A Path Integral Way to Option Pricing

Abstract

An efficient computational algorithm to price

financial derivatives is presented. It is based on a path integral

formulation of the pricing problem. It is shown how the path integral

approach can be worked out in order to obtain fast and accurate

predictions for the value of a large class of

options, including those with path-dependent and early exercise

features. As examples, the application of the method to European and

American options in the Black-Scholes model is illustrated.

A particularly simple and fast semi-analytical approximation for the price

of American options is derived.

The results of the algorithm are compared with those obtained with the standard

procedures known in the literature and found to be in good agreement.

keywords:

Econophysics; Stochastic Processes; Path Integral; Financial Derivatives; Option Pricing.pacs: 02.50.Ey - 05.10.Gg - 89.75.-k

FNT/T-2001/19

1 Introduction

The classical theory of option pricing is based on the results found in 1973 by Black and Scholes [1] and, independently, Merton [2]. Their pioneering work starts from the basic assumption that the asset prices follow the dynamics of a particular stochastic process (geometric Brownian motion), so that they have a lognormal distribution [3, 4]. In the case of an efficient market with no arbitrage possibilities, no dividends and constant volatilities, they found that the price of each financial derivative is ruled by an ordinary partial differential equation, known as the Black-Scholes-Merton (BSM) formula. In the most simple case of a so-called European option, the BSM equation can be explicitly solved to obtain an analytical formula for the price of the option [3, 4]. When we consider other financial derivatives, which are commonly traded in real markets and allow anticipated exercise and/or depend on the history of the underlying asset, the BSM formula fails to give an analytical result. Appropriate numerical procedures have been developed in the literature to price exotic financial derivatives with path-dependent features, as discussed in detail in Refs. [3, 5, 6]. The aim of this work is to provide a contribution to the problem of efficient option pricing in financial analysis, showing how it is possible to use path integral methods to develop a fast and precise algorithm for the evaluation of option prices.

The path integral method, which traces back to the original work of Wiener and Kac in stochastic calculus [7, 8] and of Feynman in quantum mechanics [9], is today widely employed in chemistry and physics, and very recently in finance too [10, 11, 12, 13, 14], because it gives the possibility of applying powerful analytical and numerical techniques [15]. Following recent studies on the application of the path integral approach to the financial market as appeared in the econophysics literature (see Refs. [12, 14] for a comprehensive list of references), this paper is devoted to present an original, efficient path integral algorithm to price financial derivatives, including those with path-dependent and early exercise features, and to compare the results with those obtained with the standard procedures known in the literature.

The paper is organized as follows. In Section 2 the basic ideas of the classical theory of option pricing are summarized, discussing the computational complexity associated to the evaluation of the price of a path-dependent option and reviewing the standard numerical procedures adopted in the literature. In Section 3 the path integral approach to option pricing is described and analytically developed in order to obtain an efficient procedure for the calculation of the transition probability associated to a given stochastic model of asset evolution. Theoretical and computational details to obtain fast predictions for path-dependent options are also described. As applications of the method, numerical results for European and American options in the BSM model are given in Section 4, together with comparisons with results known in the literature. A particularly simple and very quick semi-analytical approximation for the price of an American option is derived in Section 5, by exploiting the possibility of anticipated exercise for any time before the expiration date. Conclusions and possible perspectives are drawn in Section 6.

2 Option pricing: theory and numerical procedures

2.1 Classical theory and path-dependent options

The basic ingredient for the development of a theory of option pricing is a suitable model for the time evolution of the asset prices. The assumption of the BSM model is that the price of an asset is driven by a geometric Brownian motion and verifies the stochastic differential equation (SDE) [3, 4]

| (1) |

which, by means of the Itô lemma, can be cast in the form of an arithmetic Brownian motion for the logarithm of

| (2) |

where is the volatility, , is the drift parameter and is the realization of a Wiener process. By virtue of the properties of a Wiener process, eq. (2) may be written as

| (3) |

where follows from a standardized normal distribution with mean 0 and variance

1.

Thus, in terms of the logarithms of the asset prices

,

the conditional transition probability to have at the

time a price under the hypothesis that the price was at the time is

given by [4, 10]111The correct way to indicate conditional transition probabilities is

. We omit the times in order to simplify the notation.

| (4) |

which is a gaussian distribution with mean and variance .

If we require the options to be exercised

only at specific times , the asset price, between two

consequent times and , will follow eq. (3) and the

related transition probability will be

| (5) |

with .

A time-evolution model for the asset price is strictly necessary in a theory of option pricing because the fair price at time of an option , without possibility of anticipated exercise before the expiration date or maturity (a so-called European option), is given by the scaled expectation value [3]

| (6) |

where is the risk-free interest and

indicates the mean value, which can be computed only if

a model for the asset underlying the option is understood.

For example, the value of an European call

option at the maturity will be

, where is the strike price, while

for an European put option the value at the maturity will

be . It is worth emphasizing, for what follows, that the

case of an European option is particularly simple, since in such a situation

the price of the option can be evaluated by means of analytical formulae,

which are obtained by solving the BSM partial differential equation

with the appropriate boundary

conditions [3, 4]. On the other hand, many further

kinds of options are present in the financial markets, such as American options

(options which can be exercised at any time up to the expiration date) and

exotic options [3], i.e. derivatives with complicated payoffs or whose value

depend on the whole time evolution of the underlying asset and not just on its value

at the end. For such options with path-dependent and early exercise features

no exact solutions are available and pricing them correctly is a great challenge.

Actually, in the case of options with possibility

of anticipated exercise before the expiration date, the above discussion

needs to be generalized, by introducing a slicing

of the time interval . Let us consider, for definiteness,

the case of an option which can be exercised within the maturity

but only at

the times

At each time slice the value of the

option will be the maximum between its expectation value at the time

scaled with and its value in the case of

anticipated exercise

222For example, the value of a call

option in the case of exercise at the time will be

, being the strike price.. If

denotes the price of the underlying

asset at the time , we can thus write for each

| (7) |

where is the conditional

expectation value of , i.e. its expectation value under

the hypothesis of having the price at the time

. In this way, to get the actual price ,

it is necessary to proceed backward

in time and calculate , where the value

of the option at maturity is nothing but

. It is therefore clear that evaluating the price

of an option with early exercise features means to simulate the evolution of the

underlying asset price (to obtain the ) and to

calculate a (usually large) number of expectation

conditional probabilities.

2.2 Standard numerical procedures

To value derivatives when analytical formulae are not available, appropriate numerical techniques have to be advocated. They involve the use of Monte Carlo (MC) simulation, binomial trees (and their improvements) and finite difference methods [3, 5].

A natural way to simulate price paths is to discretize eq. (3) as

or, equivalently,

| (8) |

which is correct for any , even if finite. Given the spot price , i.e. the price of the asset at time , one can extract from a standardized normal distribution a value for the random variable to simulate one possible path followed by the price by means of eq. (8):

Iterating the procedure times, one can simulate price paths , to which apply the procedure exemplified in Section 2.1 and evaluate the price of the option. In such a MC simulation of the stochastic dynamics of asset price (Monte Carlo random walk) the mean values can be simply obtained as

with no need to calculate transition probabilities because, through

the extraction of the possible values, the paths

are automatically weighted according to the

probability distribution function of eq. (5).

Unfortunately, this method leads to an estimated value whose

numerical error

is proportional to . Thus, even if it is powerful

because of the possibility to control the paths and to

impose additional constrains (as it is usually required by

exotic and path-dependent options), the MC random

walk is extremely time consuming when precise predictions are required

and appropriate variance reduction procedures have to be

used to save CPU time [3].

This difficulty can be overcome by means of the method of

the binomial trees and its extensions (see [3] and

references therein), whose main idea

stands in a deterministic choice of the possible paths to limit the number of

intermediate points. At each time step the price is

assumed to have only two choices: increase to the value

or decrease to , where the parameters

and are

given in terms of and in such a way to give the

correct values for the mean and variance of stock price changes over

the time interval .

Also finite difference methods are known in the literature [3] as an

alternative to time-consuming MC simulations. They provide

the value of the derivative by solving the differential equation satisfied

by the derivative, by converting it into a difference equation. Although

tree approaches and finite difference methods are known to be faster than

the MC random walk, they are difficult to apply when a detailed

control of the history of the derivative is required and are also

computationally time consuming when a number of stochastic variables

is involved [3]. It follows that the development of efficient and fast

computational algorithms to price financial derivatives is still

a key issue in financial analysis.

3 The path integral method

The path integral method is an integral formulation of the

dynamics of a stochastic process. It is a suitable framework

for the calculation of the transition probabilities associated

to a given stochastic process, which is seen as the convolution of

an infinite sequence of infinitesimal short-time steps [10, 15].

For the problem of option pricing,

the path integral method can be employed for the

explicit calculation of the expectation values

of the quantities of financial interest, given by

integrals of the form [10]

| (9) |

where and is the transition probability. is the conditional expectation value of some functional of the stochastic process. For example, for an European call option at the maturity the quantity of interest will be , being the strike price. As already emphasized, and discussed in the literature [3, 5, 6, 11, 14], the computational complexity associated to this calculation is generally great: in the case of exotic options, with path-dependent and early exercise features, integrals of the type (9) can not be analytically solved. As a consequence, we demand two things from a path integral framework: a very quick way to estimate the transition probability associated to a stochastic process (3) and a clever choice of the integration points with which evaluate the integrals (9). In particular, our aim is to develop an efficient calculation of the probability distribution without losing information on the path followed by the asset price during its time evolution.

3.1 Transition probability

The probability distribution function related to a SDE verifies the so-called Chapman-Kolmogorov equation [4], i.e. the relation

| (10) |

which states that the probability (density) of a transition

from the value (at time ) to the value (at time

) is the “summation” over all the possible

intermediate values of the probability of separate and

consequent transitions , .

As a consequence, if we consider a finite time interval and we

apply a time slicing,

by considering subintervals of length , we can write, by iteration of eq. (10)

which, thanks to eq.(4), can be written as

| (11) |

In the limit , such that (infinite sequence of infinitesimal time steps), the expression (11), as explicitly shown in Ref. [10], exhibits a Lagrangian structure and it is possible to express the transition probability in the path integral formalism as a convolution of the form [10]

where is the Lagrangian

and the integral is performed (with functional measure )

over the paths

belonging to , i.e. all the continuous functions with constrains

, .

As carefully discussed

in Ref. [10], a path integral is well defined only if both a continuous formal

expression and a discretization rule are given. As done in many applications,

the Itô prescription is adopted in the present work.

A first, naïve evaluation of the transition probability (11)

can be performed via Monte Carlo simulation, by writing

eq. (11) as

| (12) |

in terms of the variables defined by the relation

| (13) |

and extracting each from a gaussian distribution of mean and variance . However, as we will see, this method requires a large number of calls to obtain a good precision. This is due to the fact that each is related to the previous , so that this implementation of the path integral approach can be seen to be equivalent to a naïve MC simulation of random walks, with no variance reduction.

By means of appropriate

manipulations [15] of the integrand entering eq. (11),

it is possible, as shown in the following, to

obtain a path integral expression which

will contain a factorized integral with a constant kernel and a

consequent variance reduction. We will refer to this second

implementation of the method as path integral with importance sampling.

If we define

and , , we

can express the transition probability distribution as

| (14) |

in order to get rid of the contribution of the drift parameter. Now let us extract from the argument of the exponential function a quadratic form

| (15) |

by introducing the -dimensional array and the matrix defined as

| (16) |

where is a real, symmetric, non singular and tridiagonal matrix. In terms of the eigenvalues of the matrix , the contribution in eq. (15) can be written as

| (17) |

by introducing the orthogonal matrix which diagonalizes , with . Because of the orthogonality of , the Jacobian

of the transformation equals 1, so that . Thanks to eqs. (16)-(17), and after some algebra, eq. (15) can be written as

| (18) |

Now, if we introduce new variables obeying the relation

| (19) |

it is possible to express the finite-time probability distribution as

| (20) |

Equation (20) is one of the main results of the present work. Actually, the probability distribution function, as given by eq. (20), is an integral whose kernel is a constant function (with respect to the integration variables) and which can be factorized into the integrals

| (21) |

given in terms of the , which are gaussian variables

that can be extracted

from a normal distribution

with mean and variance

. Differently to the first, naïve

implementation of the path integral, now each is no longer

dependent on the previous , and importance sampling over

the paths is automatically accounted for.

It is worth noticing that, by means of the extraction of

the random variables , we are creating price

paths, since at each intermediate time the asset price is given

by

| (22) |

Therefore, the path integral algorithm can be easily adapted to the cases

in which the derivative to be valued has, in the time

interval , additional

constraints, as in the case of interesting path-dependent options,

such as Asian and barrier options [3].

The results of the

two realizations of the path integral method here discussed

will be compared in

Section 4.

3.2 Integration points

Thanks to the method illustrated in Section 3.1, a powerful

and fast tool to compute the transition probability

in the path integral framework is available and it can be employed if

we need to value a generic option with maturity and with

possibility of anticipated exercise at times

(. As a consequence of this time slicing,

one must numerically evaluate

mean values of the type (9),

in order to

check at any time , and for any value of the stock price,

whether early exercise is more convenient with respect to

holding the option for a future time. To keep under

control the computational complexity and the time of execution,

it is mandatory to

limit as far as possible the number of points for the integral

evaluation. This means that we would like to have a linear growth

of the number of integration points with the time.

Let us suppose to evaluate each mean value

with integration points, i.e. considering only fixed values for . To this end, we can create a grid of possible prices, according to the dynamics of the stochastic process as given by eq. (3)

| (23) |

Starting from , we thus evaluate the expectation value with values of centered333Let us recall that between two possible exercise times the probability distribution function is gaussian and it is therefore symmetrical with respect to its mean value. on the mean value and which differ from each other of a quantity of the order of

Going on like this, we can evaluate each expectation value obtained from each one of the ’s created above with values for centered around the mean value

Iterating the procedure until the maturity, we create a

deterministic grid of points

such that, at a given time , there are values of

, in agreement with the request of linear growth.

This procedure of selection of integration points, together with

the calculation of the transition

probability previously described, is the basis of our

path integral simulation of the

price of a generic option.

4 Numerical results and discussion

By applying the results derived in Section 3, we have at disposal an efficient path integral algorithm both for the calculation of transition probabilities and the evaluation of option prices. In the present section, the application of the method to European and American options in the BSM model is illustrated and comparisons with the results obtained with the standard procedures known in the literature are shown.

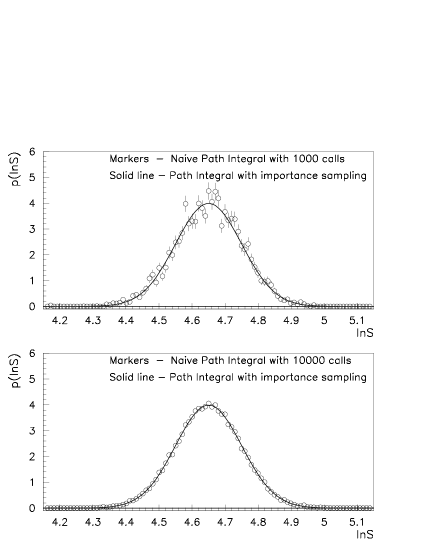

First, the path integral simulation of the probability distribution

of the logarithm of the stock prices, , as a function of the

logarithm of the stock price,

for a BSM-like stochastic model, as given by eq. (2), is shown in

Fig. 1. The parameters used in the simulation are: ,

, , , year and year,

with 100 time slices. As can be seen, the expected lognormal distribution of

the stock prices is correctly reproduced by the path integral

numerical simulation. The plot shows

a comparison of the calculation of as obtained by means of the

two path integral algorithms described

in Section 3.1. The markers correspond

to the naïve path integral computation of the probability distribution,

without variance

reduction, for (upper plot) and (lower plot)

MC iterations. The error bars indicate the statistical error

of the MC calculation. The solid line is the prediction for as

obtained with the path integral simulation with importance sampling. In

such a case, only two calls for each variables

are needed to correctly fit a gaussian

distribution, the numerical error being totally negligible and the

algorithm very fast, with a typical execution time of a few seconds

on a PentiumIII 500 Mhz PC. On the contrary,

the first path integral implementation

is much less accurate and CPU time consuming. This is a consequence of the

fact that, in the path integral simulation with importance sampling,

the presence of constant integration kernel squeezes to zero the

standard estimation error. The diagonalization of the tridiagonal

matrix , which is a basic ingredient of the efficient path integral

algorithm developed, is performed according to the standard numerical

procedure described in Ref. [16], realized by means of the routine

F02FAF of the NAG program library [17], while the generation of

the gaussian

variables follows from the routine RNORML of the CERN program library.

| analytical | binomial tree | GFDNM | path integral | |

|---|---|---|---|---|

| 6.0 | 3.558 | 3.557 | 3.557 | 3.558 |

| 8.0 | 1.918 | 1.917 | 1.917 | 1.918 |

| 10.0 | 0.870 | 0.866 | 0.871 | 0.870 |

| 12.0 | 0.348 | 0.351 | 0.349 | 0.348 |

| 14.0 | 0.128 | 0.128 | 0.129 | 0.128 |

As previously emphasized, the knowledge of the asset price at each intermediate time through eq. (22) gives the possibility of applying the procedure of calculation of the transition probability illustrated in Section 3.1 also to those types of financial derivatives whose payoff depends on the price path of the underlying asset. For such exotic options, the fast computation of the transition probability is a basic ingredient of our path integral algorithm as an efficient alternative to time-consuming MC simulation.

Once the transition probability has been computed, the price of an option can be computed in a path integral approach as the conditional expectation value of a given functional of the stochastic process. For example, the price of an European call option will be given by

| (24) |

while for an European put it will be

| (25) |

where is the risk-free interest rate. Therefore just one-dimensional integrals need to be evaluated. They can be precisely computed with standard quadrature rules. In our calculation, the one-dimensional integrals are simply performed with a standard trapezoidal rule, cross-checked with the routine of adaptive integration D01EAF from the NAG library [17]. A sample of the results obtained for an European put option in the BSM model is shown in Tab. 1. The predictions of our approach, indicated as path integral, are compared with results available in the literature, as quoted in Ref. [11]. In Tab. 1, the entries correspond to the analytical results, the results by binomial trees, and the results of the Green Function Deterministic Numerical Method (GFNDM) developed in Ref. [11]. As can be noticed, our results are in perfect agreement with the analytical predictions, while the differences with the other numerical procedures are within the 1% level. The errors in our numbers as due to numerical integration are not specified being well below the digits quoted.

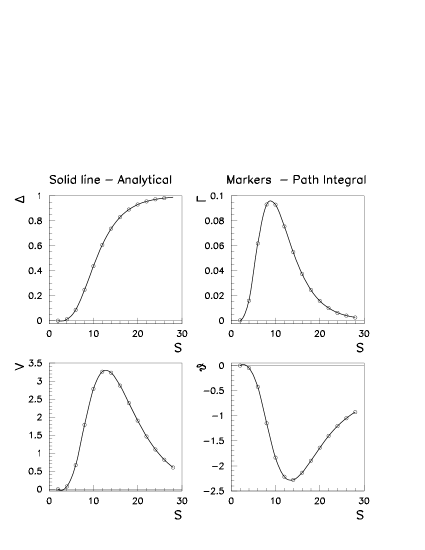

Further numerical results of our path integral method are shown in Fig. 2, where the behaviour of the Greek letters [3] of an European call option in the BSM model is plotted as a function of the stock price. The solid lines correspond to the analytical predictions, while the markers are the results by our path integral approach. The model parameters used in the simulation are: , , , year and year. The four Greeks shown are important variables to manage the risk associated to an option and are defined as [3]

where is the price of the European call option. They are computed through standard numerical differentiation of the numerical value returned by the path integral, by means of the NAG routine D04AAF [17]. Also for the Greeks, there is perfect agreement between the results obtained via our path integral simulation and the analytical predictions.

To test the reliability of the sampling over the integration points discussed in Section 3.2, we present results for the particular case of the price of an American option in the BSM model in Tab. 2, as obtained with the grid technique described in Section 3.2. Comparisons with independent results available in the literature are also shown. As can be seen from Tab. 2, there is generally a good agreement of our path integral results with those known in the literature [11] and obtained by means of the binomial tree, of the finite difference method and of the GFDNM method. It is worth noticing that our results in the path integral framework require only a few seconds on a PentiumIII 500MhZ PC.

| finite difference | binomial tree | GFDNM | path integral | |

|---|---|---|---|---|

| 6.0 | 4.00 | 4.00 | 4.00 | 4.00 |

| 8.0 | 2.095 | 2.096 | 2.093 | 2.095 |

| 10.0 | 0.921 | 0.920 | 0.922 | 0.922 |

| 12.0 | 0.362 | 0.365 | 0.364 | 0.362 |

| 14.0 | 0.132 | 0.133 | 0.133 | 0.132 |

5 The limit of continuum and American options

In the case of an American option, the possibility of exercise

at any time up to the expiration date

allows to develop, within the path integral formalism,

a specific algorithm, which, as shown in the following,

is precise and very quick.

Given the time slicing considered in Section 3.2, the case of

American options requires the limit which, putting

,

leads to a delta-like transition probability

This means that, apart from volatility effects, the price at time will have a value remarkably close to the expected value , given by the drift growth. Needless to say, if we should substitute the expression inside the integrals (9), we would neglect the role of the volatility and consider only a drift growth of the asset prices. In order to take care of the volatility effects, a possible solution is to estimate the integral of interest, i.e.

| (26) |

by inserting in eq. (26) the analytical expression for the transition probability

together with a Taylor expansion of the kernel function around the expected value . Hence, up to the second order in , the kernel function becomes

| (27) |

which, together with eq. (5), yields

| (28) |

since the first derivative does not give contribution to eq. (26), being the integral of an odd function over the whole range. The second derivative can be numerically estimated as

| (29) |

with , as dictated by the

dynamics of the stochastic process.

| finite difference | binomial tree | GFDNM | path integral | |

|---|---|---|---|---|

| 6.0 | 4.00 | 4.00 | 4.00 | 4.00 |

| 8.0 | 2.095 | 2.096 | 2.093 | 2.095 |

| 10.0 | 0.921 | 0.920 | 0.922 | 0.922 |

| 12.0 | 0.362 | 0.365 | 0.364 | 0.362 |

| 14.0 | 0.132 | 0.133 | 0.133 | 0.132 |

It is worth noticing that each expectation value can be now computed once and are known. Consequently, if we employ the deterministic grid illustrated in Section 3.2, it is enough to put to obtain reliable results, provided is taken sufficiently small. Actually, the results obtained with this simple semi-analytical procedure are shown in Tab. 3, using for numerical differentiation and 300 time slices. For such path integral evaluation of an American option the CPU time is negligible. The results are in nice agreement with those of other numerical procedures and in perfect agreement, as we explicitly checked for different model parameters, with those quoted in Tab. 2 as obtained with the path integral algorithm discussed in Section 3.2.

6 Concluding remarks and outlook

In this paper we have shown that the path integral approach to stochastic processes can be successfully applied to the problem of option pricing in financial analysis. In particular, an efficient implementation of the path integral method has been presented, in order to obtain fast and accurate predictions for a large class of financial derivatives, including those with path-dependent and early exercise features. The key points of the algorithm are a careful evaluation of the transition probability associated to the stochastic model for the time evolution of the asset prices and a suitable choice of the integration points needed to evaluate the quantities of financial interest. Furthermore, a simple and very fast procedure to value American options has been derived, by exploiting the possibility of continuous exercise up to the expiration date.

The results of the path integral algorithm have been carefully compared with those available in the literature for European and American options in the BSM model and found to be in good agreement with the standard numerical procedures used in finance. The computational time of the algorithm developed is, to the best of our knowledge, competitive with the most efficient strategies used in finance. The method is general and it can be quite easily extended to cope with other financial derivatives (with path-dependent features) and other models beyond the dynamics of geometric Brownian motion.

The natural developments of the path integral algorithm here presented concern the application of the method to value other kinds of quantities of financial interest, for which the analytical solution is not available or not accessible, and the extension of the method of option pricing to more realistic model of the financial dynamics, such as models with stochastic volatility [3, 12, 18] or beyond the BSM Gaussian limit [19, 20, 21, 22, 23, 24], in order to search for a better agreement with the real prices as observed in the real market. A further interesting perspective would be using the path integral algorithm as a benchmark to train neural networks.

Such developments are by now under consideration.

Acknowledgments

We acknowledge collaboration of F. Piccinini at the early stage

of this work. We wish to thank M. Cersich, E. Melchioni and A. Pallavicini of

FMR Consulting for useful discussions. We are also grateful to FMR

Consulting for having provided the software for the analytical

predictions of the price and Greeks of European options.

References

- [1] F. Black and M. Scholes, Journal of Political Economics 72 (1973) 637.

- [2] R. Merton, Bell J. Econom. Managem. Sci. 4 (1973) 141.

- [3] J.C. Hull, Options, Futures, and Other Derivatives, Fourth Edition, Prentice Hall, New Jersey, 2000.

- [4] W. Paul and J. Baschnagel, Stochastic Processes: from Physics to Finance, Springer-Verlag, Berlin Heidelberg, 1999.

- [5] P. Wilmott, J. Dewynne and S. Howinson, Option Pricing: Mathematical Models and Computation, Oxford Financial Press, Oxford, 1993.

- [6] M. Potters, J.-P. Bouchaud and D. Sestovic, Physica A 289 (2001) 517.

- [7] N. Wiener, Proc. Nat. Acad. Sci. (USA) 7 (1952) 253; Proc. Nat. Acad. Sci. (USA) 7 (1952) 294.

- [8] M. Kac, Bull. Amer. Math. Soc. 72 (1966) 52.

-

[9]

R. P. Feynman, Rev. Mod. Phys. 20 (1948) 367;

R. P. Feynman and A. R. Hibbs, Quantum Mechanics and Path Integral, McGraw-Hill, New York, 1965. - [10] E. Bennati, M. Rosa-Clot and S. Taddei, A Path Integral Approach to Derivative Security Pricing: I. Formalism and Analytical Results, Int. Journ. Theor. Appl. Finance 2 (1999) 381, cond-mat/9901277.

- [11] M. Rosa-Clot and S.Taddei, A Path Integral Approach to Derivative Security Pricing: II. Numerical Methods, cond-mat/9901279.

- [12] B.E. Baaquie, J. Phys. I France 7 (1997) 1733.

- [13] L. Ingber, High-Resolution Path-Integral Development of Financial Options, physics/0001048.

- [14] A. Matacz, Path Dependent Option Pricing: the Path Integral Partial Averaging Method, cond-mat/0005319.

- [15] L.S. Schulman, Techniques and Applications of Path Integration, John Wiley & Sons, New York, 1981.

- [16] W.H. Press, B.P. Flannery, S.A. Teukolsky and W.T. Vetterling, Numerical Recipes - The Art of Scientific Computing, Cambridge University Press, New York, 1989.

- [17] NAG Fortran library, The Numerical Algorithms Group Ltd, Oxford.

-

[18]

J.C. Hull and A. White, Journal of Finance 42 (1987) 281;

J. Masoliver and J. Perello, A Correlated Stochastic Volatility Model Measuring Leverage and Other Stylized Facts, cond-mat/0111334. - [19] R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge University Press, Cambridge, 2000.

- [20] J.P. Bouchaud and M. Potters, Theory of Financial Risk: from Statistical Physics to Risk Management, Cambridge University Press, Cambridge, 2000.

- [21] B.B. Mandelbrot, Fractals and Scaling in Finance, Springer-Verlag, Berlin Heidelberg, 1997.

-

[22]

R.N. Mantegna and H.E. Stanley,

Phys. Rev. Lett. 73 (1994) 2946;

R.N. Mantegna and H.E. Stanley, Nature 383 (1996) 587;

R.N. Mantegna, Z. Palágyi and H.E. Stanley, Physica A 274 (1999) 216. - [23] A. Matacz, Financial Modeling and Option Theory with the Truncated Levy Process, cond-mat/9710197.

- [24] Frederick Michael and M.D. Johnson, Financial Market Dynamics, cond-mat/0108017.