KUCP0189

Small-World Effects in Wealth Distribution

Wataru Souma 111e-mail: souma@isd.atr.co.jp

Information Sciences Division, ATR International, Kyoto 619-0288, Japan

Yoshi Fujiwara 222e-mail: yfujiwar@crl.go.jp

Keihanna Research Center, Communications Research Laboratory, Kyoto 619-0289, Japan

Hideaki Aoyama 333e-mail: aoyama@phys.h.kyoto-u.ac.jp

Faculty of Integrated Human Studies, Kyoto University, Kyoto 606-8501, Japan

Abstract

We construct a model of wealth distribution, based on an interactive multiplicative stochastic process on static complex networks. Through numerical simulations we show that a decrease in the number of links discourages equality in wealth distribution, while the rewiring of links in small-world networks encourages it. Inequal distributions obey log-normal distributions, which are produced by wealth clustering. The rewiring of links breaks the wealth clustering and makes wealth obey the mean field type (power law) distributions. A mechanism that explains the appearance of log-normal distributions with a power law tail is proposed.

With the advance of the theory of complex networks [1], it has become clear that many social networks can be understood as small-world networks [2]. On the other hand, recent high-precision studies of economic phenomena, helped by the availability of high-quality data in digital format [3], is starting to reveal the basic characterics of wealth distribution, which form a basis and at the same time a final product of economic activities. In view of these developments, we propose a stochastic model of wealth distribution built on a complex network and present the results of our numerical simulation in this paper.

Several models for wealth distribution have been proposed with some reality and success [4, 5, 6, 7]. They, however, lack one feature we consider important: In some models, each agent (economic body) goes through a stochastic process of increasing and decreasing wealth, quite independently from other agents. In some others, each agent interacts with either randomly-selected agents or neighboring agents on a fixed lattice. Apparently, such a selection of economic partnership/competition is far from reality, as is evident from complex network studies. This is one reason we propose our model, which features both the stochastic nature of economic activities and underlying network structures that are expected to be close to those of the relevant social activities. We also note that studies of economic phenomena that build upon the underlying complex networks are novel.

In considering the mechanisms behind wealth distribution, it is important to include at least two basic natures of the wealth. One is a random change of the value of wealth and the other is the liquidity of it. As a minimal model that contains these features we chose an interactive multiplicative stochastic process [6], which is defined by the following evolution equation:

| (1) |

where is the wealth of the -th agent at the time , is a Gaussian random variable with mean and variance , which describes the spontaneous increase or decrease of the wealth. The rest of the terms in the r.h.s. of Eq. (1) describe transactions on business networks. We note that in Ref. [6] the process corresponding to Eq. (1) is described by a stochastic differential equation in the Stratonovich sense, which generates the second term proportional to when discretized. In addition, although naive discretization brings in a time interval in Eq.(1), it has been absorbed by the rescaling of the parameters.

The transaction matrix is chosen based on the underlying network structure: If the -th agent is directly connected to the -th agent by a link, we take , where is the number of agents connected to the -th agent (“neighbors”). Otherwise, . The parameter is a positive number, which represents the ratio of transactions and the wealth. Thus, the third term in the r.h.s. of Eq. (1) describes the incoming wealth, and the fourth term describes the outgoing wealth. Under this selection of transaction matrix, Eq. (1) can be written as follows:

| (2) |

where is the mean wealth of the neighbors of the -th agent.

We consider one-dimensional and static network of -agents with periodic boundary conditions [1, 2], which are determined by two parameters, i.e., a rewiring probability and a mean number of links per agent . (We will also use a notation .) The rewiring probability is defined by . At we have a regular network with , in which the -th agent is connected only with -th agents. For , links are rewired to conserve the total number of links. At we obtain completely random networks.

In the mean field (MF) case, i.e., , the stationary probability density function is known to be the following in the large limit [6],

| (3) |

where is the wealth normalized by the mean wealth ; . (We will simply call the normalized wealth hereafter.) The exponent is given by . In the large range Eq. (3) becomes a power law distribution, , and therefore the exponent is the Pareto index in economics.

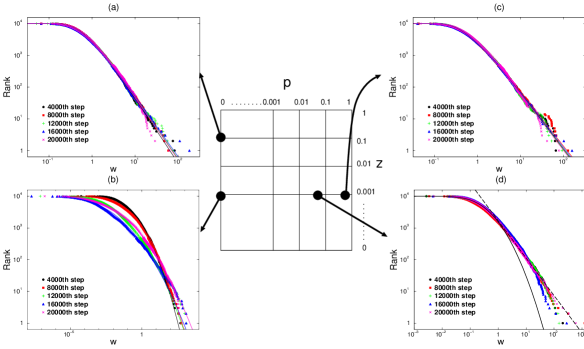

We have carried out numerical simulations for , , and . Under this parameter set, the Pareto index in the MF case is . Some of the distributions we obtained are shown in Figs. 1 (a)-(d). In these figures the horizontal axis is the logarithm of and the vertical axis is that of the rank. We have numerically calculated up to time steps, and drawn distributions at each step. The rank distributions in the case of regular networks with correspond to Fig. 1 (a). The solid lines show the best fits with the MF result Eq. (3). We see that all of the resulting distributions fit well with the MF result with . Figure 1 (b) is a case of regular networks with . We find that the results do not agree with the MF result, but instead fit well with log-normal distributions, which are shown by the solid lines. Note that the best fit log-normal distributions have time-dependent mean value and time-dependent variance . On the other hand, if we rewire links with high probability the MF type distributions reappear. Figure 1 (c) is a case of regular networks with and . The solid lines are the fitting by MF type solutions with , which is slightly smaller than . Hence we observe that the change in wealth distribution occurs at the intermediate value of . Figure 1 (d) is a case of small-world networks with and . We have found that the distributions can not be fitted well by either the log-normal functions or the MF type functions. Interestingly, however, we find that a combination of log-normal and power-law distributions fits well with the results. One such example at the -th time step is shown with a log-normal function for middle and low wealth ranges (solid line) and a power-law function for the high wealth range (dashed line). Log-normal distributions with a power law tail like this are frequently observed in real world economic phenomena [3].

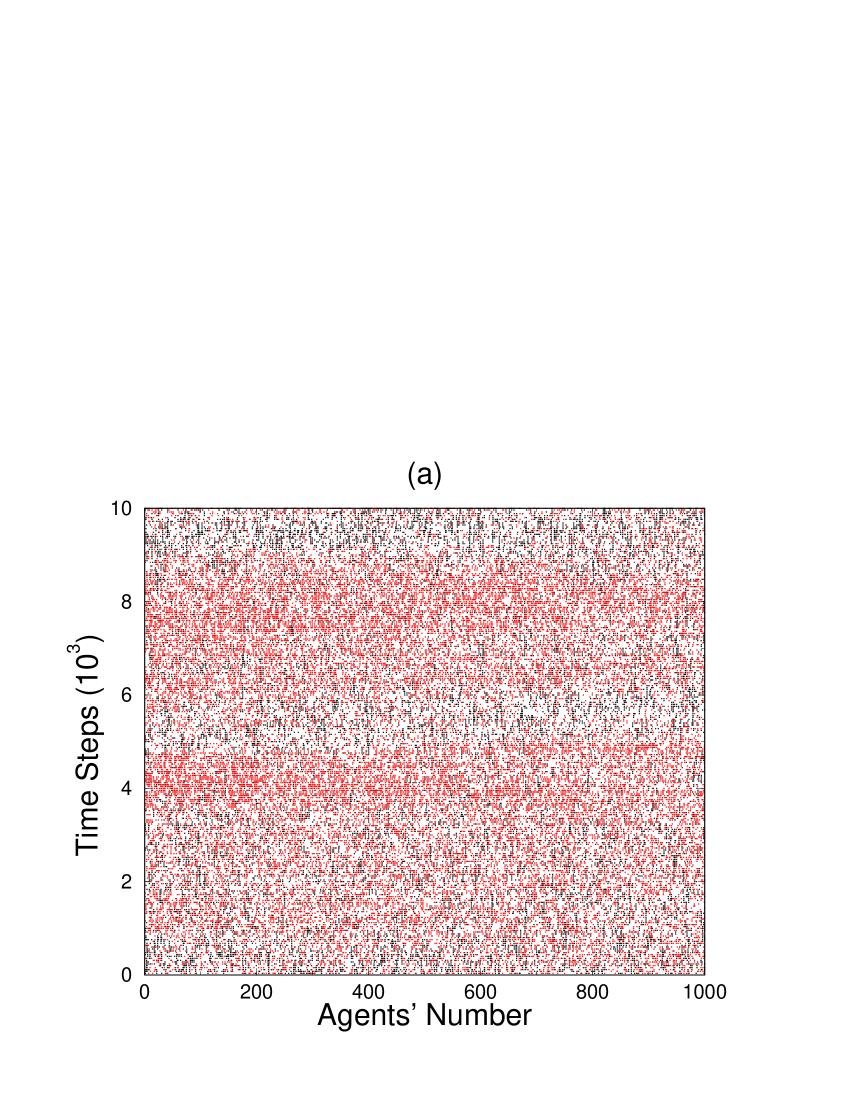

It is natural to question why distribution patterns change. To answer this question, we directly consider the development of the wealth. Examples of numerical simulations are shown in Figs. 2 (a)-(d). In these figures the horizontal axis shows the agents’ number and the vertical axis shows time steps. Though we have simulated for agents, wealth developments for agents are shown. We have calculated up to time steps. If any agent ranks in the top , we mark it with a black dot, and if any agent ranks in the bottom we mark it with a red dot.

Figure 2 (a) is a case of regular networks with . We can see that the black and red dots are uniformly distributed without notable clustering. Since each agent has neighbors, each agent transacts with agents from various ranks, covering a wide range. Figure 2 (b) is a case of regular networks with . Contrary to the case of , the black and red dots cluster heavily. This “wealth clustering” phenomenon is supported by the fact that each agent has only neighbors and rich agents transact mainly with rich agents and poor agents transact mainly with poor agents. Hence and have strong correlations. Actually, for the case of regular networks with , we can obtain . Here . On the other hand we can obtain for the case of regular networks with . Figure 2 (c) is a case of small-world networks with and . This case is almost similar to Fig. 2 (a). Figure 2 (d) is a case of small-world networks with and . Although wealth clustering is observed, the size of each cluster is smaller than the case of regular networks with . From these results we find that a decrease in the number of links causes wealth clustering and the rewiring of links disperses it.

If and have strong correlations, Eq. (2) becomes a pure multiplicative stochastic process, and the wealth obeys log-normal distributions with mean and variance , where and . On the other hand if and have no correlations, Eq. (2) is regarded as a multiplicative stochastic process with additive noise [8]. It is known that this process induces power law distributions in large ranges, if two conditions are satisfied: One condition is that the stochastic variable and the additive noise must behave independently. The other condition is . Although the first condition does not matter in our model, the parameter ranges of and are restricted by the second condition. If and have no correlations in the high wealth ranges and have strong correlations in the middle and low wealth ranges, the wealth will obey log-normal distributions with a power law tail such as those observed in many real world economic phenomena [3].

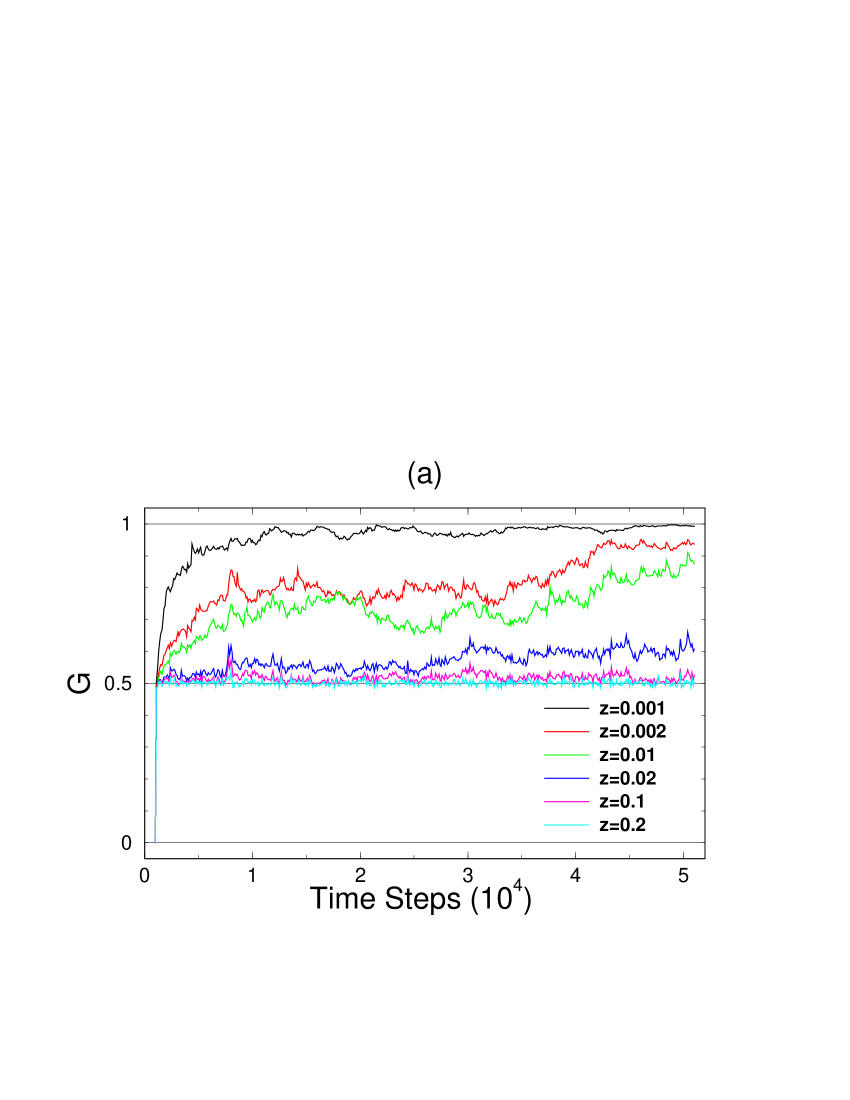

We will now study the inequality of wealth distribution by using the Gini coefficient to quantify it. Take every possible pair of income recipients (wealth possessors) and calculate the average of the absolute differences of the two incomes (wealth) for each pair. is then half the ratio of the average to the mean value of all the incomes (wealth). Obviously when everyone has the same, and when the entire amount is concentrated in a single person. With our parameter set, the Gini coefficient of the MF case is .

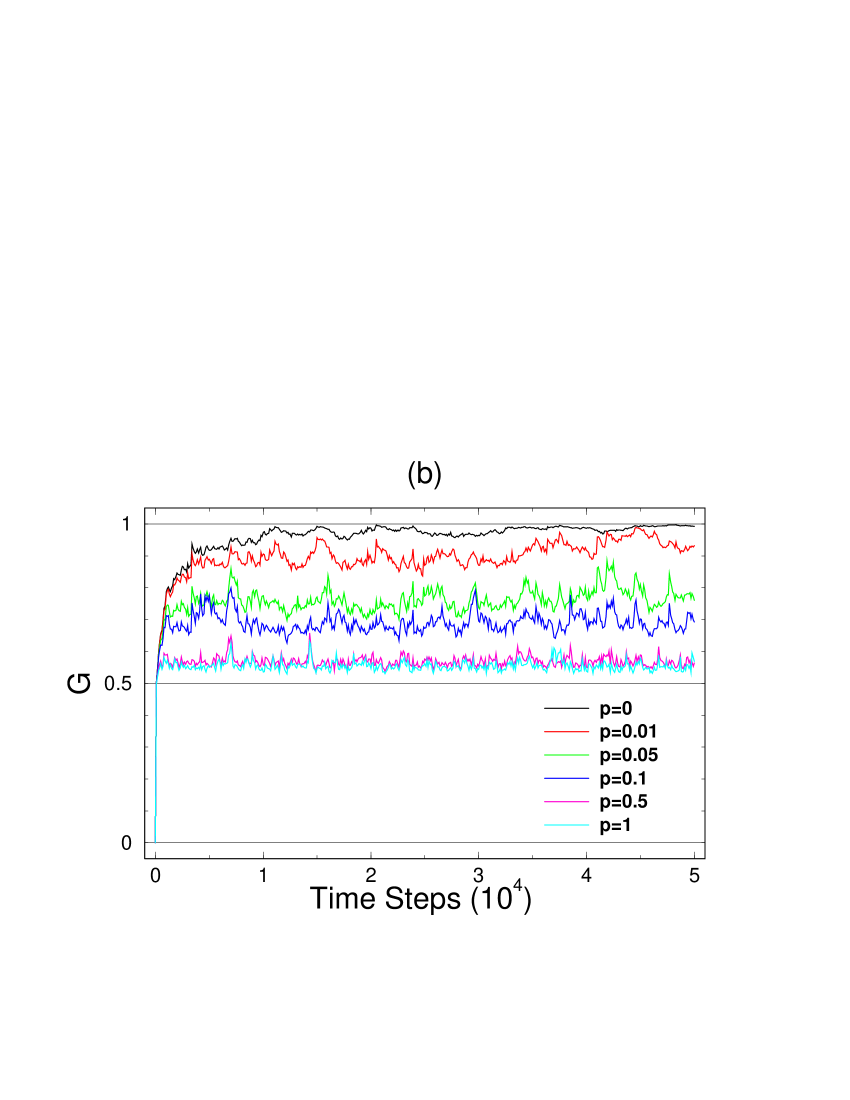

The temporal changes of are shown in Figs. 3 (a) and (b). In these figures, the horizontal axis shows time steps and the vertical axis shows the value of . We have numerically simulated up to time steps. The temporal changes of in the case of regular networks are shown in Fig. 3 (a). In this figure we observe that gradually increases with time steps in the case of and , which is in accordance with the log-normal distributions with and . We also observe that almost completely inequal distributions appear in the case of . We find that the decrease of makes distributions inequal. The temporal changes of in the case of small-world networks with are shown in Fig. 3 (b). From this figure we find that the rewiring of links in small-world networks makes distributions equal.

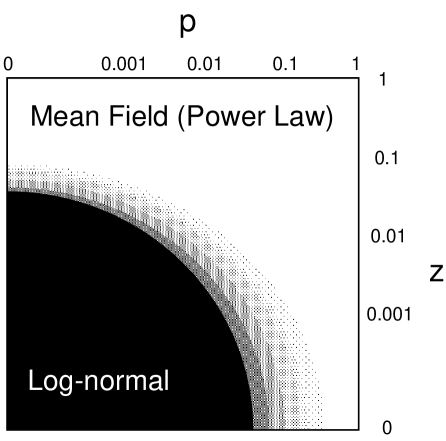

The results of this study are summarized in two parts. First, we have carried out a simulation for a wide range of values of and , which is summarized by the phase diagram shown in Fig. 4. This diagram has two extreme distributions, the log-normal distributions with and and the MF type distributions represented by Eq. (3). These two ranges are interpolated by a decrease in the number of links or the rewiring of the links. In the intermediate region, the wealth distribution may be fitted well with log-normal distributions with a power law tail, which are observed in real world economic phenomena [3]. Lastly, from the study of the Gini coefficient we have found that a decrease in the number of links makes wealth distribution inequal and the rewiring of links in small-world networks makes it equal. Hence society will be protected against exceeding inequalities in wealth by small-world effects in economic networks.

We note that it would be very interesting to carry out an analysis of models similar to the ones studied here, but built on other kinds of networks. For example, the network can be dynamic, allowing rewiring to be either independent from or dependent on wealth. Other novel networks, like scale-independent networks, would also be worth studying. We believe that the work presented here forms a basis for the study of general stochastic processes on complex networks.

The authors would like to thank Dr. K. Shimohara (ATR-ISD) for his continuous encouragement and warm support.

References

- [1] D. J. Watts and S. H. Strogatz, Nature 393, 440 (1998); D. J. Watts, Small Worlds: The Dynamics of Networks between Order and Randomness. (Princeton University Press, Princeton, New Jersey 1999)

- [2] M. E. Newman, cond-mat/0001118; S. H. Strogatz, Nature 410, 268 (2001); R. Albert and A.-L. Barabási, cond-mat/0106096; S. N. Dorogovtsev and J. F. F. Mendes, cond-mat/0106144.

- [3] H. Aoyama, W. Souma, Y. Nagahara, H. P. Okazaki, H. Takayasu and M. Takayasu, Fractals 8, 293 (2000); W. Souma, to appear in Fractals 9, (2001), cond-mat/0011373.

- [4] S. Ispolatov, P. L. Krapivsky and S. Redner, Eur. Phys. Jour. B 2, 267 (1998).

- [5] S. Solomon, Computational Finance 97, ed. A-P. N. Refenes, A. N. Burgess, J. E. Moody, (Kluwer Academic Publications, Dordecht 1998), cond-mat/9803367.

- [6] J. P. Bouchaud and M. Mézard, Physica A 282, 536 (2000).

- [7] Z. Burda, D. Johnston, J. Jurkiewicz, M. Kamiński, M. A. Nowak, G. Papp and I. Zahed, cond-mat/0101068.

- [8] H. Kesten, Acta Math. 131, 207 (1973); D. Sornette and R. Cont, J. Phys. I 7, 431 (1997); H. Takayasu, A.-H. Sato and M. Takayasu, Phys. Rev. Lett. 79, 966 (1997); D. Sornette, Phys. Rev. E 57, 4811 (1998).