Corporate Default Behavior: A Simple Stochastic Model

Abstract

We compare observed corporate cumulative default probabilities to those calculated using a stochastic model based on an extension of the work of Black and Cox [1] and find that corporations default as if via diffusive dynamics. The model, based on a contingent-claims analysis of corporate capital structure, is easily calibrated with readily available historical default probabilities and fits observed default data published by Standard and Poor’s. Applying this model to the Standard and Poor’s default data we find that the difference in default behavior between credit ratings can be explained largely by a single variable: the “distance to default” at the time the rating is given. The ability to represent observed default behavior by a single analytic expression and to differentiate credit-rating-dependent default behavior with a single variable recommends this model for a variety of risk management applications including the mapping of bank default experience to public credit ratings.

pacs:

PACS number(s): 89.90.+n, 05.40+jI Introduction

Estimation of corporate default probability is of central importance in credit risk management and pricing. While bankruptcy forecasting has been the subject of active research for decades [2, 3], the relationship between observed corporate default data and the stochastic dynamics of firm value remains indirectly explored. This is due, in part, to the historical development of the two major research programs in this area. One program can be characterized as originating with the Z-score of Altman [4] and zeta model of Altman and colleages [5] where a credit score is developed as a linear function of explanatory accounting variables. While this approach has been successful in predicting bankruptcy and is not inconsistent with what one might expect given the focus of rating agencies on such financial ratios [6, 7], its linear deterministic structure provides limited insight into the stochastic dynamics of the corporate default behavior. The other major research program began with the work of Merton [8] who applied a contingent-claims approach [9, 10] to the calculation of corporate bond spreads. Although this approach is explicitly stochastic, it fails to predict some key features of corporate bond spreads - the magnitude of the observed spread in general and the finite value of the observed spread in the zero-tenor limit of the yield curve in particular - indicating that corporate bond spread dynamics are driven only partially by corporate default dynamics [11]. Thus, while extensions of Merton’s model (e.g. [12, 13, 14]) that typically involve multiple stochastic processes can reproduce bond spreads, they provide limited direct information regarding the stochastic dynamics of firm value. Nevertheless, the success these models and of commercial products based on proprietary stochastic models of default such as KMV’s CreditMonitorTM [15] , J.P. Morgan’s CreditMetricsTM [16], and Moody’s Public Firm Risk Model [17] provide compelling evidence in support of the usefulness of a stochastic approach to explaining default dynamics. The purpose of our paper is to show that a simple stochastic model of corporate default dynamics implicit in the bond indenture work of Black and Cox [1] yields a straightforward analytic expression for the cumulative default probability that provides a remarkably good description of the cumulative default rates published by Standard and Poor’s.

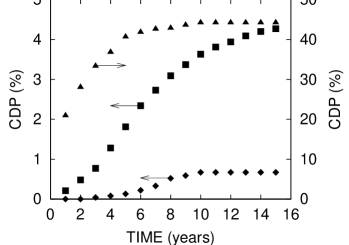

The empirical analysis of corporate default dynamics is complicated by the comparatively rare nature of the corporate default event. Fortunately, a variety of financial institutions including rating agencies monitor and collect default data and have compiled cumulative default probabilities. The challenge posed to an analytic description of corporate default is illustrated in Figure 1 where we present the cumulative default probability as a function of time for AAA, BBB, and CCC rated companies published by Standard and Poor’s [18]. The AAA data denoted by the diamonds is roughly convex for all time less than 10 years. Beyond 10 years there are no observed defaults and the cumulative default probability is constant. The CCC data denoted by the triangles are quite different with a concave function for all time. The BBB data show characteristics of both AAA and CCC: convex for short times and concave for long times. Furthermore we see that in passing from AAA to CCC the cumulative default probabilities change by an order of magnitude. To describe this default behavior we develop an analytic expression based on the structural model of Black and Cox [1] in Sec. II and apply it to the observed default data published by Standard and Poor’s [18] in Sec. III. Our analysis will demonstrate that a single variable in the analytic formula provides effective discrimination between various credit ratings and that this variable is similar to the initial “distance to default” discussed by Crosbie [19, 20]. We conclude this paper in Sec. IV.

II The Default Model

The basis of a simple stochastic model of time-dependent and credit-rating-dependent default probability appeared years ago in the work of Black and Cox [1] where they presented a theoretical analysis of bond indenture provisions that, among other things, examined the effect of safety covenants on the value and behavior of corporate securities. They proposed a simple model of corporate capital structure where the value of the firm would vary through time until it hit a prescribed level. Once reached the prescribed level indenture agreements would specify that the firm be reorganized. Such indenture agreements clearly impact the value of bonds and other corporate securities as demonstrated by Black and Cox. Their work also, however, contains the basis for a stochastic model of bankruptcy.

The model begins with the now common assumption that a corporation is represented as an asset with a market value, , and that, while the return of the asset is uncertain because of various risks associated with the business, it is lognormally distributed, namely,

| (1) |

where and are the constant drift and volatility of the asset value, denotes time, and is a standard Brownian motion.***The notion of the value of the firm as a time-dependent stochastic variable can be traced at least as far back as the pioneering options work of Black and Scholes [9] and Merton [10], and is a basic tenant of essentially all contingent-claims security analysis. Following Black and Cox [1] we also assume that when the asset value falls to a prescribed level denoted by the company defaults. Transforming to the normalized variable , defined by

| (2) |

and, using Ito’s Lemma, we have that

| (3) |

where . The default level now becomes . Since is a measure of how far the firm is from the default level, it has a natural interpretation as the distance to default discussed by Crosbie [19, 20]. Given the initial value , we can calculate the expected cumulative default probability from the first-passage time probability [21, 22]

| (4) |

where is the cumulative normal distribution function.†††Those familiar with the work of Black and Cox [1] will see a strong similarity between our Eq. 4 and their Eq. 7. There is, indeed a direct correspondence that can be derived by taking their reorganization boundary to be independent of time and noting that their Eq. 7 is for the probability that the firm has not defaulted while our Eq. 4 is for the probability that the firm has defaulted. The model for ratings-based default embodied by this expression can be interpreted as follows. When a firm is initially rated () it will be standard deviations away from default. As time passes () the company’s credit state, buffeted by the vaguaries of the economic environment, diffuses with drift and unit volatility. Should the firm’s fortunes evolve such that becomes zero, it encounters the absorbing boundary of default. We now consider whether this model can describe observed default behavior.

III The Default Model and Observed Default Behavior

There are two parameters in Eq. 4, and , that can be varied to fit the observed default probabilities for each rating. As an example of how this expression can be used to represent observed default behavior we consider the published static pool average cumulative default probabilities for each credit rating given by Standard & Poor’s [18] shown in Table I. These values represent the probability of default as a function of time following the initial rating of the company. For example, while a company that was initially rated BBB may undergo any number of rating changes over time, once it defaults it is treated in this analysis as being a BBB default. It can be seen that for each rating the change in the cumulative default probability slows (and in some cases ceases) around 10 years, reflecting the fact that few defaults (and in some cases no defaults) have been observed beyond 10 years. This, as discussed below, is most likely due to the limitation of the sample sizes available. Consequently, we used data from the first 8 years for each rating to fit Eq. 4. The parameters and were obtained by minimizing the sum of the squared difference between the observed default behavior shown in Table I and the calculated values obtained from Eq. 4 subject to the constraint that the long-time cumulative default probability, , be ordered as expected (i.e. ). This multidimensional minimization was effected using the generalized reduced gradient (GRG2) nonlinear optimization solver in Microsoft ExcelTM. The fitted default probabilities using Eq. 4 and the parameters and resulting from the fitting procedure just described are shown in Table 2.

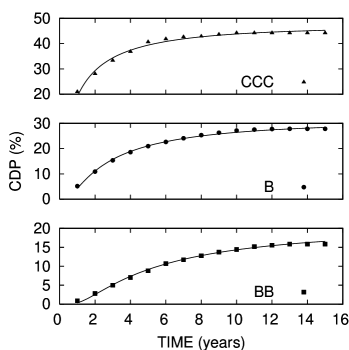

The result of this fit for non-investment grade credits is shown in Table II and Figure 2. The fit to the CCC credit data illustrates the rather good ability of this 2-parameter model to describe the default behavior over the entire 15 year horizon based on a fit to only the first 8 years of data. The concave nature of the data is well reproduced by Eq. 4 as is the substantial slowing of default probability accumulation beyond 10 years. A similarly good description of B credits is seen in this Figure. We see also that BB behavior is more linear with respect to time than that of B or CCC for horizons less than 5 years and that the model is able to follow this as well as the more concave behavior between 5 and 13 years. Beyond 13 years there are no observed defaults and the cumulative default probability is that same from year 13 to year 15 because of this. The model, however, continues to rise gradually indicating that the lack of observed defaults is, likely, due to a limited sample size and that, in time, we can expect to see more defaults in this area. Financially, there is nothing special about the 13th year after a BB rating that would account for the observed sudden lack of defaults.

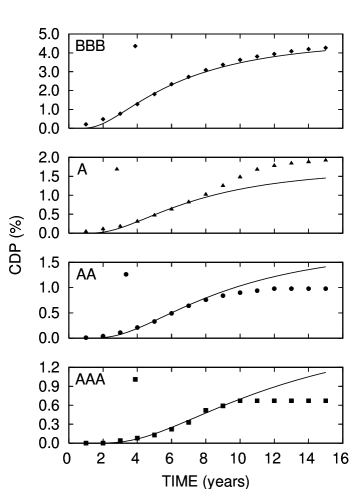

The result of our fit for investment grade credits is shown in Table II and Figure 3. The BBB credits shown in this Figure illustrate an interesting qualitative change in default behavior: the short horizon data are convex in time. The intermediate horizon data are linear in time and the longer horizon data are concave. We see that our simple 2-parameter model provides a very reasonable description of the data. The cumulative default behavior A credits is a challenge to the model. The model clearly tracks the observed data well between 1 and 8 from years and 11 to 15 years, but an accumulation of defaults in the 8 to 11 year time frame results in a substantial offset between the observed and the calculated data in the 11 to 15 year region. One solution is to fit over the 1st 10 years. While this is perfectly reasonable and most people using such a model to fit their data would likely do so, we felt it useful to see how far we could get using a uniform time range for fitting purposes. For AA and AAA credit default behavior we see good fits to observations over the 1st 8 years and reasonable extrapolations with significant deviations coinciding with the point at which the cumulative default data stop changing due to lack of observed defaults.

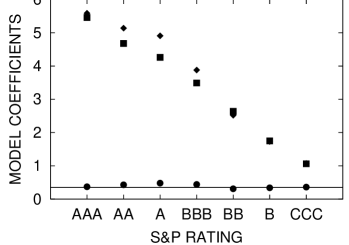

The coefficients of Eq 4, and , that resulted from the fitting procedure that generated Figures 2 and 3 are shown as a function of credit rating in Figure 4. The squares correspond to the fitted values of and the circles correspond to the fitted values of . This graph demonstrates the intuitively expected result that the better the credit rating the larger the initial distance to default. Recalling from our earlier discussion that the distance to default is measured in standard deviations, we see that the average AAA company is initially about 5.5 standard deviations from default, the average BBB company is initially about 4 standard deviations from default, and the average CCC company is initially about 1 standard deviation from default.

The normalized drift, , resulting from the fitting procedure that generated Figures 2 and 3 is remarkable in that, while each credit was fit individually, the normalized drifts are quite similar. This similarity prompted us to explore the results that would follow if was assumed a priori to be the same for all credits. The results of a global fit with this restriction are shown as diamonds in Figure 4 where we see the initial distance-to-default as a function of credit. This analysis also found that : shown as a horizontal line in Figure 4. Comparing the for constant and variable drift we see that setting constant across credits has essentially no impact on for the lower credits and has a minor impact on the higher credits. That the default dynamics of all credits can be represented by a single value of implies that differences in cumulative default behavior among various ratings are driven almost exclusively by the initial distance to default .

Modeling the default process as a first-passage time yields a simple expression for the mean time to default: . Comparing the results of this expression with those reported by Standard and Poor’s in Table III. The deviation between the calculated and observed results reflects the lack of observed default at longer tenors. However, for the same reason that we would expect the longer-tenor cumulative default probability for the AA and AAA credits to increase over time, so too do we expect the mean time to default to increase over time for investment-grade credits.

IV Summary

Comparing observed corporate cumulative default probabilities to those calculated using a stochastic model based on an extension of the work of Black and Cox [1], we find that corporations default as if via diffusive dynamics. The model, based on a contingent-claims analysis of corporate capital structure, yields a single analytic expression for corporate default behavior that is calibrated easily with historical default probabilities. We used this model to analyze the observed default data published by Standard and Poor’s [18] and found that a single variable in the analytic formula provides effective discrimination between various credit ratings. This variable is quite similar to the “distance to default” described by Crosbie [19, 20] and provides an attractive interpretation of the default process in terms of the bond indenture provision analysis of Black and Cox [1]. Despite its simple underpinnings, the model is remarkably successful in describing the cumulative default rates published by Standard and Poor’s [18]. This implies that the capital structure of corporations, despite their differences, map onto the simple “effective” capital structure given in the Merton model. The ability to represent observed default behavior by a single analytic expression and to differentiate credit-rating-dependent default behavior with a single variable recommends this model for a variety of risk management applications including the mapping of bank default experience to public credit ratings.

Acknowledgements.

We thank Arden Hall and Jim Westfall for enlightening discussions and Vincent Chu and Terry Benzschawel for their helpful comments. This article was written before Ting Lei joined Wells Fargo and Raymond J. Hawkins joined Bear, Stearns Securities Corporation. Neither Wells Fargo or Bear, Stearns Securities Corporation are responsible for any statements or conclusions herein; and no opinions, represented herein in any way represent the position of Wells Fargo or of Bear, Stearns Securities Corporation.REFERENCES

- [1] F. Black and J. C. Cox, Journal of Finance 31, 351 (1976).

- [2] Managing Credit Risk: The Next Great Financial Challenge, edited by J. B. Caouette, E. I. Altman, and P. Narayanan (John Wiley & Sons, Inc., New York, 1999).

- [3] A. Saunders, Credit Risk Measurement: New Approaches to Value at Risk and Other Paradigms (John Wiley & Sons, New York, NY, 1999).

- [4] E. I. Altman, Journal of Finance September, 589 (1968).

- [5] E. I. Altman, R. Haldeman, and P. Narayanan, Journal of Banking & Finance 1, 29 (1977).

- [6] H. C. Sherwood, How Corporate and Municipal Debt is Rated: An Inside Look at Standard & Poor’s Rating System (John Wiley & Sons Inc., New York, NY, 1976).

- [7] Standard & Poor’s 2000 Corporate Ratings Criteria, downloaded from www.standardandpoors.com (unpublished).

- [8] R. C. Merton, Journal of Finance 29, 449 (1974).

- [9] F. Black and M. Scholes, Journal of Political Economy 81, 637 (1972).

- [10] R. Merton, Bell Journal of Economics and Management Science 4, 141 (1973).

- [11] J. Bohn, ‘A Survey of Contingent-Claims Approaches to Risky Debt Valuation’, Available at www.kmv.com (unpublished).

- [12] I. Kim, K. Ramaswamy, and S. Sundaresan, Financial Managment 117 (1993).

- [13] D. Shimko, N. Tejima, and D. van Deventer, Journal of Fixed Income September, 58 (1993).

- [14] F. A. Longstaff and E. S. Schwartz, Journal of Finance 50, 789 (1995).

- [15] KMV Corporation. CreditMonitorTM, www.kmv.com.

- [16] G. M. Gupton, C. G. Finger, and M. Bhatia, CreditMetricsTM - Technical Document, J. P. Morgan & Co., Inc., New York, New York (1997).

- [17] J. R. Sobehart and R. M. Stein, Moody’s Public Firm Risk Model: A Hybrid Approach to Modeling Short Term Default Risk, Moody’s Investors Service, Global Gredit Research, New York, New York (2000).

- [18] L. Brand and R. Bahar, Special Report: Ratings Performance 1999 (Standard & Poors, New York, 2000), p. 10.

- [19] P. J. Crosbie, Modeling Default Risk, www.kmv.com 999-0000-031, San Francisco, CA (1997).

- [20] P. Crosbie, Credit Derivatives: Trading & Management of Credit & Default Risk (John Wiley & Sons (Asia) Pte Ltd., Singapore, 1998), pp. 299–315.

- [21] C. W. Gardiner, Handbook of Stochastic Methods for Physics, Chemistry and the Natural Sciences, Vol. 13 of Springer Series in Synergetics, 2nd ed. (Springer-Verlag, New York, NY, 1985).

- [22] J. E. Ingersoll, Theory of Financial Decision Making, Rowman & Littlefield Srudies in Financial Economics (Rowman & Littlefield, Savage, MD, 1987).

| Time (years) | AAA | AA | A | BBB | BB | B | CCC |

|---|---|---|---|---|---|---|---|

| 1 | 0.00 | 0.01 | 0.04 | 0.21 | 0.91 | 5.16 | 20.93 |

| 2 | 0.00 | 0.04 | 0.11 | 0.48 | 2.82 | 10.90 | 28.04 |

| 3 | 0.04 | 0.11 | 0.18 | 0.77 | 5.00 | 15.36 | 33.35 |

| 4 | 0.08 | 0.21 | 0.31 | 1.28 | 7.04 | 18.60 | 36.83 |

| 5 | 0.13 | 0.33 | 0.47 | 1.81 | 8.82 | 20.95 | 40.67 |

| 6 | 0.22 | 0.49 | 0.63 | 2.34 | 10.68 | 22.65 | 41.83 |

| 7 | 0.33 | 0.64 | 0.82 | 2.73 | 11.71 | 24.08 | 42.64 |

| 8 | 0.52 | 0.76 | 1.02 | 3.09 | 12.78 | 25.32 | 42.86 |

| 9 | 0.59 | 0.84 | 1.25 | 3.37 | 13.71 | 26.29 | 43.63 |

| 10 | 0.67 | 0.90 | 1.48 | 3.63 | 14.42 | 27.13 | 44.23 |

| 11 | 0.67 | 0.94 | 1.68 | 3.81 | 15.19 | 27.54 | 44.23 |

| 12 | 0.67 | 0.98 | 1.78 | 3.94 | 15.55 | 27.76 | 44.23 |

| 13 | 0.67 | 0.98 | 1.84 | 4.09 | 15.84 | 27.83 | 44.23 |

| 14 | 0.67 | 0.98 | 1.88 | 4.20 | 15.84 | 27.83 | 44.23 |

| 15 | 0.67 | 0.98 | 1.92 | 4.27 | 15.84 | 27.83 | 44.23 |

| Time (years) | AAA | AA | A | BBB | BB | B | CCC |

|---|---|---|---|---|---|---|---|

| 1 | 0.00 | 0.00 | 0.00 | 0.01 | 0.35 | 4.24 | 19.19 |

| 2 | 0.00 | 0.01 | 0.03 | 0.25 | 2.54 | 11.11 | 29.49 |

| 3 | 0.02 | 0.07 | 0.14 | 0.77 | 5.08 | 15.72 | 34.60 |

| 4 | 0.07 | 0.19 | 0.31 | 1.35 | 7.27 | 18.84 | 37.66 |

| 5 | 0.15 | 0.34 | 0.50 | 1.88 | 9.06 | 21.06 | 39.69 |

| 6 | 0.25 | 0.49 | 0.67 | 2.34 | 10.51 | 22.71 | 41.13 |

| 7 | 0.36 | 0.64 | 0.83 | 2.73 | 11.70 | 23.97 | 42.20 |

| 8 | 0.47 | 0.78 | 0.97 | 3.05 | 12.68 | 24.97 | 43.02 |

| 9 | 0.58 | 0.90 | 1.09 | 3.31 | 13.49 | 25.76 | 43.66 |

| 10 | 0.69 | 1.01 | 1.19 | 3.53 | 14.17 | 26.41 | 44.17 |

| 11 | 0.79 | 1.10 | 1.27 | 3.72 | 14.76 | 26.94 | 44.59 |

| 12 | 0.88 | 1.19 | 1.35 | 3.87 | 15.25 | 27.38 | 44.93 |

| 13 | 0.96 | 1.26 | 1.41 | 4.00 | 15.68 | 27.76 | 45.22 |

| 14 | 1.04 | 1.32 | 1.46 | 4.11 | 16.05 | 28.07 | 45.46 |

| 15 | 1.11 | 1.37 | 1.50 | 4.20 | 16.37 | 28.35 | 45.66 |

| Rating | Variable | Constant | Observed |

|---|---|---|---|

| AAA | 14.7 | 16.1 | 8.0 |

| AA | 10.8 | 14.8 | 8.3 |

| A | 9.0 | 14.1 | 8.2 |

| BBB | 8.0 | 11.2 | 6.6 |

| BB | 8.4 | 7.2 | 4.7 |

| B | 5.1 | 5.0 | 3.4 |

| CCC | 3.0 | 3.1 | 3.2 |