For APFA3, London, Dec. 2001

Nucleation of Market Shocks in Sornette-Ide model

Ana Proykova1, Lena Roussenova2 and Dietrich Stauffer3

1 Department of Atomic Physics, University of Sofia, Sofia-1126, Bulgaria

2 Department of Finance, University of National and World Economy, Sofia, Bulgaria

3 Institute for Theoretical Physics, Cologne University, D-50923 Köln, Euroland

Abstract: The Sornette-Ide differential equation of herding and rational trader behaviour together with very small random noise is shown to lead to crashes or bubbles where the price change goes to infinity after an unpredictable time. About 100 time steps before this singularity, a few predictable roughly log-periodic oscillations are seen.

Bubbles and crashes are a property of market prices since centuries. Some may arise from external perturbations like changes of the interest rate by the central bank, government decisions on war and peace, or for stocks of single companies the introduction of new (un)successful products. Some, like the October 1987 crash on Wall Street, may arise from intrinsic market mechanisms [1]. While we cannot make a clear distinction between external and intrinsic reasons for a crash in reality, we can do so at least in computer simulations. There a single external event can be put in explicitly into the program, the multitude of individual decisions can be approximated by a small random noise while the general rational as well as psychological (“herding”) behaviour of investors and traders can be approximated by deterministic algorithms. We show here that in the Sornette-Ide [2,3] approach this small noise can escalate to a singularity (bubble or crash) where the price change goes to .

The Sornette-Ide approach [2] used two different contributions. One is the nonlinear fundamentalist assumption of [3] that traders buy (sell) if the prices are low (high). Thus a positive difference between the actual and the perceived fundamental price encourages selling and thus causes a downwards tendency in such that is proportional to . This effect stabilizes prices. But a rising price, , creates the hope or illusion that the price will increase further and thus will encourage further buying, with varying as ; this second term alone leads to a divergence at some critical time (bubble or crash). The combination of both terms leads to roughly [4] log-periodic oscillations preceding the singularity, which may be used to make profit or to prevent this singularity.

The deterministic nonlinear differential equation for the “return” (the logarithm of the current price to the initial “fundamental” or “equilibrium” price) and its velocity (short-time return) is

if and are odd integers. The damped harmonic oscillator has . Suitable absolute values are needed if and are not odd integers [2]. Noise can be introduced here in various ways: Chang et al [5] added a small random value to ; then after a long time regular oscillations appeared, of increasing strength and decreasing period, until diverged. While this behaviour is what we want, the assumption about the noise has little justification except that it is close to Langevin equations.

We instead first made vary randomly between 0 and +1, but then the curves were too regular, and different initial seeds for the random number generator gave nearly the same curves. This multiplicative assumption was supposed to simulate the volatile psychology of the traders who follow more or less the current trend. When we applied the random noise to instead of this noise influenced the prices more strongly but we got oscillations right from the beginning while we want them to emerge only later. Also applying noise to did not give satisfactory results.

To get better results, in our second method we made a multiplication for itself, not for a contribution to its time derivatives. Thus the resulting from the discretized differential equation was multiplied by a factor which differed from unity by a small amount between –0.0001 and +0.0001. Since we use multiplication instead of addition, we cannot start with and both zero, and thus took initially, to create some fluctuations. We thus assume that traders decide in a deterministic way on fundamental value through and on herding through , but finally some small randomness also affects the market.

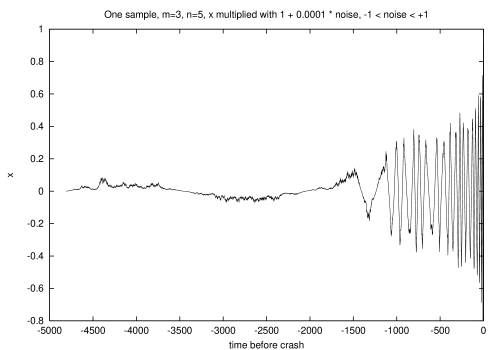

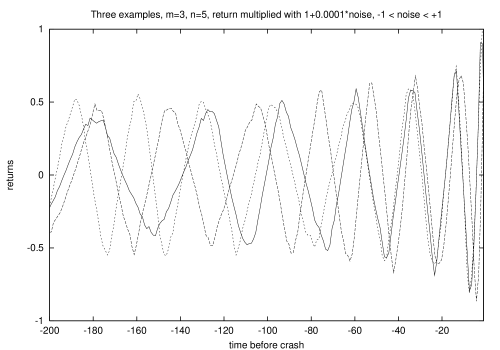

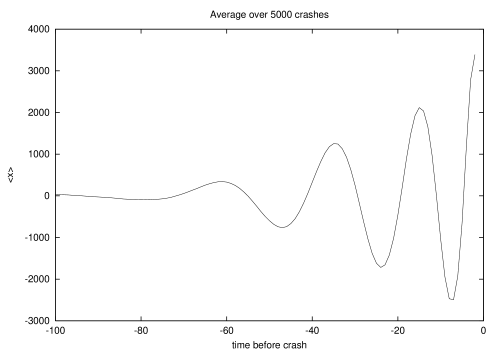

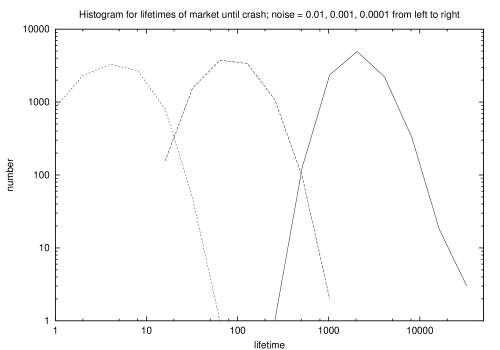

Figure 1 shows a run over all nearly 5000 time steps, Fig.2 is the same run over the last 200 time steps before the crash, together with two other runs using the same parameters but different random numbers. We see that first the prices fluctuate in a rather random way about the fundamental value. In other runs, the noise can make the deviations larger leading to a few nearly regular oscillations which die down again. Finally, again such oscillations occur, but now they become stronger, faster and finally lead to a crash at time = 0. Averaging over thousands of samples gives smooth oscillations before the crash, Fig.3. If we increase the noise, the times needed for a crash to build up get shorter and there are less oscillations; these times are roughly log-normally distributed, Fig.4.

Mathematically it is easy to understand why this second method works better than our first method. In the first method, the noise affects the time derivative only, meaning it changes the curvature or slope of only. Our second method affects directly.

Without any noise, the origin of the phase space plays a special role as the unstable fixed point around which spiral structures of trajectories are organized. It corresponds to the case of fundamental prices; there is no trend and the market does not know which direction to take.

Our parameters for this simulation were . We used the leap frog method of molecular dynamics with 1000 iterations per unit time. Thus first we calculate from the above equation the acceleration , from the change in the velocity , and finally the new is obtained by first adding to it using the new velocity, and then multiplying by , with selected randomly between –0.0001 and + 0.0001.

The “noise” symbolizes all the new information coming in every day (or every simulation interval). We also tried to simulate insider trading: Half of the market movement uses not today’s noise but the one of tomorrow. Not much is changed since the equations describe the overall market behaviour, not the profits of some at the expense of others.

Of course, this method is similar to that of Chang et al; the main difference is that the present noise in is proportional to while for Chang et al it is independent of . An additional linear friction term, restricts the fluctuations mostly to one sign, except for very small friction coefficients .

We thank D. Sornette for helpful criticism. This work was supported by the Sofia-Cologne university partnership.

[1] G.W. Kim and H.M. Markowitz, J. Portfolio Management 16, 45 (fall 1989).

[2] D. Sornette and K. Ide, cond-mat/0106054; K. Ide and D. Sornette, cond-mat/0106047

[3] R.B. Pandey and D. Stauffer, Int. J. Pure Appl. Finance 3, 279 (2000)

[4] D. Sornette and A. Johansen, Quant. Finance 1, 457 (2001).

[5] I. Chang, D. Stauffer and R. B. Pandey, cond-mat/0108345 (2001).