Volatility in Financial Markets:

Stochastic Models and Empirical Results

Abstract

We investigate the historical volatility of the 100 most capitalized stocks traded in US equity markets. An empirical probability density function (pdf) of volatility is obtained and compared with the theoretical predictions of a lognormal model and of the Hull and White model. The lognormal model well describes the pdf in the region of low values of volatility whereas the Hull and White model better approximates the empirical pdf for large values of volatility. Both models fails in describing the empirical pdf over a moderately large volatility range.

keywords:

Econophysics, Stochastic processes, Volatility. PACS: 89.90.+n, , and

1 Introduction

Volatility of financial time series is a key variable in the modeling of financial markets. It controls all the risk measures associated with the dynamics of price of a financial asset. It also affects the rational price of derivative products. In this paper we consider some stochastic volatility models proposed in the financial literature by investigating their ability in modeling statistical properties detected in empirical data. Specifically, we investigate the probability density function (pdf) of historical volatility for 100 highly capitalized stocks traded in the US equity markets. We observe that widespread volatility models such as the Hull and White model [1] and the lognormal model fail in describing the volatility pdf when we ask the model to describe both low and high values of volatility. Our results show that a lognormal pdf better describes low values of volatility whereas the Hull and White pdf gives a better approximation of the empirical pdf for large values.

2 Volatility models

The volatility of a financial asset is a statistical quantity which needs to be determined starting from market information [2]. It is the standard deviation of asset return (or, almost equivalently, of logarithm price changes of the asset). Different methodologies are used to infer volatility estimation from market data ranging from a direct calculation from past return data (historical volatility) to the computation of the volatility implied in the determination of an option price computed using the Black and Scholes formula [3] or some variant of it. There is a large empirical evidence that volatility is itself a stochastic process. In the present study we aim at comparing the theoretical predictions for the pdf of the volatility obtained with two different stochastic volatility models with empirical observations obtained for the 100 most capitalized stocks traded in US equity markets (mostly the New York Stock Exchange and the NASDAQ). The first model we consider is the Hull and White model [1]. In this model, the variance rate is described by the Ito’s equation

| (1) |

where and are parameters controlling the mean reverting nature of the stochastic process, is controlling its diffusive aspects and is a Wiener process. The stochastic process is reverting at a level at a rate . The exponent has been set to 1 in the investigation of Hull and White [1] and to 1/2 in the investigation of Heston [4]. In the present study we investigate the Hull and White model with . The Ito’s equation of this model for the volatility is

| (2) |

This equation has been obtained starting from Eq. (1) and using Ito’s lemma. The Hull and White model has associated a stationary pdf of the volatility which has the form

| (3) |

This pdf has a power-law tail for large values of . A power-law tail in the empirical volatility pdf has been observed in Ref. [5] for large values of the volatility. Another model is the lognormal model of volatility [6, 7]. An Ito’s stochastic differential equation associated with a lognormal pdf is

| (4) |

where , and are control parameters of the model. The two models are characterized by quite different pdfs especially for large values of the volatility where the Hull and White pdf shows a power-law behavior. The present study aims at detecting the regions of validity of these two models in empirical data.

3 Empirical Results

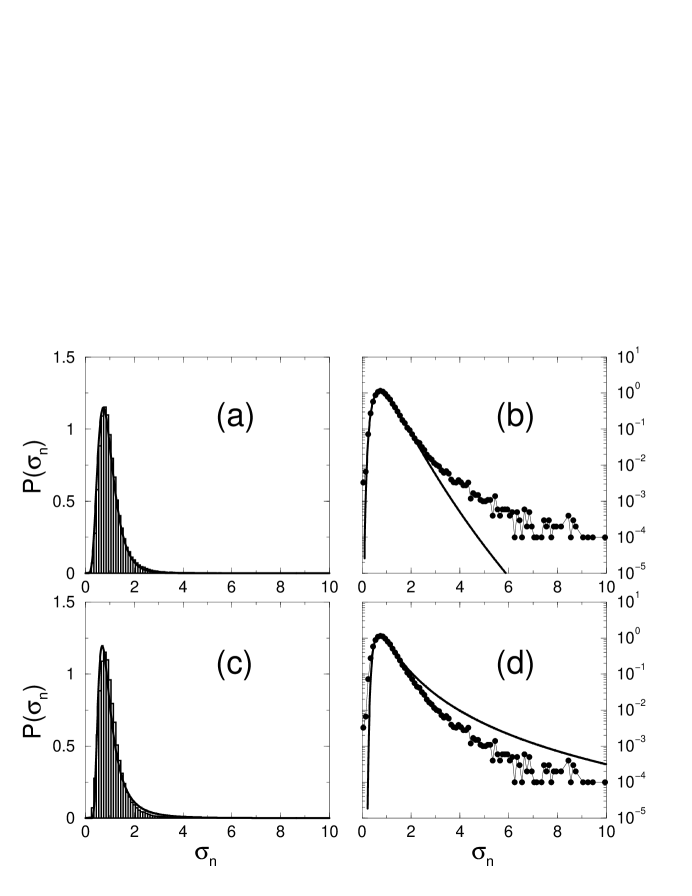

With this goal in mind, we investigate the statistical properties of volatility for the 100 most capitalized stocks traded in US equity markets during a 4 year time period. The empirical data are taken from the trade and quote (TAQ) database, maintained by the New York Stock Exchange (NYSE). In particular, our data cover the whole period ranging from January to December ( trading days). This database contains all transactions occurred for each stock traded in the US equity markets. The capitalization considered is the one recorded on August 31, . For each stock and for each trading day we consider the time series of stock price recorded transaction by transaction. Since transactions for different stocks do not happen simultaneously, we divide each trading day (lasting ) into intervals of seconds each. In correspondence to each interval, we define (intraday) stock’s prices proxies – with defined as the transaction price detected nearest to end of the interval (this a one possible way to deal with high-frequency financial data [8]).

We choose 12 intraday intervals since this value ensures that at least one transaction is in average observed in each interval for all considered stocks in the present study. For each stock we can thus compute a historical daily volatility as , where indicates the standard deviation of the argument of the function. Hence, for each stock we have values of daily volatility. These volatility data have then been analyzed to compute the volatility pdf for each stock. The 100 empirical pdfs we obtain are then fitted with the theoretical pdfs of the considered models. Due to the limited number of records used to estimate the empirical pdfs (1011 records per stock) the results of our fittings are not able to indicate strengths and weaknesses of the two models. For this reason we rescale the volatility value of each stock to its mean value and we investigate the pdf of the normalized variable for the ensemble of 100 stocks. In this way we obtain an empirical pdf which is quite accurate being based on the recording of 101,100 events. The best fittings of this empirical pdf with Eq. (3) and with a lognormal pdf are shown in Fig. 1. It should be noted that the form of Eqs (2) and (4) implies that the three control parameters of these equations reduce to two independent fitting parameters. For the lognormal pdf the fitting parameters can be chosen as the mean and the variance whereas for the Hull and White model the fitting parameters can be written as and . The top two panels show the best fittings of the lognormal pdf. The lognormal pdf describes very well low values of volatility in the interval but completely fails in describing large values . In particular a lognormal pdf underestimates large values of volatility. The bottom two panels show the best fits obtained with the Hull and White pdf. In this case the volatility low values are only approximately well described by the theoretical pdf. Moreover, for large values of volatility, the best fit overestimates by approximately a factor two empirical results. Both the lognormal model and the Hull and White models fail in describing well the normalized volatility over a relatively wide range of volatility values (). This implies that there is still room for the improvement of volatility models down to the basic aspect of well describing the asymptotic pdf of volatility over a realistically wide range. For example, we have verified that a volatility model described by the Ito’s equation

| (5) |

is characterized by a pdf which has intermediate properties to the ones of the pdfs of the two volatility models investigated in this paper. This model predicts a pdf of the volatility which has the form

| (6) |

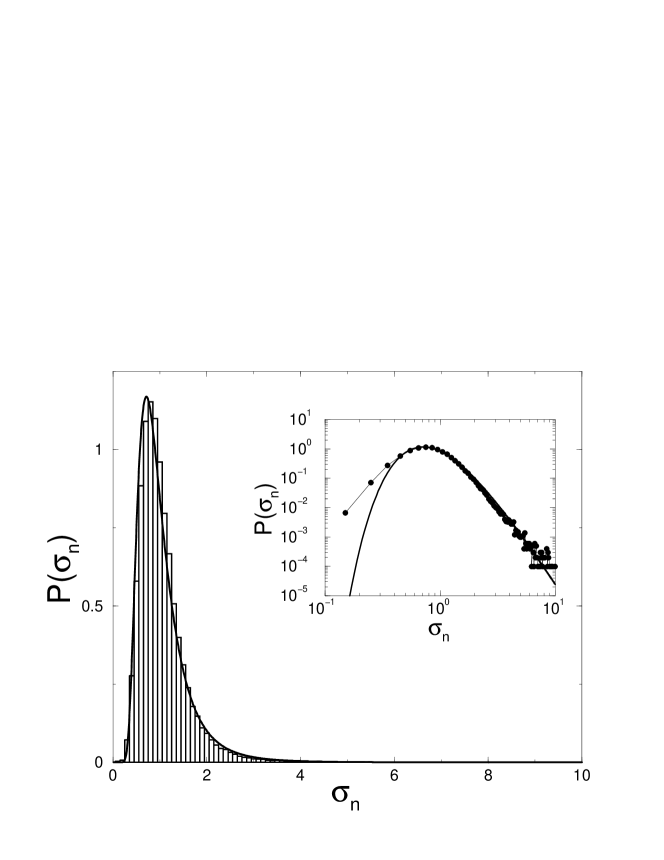

This pdf has also a power-law tail for large values of but it predicts a different shape for low values of . The two independent fitting parameters of this pdf can be written in terms of and . In Fig. 2 we show the best fit with the pdf of Eq. (6). The agreement with empirical data is rather good in a volatility range from to .

In summary, we report on a comparison of two widespread theoretical models of volatility with empirical data obtained by collecting together the volatility of 100 most capitalized stocks traded in US equity markets. The comparison is focused on the shape of the asymptotic pdf of volatility. Two widespread models (lognormal and Hull and White) fail in describing the pdf over a relatively wide volatility range. We show that the model of Eq. (5) improves the overall description of the pdf especially for values of normalized volatility . Further research attempts are needed to select the most appropriate Ito’s model able to describe volatility both under the aspects of the pdf and under the dynamics aspects of the nature and form of volatility auto-correlation function. Indeed, there is a growing evidence that the volatility autocorrelation function is long-range correlated [8] and this key aspect is not taken into account in most of the widespread models of volatility (as the ones considered in the present study) which are typically characterized only by short-range time memory.

References

- [1] J. Hull, A. White, Journal of Finance XLII (1987) 281.

- [2] J. C. Hull Options, Futures and Other Derivatives Prentice Hall, Inc. (1997)

- [3] F. Black, M. Scholes, Journal of Political Economy 81 (1973) 637.

- [4] S. L. Heston, Review of Financial Studies 6 (1993) 327.

- [5] Y. Liu, P. Gopikrishnan, P. Cizeau, M. Meyer, C.-K. Peng, H.E. Stanley, Phys. Rev. D 60 (1999) 1390.

- [6] P. Cizeau, Y. Liu, M. Meyer, C.-K. Peng, and H. E. Stanley, Physica A 245 (1997) 441.

- [7] M. Pasquini, M. Serva, Physica A 269 (1999) 140.

- [8] M.M. Dacorogna, R. Gencay, U.A. Müller, R.B. Olsen, O.V. Pictet, An Introduction to High-Frequency Finance, Academic Press (2001)