Distributionally Robust Dynamic Structural Estimation: Serial Dependence and Sensitivity Analysis††thanks: I would like to thank Lars Nesheim, Dennis Kristensen, and Aureo de Paula for their continuous guidance and support. I am grateful to Victor Aguirregabiria, Dante Amengual, Debopam Bhattacharya, Stephane Bonhomme, Cuicui Chen, Tim Christensen, Kevin Dano, Ben Deaner, Ivan Fernandez-Val, Hugo Freeman, Alfred Galichon, Raffaella Giacomini, Gautam Gowrisankaran, Joao Granja, Jiaying Gu, Sukjin Han, Stefan Hubner, Hiroaki Kaido, Hiroyuki Kasahara, Yuichi Kitamura, Adam Lee, Arthur Lewbel, Lorenzo Magnolfi, Chuck Manski, Matt Masten, Robert McCann, Bob Miller, Marcel Nutz, Ariel Pakes, Silvana Pesenti, Lei Qiao, Eduardo Souza-Rodrigues, Pietro Emilio Spini, Jörg Stoye, Elie Tamer, Xun Tang, Weining Wang, Leonard Wong, Andrei Zeleneev for helpful discussions and comments. I also thank seminar participants at UCL and University of Toronto, and conference audiences at 2025 Bristol Econometric study group, 2025 Midwest Econometrics Group Conference, and IAAE 2025.

Distributional assumptions that discipline serially correlated latent variables play a central role in dynamic structural models. We propose a framework to quantify the sensitivity of scalar parameters of interest (e.g., welfare, elasticity) to such distributional assumptions. We derive bounds on the scalar parameter by perturbing a reference distribution, while imposing a stationarity condition for time-homogeneous models or a Markovian condition for time-inhomogeneous models. The bounds are the solutions to optimization problems, for which we derive a computationally tractable dual formulation. We establish consistency, convergence rate, and asymptotic distribution for the estimator of the bounds. We demonstrate the approach with two applications: an infinite-horizon dynamic demand model for new cars in the United Kingdom, Germany, and France, and a finite-horizon dynamic labor supply model for taxi drivers in New York City. In the car application, perturbed price elasticities deviate by at most 15.24% from the reference elasticities, while perturbed estimates of consumer surplus from an additional $3,000 electric vehicle subsidy vary by up to 102.75%. In the labor supply application, the perturbed Frisch labor supply elasticity deviates by at most 76.83% for weekday drivers and 42.84% for weekend drivers.

Keywords: Serial dependence, Sensitivity analysis, Dynamic structural models, Robustness, Misspecification

JEL Codes: C14, C18, C51, C61

1 Introduction

Dynamic structural models are useful tools for counterfactual policy analysis in various fields of economics. The correlation structure of latent variables is a key feature of these models, as it captures the persistence of unobserved factors that affect agents’ decisions over time. Examples of potentially serially correlated latent variables include: product characteristics in demand estimation (Nair, (2007); Schiraldi, (2011); Gowrisankaran and Rysman, (2012)), search costs in consumer search (Koulayev, (2014)), firm productivity in trade (Piveteau, (2021)), patent profitability in optimal stopping (Pakes, (1984)), quality in technology adoption (De Groote and Verboven, (2019)), health shocks in insurance (Fang and Kung, (2021)), and beliefs about ability in labor economics (Miller, (1984); Arcidiacono et al., (2025)).

Distributional assumptions about the serial dependence of latent variables play a central role in the estimation and counterfactual analysis of dynamic structural models. These assumptions capture agents’ uncertainty about the future, such as a consumer’s uncertainty about future product characteristics in demand estimation. The misspecification of these assumptions can lead to biased estimates of future continuation value, which in turn bias counterfactual predictions (e.g., welfare and elasticity). However, the direction and magnitude of this bias are unclear, because the models are dynamic and nonlinear. This raises the need for sensitivity analysis of empirical results to these distributional assumptions.

In this paper, we propose a framework to quantify this sensitivity by perturbing a reference distribution to compute bounds on a scalar parameter of interest. The scalar parameter (e.g., welfare and elasticity) is a function of model primitives, such as model parameters, the distribution of latent variables, and the value function in dynamic structural models. In our proposed framework, the bounds on this scalar parameter are the solutions to constrained optimization problems whose feasible region (identified set) is defined by moment conditions for estimation, structural constraints (e.g., the Bellman equation), and the perturbation set around the reference distribution. The distribution that attains the bound is called the worst-case distribution.

A central challenge is to define the perturbation set in a way that simplifies computation while maintaining key structural features of the distribution of latent variables. For time-homogeneous models, the structural feature is the stationarity condition, i.e., the perturbed transition distribution must be stationary. For finite-horizon, time-inhomogeneous models, the perturbed trajectory of latent variables must be Markovian. In addition, the terminal distribution is fixed becuase it can be nonparametrically point identified (Lewbel, (2000); Matzkin, (2007)). Because the stationarity and Markov conditions are functional constraints imposed directly on the distribution being optimized, they are computationally difficult to impose. We contribute to the sensitivity analysis literature (e.g., Christensen and Connault, (2023)) by providing a computationally tractable framework to deal with these constraints.

There are further practical challenges. First, the properties (e.g., closed-form, smoothness) of the worst-case distribution are typically unclear, complicating the choice of approximation methods. Second, the expectations that define the scalar parameter, the model-implied moments, and the structural constraints are all calculated with respect to the perturbed distribution. Because this distribution is itself an optimization variable that changes during the optimization, the numerical integration can be difficult to implement. Third, the value function in dynamic structural models is infinite-dimensional due to the serial dependence of latent variables, which complicates the optimization problem further.

To address these challenges, we define the perturbation set as a Kullback-Leibler (KL) divergence ball around the reference distribution. The KL radius controls the size of the perturbation set. Then, we employ the Optimal Transport (OT) framework to impose constraints on the distribution of latent variables. These constraints, combined with the KL divergence constraint, form a computationally tractable entropic optimal transport (EOT) problem. For the time-homogeneous case, the reference distribution is a joint distribution of current and future latent variables. The stationarity condition requires that the marginal distributions of current and future latent variables of the perturbed joint distribution are the same, which can be imposed using OT. This marginal constraint, when combined with the KL divergence penalty from the problem’s Lagrangian, forms an EOT problem. For the time-inhomogeneous case, the perturbed trajectory must be Markovian, and the terminal distribution is fixed. We show how to formulate this as an EOT problem.

The EOT problem can be solved using its dual formulation, which has three key advantages over the primal formulation. First, it provides a closed-form expression for the worst-case distribution and characterizes its smoothness. During our proposed optimization algorithm, this closed-form expression is used to update the value function in dynamic structural models. Second, the Sinkhorn algorithm (Sinkhorn and Knopp, (1967); Cuturi, (2013)) allows us to solve the EOT problem and compute the worst-case distribution efficiently. Finally, because the expectations in the dual problem are taken with respect to the reference distribution, an appropriate numerical integration method can be chosen in advance.

Then, we propose three complementary sensitivity measures to interpret the results. First, the global sensitivity approach computes the largest deviation from the reference value. It progressively increases the KL radius until the bounds flatten. We show that it provides a tractable approximation to the nonparametric bounds on the scalar parameter when the KL divergence constraint is removed. Second, the local sensitivity approach analyzes the effect of small perturbations. It computes the right derivatives of the bounds with respect to the KL radius at zero, which is our local sensitivity measure. Finally, the robustness metric approach, inspired by Spini, (2024), computes the smallest deviation from the reference distribution required to produce sensitive results. It is the smallest KL divergence from the reference distribution required for the scalar parameter’s value to fall below a user-specified threshold (e.g., 5% below the reference value). In addition to our three sensitivity measures, we can also estimate an alternative model and set the radius as the KL divergence between the alternative and reference models.

For estimation and inference, we propose an estimator for the bound, establishing its consistency and convergence rate. To this end, we first establish the consistency and convergence rate of the estimator of the identified set, following Chernozhukov et al., (2007). We then derive the asymptotic distribution of the plug-in estimator by proving the Hadamard directional differentiability of the bound, building on the work of Fang and Santos, (2019).

We apply our framework to an infinite-horizon dynamic demand model for new cars in the UK, Germany, and France. We consider the sensitivity of the price elasticity and consumer surplus from an additional $3,000 electric vehicle subsidy. In the model, the indirect utility of purchasing is a latent variable due to unobserved product characteristics, and its transition is typically modeled as an AR(1) process (e.g., Schiraldi, (2011); Gowrisankaran and Rysman, (2012)). For the price elasticity, we find that the French market is the least sensitive to the distributional assumption (at most 6.20% deviation from the reference elasticity), while the German market is the most sensitive (at most 15.24% deviation). We also find that this sensitivity is relatively stable over time for all three markets. For the consumer surplus, the German market is also the most sensitive (at most 102.75% deviation from the reference consumer surplus), while the UK and French markets are less sensitive (at most 25.17% and 24.73% deviation, respectively). More importantly, the results are still economically meaningful even under the worst-case distribution, with the consumer surplus remaining at least $309 million for the German market, $1,243 million for the French market, and $2,584 million for the UK market.

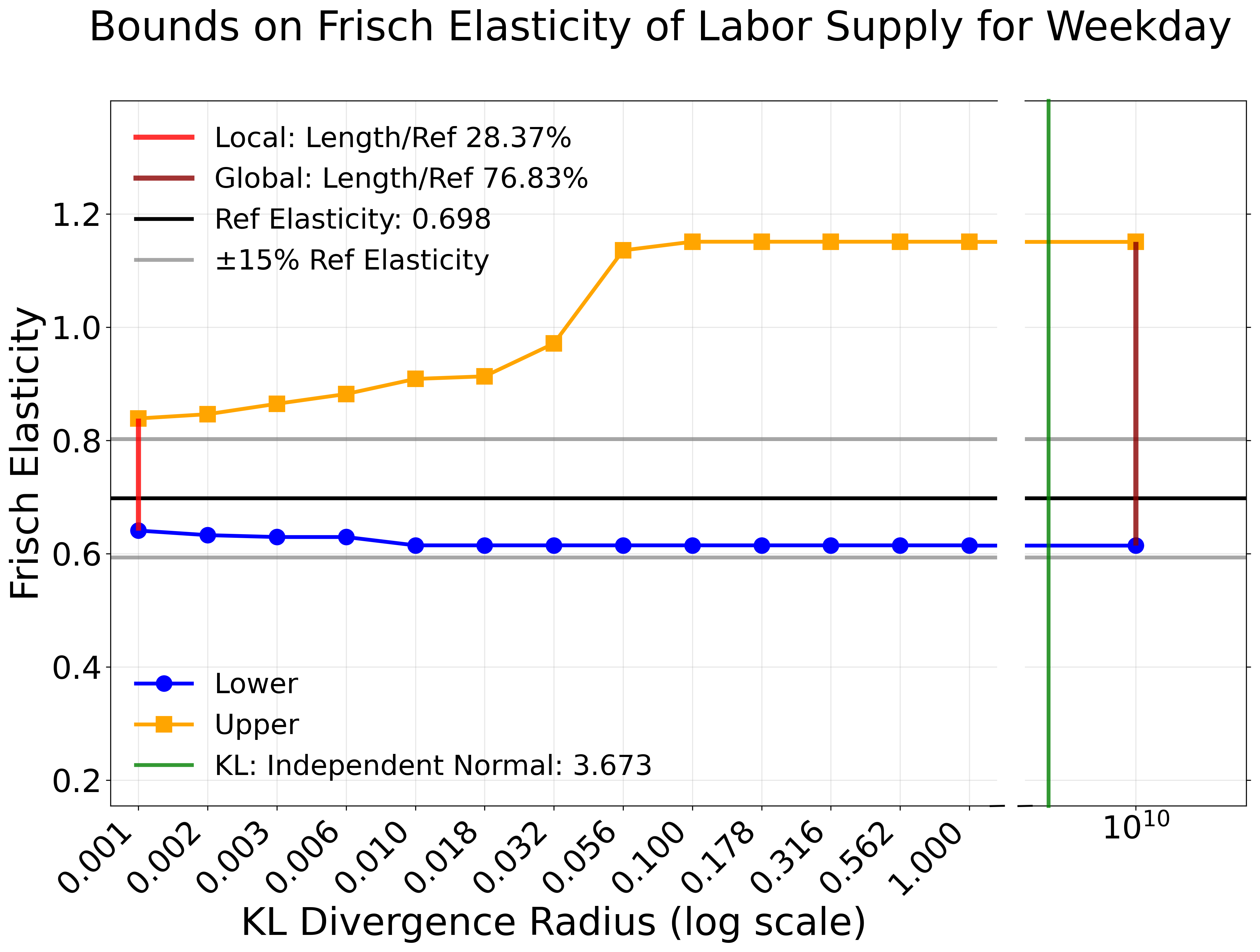

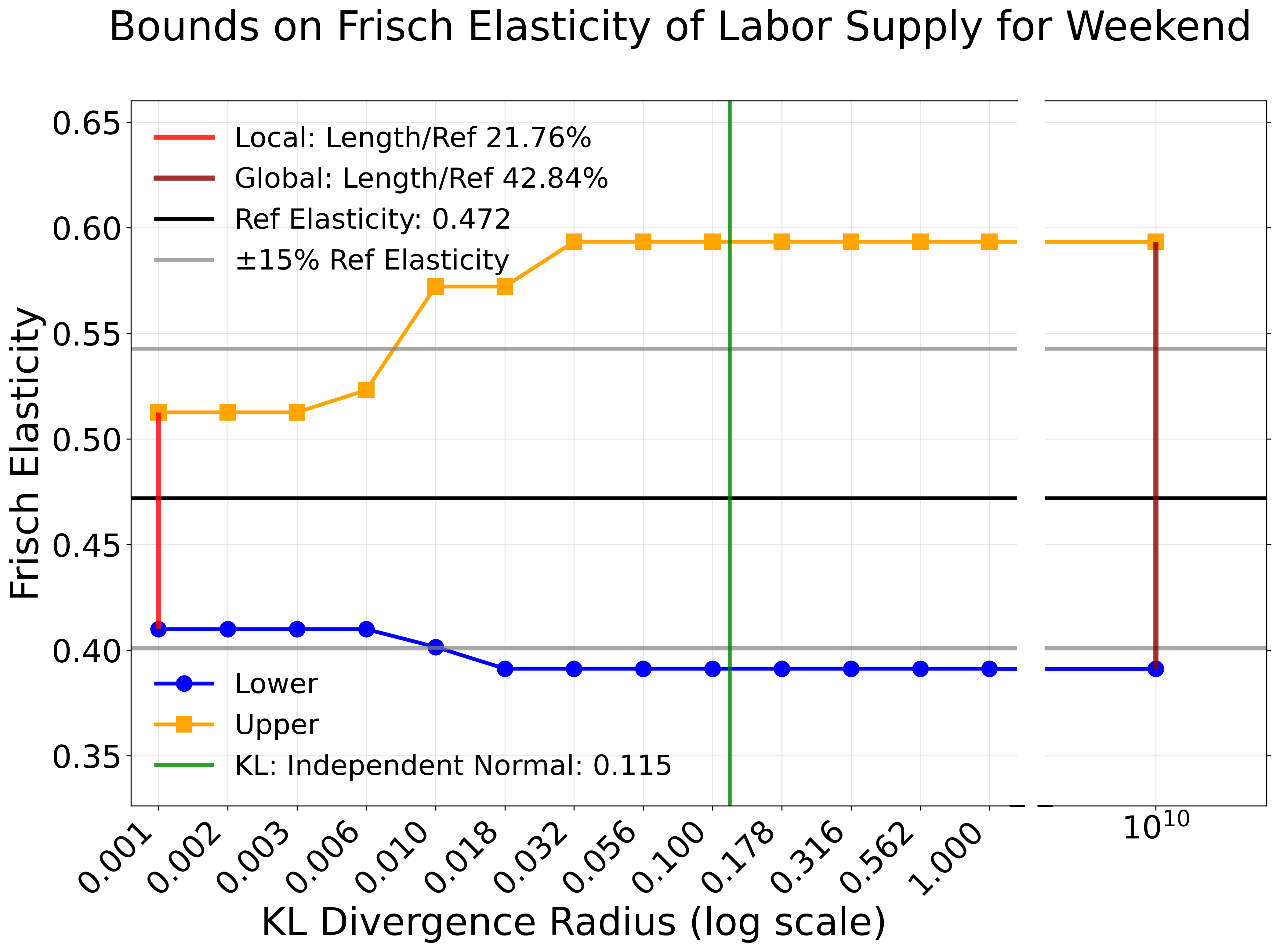

We also apply our framework to a finite-horizon dynamic labor supply model for taxi drivers in New York City. We consider the sensitivity of the elasticity of stopping work and the Frisch elasticity of labor supply. In the model, the market-level supply shock is a latent variable. The reference distribution is also modeled as an AR(1) process. For the elasticity of stopping work, we find that weekday drivers’ elasticity is more sensitive in the morning, while weekend drivers’ elasticity is more sensitive in the afternoon. For the Frisch elasticity, both weekday and weekend drivers’ elasticities are sensitive to the distributional assumption, with at most 76.83% and 42.84% deviation from the reference elasticity, respectively.

1.1 Related Literature

Identification and estimation. Many papers have focused on identification in a range of dynamic structural models including finite mixture models (Kasahara and Shimotsu, (2009); Luo et al., (2022); Higgins and Jochmans, (2023)), unobservable Markov processes (Hu and Shum, (2012)), and counterfactual conditional choice probabilities in dynamic binary choice models (Norets and Tang, (2014)). Berry and Compiani, (2023) uses the generalized instrumental variable approach for unobserved state variables in dynamic discrete choice (DDC) models. In fixed effects DDC models, Aguirregabiria et al., (2021) considers identification of structural parameters using sufficient statistics, while Aguirregabiria and Carro, (2024) studies identification of average marginal effects. Hwang, (2024) employs proxy variables for the latent variables. Kalouptsidi et al., 2021c proposes the Euler Equations in Conditional Choice Probabilities (ECCP) estimator. By leveraging finite-dependence properties and cross-sectional data, it identifies structural parameters in the presence of serially correlated market-level unobserved variables without distributional assumptions. Arcidiacono and Miller, (2011) adapts the Expectation-Maximization algorithm to estimate DDC models with discrete latent types. Norets, (2009) extends the Bayesian estimation of DDC models by Imai et al., (2009) to allow for serially correlated latent variables, while Blevins, (2016) proposes a sequential Monte Carlo method. Chiong et al., (2016) shows identification in DDC models is an optimal transport problem under serial independence of utility shocks. In addition, Chen et al., (2011), Schennach, (2014), and Fan et al., (2023, 2025) consider inference of finite-dimensional parameters in the presence of an infinite-dimensional parameter, namely the distribution of latent variables.

Our framework contributes to this literature in three ways. First, we focus on a scalar parameter (outcome of interest) directly instead of the identified set of model primitives. Second, to analyze sensitivity, we consider a perturbation set around the reference distribution rather than the set of all distributions. Third, we complement identification strategies that do not rely on distributional assumptions. In the labor supply application, we use the ECCP estimator by Kalouptsidi et al., 2021c to point identify the utility parameters, and then conduct sensitivity analysis of the labor supply elasticity to the distributional assumption about the market-level supply shock.

Sensitivity analysis and robustness. In DDC models, Kalouptsidi et al., 2021a ; Kalouptsidi et al., 2021b relax common normalization on the utility function. Bugni and Ura, (2019) considers the local misspecification of the transition density of observable variables, assuming the transition density is correctly specified in the limit (as the sample size goes to infinity) in DDC models. Andrews et al., (2017) considers a setting in which the moments are locally misspecified under the reference distribution. Subsequent work, Armstrong and Kolesár, (2021), constructs near-optimal confidence intervals in such models. In contrast, we perturb the reference distribution subject to the moment conditions. Bonhomme and Weidner, (2022) perturbs the reference model and assumes the size of the perturbation shrinks to zero as the sample size goes to infinity. Chen et al., (2024) relaxes the rational expectation assumption. Gu and Russell, (2024) considers the identification of scalar counterfactual parameters using optimal transport. Spini, (2024) studies the robustness of policy effects to changes in the distribution of covariates. Armstrong, (2025) provides a selective review of misspecification in econometrics. Most closely related is Christensen and Connault, (2023), who conducts sensitivity analysis with respect to parametric assumptions about the distribution of latent variables in structural models. However, they focus on relaxing the marginal distribution assumption while maintaining serial independence.

We contribute to this literature in three ways. First, our focus on serial dependence complements analyzes of misspecification in the marginal distribution assumption (e.g., Christensen and Connault, (2023)). Second, the size of our perturbation set is fixed and does not shrink with the sample size. Third, we provide a computationally tractable dual formulation for the optimization problem. While prior work (Schennach, (2014); Gu and Russell, (2024); Christensen and Connault, (2023)) uses duality to convert the infinite-dimensional problem to a finite-dimensional one, our dual problem is still infinite-dimensional. This is because the stationarity condition for time-homogeneous models and fixed terminal distribution for time-inhomogeneous models are infinite-dimensional, and serial dependence leads to an infinite-dimensional value function in dynamic structural models. However, by leveraging EOT duality, we provide a tractable implementation and demonstrate our approach through two empirical applications.

Distributionally robust optimization (DRO). The literature on DRO (Kuhn et al., (2019); Rahimian and Mehrotra, (2019); Blanchet et al., (2022); Gao and Kleywegt, (2023); Wang et al., (2021)) usually studies the uncertainty due to limited observability of data, noisy measurements, or estimation errors.

Our work is distinct in that we study the misspecification due to assumptions about the serial dependence of latent variables—a problem of model specification rather than data limitation. In addition, because our framework can be treated as a moment-constrained DRO problem, we employ the minimax theorem (see Fan, (1953) and Ricceri and Simons, (1998), Theorem 1.3) to exchange the order of the supremum over Lagrangian multipliers (for the moment conditions and structural constraints) and the infimum over distributions in the perturbation set. This exchange allows a direct application of duality results from the DRO literature.

Applied work. Building on the seminal work on the estimation of DDC models (Rust, (1987); Hotz and Miller, (1993); Aguirregabiria and Mira, (2002, 2007); Pesendorfer and Schmidt-Dengler, (2008); Arcidiacono and Miller, (2011)), most applied work assumes the serial independence of utility shocks. In the presence of serially correlated latent variables, parametric models are often used, as seen in the works of Schiraldi, (2011); Gowrisankaran and Rysman, (2012); Blevins et al., (2018); Piveteau, (2021) and others mentioned in the introduction.

We contribute to this literature by developing a computationally tractable framework for sensitivity analysis of scalar parameters of interest to these distributional assumptions. We also demonstrate our framework through two empirical applications: an infinite-horizon dynamic demand model, and a finite-horizon dynamic labor supply model.

Outline: Sections 2 and 3 present our framework for time-homogeneous and time-inhomogeneous models. Section 4 establishes the large sample properties of our estimator. Section 5 introduces three sensitivity measures. Section 6 discusses practical implementation. Sections 7 and 8 present two empirical applications. Section 9 concludes. Appendix A presents two additional examples. All proofs are in Appendix B.

Notation: Let be a vector of latent variables with support where is assumed to be Polish. Let be the space of Borel probability measures on and be the Borel -algebra on . In this paper, all measures are assumed to be absolutely continuous with respect to the Lebesgue measure. Denote by , the expectations with respect to and the probability distribution of the random variable , respectively. For variables in a stationary dynamic context, a prime (e.g., ) denotes the variable’s value in the next period. Let , we write if is absolutely continuous with respect to , and as the product measure. For a finite-dimensional vector, denote by the -norm. Denote by the space of functions for which . For a set , denote by its interior. Denote by the set of non-negative real numbers, and the set of natural numbers. Finally, let .

2 Methodology for Time-Homogenous Models

This section develops our methodology for time-homogeneous models. We first define the perturbation set in Section 2.1, and present two examples in Section 2.2. Then, we present a general framework that nests the examples, and derive its duality in Section 2.3. Finally, Section 2.4 discusses how to perturb the stationary distribution.

2.1 Definition of Perturbation Set

We partition a vector of latent variables into subvectors, i.e., .111The vector can also contain observable variables. Each subvector has a marginal distribution for . Let denote the reference distribution for . The perturbation set around this reference distribution is defined as:222The perturbation set is compact and closed in the topology of weak convergence (see Lemma 8).

where is the set of joint distributions on with marginals , and measures the “size” of the perturbation set, defined by the Kullback-Leibler (KL) divergence:

In time-homogeneous models, the marginal constraints are used to impose the stationarity. Consider an unobserved stationary first-order Markov process with state space . The process is stationary with respect to if for all , where is the reference transition kernel (e.g., conditional Gaussian distribution for an AR(1) process). This is equivalent to requiring that the marginal distributions of the joint distribution are both , i.e., . Moreover, for any , its conditional density preserves as a stationary distribution.333We can further partition into some subvectors to analyze sensitivity to distributional assumptions about cross-sectional dependence. For this example, let . Then, the perturbation set is:

This definition allows us to perturb the transition kernel of the Markov process while keeping its stationary distribution unchanged. It can introduce non-linear dynamics into the latent variable process. For example, if the reference model is an AR(1) process, the perturbation set includes any nonlinear first-order Markov process with the same stationary distribution as the AR(1) process. Section 2.4 discusses how to perturb the stationary distribution. In this case, we replace the condition with , where is the perturbed stationary distribution that is in a neighborhood of .

2.2 Examples

This section presents two examples of single-agent DDC models. We focus on a parametric model for latent variables in both infinite and finite-horizon DDC models. Appendix A presents two additional examples: (i) serial independence of utility shocks in DDC models (ii) serial independence of consumption shocks in dynamic discrete-continuous choice models. Our framework seeks to find the lower bound on a scalar parameter of interest by solving a constrained optimization problem over the perturbation set that is subject to the structural constraints (e.g., Bellman equation) and moment conditions.

Example 1 (Infinite Horizon Dynamic Discrete Choice Models with Serially Correlated Latent Variables).

This example considers a parametric model for serially correlated latent variables in a single-agent DDC model as in Rust, (1994). Let be the exogenously evolving latent variable. Agents solve the smoothed444We assume that the utility shock is additively separable in the period utility function and follows an i.i.d. Extreme Value Type I distribution, leading to the log-sum-exp form of the value function Rust, (1987). Bellman equation for the conditional value function where is a function class (e.g., square integrable functions, the Hölder class, etc.): for , it holds that

| (1) |

where is the observable state variable, is the discount factor, is the Euler constant, and is the period utility of choosing action parameterized by . The model-implied Conditional Choice Probability (CCP) is:

Let be a vector of current and future latent variables. An AR(1) process is often used to model the transition of . Therefore, the reference distribution is where is the conditional distribution parameterized by (e.g., the parameters of the AR(1) process), and is its stationary distribution. The perturbation set for a given is defined as:

Suppose the scalar parameter of interest is the average elasticity of action with respect to variable , defined as:

where is the population CCP, and the expectation is taken with respect to the joint distribution and the distribution of .

We convert the smoothed Bellman equation (1) into an unconditional moment restriction that depends on the joint distribution . We assume555The Lagrange multiplier function converts the continuum of conditional moment restrictions into a single unconditional moment restriction (see for example Andrews and Shi, (2013) and Schennach, (2014)). there exists a class of Lagrange multiplier functions 666For example, if is the class of square integrable functions, is the class of square integrable functions. such that solves the Bellman equation (1) if and only if:

where the inner expectation is taken with respect to the stationary distribution of , the population CCPs, and the conditional distribution of given . Let . Then, we rewrite the structural constraints as:

We consider the following moment conditions for estimation:

We assume has discrete support, and rewrite the moment conditions as:

where stacks the model-implied CCPs, and stacks the population CCPs.

Then, the lower bound on the elasticity is given by:

| s.t. | |||

In the next section, we will discuss the implementation for a fixed . The overall lower bound requires an additional optimization over . In practice, we can discretize the estimated AR(1) process, and scale the grid points according to the candidate during the optimization. Then, the optimization over can be implemented using the algorithm proposed in Section 6.2.

Example 2 (Finite Horizon Dynamic Discrete Choice Models).

This example considers a finite-horizon DDC model where the latent variable follows a first-order stationary Markov process. The conditional value function at time period solves the smoothed Bellman equation: for ,

| (2) |

where is the observable state variable, is the discount factor, is the Euler constant, is the period utility parameterized by , and . The model-implied CCP is:

Let be a vector of current and future latent variables. In practice, we may set the reference distribution as the estimated distribution from a parametric model, such as an AR(1) process. The reference distribution is the product of the conditional distribution and its stationary distribution, . The perturbation set is defined as:

Suppose the scalar parameter of interest is the consumer surplus derived from the choice set at period :

where we assume is linear in price and is the price coefficient.

We convert the smoothed Bellman equation (2) into restrictions that depend on the joint distribution . We assume there exists a class of Lagrange multiplier functions such that for each , solves (2) if and only if:

where , is distributed according to the observed data at time , and follows the conditional distribution given . Let and . Then, we rewrite the structural constraints as:

where is the sum of the objective functions in the above equation for each .

We consider the following moment conditions for estimation: for each ,

where is the population CCP at period . We assume has discrete support, and rewrite the moment conditions as:

where and stack the model-implied and population CCPs for all .

Then, the lower bound on consumer surplus at period is given by:

2.3 Framework and Duality

We now present a general framework that nests the above examples. In general, the model is not point-identified when is not a singleton.777For example, see Schennach, (2014); Christensen and Connault, (2023). Therefore, we propose to compute upper and lower bounds on the outcome of interest. Let the scalar parameter of interest, , be a function of the latent variable , and the model primitives . The lower bound is the solution to the following optimization problem:

| ( Primal) | ||||

where .

The first constraint is a moment condition where the moment function is finite-dimensional as we assume the observable variable has discrete support and stack the moment functions for each . The second constraint is a structural constraint defined by that is linear in the Lagrange multiplier function for a given . Finally, is the solution to the structural constraint.

Remark 1.

-

(i)

The upper bound can be obtained by replacing with .

-

(ii)

The moment condition can contain restrictions linear in , e.g., covariance restrictions.

-

(iii)

If some model primitives (e.g., a subvector of ) are point-identified, they are treated as fixed values rather than optimized over.

-

(iv)

The framework can also be applied to models without structural constraints, such as static and panel discrete choice models.

The Primal problem can be intractable due to the optimization over . First, the properties (e.g., closed-form and smoothness) of the optimal are typically unknown, complicating the choice of approximation methods. Second, the marginal distribution conditions are functional constraints imposed directly on the distribution being optimized, which are computationally difficult to impose. Third, expectations are taken with respect to the perturbed distribution, making numerical integration difficult.

To overcome these issues, we derive the Dual problem corresponding to the Primal. The Dual provides the closed-form of the optimal , and characterizes its smoothness. Moreover, in the dual, the expectation is taken with respect to the reference distribution . Section 6.2 proposes a computationally tractable algorithm that utilizes the optimal . To motivate the duality, consider the Lagrangian of the Primal:

| (3) |

where , is the Lagrange multiplier for the moment condition and is the Lagrange multiplier for the KL divergence constraint. For given , under regularity conditions, we can swap the order of the infimum over and the supremum over . Then, we can rewrite (3) as:

The inner infimum is the Entropic Optimal Transport (EOT) problem (for )888See Nutz, (2021) for a comprehensive introduction to the EOT problem. The EOT problem has close connection to the static Schrödinger bridge problem. It is called the Optimal Transport (OT) problem when (see Villani et al., (2009)). The optimal value is called the optimal OT value.:

where is the cost function, and is called the optimal EOT value. The EOT problem is computationally fast to solve using the Sinkhorn algorithm, which relies on the duality of the EOT problem. Moreover, the closed-form and smoothness of the unique solution to the EOT problem can be derived from its duality (see Theorem 1 and Proposition 1). Section 6.1 reviews the EOT duality and the Sinkhorn algorithm. Next, we impose assumptions for the minimax theorem to swap the order of infimum and supremum, and the EOT duality to hold:

Assumption 1.

We assume:

-

(i)

The marginals have finite -th moment for some integer .

-

(ii)

, and let .

-

(iii)

is convex and symmetric, i.e., for , for , and if . Moreover, if , then for .

-

(iv)

For , it holds that are lower semicontinuous in .

-

(v)

For , there exist a finite positive constant and such that for , it holds that where and is a metric on .

Assumptions 1(i)-1(iv) are mild. Assumption 1(iv) holds for indicator functions. There is no particular necessity to write in log-density form in Assumption 1(ii). Our notation is chosen to simplify the expression in Assumptions 1(iv) and 1(v). Assumption 1(v) imposes the growth rate condition. It is satisfied for all Examples in Section 2.2 if we assume , , and satisfy the growth rate condition. It ensures that for , and can also be used to show the convergence of the Sinkhorn algorithm and the convergence of optimal EOT value to optimal OT value as (Eckstein and Nutz, (2022, 2024)).999For the convergence of optimal EOT value to optimal OT value, lower semicontinuity alone is not sufficient (Nutz, (2021) Example 5.1). A sufficient condition is the continuity condition on the cost function.

Theorem 1.

Let where . Under Assumption 1, the following holds:

-

(i)

(Minimax Duality)

( Dual) where is the EOT problem with regularization parameter :

-

(ii)

(Entropic Optimal Transport Duality) For , we have:101010See Villani, (2021) for optimal transport duality ().

Moreover, there are unique maximizers up to additive constants -almost surely, and the unique worst-case distribution has the density of the form:

Furthermore, we have .

-

(iii)

If the lower semicontinuity in Assumption 1(iv) is strengthened to continuity, then optimizing over is equivalent to optimizing over .

Theorem 1 establishes the duality and provides the closed-form of . is the test function for the marginal distribution condition for . The optimal are the optimal EOT potentials, which can be efficiently obtained using the Sinkhorn algorithm.

The Dual is computationally tractable. First, it provides the closed-form of the worst-case distribution , which can be used in the Primal problem even if we want to solve it directly. In Section 6.2, we propose an iterative algorithm that alternates between solving the EOT to obtain the worst-case distribution and updating by solving the structural constraint with the worst-case distribution. Second, for given , the optimal (and thus ) can be efficiently computed using the Sinkhorn algorithm, which is computationally very fast. Third, the expectations in the Dual are taken with respect to the marginal distributions and the reference distribution. Therefore, numerical integration methods can be determined in advance. Finally, we have:

Proposition 1.

If is -times continuously differentiable in , and , then are -times continuously differentiable in . Therefore, is also -times continuously differentiable in .

Proposition 1 shows the smoothness of for (the EOT case). For (the OT case), it is not straightforward to obtain the smoothness of the worst-case distribution (see Villani et al., (2009) Chapter 12).

2.4 Perturbation of Stationary Distribution

This section discusses how to perturb the stationary distribution in the time-homogeneous setting. We consider the serial dependence of the latent variables, as detailed in the example in Section 2.1. Let be the vector of current and future latent variables. We define the perturbation set for the stationary distribution as where . The perturbation set for the joint distribution is:

Let denote the lower bound on the scalar parameter of interest under this perturbation set. Under regularity conditions, we can swap the order of infimum over and the supremum over :

where is the EOT problem with respect to the perturbed stationary distribution : . Its dual formulation is:

Under regularity conditions, we can swap the order of infimum over and the supremum over . Then, the inner infimum over is:

which is a KL-divergence distributionally robust optimization problem (see Hu and Hong, (2013); Rahimian and Mehrotra, (2019)) whose dual formulation is:

where is the Lagrange multiplier for the KL divergence constraint for . To summarize:

Theorem 2.

Suppose Assumption 1 holds for any . Assume is compact and that for any , the optimal potentials are lower semicontinuous. Then, we have:

Theorem 2 shows the dual formulation when the stationary distribution is perturbed. Although the Sinkhorn algorithm does not apply directly, we can sequentially update using the first-order optimality conditions like the Sinkhorn algorithm (see Section 6.1 for a review of the Sinkhorn algorithm).

3 Methodology for Time-Inhomogeneous Models

This section extends our framework to the time-inhomogeneous setting. We begin by defining the perturbation set for these models in Section 3.1. Section 3.2 provides an example of a finite-horizon dynamic discrete choice model. Section 3.3 presents the duality result. Finally, Section 3.4 discusses how to perturb the initial distribution.

3.1 Definition of Perturbation Set

Consider a sequence of latent variables over a finite horizon, , that follows a first-order Markov chain. The reference joint distribution is the product of an initial distribution and transition kernels:

where is the initial distribution, and is the transition kernel from period to . Let be the terminal distribution implied by this process.

We consider perturbing the reference distribution while holding its initial and terminal distributions fixed, i.e.,

where is the set of all joint distributions over that satisfy the first-order Markov property111111That is, for any , almost surely under . and have and as their initial and terminal marginal distributions. Our perturbation set allows for any transition dynamics of the latent variables between the initial and terminal periods, as long as the overall process remains Markovian and the initial and terminal distributions are fixed.

We will discuss how to perturb the initial distribution in Section 3.4. The terminal distribution can often be nonparametrically identified; therefore, we fix it. For instance, in a finite horizon DDC model, the terminal period is a static discrete choice problem where the distribution of the latent variable can be identified (Lewbel, (2000); Matzkin, (2007)). Moreover, if is the market-level latent variable, and the model has the finite dependence property (see Arcidiacono and Miller, (2011))121212For example, a model with a terminating action has the finite dependence property., then the utility parameters can be identified without a distributional assumption for the latent variables (see Kalouptsidi et al., 2021c ), which in turn identifies the terminal distribution.

3.2 Example

Example 3 (Finite Horizon DDC with Time-Inhomogeneous Transition of Latent Variables).

This example considers a time-inhomogeneous transition for the latent variables, , whose perturbation set is . The model is similar to Example 2 but with a time-inhomogeneous transition.

We convert the smoothed Bellman equation (2) into restrictions that depend on the sequence of two-period marginal distributions , where:

We assume there exists a class of Lagrange multiplier functions such that for each , solves (2) if and only if:

where , and is distributed according to the observed data at time , and follows the conditional distribution given . Let and . We then rewrite the structural constraints as:

where is the sum over of terms inside the expectation of the previous equation.

Then, the lower bound on consumer surplus at period is given by:

where is the marginal distribution of implied by .

3.3 Framework and Duality

The bound for the time-inhomogeneous case, , is defined similarly to the time-homogeneous case, but with the optimization performed over :

| ( TI) | ||||

where “TI” stands for time-inhomogeneous. To solve TI, we follow the procedure in Theorem 1. However, the set is not necessarily convex, which prevents the proof strategy of the minimax duality in Theorem 1 from being applied directly. Therefore, we propose to solve a relaxed problem where the Markov property condition is removed. We then show that, under certain reasonable conditions, the solution to the relaxed problem is Markovian, thereby also solving the original problem. The perturbation set for the relaxed problem is defined as:

where is the set of joint distributions with initial distribution and terminal distribution . The relaxed problem is given by:

| ( Relaxed) | ||||

whose Lagrangian is:

| (4) |

where , is the Lagrange multiplier for the moment condition and is the Lagrange multiplier for the KL divergence constraint. For given , under regularity conditions, we can swap the order of the infimum over and the supremum over . Then, we can rewrite (4) as:

The inner infimum is:

which can be rewritten as the discrete-time dynamic Schrödinger bridge (SB) problem (see Léonard, (2013); De Bortoli et al., (2021)). Because it only restricts the initial and terminal distributions, we can decompose it into two parts: the two-period marginal distribution part (the first and last period) and the conditional distribution part (the intermediate variables conditional on the first and last period). The second part is unconstrained, thereby having a closed-form solution. The first part is the static SB (or EOT) problem whose duality is similar to Theorem 1. We impose the following assumptions for the minimax duality, decomposition, static SB duality, and the Markov property:

Assumption 2.

Let be the two-period marginal of at periods and . We assume:

-

(i)

is compact.

-

(ii)

, i.e., and are mutually absolutely continuous. Moreover, .

-

(iii)

For , it holds that .

-

(iv)

The functionals , , and are pairwise additive, i.e., , , and for some functions , , and .

The boundedness condition in Assumption 2(iii) is stronger than Assumption 1(v), which does not guarantee that for any . Assumption 2(ii) is a sufficient condition for the SB duality to hold. Finally, Assumption 2(iv) is the key to the Markov property of the solution to the Relaxed problem, and is satisfied in Example 3. It does not hold if the moment function depends on the entire path of the latent variables.

Theorem 3.

Theorem 3 shows the duality for the Relaxed problem. The difference between Theorem 3(i) and Theorem 1(i) is that ( ) does not fix the intermediate marginal distributions. Therefore, we can decompose ( ) into the sum of two-period marginal distribution () part, and the conditional distribution (the distribution of given and ) part. The latter part is an unconstrained optimization problem, thereby having a closed-form solution. The first part is the static SB problem, whose duality is given by Theorem 3(ii).

Assumption 2(iv) is crucial for the solution to have the Markov property. Under this assumption, the cost function is also pairwise additive. Therefore, the density ratio in Theorem 3(ii) has the Markov property.131313It can be treated as the (unnormalized) pairwise Markov random field Wainwright et al., (2008). If there exists one optimal , then the TI problem is equivalent to the Relaxed problem.

The Relaxed problem can also be solved using the iterative algorithm proposed in Section 6.2. There is an additional step to obtain the two-period auxiliary reference distribution . The can also be solved using the Sinkhorn algorithm.

3.4 Perturbation of Initial Distribution

Let be a convex closed set around the initial distribution , e.g., where . Then, the perturbation set is defined as:

Let be the lower bound on the scalar parameter for the Relaxed problem with the perturbation set . The following minimax duality similar to Theorem 3 holds:

Theorem 4 (Minimax Duality with Perturbation of Initial Distribution).

Suppose is convex and closed, and that the assumptions in Theorem 3 hold for each . Then,

where is defined as follows:

| (5) |

To solve (5), as shown in the proof of Theorem 3(ii) and Section 3.3, we can decompose the problem into two parts: the two-period marginal distribution part, and the conditional distribution part. The first part requires solving:

where is the set of distributions of whose marginal distributions are and , respectively. It is equivalent to solving:

The inner infimum is an EOT problem. Let be its optimal value.

Lemma 1.

Under the assumptions in Theorem 3, is convex in . Its directional derivative with respect to in the direction is given by:

where is the optimal EOT potential for .

4 Large Sample Properties

This section establishes the large sample properties of the estimator for the bound. Section 4.1 proposes a consistent estimator and shows its convergence rate. Section 4.2 establishes the asymptotic distribution of the plug-in estimator for the bound.

4.1 Consistency and Convergence Rate

The bound on the scalar parameter is the projection of the identified set defined by the moment conditions and structural constraints onto the scalar parameter. We follow Chernozhukov et al., (2007) to propose an estimator for the identified set and show its consistency and convergence rate. Let be an estimator for where is the sample size. Denote by the tolerance level for the moment conditions that goes to zero at a suitable rate as . Our estimators , and for the bounds replace the moment conditions by the approximate moment conditions.141414To compute the estimator, the number of moment conditions is doubled due to the use of approximate moment conditions. The duality is similar to Theorems 1 and 3, thus is omitted for brevity.

Assumption 3.

Let be either or , and . Assume:

-

(i)

is convex and compact.

-

(ii)

If , then Assumption 2(i) holds.

-

(iii)

For , the structural constraint -a.s. has a unique solution .

-

(iv)

The identified set is nonempty.

-

(v)

is continuous in , i.e., the preimages of closed sets are closed.

Assumption 3(i) is mild. Assumption 3(iii) holds in single-agent DDC models. It rules out dynamic games with multiple equilibria. Assumption 3(iv) is also mild as the identified set for is usually nonempty under the reference distribution . Moreover, if the identified set for 151515In this case, the KL divergence constraint is replaced by the absolute continuity constraint, i.e., . is nonempty, then Assumption 3(iv) implicitly assumes the radius is large enough. The smallest radius such that the identified set is nonempty can be estimated (see Remark 3). Assumption 3(v) implies that the identified set and its estimator are compact as is compact (see Lemma 8) and thus is compact (see Lemma 2).

Under Assumption 3, the estimator for is defined as:

The analysis of the consistency and convergence rate uses the Hausdorff Distance:

where and is a metric on .

Assumption 4.

Assume is a -consistent estimator for , and there exists such that with probability approaching 1 where can be data-dependent. Let , and assume .

Assumption 4 is mild as we assumed the observable variable has discrete support, e.g., can be the frequency estimator. In practice, we can set . Then, the convergence rate in Theorem 5(ii) is -consistent up to a logarithmic factor. We show some properties of the identified set and its estimator:

By the extreme value theorem, the infimum is achieved if the scalar parameter is continuous on , i.e., Assumption 6(i) holds. Therefore, the optimization problem has a solution. Next, we impose the polynomial minorant condition as in Chernozhukov et al., (2007) for the convergence rate of the estimator:

Assumption 5 (Polynomial Minorant Condition).

There exists positive constants and such that: .

Theorem 5.

Under Assumptions 3 and 4, we have:

-

(i)

(Consistency) .

-

(ii)

(Convergence Rate) Under Assumption 5, .

Theorem 5 establishes the -consistency up to a logarithmic factor (if ). Then, we impose the following continuity assumption on the scalar parameter of interest:

Assumption 6.

Let , assume one of the following:

-

(i)

is continuous in .

-

(ii)

is Lipschitz continuous in .

Theorem 6.

Under Assumptions 3 and 4, we have:

-

(i)

(Consistency) Under Assumption 6(i), , and .

-

(ii)

(Convergence Rate) Under Assumption 6(ii), , and .

4.2 Asymptotic Distribution

This section establishes the asymptotic distribution of and . To this end, we first show the Hadamard directional differentiability of and with respect to at , enabling us to apply Fang and Santos, (2019).

Definition 1.

The map is Hadamard directionally differentiable at , if there exists a continuous map such that for , we have:

for all sequences , , and as .

Under Assumption 3, we can restate the optimization problem as:

where . Moreover, the identified set is nonempty, which means the feasible set for the optimization problem is nonempty. By Lemma 2, is compact. Under Assumption 6(i), the Extreme Value Theorem (see Rudin et al., (1976) Theorem 4.16.) implies that the infimum is attained. Denote by , the nonempty sets of optimizers for the problems and , respectively.

Assumption 7.

Assume and are continuously differentiable on . That is, they are Gâteaux differentiable on and the corresponding derivatives and are continuous on (in the operator norm topology).161616For a given direction , the Gâteaux derivatives are understood as and . See Bonnans and Shapiro, (2013) Page 35 for the definition of Gâteaux derivative.

Assumption 8.

Let be either or . Assume:

-

(i)

for .

-

(ii)

For , it holds that for and small enough, the problem has an -optimal solution such that .

-

(iii)

For the sequence has a limit point (in the norm topology) .

Theorem 7.

Under Assumptions 3, 7, and 8, the maps and are Hadamard directionally differentiable at in any direction , and:

where is the nonempty set of Lagrange multipliers for .171717See Bonnans and Shapiro, (2013) Definition 3.8 and Theorem 3.9. Robinson’s constraint qualification is satisfied under Assumptions 3, 7, and 8 (see Section B.4.4). Therefore, is nonempty.

Moreover, if , then and .

Theorem 7 shows the asymptotic distribution of the bound’s estimator. However, the computation of the derivatives can be intractable due to the optimization over the set of optimizers and the set of Lagrange multipliers. The numerical delta method Hong and Li, (2018) combined with our practical implementation in Section 6 can be used to overcome the computational challenge.

5 Interpreting the Results

In practice, we can estimate an alternative (parametric) model and set the radius to be the KL divergence between the alternative and the reference distribution. In addition, this section proposes three complementary sensitivity measures to interpret the results: global sensitivity, local sensitivity, and robustness metric.

5.1 Global Sensitivity

The global sensitivity approach progressively increases the radius until the bounds flatten. We show that it provides a computationally tractable approximation to the nonparametric bounds when the KL divergence constraint is removed. We focus on the time-homogenous case, for which the “nonparametric” perturbation set is:

After applying the minimax duality, we need to solve the following problem:

where the inner problem is an OT problem, which is computationally challenging in high-dimensional settings. However, the EOT is a computationally tractable approximation to the OT problem. Recall .

Theorem 8 (Adapted from Eckstein and Nutz, (2024) Theorem 3.1(i)).

Suppose Assumption 1 holds. Assume the marginals have finite -th moment for and some integer , and satisfies the condition in Eckstein and Nutz, (2024) where depend on . Let denote the dimension of . Then, for any ,

Theorem 8 provides an explicit upper bound on the approximation error of to . For DDC models, the constants and can be explicitly characterized, see Eckstein and Nutz, (2022) Lemma 3.5, and Eckstein and Nutz, (2024) Remark 2.1. The upper bound is strictly decreasing to zero as . Therefore, we can choose a sufficiently small (or sufficiently large radius ) to achieve a desired accuracy for the approximation. Our framework can thus approximate the nonparametric bounds in a computationally tractable way.

Remark 2.

Under certain conditions, one can establish the convergence of the EOT worst-case distribution to the OT worst-case distribution as the regularization parameter . Nutz, (2021) Theorem 5.5 provides one sufficient condition: the existence of a solution to the OT problem such that .

5.2 Local Sensitivity

The local sensitivity approach computes the right derivative of the bounds at , which measures the effect of a small perturbation of the reference distribution on the bounds. We show the right differentiability of the bounds with respect to . Define:

where is the Lipschitz constant, and are positive constants. We assume:

Assumption 9.

Let be either or defined as:

and be either or that are the sets of solutions to the optimization problems and over and . Assume:

-

(i)

is finite.181818The smallest radius can be computed by the robustness metric defined in Section 5.3, see Remark 4.

-

(ii)

is compact.

-

(iii)

.

-

(iv)

for .

-

(v)

For and small enough, the optimization problem corresponding to has an -optimal solution such that .

-

(vi)

For the sequence has a limit point (in the norm topology) .

Theorem 9.

Theorem 9 shows the right differentiability. With the derivatives of both upper and lower bounds, we can compute the derivative of the length of the bounds. In practice, we may need to compute it numerically due to the optimization over the set of optimizers and the Lagrange multipliers.

5.3 The Robustness Metric

The robustness metric is the smallest deviation from the reference distribution that can lead to sensitive results. In practice, we begin by estimating a reference scalar parameter, , under the reference distribution. If the perturbed scalar parameter is below a certain threshold, e.g., , then we may be concerned about the robustness of the results. The robustness metric is defined as:

| (6) |

where is a user-specified threshold. The optimization problem searches for a distribution in the identified set that results in and is the closest to the reference distribution in terms of KL divergence.

Remark 3.

Remark 4.

The robustness metric shares similarity with Schennach, (2014) as both approaches minimize the KL divergence subject to constraints. However, there are three differences. First, we aim to find the smallest radius that generates sensitive results, while Schennach, (2014) uses KL divergence to rank the distributions in the identified set for a given finite-dimensional parameter. Second, our reference distribution is the distribution that we use in practice, while the reference measure in Schennach, (2014) is a dominating measure to define the KL divergence. Third, we have the marginal distribution constraints and the structural constraints.

We can first plot the bounds against and then find the radius corresponding to the threshold . Alternatively, we can compute it directly by solving the optimization problem in (6), whose duality is analogous to Theorems 1 and 3:

Theorem 10.

Let where . Under Assumption 1, the following holds:

-

(i)

(Minimax Duality)

where is the EOT problem with regularization parameter 1:

-

(ii)

(Entropic Optimal Transport Duality) We have:

Moreover, there are unique maximizers up to additive constants almost surely, and the unique worst-case distribution has the density of the form:

Theorem 10 presents the dual formulation to compute the smallest radius. Unlike Theorem 1, it includes the Lagrange multiplier for the threshold constraint.

Theorem 11.

Let where . Under Assumptions 1(i), 1(iii), 1(iv), and 2, the following holds:

-

(i)

(Minimax Duality)

where is defined as follows:

(7) -

(ii)

The unique worst-case distribution to (7) has the form:

where and are the unique maximizers (up to an additive constant) to:

where the auxiliary reference measure is defined as:

Furthermore, the solution has the Markov property, i.e., .

-

(iii)

(Equivalence) where is the optimal value of the optimization problem in (6) for the time-inhomogeneous case with the first-order Markov property constraint on .

Theorem 11 provides the dual formulation for computing the smallest radius in the time-inhomogeneous case. The equivalence holds as the multiplier for the KL divergence is 1.

6 Practical Implementation

This section presents the practical implementation of the proposed framework. Section 6.1 reviews the entropic optimal transport problem and the Sinkhorn algorithm. Section 6.2 proposes a computationally feasible algorithm.

6.1 Entropic Optimal Transport and Sinkhorn Algorithm

This section reviews the Sinkhorn algorithm for the entropic optimal transport problem.191919See Sinkhorn and Knopp, (1967), Cuturi, (2013) and Nutz, (2021). Let for be probability spaces, where is the support for the random variable . For a cost function , the entropic optimal transport problem202020If , then Lemma 12 reformulates the problem as the EOT problem. with regularization parameter is defined as:

| ( EOT) |

whose dual is given by:

| (8) |

where is the test function for the marginal distribution constraint . The dual problem is a concave maximization problem over . The worst-case distribution is given by:

where the optimizers are known as the optimal EOT potentials (also called Schrödinger potentials), which are the solutions to the Schrödinger equation (SE):

| (SE1) | ||||

| (SEk) |

where is the product measure of all marginals except for the -th marginal. The Schrödinger equations (SE1) to (SEk) can be interpreted as the variational first-order conditions for optimality (see Nutz, (2021) Remark 3.4). Moreover, they also characterize the marginal constraints. To see this, define:

The marginal density can be obtained by integrating out the other marginals; therefore:

The Sinkhorn algorithm can be interpreted as a coordinate ascent scheme for the optimization problem (8). It is a computationally fast212121For its convergence rate, see Peyré et al., (2019), Carlier, (2022), and Eckstein and Nutz, (2022)., iterative method for solving (SE1)-(SEk).

Algorithm 1 (Sinkhorn Algorithm).

Initialize for . For iteration , sequentially update for by:

Stop if for a tolerance .

6.2 Proposed Algorithm

For given , the EOT problem provides the worst-case distribution, . This allows us to update by solving the structural constraint with . We therefore propose an iterative algorithm to solve the minimax problem. The algorithm proceeds by alternating between updating and the dual (Lagrange multiplier) variables, . After initializing all parameters, each iteration involves the following steps:

Algorithm 2.

Initialize . At iteration ,

-

1.

Update Model Primitives : For , update222222If gradient-based methods are used, then we smooth the non-differentiable components (e.g., the indicator function in Example 4) using a smooth approximation. the model parameters by:

-

(a)

Propose a new candidate .

-

(b)

Solve the EOT problem with and obtain .

-

(c)

Update by solving the structural constraint with .

-

(d)

Accept/reject the proposed .

-

(a)

-

2.

Update Dual Variables : For , update following the same procedure as in the previous step.

-

3.

Iterate until convergence, or a pre-specified number of iterations is reached.

The computational cost per iteration mainly comes from solving the EOT problem and the structural constraint, which are both computationally fast. However, the number of iterations required for convergence can be much larger, as our optimization problem is a minimax problem that is potentially non-differentiable.

7 Empirical Application: Infinite Horizon DDC

This section applies our framework to an infinite-horizon dynamic demand for new cars in the UK, France, and Germany. Due to the unobserved product characteristics, the indirect utility of purchasing is the latent variable. To estimate the price elasticity and conduct welfare analysis of electric vehicles (EV) subsidy, we require a distributional assumption for the latent variable to solve the Bellman equation. Existing literature often uses an AR(1) process (e.g., Schiraldi, (2011); Gowrisankaran and Rysman, (2012)), which may be misspecified. For example, the indirect utility may exhibit nonlinear dynamics. Therefore, we conduct a sensitivity analysis with respect to this reference distribution.

7.1 Data

We use the trim-level232323In the automobile industry, a trim-level refers to a specific version of a vehicle model that comes with a particular set of features, options, and styling elements. data from IHS Markit during the period from 2014 to 2023. The monthly level dataset contains sales, list price, and characteristics of car models in the UK, France and Germany, which are treated as three independent markets in our analysis. To construct the final dataset, we first aggregate data from the trim-level to the model-level. Then, we aggregate fuel types into: petrol, diesel, electric, and hybrid. We remove models whose total sales during the data period are less than 20,000.242424In addition, we remove monthly observations with sales below 150 for the German market and below 5 for the French market. Finally, we adjust list prices by subtracting EV subsidies. The initial market size for January 2014 is calculated by subtracting the number of registered cars from the total population of each country. The market size is then updated each subsequent month by subtracting the total number of cars sold in the preceding period.

Table 1 presents the summary statistics. The three markets offer around 141–215 products from around 23 to 30 brands per month. In terms of average sales per model, Germany has 81,401 units, closely followed by France with 81,357 units, and the UK with 70,682 units. The average price is around $33,444 in the UK, $27,830 in France, and $36,117 in Germany.

| Avg # | Avg # | Avg # | Price (USD) | Horsepower | Weight (kg) | |

| Country | Products | Brands | Sales | Mean | Mean | Mean |

| UK | 196 | 30 | 70,682 | 33,444 | 140 | 1,836 |

| France | 141 | 23 | 81,357 | 27,830 | 112 | 1,702 |

| Germany | 215 | 26 | 81,401 | 36,117 | 151 | 1,952 |

Note: The price is adjusted for EV subsidies. First two columns are average number of products and brands per month. Average sales is the average number of cars sold per model. Mean price, horsepower, and weight are weighted by total sales.

7.2 The Model

The model is infinite horizon. At each month , a consumer chooses where is the set of available cars at , and 0 is the outside option of not purchasing. Each car is characterized by a vector of observable characteristics , price , and an unobserved characteristic . The period utility of choosing is given by:

where is a vector of i.i.d. type I extreme value utility shocks, and are the vectors of observable characteristics, prices, and unobserved characteristics for all cars in .

We assume a purchase is a terminating decision, i.e., consumers exit the market after the purchase. The conditional value function of purchasing car can be written as the sum of the current period utility and the flow utility after purchase:

where is the discount factor. The inclusive value of purchasing is defined as:

Following Schiraldi, (2011) and Gowrisankaran and Rysman, (2012), we assume:

Assumption 10 (Inclusive Value Sufficiency252525The IVS assumption has also been used in Hendel and Nevo, (2006); Melnikov, (2013); Osborne, (2018). (IVS)).

can be summarized by where is the conditional distribution function.

Under the IVS assumption, is the only state variable, and the value function is the solution to the smoothed Bellman equation:

| (9) |

where and are the conditional value functions of not purchasing and purchasing, respectively. The market share of car at time is given by:

| (10) |

7.3 First-Stage Estimation

In each market, the car with the highest total sales is set as the reference product, denoted by .262626The reference cars are Volkswagen Golf (Petrol) in Germany, Peugeot 208 (Petrol) in France, and Ford Fiesta (Petrol) in the UK. The reference car for each country is always available in that country’s market. Taking the log-odds ratio for cars and at time yields:

| (11) |

where , , and . The parameters are identified272727The intercept and reference fixed effects are not identified from (11); they are absorbed into . by the BLP instruments Berry et al., (1993). Moreover, can be recovered by fitting the relative market share , while the unobserved characteristic of the reference car, , cannot.

The exogenous characteristics, , include vehicle log-weight, log-horsepower, brand fixed effects, SUV fixed effect, and fuel type fixed effects.282828The instruments are the exogenous product characteristics, average log-weight and log-horsepower of competitors’ products, the proportion of competitors’ products, the proportion of hybrid cars squared, and the number of brands. A competitor product is defined as a car whose brand is not that of or . Table 2 presents the regression results. Price coefficients are negative and significant in all markets, ranging from -0.158 in France to -0.192 in Germany. Relative to petrol vehicles, EVs are preferred in the UK (0.019) and France (0.004), but not in Germany (0.000). Hybrid vehicles are valued positively across all three markets, with coefficients ranging from 0.029 in Germany to 0.037 in France. In contrast, diesel has a negative coefficient in the UK (-0.015) but positive effects in Germany (0.008) and France (0.006).

| UK | Germany | France | ||||

| Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | |

| Price | ||||||

| Log horsepower | ||||||

| Log weight | ||||||

| SUV | ||||||

| Diesel | ||||||

| Electric | ||||||

| Hybrid | ||||||

| Adjusted | 0.549 | 0.533 | 0.803 | |||

| # of Month-Years | 120 | 120 | 120 | |||

| # of Obs. | 23,451 | 25,715 | 16,862 | |||

Note: An observation is a pair of where is a car model other than the reference car and is the time period. Standard errors are in parentheses. Brand fixed effects are not reported.

7.4 The Reference Distribution and Scalar Parameters of Interest

We first define the reference distribution and then introduce the scalar parameters of interest. After the first stage estimation, we can calculate up to as:

| (12) |

As we have identified the utility parameters, the potential sensitivity of the empirical results solely arises from the distributional assumption on .

The reference transition of to solve the Bellman equation is an AR(1) process:

| (13) |

where follows an i.i.d. normal distribution with mean 0 and variance .

The parameters are estimated using an iterative procedure. We begin with an initial guess of and circulate between: (i) solving the Bellman equation (9), (ii) recovering from the market share of purchasing (the first part of (10)), (iii) updating by refitting an AR(1) process (13) until we find a fixed point. The reference distribution for is the product of the transition kernel of the estimated AR(1) process and its stationary distribution . The perturbation set is defined as:

We consider two scalar parameters: (i) the industrywide price elasticity of demand, (ii) the welfare analysis of an additional EV subsidy. For both cases, the transition of is unchanged, i.e., we assume consumers’ beliefs about the transition of stay the same.

For industrywide price elasticity at period , we consider a 1% increase in the price of all cars. The future is conditional on:

and the industrywide price elasticity at time is:

where is the model-implied market share of not purchasing.

For EV subsidy at , we consider an additional 3,000 USD subsidy. Denote by the set of EVs at . The future is conditional on:

and the consumer surplus from the subsidy is given by:

where is the market size at time .292929The cost of the subsidy is .

7.5 Sensitivity Analysis

Our framework requires the constraints to be linear in , while the Bellman equation (9) is not. We first reformulate it to fit into our framework. By the Hotz-Miller Inversion Lemma (Hotz and Miller, (1993)), we have:

| (14) |

Taking the log-odds ratio of purchasing and not purchasing, and using (14), we have:

| (15) |

The above constraint is the fixed point problem on the market share space (see Aguirregabiria and Mira, (2002)). The right-hand side is linear in the conditional distribution. The following lemma establishes the relationship between the fixed point problems in (9) and (15).

Assumption 11.

Assume the inclusive value has compact support with nonempty interior equipped with the sup-norm and for any where is the space of continuous functions on .

Lemma 3.

The following holds:

-

(i)

Under Assumption 11, the fixed point problem (9) has a unique solution on .

- (ii)

- (iii)

Lemma 3 shows that solving the Bellman equation (9) is equivalent to solving (15). We further convert (15) into an unconditional moment constraint by assuming that is the solution to (15) if and only if:

| (16) |

Assumption 12.

For , the solution corresponding to (15) satisfies the following: for all , there exists a unique such that .

Assumption 12 allows us to profile out , which is useful for the implementation. A sufficient condition is that is continuous and strictly decreasing, and its smallest and largest values are small and large enough. Under Assumption 11, we have . Moreover, we can expect that a higher inclusive value corresponds to a lower market share of not purchasing, i.e., is decreasing in . Therefore, Assumption 12 is mild.

The last condition is the fixed point constraint similar to the procedure to estimate the AR(1) process. Suppose the distribution is used in (16), and is the sequence of recovered inclusive values. Denote by the estimator of the joint distribution for the pairs . Then, our fixed point constraint is:

where is the tolerance level. To choose , we estimate the joint distribution of inclusive values recovered from the AR(1) process by the kernel density estimator with Gaussian kernel and bandwidth selected by the 5-fold cross-validation. Then, we set to be the KL divergence between the kernel density estimator and the reference distribution.

For EV subsidy, by (14), the consumer surplus (CS) is given by:

where does not depend on . Therefore, to bound CS, it is equivalent to bounding the change in the market share of purchase.

Putting everything together, the lower bound on the elasticity at is given by:

| s.t. | |||

where is replaced by for the EV subsidy case. For , the reference distribution is the unique solution to the above problem. The corresponding elasticity is the reference industrywide elasticity.

7.6 Implementation

We adapt 2 proposed in Section 6.2. We will use numerical integration to discretize the support of the AR(1) process. Therefore, the recovered inclusive values are not differentiable with respect to the discretized market share function . To address this issue, we employ the MCMC optimization method. We alternate between solving the EOT problem to obtain the worst-case distribution, solving the Bellman equation to update , recovering the inclusive values, and checking the fixed point constraint. To derive a tractable dual formulation, we handle the fixed point constraint in a specific way. Because this constraint depends on an estimator, , that changes during optimization—potentially causing numerical instability—we first derive the dual formulation without it.303030In principle, we can choose other constraints like the integral probability metrics and adapt the minimax theorem in Theorem 1. However, such constraints lead to more optimization parameters. Then, the fixed point constraint determines the acceptance/rejection of the candidate parameters in the Metropolis-Hastings step. Consider the following optimization problem:

| s.t. | |||

Applying Theorem 1, its dual is:

| s.t. |

where is the EOT problem: whose cost function is and the worst-case conditional distribution is given by:

where and are the optimal EOT potentials. During the optimization process, is used to update by solving (15) using fixed point iteration.

As shown in Theorem 1, the expectation in the dual is taken with respect to the reference distribution. Therefore, we discretize the estimated AR(1) process, which results in three approximation errors: (i) the Bellman equation is solved on the discretized support, (ii) are recovered approximately, and (iii) the elasticity is computed approximately. That is, we approximate by the market share of the nearest grid point to . Therefore, there is a trade-off between approximation error and computational cost. A finer discretization reduces the approximation error, while increasing the number of optimization parameters.

However, our dual formulation significantly improves computational efficiency. Suppose we discretize the AR(1) process into grid points. If we directly solve (16), the number of optimization parameters is due to the transition matrix. In contrast, the number of optimization parameters is in the dual formulation.

Algorithm 1 summarizes the simulated annealing MCMC optimization algorithm (Kirkpatrick et al., (1983)). It starts with the reference market share , and alternate between proposing new parameters , solving the EOT problem, solving the Bellman equation using the worst-case distribution, and accepting or rejecting the proposed parameters using the Metropolis-Hastings step based on the change in the elasticity penalized by the violation of the market share and fixed-point constraints. At each improvement step, it pools previous results across all radii for initialization. We choose 51 grid points, 5,000 MCMC steps, 5 optimization steps, 14 radii (the last is ), and 100 as the simulated annealing multiplier.

7.7 Results

We estimate two alternative transition density for each market. The first assumes that the inclusive values are i.i.d. normally distributed. The second estimates a nonlinear AR(1) process using a cubic spline313131The nonlinear AR(1) process is specified as: where is the minimum of the discretized support of , is the distance between two adjacent grid points, are parameters to be estimated, and . For this model, we set to avoid overfitting. Then, we discretize the reference AR(1) process into 4 grid points, and compute the KL divergence between the nonlinear AR(1) process and the reference AR(1) process.. In the following figures, we plot the KL divergence between the alternative models and the reference model. The independent model is closer to the reference model with KL divergence between 0.04 to 0.67, while the nonlinear AR(1) process is farther away, with KL divergence between 3.94 to 10.09.

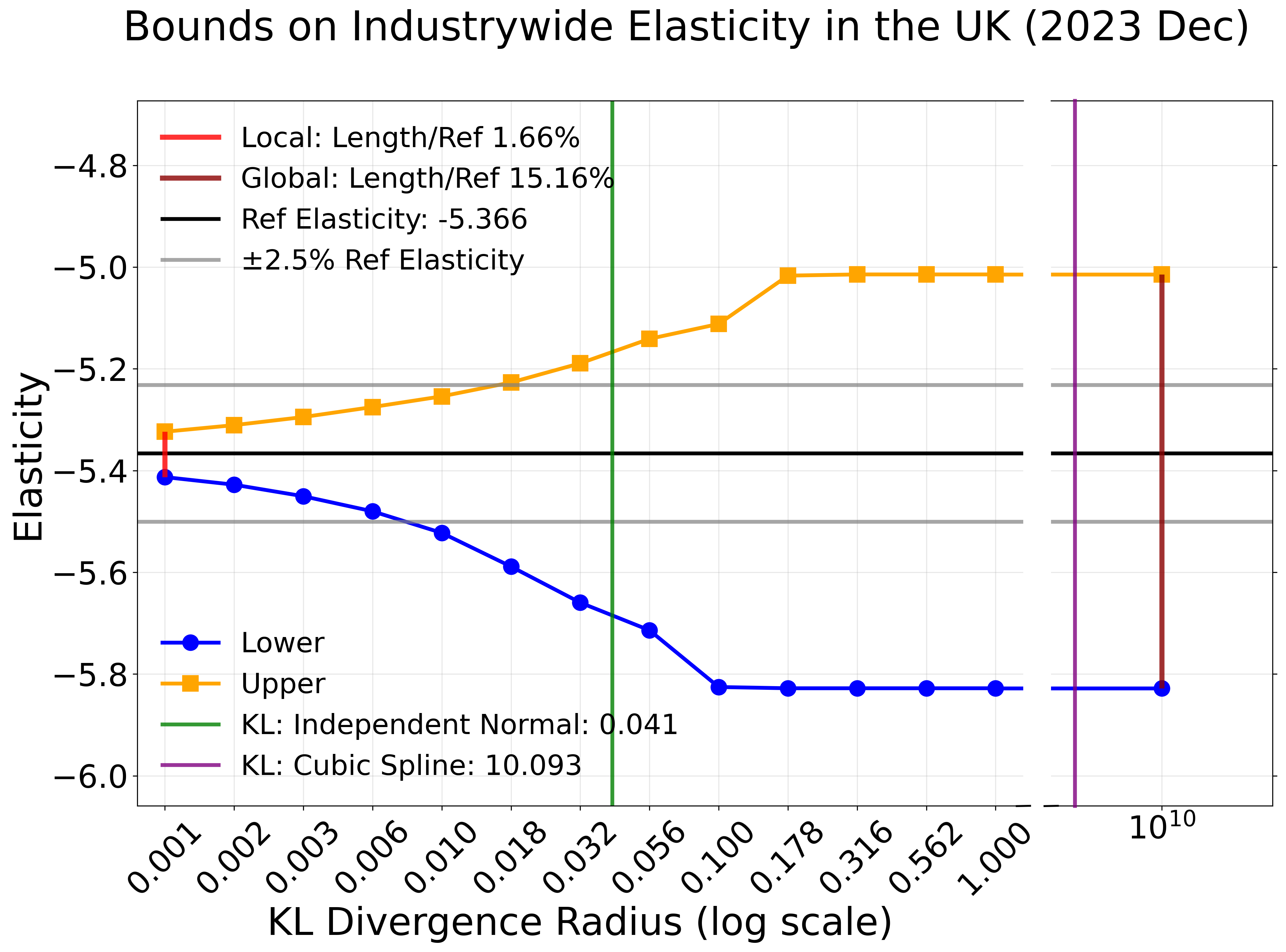

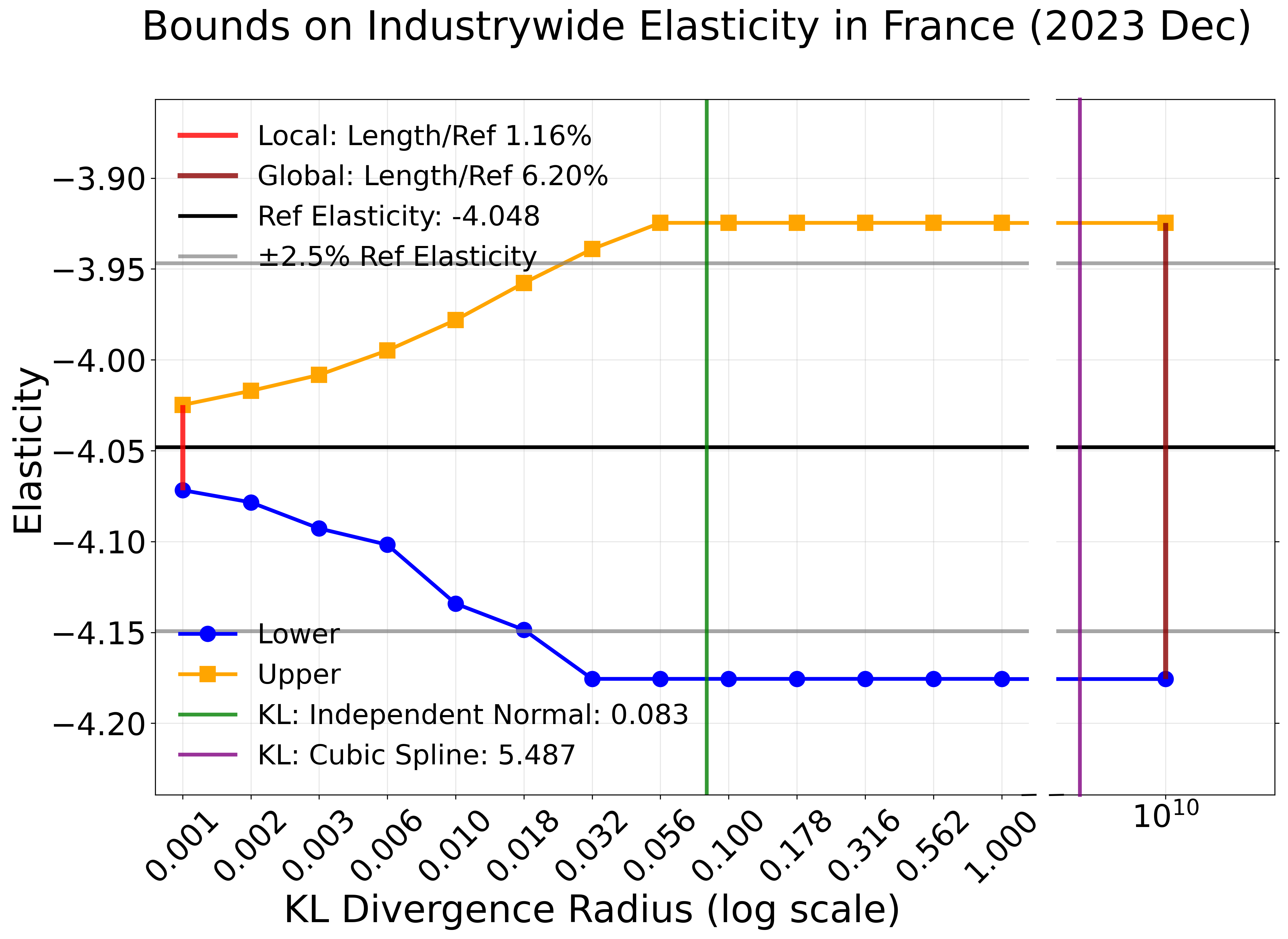

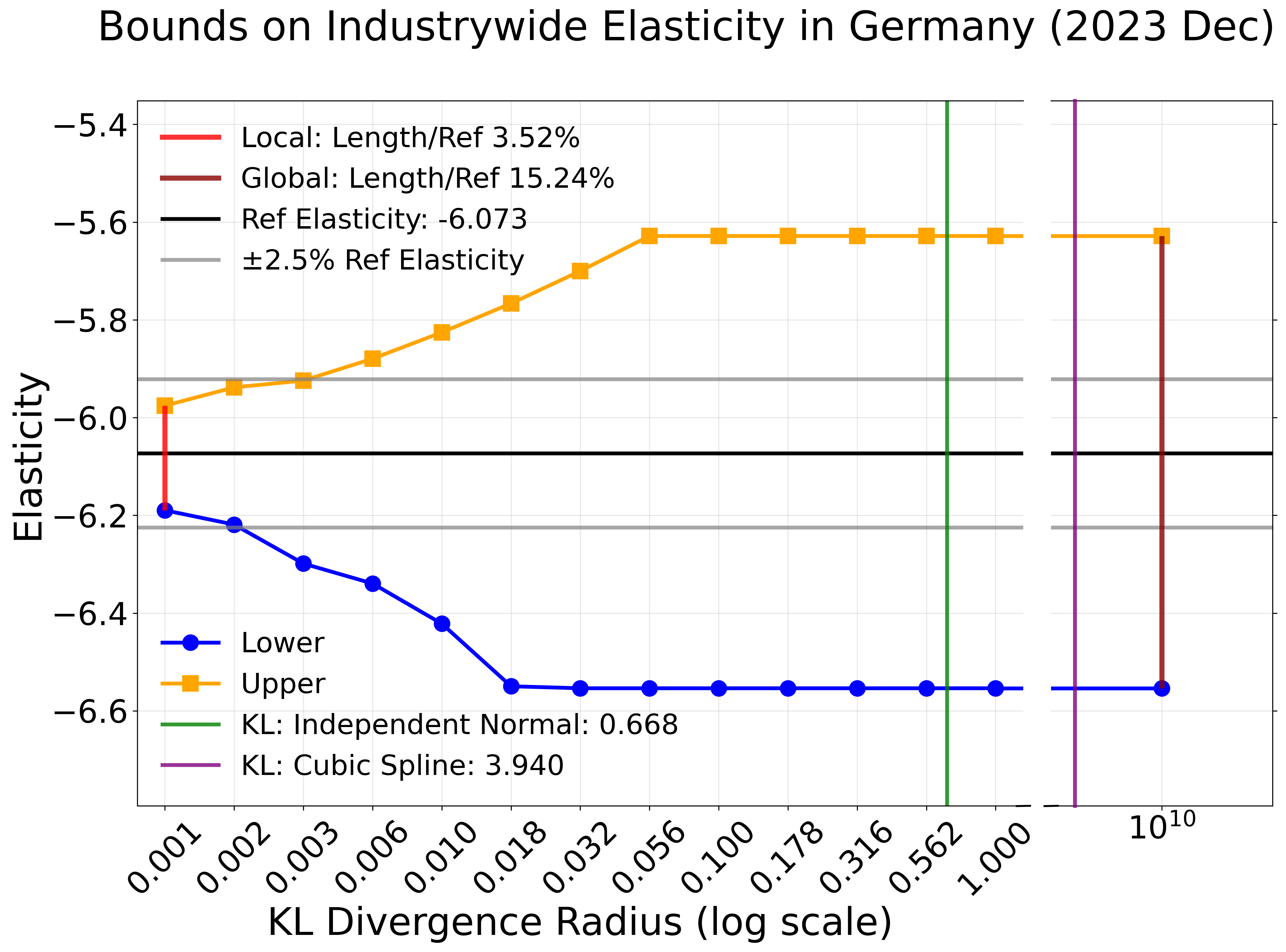

Figures 1-3 plot the bounds on the industrywide elasticities323232Schiraldi, (2011) finds a average long-run price elasticities ranging from -3.54 to -4.34 across different car segments for the Italian market. D’Haultfœuille et al., (2019) reports average elasticities between -3.94 and -6.40 across consumer groups for the French market. Reynaert and Sallee, (2021) finds a mean own-price elasticity of -5.45 for the European market. Grieco et al., (2024) estimates an average elasticity of -5.36 for the U.S. market in 2015. Remmy, (2025) reports a mean price elasticity of -4.043 for the German market. for the UK, Germany, and France in December 2023. French market is the least elastic (reference elasticity: -4.048), while Germany’s is the most elastic (reference elasticity: -6.073). The UK market’s reference elasticity is -5.336. Based on our three sensitivity measures, we define the local (global) sensitivity as the ratio of the local (global) interval length to the reference value. For local sensitivity, we set , while for global sensitivity, we set . The robustness metric is defined as the smallest deviation from the reference distribution such that the elasticity can deviate by, for example, 2.5% from the reference elasticity.

The French market is the least sensitive in terms of local and global sensitivity, with 1.16% local deviation and 6.20% global deviation from the reference elasticity. The UK market is less sensitive locally (1.66%) than the German market (3.52%). They are both more sensitive globally (15.16% for the UK vs. 15.24% for Germany) than the French market. The bounds of UK market flatten around 0.178, while the French and German market flatten around 0.056. For the robustness metric, we consider 2.5% deviation from the reference elasticity. The UK market’s robustness metric is around 0.018 for the upper bound and 0.008 for the lower bound. The French market’s robustness metric is around 0.025 for the upper bound and 0.018 for the lower bound. The German market’s robustness metric is around 0.002 for the lower bound and 0.003 for the upper bound. Therefore, in terms of robustness metric, the French market is also the most robust, while the German market is the least robust.

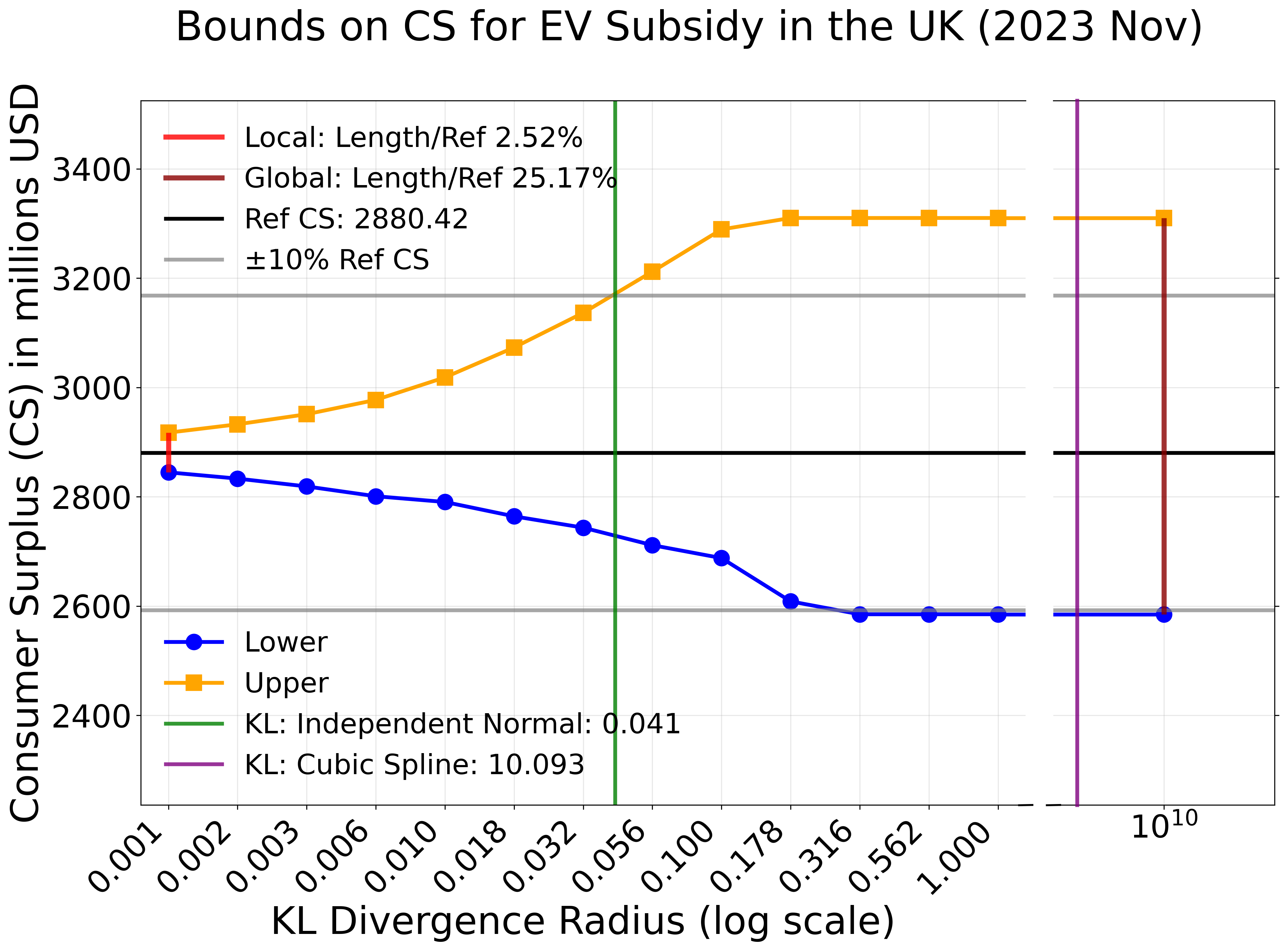

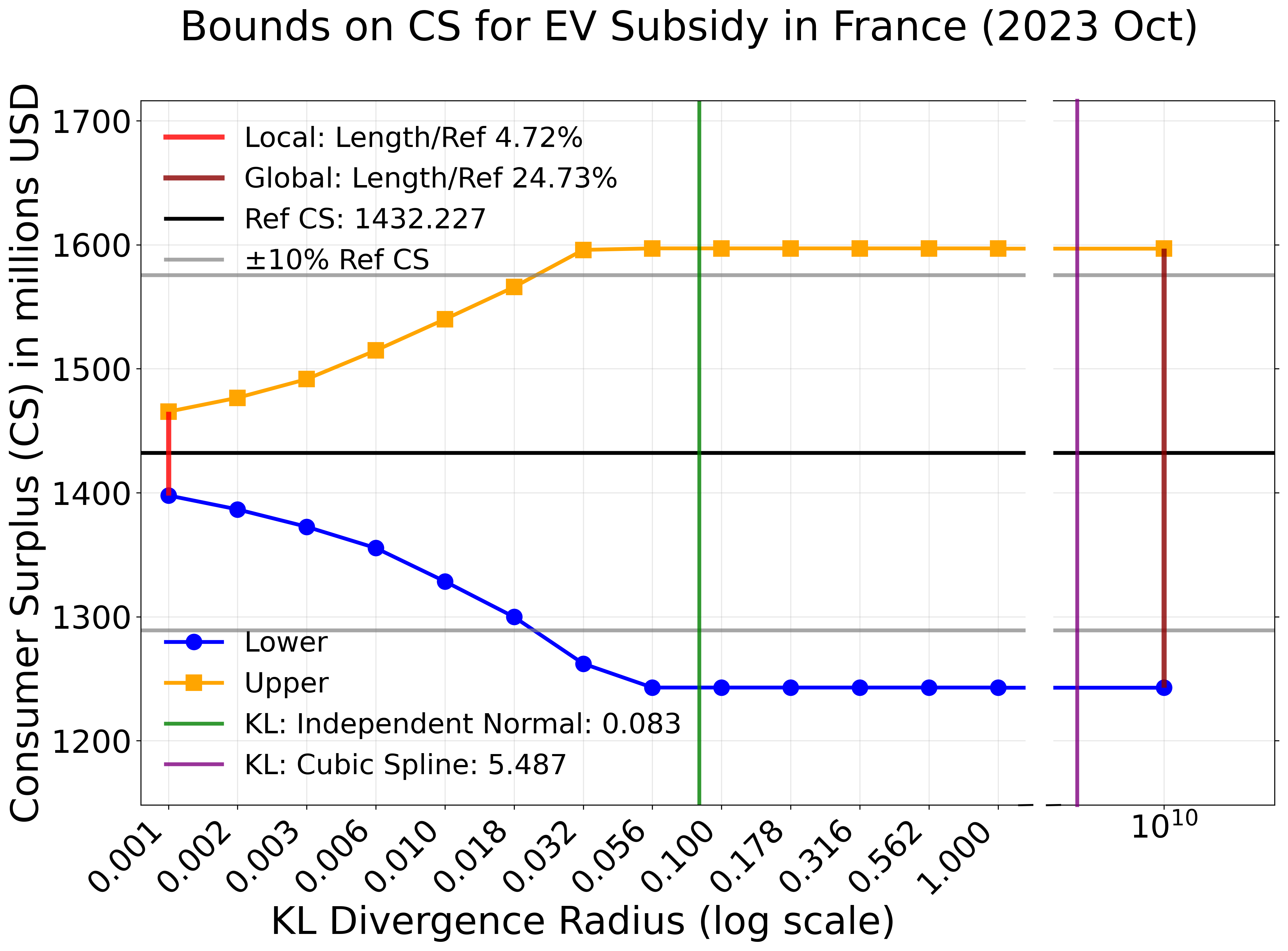

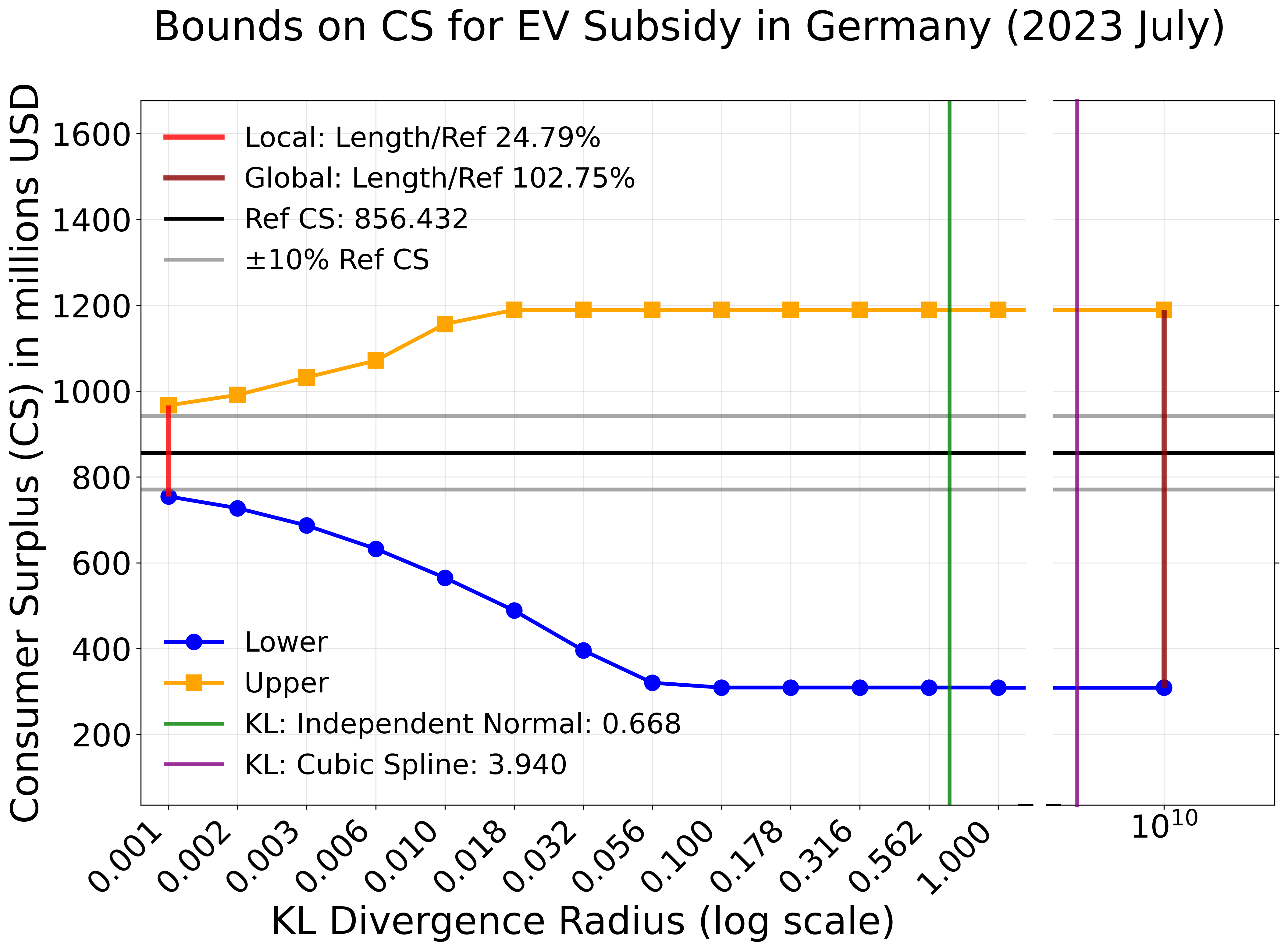

Figures 1-3 also plot the bounds on the consumer surplus from an additional $3,000 EV subsidy. The subsidy is implemented between July and December 2023, when the reference consumer surplus is maximized. They are November for the UK (reference CS: $2,880 million), October for France (reference CS: $1,432 million), and September for Germany (reference CS: $856 million). Overall, the EV subsidy is beneficial as the lower bounds are $2,584 million for the UK, $1,243 million for France, and $309 million for Germany. The corresponding costs for subsidy are around $12 million for the UK, $23 million for France, and $41 million for Germany. The costs are insensitive to the misspecification, as they only depend on the absolute change in the market share of purchases, and the conditional market share of EVs, instead of percentage change used for consumer surplus.