Networked Markets, Fragmented Data: Adaptive Graph Learning for Customer Risk Analytics and Policy Design

Abstract

Financial institutions face escalating challenges in identifying high-risk customer behaviors within massive transaction networks, where fraudulent activities exploit market fragmentation and institutional boundaries. We address three fundamental problems in customer risk analytics: data silos preventing holistic relationship assessment, extreme behavioral class imbalance (<1% suspicious transactions), and suboptimal customer intervention strategies that fail to balance compliance costs with relationship value. We develop an integrated customer intelligence framework combining federated learning, relational network analysis, and adaptive targeting policies. Our federated graph neural network enables collaborative behavior modeling across competing institutions without compromising proprietary customer data, using privacy-preserving embeddings to capture cross-market relational patterns. Focal loss optimization addresses class imbalance by amplifying learning from rare high-risk behavioral segments. We introduce cross-bank Personalized PageRank (PPR) to identify coordinated behavioral clusters—revealing fan-out, loop, and gather-scatter relationship structures—providing interpretable customer network segmentation for risk managers. A hierarchical reinforcement learning mechanism optimizes dynamic intervention targeting, calibrating escalation policies to maximize prevention value while minimizing customer friction and operational costs. Analyzing 1.4 million customer transactions across seven markets, our approach reduces false positive and false negative rates to 6.02% and 5.53%, substantially outperforming single-institution models. The framework prevents 79.25% of potential losses versus 49.41% under fixed-rule policies, with optimal market-specific targeting thresholds (0.316-0.523) reflecting heterogeneous customer base characteristics. Cross-market intelligence sharing increases precision in identifying high-risk customer networks by 60%. These findings demonstrate that federated customer analytics materially improve both risk management effectiveness and customer relationship outcomes in networked competitive markets.

Keywords: Customer Analytics, Federated Learning, Graph Neural Networks, Financial Networks, Dynamic Targeting

1 Introduction

Financial institutions operate in an increasingly complex environment where identifying high-risk customer behaviors has become both a regulatory imperative and a strategic business challenge. As AI technologies reshape financial services and redefine business decision-making processes ([agrawal2019artificial]), financial institutions must balance predictive accuracy with operational constraints, regulatory compliance, and customer relationship value. Between 2020 and 2024, U.S. banks filed more than 137,000 suspicious activity reports linked to illicit networks [website:FinCEN], while recent investigation revealed that criminal organizations moved over $312 billion through legitimate financial channels [website:WSJ]. Globally, the United Nations estimates that 2–5% of world GDP ($800 billion–$2 trillion) is laundered annually, yet less than 1% is ever recovered [website:UN]. Beyond regulatory penalties, ineffective risk management imposes substantial operational costs through false alerts requiring manual investigation, potential reputation damage from compliance failures, and lost legitimate customer relationships due to over-cautious interventions. Understanding how well-intentioned financial regulations can produce unintended consequences is crucial for designing effective AML policies [bao2017ni].

Traditional customer risk management systems rely predominantly on rule-based heuristics that flag transactions exceeding predetermined thresholds or matching known suspicious patterns. While straightforward to implement, these systems generate overwhelming false positive rates—often exceeding 95%—creating a critical resource allocation problem: compliance teams must investigate alerts that consume investigator time without commensurate risk reduction, while legitimate customers experience unnecessary friction that erodes relationship value. More critically, rigid rule-based approaches fail to adapt to evolving customer behavioral patterns and cannot detect sophisticated schemes that deliberately fragment activities across multiple institutions, jurisdictions, and time periods. As financial transactions become increasingly digital, interconnected, and global, the limitations of static rule-based customer monitoring have become economically costly and strategically problematic.

Recent advances in machine learning offer promising alternatives for customer risk assessment. Data-driven approaches can process massive, complex behavioral datasets with efficiency and adaptability that traditional rules cannot match. By automatically identifying latent behavioral patterns and relationship anomalies, these methods can improve both detection accuracy and operational efficiency. However, despite their analytical promise, applying machine learning to customer risk management in financial markets faces four fundamental business and technical challenges that have limited widespread adoption.

The first challenge is the fragmented customer intelligence across competing institutions. Financial institutions operate as competing entities, constrained by privacy regulations, competitive concerns, and customer confidentiality requirements. Customer transaction data are distributed across different entities and platforms, and institutions cannot easily share customer information due to strict regulatory constraints and competitive dynamics [amoako2025exploring]. This fragmented view significantly limits the ability to capture illicit behavioral patterns that span multiple institutions—a deliberate strategy employed by sophisticated actors who exploit the lack of cross-institutional coordination. Models trained on isolated institutional data are prone to high false negatives, where suspicious activities appear benign within a single institution’s customer base but reveal clear patterns when viewed across the broader market ecosystem. For instance, a transaction series may appear routine within one bank’s customer portfolio but reveal layering or structuring patterns only when combined with behavioral data from other institutions. Addressing this challenge requires developing privacy-preserving collaborative frameworks that enable institutions to benefit from shared market intelligence without exposing proprietary customer information or violating competitive boundaries.

The second challenge is lack of interpretability in customer risk models. Most advanced predictive models, particularly deep learning architectures, operate as "black boxes," making it difficult for relationship managers, compliance officers, and regulators to understand why particular customers or transactions are flagged. In high-stakes financial environments, model transparency is not merely desirable but mandatory for ensuring accountability, supporting customer relationship decisions, and satisfying regulatory auditing standards. When a model flags a corporate customer for suspicious wire transfers, investigators must trace the reasoning—such as anomalous transaction frequency, counterpart network characteristics, or deviations from historical behavioral patterns—to justify the alert and determine appropriate relationship management actions. Without interpretability, analysts face opaque predictions they cannot validate or contest, leading to mistrust and resistance toward model adoption. Moreover, regulators require financial institutions to explain the logic behind automated decisions, especially when these affect customer rights, relationship continuity, or trigger legal actions. The lack of interpretability thus impedes both internal investigation workflows and creates significant compliance and governance risks, ultimately limiting the business value of sophisticated analytics investments.

Thirdly, detection is merely the first step in an effective customer risk management pipeline, as institutions must decide whether to monitor, escalate, or intervene in customer relationships under operational constraints and time pressures. Current systems typically employ rigid rule-based escalation procedures that fail to align with the probabilistic outputs of predictive models or optimize across multiple business objectives. A flagged transaction involving cross-border remittances might warrant different interventions depending on the customer’s relationship value, transaction context, historical behavior patterns, and broader network risk exposure. Without adaptive decision-support mechanisms, relationship managers must manually reconcile probabilistic risk signals with static compliance rules, leading to inconsistent interventions, relationship friction, and suboptimal resource allocation. False positives—incorrectly flagging legitimate customers—can lead to unnecessary account restrictions, customer dissatisfaction, and relationship attrition, while false negatives—failing to identify genuine risks—result in financial losses and severe regulatory penalties. These challenges are compounded by institutional fragmentation, where each institution observes only a local subset of the broader customer relationship network. There is an urgent need for adaptive targeting frameworks that coordinate detection with intervention policies across institutional boundaries while optimizing for relationship value, operational costs, compliance requirements, and customer experience.

The fourth challenge is the extreme behavioral class imbalance. In real-world financial systems, illicit transactions constitute a minute fraction of total transaction volume—often less than 1% as documented in Table 1—while the overwhelming majority corresponds to legitimate customer activities. This extreme imbalance fundamentally challenges model development and deployment. Standard machine learning algorithms become biased toward the majority (legitimate) class, achieving deceptively high overall accuracy while exhibiting poor sensitivity to rare but critical suspicious behaviors. Models may fail to detect subtle anomalies hidden within massive streams of normal customer transactions. Moreover, suspicious behaviors are highly heterogeneous and evolve over time, meaning the limited labeled positive cases cannot adequately capture the diversity of real-world schemes such as layering, structuring, or trade-based techniques. The scarcity of verified suspicious cases also reflects the costly and time-intensive nature of financial investigations, where labeling requires expert validation and cross-institutional cooperation. This imbalance complicates not only model training and evaluation but also operational deployment, as systems learn to overlook minority patterns that deviate from dominant behavioral trends.

To address these challenges, this paper proposes a privacy-preserving adaptive framework that connects three critical dimensions of modern financial security: illicit activities detection module, interpretable group identification, and hierarchical decision-making. Collectively, these innovations enable financial institutions to move from reactive detection toward proactive, coordinated, and explainable anti-money-laundering operations. Specifically, we first introduce a graph-based federated learning framework designed to detect money-laundering patterns while preserving data privacy. In this approach, each financial institution analyzes its own transaction network locally but shares abstracted, non-sensitive insights via virtual supernode to corporately learn broader patterns of suspicious laundering behavior. This enables institutions to benefit from shared intelligence without exposing proprietary or customer data. The detection module also integrates multiple analytical objectives, such as identifying hidden transaction clusters and predicting anomalous relationships, to better capture the complexity of real-world laundering schemes. Instead of using the cross-entropy loss, we apply focal loss to mitigate the data imbalanced issue by dynamically adjusting the relative importance of the minority (suspicious) versus majority (normal) classes. The results show that the Cross-Entropy Loss tends to favor the majority class (normal transactions), leading to lower false alarm rates (Type I errors) but a higher tendency to overlook true laundering cases (Type II errors). In contrast, the Focal Loss introduces a more balanced learning process by assigning greater weight to these hard-to-detect, high-risk transactions, thus achieving much lower Type II errors and slightly higher Type I errors. We then evaluate the individual contribution of each component (e.g., virtual super-node, graph cut loss) through an ablation study, where components are systematically removed and replaced. The findings demonstrate that every component contributes meaningfully to the overall detection performance.

This paper reveals one fundamental challenge for cross-border financial crime detection: subpopulation shift induced by data fragmentation resulting in performance degradation. subpopulation shift is a form of distribution shift where the overall population remains fixed, but the characteristics or proportions of underlying subgroups differ [koh2021wilds]. When transaction data are partitioned by country to reflect regulatory and privacy constraints, substantial distributional discrepancies emerge across markets, particularly for critical features such as transaction amount, which spans several orders of magnitude. Our experiments demonstrate that commonly used feature normalization strategies can inadvertently exacerbate this issue. Specifically, normalizing features independently within each country amplifies subpopulation shift, as country-level statistics differ markedly from global ones. Controlled experiments comparing country-level and global-level normalization show that this induced shift significantly degrades the performance of most machine learning models, leading to higher false negatives and lower precision-recall performance. Most approaches benefit from eliminating subpopulation shift via globally consistent normalization. These findings highlight subpopulation shift as a critical and previously underappreciated obstacle in AML modeling and motivate the need for learning framework that are robust to fragmented, privacy-constrained and heterogeneous financial data environments.

This paper also highlight several insights central to the effectiveness of detection module. First, federated learning generates substantial value from coordination without data sharing, a property particularly valuable when regulatory constraints prohibit direct information exchange. By aggregating model parameters rather than raw transactions, institutions achieve detection gains equivalent to pooled training while maintaining competitive independence. This reduces both Type I and Type II errors, demonstrating that shared model parameters (not shared data) deliver meaningful gains in detection performance. Second, models that incorporate structural information in graph data, such as federated graph neural network, consistently outperform feature-only deep learning methods, such as three-layer MLP. By leveraging relational signals that describe how accounts interact, the graph-based model better distinguishes legitimate from suspicious behaviors. Third, collaborative learning efficiency is critical: varying communication frequency in federated training demonstrates a non-monotonic trade-off between detection accuracy and synchronization cost. Moderate communication intervals improve AUPRC and reduce missed detections while lowering coordination overhead, whereas overly frequent or infrequent aggregation can degrade performance. Fourth, data fragmentation and subpopulation shift negatively impact detection quality: normalizing features independently within each country or training models solely on country-level subsets reduces performance compared with using aggregated or globally normalized data. To address this, we design a fixed-value min–max normalization strategy to mitigate subpopulation shift without sharing sensitive raw data across institutions. Overall, these findings underscore the importance of collaborative, privacy-preserving learning frameworks that can reconcile performance, structural modeling, and data heterogeneity in cross-country anti–money laundering detection.

Upon these detection results by the detection module, we further employ a network propagation mechanism via cross-bank Personalized PageRank (PPR) that starts from one suspicious account and expands the identification of suspicious neighbors entities, mimicking the process of money flows. This technique reveals sub-group structures within suspicious transaction networks, essentially identifying clusters of accounts or entities that act in coordination. By uncovering these latent community patterns, the module provides analysts and regulators with clearer explanations of what type of money-laundering behaviors are flagged, helping bridge the gap between algorithmic output and human reasoning. Together, these mechanisms turn abstract detection scores into interpretable group-level evidence, empowering financial analysts to act with greater confidence and precision. By examining the relational connections between accounts, this method uncovers hidden subgroups of potentially collusive actors and strengthens the overall detection accuracy. It ensures that the system not only flags individual transactions but also reveals the structure of laundering networks, which is a key step for investigative and regulatory follow-up.

We further provide the theoretical insights of using PPR for grouping money laundering behaviors. Specifically, in Theorem 4.1, we come up with a detectability condition for identifying a money-laundering group using PPR. Intuitively, PPR captures money-laundering behavior because it propagates the suspiciousness signal from a known malicious seed node through the transaction network. Nodes densely connected to the seed, likely participating in group laundering, accumulate higher PPR scores, while weakly connected nodes receive lower scores. The theorem formalizes this by showing that a well-separated group will stand out in the PPR ranking. Based on this, we modify the transition matrix in PPR by assigning higher weights to edges more likely associated with laundering transactions, which further amplifies scores for nodes strongly connected via suspicious interactions. Specifically, weighted edges increase the transition probability along suspicious links, causing PPR to concentrate more on nodes involved in laundering.

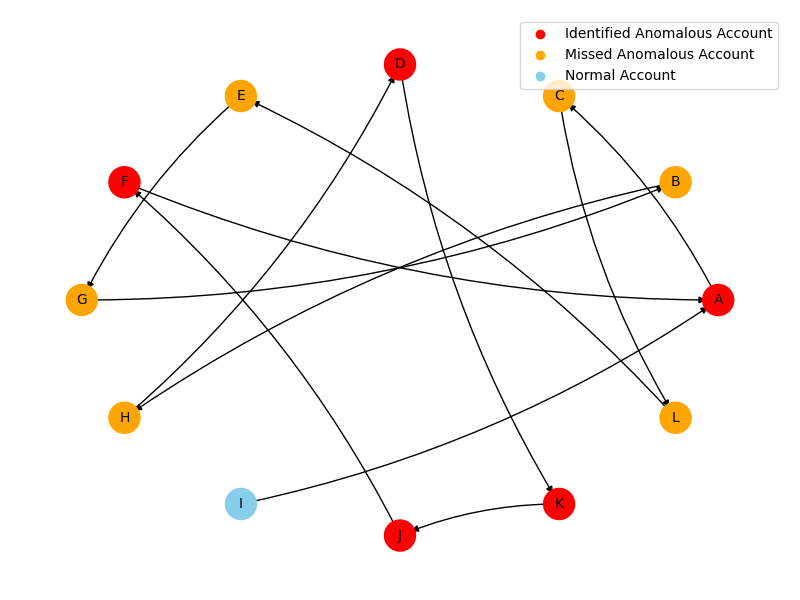

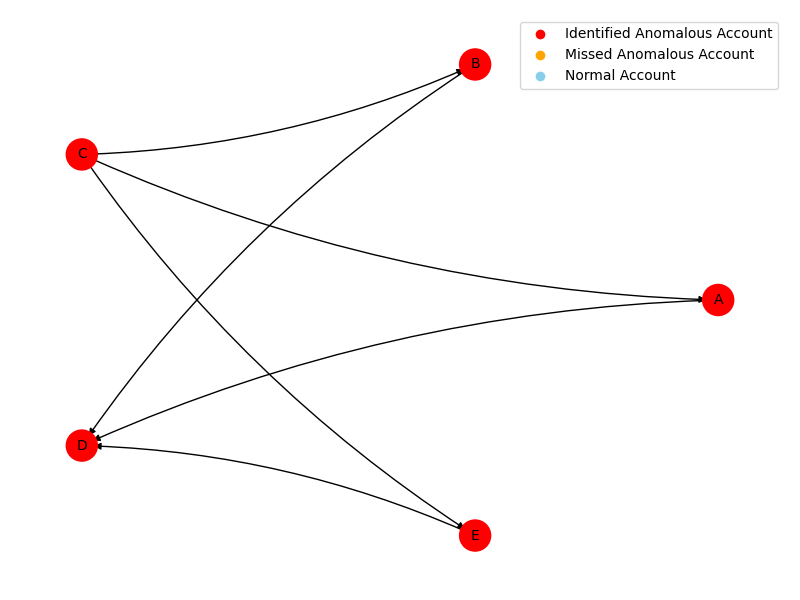

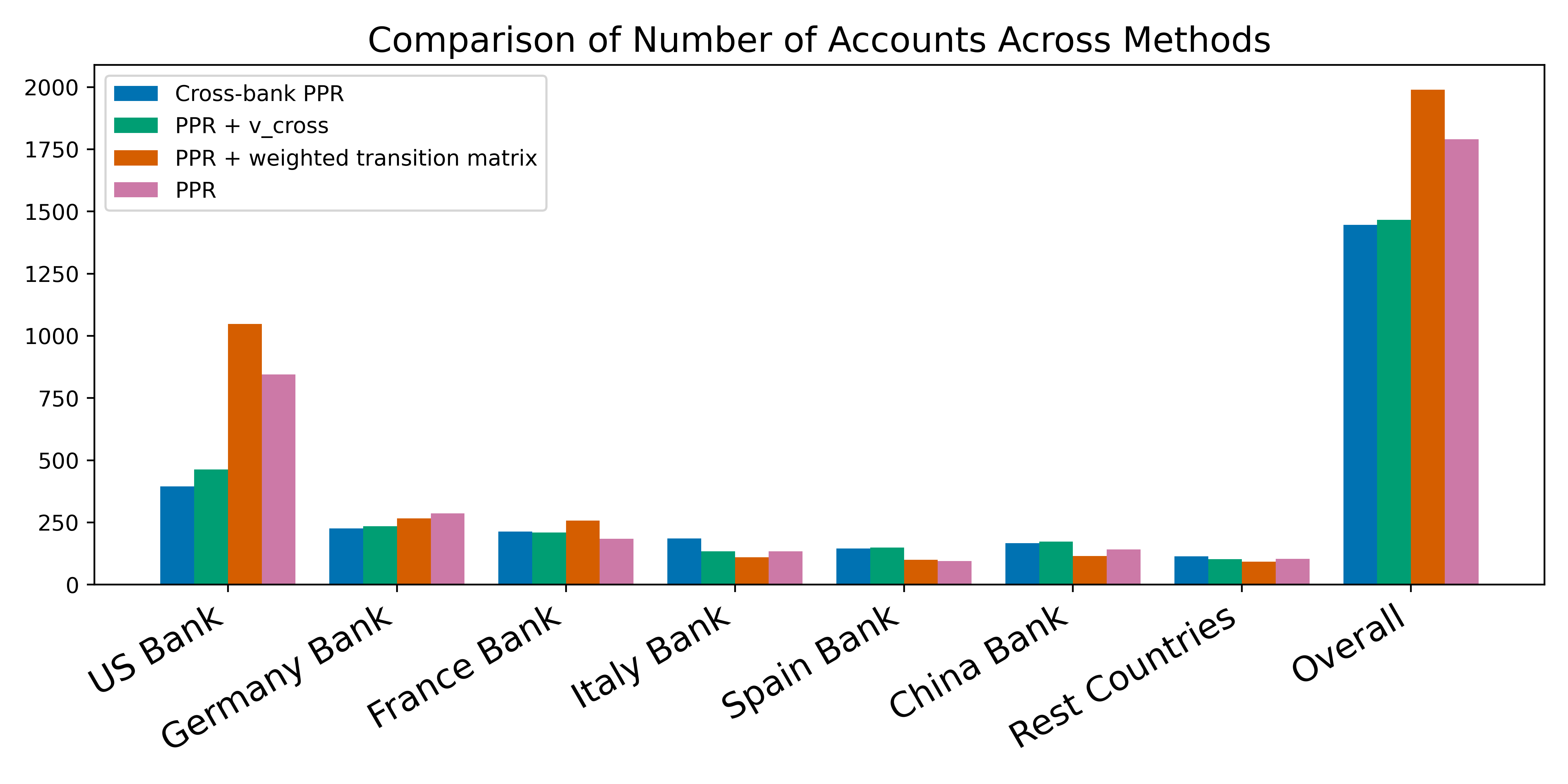

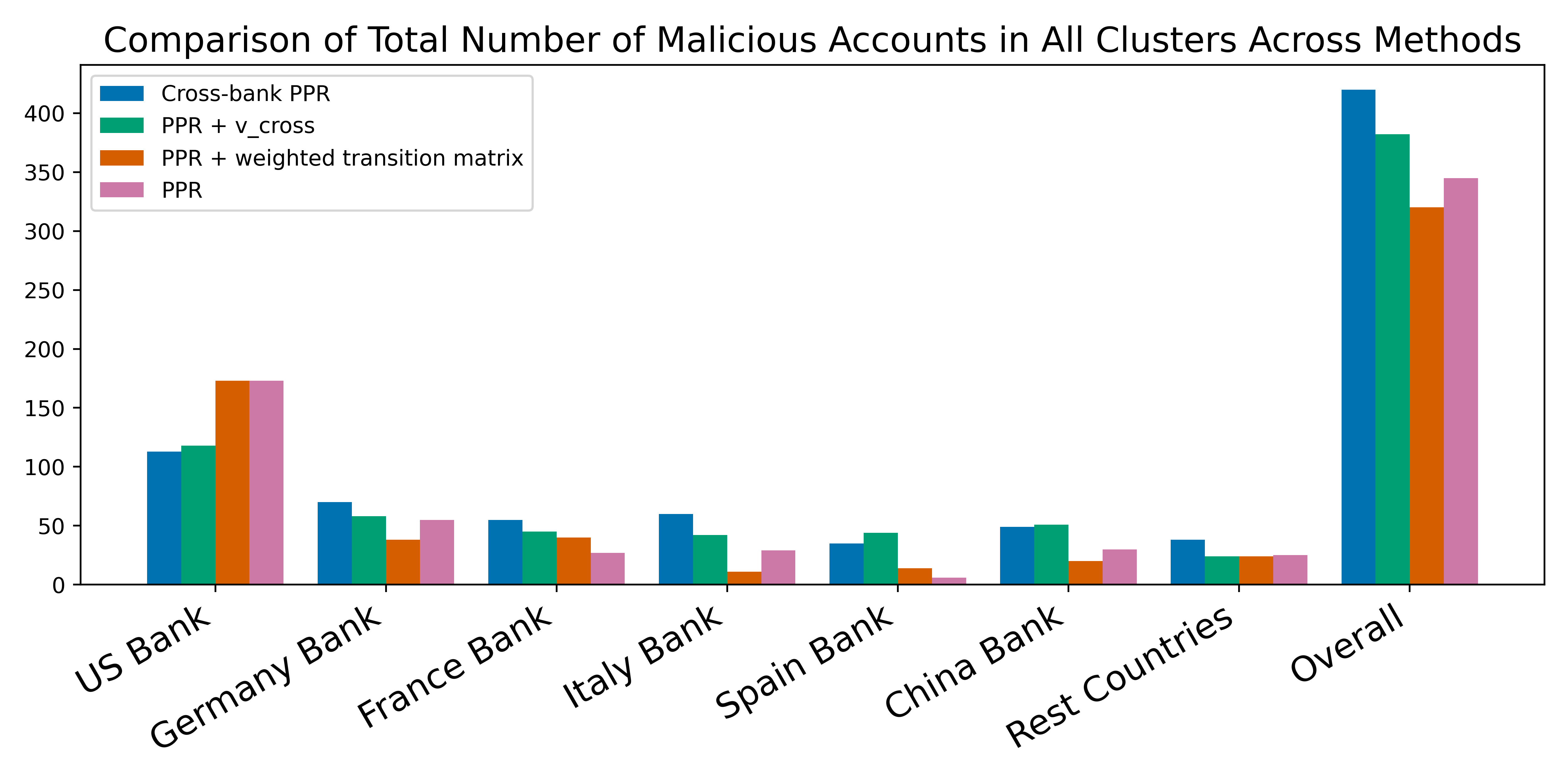

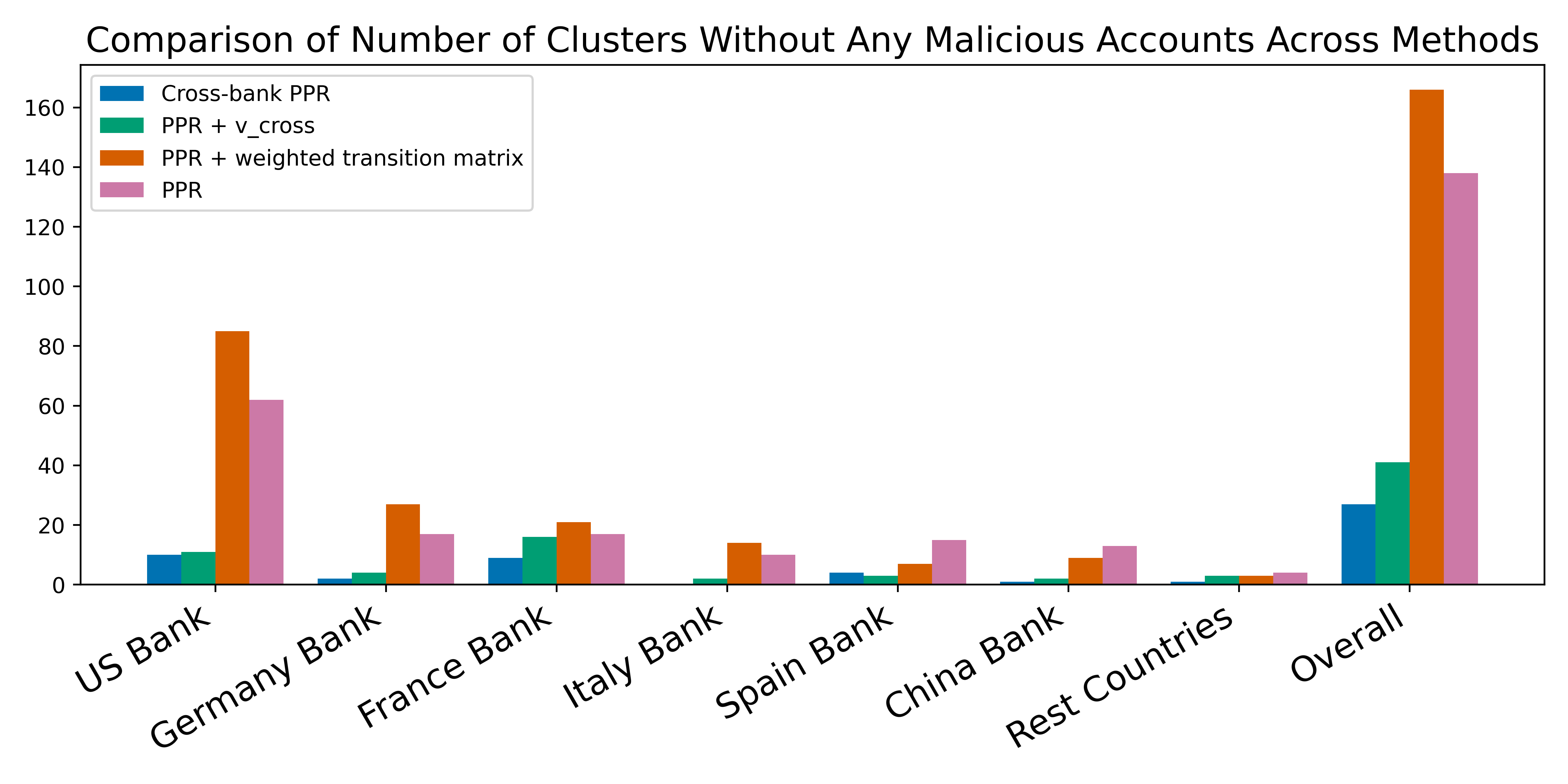

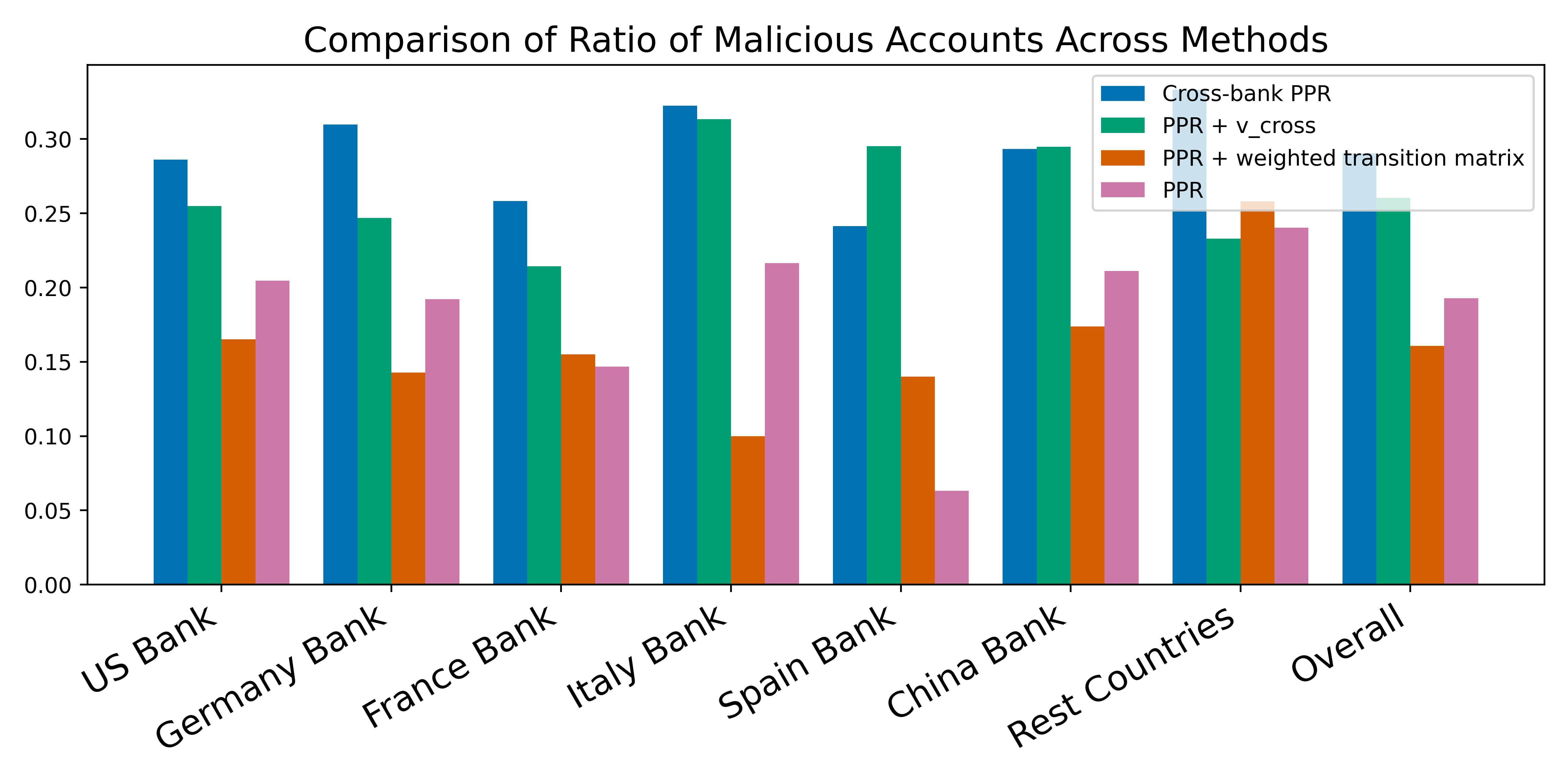

This paper demonstrates the strategic value of the proposed Cross-bank Personalized PageRank (PPR) framework. By enabling institutions to integrate Cross-bank intelligence into the ranking process, Cross-bank PPR consistently identifies substantially more true malicious accounts while flagging fewer accounts overall, compared with conventional PPR. This outcome reflects a more conservative yet more precise detection strategy, reducing unnecessary investigations while elevating the identification of genuinely high-risk entities. This paper also reveals that the incorporation of the cross-bank suspiciousness signal markedly improves precision and reduces false positives by itself, whereas the edge-level maliciousness score degrades performance, when used alone to reweight transitions. We attribute it to the reliable prediction by the detection module. However, when the edge score is fused with the cross-bank signal inside Cross-bank PPR, its weaknesses are corrected and it meaningfully enhances detection. Together, these components significantly reduce false positives, increase the concentration of malicious accounts within discovered clusters, and improve detection consistency across countries. These findings highlight that cross-institutional signal sharing, when designed with strong privacy safeguards, can meaningfully strengthen financial crime detection beyond what any single institution can achieve in isolation.

Our analysis of interpretable group identification using cross-bank Personalized PageRank reveals that money-laundering behaviors often exhibit diverse structural patterns, including fan-out, loop, gather–scatter, and hybrid mechanisms that integrate multiple strategies. The proposed cross-bank PPR method effectively uncovers the pivotal accounts orchestrating these operations, even when illicit activities are distributed across institutions and national boundaries. In particular, our approach successfully reconstructs the complete illicit group behaviors for many laundering schemes. As laundering strategies become increasingly sophisticated by mixing multiple mechanisms and fragmenting transaction flows across borders, our method continues to accurately flag primary dispersal accounts and expose partial cross-border linkages, offering critical insights into the underlying operational structure. These findings underscore that analyzing relational patterns across merged clusters not only captures the organizational essence of money-laundering schemes but also enhances interpretability, providing actionable signals for risk assessment and regulatory intervention.

Finally, we propose a hierarchical reinforcement learning strategy to move from detection to action. Rather than treating AML as a static classification problem, this approach dynamically learns how to respond to suspicious activity. It considers factors such as network risk concentration, and operational costs to determine optimal intervention strategies: when to monitor, and when to escalate a freeze intervention. By balancing accuracy with cost and compliance priorities, this decision-making layer bridges the gap between automated detection and effective financial risk management. Our empirical evaluation shows that this decision-making module delivers substantial economic value. While a fixed-threshold policy prevents 50% of illicit losses and exhibits extremely high Type II error rates, the hierarchical module prevents around 80% of potential financial loss and dramatically reduces missed detections. Moreover, the learned thresholds vary across institutions in different countries, highlighting that optimal intervention policies are inherently context-dependent rather than universal. These findings underscore that effective AML risk management requires not just accurate prediction, but a policy that intelligently maps risk signals to timely and context-sensitive actions.

The remainder of this paper is organized as follows. We review the related works in Section 2 and Section 3 presents the proposed graph-based federated detection module, which enables privacy-preserving collaboration across institutions. Section 4 introduces the personalized PageRank and label propagation mechanisms used to uncover subgroup structures and refine detection accuracy. Section 5 details the hierarchical reinforcement learning framework that supports adaptive and coordinated decision-making. Section 6 presents the empirical results. Finally, Section 7 concludes the paper and discusses future research directions.

2 Related Literature

Illicit financial activity detection has been an active area of research for decades, encompassing a wide range of applications such as financial fraud detection [fan2025unearthing, yiu2014deterrence, wu2024fair], anti–money laundering detection [deprez2025network], e-commerce fraud detection [nanduri2020microsoft, luca2016fake], social security fraud detection [van2017gotcha], securities fraud detection in emerging markets [guo2022hierarchical], etc. With the growing scale and complexity of financial transactions, machine learning has become a dominant approach for detecting illicit activities, offering improved accuracy and adaptability compared to traditional rule-based systems [august2025impact, fan2025unearthing, cecchini2010detecting, xiao2023black]. This study focuses specifically on the challenges of anti–money laundering detection.

The traditional ML-based AML systems are poorly equipped to handle this environment [pettersson2022combating, alotibi2022money, jensen2023fighting, lokanan2024predicting]. Eric and Jannis [*]pettersson2022combating evaluate four classic supervised learning algorithms (e.g., logistic regression, random forest, support vector machines, and decision trees) on the AML task and find that these models are too slow and require further optimization for the anti–money laundering context. More advanced supervised machine learning models have been proposed, trained on historical transaction data to detect anomalies and laundering patterns, offering more accurate and adaptive detection than traditional rule-based systems [golightly2023securing]. However, these methods rely on static machine learning and deep learning models, which fail to integrate information across institutions and struggle to adapt to temporally complex laundering strategies. Furthermore, studies show that some laundering schemes are executed rapidly over a handful of transactions, while others evolve over months and mix tactics such as layering and cross-border transfers [amoako2025exploring]. Anti–money laundering detection models tuned to one temporal horizon often miss others, creating a persistent tension between premature intervention and delayed action. Wang et al. [*]wang2024temporal demonstrate that traditional anti–money laundering systems struggle to detect complex schemes that leverage cross-jurisdictional gaps and the temporal dispersion of transactions, thus failing to capture complex evolving patterns in transaction networks.

Recently, Kurshan and Shen [*]kurshan2020graph and Lokanan [*]lokanan2023financial show the prominent performance of graph-based approaches on general financial fraud. For instance, Kurshan and Shen [*]kurshan2020graph provide a high-level discussion of the challenges faced by machine learning methods in combating financial crime, emphasizing issues such as scalability, data quality, and operational constraints. Although their survey does not center on AML, they underscore the strong potential of network-based methods for modeling the large-scale transactional data handled by financial institutions. Complementary to these methodological surveys, Gerbrands et al. [*]gerbrands2022effect examine AML from a policy and network-structure perspective, demonstrating how regulatory interventions reshape transactional networks and influence illicit financial behaviors. While this line of work highlights the importance of network analysis for understanding money-laundering dynamics, it does not develop learning-based detection models. More closely aligned with graph neural network approaches for AML, Kute et al. [*]kute2022explainable, kute2024explainable demonstrate how deep graph learning models can be augmented with explanation mechanisms to clarify which transaction patterns and behavioral attributes drive model outputs.

Model interpretability is critical in financial applications, as compliance officers and investigators must understand, trust, and act upon the model’s recommendations. Contemporary work on interpretable AML detection spans methodological advances in feature-based models, post-hoc explanation techniques, and network-aware methods and much of this literature appears in business-oriented outlets. Early applied studies established the value of supervised learning for prioritizing alerts while emphasizing model transparency [chen2018machine, han2020artificial]. Building on these works, Jullum et al. [*]jullum2020detecting develop and validate machine-learning scoring systems for transaction prioritization, showing how transparent feature design and risk-scoring improve investigatory efficiency. Konstantinidis and Gegov [*]konstantinidis2024deep evaluate explainable AI tools (e.g., SHAP and LIME) as operational supplements to black-box models, demonstrating that feature-attribution explanations improve auditability and the quality of Suspicious Activity Reports. Oloyede [*]oloyede2025evaluating explores how interpretability (e.g., transparent ML models) affects regulatory compliance, trust, and operational effectiveness in financial institutions. In parallel, Gu, Yang, and Liu [*]gu2025optimization incorporates causal reasoning to improve both the transparency and the decision consistency of AML systems. Recent reviews [mazumder2025explainable] synthesize these strands and call explicitly for XAI and socio-technical integration so that automated detection maps cleanly onto operational workflows and regulatory expectations. Collectively, these works show that effective AML solutions must go beyond predictive accuracy to provide clear, auditable rationales for their decisions, thereby enhancing investigator trust, supporting compliance verification, and ensuring that automated detection remains aligned with financial governance standards.

In the past decades, a growing body of research examines how anti–money laundering decisions and policies are shaped by regulatory frameworks, organizational practices, and behavioral responses to financial crime risks. Early work [ross2007money] highlights the central tension in AML supervision between rule-based requirements and risk-based decision-making, showing how compliance officers must interpret ambiguous regulations under conditions of limited information. Unger and Van Waarden [*]unger2009dodge further compare rule-based and risk-based AML strategies, arguing that excessive data collection without effective prioritization can overwhelm institutions and undermine detection quality. Complementing these policy-oriented perspectives, McCarthy, van Santen, and Fiedler [*]mccarthy2015modeling develop a microtheoretical model of money launderer behavior, illustrating how adversarial adaptation should inform AML policy design. Similarly, research on strategic learning behavior in markets demonstrates that sophisticated actors rapidly adapt their strategies in response to observed outcomes and platform policies ([xu2022ni]), underscoring the importance of adaptive detection systems that evolve alongside increasingly sophisticated laundering tactics. Helgesson and Mörth [*]helgesson2016involuntary shift attention to the role of professional intermediaries, demonstrating that lawyers become de facto policy actors when implementing AML and counter-terrorism financing mandates, often shaping regulatory outcomes through everyday compliance decisions. More recently, methodological advances have emerged, such as the reinforcement learning framework proposed by [rao2025reinforcement], which models cross-border transaction anomalies from a behavioral-economics perspective and offers a data-driven approach to dynamic AML decision-making. Together, these studies reveal an evolving landscape in which AML effectiveness depends not only on formal rules and technologies but also on how institutions interpret risks, allocate attention, and adapt to strategic adversaries.

Despite significant progress, these AML detection methods suffer from several critical limitations that prevent them from keeping pace with increasingly complex laundering behaviors. Traditional supervised machine learning and deep learning models [pettersson2022combating, alotibi2022money, jensen2023fighting, lokanan2024predicting, chen2018machine], while effective in narrow settings, remain largely static, siloed, and institution-specific. These systems struggle to generalize across heterogeneous financial institutions, cannot integrate cross-bank intelligence, and often fail under data imbalance or rapidly evolving laundering tactics. Recent interpretable or explainable AI approaches [chen2018machine, han2020artificial, kute2024explainable, kute2022explainable] focus primarily on feature-level transparency and do not reveal coordinated group behaviors or network structures underlying illicit flows. At the policy and decision-making level, current systems [ross2007money, unger2009dodge, helgesson2016involuntary, mccarthy2015modeling] are still reactive, offering little guidance on when and how local institutions should intervene in unfolding laundering schemes under a global coordination system. As a result, AML operations remain fragmented: models detect anomalies, investigators manually infer group structures, and compliance teams determine actions without principled support. The privacy-preserving adaptive framework proposed in this paper directly addresses these gaps. By enabling graph-based federated learning, our method preserves institutional privacy while facilitating cross-bank sharing. The integration of focal-loss–based detection, cross-bank PPR based group identification, and hierarchical reinforcement learning creates a unified pipeline that not only identifies suspicious entities but also uncovers their coordinated structures and recommends cost-sensitive, context-aware interventions. In doing so, the proposed system advances AML practice from isolated, static prediction tools toward proactive, explainable, and strategically optimized financial crime prevention.

3 Detection module

3.1 Graph Construction

Financial fraud, particularly money laundering [chen2018machine], poses a major risk to the stability and integrity of financial systems. A fundamental challenge in detecting money laundering is that transactional data are fragmented across banks due to privacy concerns, preventing the construction of a global view of illicit activities [le2018preventing, van2024privacy]. This bank isolation limits existing detection systems, leading to both false positives and false negatives, as suspicious behaviors often only emerge when transactions across multiple institutions are jointly analyzed [wang2024temporal, amoako2025exploring]. However, directly aggregating transaction data across banks is infeasible due to privacy and regulatory constraints [thommandru2023exploring].

Traditional machine learning approaches typically treat each transaction as an independent observation and largely ignore the relationships among consecutive money-laundering transactions made by the same group of accounts [wang2024temporal, amoako2025exploring, pettersson2022combating, alotibi2022money, jensen2023fighting, lokanan2024predicting]. Such independence assumptions limit their ability to recognize coordinated or evolving laundering schemes, where illicit funds are often transferred through a sequence of interconnected entities to obscure their origin and ownership. Inspires by this observation, we represent the transaction records as a set of graphs in which nodes represent accounts and edges denote fund transfers between them. The conversion to graph-structured data allows us to capture the interdependencies among transactions both direct and indirect within and across laundering groups.

Consider a transaction network111We use the terms graph and network interchangeably. consisting of subgraphs, where each subgraph represents the financial transaction system within a specific country. The set of nodes consists of entities (such as individual or corporate accounts) operating in country , while the set of edges captures the transaction links among these entities. When an edge connects and with , it represents a cross-border transaction, reflecting international fund transfers between entities in different jurisdictions. is the label vector, where indicates that the -th transaction is a money-laudering behavior and , otherwise. Here, we convert the set of edges into an adjacency matrix , where indicates an existing transaction link and , otherwise. Each node is associated with an attribute matrix that records its observable financial or behavioral characteristics, such as transaction frequency, while each edge is characterized by an attribute matrix that describes the properties of a transaction, including payment amount, method, and timing. Ultimately, our objective is to identify money-laundering activities, represented by malicious transaction links among accounts, and to understand how these illicit behaviors manifest and propagate across different countries.

3.2 Federated Graph-based Detection module

Given the adjacency matrix , we employ a graph neural network (GNN)–based encoder [kipf2016semi, DBLP:conf/iclr/XuHLJ19] to map the pair into a set of latent representations at the -layer:

| (1) |

where is the raw node attribute at the first layer, is the weight matrix at the -th layer, and is the ReLU activation function. Intuitively, this graph encoder aggregates information from each entity’s local neighborhood, allowing the representation of an account to be informed not only by its own attributes but also by the behaviors and characteristics of the entities it transacts with. This relational learning process captures how risk exposure or suspicious activity propagates through the transaction network. In financial systems, money-laundering behaviors often span multiple accounts and evolve through multi-step transaction chains. To emulate such interlinked and layered behaviors, we concatenate the latent representations learned from all layers to form the final embedding . This multi-level aggregation allows the module to integrate both local and global structural information, thereby capturing higher-order dependencies that reflect complex transaction patterns, such as circular money flows, bursty transfers, or structured layering activities commonly used to disguise illicit origins. To transform node-level representations into edge-level embeddings for transaction classification, we design an edge construction function that aggregates the features of the source and destination nodes together with the edge-specific attributes before computing the prediction via a multi-layer perceptron (MLP). Specifically, given two latent representations , for nodes , , and the edge associated attribute vector , we construct the edge representation as

| (2) |

where denotes the vector concatenation operation. In the representation , encodes the intrinsic behavioral and structural characteristics of the source account; models the directional discrepancy between the destination and source accounts, thereby encoding the asymmetric flow of information or funds, which is crucial for detecting suspicious transfers; preserve contextual information specific to the transaction, such as the amount or transaction type, providing direct evidence for abnormal activity. Overall, the resulting vector integrates both node-level and edge-level information into a unified representation that characterizes each transaction from multiple perspectives. This representation is then passed through a multi-layer perceptron followed by a sigmoid activation to predict the probability of the transaction being illicit:

| (3) |

where denotes the sigmoid function. The model can be trained end-to-end using the binary cross-entropy loss between the predicted probability and the ground-truth label :

| (4) |

Through this formulation, the model learns to distinguish illicit transactions by jointly considering node characteristics, their directional interactions, and edge-level contextual evidence. However, in real-world financial networks, the distribution of transactions is highly skewed as the vast majority are legitimate, and only a minute fraction correspond to money-laundering activities. This extreme class imbalance poses a fundamental learning challenge because the model tends to be biased toward predicting normal behavior, as minimizing cross-entropy naturally favors the dominant class. Consequently, even a trivial classifier that labels every transaction as normal can achieve deceptively high accuracy but fail to identify the rare yet critical illicit links that drive regulatory risk. To mitigate this imbalance, we adopt the focal loss [lin2017focal], which dynamically reweights training samples to focus more on hard-to-classify, minority cases. The focal loss modifies the cross-entropy objective as follows:

| (5) |

where is a class-balancing factor that adjusts the relative importance of the minority (suspicious) versus majority (normal) classes, and is a focusing parameter that controls the attention on misclassified or uncertain samples. Intuitively, serves as an “attention weight” for class imbalance. A higher increases the importance of correctly identifying suspicious transactions, ensuring that rare but high-impact money-laundering cases receive more focus, whereas a lower reduces sensitivity to the minority class. The focusing parameter emphasizes hard-to-classify samples. For a positive example (), when the model is confident (), the factor downweights the loss contribution, reducing the influence of easy cases. Conversely, for uncertain or misclassified positive examples (), the loss remains high, drawing attention to these high-risk transactions. Similarly, for negative examples (), the factor ensures the model focuses on ambiguous normal transactions. Collectively, and enable the model to prioritize learning from rare and high-risk transactions without being overwhelmed by the abundant routine activity.

From a managerial perspective, these hyperparameters encode distinct dimensions of institutional risk tolerance. The class-balancing factor reflects the strategic trade-off between compliance and customer experience: higher prioritizes catching illicit transactions even at the cost of more false positives, while lower minimizes unnecessary account friction to preserve customer relationships. The focusing parameter controls operational attention allocation: higher concentrates learning on ambiguous, hard-to-classify transactions—precisely the borderline cases that consume investigator time—while lower treats all misclassifications more uniformly. This parameterization allows institutions to calibrate detection systems to their specific regulatory environment and operational capacity.

As discussed earlier, one of the most critical challenges in cross-border money-laundering detection lies in the bank-isolation problem, where financial institutions are prohibited from directly sharing transactional data across borders due to strict regulatory and privacy constraints. This limitation hinders the ability to identify complex laundering schemes that intentionally distribute suspicious transfers across multiple banks or jurisdictions. To address this challenge while maintaining data confidentiality, we introduce the concept of a virtual super-node (), which abstractly represents the transactional relationship between two accounts belonging to different financial institutions. The super-node serves as a “boundary connector” between two subgraphs and , enabling institutions to share structured insights rather than raw transaction details. Formally, we denote by the set of virtual super-nodes, i.e., . Each super-node summarizes localized transaction behavior in a privacy-preserving form that can be exchanged for collaborative analysis. Specifically, we define the representation of a super-node as:

| (6) |

where and capture aggregated local neighbor information from their neighbor set and in subgraphs and , respectively. Notice that we can extend the mean aggregation (first-order statistical moment) to the combination of first-order and high-order moment, such as the aggregation of mean and variance, while our empirical results in Section 6.2.4 only show the marginal effect of including high-order moment. These embeddings act as compact statistical summaries of local cross-border activities, allowing each institution to participate in a federated learning process without revealing any sensitive data. To ensure semantic consistency across institutions, we introduce a self-consistency loss:

| (7) |

where is the subset of super-nodes associated with . This objective encourages alignment between the embeddings of shared super-nodes across banks, ensuring that the same cross-institutional transaction pattern is interpreted consistently. Conceptually, it enables a federated network of banks to “agree” on the structural signature of suspicious behavior, thereby strengthening the global defense against coordinated money-laundering schemes while respecting jurisdictional boundaries.

Beyond individual transaction links, money-laundering often manifests in higher-order structures, such as rings, chains, or star-shaped hubs that circulate illicit funds across multiple accounts. To explicitly encourage the model to capture such patterns, we employ a soft-membership differentiable graph cut loss [nazi2019gap], which promotes the identification of dense, irregular clusters in a fully differentiable manner:

| (8) |

where represents the soft community assignment of nodes in subgraph , is the diagonal degree matrix of , is the identity matrix, and is a regularization hyperparameter. The first term encourages nodes with strong transactional connections to be grouped together in the same cluster, effectively capturing tightly knit substructures that may indicate coordinated money-laundering activity. The second term regularizes the assignments to promote orthogonality among different clusters, ensuring that each node’s membership is distributed consistently and that communities remain distinct. Intuitively, this loss guides the embeddings to highlight anomalous clusters, such as small rings or star-shaped hubs, that deviate from normal transaction patterns, surfacing laundering groups that may evade detection through standard anomaly scoring alone. Finally, each bank optimizes a multi-objective loss:

| (9) |

where is the focal loss for edge prediction under weak supervision to distinguish suspicious transaction links, is the soft-membership differentiable graph cut loss that encourages discovery of dense and anomalous clusters indicative of coordinated laundering schemes, and is the cross-bank consistency loss that aligns shared super-node representations. The hyperparameters and balance the relative importance of the community structure and cross-bank alignment objectives, allowing banks to jointly learn risk-sensitive embeddings while preserving privacy and regulatory compliance.

Building upon the federated learning paradigm, each bank optimizes its local objective to update its model parameters using only its internal transaction data. Critically, raw data never leaves the institution, preserving privacy and regulatory compliance. At predefined communication rounds, each bank transmits only its model updates (gradients or parameters) and the aggregated super-node embeddings to a central server, which acts as a coordination hub rather than a data repository. Following the widely used federated averaging protocol [zhang2021survey, li2020review], the server updates the global model parameters as

| (10) |

where is the total number of participating banks. This weighted averaging effectively combines the knowledge learned from heterogeneous local datasets while mitigating biases that may arise from imbalanced or institution-specific transaction patterns. The updated global parameters are then redistributed to all participating banks, allowing each institution to benefit from the collective intelligence of the network without ever accessing another bank’s raw transactions. Intuitively, this collaborative process enables banks to detect complex, distributed money-laundering schemes that span multiple institutions or jurisdictions. By leveraging federated learning, the system simultaneously improves detection accuracy, respects data privacy, and aligns with regulatory constraints, creating a practical and scalable framework for cross-border financial crime prevention.

4 Identifying Group Patterns with Cross-bank Personalized PageRank

4.1 Personalized PageRank

While graph-based detection modules achieve strong predictive performance in identifying suspicious transactions, their complexity often limits interpretability, making it challenging for compliance officers to understand why certain accounts are flagged. In our proposed method, we employ a differentiable graph cut loss to capture higher-order structures, such as rings, chains, or star-shaped hubs that circulate illicit funds across multiple accounts. However, this approach alone may not capture group-level suspicious behaviors spanning multiple countries or accounts that often represent a mixture of incomplete laundering schemes rather than compact local structures. To enhance interpretability at the group-level, we incorporate Personalized PageRank (PPR) [page1999pagerank], a well-established algorithm originally developed and deployed by Google in the early 2000s to rank and organize web pages in its search engine. In the web context, PPR models how user interest in a particular page propagates through hyperlinks to identify other closely related pages. This intuitive notion of relevance diffusion motivates its application in financial networks. Specifically, starting from known high-risk accounts, PPR enables us to trace and quantify how suspicion propagates through transactional links to other closely connected accounts. By diffusing risk signals along multi-hop transaction paths, PPR reinforces model predictions while producing transparent and interpretable local clustering results that highlight intermediary accounts, relational dependencies, and latent laundering structures. This relational perspective allows compliance officers to better understand the contextual basis of flagged accounts, thereby increasing trust in model outputs and supporting more targeted and actionable investigations.

Formally, let the transactional network in a country be represented as a directed graph , with a weighted adjacency matrix , where reflects the normalized transaction intensity (e.g., frequency, volume, or dollar amount) from node to node . Traditional rule-based systems often focus on local anomalies, such as unusually large transfers or sudden spikes in activity. In contrast, money-laundering schemes are inherently relational, spanning multiple transactions, intermediaries, and jurisdictions. PPR addresses this limitation by diffusing initial suspicion scores across the network topology, allowing latent patterns, collusive groups, and hidden intermediaries to surface naturally. Formally, the PPR vector represents a steady-state distribution of a random walk over the network. At each step, the walk either follows an outgoing transaction with probability or teleports back to a set of high-suspicion seed nodes with probability :

| (11) |

where is a factor that balances local versus global influence, and is the personalization vector that concentrates probability mass on a set of known high-risk accounts . Specifically:

| (12) |

where is the initial suspiciousness score of node , derived from prior models, expert labeling, or regulatory flags.

4.2 Cross-bank Personalized PageRank

While PPR effectively amplifies and contextualizes suspiciousness signals within a single financial institution, it faces inherent limitations in the cross-border setting. Because of strict privacy and data-sharing regulations, transaction networks are fragmented across banks and jurisdictions, preventing the propagation of suspicion signals across institutional boundaries. Local biases in financial markets, documented in contexts such as crowdfunding [ni2025xinyang], suggest that institutions may systematically underweight cross-border signals, further motivating the need for mechanisms like Cross-bank PPR that explicitly integrate geographically distributed intelligence. As a result, money-laundering activities spanning multiple countries may appear incomplete or innocuous when analyzed in isolation as each country observes only a fragment of the global laundering pattern.

The effectiveness of PPR-based detection depends fundamentally on the separability of money-laundering groups within the network topology—a property we formalize in Theorem 4.1. To enhance detectability in fragmented settings, we introduce Cross-bank PPR, which incorporates cross-institutional intelligence while maintaining privacy constraints. Specifically, we modify the standard PPR formulation to incorporate the cross-bank suspicious signal from other countries into PPR design. Formally, by incorporating the cross-bank component , the formulation of PPR can be updated as follows:

| (13) | ||||

| (14) |

where is the prediction of the edge and if the edge does not exist, is the degree matrix of , encodes the bank’s internal suspicion sources, and represents external suspicious signals towards the cross-bank transaction shared across banks. Different from traditional PPR, we define the normalized weighted adjacency matrix that captures transaction intensity and encodes the suspicious score of the edge through and respectively. The teleportation factor thus determines the balance between exploring local transactional neighborhoods and returning to known suspicious nodes. By incorporating the cross-bank component , we enable a privacy-preserving exchange of aggregated suspicion information, allowing each bank to indirectly benefit from the intelligence gathered by others without revealing raw transactions. This cross-institutional diffusion enriches each bank’s PPR computation, helping surface hidden multi-bank laundering rings that would otherwise remain undetected due to regulatory isolation. In this way, the cross-bank PPR formulation combines fragmented data while maintaining compliance, substantially enhancing both the interpretability and completeness of risk detection.

In practice, the Cross-bank PPR vector can be computed iteratively as:

| (15) | ||||

| (16) |

which converges to a unique solution under mild conditions. Since the largest score in corresponds to the most suspicious seed node with the highest likelihood of being anomalous, we normalize by dividing each node’s score by the maximum value in , thereby converting the raw scores into anomaly probabilities. Using a predefined threshold, nodes with sufficiently high probabilities are identified as suspicious. Intuitively, in the PPR, nodes that are both structurally proximate to and frequently transacting with high-suspicion accounts accumulate higher steady-state probabilities. The PPR spreads risk signals through the network: even accounts not directly involved with known suspicious actors may receive elevated scores if they participate in multi-step chains, loops, or intermediary hubs commonly used in layering and integration stages of money laundering. Notice that high-ranking nodes can be traced through their most probable propagation paths back to seed nodes, offering analysts narrative explanations such as “Account connects to seeded node through a series of small but structured transfers.” These interpretable trails facilitate compliance documentation and regulatory auditing. Overall, PPR provides a mathematically grounded and operationally transparent mechanism to uncover money laundering rings by diffusing known suspicion through the transactional network. By integrating graph-theoretic reasoning with domain-aware weighting and temporal adaptation, it bridges the gap between static anomaly scoring and dynamic, relationship-centric risk discovery, thus improving both the precision and explainability of anti-money-laundering analytics.

To obtain a more comprehensive view of money-laundering activities across multiple countries, we merge clustering results from different national transaction networks into a unified framework. We start by identifying the cluster dictionary with the largest number of accounts as the initial reference. For each cluster in this reference dictionary, we iteratively examine clusters from other country-specific dictionaries to detect overlapping accounts. When overlaps are found, the clusters are merged to form a larger, consolidated cluster, ensuring that duplicated accounts are avoided. This process is repeated iteratively across all clusters, further merging any partially overlapping clusters to capture extended relational structures. By combining clusters in this way, the resulting merged dictionary integrates patterns spanning multiple financial institutions and geographies, allowing us to recover more complete money-laundering behaviors that may be fragmented across different national datasets. The merged clusters are then cross-validated against known laundering attempts to highlight clusters that contain multiple suspicious accounts, enhancing the interpretability and practical utility of the results.

4.3 Theoretical Insights of Using PPR for Grouping Money Laundering Behaviors

Having introduced Cross-bank PPR and demonstrated its empirical effectiveness, we now provide theoretical foundations for understanding when and why PPR-based methods can successfully identify money-laundering groups. We show that Personalized PageRank (PPR) initialized from a malicious seed node concentrates its probability mass inside the laundering group whenever the within-group connectivity is sufficiently stronger than the background connectivity, following the analysis by Avrachenkov and Andersen et al. [avrachenkov2015pagerank, andersen2006local]. Let denote a random graph generated by a two-block Stochastic Block Model (SBM) with nodes (we omit the graph index in this theoretical analysis for notation simplicity) and a planted laundering group of size . Edges are sampled independently as

| (17) |

Let be the adjacency matrix, the degree diagonal, and the random-walk transition operator. Given and a one-hot seed vector (corresponding to a known malicious seed ), the Personalized PageRank vector is

| (18) |

Denote by the mean-field (two-block averaged) transition matrix from the expected graph, whose block-averaged version is

| (19) |

We write and for the mean-field average PPR per node inside and outside the planted group:

| (20) |

and define the mean-field gap: .

Theorem 4.1 (Detectability of PPR under Planted Laundering Group).

Let with and assume that degrees concentrate around their expectations (i.e., Lemma 2 holds). Let be the Personalized PageRank vector seeded at a known malicious account with a constant , and denote the entrywise perturbation scale arising from stochastic fluctuations of around the mean-field transition matrix . There exist constants such that, with probability at least , if the mean-field gap satisfies

then

-

1.

the average PPR score on exceeds that on by at least ;

-

2.

ordering nodes by normalized PPR and selecting the prefix with smallest conductance recovers a subset with for some constant .

In the standard regime , the detectability condition simplifies to

where .

Proof. See Appendix A.

Theorem 4.1 establishes a detectability condition for identifying a money-laundering group using Personalized PageRank (PPR). Intuitively, PPR captures money-laundering behavior because it propagates the suspiciousness signal from a known malicious seed node through the transactional network. Nodes densely connected to the seed, likely participating in group laundering, accumulate higher PPR scores, while weakly connected nodes receive lower scores. The theorem formalizes this by showing that a well-separated group will stand out in the PPR ranking. In our proposed cross-bank PPR, we modify the transition matrix in PPR by assigning higher weights to edges more likely associated with laundering transactions as defined in Equation 13, which further amplifies scores for nodes strongly connected via suspicious interactions. Specifically, weighted edges increase the transition probability along suspicious links, causing PPR to concentrate more on nodes involved in laundering. This effectively increases relative to , enlarging the gap . Consequently, the detectability threshold is easier to satisfy, and PPR can recover a larger fraction of the laundering group or rank them higher in the graph cut procedure. On the other hand, to ensure that PPR starts with the malicious seed node, we reduce the probability of starting with a normal seed nodes by incorporating the cross-bank suspicious signal from other countries.

4.4 Label Refinement via Label Propagation

In the previous subsections, we demonstrated how cross-bank PPR captures group-wise money laundering patterns and provided theoretical insights into the detectability of PPR under planted laundering groups. In Section 6.3.1, we further visualize the identified laundering groups to highlight the interpretability of the proposed method. Beyond interpretation, a natural follow-up question arises: Can the discovered group-wise laundering patterns be further exploited to improve detection performance? To address this question, we propose a label refinement strategy based on label propagation. This design is motivated by the observation that money laundering activities are inherently group-based and densely connected. Similar to the diffusion mechanism underlying PPR, we hypothesize that malicious signals identified within high-confidence laundering groups can be propagated to neighboring nodes. This is particularly useful for suspicious nodes that receive low confidence scores from the base detection module and may otherwise be overlooked. By propagating malicious signals from confidently identified nodes to their neighbors, we increase the likelihood of recovering such borderline cases.

Formally, given a weighted graph represented by a sparse adjacency matrix, we first construct a row-normalized transition matrix . Starting from the edge-level prediction produced by the detection module, we compute a node-level malicious score for each account as

| (21) |

which corresponds to the average malicious score over all edges incident to node . These node-level scores form the initial label vector . Following the same idea of PPR, the label propagation process then iteratively updates the soft node labels according to

| (22) | ||||

where is the degree matrix, denotes the original graph adjacency matrix, and encodes the group-wise laundering structures identified by cross-bank PPR. The parameter controls the strength of propagation. Iterations continue until convergence, measured by the -norm difference between successive estimates, or until a predefined maximum number of iterations is reached. The resulting node labels are normalized to ensure numerical stability and rescale the malicious score within the range of [0,1]:

| (23) |

Since represents node-level malicious scores, we need to convert them back to edge-level signals by assigning each edge the maximum score of its incident nodes,

| (24) |

Finally, the original edge prediction is refined by incorporating the propagated malicious signal:

| (25) |

where balances the contribution between the base detector and the propagated group-level information.

5 Hierarchical Adaptive Decision-Making for Financial Security

5.1 Hierarchical Adaptive Decision-Making module

Regulatory authorities face clear-cut cases where intervention is straightforward: transactions flagged with very high confidence as suspicious should be immediately frozen. However, a critical challenge arises with transactions that receive low or moderate suspicion scores. Simply ignoring them risks missing coordinated laundering activities that unfold across multiple accounts and institutions, while indiscriminately freezing low-confidence transactions can lead to excessive disruption and unnecessary false positives. To address this challenge, we propose a Hierarchical Adaptive Decision-Making module that integrates local threshold-based reinforcement learning with a global coordinator to ensure the consistency between local and global policies. The module treats the outputs of the graph-based detection as initial probabilistic labels for each transaction, providing prior knowledge of suspicious activity. Then, it captures both short-term (local bank-level) decision feedback and long-term (global system-level) optimization of cooperative anti-laundering policies.

Each bank manages a local transaction network , where each transaction carries an anomaly probability . At time , the bank maintains an intervention threshold and decides whether to intervene:

| (26) |

To adaptively determine the threshold, we formulate the problem of adjusting thresholds as a reinforcement learning (RL) problem [li2017deep, szepesvari2022algorithms, ladosz2022exploration]. At time , the agent observes state , selects an action corresponding to a threshold , and receives a reward that measures the quality of decisions across all edges at the time :

| (27) | ||||

| (28) |

where is the cost of missing effective actions that should be deployed (which could be the amount of financial loss in this transaction), is the label showing whether this transaction is illicit, , , , , and are positive hyperparameters balancing the importance of different actions in six scenarios. Specifically, when a transaction is malicious (i.e., ), we reward the model if the model begins to intervene in this transaction either by freezing or monitoring this transaction, with showing the different weight for three actions. Otherwise, we reduce its rewards if no intervention is deployed. When a transaction is normal activity, we reward the model if it does not intervene in this normal behavior. Otherwise, we penalize the model at different degrees with . This reward design encourages high-probability suspicious transactions to trigger appropriate interventions, penalizes unnecessary actions on benign transactions, and incorporates operational cost through both the constant penalties and the cost-aware logarithmic terms. The goal of the local policy is to maximize the expected cumulative reward:

| (29) |

Our dynamic decision-making framework draws on the tradition of modeling sequential choice under uncertainty, where agents make decisions that affect both immediate outcomes and future states [mehta2017ni]. To address the negative impact of bank isolation issue, we propose a global-local coordinator to ensure the consistency between local and global policies. Specifically, local institutions adaptively respond to evolving transaction patterns, while the global coordinator aligns their behavior toward collective objectives. The global policy updates local thresholds using soft coordination:

| (30) |

where represents the relative institutional importance or transaction volume weight. To ensure the consistency between local and global policies, we define the coupling constraint as:

| (31) |

where the first term enforces consistency between local and global thresholds, and the second term aligns local policies with global intent through a KL-divergence regularization weighted by . The joint optimization objective becomes:

| (32) |

where controls the strength of policy coupling. The proposed hierarchical adaptive decision-making framework establishes a principled coordination structure for multi-institution financial security systems. Local RL agents autonomously learn transaction-level thresholds for each bank, while a global coordinator ensures cooperative, privacy-preserving, and regulation-compliant adaptation.

6 Empirical Results

6.1 Dataset Statistics and Feature Preprocessing

Our empirical analysis leverages the IBM Anti–Money Laundering (AML) Small dataset, which comprises over 5 million transaction records collected between September 1 and September 10, 2022. IBM Anti–Money Laundering dataset is a synthetic dataset, which is generated through a structured, multi-stage simulation framework designed to mimic real-world financial behavior while injecting realistic illicit activities [altman2023realistic]. According to Altman et al. [*]altman2023realistic, the process begins by constructing a population of synthetic customers, accounts, and financial entities whose demographic and behavioral attributes are sampled from empirically observed distributions. A transaction network is then formed by modeling normal financial activities using probabilistic rules calibrated to real banking data, capturing patterns such as salary deposits, bill payments, peer-to-peer transfers, and business-to-consumer flows. On top of this baseline, the system overlays money-laundering schemes—such as structuring, smurfing, round-tripping, and funnel accounts—through explicit scenario scripts that specify how illicit funds are introduced, layered, and integrated. Each scenario defines the actors involved, temporal patterns, transaction amounts, and network structures, ensuring that both benign and suspicious behaviors emerge organically within the same simulated environment. This combination of bottom-up population modeling and top-down illicit activity injection allows the IBM AML dataset to faithfully approximate real transaction ecosystems while providing ground-truth labels for evaluating detection modus 222Please refer to the paper by [altman2023realistic] for more details of generating the AML dataset..

| Country | #Accounts | #Total Transactions | #Illicit Transactions | Ratio of Illicity |

| United States | 71,796 | 855,006 | 3,043 | 0.35% |

| Germany | 31,566 | 275,129 | 1,308 | 0.47% |

| France | 28,126 | 244,589 | 952 | 0.38% |

| Italy | 23,262 | 194,155 | 804 | 0.41% |

| Spain | 24,363 | 207,098 | 763 | 0.36% |

| China | 21,345 | 181,341 | 961 | 0.52% |

| Rest Countries | 16,213 | 111,847 | 952 | 0.85% |

Since most of the baseline methods is not scalable to the large-scale dataset, we first compare the performance of our detection module with the existing methods in a subset with 1.4 million transaction records in this section and then we demonstrate the scalability of our method in Section 13. We summarize the transaction networks across different countries in Table 1 for the subset with 1.4 million transaction records. To mimic the cross-boarder money-laundering detection, we split the entire dataset into multiple subsets based on the nationality of banks. Transactions involving multiple banks are duplicated so that they appear in the networks of all relevant countries. After splitting, the United States represents the largest network, with over 71,000 accounts and approximately 855,000 transactions, followed by major European economies such as Germany, France, Italy, and Spain. Despite the variations in network size, a consistent pattern emerges across all markets: illicit transactions account for less than 1% of total activity. For instance, while China exhibits the highest proportion of suspicious transactions at 0.52%, the overall prevalence of illicit activity remains extremely low, reflecting the severe class imbalance that characterizes real-world financial data. Interestingly, the “Rest Countries” category, comprising smaller or less-regulated markets, shows a noticeably higher illicit ratio of 0.85%, suggesting that money-laundering activities may be more concentrated in regions with weaker oversight or fragmented compliance mechanisms. The prevalence of informal financial channels in emerging markets [bao2018nisingh] creates additional vulnerabilities that sophisticated laundering networks can exploit. This statistical profile underscores the operational challenge faced by financial institutions: effectively identifying rare, high-risk activities within overwhelmingly legitimate transaction flows. We partition each country-level dataset into a 5% training set and a 95% test set to evaluate model generalization under limited supervised data.

On the IBM AML dataset, a critical feature is transaction amount, which ranges from 1 cent to 8.04 billion dollars. Such a wide scale increases the number of training iterations required for most models to converge, and prior work has shown that appropriate feature normalization significantly accelerates deep network training ([ioffe2015batch]). Therefore, feature normalization is essential in our preprocessing pipeline. During preprocessing, we observed that the order of feature normalization and data partitioning meaningfully affects the performance of both our method and baseline models. This performance degradation stems from subpopulation shift [koh2021wilds]—a form of distribution shift where the overall population remains fixed, but the characteristics or proportions of underlying subgroups differ. In our setting, these subpopulations correspond to transactions originating from different countries/markets. When features are normalized before partitioning, each country receives data with similar statistical properties. However, when we first split the data by country and then apply feature normalization within each subset, the resulting country-level scales diverge substantially, increasing the degree of subpopulation shift.

| GraphName | Min | Max | Mean | SD | Min | Max | Mean | SD |

| United States | 0.01 | 2134359601 | 388627.61 | 10616792.77 | 0 | 5911955518 | 50279.46 | 9334910.41 |

| Germany | 0.01 | 8046315118 | 541468.28 | 31701228 | 0 | 0 | -102561.21 | -11749524.82 |

| France | 0.02 | 2134359601 | 410596.91 | 11738295.85 | -0.01 | 5911955518 | 28310.16 | 8213407.33 |

| Italy | 0.01 | 1825924651 | 446492.93 | 11949073 | 0 | 6220390468 | -7585.86 | 8002630.18 |

| Spain | 0.01 | 1825924651 | 472743.68 | 11263536.13 | 0 | 6220390468 | -33836.61 | 8688167.05 |

| China | 0.01 | 1825924651 | 432847.84 | 11948125.86 | 0 | 6220390468 | 6059.23 | 8003577.32 |

| Rest Countries | 0.01 | 7512426017 | 618635.73 | 34107069.54 | 0 | 533889100.7 | -179728.66 | -14155366.36 |

| Overall | 0.01 | 8046315118 | 438907.07 | 19951703.18 | 0 | 0 | 0 | 0 |

Subpopulation shift poses a practical challenge: (1) data cannot be shared across banks due to privacy and regulatory constraints, yet (2) proper normalization is necessary for model convergence. To validate our hypothesis that post-partition normalization amplifies subpopulation shift, we conduct an exploratory analysis using Min–Max normalization:

| (33) |

Table 2 reports the minimum, maximum, mean, and standard deviation (denoted as SD) of transaction amount for each country and for the global dataset. To quantify deviations between country-level and global distributions, we compute

| (34) |

where . Across all countries, the last three metrics vary substantially. This implies that widely used normalization strategies, such as Min–Max Normalization, Z-Score Normalization, and Mean Normalization, are likely to induce significant subpopulation shift when country-level statistics are used as proxies for global ones.

Next, we empirically evaluate how subpopulation shift affects model performance. To isolate its impact, we design a controlled experiment with two settings. (1) Country-level Normalization: We normalize the feature in each subset independently based on the country-level statistics. Notice that the country-level normalization induces the significant subpopulation shift due to the significant difference between the country-level statistics and global statistics. (2) Global-level Normalization: We normalize the feature in the entire dataset using global statistics. Because the second setting applies consistent scaling across all countries, it eliminates subpopulation shift. In both settings, we aggregate all transactions from different subsets into a single dataset and train each model once on the unified dataset. Table 3 presents the results, where Panel A corresponds to the setting country-level normalization and Panel B to the setting with global-level normalization. The results reveal two key findings. First, Random Forest shows mixed behavior: with global-level normalization, its Type II error decreases by over 11%, but its AUPRC drops by about 3% compared with country-level normalization, making it difficult to infer the overall effect solely from this model. Second, rest models, including Support Vector Machine (SVM), logistic regression, Federated MLP, and our proposed method, achieve higher AUPRC and lower Type II error when subpopulation shift is removed or replacing country-level normalization with global-level normalization. These empirical findings confirm that subpopulation shift meaningfully reduces the detection performance of most machine learning models in the AML setting.

| Panel A: Country-level Normalization | ||||||||||

| Graph | Logistic Regression | SVM | Random Forest | Federated MLP | Our Method | |||||

| AUPRC | Type II | AUPRC | Type II | AUPRC | Type II | AUPRC | Type II | AUPRC | Type II | |

| United States | 0.2381 | 0.0193 | 0.3412 | 1.0000 | 0.7503 | 0.3961 | 0.4977 | 0.0699 | 0.6881 | 0.0636 |

| Germany | 0.2875 | 0.0293 | 0.3340 | 1.0000 | 0.4101 | 0.7594 | 0.3771 | 0.0920 | 0.5544 | 0.0657 |

| France | 0.2370 | 0.0179 | 0.3086 | 1.0000 | 0.7266 | 0.3824 | 0.3369 | 0.0702 | 0.5299 | 0.0413 |

| Italy | 0.2717 | 0.0147 | 0.3070 | 1.0000 | 0.6896 | 0.4517 | 0.3759 | 0.1195 | 0.5363 | 0.0753 |

| Spain | 0.2712 | 0.0157 | 0.2754 | 1.0000 | 0.7010 | 0.3916 | 0.3347 | 0.0892 | 0.5026 | 0.0507 |

| China | 0.3202 | 0.0217 | 0.3443 | 1.0000 | 0.7047 | 0.4393 | 0.3924 | 0.0564 | 0.4716 | 0.0477 |

| Rest Countries | 0.5487 | 0.0156 | 0.6186 | 1.0000 | 0.6542 | 0.7337 | 0.6527 | 0.1020 | 0.7854 | 0.0666 |

| Overall | 0.3106 | 0.0192 | 0.3613 | 1.0000 | 0.6624 | 0.5077 | 0.4239 | 0.0856 | 0.6046 | 0.0600 |

| Panel B: Global-level Normalization | ||||||||||

| Graph | Logistic Regression | SVM | Random Forest | Federated MLP | Our Method | |||||

| AUPRC | Type II | AUPRC | Type II | AUPRC | Type II | AUPRC | Type II | AUPRC | Type II | |

| United States | 0.2761 | 0.0076 | 0.3752 | 0.8974 | 0.6446 | 0.3508 | 0.5136 | 0.0542 | 0.6922 | 0.0641 |

| Germany | 0.2886 | 0.0020 | 0.3642 | 0.8443 | 0.5961 | 0.4014 | 0.3867 | 0.0748 | 0.5617 | 0.0647 |

| France | 0.2471 | 0.0041 | 0.3453 | 0.8308 | 0.5714 | 0.4017 | 0.3485 | 0.0495 | 0.5399 | 0.0440 |

| Italy | 0.2722 | 0.0033 | 0.3801 | 0.8003 | 0.5758 | 0.4354 | 0.3757 | 0.1015 | 0.5406 | 0.0736 |

| Spain | 0.2585 | 0.0017 | 0.3300 | 0.8269 | 0.5762 | 0.3881 | 0.3379 | 0.0752 | 0.5153 | 0.0507 |

| China | 0.3017 | 0.0043 | 0.3458 | 0.8699 | 0.5919 | 0.4118 | 0.3865 | 0.0477 | 0.4774 | 0.0477 |

| Rest Countries | 0.5742 | 0.0042 | 0.6151 | 0.8229 | 0.7954 | 0.3541 | 0.6804 | 0.0949 | 0.7833 | 0.0609 |

| Overall | 0.3169 | 0.0039 | 0.3937 | 0.8418 | 0.6216 | 0.3919 | 0.4327 | 0.0711 | 0.6105 | 0.0596 |