Wealth condensation in a simple model of economy

Orme des Merisiers, 91191 Gif-sur-Yvette Cedex, France

2 Science & Finance, 109-111 rue Victor Hugo, 92532 Levallois cedex, France;

http://www.science-finance.fr

3 Laboratoire de Physique Théorique de l’Ecole Normale Supérieure 111UMR 8548: Unité Mixte du Centre National de la Recherche Scientifique, et de l’École Normale Supérieure. ,

24 rue Lhomond, 75231 Paris Cedex 05, France )

Abstract

We introduce a simple model of economy, where the time evolution is described by an equation capturing both exchange between individuals and random speculative trading, in such a way that the fundamental symmetry of the economy under an arbitrary change of monetary units is insured. We investigate a mean-field limit of this equation and show that the distribution of wealth is of the Pareto (power-law) type. The Pareto behaviour of the tails of this distribution appears to be robust for finite range models, as shown using both a mapping to the random ‘directed polymer’ problem, as well as numerical simulations. In this context, a transition between an economy dominated by a few individuals from a situation where the wealth is more evenly spread out, is found. An interesting outcome is that the distribution of wealth tends to be very broadly distributed when exchanges are limited, either in amplitude or topologically. Favoring exchanges (and, less surprisingly, increasing taxes) seems to be an efficient way to reduce inequalities.

LPTENS preprint 00/06

Electronic addresses : bouchaud@spec.saclay.cea.fr mezard@physique.ens.fr

It is a well known fact that the individual wealth is a very broadly distributed quantity among the population. Even in developed countries, it is common that of the total wealth is owned by only of the population. The distribution of wealth is often described by ‘Pareto’-tails, which decay as a power-law for large wealths [1, 2, 3]:

| (1) |

where is the probability to find an agent with wealth greater than , and is a certain exponent, of order both for individual wealth or company sizes (see however [4]).

Here, we want to discuss the appearance of such Pareto tails on the basis of a very general model for the growth and redistribution of wealth, that we discuss in some simple limits. We relate this model to the so-called ‘directed polymer’ problem in the physics literature [5], for which a large number of results are known, that we translate into the present economical framework. We discuss the influence of simple parameters, such as the connectivity of the exchange network, the role of income or capital taxes and of state redistribution of wealth, on the value of the exponent . One of the most interesting output of such a model is the generic existence of a phase transition, separating a phase where the total wealth of a very large population is concentrated in the hands of a finite number of individuals (corresponding, as will be discussed below, to the case ), from a phase where it is shared by a finite fraction of the population.

The basic idea of our model is to write a stochastic dynamical equation for the wealth of the agent at time , that takes into account the exchange of wealth between individuals through trading, and is consistent with the basic symmetry of the problem under a change of monetary units. Since the unit of money is arbitrary, one indeed expects that the equation governing the evolution of wealth should be invariant when all ’s are multiplied by a common (arbitrary) factor. The evolution equation that we consider is therefore the following:

| (2) |

where is a gaussian random variable of mean and variance , which describes the spontaneous growth or decrease of wealth due to investment in stock markets, housing, etc., while the terms involving the (assymmetric) matrix describe the amount of wealth that agent spends buying the production of agent (and vice-versa). It is indeed reasonable to think that the amount of money earned or spent by each economical agent is proportional to its wealth. This makes equation (2) invariant under the scale transformation . Technically the above stochastic differential equation is interpreted in the Stratonovich sense [6].

The simplest model one can think of is the case where all agents exchange with all others at the same rate, i.e for all . Here, is the total number of agents, and the scaling is needed to make the limit well defined. In this case, the equation for becomes:

| (3) |

where is the average overall wealth. This is a ‘mean-field’ model since all agents feel the very same influence of their environment. By formally integrating this linear equation and summing over , one finds that the average wealth becomes deterministic in the limit :

| (4) |

It is useful to rewrite eq. (3) in terms of the normalised wealths . This leads to:

| (5) |

to which one can associate the following Fokker-Planck equation for the evolution of the density of wealth :

| (6) |

The equilibrium, long time solution of this equation is easily shown to be:

| (7) |

where is the normalisation factor. One can check that , as it should.

Therefore, one finds in this model that the distribution of wealth exhibits a Pareto power-law tail for large ’s. In agreement with intuition, the exponent grows (corresponding to a narrower distribution), when exchange between agents is more active (i.e. when increases), and also when the success in individual investment strategies is more narrowly distributed (i.e. when decreases).

One can actually also define the above model in discrete time, by writing:

| (8) |

where is an arbitrary random variable of mean and variance , and . In this setting, this amounts to study the so-called Kesten variable [7] for which the asymptotic distribution again has a power-law tail, with an exponent found to be the solution of:

| (9) |

Therefore, this model leads to power-law tails for a very large class of distributions of , such that the solution of the above equation is non trivial (that is if the distribution of decays at least as fast as an exponential). Is is easy to check that is always greater than one and tends to in the limit . Let us notice that a somewhat similar discrete model was studied in [8] in the context of a generalized Lotka-Volterra equation. However that model has an additional term (the origin of which is unclear in an economic context) which breaks the symmetry under wealth rescaling, and as a consequence the Pareto tail is truncated for large wealths.

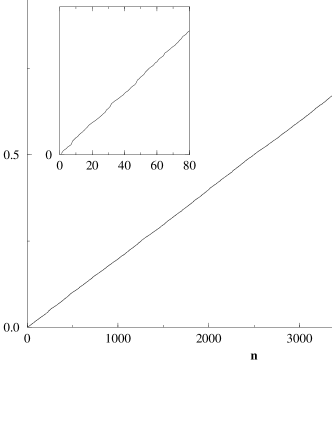

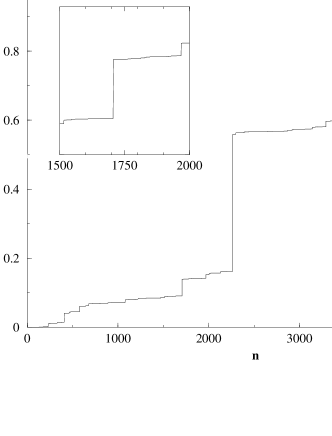

In this model, the exponent is always found to be larger than one. In such a regime, if one plots the partial wealth as a function of , one finds an approximate straight line of slope , with rather small fluctuations (see Fig. 1). This means that the wealth is not too unevenly distributed within the population. On the other hand, the situation when , which we shall encounter below in some more realistic models, corresponds to a radically different situation (see Fig. 2). In this case, the partial wealth has, for large , a devil staircase structure, with a few individuals getting hold of a finite fraction of the total wealth. A quantitative way to measure this ‘wealth condensation’ is to consider the so-called inverse participation ratio defined as:

| (10) |

If all the ’s are of order then and tends to zero for large . On the other hand, if at least one remains finite when , then will also be finite. The average value of can easily be computed and is given by: for and zero for all [9, 10, 11]. is therefore a convenient order parameter which quantifies the degree of wealth condensation.

It is interesting to discuss several extensions of the above model. First, one can easily include, within this framework, the effect of taxes. Income tax means that a certain fraction of the income is taken away from agent . Therefore, there is a term appearing in the right-hand side of Eq. (2). Capital tax means that there is a fraction of the wealth which is substracted per unit time from the wealth balance, Eq. (2). If a fraction of the income tax and of the capital tax are evenly redistributed to all, then this translates into a term in the right-hand side of the wealth balance, which now reads:

| (11) |

All these terms can be treated exactly within the above mean-field model allowing for a detailed discussion of their respective roles. The rate of exponential growth of the average wealth becomes equal to:

| (12) |

The Pareto tail exponent is now given by:

| (13) |

This equation is quite interesting. It shows that income taxes tend to reduce the inequalities of wealth (i.e., lead to an increase of ), even more so if part of this tax is redistributed. On the other hand, quite surprisingly, capital tax, if used simultaneously to income tax and not redistributed, leads to a decrease of , i.e. to a wider distribution of wealth. Only if a fraction is redistributed will the capital tax be a truly social tax. Note that in the above equation, we have implicitly assumed that the growth rate is positive. In this case, one can check that is always greater than , which is larger than one.

Another point worth discussing is the relaxation time associated to the Fokker-Planck equation (6). By changing variables as and , one can map the above Fokker-Plank equation to the one studied in [12], which one can solve exactly. For large time differences , one finds that the correlation function of the ’s behaves as:

| (14) |

and

| (15) |

This shows that the relaxation time is, for , given by . Therefore, rich people become poor (and vice versa) on a finite time scale in this model. A reasonable order of magnitude for is per . In order to get , one therefore has to choose per year, i.e. of the total wealth of an individual is used in exchanges. [This value looks rather small, but in fact we shall see below that a more realistic (non-mean field model) allows to increase while keeeping fixed]. In this case, the relaxation time in this model is of the order of years.

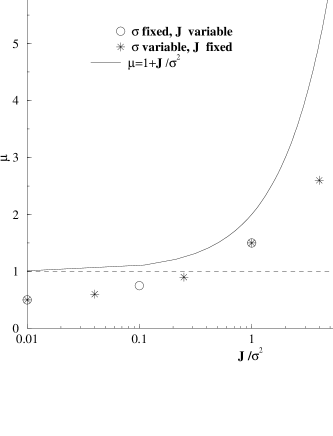

Let us now escape from the mean-field model considered above and describe more realistic situations, where the number of economic neighbours to a given individual is finite. We will first assume that the matrix is still symmetrical, and is either equal to (if and trade), or equal to . A reasonable first assumption is that the graph describing the connectivity of the population is completely random, i.e. that two points are neighbours with probability and disconnected with probability . In such a graph, the average number of neighbours is equal to . We thus scale in order to compare results with various connectivities (and insure a smooth large connectivity limit). We have performed some numerical simulations of Eq. (2) for and have found that the wealth distribution still has a power-law tail, with an exponent which only depends on the ratio . This is expected since a rescaling of time by a factor can be absorbed by changing into and into ; therefore, long time (equilibrium) properties can only depend on the ratio . As shown in Fig. 3, the exponent can now be smaller than one for sufficiently small values of . In this model, one therefore expects wealth condensation when the exchange rate is too small. Note that we have also computed numerically the quantity and found very good agreement with the theoretical value determined from the slope of the histogram of the ’s.

From the physical point of view, the class of models which we consider here belong to the general family of directed polymers in random media. The two cases we have considered so far correspond respectively to a polymer on a fully connected lattice, and a polymer on a random lattice. A variant of this model can be solved exactly using the method of Derrida and Spohn [13] for the so-called directed polymer problem on a tree. In this variant one assumes that at each time step the connectivity matrix is completely changed and chosen anew using the same probabilities as above. Each agent chooses at random exactly new neighbours , the wealth evolution equation becomes

| (16) |

where is a gaussian random variable of mean zero and variance . One can then write a closed equation for the evolution of the wealth distribution [13]. In this case, the wealth condensation phenomenon takes place whenever . For the transition occurs for .

For , one finds that is given by:

| (17) |

and is less than one, signalling the onset of a phase where wealth is condensed on a finite number of individuals. This precisely corresponds to the glassy phase in the directed polymer language. The above formula shows that depends only weakly on or , in qualitative agreement with our numerical result for the continuous time model (see Fig. 3). Note that in the limit , and the glassy phase disappears, in agreement with the results above, obtained directly on the mean-field model. Note also that in the limit , where the reshuffling of the neighbours becomes very fast, wealth diffusion within the population becomes extremely efficient and, as expected, the transition again disappears. Finally, in the simple case where (each agent trading all of his wealth at each time step), the critical value is and the exponent in the condensed phase is simply , and for (see [13]).

Let us note, en passant, that the model considered by Derrida and Spohn has another interesting interpretation if the ’s describe the wealth of companies. The growth of a company takes place either from internal growth (leading to a term much as above), but also from merging with another company. If the merging process between two companies is completely random and takes place at a rate per unit time, then the model is exactly the same as the one considered in Section 3 of [13] (see in particular their Eq. (3.2)).

Although not very realistic, one could also think that the individuals are located on the nodes of a d-dimensional hypercubic lattice, trading with their neighbours up to a finite distance. In this case, one knows that for there exists again a phase transition between a ‘social’ economy where and a rich dominated phase . On the other hand, for , and for large populations, one is always in the extreme case where at large times. In the case , i.e. operators organized along a chain-like structure, one can actually compute exactly the distribution of wealth by transposing the results of [14]. One finds for example that the ratio of the maximum wealth to the typical (e.g. median) wealth behaves as , where is the size of the population, instead of in the case of a Pareto distribution with . The conclusion of the above results is that the distribution of wealth tends to be very broadly distributed when exchanges are limited, either in amplitude (i.e. too small compared to ) or topologically (as in the above chain structure). Favoring exchanges (in particular with distant neighbours) seems to be an efficient way to reduce inequalities.

Let us now discuss in a cursory way the extension of this model to the case where the matrix has a non trivial structure. One can always write:

| (18) |

where is a symmetric matrix describing the frequency of trading between and . is a local bias: it describes by how much the amount of trading from to exceeds that from to . In the absence of the speculative term , Eq. (2) is actually a Master equation describing the random motion of a particle subject to local forces , where is the hopping rate between site and site . This problem has also been much studied [15]. One can in general decompose the force into a potential part and a non potential part. For a purely potential problem, the stationary solution of Eq. (2) with is the well known Bolzmann weight:

| (19) |

The statistics of the therefore reflects that of the potential ; in particular, large wealths correspond to deep potential wells. Pareto tails correspond to the case where the extreme values of the potential obey the Gumbel distribution, which decays exponentially for large (negative) potentials [11].

The general case where is non zero and/or contains a non potential part is largely unknown, and worth investigating. A classification of the cases where the Pareto tails survive the introduction of a non trivial bias field would be very interesting. Partial results in the context of population dynamics have been obtained recently in [16]. The case where the ’s are on the nodes of a dimensional lattice should be amenable to a renormalisation group analysis along the lines of [17, 18], with interesting results for . Work in this direction is underway [19].

In conclusion, we have discussed a very simple model of economy, where the time evolution is described by an equation capturing, at the simplest level, exchange between individuals and random speculative trading in such a way that the fundamental symmetry of the economy under an arbitrary change of monetary units is obeyed. Although our model is not intended to be fully realistic, the family of equations given by Eq. (2) is extremely rich, and leads to interesting generic predictions. We have investigated in details a mean-field limit of this equation and showed that the distribution of wealth is of the Pareto type. The Pareto behaviour of the tails of this distribution appears to be robust for more general connectivity matrices, as a mapping to the directed polymer problem shows. In this context, a transition between an economy governed by a few individuals from a situation where the wealth is more evenly spread out, is found. The important conclusion of the above model is that the distribution of wealth tends to be very broadly distributed when exchanges are limited. Favoring exchanges (and, less surprisingly, increasing taxes) seems to be an efficient way to reduce inequalities.

Acknowledgments: We want to thank D.S. Fisher, I. Giardina and D. Nelson for interesting discussions. MM thanks the SPhT (CEA-Saclay) for its hospitality.

References

- [1] V. Pareto, Cours d’économie politique. Reprinted as a volume of Oeuvres Complètes (Droz, Geneva, 1896-1965).

- [2] B.B. Mandelbrot, Int. Eco. Rev. 1 (1960) 79, B.B. Mandelbrot, ‘The Fractal Geometry of Nature’ (Freeman, San Francisco, 1983).

- [3] A. B. Atkinson, A. J. Harrison, Distribution of total wealth in Britain (Cambridge University Press, 1978), Y. Ijri, H. A. Simon, Skew distribution of sizes of Business Firms (North-Holland, Amsterdam).

- [4] M. H. R. Stanley, S. Buldyrev, S. Havlin, R. Mantegna, M. Salinger, H. E. Stanley, Eco. Lett. 49 (1995) 453.

- [5] for a review, see T. Halpin-Healey and Y.C. Zhang; Phys. Rep. 254 (1995) 217 and refs. therein.

- [6] see e.g. N.G. Van Kampen, J. Stat. Phys. 24 (1981) 175. With the Ito convention, our evolution equation would have an extra factor of on the right hand side.

- [7] H. Kesten, Acta. Math 131 (1973) 208.

- [8] S. Solomon, in Computational Finance 97, eds. A-P. N. Refenes, A.N. Burgess, J.E. Moody (Kluwer Academic Publishers 1998); cond-mat/9803367.

- [9] M. Mezard, G. Parisi, N. Sourlas, G. Toulouse, M. Virasoro, J. Physique 45 (1984) 843.

- [10] B. Derrida, Non-Self averaging effects in sum of random variables, in ‘On Three Levels’, Edited by Fannes et al, page 125 Plenum Press, NY, 1994.

- [11] J.P. Bouchaud, M. Mézard, J. Phys. A. 30 (1997) 7997.

- [12] R. Graham, A. Schenzle, Phys. Rev. A 25 (1982) 1731.

- [13] B. Derrida, H. Spohn, J. Stat. Phys. 51 (1988) 817

- [14] D.S. Fisher, C. Henley, D.A. Huse, Phys. Rev. Lett. 55 (1985) 2924.

- [15] for a review, see e.g.: J.P. Bouchaud, A. Georges, Phys. Rep. 195 (1990) 127.

- [16] K. Dahmen, D.R. Nelson and N. Shnerb, e-print cond-mat/9807394 and refs. therein.

- [17] D. S. Fisher, Phys. Rev. A 30 (1984) 960.

- [18] J. M. Luck, Nucl. Phys B 225 (1983) 169

- [19] I. Giardina, J.P. Bouchaud, M. Mézard, in preparation.