Automated Market Making for Energy Sharing††thanks: We are grateful to Ulysse Griffon for his research assistance. We also thank the audiences at the following events for their feedback: The guest lecture in the CS 6501: Economics of Distributed Systems course at the University of Virginia (Fall 2024), seminars at École Polytechnique (January 2025), the University of Virginia Computer Science Theory Seminar (February 2025), the UCSB DeFi Seminar (April 2025), the TLDR Conference at Columbia Business School (May 2025), the Second Tech4Finance Conference at Université Paris Dauphine (March 2025), Télécom Paris (June 2025), Princeton DeCenter (June and November 2025), ANR BlockFi Workshop Grenoble (December 2025). We also thank Julien Prat, Alfred Lehar, Ciamac Moallemi, Alkis Georgiadis-Harris for their valuable comments. Financial support from the Fellowship “The Latest in Decentralized Finance” (TLDR, 2024/2025 cohort) is gratefully acknowledged.

Abstract

We develop an axiomatic theory for Automated Market Makers (AMMs) in local energy sharing markets and analyze the Markov Perfect Equilibrium of the resulting economy with a Mean-Field Game. In this game, heterogeneous prosumers solve a Bellman equation to optimize energy consumption, storage, and exchanges. Our axioms identify a class of mechanisms with linear, Lipschitz continuous payment functions, where prices decrease with the aggregate supply-to-demand ratio of energy. We prove that implementing batch execution and concentrated liquidity allows standard design conditions from decentralized finance—quasi-concavity, monotonicity, and homotheticity—to construct AMMs that satisfy our axioms. The resulting AMMs are budget-balanced and achieve ex-ante efficiency, contrasting with the strategy-proof, ex-post optimal VCG mechanism. Since the AMM implements a Potential Game, we solve its equilibrium by first computing the social planner’s optimum and then decentralizing the allocation. Numerical experiments using data from the Paris administrative region suggest that the prosumer community can achieve gains from trade up to 40% relative to the grid-only benchmark.

1 Introduction

The traditional architecture of the electric power grid is increasingly strained by the proliferation of Distributed Energy Resources (DERs), such as rooftop solar, electric vehicles, and residential batteries. Designed primarily for uni-directional power flows from centralized generators, the existing infrastructure struggles to accommodate the volatility and bi-directional flows inherent to markets with significant DER penetration. Central to this landscape is the figure of the power producer-consumer, or prosumer. As the legacy grid model falters, these actors offer the potential to reduce reliance on centralized generation and provide essential distributed flexibility. This necessity is underscored by recent instability events, such as the April 2025 blackout in the Iberian Peninsula (entsoe2025blackout) triggered by disturbances at large-scale solar farms. This event exposed the fragility inherit in centralized power architectures, highlighting the need for decentralized markets mechanisms that coordinate prosumer behavior to absorb such systemic shocks. In response to these challenges, this paper investigates the potential of Automated Market Makers (AMMs) to facilitate decentralized market clearing within prosumer communities. We propose a design where the AMM functions as an algorithmic intermediary that coordinates prosumers by quoting dynamic price curves based on aggregate supply and demand. Our contribution is to provide an axiomatic characterization of this mechanism and to analyze the properties of the resulting market equilibrium within a mean-field game.

The AMM mechanism introduced in this paper is fundamentally different from AMMs in decentralized finance (DeFi). First and foremost, the proposed energy AMM does not hold an inventory, and thus does not rely on liquidity providers. It rather utilizes the main grid as a buyer and seller of last resort. This configuration allows one to designate a coordinator node within the local power grid to offer effectively “infinite liquidity” for residual imbalances. The economic logic of the mechanism is to profit from operating within the spread between the grid’s retail price—purchase price—and the feed-in tariff (FIT)—sale price. This margin is often substantial; indeed, in many jurisdictions (such as Brazil) the FIT is effectively zero (epe2022nota).555In Brazil, the selling price is effectively zero for cash flows under the 2022 regulation. This policy reflects a broader issue of renewable curtailment—exceeding 10% in some regions (ONS_PEN2024)—caused by transmission congestion and insufficient local demand during peak generation hours. By signaling abundance through lower prices, the AMM incentivizes local consumption and storage, mitigating the need for such curtailment.666In the European Union, 2023 data show that substantial spreads at peak-hours, e.g.: Spain (Buy €0.32 vs. Sell €0.06–0.10/kWh), France (Buy €0.25 vs. Sell €0.13–0.18/kWh), and the Netherlands (Buy €0.32 vs. Sell €0.08–0.12/kWh). Similarly, in the United States, the shift from Net Metering to Net Billing (e.g., California’s NEM 3.0) seems to have widened this gap, with export rates dropping to cost-avoidance levels ($0.05/kWh) against retail rates exceeding $0.30–0.40/kWh.

1.1 Contribution and Paper Structure

This paper makes both conceptual and quantitative contributions to the design and analysis of local energy sharing markets. In the first part of the paper, Sections 2 and 3, we demonstrate that design principles from blockchain-based Constant Function Market Makers (CFMMs) apply in this context. In particular, price curves derived from trading functions (i.e., potentials) that are suited for blockchain applications—namely those quasi-concave, homothetic, and monotone—are compliant with market design axioms that guarantee an efficient operation of local electricity markets. These axioms impose anonymous execution of local trade, which distinguishes the AMM from order books and bilateral P2P matching where the order of bids and the identity of the bidders matters. Furthermore, a coalition-proofness requirement implies that the AMM payment function is linear in the prosumer’s power flows and quotes marginal buying and selling prices that are bounded and decreasing in the aggregate supply-to-demand ratio of power. The resulting AMM operates through three distinct phases: (1) dynamic re-anchoring the trading function to align it in real-time with the energy price (buying price) and the feed-in-tariff (selling price); (2) determination of the internal clearing price via batch execution and concentrated liquidity; and (3) distribution of power export revenues and import costs proportionally to prosumers’ contribution to the community power balance.

In the second part of the paper, Sections 4 and 5, we move from the definition of the market mechanism to the analysis of strategic behavior within the market. We model the prosumer community interaction as a dynamic stochastic game involving a large population of price-taking prosumers. Within this environment, each prosumer solves a dynamic optimization problem to determine their net power profile—jointly optimizing consumption, battery usage, and trading decisions—to maximize expected discounted profits over discrete trading sessions.

As prosumers interact, market prices (and rational expectations on them) arise endogenously from the aggregate net flows induced by the mixed-strategy Markov Perfect Equilibrium (MPE) of the game. Solving for such equilibrium can, in principle, be challenging due to the curse of dimensionality. However, a central finding of our paper establishes an equivalence between the decentralized MPE and a centralized Social Planner problem. We prove that the AMM frames the strategic environment as a potential game: the mechanism acts as a coordination device where the gradient of prosumers’ profit functions aligns with the gradient of a global potential function, representing the prosumer community’s expected gains from trading with the power grid (importing and exporting electricity). Under our axioms, the “invisible hand” of the market is at work: a sub-optimal clearing of internal supply and demand leads to arbitrage opportunities over quoted prices, which prosumers are incentivized to exploit to restore efficiency.

The capability of coordinating prosumers purely by market forces, combined with its simplicity, position the AMM as a practical alternative to market designs that have struggled to gain traction in recent years. For instance, pilot programs based on double auctions often struggle to scale because they require residential users to actively bid and commit to consumption schedules before the actual power flows occur—a feature which may discourage non tech-savvy residential households. Conversely, while the Vickrey-Clarke-Groves (VCG) mechanism achieves a stronger notion of efficiency (ex-post efficiency) and satisfies strategy-proofness, it again requires full type disclosure ahead of power flows, and generally runs a budget deficit. The AMM instead is budget-balanced and charges prosumers right after power exchanges occur based solely on on real-time metering data—making it more suitable for possible integrations with automated smart-home energy management systems. Moreover, by decentralizing the power flow optimization on the user side, the AMM fosters the development of an open marketplace where energy startups can develop and offer power profile optimization tools.

Besides conceptual relevance, our main equivalence result has practical implications. In fact, we use it to develop a procedure that computes the equilibrium and simulates the behavior of a representative prosumer community. A key property for doing so is the scale-invariance (homogeneity of degree one) of the AMM payment function. This property allows us to circumvent numerical integration over a high dimensional type space by making the Planner’s Problem asymptotically equivalent to its deterministic mean-field limit—the certainty-equivalent surplus of a representative prosumer. Based on this, we compute the MPE by approximating the equilibrium mixed strategy of the infinite-dimensional population via state-dependent representative types and “Monte-Carlo decentralization”—a procedure that solves the equilibrium mixing weights for representative prosumers, then simulates the distribution of induced actions it via Monte-Carlo sampling and Euclidean projection onto the actual prosumers’ action spaces to enforce feasibility. Furthermore, we approximate the infinite-horizon Bellman equation of the Planner by employing Model Predictive Control (MPC) with a finite lookahead window, a technique established in battery optimization theory and practice.

Finally, in the last part of our paper (Section 6), we bring the model to data to quantify the benefits for both individual prosumers and their community. Using real-world weather and consumption data from the Île-de-France (Paris) region, we simulate a heterogeneous community of 1,000 agents over a full year (2023), allowing them to optimize their strategies over discrete 15-minute intervals (96 decision time-steps per day). The population is composed of 40% pure consumers, 30% solar prosumers (equipped with 1.6 panels at 15% efficiency), and 30% wind prosumers (using 1.9m-blade turbines), all managing 20 kWh residential batteries and a demand profile with 30% flexible load.

Our experiments reveal that the AMM generates substantial value by arbitrating the spread between electricity retail tariffs and the community’s flexible needs. While the main grid charges a peak rate of 21.46 c€/kWh and offers a meager feed-in tariff (FIT) of 8.86 c€/kWh, the AMM allows prosumers to trade internally at dynamic clearing prices that frequently settle near 13–15 c€/kWh. This allows prosumers to satisfy demand at roughly half the cost of peak grid power, while simultaneously selling surplus generation at a premium of 50–60% over the standard FIT. By enabling agents to shift 30% of their flexible load and synchronize 20 kWh batteries to these internal prices, the mechanism reduces the average daily energy cost per agent from €1.24 to €0.72—a 60% reduction in individual spend—and achieving community’s gains from internal trade of 42% relative to uncoordinated trading with the power grid.

Related Work

To the best of our knowledge, this work represents the first effort to bridge literatures on the economics and optimization of power systems, computational game theory, and decentralized finance (DeFi).

Distributed Optimization in Power Systems.

A substantial body of literature applies the Alternating Direction Method of Multipliers (ADMM) and related decomposition techniques to Optimal Power Flow (OPF) and grid coordination problems (boyd2011admm; erseghe2014opf; Moret2024). These approaches typically decompose the global optimization problem into coupled subproblems solved iteratively by network agents. While effective for computation, standard ADMM-based schemes do not generally ensure incentive compatibility during the iterative process, nor do they offer a clear economic interpretation of the intermediate “prices” (dual variables) prior to convergence. In contrast, the market mechanism proposed herein relies on axiomatic pricing rules which guarantee that prices remain economically meaningful even when the community has not yet reached its equilibrium.

There is also an extensive literature on battery optimization techniques. We draw upon recent advances in finite-horizon approximations for storage scheduling; in particular, (prat2024finitehorizon) show that (under mild regularity conditions) the quality of approximation to the solution of an infinite-horizon Bellman equation using a rolling-horizon Model Predictive Control (MPC) improves exponentially with the size of the MPC lookahead window.

Equilibrium Analysis of Power Systems.

Strategic bidding and market clearing in power systems populated by DERs have traditionally been modeled as bilevel optimization problems or Mathematical Programs with Equilibrium Constraints (MPECs) (hobbs2000strategic; Hasan2008; gabriel2012complementarity). Our equilibrium analysis, however, diverges from that paradigm and shares closer similarities with routing and congestion games. In these frameworks, agents optimize flows over a network subject to costs that depend on aggregate usage, often admitting a potential function that guarantees the existence and uniqueness of an equilibrium (rosenthal1973congestion; monderer1996potential).

Automated Market Makers and Decentralized Finance.

Constant Function Market Makers (CFMMs) have emerged as the dominant design paradigm for on-chain decentralized exchanges. The axiomatic foundations of these mechanisms have been extensively studied, demonstrating that trading functions which are quasi-concave, monotonic and homothetic induce markets with desirable properties (angeris2020improved; angeris2023geometry; schlegel2023axioms; fabi2025economics). In this paper we show that such trading functions can be implemented in this context to generate prices that effectively coordinate a community of prosumers. AMMs with batch order execution—a feature of our proposed design—has been analyzed as a possible way to implement execution fairness (canidio2023batching; he2024optimaldesignautomatedmarket). We adapt these principles to the energy domain, replacing token inventories with grid-backed liquidity.

The implementation of an AMM for energy grids falls into the scope of Decentralized Physical Infrastructure Networks (DePIN). While recent work has addressed incentive-compatible signal recovery in DePIN systems—such as verifying bandwidth claims (milionis2025depin)—our work assumes reliable smart meter data and focuses on the economic behavior of agents.

Peer-to-Peer Markets and Prosumer Economics.

The rise of the ”prosumer” has necessitated new economic models for distributed energy interaction (gautier2018prosumersgrid; gautier2024economicsofprosumers). Extensive surveys on peer-to-peer (P2P) energy trading and local flexibility markets highlight the diversity of proposed pricing mechanisms (SOUSA2019367; CROWLEY2025125154; pinsonP2P; alfaverh2023dynamic). Our analysis demonstrates that many existing P2P pricing rules can be recovered as special cases of the generalized trading functions presented in this paper (8279516; 8572734), providing a unified theoretical framework for local energy exchange.

Mean-Field Games.

Our equilibrium results derived under large population approximations by The theory of Mean Field Games (MFG) (lasry2007meanfield; GueantLasryLions2011), which deals with limits of games when the number of agents goes to infinity and payoff externalities occur only through aggregate statistics of population actions, such as the ratio of supply to demand in our case. While the core literature is focused on continuous-time stochastic games, our approach builds on recent discrete-time formulations (e.g., Doncel_2019; guo2024mf). Our algorithm combines MPC and “Monte Carlo decentralization” to solve numerically the Master Equation of the game, given by the Social Planner’s value function, together with the evolving distribution of battery States of Charge (SoC) across the population.

2 Axiomatic Design of an Energy Sharing Market

This section develops a formal model for a peer-to-peer (P2P) energy sharing market and introduces a set of axioms that characterize a desirable pricing mechanism. For the purpose of this axiomatic analysis, we treat individual energy flows as exogenously given; these flows will be endogenized as solutions to prosumer optimization programs and as Markov Perfect Nash Equilibrium (MPE) outcomes in Sections 4 and 5.

2.1 The Microgrid

We consider a local energy community (i.e., a microgrid) composed of a set of prosumers. These prosumers interact through a central aggregator, which facilitates local energy trades to import or export power. The aggregator is also connected to the main electrical grid.777In principle, we can allow every prosumer to be also connected to the main grid, forming a double-star network. However, the axoms defined later on in this section impose a participation (individual-rationality) constraint such that prosumers always prefer to trade with the aggregator rather than directly with the external gird.

Within this framework, the aggregator operates as the community’s local market maker. Its function is to pool all energy supply and demand from the prosumers and to set a single, uniform price for buying and selling energy within the community, based on a deterministic function of these aggregates. This pooling mechanism provides “infinite” liquidity and abstracts away the need for direct, bilateral negotiations between prosumers.

By complementing the local market maker, the main grid functions as the market of last resort. It is an infinitely liquid external venue that guarantees the local community can always balance its net energy position after all internal trading has been resolved by the aggregator. The main grid will buy any community-wide surplus and supply any community-wide deficit. For most of our analysis, we assume the grid’s capacity to do so is not binding.

The main grid, operated by a retailer (or a competitive retail market), sets two distinct prices at each time for trading electricity. It buys energy from the community at an exogenous Feed-in Tariff (FiT), denoted by , and sells energy to the community at a higher retail price, . These two prices form the external benchmark and the price boundaries for the local market.

2.2 Market Definition

We now formally define the local energy market and its properties. Market interactions involve each prosumer submitting a net energy flow, or netput , to the aggregator. Since we will describe pricing at a given time step, for notational simplicity, we omit the time index . A positive flow () represents a net supply to the local market, while a negative flow () represents a net demand. The collection of these individual flows constitutes the market’s allocation vector, .

Although our full model is dynamic, with trades occurring at discrete trading sessions within epochs (e.g., days), the definition of market and payment rules applies to any single trading session. For this reason, for now we adopt a static view and omit the time and epoch index for simplicity.

The mechanism’s function is to map this allocation to a vector of payments:

Definition 1 (Market Mechanism).

A market mechanism for energy sharing is a pair , where:

-

•

is the energy allocation vector.

-

•

is the payment function, which maps an allocation to a payment vector .

A positive payment represents a revenue for prosumer , while a negative payment represents a cost.

For our analysis, it is useful to decompose the net flows and payments into more intuitive components. Specifically, An individual prosumer’s net flow can be split into non-negative supply () and demand ():

| (1) |

Summing these across all prosumers gives the aggregate local supply () and aggregate local demand ():

| (2) |

The community’s net position relative to the main grid is . This can be decomposed into the total energy exported to () or imported from () the main grid:

| (3) |

Similarly, each prosumer’s net payment is the difference between a non-negative revenue function and a non-negative cost function :

| (4) |

2.3 Axiomatic Characterization

Our goal is now to define design a mechanism based on a set of desirable features, detailed by the axioms that will follow.

2.3.1 Anonymity

In many P2P markets, such as those based on limit order books, the identity and arrival time of an order can influence its execution price. This creates opportunities for preferential treatment or strategic exploitation like front-running. To avoid this, a local energy sharing market should be anonymous. Informally, this means that a prosumer’s payment should depend only on their own energy contribution and the collective contributions of others, not on anyone’s identity.

Axiom 1 (Anonymity).

A market mechanism is anonymous if for any prosumer and any permutation of the other prosumers, the payment to remains unchanged:

where is the vector of allocations for all prosumers other than , and is the vector with those allocations permuted.

Anonymity and Batched Pricing.

The axiom of anonymity forces the payment function to disregard the identities of the prosumers, meaning all trades can be processed as a single batch. Formally, a prosumer’s payment can only depend on their own allocation, , and the multiset of all other allocations, denoted .

Proposition 1.

A market is anonymous if and only if there exists a function such that for any prosumer :

This functional form is the essence of an Automated Market Maker (AMM) in this context. Because the rules are anonymous, the mechanism is stripped of any discretion; it cannot rely on subjective information about participants (e.g., identity, reputation, or past behavior). Pricing must be determined solely from the submitted quantitative data via a pre-defined, deterministic rule. This rule is, in effect, an algorithm, which is precisely what makes the market maker ”automated.” Consequently, mechanisms that rely on order arrival or identity, like limit order books and bilateral matching, are precluded.

Notice also that Anonymity is equivalent to the principle of Fairness, which requires that prosumers who contribute identically are paid identically. A market is fair if for any two prosumers and .

Equivalence to Fairness and Aggregation.

While the function could depend on the full distribution of trades, a powerful simplification is to make payments depend only on the total aggregate supply () and demand (). This leads to a more tractable pricing rule, :

The mechanisms constructed in this paper will adhere to this aggregation-based pricing principle.

2.3.2 Coalition-Proofness

A robust market mechanism should not incentivize strategic manipulation by groups of participants. The axiom of coalition-proofness ensures that a group of prosumers (e.g., all sellers or all buyers) cannot benefit by merging their individual trades into a single, larger trade, or by splitting a large trade into several smaller ones. This guarantees that the mechanism treats individual contributions additively.

Axiom 2 (Coalition-Proofness).

A market mechanism is coalition-proof if for any coalition of pure sellers and any coalition of pure buyers , the following additivity conditions hold:

| (5) |

This additivity requirement implies a linearity restriction on the functional form of the payment function:

Proposition 2 (Linear Payment Function).

A market mechanism satisfying aggregation-based pricing is coalition-proof if and only if the payment function is linear in the prosumer’s own supply and demand . Specifically, there exist price functions and such that:

where and are the aggregate supply and demand.

This proposition is a crucial step in our design. It proves that any anonymous, coalition-proof mechanism must operate by establishing a uniform marginal selling price, , for all sellers and a uniform marginal buying price, , for all buyers. This result dramatically simplifies our analysis: instead of reasoning about a complex, high-dimensional payment function , we can now focus on the properties of these two intuitive, one-dimensional price functions. All remaining axioms will be defined as constraints on the behavior of and .

2.3.3 Core Economic Axioms

Having established that a rational market mechanism must use linear pricing, we now introduce three fundamental axioms that govern the behavior of the marginal price functions, and . These axioms ensure the mechanism is internally consistent, financially viable, and economically beneficial to its participants.

No-Arbitrage.

First, the mechanism must be free from internal arbitrage. A participant must not be able to generate a risk-free profit by simultaneously buying and selling energy from the aggregator. This requires that the marginal selling price can never exceed the marginal buying price.

Axiom 3 (No-Arbitrage).

A market mechanism satisfies no-arbitrage if for any pair :

| (6) |

Budget-Balance.

A core requirement for a self-sustaining market is that it must be financially viable without external subsidies. The axiom of budget-balance ensures this by requiring that the total payments collected from buyers are at least as great as the total revenues paid out to sellers.

Axiom 4 (Budget-Balance).

A market mechanism is budget-balanced if for any state :

| (7) |

If the condition holds with equality, the mechanism is exactly budget-balanced.

Individual Rationality (IR).

Finally, the mechanism must provide an incentive for prosumers to participate over their outside option of trading directly with the grid. The prices offered by the local market must be strictly better than the grid’s prices when local supply and demand can be matched, and they should converge to the grid’s prices when the community has a net surplus or deficit that must be cleared externally.

Axiom 5 (Individual Rationality).

A market mechanism satisfies Individual Rationality (IR) if the price functions and adhere to the following boundary conditions:

| (8) |

This IR condition is the economic justification for the local market’s existence and is achieved in AMMs via concentrated liquidity.

Remark on Continuity.

A direct consequence of Individual Rationality is that the total cost and revenue functions, and , must be Lipschitz continuous with constants and respectively, implying that for any two allocations and that differ only for prosumer :

2.3.4 Axioms on Qualitative Price Properties

The final set of axioms governs the dynamic behavior of the price functions, ensuring they respond to market conditions in an economically intuitive way.

Monotonicity (Positive Prices).

To ensure that trades are meaningful, selling energy must generate revenue and buying energy must incur a cost. This is guaranteed if the marginal prices are strictly positive.

Axiom 6 (Monotonicity).

A market mechanism is monotonic if its price functions are strictly positive:

| (9) |

for all .

Responsiveness.

A well-behaved market should naturally counteract imbalances through price signals. When aggregate supply increases, prices should strictly decrease to encourage demand, and when aggregate demand increases, prices should strictly increase to encourage supply. These conditions ensure that prosumers’ actions are strategic substitutes, preventing extreme coordination failures. This property also provides incentives for peak shaving.

Axiom 7 (Responsiveness).

A mechanism is responsive if its price functions’ partial derivatives satisfy:

| (10) |

Notice that Responsiveness combined with Individual Rationality (Eq. 8) imply that internal prices are strictly more favorable than the grid bounds whenever the community is in a net imbalance:

| (11) |

Remark on Concavity.

The Responsiveness axiom does not, by itself, imply the convexity or concavity of the prosumers’ total cost and revenue functions, However, the axiom is closely related to the geometric properties of the underlying market mechanism. For example, in the AMM constructions introduced later in Section 3 it is a direct consequence of implementing a strictly quasi-concave bonding curve.

Homogeneity.

For many theoretical models, it is useful to assume that prices depend only on the ratio of supply to demand, not on their absolute scale. A market with 100 kWh of supply and 50 kWh of demand should have the same price as one with 10 kWh of supply and 5 kWh of demand. This is the property of homogeneity of degree zero.

Axiom 8 (Homogeneity).

A mechanism is homogeneous if its price functions are homogeneous of degree zero, meaning for any scaling factor :

| (12) |

This implies the prices can be written as a function of the supply-to-demand ratio, .

The Homogeneity axiom plays a key role in Section 5 (Equilibrium Analysis) since scale invariance of prices implies proportional scaling of the total prosumer community welfare in the population size . This property is thus a necessary condition to approximate the stochastic finite-player game implemented by the AMM with its deterministic Mean-Field limit as .

3 AMM Construction and Applications

We now present a procedure to construct Automated Market Makers (AMMs) for energy trading that satisfies the design principles outlined in Section 2. While other market mechanisms exist, an AMM offers a streamlined solution for local energy markets. Prices are quoted automatically after energy transfers occur, making the market user-friendly as prosumers do not need to commit to a trade schedule ahead of time. Furthermore, AMMs mitigate the lack of liquidity common in small residential communities by pooling supply and demand, which can lead to tighter bid-ask spreads and faster matching than bilateral exchange mechanisms.

CFMM-style construction.

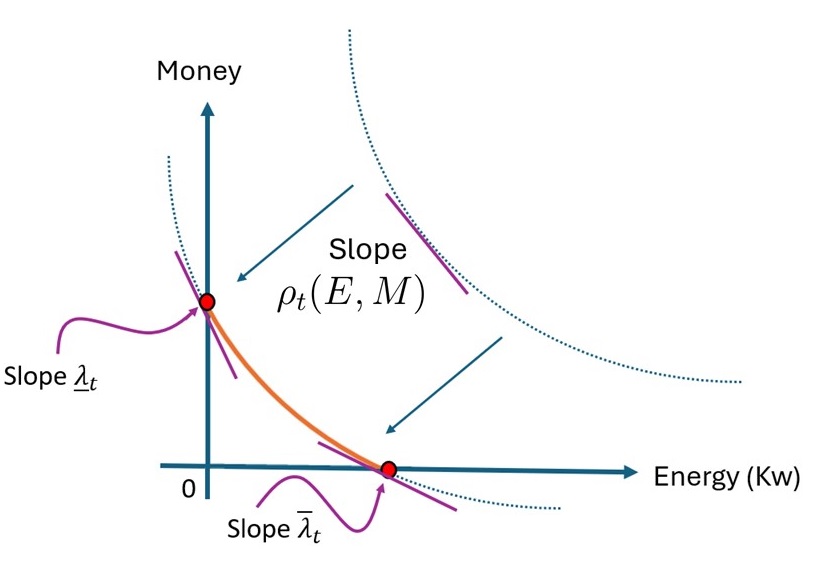

Our approach is to derive prices from a trading function, , which defines a potential over the money () and energy () in the AMM’s pool. This logic is akin to the Constant-Function Market Makers (CFMMs) popular in decentralized finance (e.g., AngerisChitra2020AFT; AngerisEtAl2022Handbook). The core of a CFMM is an invariant relationship, , where is constant for a trading session. Standard CFMM theory indicates that the marginal price of energy, , is the slope of the function’s level sets:

A canonical starting point is the constant-product function , used by the original Uniswap protocol, which yields a price of . While this specific function is not directly compatible with our axioms, its underlying principle forms the foundation for our adapted models.

Infrastructural and Operational Adaptations.

Adapting a financial CFMM to a physical commodity market requires two key modifications. First, an energy AMM must be embedded in physical infrastructure. Unlike purely digital assets, energy is delivered through a distribution grid, and prosumers’ contributions are mediated by trusted devices like smart meters that record net energy flows. The AMM must also remain consistent with the external market, importing deficits and exporting surpluses at the grid’s prices.

Second, the operational logic is fundamentally different. An energy market lacks the traditional liquidity providers (LPs) of DeFi, as prosumers themselves supply the energy that initializes the pool for each session. This inspires our mechanism guided by a dynamic bonding curve. Through a process of “re-anchoring,” the level set of the trading function is shifted at the start of each session based on the available energy and market conditions. The market clearing process then proceeds in two steps: (1) internal matching of units of energy along the newly anchored curve, and (2) external balancing of any residual with the grid.

Remark on Implementation.

While we often consider a blockchain setting where a smart contract can automate this process, the construction does not require it. The AMM can be constructed by any trusted operator able to measure aggregate flows and apply the pricing rules. These physical requirements—and the need to prevent sensor manipulation—are key challenges in the broader field of Decentralized Physical Infrastructure (DePIN) projects (milionis2025depin).

3.1 Energy Provision and Trade

We will now construct the AMM starting from the constant-product invariant and adjusting it progressively. As mentioned previously, the bonding curve is now dynamic and adjusted at each trading session. We let denote a family of trading functions parameterized by time and the value achieved at the target level set for time .

Concentrated Liquidity

To prevent arbitrage with the main grid’s feed-in tariff and retail price , the AMM must concentrate liquidity and quote a local price . Figure 2 shows how we shift the bonding curve to ensure the (internal) energy price cannot exceed or drop below these boundary rates.

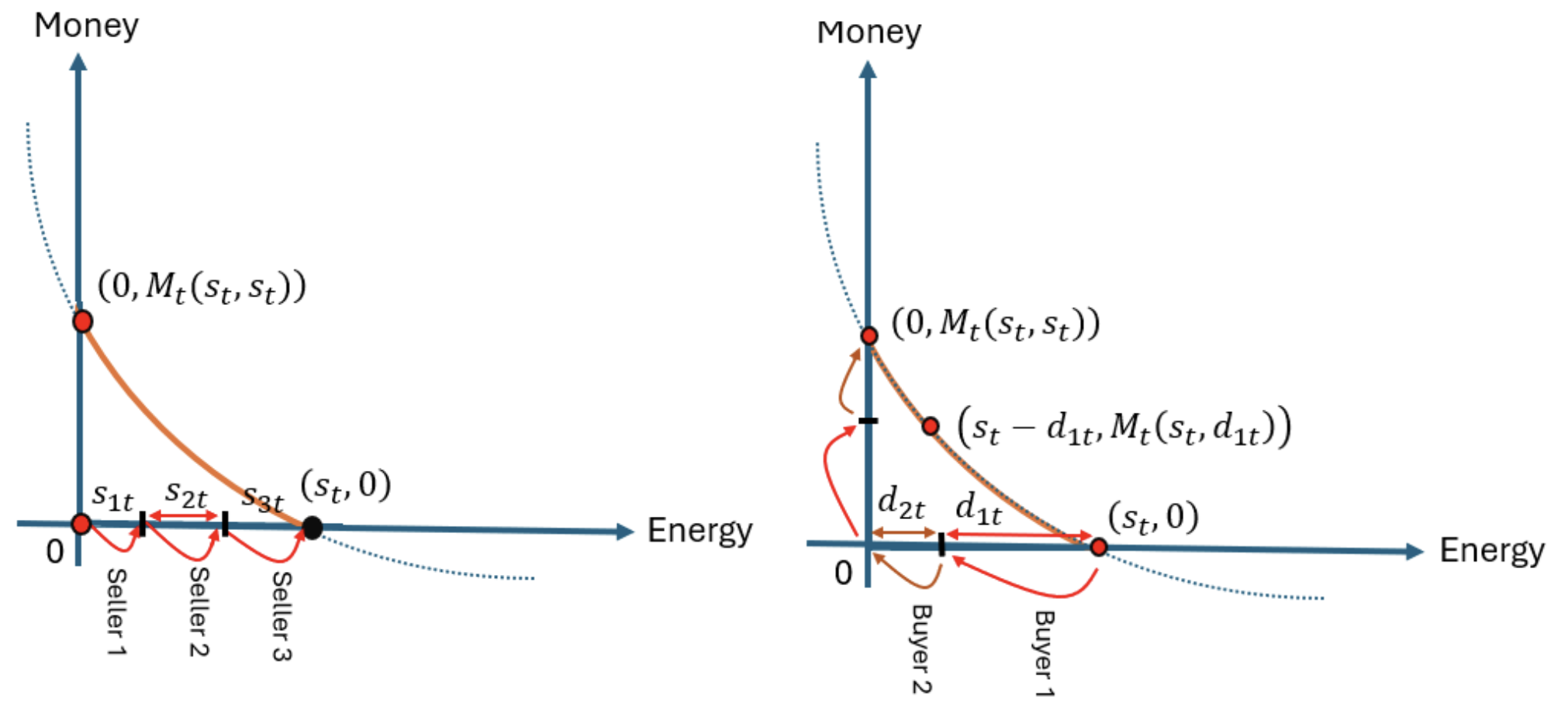

Batching and re-anchoring

At the beginning of the trading session , prosumers charge the pool with the total energy supplied . The pool starts with no monetary reserves, so its initial state is . We use this initial state along with the main grid’s prices to calculate a session-specific level set

thus fixing a bonding curve for the trading session:

The bonding curve determines the amount of money the pool collects as a function of the energy reserve (given the energy available at the start of the trading session). Once the session’s bonding curve is fixed, we can derive how much money will the AMM collect from prosumers:

| (13) |

this can be computed given the initial supply can be calculated from Eq. 13 setting . Figure 3 illustrates how capacity is deposited and depleted for the case of three sell orders and two buy orders, starting with an empty battery and no initial capital.

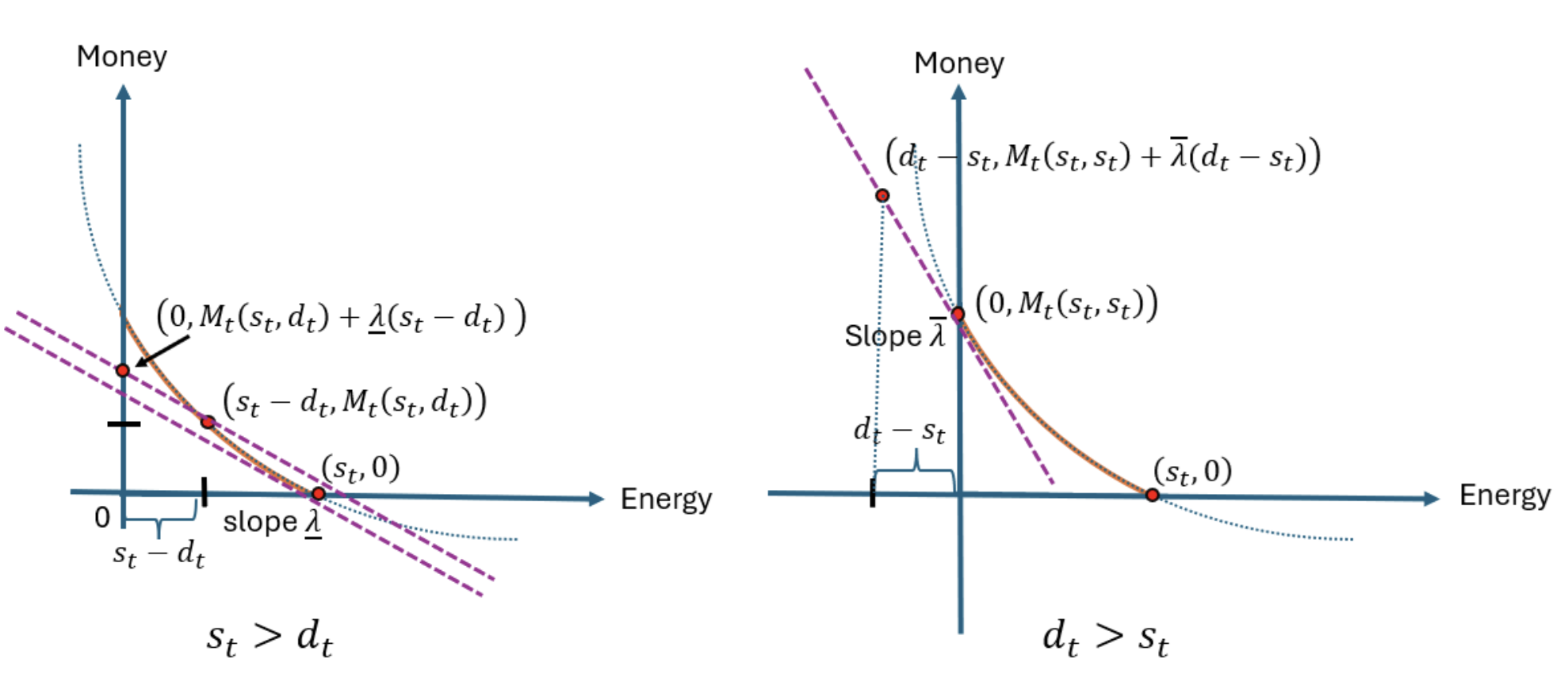

Imbalance Management

After the internal P2P exchange is complete, the AMM must settle any net energy imbalance by trading with the main grid. This process handles two distinct scenarios, both of which can be understood geometrically using tangent lines to the bonding curve, as illustrated in Figure 4.

When local supply exceeds demand, an energy surplus of remains after all internal demand has been met. At this point, the pool’s state is . This surplus is then sold to the main grid at the feed-in tariff . The additional revenue generated from this external sale is . Geometrically, this corresponds to the monetary value gained by moving along the tangent line from the final internal trading state, as shown in the left panel of Figure 4.

When local demand exceeds supply, the entire internal supply is consumed. The internal trading phase concludes with the pool in a state of full depletion: . To satisfy the remaining demand, the AMM must import the energy shortfall of from the main grid at the retail price . The additional cost incurred is . Geometrically, this cost is represented by the tangent line at the point of full depletion, as illustrated in the right panel of Figure 4.

Payments.

Finally, the AMM distributes costs and revenues among prosumers. The smart contract first categorizes prosumers as net buyers or net sellers based on their energy contribution. It then calculates the total costs for buyers and total revenues for sellers, distributing them proportionally based on each prosumer’s share of the total demand () or supply (), respectively. This distribution process depends on the net energy balance of the community, leading to three distinct cases:

Case I: (Balanced Market). The total cost and revenue are equal to the pool’s final monetary value, . The resulting per-unit prices are:

| (14) |

Case II: (Excess Supply). The total cost for buyers is determined by the internal trade, . The total revenue for sellers includes this amount plus the income from selling the surplus to the grid at price . The prices are:

| (15) |

Case III: (Excess Demand). The total revenue for sellers is determined by the full depletion of their supply, . The total cost for buyers includes this amount plus the cost of importing the deficit from the grid at price . The prices are:

| (16) |

While payments can be generalized to other repartition schemes, the proportional method is unique in ensuring the market is coalition-proof, as established in the previous section. Furthermore, if the AMM is not required to be strictly budget-balanced in every session, a dynamic fee can be introduced based on aggregate supply or demand.

3.2 Bonding Curves and Other Pricing Functions

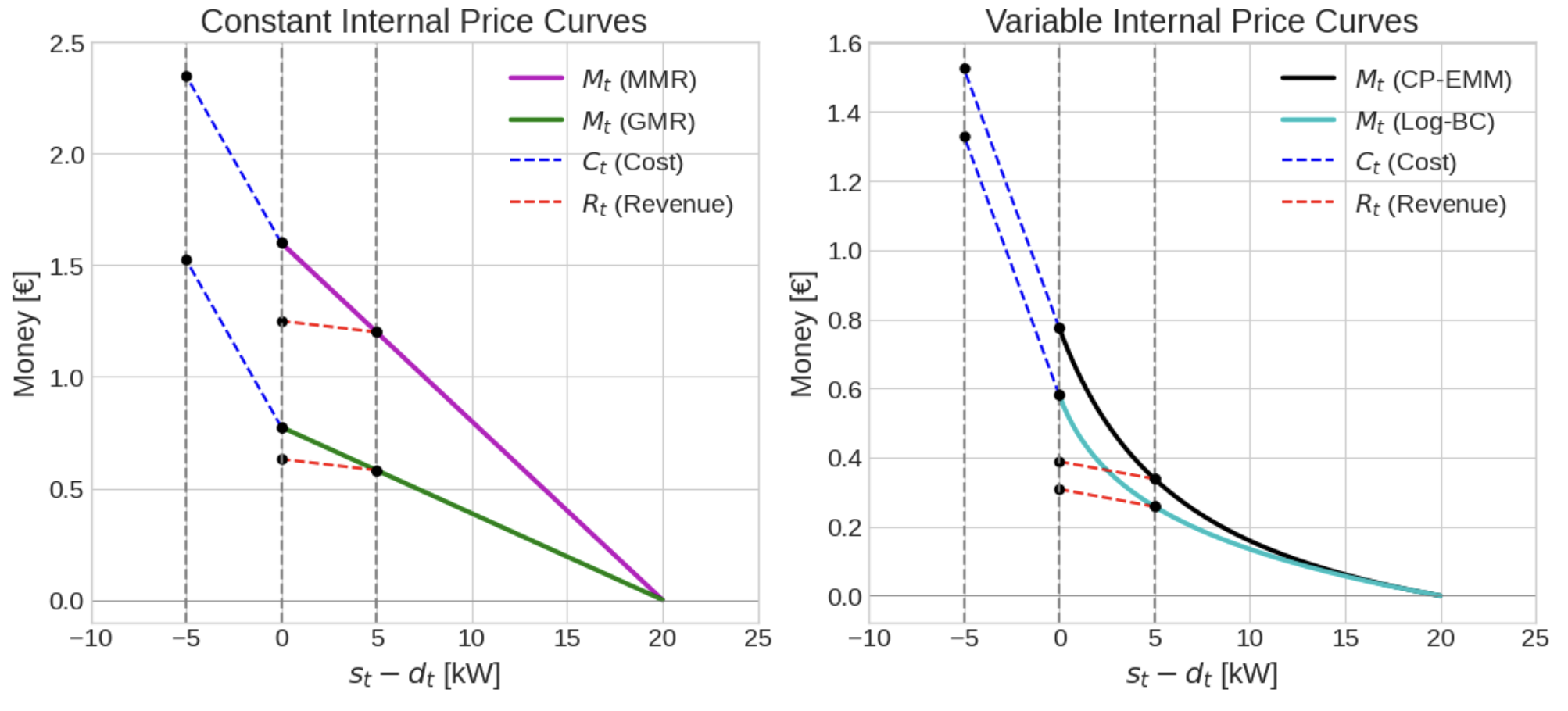

We now present three applications of the general construction from the previous section: linear, hyperbolic, and logarithmic bonding curves. Figure 5 compares the resulting buy () and sell () price curves for each model as a function of the supply-demand ratio .

Linear Bonding Curve (Constant Internal Price)

To implement a constant internal price for all internally matched energy, we use a linear trading function. The trading function and corresponding session invariant are:

| (17) |

Solving for the monetary reserve yields a simple, linear Pool Value Function:

This simple form gives rise to the following price functions after accounting for imbalances with the grid:

| (18) |

Hyperbolic Bonding Curve (CP-EMM)

This AMM is constructed from a hyperbolic trading function adapted from the standard constant-product formula. We first define a session-specific parameter 888The symbol will be redefined later on to represent collections of Lagrange multipliers and representative prosumer types.

The trading function and session invariant are then defined as:

| (19) |

This construction gives rise to pricing based on an adjusted geometric-market-rate. When the market is balanced (), it implements an over-provision penalty to incentivize an efficient match between local generation and consumption. The final price functions are:

| (20) | ||||

| (21) |

In CREF APPENDIX, we show that the hyperbolic trading function gives rise to pricing based on an adjusted geometric-market-rate (GMR): when the market is perfectly balanced (), the effective price for internally traded energy is the geometric mean of the grid prices, . When supply exceeds demand (), the AMM implements an over-provision penalty to incentivize an efficient match between local generation and consumption.

Logarithmic Bonding Curve

This model is derived from a price function that depends on the ratio of total supply to demand withdrawn.999The expression is derived from a price function of the form , where the constants are determined by the boundary conditions and . The marginal price for internal trades is:

Integrating this price function yields the Money Reserve function:

The final per-unit prices for sellers () and buyers () are determined by substituting this into the general payment rules:

| (22) | ||||

| (23) |

The behavior of this pricing rule is similar to the Hyperbolic one. While a corresponding trading function exists, its form is convoluted. It is therefore more intuitive in this case to define the mechanism directly via its bonding curve.

3.3 Other Pricing Rules from the Literature

We now review several common pricing mechanisms from the energy sharing literature and evaluate them against our axiomatic framework. We will see that some of them can be generated by the above trading functions.

Bill Sharing (BS).

An intuitive mechanism, Bill Sharing (BS) assigns the community’s total grid costs to buyers and total grid revenues to sellers XIONG2022300. The effective prices are and . While simple, this mechanism is structurally flawed. It violates Individual Rationality, as a prosumer is not guaranteed a better price than their outside option. For example, a seller receives zero revenue if the community has a net deficit.

Mid-Market Rate (MMR).

The Mid-Market Rate (MMR) rule sets the internal trading price to the average of the grid’s bid and ask prices muntasir2023developing. This mechanism is a special case of our Linear Bonding Curve model where the internal price is set to the arithmetic mean, . When imbalances occur, the cost or revenue is shared proportionally. The linear model is a general framework that also allows for other constant-price rules, such as the Geometric-Market-Rate (GMR), by setting .

Supply-Demand Ratio (SDR).

The SDR mechanism defines a responsive price that interpolates between the grid’s prices based on the supply-demand ratio XIONG2022300. The selling price is a decreasing function of market surplus, and the buying price is determined by the budget-balance condition:

Table 1 summarizes our axiomatic analysis. Both MMR and SDR are robust mechanisms that satisfy all axioms unconditionally. Our CP-EMM, representative of AMMs derived from strictly quasi-concave potentials (e.g., Log-EMM), also satisfies the axioms, with a single conditional exception for Monotonicity.

| Axiom | BS | MMR | SDR | CP-EMM |

|---|---|---|---|---|

| Anonymity | ✓ | ✓ | ✓ | ✓ |

| Coalition-Proof | ✓ | ✓ | ✓ | ✓ |

| No-Arbitrage | ✓ | ✓ | ✓ | ✓ |

| Budget-Balance | ✓ | ✓ | ✓ | ✓ |

| Individual Rationality | ✗ | ✓ | ✓ | ✓ |

| Monotonicity | ✗ | ✓ | ✓ | |

| Responsiveness | ✓ | ✓ | ✓ | |

| Homogeneity | ✓ | ✓ | ✓ | ✓ |

Axiom holds only if .

3.4 Market Design Guarantees

We now formalize the link between the properties of the underlying trading function and the axiomatic compliance of the resulting AMM.

Proposition 3 (Axiom Compliance via Geometric Construction).

Let an AMM be constructed using batch execution, proportional payment rules, and with its liquidity concentrated strictly within the grid’s prices, . Then, a market mechanism satisfies the axioms of Anonymity, Coalition-Proofness, Budget-Balance, Individual Rationality, No-Arbitrage, Monotonicity, Homogeneity, and Responsiveness if and only if the underlying trading function is (i) strictly increasing in E and M, (ii) homothetic, and (iii) quasi-concave.

Both directions of the equivalence arise from the interaction between the axioms of Section 2 and the geometry of the trading function.

In the forward direction, once batch execution and proportional payments are fixed, the mechanism is entirely determined by the trajectory traced along a single bonding curve during internal matching. Increasingness of the curve then guarantees that both reserves represent positively valued assets, ensuring strictly positive prices. Homotheticity guarantees that only the supply–demand ratio matters, yielding homogeneous pricing. Quasi-concavity ensures convex level sets and thus a price schedule that reacts monotonically to imbalances, producing the responsiveness required for peak shaving and strategic substitutability. Finally, concentrating liquidity strictly within the grid’s bid–ask interval ensures that all internal trades occur at strictly better prices than the outside option, enforcing individual rationality, preventing arbitrage with the main grid, and, together with proportional sharing, guaranteeing budget balance.

In the reverse direction, the axioms themselves impose strong shape restrictions that precisely recover the geometric structure of such a trading function. Anonymity eliminates dependence on order identity and forces the mechanism to aggregate trades into a single batch, while coalition-proofness requires that payments be linear in individual quantities, leaving proportional sharing as the unique feasible allocation rule. No-arbitrage, individual rationality, and budget-balance together imply the existence of a well-defined demand curve, describing how much energy the mechanism is willing to hold at a given price. Under the axioms, this curve must be flat outside the interval and strictly decreasing within it; as shown in the Myersonian framework of milionis2023myersonian, such curves are in one-to-one correspondence with strictly increasing, homothetic, quasi-concave trading potentials whose liquidity is concentrated inside the same interval. Thus the axioms force the mechanism to admit exactly the geometric representation used in our construction, completing the necessity direction.

Remark.

Since MMR and SDR also satisfy the axioms, we can simply derive the quasi-concave curves for them. It turns out that they are all a special type of a linear trading function. Specifically, they can all be represented as , where is for the arithmetic MMR, for the geometric MMR, and for the SDR pricing rules.

4 Prosumer Optimization

Having defined a market mechanism, we now model the behavior of individual prosumers operating within it. This section develops a dynamic optimization model for a single prosumer facing the AMM prices. We will use this formalism analyze a prosumer’s optimal decision (their best-response) given a belief on the price path. This forms the basis for the equilibrium characterization of Section 5. We also use the prosumer model to quantify the benefits of participating in the AMM compared to direct grid trading in Section 6.

4.1 Prosumer Model

We model the prosumer’s decision-making process using (epoch-based) discrete-time dynamic programming. Time unfolds over epochs , here representing days. Each epoch is divided into timesteps , each of duration hours (e.g., for 15-minute intervals, ). Table 2 summarizes the notation needed to define the prosumer’s optimization problem.

Prosumer Characteristics.

A prosumer is characterized by a set of static parameters and dynamic (state) variables. The static parameters include physical constraints—battery energy capacity (kWh), battery power limit (kW), and grid connection limit (kW)—and parameters governing energy generation and consumption profiles. Within each epoch , the prosumer observes their initial battery state (kWh) and forecasts for their net load profile over the timesteps. This profile consists of local generation (kW) and baseline consumption (kW). Additionally, the prosumer has a total flexible energy requirement (kWh) that must be met cumulatively over the epoch.

Decision Variables.

In each timestep of epoch , the prosumer chooses three power flows: consumption , battery charge/discharge (with indicating charging), and net grid trade . We decompose into non-negative power sold, , and power bought, .

Power Balance.

At each timestep , the instantaneous power flows must balance. Formally, local generation () plus power imported from the grid () must equal the power consumed locally (), power stored in the battery (, positive if charging), and power exported to the grid (): (kW).

Consumption Constraints.

Power consumption must always cover the essential, non-shiftable baseline load, (kW). Additionally, the total energy consumed above this baseline over the entire epoch must exactly meet the flexible load target: .101010It is equivalent to have since the constraint will bind at the optimum. This cumulative constraint models deferrable energy needs, such as electric vehicle charging or running specific appliances, that must be completed within the epoch but whose timing can be optimized.111111For notational simplicity we treat the timestep as the unit of time in the constraints. This makes energy quantities (kWh) numerically equivalent to average power (kW). To ensure the objective function is correctly calculated in Euros, we multiply the price parameters by the timestep duration . This converts hourly tariffs (€/kWh) into effective prices per unit of power (€/kW).

Battery Constraints.

For prosumers equipped with storage (), the battery’s state of charge (SoC) (kWh) at the end of timestep evolves according to the battery dynamics , where is the charging () or discharging () power and is the initial state for the epoch. The SoC is constrained by the physical battery capacity limits, (kWh). Furthermore, the rate of charge or discharge is limited by the battery power limits, (kW).

Grid Connection Limits.

Power exchanged with the grid is constrained by the connection capacity . Both selling and buying are non-negative power flows, individually bounded by this limit: (kW) and (kW). These bounds implicitly enforce the net trade constraint .

Inter-Epoch Link.

The prosumer value function is connected across consecutive epochs through the battery state. The terminal state of charge at the end of epoch , , becomes the initial state of charge for the subsequent epoch : .

Objective Function.

The prosumer’s objective is to maximize the total expected discounted (net) profit over an infinite horizon. This dynamic optimization problem can be expressed recursively using the Bellman equation. For a single epoch , given the initial battery state , the value function represents the maximum achievable expected future profit:121212To be fully rigorous, the prosumer’s payoff in a given epoch is quasi-linear and defined as , where is the (convex) characteristic function of the feasible set: if the consumption schedule satisfies the load requirements, i.e., for all and , and otherwise.

| (24) |

Here, the maximization is over the sequences of decisions within epoch . The term represents the total net profit (€) accumulated within the current epoch , where is the net payment received (positive for revenue, negative for cost) for the power allocation at timestep . The term is the discounted continuation value, starting from the next epoch’s initial state , with being the discount factor between epochs.

4.2 The Best-Response Program

We now analyze the prosumer’s problem of optimizing profits by best responding to a (perfectly) forecasted path of prices and (€/kW):

| (25) |

subject to the following constraints for :

-

•

Power Balance: (Lagrange multiplier: )

-

•

Baseline Consumption:

-

•

Flexible Load Target:

-

•

Battery Dynamics:

-

•

Battery State Limits:

-

•

Battery Power Limits:

-

•

Grid Transmission Limits: ,

Appendix B shows how to express Eq. 25 and its constraints in a more compact matrix form. Since the objective function is concave and the feasible set defined by the linear constraints is convex, this is a convex optimization problem.

Remark.

The value function in Eq. 25 can account for intra-epoch discounting by scaling prices by .

Trading Behavior.

The optimal action plan of the prosumer follows from the KKT and stationary condition of the Lagrangian associated to the above optimization problem. In particular, the trading strategy can be understood looking at the dual space of the optimization problem, in particular by analyzing how the Lagrange multiplier of the Power Balance constraint, relates to the market prices .

Intuitively, the multiplier represents the shadow price of power, or the price that the prosumer would attribute to its power budget. This leads the prosumer to sell power in periods where , to buy power in periods where , and to not trade in the intermediate range, . In the previous relationships for active trading, strict inequalities denote binding transmission limits (), whereas equalities imply internal constraints (e.g., consumption constraints, battery capacity) determine the volume by equating marginal value to price. Formally,

| (26) |

4.3 Computation via Model Predictive Control

Directly solving the infinite-horizon problem (24) is computationally intractable. We therefore approximate the solution using Model Predictive Control (MPC) on rolling-horizon (prat2024finitehorizon). In each epoch , the prosumer solves a deterministic Linear Program (LP) over a finite lookahead window of epochs (), based on available forecasts.

Let denote the stacked vector of decision variables over these epochs. The optimization problem is given by:

| (27) |

where represents the feasible set over epochs starting from state , and is the vector of forecasted effective prices. After doing so, only the optimal plan for the first epoch, , is implemented.

The lookahead horizon is adaptively increased until the terminal state stabilizes, ensuring the finite window approximation is sufficiently precise. The resulting terminal state then serves as the initial state for the subsequent epoch’s optimization.

Algorithm 1 shows the full implementation of this procedure.

5 Equilibrium Analysis

In the previous section, we analyzed a single prosumer’s optimization problem by assuming perfect foresight of the price path. We now relax this assumption and study the strategic interactions among all prosumers in a multi-agent setting.

As prosumers’ decision-making unfolds over an infinite horizon, the appropriate framework to study their interaction is a dynamic stochastic game. We first characterize the Bayes-Nash Equilibrium (BNE) for a single epoch, taking continuation values as given. We then concatenate these stage games to analyze the resulting Markov Perfect Equilibrium (MPE) of the stochastic game.

5.1 Equilibrium Concept

Strategic Environment and Prosumer Beliefs.

At the beginning of each epoch , the stage game is determined a public state (e.g., meteorological conditions) and by each prosumer ’s private state, consisting of their battery level and their epoch-specific type .

The public state captures common sources of randomness as the joint distribution of types is conditional on it, . Each prosumer observes their own type but only holds probabilistic beliefs about the types of others.

We focus on mixed-strategy equilibria. A prosumer with type has a feasible action set . Because prosumers are atomistic, their individual optimization problem is a linear program (see Section 4.2). Thus, any best response to an expected price path is an extreme point of this set, . A mixed strategy is therefore a measurable mapping which assigns to each type a probability distribution over the extreme points available to that type. Therefore, a mixed-strategy profile for the -prosumer game is given by the following mapping:131313Since depends only on a prosumer’s type and not on their index, the strategy space is type-symmetric.

Given a mixed-strategy profile, and conditional on a realized type profile , a pure action profile is played with probability

Under the common prior assumption, all prosumers hold the same belief about the expected price paths, which can be computed by taking expectations over types and induced actions:

| (28) | ||||

| (29) |

where is the aggregate supply-to-demand ratio resulting from the action profile .

Equilibrium Definitions.

A strategy profile is a BNE if each prosumer’s strategy is a best response to the strategies of all others, . Since prices are determined by the aggregate behavior induced by , equilibrium solves a fixed-point problem in which beliefs about prices coincide with the expected prices arising in equilibrium. Let denote these equilibrium expected prices.141414For notational convenience, we use variations of the symbol to define AMM prices in different contexts: in Section 3, denotes the AMM internal marginal price, while in the current section, denotes the rational expectation of “final” AMM prices, accounting for the pro-rata repartition of the trading surplus or deficit. Given , the payoff from a pure (extreme-point) action plan for prosumer is

Since we consider a large population of prosumer, we model each prosumer as atomistic and hence price-taker: a unilateral deviation of a single prosumer from the strategy profile does not affect the net marginal prices quoted by the AMM. Formally,

Assumption 1 (Atomicity).

For any prosumer and type , a deviation form to leaves the prices quoted by the AMM unchanged:

We can now define BNE in this context as follows:151515An equivalence definition of incentive-compatibility can be stated requiring indifference among pure strategies in the mixing support: for each type and any with and , we have .

Definition 2 (Mean-Field BNE).

A pair is a Mean-Field Bayes-Nash Equilibrium of the stage game if:

-

(a)

Incentive-Compatibility: For every prosumer and type , the mixed strategy maximizes the prosumer’s expected profit given the equilibrium prices :

(30) - (b)

-

(c)

Atomicity: The prices quoted by the AMM and are not affected by a deviation of single prosumer from strategy to (1).

Dynamic Extension: Markov Perfect Equilibrium.

The definition of BNE describes equilibrium interaction for a single epoch. However, prosumers interact with the AMM repeatedly over epochs to maximize discounted future profits. The previous Equilibrium definition 2 can thus be extended to the dynamic setting by requiring strategies to be Markovian in payoff-relevant state variables, such as the initial battery level and the public signal. Letting denote prosumer ’s value function, we now define:

Definition 3 (MPE).

A triple is a Markov Perfect Equilibrium if, for every prosumer , the value function satisfies

and the maximizer is the equilibrium strategy . The continuation value is stationary under the equilibrium strategy profile.

5.2 Characterization of prosumer equilibria

So far, we have analyzed how prosumers would best-respond to a market making mechanism. Given their response, the question still remains whether the resulting power flows and prices maximize some notion of welfare.

To this end, we now show a powerful equivalence based on the Axioms of Section 2. Under those axioms indeed the BNE of the prosumers’ stage game leads to a (randomized) allocation of power flows that is the same as the one a Social Planner would choose to maximize the expected trade profits of the prosumer community with the power grid.

Proposition 4 (Welfare Equivalence).

A strategy profile is a BNE of the stage-game if and only if it maximizes the expected value of trade profits with the grid:

| (31) |

This result is powerful because it establishes that, in this context, the First and Second Welfare Theorems hold (mascolell1995) and the AMM essentially implements a competitive equilibrium among prosumers: The AMM serves as a “zero-sum redistribution engine” that complements the main electrical market to coordinate prosumers into solving collectively a (soft) market clearing problem.

To better see this, we can express the objective of the Planner (and hence of the prosumer collective) in terms of netput vectors:161616The transformation follows using the properties of the absolute value operator: , .

| (32) |

where , and , are vectors of mid-prices and mid-spreads. with respective elements , and .

According to Eq. 32, the Planner achieves optimality by matching internal demand with supply to avoid the bid-ask spread (with penalty coming from the -norm), while shifting any residual grid trades to periods where the mid-price is favorable. Since the community’s total net energy balance over an epoch is mostly fixed, the planner objective is usually dominated by the minimization of the weighted -minimization of a weighted netput vector:

The sufficiency part of Proposition 4 () can be established solely based on Exact Budget Balance (Axiom 4) and Atomocity (Assumption 1). In particular, from these two assumptions it emerges that the AMM creates a Potential Game (monderer1996) where the potential function is exactly the community welfare.

Proposition 5 (Potential Game).

The prosumer game is a potential game with potential function equal to the expected global welfare, .

This is intuitive since Budget Balance establishes that internal transfers net-out and Atomicity ensures that a single prosumer’s deviation has a negligible effect on the prices faced by others, effectively eliminating price externalities. This potential game structure guarantees no efficiency loss due to decentralization (i.e., a Price of Anarchy of 1).

The necessity direction of Proposition 4 () is slightly trickier to prove and relies on two additional axioms on top of those needed for proving sufficcy, namely Individual Rationality (Axiom 5) and Responsiveness (Axiom 7). These two axioms ensure that whenever internal clearing is not optimized, there exists a profitable arbitrage opportunity on AMM prices that prosumers can be exploit to increase profits.

It is important to notice that Proposition 4 holds regardless of which internal price functions or trading function is used—as long as it is axiom-compliant and prosumers behave atomistically. In this sense, Proposition 4 provides us with a benchmark result. One way to pin down a specific curve or pricing mechanism would be by attributing priorities among prosumers, which would relax the linearity assumption on welfare. Doing so could be done for example by assigning different utility functions in accordance to assigned priorities (for example, the hospital would have higher priority than residential households.) We will discuss more this aspect in the conclusion (Section 7).

Besides of theoretical importance, Proposition 4 has also practical implication for computing equilibria. Thanks to it we can reduce a complex equilibrium problem to solving a Planner’s problem and then decentralizing the solution satisfying individual feasibility (see Section 5.4).

Dynamic Extension

The stage-game analysis above focuses on a single epoch. When we consider how strategies evolve over time, we extend these efficiency results to the dynamic setting.

Proposition 6 (Markov Perfect Equilibria).

The dynamic game exhibits a multiplicity of mixed-strategy MPEs. However, every equilibrium strategy profile implements the same unique aggregate outcome that maximizes the expected discounted profit of the local grid:

| (33) |

This proposition confirms that the static welfare equivalence extends to the dynamic case: any MPE maximizes the long-term discounted net trade profits.

While the aggregate value and the optimal path of grid trades are unique, the specific strategy profile is not. Because (in every interesting application) the number of degrees of freedom in the choice of the mixing weights vastly exceeds the number of aggregate constraints, there exists a continuum of mixed strategies that all map to the exact same optimal aggregate outcome.

5.3 Efficiency and Mechanism Comparison

We benchmark the proposed AMM by comparing its welfare properties against the theoretical first-best outcome achievable by an omniscient social planner. While Proposition 4 establishes that the AMM maximizes the expected welfare of the community, this is an ex-ante notion of efficiency, as prosumers optimize their strategies based on probabilistic beliefs about others. An ideal planner who observes the realization of all types before allocating resources could achieve a higher ex-post welfare by making the power flows contingent on the realization of the private state (as well as the the public state). The relationship is captured by the following inequality:

| (34) |

where denotes the realized global welfare for a specific type profile. The gap between these two values can be interpreted as the “price” of higher privacy and decentralization.

The Vickrey-Clarke-Groves (VCG) Benchmark.

The canonical mechanism for implementing the ex-post social optimum () is the Vickrey-Clarke-Groves (VCG) mechanism (vickrey1961; clarke1971; groves1973). In this direct-revelation setup, each agent reports their type . The mechanism then implements the socially optimal allocation and charges each agent a payment equal to the externality they impose on others:

VCG is strategy-proof (truthful reporting is a dominant strategy) and achieves the unconstrained ex-post maximum welfare. However, its theoretical optimality is hardly practical for local energy communities.

First, VCG is not budget-balanced (it generally runs a deficit), implying that the community would require an external subsidy to operate. Also, it requires prosumers to reveal their full private types (e.g., battery states and consumption/generation profiles) to the Planner before choosing their power flows. Besides raising possibly privacy concerns, it can be particularly inconvenient for residential prosumers having to commit ahead of time to an energy schedule.

In contrast, the AMM described in this paper is an indirect mechanism that can better deal with these issues. It sacrifices strategy-proofness and ex-post optimality to guarantee the two properties that VCG lacks: By satisfying Budget Balance (Axiom 4), the AMM ensures the market is self-sustaining without external subsidies. Furthermore, pricing is purely based on traded quantities rather than the full prosumer type, and payments are determined after recording the power flows.

For these reasons, the AMM is a practical alternative to a full VCG implementation: It is an optimal mechanism within the class of budget-balanced, anonymous, and responsive mechanisms, and achieves the maximum possible welfare without subsidies and with lower informational requirements on the prosumers.

5.4 Equilibrium Computation

Computing the Markov Perfect Equilibrium (MPE) for a dynamic game with a continuum of heterogeneous agents can be challenging. However, the Welfare Equivalence result (Proposition 4) provides a crucial simplification: instead of solving for the fixed point of coupled Bellman equations, we can simply solve a single concave Planner’s Problem and then decentralize the allocation. We leverage this insight to construct the numerical procedure applied in Section 6 to data from metropolitan Paris.

The algorithm that we develop hereafter to approximate the infinite-horizon equilibrium proceeds epoch by epoch. In each epoch , given the current empirical distribution of battery states , we compute an approximate BNE over a lookahead horizon of epochs. This computation follows a four–stage procedure:

(i) the continuous population is quantized into state-dependent representative types,

(ii) the dimensionality of the action space is reduced by restricting choices to a subset of salient strategies for these types based on their current state,

(iii) a (potentially regularized) planner problem is solved to find the equilibrium strategies maximizing the mean-field welfare, and

(iv) the coordinated allocation is decentralized back to individuals via Euclidean projection.

While the equilibrium calculation considers the full -epoch horizon to incorporate forward-looking behavior, only the actions corresponding to the first epoch () are implemented. The resulting distribution of terminal battery states then determines the initial state distribution for the next epoch. Algorithm 2 summarizes this rolling-horizon procedure that we will now outline in detail.

Population Approximation.

To begin with, the equilibrium solver algorithm needs a type population as input. We represent such population by approximating the type space with a mixed histogram. This structure enables the joint modeling of discrete categories (e.g., simple consumers and solar prosumers) and continuous attributes (e.g., capacities, generation profiles). For each category , we partition the attribute space into cells with associated weights , inducing a collection of uniform classes:

We then generate a simulated population of agents by Monte-Carlo sampling from this structure:

In each epoch , an agent’s full state consists of their static type and their initial state of charge . To maintain tractability as battery levels evolve, we group the agents into state-dependent representative types corresponding to the static bins. The representative for bin in epoch is defined as the tuple , where is the midpoint (centroid) of cell and is the current average state of charge of all agents belonging to that bin.

Dimensionality Reduction of the Action Space.

The feasible action set is depends on the agent’s initial state of charge. Therefore, to ensure the BNE approximation remains accurate as the population state distribution evolves, the strategy banks that form the mixed-strategy support are recomputed in every epoch .

For each state-dependent representative type , we generate a new strategy bank for a lookahead window of epochs: . We take the support of the equilibrium mixed strategy to be a the strategy bank populated by solving the -epoch best-response LP using Algorithm 1 (with parameters and ) under a large number of diverse price profiles. The resulting equilibrium strategy for type is a distribution over this bank, , and the support for the overall mixed strategy profile is the Cartesian product of these dynamic banks, .

Planner Problem for Ex-Ante Welfare Maximization.

With the strategy banks populated, we can now determine how agents should mix among these candidate plans. We accomplish this by solving for the equilibrium strategy profile that maximizes the ex-ante expected community welfare.

To handle the non-differentiable absolute value in the welfare function (Equation 31), we introduce auxiliary variables for the aggregate export and import . The problem of the Equilibrium Solver can thus be defined as maximizing the linear welfare term with an optional Tikhonov regularization term:171717The regularization term increases the smoothness of the resulting equilibrium aggregate profiles.

Definition 4 (Equilibrium Solver).

The Equilibrium Solver is given by the following Quadratic Programming problem:

| (35) |

subject to:

| (36) |

| (Net trade decomposition) | ||||

| (Non-negativity) | ||||

| (Probability simplex) | ||||

| (Non-negativity) |

In the objective function of the Solver, is a scalar and is the temporal difference matrix.181818Diff has entries and . The choice variable for type is the probability vector . The constraints enforce consistency between the net trade and the auxiliary variables and restrict the vector so that probabilities are correctly defined over the relevant simplices ().

The connection between the decision variables and the action aggregates is given by the aggregate netput vector . We will now see how to compute it: Let be the number of strategies in the bank for representative type . Each plan in the bank induces specific supply and demand trajectories, denoted and . We construct the supply matrix and the demand matrix by stacking these trajectories as columns:

The resulting aggregate netput in Eq. 36 is thus the sum of these expected power (net) injections weighted by across all bins.

Decentralization and Feasibility Projection.

Finally, to implement the equilibrium, we decentralize the aggregate solution via Monte-Carlo assignment.

Specifically, each agent (belonging to bin ) independently samples a candidate plan from the bank. Then, since the agent’s realized state generally deviates from the bin archetype, we enforce feasibility by mapping the candidate to the closest feasible action via Euclidean projection: . This step restores feasibility while preserving approximate incentive compatibility.

The procedure concludes by executing the first epoch of , determining the initial state distribution for the subsequent loop.

5.5 Theoretical Guarantees for the Equilibrium Solver

The careful reader will have noticed that the Solver in Eq. 35 maximizes the welfare at the average trade—evaluating welfare as if the entire community were composed of identical “average” agents, each executing the same action—whereas the true objective (Eq. 31) is to maximize the expected total welfare of the community. This is a crucial simplification since it allows us to optimize a deterministic proxy rather than integrating over the intractable -dimensional joint distribution of types , which would be required to compute the exact expectation of the piecewise-linear welfare function. We now explain why this approach is valid.

First, thanks to the Homogeneity Axiom (8), the welfare function scales linearly in aggregate netput (i.e., it is 1-homogeneous). This allows us to relate total welfare and welfare at the average trade: Let be the total realized net trade and be the realized average net trade per agent. The total welfare is exactly times the welfare of the average:

where is simply the standard welfare function defined in Eq. 32 applied to unit-normalized quantities. Because is a positive constant, maximizing the expected total welfare is equivalent to maximizing the expected average welfare:

Nevertheless we did not eliminate yet the integration problem. Since is concave and the realized average is a random variable, and by Jensen’s Inequality, . The solver optimizes the right-hand side (the certainty-equivalent welfare of the expectation), which overestimates the welfare function.

However, this “Jensen gap” is driven by the variance of the realized average, . As the population size , the Strong Law of Large Numbers (SLLN) ensures that the realized average converges almost surely to the sample mean . Consequently, the variance vanishes, and by continuity and boundedness of the welfare function, the welfare of the stochastic average converges to the welfare of the deterministic mean field approximation.

Proposition 7 (Convergence to the Mean-Field Welfare Limit).

Let be the continuous welfare function and let individual actions be conditionally i.i.d. and bounded given . Let be the realized average and be the theoretical mean field. Then, the true expected welfare converges to the welfare of the mean field:

Approximation Error and -Incentive Compatibility.

Finally, we note that quantizing the continuous type space into discrete bins and ensuring feasibility by projection can result in a strictly positive regret relative to the true optimal strategy:

However, as the prosumer’s individual optimization problem (Eq. 25) is a linear program, their optimal value functions and the feasible set boundaries are Lipschitz continuous with respect to the elements of (e.g., battery capacity, grid limits). Consequently, the regret is bounded by the distance between the agent’s true type and the bin centroid.

As the histogram mesh becomes finer, this error vanishes linearly, ensuring that the mechanism is asymptotically Incentive Compatible.191919Notice that the regret bound is stronger than payoff continuity as the latter only implies while the regret bound ensures the specific mixed strategy (optimized for ) yields an expected payoff close to the true optimum when played by type .

Proposition 8 (Vanishing Regret).

Let be the maximum diameter of the type bins. Under the assumption that the feasible set correspondence is Lipschitz continuous, the expected regret for any agent is bounded linearly by the quantization error:

where is a problem-dependent Lipschitz constant. Thus, as the population approximation becomes exact (), the regret vanishes and the equilibrium becomes exact.

6 Quantitative Experiments

Our goal in this section is to build simulations to quantify gains with our approach. We explore two scales with this model, both advantages in the prosumer and in the community level.

6.1 Data description and source

Two datasets are used and explored in this quantitative simulations. The first dataset contains historical weather information from Paris during the year of 2023. Paris was chosen as the base of our simulation due to its economical importance and the access to information such as energy consumption, demographic, solar irradiance and eolic power potential hakkarainen2015role. The contrast between different regions in France for energy potential is shown in Figure 7(a) solargris, indicating differences in solar energy production potential in relevant regions, while Figure 7(b) shows the average wind speed at 100 meters which is the basis for eolic energy.

Historical data is taken for open-meteo weather weather2023, containing information which impacts energy production, such as solar irradiance, cloud cover percentage, and wind speed. These values are measured and recorded hourly. Irradiance is measured as the total radiation received in the preceding hour per meter squared, , taking into consideration Earth’s tilt for the non-normal incidence. Cloud cover is defined as the fraction of the sky that is covered in clouds, affecting the performance and efficiency of solar panels. Wind speed is measured in at an altitude of 100 meters from the ground.