect all times to be equivalent. In other words, there is good reason to expect 333Obviously, automatically implies . This is not satisfied by the constant rigidity models or by the varying rigidity model (if the limit is taken). For the latter model, this is slightly surprising since as and we might expect that for large the varying rigidity model should go into the HJM model limit (). However, this does not happen as previously discussed since we have taken the limit .

Further, the relatively marginal reduction of the error shows that varying the rigidity parameter does not quite reflect the data. An alternative way to consider the problem would be to use the observed correlation structure to induce a metric onto the direction. In some sense, this metric would be measuring the “psychological distance” in the investor’s minds which corresponds to a certain separation in maturity time. To make this concrete, let us write the observed correlation as . Since , and is symmetric as well. If we can show the triange property (which in the case of one dimension reduces to the straightforward condition that ), we can see that makes a good definition of distance in . From the market data, it can be shown that this rule is very approximately satisfied and we can use it as an approximate way to induce a metric onto the direction from the observed market data.

It should also be noted that introducing the metric is different from changing the form of the rigidity function . To see this, we write the action with the rigidity function as

| (28) |

where the functional variation of with has been absorbed into the variable (where is invertible) so that the above is a constant. With a change of variables we get the action as

| (29) |

where . With the introduction of the metric, we obtain the action

| (30) |

The Green’s functions for should be solved using the variables, and as expected the solution is given by . It can be shown that the martingale condition is satisfied with the Green’s function given by .

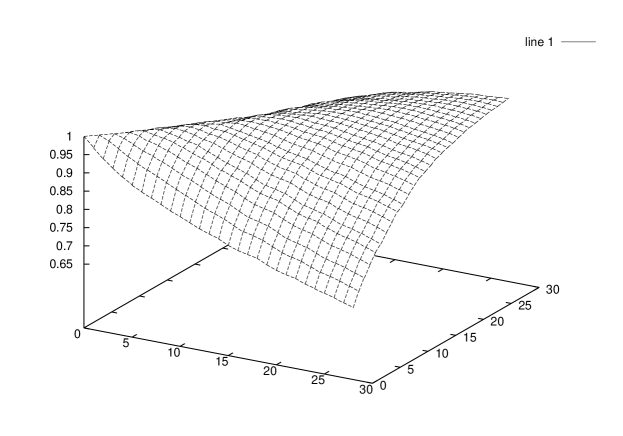

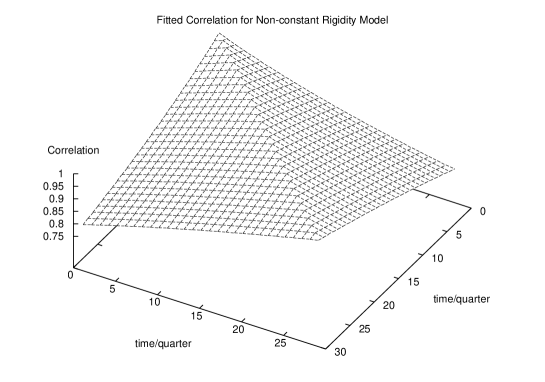

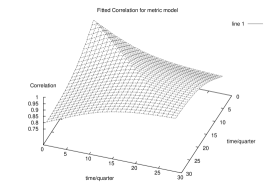

Bearing in mind the condition that, at large , the correlations should be close to 1, or equivalently that the distance should be small, we choose a metric that satisfies property, . We use this form of the metric to fit the correlation structure and obtain the result that and with a root mean square error of only 2.46%. Both parameters are also stable when the error analysis for the parameters is carried out. The 90% confidence interval for is (0.45, 0.58) and that for is (0.22, 0.33). Hence, we see that even the parameter estimation for this model is more robust as the parameters are atleast stable. Further, the shape of the fitted function is clearly closer to the observed one as can be seen from figures 4, 6, 7, 8 and 9. The error that remains is largely confined to the correlation between the spot rate and other forward rates which is not too surprising since the spot rate behaves very differently from the other forward rates.

We emphasize here that this involves a fundamentally new way of thinking of the interest rate models. So far, we have made models which generalized HJM so as to achieve a theory without too little freedom as in the one factor HJM model or too much freedom as in the two factor HJM model. While retaining this framework, we now use empirical data to guide us in refining the model to give us an insight into market psychology which will result from the induced metric.

11 Acknowledgements

We would like to thank Jean-Philippe Bouchaud and Science and Finance for kindly providing us with the data used for this study.

References

- [1] B. E. Baaquie, Physical Review E 64, 1 (2001).

- [2] B. E. Baaquie, Physical Review E 65, 056122 (2002), cond-mat/0110506.

- [3] B. E. Baaquie, Quantum finance, In preparation, 2002.

- [4] A. Matacz and J.-P. Bouchaud, International Journal of Theoretical and Applied Finance 3, 703 (2000).

- [5] B. E. Baaquie and M. Srikant, Empirical Investigation of a Quantum Field of Forward Rates, National University of Singapore http://xxx.lanl.gov/abs/cond-mat/0106317, 2002.

- [6] W. H. Press, S. A. Teukolsky, W. T. Vettering, and B. P. Flannery, Numerical Recipes in C : The Art of Scientific Computing, Cambridge University Press, 1995.