Non-Parametric Estimation Techniques of Factor Copula Model using Proxies

Abstract

Parametric factor copula models typically work well in modeling multivariate dependencies due to their flexibility and ability to capture complex dependency structures. However, accurately estimating the linking copulas within these models remains challenging, especially when working with high-dimensional data. This paper proposes a novel approach for estimating linking copulas based on a non-parametric kernel estimator. Unlike conventional parametric methods, our approach utilizes the flexibility of kernel density estimation to capture the underlying dependencies more accurately, particularly in scenarios where the underlying copula structure is complex or unknown. We show that the proposed estimator is consistent under mild conditions and demonstrate its effectiveness through extensive simulation studies. Our findings suggest that the proposed approach offers a promising avenue for modeling multivariate dependencies, particularly in applications requiring robust and efficient estimation of copula-based models.

Keywords: Factor copula, Non-parametric estimation, Proxy variables, Tail dependence

1 Introduction

Factor copula models provide a flexible yet concise framework, assuming that variables become independent when conditioned on one or more unobserved common factors. The general class of factor copula models proposed by Krupskii and Joe, (2013), which is an extension of classical Gaussian factor models, explains the dependence structure of high dimensional variables in terms of a few latent variables. Krupskii and Joe, (2015) extended their approach to model dependence when the observed variables belong to several non-overlapping groups with homogeneous dependence in each group.

Factor copulas have demonstrated their ability to capture both the correlations and dependence in the joint tails, thanks to the flexibility of copula functions. Since introducing the Gaussian factor copula model by Hull and White, (2004), factor copulas have been further developed to account for various data characteristics. For instance, Chen et al., (2015) employed factor copulas to examine the mortality dependence of multiple populations and factor copulas have also been used to study the behavior dependence of item responses in Nikoloulopoulos and Joe, (2015). In Oh and Patton, (2017), it is shown that a linear factor copula model, as a particular case of factor models, can be used to capture dependence between economic variables while the properties of these models and their extreme-value limits are studied by Krupskii et al., (2018). Financial time series can significantly benefit from the factor copula models as they provide a superior fit compared to truncated vines (Brechmann et al., (2012)) and classical Gaussian factor models, especially when utilizing stock returns from the same industry sector.

In parametric factor copula models, the choice of bivariate linking copulas is of interest to define appropriately the dependence structure between observed and latent variables. To deal with this, various diagnostic tools have been proposed; see Krupskii and Genton, (2017), which used bivariate normal score plots of the observed data or measures of tail asymmetry. Bayesian inference was used by Nguyen et al., (2019) as an alternative approach, but it is computationally demanding. Krupskii and Joe, (2022) showed how the use of proxies for estimating latent variables in factor copula models can aid in selecting bivariate copula families, while Fan and Joe, (2023) extended their work to bi-factor and other structured -factor copulas using two-stage proxies.

Parametric models for linking copulas are frequently utilized, but they can lead to incorrect specifications and inconsistencies in estimators. The most common parametric estimation methods include maximum likelihood employing a two-stage procedure, as demonstrated in Ko and Hjort, (2019), or penalized likelihood, as illustrated in Qu and Yin, (2012) and more recently applied to Archimax copulas according to Chatelain et al., (2020). However, these methods can be restricted by the number of parameters and may only be suitable for copulas that conform to the widely used parametric families. In contrast to traditional estimation techniques, non-parametric estimation does not assume that data are drawn from a known distribution. Instead, non-parametric models determine the model structure from the underlying data. These methods provide a more flexible alternative with several different approaches, such as deep learning theory Liu et al., (2024), kernel estimators Nagler and Czado, (2016); Wang et al., (2023); Modak, (2023), B-spline estimators Kauermann et al., (2013); Kirkby et al., (2023), Bernstein polynomials Bouezmarni et al., (2010, 2013); Kiriliouk et al., (2018), linear wavelet estimators Genest et al., (2009); Ghanbari et al., (2019), nonlinear wavelet estimators Autin et al., (2010); Ghanbari and Shirazi, (2023), or Legendre multiwavelet estimators Chatrabgoun et al., (2017).

Non-parametric kernel methods are a class of statistical techniques widely employed in data analysis and machine learning, offering flexible and versatile solutions particularly suitable for situations where underlying data distributions are not well-known or may deviate from parametric assumptions. Jin et al., (2021) proposed an improved kernel density estimation based on regularization term. He et al., (2021) studied a novel kernel density estimator to determine the expectation of an estimated PDF using an ensemble of data depending on unbiased cross-validation. These methods avoid explicit functional form assumptions and instead rely on local information around data points to make inferences. Central to these approaches are kernel functions, which efficiently capture local patterns and relationships within the data. Typical applications of non-parametric kernel methods include density estimation, regression analysis, and classification tasks. In kernel density estimation, these methods allow for constructing smooth and continuous probability density functions without imposing rigid distributional assumptions. Moreover, non-parametric kernel regression methods enable the modeling of complex relationships between variables by incorporating local weighted averages. The adaptability and resilience to diverse data structures make non-parametric kernel methods valuable in various scientific disciplines, offering practical solutions for analyzing and understanding complex datasets without requiring restrictive parametric assumptions.

The use of kernel methods in analyzing high-dimensional datasets has gained increasing attention from researchers and practitioners due to the complex datasets characterized by numerous variables. Traditional parametric methods often need help with challenges such as the curse of dimensionality and the risk of model overfitting in high-dimensional spaces Scott, (1992); Bellman, (2003). Kernel methods provide a valuable alternative by implicitly mapping the data into a higher-dimensional space using kernel functions. This transformation captures intricate relationships among variables, facilitating the extraction of meaningful patterns in high-dimensional data. For example, Support Vector Machines (SVMs) equipped with kernel functions have been proven effective in classification tasks where the number of features significantly exceeds the number of observations Sánchez, (2003). Additionally, kernel principal component analysis enables dimensionality reduction while preserving the non-linear structures inherent in the data. Recent research has also focused on developing novel kernel functions specifically tailored to address the challenges posed by high-dimensional datasets, enhancing the adaptability and performance of kernel methods in this context Liu et al., (2021).

Although the kernel estimators are widely utilized for estimating general densities, to our knowledge, our work is the first to apply these estimators to estimate the factor copula density. Inspired by the technique proposed by Nagler and Czado, (2016) for linking copulas within vine copula models to overcome the curse of dimensionality, we introduce a novel non-parametric kernel-based method for estimating linking copulas in one-factor copula models. Our analysis focuses explicitly on its computational complexity in the presence of a single latent variable and studies the asymptotic properties of the estimator which uses proxy methods to estimate the unobserved latent variable. Our method is beneficial when the factor copula model and the linking copulas must be correctly specified. This alternative approach enables the selection of suitable linking copulas necessary for modeling dependency when the common factor drives the dependence among observed variables.

The remainder of this paper is structured as follows. In Section 2 we review the class of one-factor copula models, introduce the proposed kernel estimator, and study its asymptotic properties. In Section 3, we evaluate the performance of the proposed method through an extensive simulation study. In Section 4, we use the proposed methodology for the analysis of financial stock returns data, and Section 5 concludes the paper with a discussion of the findings and potential directions for future research. Lastly, the proof of the theoretical results is provided in the Appendix.

2 Methodology

Both parsimonious and flexible-factor copula models can handle the dependence between the observed variables based on a few unobserved (latent) variables. These models are particularly useful when tail asymmetry or dependence is observed in multivariate data, so the standard models based on the multivariate normality assumption are unsuitable. Recently, Oh and Patton, (2017); Krupskii and Joe, (2013) proposed factor copula models, which overcome some disadvantages of traditional copulas and are more flexible than the classical Gaussian factor models. The first approach combines the class of dynamic factor models commonly used in time series analysis with arbitrary marginal distributions. However, this approach restricts the choice of copula functions to certain extensions of elliptical distributions, such as the Student’s- and skew Student’s- copulas.

Alternatively, the second model assumes that the dependence among observed variables can be captured using a multivariate factor copula model. In this framework, it is assumed that the dependence structure arises from a set of latent factors . A common approach is to transform the observed variables into uniform random variables , where each . The transformed variables satisfy , where is the marginal cumulative distribution function (CDF) of . The dependence among these variables is captured by a copula function , which allows for a flexible representation of a complex dependence structure.

In this paper, we focus on the one-factor copula model, where a single latent factor drives the dependence among observable variables. This structure strikes a balance between simplicity and flexibility, making it particularly suitable for high-dimensional datasets. Specifically, we estimate the one-factor copula model non-parametrically using a kernel estimation technique, allowing for greater flexibility in capturing complex dependence structures without restrictive parametric assumptions.

2.1 One-factor copula models

The one-factor copula model provides a flexible framework for capturing dependence among multiple variables while maintaining computational tractability Krupskii and Joe, (2013). In this model, we consider observable variables , each following a uniform distribution on . These variables are assumed to be conditionally independent given an underlying latent factor , which follows a uniform distribution: .

To describe the dependence structure between each and the latent factor , we introduce the bivariate copula density and their CDFs . Under the one-factor framework, the joint CDF of can be expressed as:

| (1) |

Here is defined as the conditional CDF of given .

Let us denote the partial derivative . Note that . As shown in Krupskii and Joe, (2013), the copula density for the one-factor copula model is:

| (2) |

The factor copula models have become increasingly popular in recent years due to their ability to account for dependencies among the observed variables. However, these dependencies are mostly determined by the unobserved common factors, referred to as latent variables. Consequently, estimating these latent variables can help select appropriate bivariate linking copulas or accurately estimate them.

To achieve that, Krupskii and Joe, (2022) proposed a new proxy method that uses the unweighted averages computed from the observed variables . Denote and . To construct the proxy for , we first compute the average of the transformed variables as follows:

| (3) |

Then, we compute , where is the empirical CDF of . This step transforms to the uniform scale. Finally the proxy for is obtained by applying the inverse normal CDF, . This transformation ensures that is approximately normally distributed. To use the proxy method in Krupskii and Joe, (2022), it is required that the bivariate linking copulas have monotonic dependence (in particular, stochastically increasing copulas satisfy this requirement), implying that the observed variables are monotonically related to the latent variable, which is not a very restrictive assumption in many applications.

2.2 Proposed non-parametric estimator

We develop the non-parametric estimator of the one-factor copula density, which involves the kernel estimation of the bivariate linking copulas. The primary challenge here is estimating the linking copulas in the presence of a latent variable. To address this, we initially apply the proxy method introduced by Krupskii and Joe, (2022) to estimate the latent variable, followed by the kernel method to estimate the linking copulas.

The idea behind estimating the factor copula density function in (2) is to estimate each bivariate linking copula density individually while taking into consideration that there is a key distinction between this approach and typical kernel estimation techniques that have been extensively studied in the literature. The key distinction of this approach compared to conventional kernel estimation techniques lies in its consideration of a latent variable. Unlike standard kernel estimation methods, which typically estimate density functions directly from observable data, the proposed procedure accounts for the dependence structure induced by an unobservable (latent) factor. We employ a step-wise estimation procedure to systematically detail our non-parametric estimator’s construction.

-

•

Transform observed data into uniform variables : Assume that is a random vector with the joint cdf and marginal cdfs . We obtain the estimates of the respective marginal CDFs based on all observations () for . Let be the kernel estimator of , , which is defined in Nagler et al., (2017):

(4) where for all , and is a kernel function with the bandwidth that satisfy the following conditions:

-

–

C1: is a symmetric density function supported on and has continuous first-order derivative.

-

–

C2: and as .

To estimate the latent variable and linking copula densities, we need data on scale, i.e., the random vector . In practice, we do not have access to observations from this vector; instead, we can use pseudo-observations by replacing with their estimators:

(5) -

–

-

•

Estimating the latent factor : Utilizing the full dataset in (5) with variables, we first compute the proxy as defined in (3). To do that, we need to compute where is the empirical CDF of . We then use this proxy (the estimated latent variable) to estimate the density of the copula linking variables denoted (without loss of generality, we can assume these are the first variables).

Copula densities are supported on the unit hypercube, which necessitates careful consideration during estimation. Only a few kernel estimators are suitable for addressing bias and consistency issues that arise at the boundaries of the support. To overcome these challenges and be able to estimate the -dimensional marginal copula density , represented as the product of the bivariate linking copulas in the presence of a latent variable, we employ the techniques of the transformation estimator presented in Nagler et al., (2017), which transforms the data into standard normal margins, thereby enabling unbounded support. Assume is the standard Gaussian distribution function, while and are its density and quantile functions, respectively. According to Sklar, (1959), The joint density of variables , can be expressed in terms of the respective copula density and marginal densities as:

(6) Changing variables , we get

(7) Using a kernel estimator of defined as

we obtain from (7) the kernel estimator of the copula density as follows:

(8) The copula density can take infinite values at the boundaries of the support. To avoid the variance of the estimator defined in (8) from exploding, we therefore constrain the estimator to pairs .

-

•

Estimating the linking copula densities : We follow a few steps to develop the kernel estimator for the bivariate linking copula density function. These steps build on the notation introduced in Section 2.1 and incrementally refine the estimator to handle practical challenges. First, inspiring (8), we define the estimator of the linking copula density provided that is observed as follows:

(9) Here, is a kernel estimator of under the idealized scenario where the latent variable is directly observable. Next, recognizing that the latent variable is unobservable in practice, we approximate it using the proxy variable defined in (3). Incorporating this proxy variable, we redefine the estimator as:

(10) where , , and is positive definite bandwidth matrix with parameters .

We further refine the estimator to address the practical scenario where pseudo-observations are used to estimate unobservable quantities. Using pseudo-observations defined as in (5), the kernel estimator of the linking copula density becomes:

(11) The estimator incorporates observed data, providing a practical approximation for the linking copula density.

-

•

Estimating of one-factor copula density: Following the steps from equation (9) to (11), we propose our novel kernel estimator for the one-factor copula density . This estimator is obtained by integrating the product of the first estimated linking copula densities over the latent variable:

(12) This integral combines the contributions of all individuals linking copula densities to provide a comprehensive estimate of the one-factor copula density.

2.3 Asymptotic properties

In this section, we establish the asymptotic properties and convergence rate of the estimator proposed in Section 2.2, along with the necessary assumptions to ensure consistency. Recall that the variables are assumed to be conditionally independent given an underlying latent factor , which follows a uniform distribution: and also assume where the is the inverse normal CDF.

Assumption 2.1

Let be the non-parametric estimator of a distribution function , then the following conditions hold:

-

•

(a) For and with be the support of ,

-

•

(b) For

-

•

(c) For all

where , assuming that the copula densities are times continuously differentiable on .

Remark 2.1

While conditions (a) and (c) are standard and are satisfied for most nonparametric estimators of the marginal CDFs and copula densities , condition (b) requires stochastically increasing copulas with for some constant and all , and it follows from the conditional independence of the observed variables and the uniform upper bound of error for the normal probability approximation Chernozhukov et al., (2017); Koike, (2021) provided that :

where , and , where is a monotonically increasing function of for stochastically increasing linking copulas . This implies that

and hence

where , where and is the CDF and empirical CDF of , respectively.

Proposition 2.1

The proof is given in the Appendix 6.1.

Theorem 2.1

The proof is deferred to Appendix 6.1.

Remark 2.2

In deriving the results presented above, we consider the full dataset, allowing , to estimate the latent variable. However, for the copula density estimation, we focus on a finite-dimensional marginal density corresponding to the first variables. It is important to note that the consistency and asymptotic properties of the copula density estimator are derived under the condition that is fixed and . This approach ensures that the latent variable estimation benefits from the complete dataset, while the copula density estimation is confined to the selected -dimensional marginal.

Remark 2.3

The consistency of the proposed estimator is achieved if and which requires a large . In many practical applications, the number of observed variables is often much smaller than the sample size, but we show in the next section that the proposed approach yields accurate estimates of the copula density even if is not very large.

3 Simulation Study

This section illustrates the finite sample performance of the proposed kernel estimator of a one-factor copula density, highlighting its advantages over traditional kernel-based methods. Section (3.1) explores techniques of numerical implementation for efficiently computing the proposed model estimator, with the simulation results detailed in Section 3.2.

3.1 Simulation implementation

We conducted the analysis using the R 4.2.3 statistical computing environment R Core Team, (2023). The estimation approach followed the procedures outlined in Section 2.2. The marginal distributions are estimated using the standard kernel density estimator (4) with bandwidth selection using the methods implemented in the ks package (function hpi) and the guidelines provided by Duong, (2014). Subsequently, the linking copula densities are estimated using transformation estimators (9), (10), and (11), inspired by the kdecopula package proposed by Nagler, (2016).

In the final step, we used numerical integration to compute the one-factor copula density estimator as given in (12). For the classical kernel estimator of the one-factor copula density (denoted as , referred to as the naive estimator), we utilized the kde function from the ks package Duong, (2014). This estimator was applied directly to the observed data without accounting for the factor structure. Bandwidth selection for this approach followed the plug-in method by Chac´on and Duong, (2010).

To evaluate the performance of our estimator , defined in (12), and the naive estimator , we employed four metrics: root mean squared error (RMSE), mean absolute error (MAE), standard deviation (SD), and bias. We considered the sample sizes and of observed variables used to compute the proxy to the unobserved factor. The analysis proceeded as follows:

-

1.

Simulate a sample of size from a -dimensional one-factor copula model (2), considering two scenarios for all bivariate linking copulas:

-

•

Gumbel copula with parameter .

-

•

Clayton copula with parameter .

-

•

-

2.

Estimate the latent variable based on the observed variables. Use this estimate to compute all the bivariate linking copulas in (12) and the copula density linking the first variables. Numerical integration was then applied to compute the one-factor copula density (12). Results are compared with the naive estimator obtained via the kde package.

-

3.

Repeat the above steps 1000 times, calculating the RMSE, MAE, SD, and bias for both estimators across 1000 simulations.

3.2 Simulation results

Tables 1-4 show the simulation results. It is seen that the RMSEs and the other three performance metrics improve for the proposed estimator for larger values of and . It is also evident that the proposed estimator significantly outperforms the naive estimator, demonstrating its superior accuracy in estimating the one-factor copula density.

| Estimator | RMSE | MAE | SD | BIAS | ||

|---|---|---|---|---|---|---|

| Naive | 0.494 | 0.866 | 0.245 | |||

| One-Factor | 0.152 | 0.119 | 0.088 | |||

| One-Factor | 0.139 | 0.108 | 0.083 | |||

| One-Factor | 0.134 | 0.105 | 0.079 | |||

| Naive | 0.365 | 0.322 | 0.147 | |||

| One-Factor | 0.074 | 0.058 | 0.041 | |||

| One-Factor | 0.070 | 0.056 | 0.038 | |||

| One-Factor | 0.069 | 0.055 | 0.038 | |||

| Naive | 0.349 | 0.306 | 0.112 | |||

| One-Factor | 0.059 | 0.047 | 0.033 | |||

| One-Factor | 0.057 | 0.046 | 0.032 | |||

| One-Factor | 0.054 | 0.044 | 0.030 |

| Estimator | RMSE | MAE | SD | BIAS | ||

|---|---|---|---|---|---|---|

| Naive | 1.793 | 0.984 | 1.29 | |||

| One-Factor | 0.378 | 0.214 | 0.248 | |||

| One-Factor | 0.323 | 0.192 | 0.197 | |||

| One-Factor | 0.320 | 0.190 | 0.182 | |||

| Naive | 1.047 | 0.703 | 0.353 | |||

| One-Factor | 0.174 | 0.109 | 0.073 | |||

| One-Factor | 0.171 | 0.105 | 0.071 | |||

| One-Factor | 0.164 | 0.099 | 0.070 | |||

| Naive | 0.917 | 0.684 | 0.286 | |||

| One-Factor | 0.121 | 0.075 | 0.069 | |||

| One-Factor | 0.115 | 0.064 | 0.055 | |||

| One-Factor | 0.146 | 0.093 | 0.056 |

| Estimator | RMSE | MAE | SD | BIAS | ||

|---|---|---|---|---|---|---|

| Naive | 0.600 | 0.468 | 0.212 | |||

| One-Factor | 0.127 | 0.109 | 0.084 | |||

| One-Factor | 0.121 | 0.103 | 0.081 | |||

| One-Factor | 0.116 | 0.101 | 0.079 | |||

| Naive | 0.522 | 0.430 | 0.122 | |||

| One-Factor | 0.107 | 0.125 | 0.094 | |||

| One-Factor | 0.106 | 0.124 | 0.092 | |||

| One-Factor | 0.104 | 0.121 | 0.091 | |||

| Naive | 0.431 | 0.302 | 0.107 | |||

| One-Factor | 0.078 | 0.061 | 0.069 | |||

| One-Factor | 0.078 | 0.060 | 0.070 | |||

| One-Factor | 0.073 | 0.065 | 0.064 |

| Estimator | RMSE | MAE | SD | BIAS | ||

|---|---|---|---|---|---|---|

| Naive | 1.858 | 0.909 | 1.157 | |||

| One-Factor | 0.478 | 0.309 | 0.219 | |||

| One-Factor | 0.447 | 0.291 | 0.200 | |||

| One-Factor | 0.453 | 0.292 | 0.207 | |||

| Naive | 1.016 | 0.657 | 0.464 | |||

| One-Factor | 0.296 | 0.197 | 0.126 | |||

| One-Factor | 0.285 | 0.190 | 0.121 | |||

| One-Factor | 0.280 | 0.187 | 0.119 | |||

| Naive | 0.785 | 0.560 | 0.269 | |||

| One-Factor | 0.275 | 0.190 | 0.106 | |||

| One-Factor | 0.261 | 0.179 | 0.102 | |||

| One-Factor | 0.263 | 0.182 | 0.101 |

4 Empirical study

In this section, we apply the proposed methodology to analyze financial data. The dataset comprises S&P 500 daily stock returns from the Industrials Sector. It consists of a total of stocks with the following tickers: AXON, BA, GE, GD, HWM, HII, LHX, LMT, NOC, RTX, TXT, TDG, DOV, FTV, IEX, HUBB, ITW, NDSN, PH, PNR, SNA, SWK, GWW, XYL, AOS, ALLE, BLDR, JCI, Mas, TT, CAT, CMI, PCAR, WAB, J, PWR, AME, ETN, EMR, GNRC, ROK. The stock returns are observed from January 2, 2017, to July 31, 2024, spanning a sample size of days.

To address serial autocorrelation, we employ an AR(1)–GARCH(1,1) model featuring symmetric Student’s- innovations to model univariate marginals for log-returns where is the th stock price at time :

The error terms, denoted as , are independently and identically (i.i.d.) -distributed with degrees of freedom for the th stock. We used the Ljung–Box test to assess whether the fitted residuals are uncorrelated. The model standardized residuals are then transformed to uniform scores .

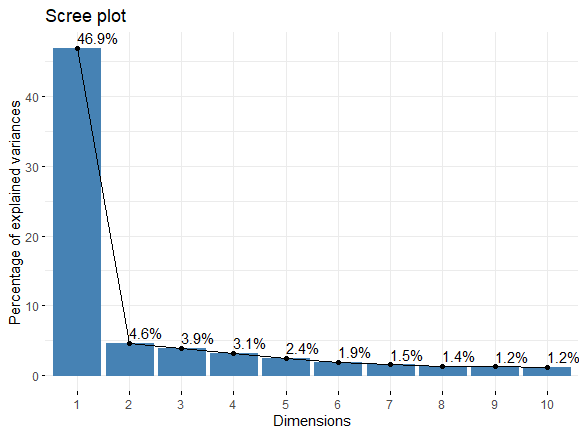

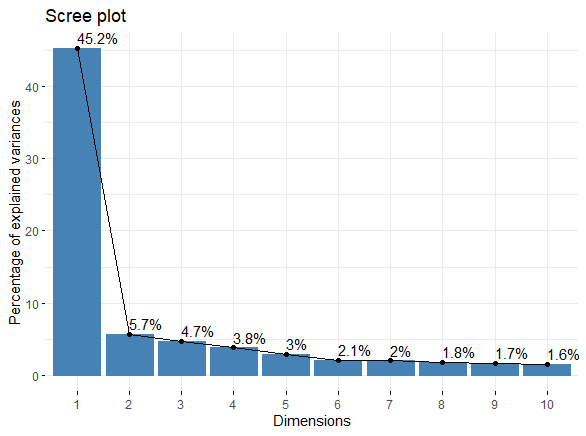

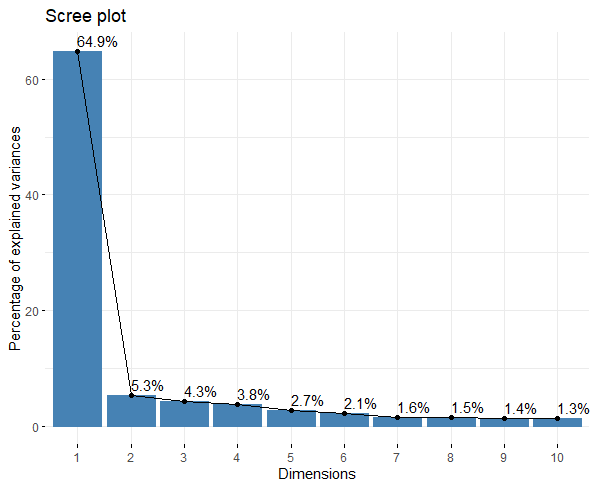

In the subsequent discussion in Section 2.4 of Oh and Patton, (2017) which is inspired by Cattell, (1966), it is shown that, subject to certain regularity conditions, it is possible to determine the optimal number of factors by examining a scree plot based on the eigenvalues of the rank correlation matrix. Figure (1) shows the scree plot for the standardized residuals. The results indicate that a single factor effectively accounts for the dominant variance in the data.

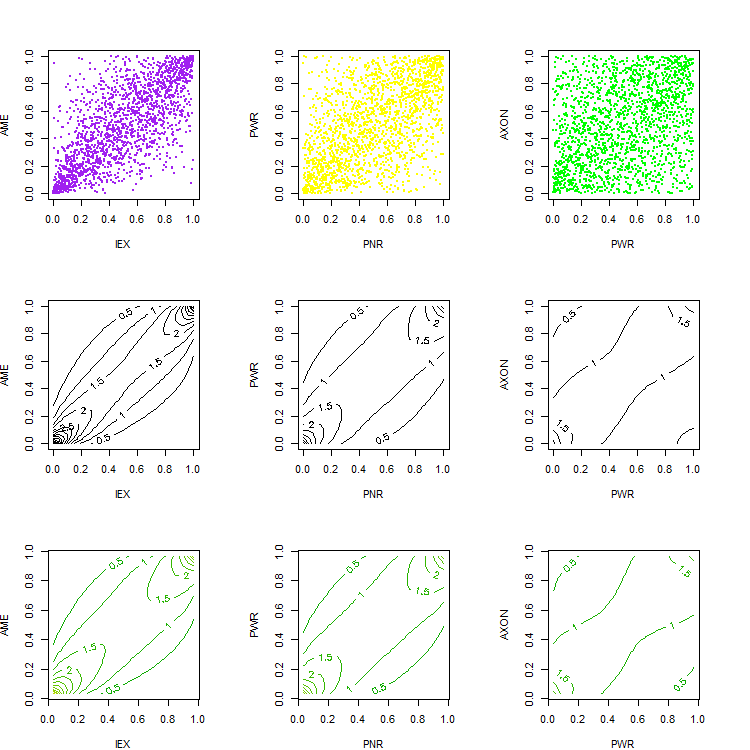

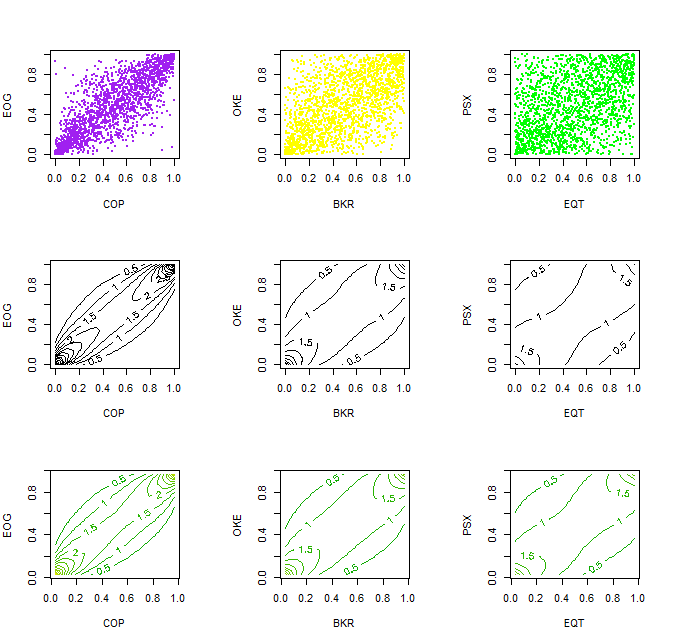

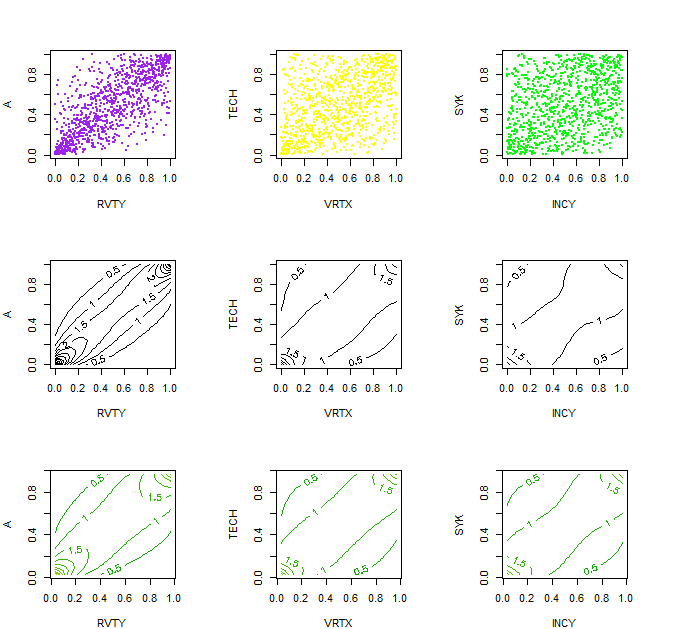

To evaluate the performance of our estimator, we apply the proposed estimator and classical bivariate copula estimator Nagler, 016b to each pair of the residuals transformed to the scale. We use the bivariate copula estimator as a benchmark since it does not rely on any assumptions (including a factor structure) and performs very well for bivariate data sets. Figure (2) shows scatter plots and estimated contour plots of the copula density linking some pairs of variables. In the figure, the columns (from left to right) show the results for pairs with strong, moderate, and weak dependence, while the rows show scatter plots (top row), the bivariate copula density estimates using the classical copula estimator (middle row), and the proposed one-factor copula density estimator (bottom row).

The results demonstrate that our estimator and the copula estimator yield very similar results for bivariate marginals. To quantify the difference between the two estimators, we use the root mean squared difference (RMSD) for each sample between our proposed estimator and the true one-factor copula model, as well as between the classical bivariate copula density estimator and the true model, as follows:

| (15) |

where is either (our proposed estimator based on equation (12) in bivariate case ) or (the classical bivariate copula estimator in Nagler, 016b ) and is the true one-factor copula (2) in bivariate case (when the dimension is ). In the bivariate case, we consider all unique pairs of stocks from the Industrial Sector, where each pair corresponds to a distinct combination of two variables among the stocks. We compute the RMSD for each of these pairs. The value of , averaged over all pairs of stocks, is 0.08, which shows that the two estimators are almost identical.

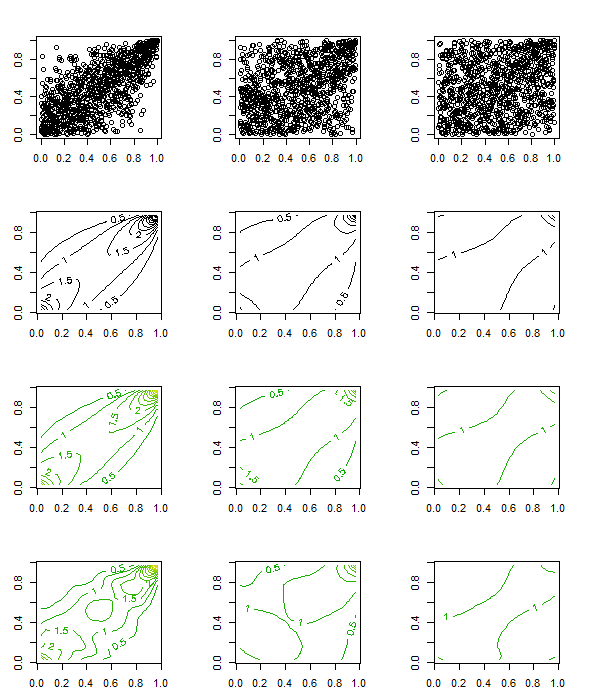

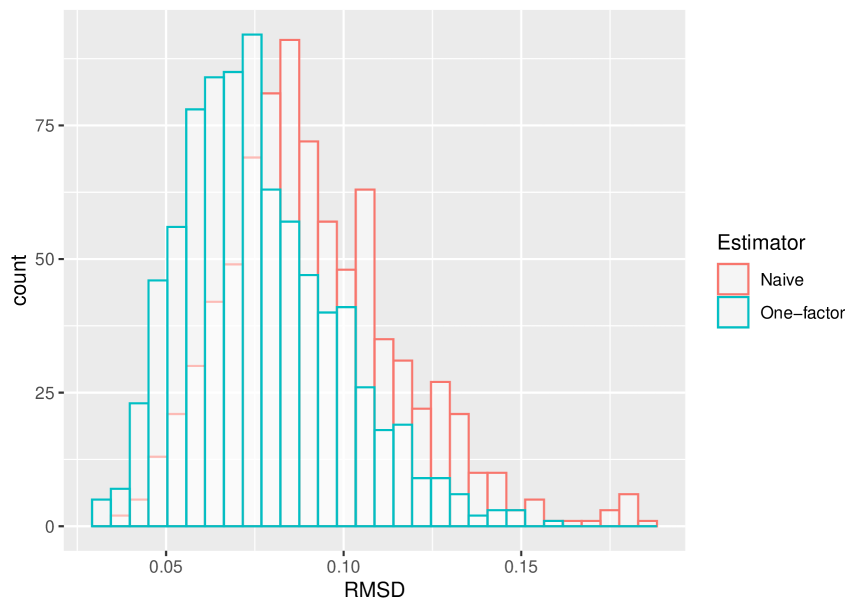

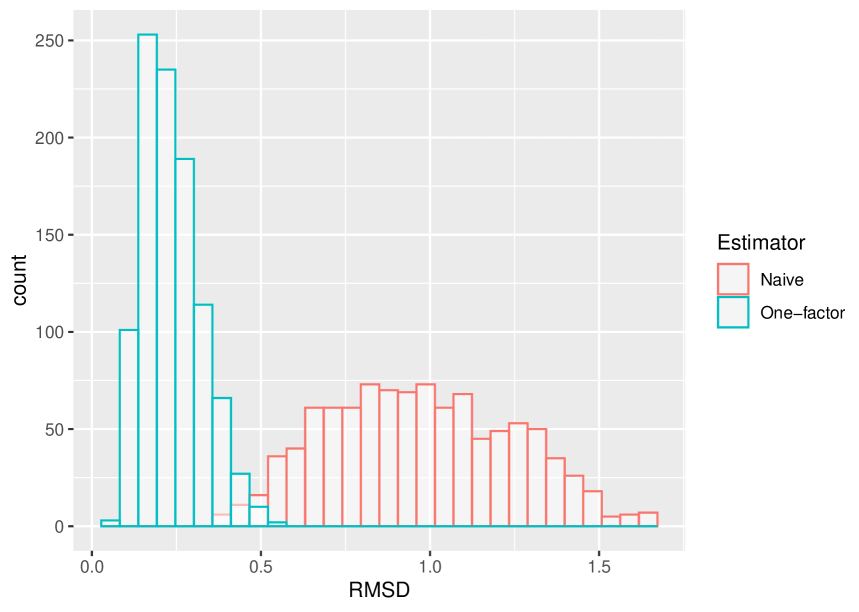

Furthermore, we fitted several parametric one-factor copula models to the dataset comprising 41 stocks from the Industrial Sector. The best-fitting model was identified using the Bayesian Information Criterion (BIC), which selected the model with the Gumbel linking copulas. Assuming this is the true model for the standardized residuals, we generated a synthetic data set of a sample of size 1000 from this model and repeated the above steps for the simulated data set. Namely, we applied our proposed estimator and the classical copula estimator to each pair of variables from the simulated data set. To evaluate the performance of the two estimators, we constructed contour plots of the estimated copula densities; Figure (3) shows results for some pairs of variables, and Figure (4) shows the histogram of RMSDs between each of the two estimators and the true copula density, computed for different pairs of variables from the generated data set using the classical (red) and proposed estimators (blue). These results clearly show that our estimator outperforms the classical estimator when the data come from the one-factor model.

To evaluate the performance of our estimator in higher dimensions, we randomly select 1000 triplets from the generated data. We compute the RMSDs for each triplet between our proposed estimator ( defined in (12)) and the true one-factor copula model (defined in (2) when the dimension is ) as well as between the naive estimator and the true model using equation (15) when , and can be either the proposed estimator or the naive one.

We use the naive estimator, denoted as introduced in Section 3.1, which differs from the classical bivariate copula estimator, as used and defined before in the bivariate case. Figure (5) shows the histograms of the RMSDs, which clearly demonstrate that the RMSDs associated with our proposed estimator are significantly smaller than those of the naive estimator. This finding highlights the superior performance of our approach in high-dimensional settings.

Finally, for the copula density linking the first variables, we compute the RMSDs between the best parametric model in terms of BIC and the naive estimator as well as the proposed estimator. We use equation (15) to compute RMSDs for and different dimensions ; table (5) shows the results.

We then repeated the analysis for the data from the Health Care and Energy sectors, with tickers and some results provided in Appendix 6.2. For all three different sectors Table (5) shows that the proposed copula density estimator is much closer to the best parametric copula model. In this table, represents the number of stocks in each sector.

| Sectors | Factor copula estimator | Naive estimator | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Industrial | 0.57 | 1.18 | 41 | ||||||

| Health Care | 0.74 | 1.08 | 37 | ||||||

| Energy | 1.39 | 2.61 | 22 |

5 Discussion

Factor copula models, studied by Krupskii and Joe, (2013), offer a parsimonious framework for capturing diverse dependence structures, including tail dependence and asymmetric relationships. However, real-world data often exhibit dependence structures that cannot be adequately modeled by existing parametric approaches, highlighting the necessity of non-parametric methods.

In this paper, we developed a novel non-parametric estimator for the one-factor copula model that combines proxy to the unobserved factor and the kernel estimation approach. We showed the consistency of the proposed estimator and its good finite-sample performance.

We applied the new estimator for the analysis of stock returns data and showed that our estimator outperforms the naive multivariate density kernel estimator, particularly in high-dimensional settings, while maintaining competitive performance even in the bivariate case. These findings underscore the potential of the proposed estimator for the analysis of data sets with complex dependence structures in real-world applications.

There are several potential directions for future research and applications, including:

-

•

Extending our approach to different types of dependent variables: this involves adapting the methodology to handle dynamic dependence structures that evolve over time, as well as mixed continuous-ordinal data where variables may have distinct measurement scales. Furthermore, the approach could be expanded to address datasets with missing values by incorporating robust imputation methods and analyzing item response variables, which are commonly used in fields like psychometrics and educational testing.

-

•

Developing non-parametric estimation methods for structured factor copula models, including nested, oblique, and -factor copula models, using the proxy method outlined by Fan and Joe, (2023).

Acknowledgments

The authors are grateful to the referees and the Associate Editor for their constructive comments, which greatly enhanced the quality of the article.

Funding

There is no funding for this paper.

Data Availability

The data sets used and analyzed during the current study are available from the corresponding author on reasonable request.

Declarations

Conflict of interest

The authors declare no conflict of interest.

6 Appendix

6.1 Proofs Theorem 2.1 and Proposition 2.1

This section illustrates the proof of Theorem (2.1) along with the proof of Proposition (2.1). We will use the following notation throughout this section:

Here, is the latent variable and is the proxy for , where denotes the CDF of as before.

Proof of Proposition (2.1): For the first equation in (13), we employ the proof techniques from Nagler et al., (2017) to analyze the bias and variance of our kernel estimator in the presence of the proxy variable. Suppose that

where is defined in (10). Then, the bias and variance terms are

where and . Also the bandwidth matrix has three parameters . Using the definition of linking copula in (10) and the notation in Section 2.1, we have

To proceed, we begin by calculating the variance of the term as follows

The last equality is obtained through a change of variables. To compute the bias, we write

| (16) | ||||

By using , and , and noting that , , the Hessian matrix of can be calculated as follows:

Let and . We find:

From (16), the bias term for is

| (17) |

The proof of the first part in Proposition (2.1) follows directly from Markov’s inequality. Now let and also define . To prove the second part of Proposition (2.1), we have

By applying the first-order Taylor approximation to the function , we have:

| (18) | ||||

The inequality in (18) follows from part (b) of Assumption (2.1). Next, we prove the third part of Proposition (2.1). We use the first-order Taylor approximation of :

| (19) |

Denote . We use the first-order Taylor approximation of to write:

| (20) |

Let , we find from (6.1) that

| (21) |

where the derivative of is continuous and bounded by Assumption (2.1), so we can use the boundedness of the kernel function to complete the proof.

Proof of Theorem (2.1): To obtain the result, first, we consider the rate of convergence of the linking copula estimator:

Recall, and by Assumption (2.1), part (a), one can obtain

| (22) |

Without loss of generality, we assume that , where is the identity matrix. When using the mean-squared optimal bandwidth and , we obtain . So, using Proposition (2.1) for and , we have

| (23) |

To complete the proof of Theorem (2.1), we will use the Dominated Convergence Theorem (DCT). We begin by demonstrating that the estimator is bounded. We assume that for any , and further assume that there exists a constant such that for all and . These are mild assumptions that are satisfied by many commonly used parametric copula families provided that dependence is not very strong.

We can redefine which does not affect the asymptotic behavior of the estimator. Using the boundedness of the estimator , we apply CDT to obtain

which concludes the proof.

6.2 Analysis of data from the Energy and Health Care sectors

We conducted a similar analysis of the stocks from the Energy and Health Care sectors. For the Energy sector, we considered stocks with the following tickers: CVX, XOM, HES, BKR, HAL, SLB, APA, COP, CTRA, DVN, FANG, EOG, EQT, MRO, OXY, MPC, PSX, VLO, KMI, OKE, TRGP, WMB. The stock returns are observed from January 2, 2017, to July 31, 2024, spanning a sample size of days. For the Health Care sector (encompassing Biotechnology, Services, Equipment, and Distributors industries), we considered stocks with the following tickers: AMGN, ABBV, BIIB, GILD, INCY, REGN, VRTX, ABT, BAX, BDX, DXCM, BSX, PODD, EW, HOLX, IDXX, ZBH, ISRG, MDT, RMD, RVTY, STE, SYK, TFX, CAH, COR, HSIC, MCK, A, BIO, TECH, CRL, DHR, IQV, MTD, TMO, WAT. The stock returns are observed from January 2, 2017, to December 30, 2020, spanning a sample size of days. This shorter period was chosen to ensure that the joint dependence of data from the Health Care sector can be adequately captured by a single common factor. When using a longer time frame, the data indicated the presence of two common factors, likely due to structural shifts in the market, particularly the impact of the COVID-19 pandemic. To maintain consistency with the one-factor assumption, we restricted the analysis to this period.

Similar to the Industrials sector data, we applied the AR(1)–GARCH(1,1) model to the returns from the two sectors, and the scree plot indicates a one-factor structure is suitable for the GARCH-filtered stock returns from these sectors; see Fig. (6).

Finally, figures (7) and (8) show the estimated contour plots of the copula density linking some pairs of variables from the two sectors. Again, the results demonstrate that the proposed estimator and the classical copula estimator yield very similar results for bivariate marginals.

References

- Autin et al., (2010) Autin, F., Pennec, E. L., and Tribouley, K. ((2010)). Thresholding methods to estimate the copula density. Journal of Multivariate Analysis, 101(1):200–222.

- Bellman, (2003) Bellman, R. E. ((2003)). Dynamic programming. New York, NY, USA: Dover.

- Bouezmarni et al., (2013) Bouezmarni, T., El Gouch, A., and Taamouti, A. ((2013)). Bernstein estimator for unbounded copula densities. Statistics and risk modeling, 30(4):343–360.

- Bouezmarni et al., (2010) Bouezmarni, T., Rombouts, J., and Taamouti, A. ((2010)). Asymptotic properties of the bernstein density copula estimator for -mixing data. Journal of Multivariate Analysis, 101(1):1–10.

- Brechmann et al., (2012) Brechmann, E., Czado, C., and Aas, K. ((2012)). Truncated regular vines in high dimensions with applications to financial data. Canadian Journal of Statistics, 40:68–85.

- Cattell, (1966) Cattell, R. ((1966)). The scree test for the number of factors. Multivariate Behav Res, 1(2):245–276.

- Chac´on and Duong, (2010) Chac´on, J. and Duong, T. ((2010)). Multivariate plug-in bandwidth selection with unconstrained pilot bandwidth matrices. TEST, 19:375–398.

- Chatelain et al., (2020) Chatelain, S., Fougères, A., and Nešlehová, J. ((2020)). Inference for archimax copulas. The Annals of Statistics, 48(2):1025–1051.

- Chatrabgoun et al., (2017) Chatrabgoun, O., Parham, G., and Chinipardaz, R. ((2017)). A legendre multiwavelets approach to copula density estimation. Stat. Pap, 58(1):673–690.

- Chen et al., (2015) Chen, H., MacMinn, R., and Sun, T. ((2015)). Multi-population mortality models: A factor copula approach. Insurance: Mathematics and Economics, 63:135–146.

- Chernozhukov et al., (2017) Chernozhukov, V., Chetverikov, D., and Kato, K. ((2017)). Central limit theorems and bootstrap in high dimensions. The Annals of Probability, 45(4):2309–2352.

- Duong, (2014) Duong, T. ((2014)). ks: Kernel smoothing. r package version 1.9.3..

- Fan and Joe, (2023) Fan, X. and Joe, H. ((2023)). High-dimensional factor copula models with estimation of latent variables. Journal of Multivariate Analysis, 201:1–29.

- Genest et al., (2009) Genest, C., Masiello, E., and Tribouley, K. ((2009)). Estimating copula densities through wavelets. Insur. Math. Econ, 44:p.e1557.

- Ghanbari and Shirazi, (2023) Ghanbari, B. and Shirazi, E. ((2023)). Using copula information in wavelet estimation of bivariate density function based on censorship observations. Communications in Statistics - Theory and Methods, 53(5):1810–1824.

- Ghanbari et al., (2019) Ghanbari, B., Yarmohammadi, M., Hosseinioun, N., and Shirazi, E. ((2019)). Wavelet estimation of copula function based on censored data. Journal of Inequalities and Applications, 2019(1).

- He et al., (2021) He, Y., Ye, X., Huang, D., Huang, J. Z., and Zhai, J.-H. ((2021)). Novel kernel density estimator based on ensemble unbiased cross-validation. Information Sciences, 581:327–344.

- Hull and White, (2004) Hull, J. and White, A. ((2004)). Valuation of a cdo and an nth to default cds without monte carlo simulation. J. Derivatives, 12:8–23.

- Jin et al., (2021) Jin, Y., He, Y., and Huang, D. ((2021)). An improved variable kernel density estimator based on regularization. Mathematics, 9(16).

- Kauermann et al., (2013) Kauermann, G., Schellhase, C., and Ruppert, D. ((2013)). Flexible copula density estimation with penalized hierarchical b-splines. Scandinavian Journal of Statistics, 40(4):685–705.

- Kiriliouk et al., (2018) Kiriliouk, A., Segers, J., and Tafakori, L. (2018). An estimator of the stable tail dependence function based on the empirical beta copula. Extremes, 21:581–600.

- Kirkby et al., (2023) Kirkby, J., Leitao, A., and Nguyen, D. (2023). Spline local basis methods for nonparametric density estimation. Statistics Surveys, 17:75–118.

- Ko and Hjort, (2019) Ko, V. and Hjort, N. ((2019)). Model robust inference with two-stage maximum likelihood estimation for copulas. Journal of Multivariate Analysis, 171:362–381.

- Koike, (2021) Koike, Y. ((2021)). Notes on the dimension dependence in high-dimensional central limit theorems for hyperrectangles. Japanese Journal of Statistics and Data Science, 4:257–297.

- Krupskii and Genton, (2017) Krupskii, P. and Genton, M. ((2017)). Factor copula models for data with spatio-temporal dependence. Spatial Statistics, 22(1):180–195.

- Krupskii et al., (2018) Krupskii, P., Huser, R., and Genton, M. ((2018)). Factor copula models for replicated spatial data. Journal of the American Statistical Association, 113(521):467–479.

- Krupskii and Joe, (2013) Krupskii, P. and Joe, H. ((2013)). Factor copula models for multivariate data. J. Multivariate Anal, 120:85–101.

- Krupskii and Joe, (2015) Krupskii, P. and Joe, H. ((2015)). Structured factor copula models: Theory, inference and computation. Journal of Multivariate Analysis, 138:53–73.

- Krupskii and Joe, (2022) Krupskii, P. and Joe, H. ((2022)). Approximate likelihood with proxy variables for parameter estimation in high-dimensional factor copula models. Statist Papers, 63(2):543–569.

- Liu et al., (2024) Liu, H., Havrilla, A., Lai, R., and Liao, W. ((2024)). Deep nonparametric estimation of intrinsic data structures by chart autoencoders: Generalization error and robustness. Applied and Computational Harmonic Analysis, 68.

- Liu et al., (2021) Liu, W., Liang, S., and Qin, X. ((2021)). A novel dimension reduction algorithm based on weighted kernel principal analysis for gene expression data. PLoS One, 16(10):e0258326.

- Modak, (2023) Modak, S. ((2023)). A new measure for the assessment of clustering based on kernel density estimation. Communications in Statistics - Theory and Methods, 52(17):5942–5951.

- Nagler, (2016) Nagler, T. ((2016)). kdecopula: Kernel smoothing for bivariate copula densities. r package version 0.2.1, url: https://github.com/tnagler/ kdecopula.

- (34) Nagler, T. ((2016b)). kdecopula: Kernel smoothing for bivariate copula densities. R package version 0.8.0.

- Nagler and Czado, (2016) Nagler, T. and Czado, C. ((2016)). Evading the curse of dimensionality in nonparametric density estimation with simplified vine copulas. J. Multivar. Anal, 151:69–89.

- Nagler et al., (2017) Nagler, T., Schellhase, C., and Czado, C. ((2017)). Nonparametric estimation of simplified vine copula models: comparison of methods. Dependence Modeling, 5:99–120.

- Nguyen et al., (2019) Nguyen, H., Ausin, M. C., and Galeano, P. ((2019)). Parallel bayesian inference for high-dimensional dynamic factor copulas. Journal of Financial Econometrics, Oxford University Press, 17(1):118–151.

- Nikoloulopoulos and Joe, (2015) Nikoloulopoulos, A. and Joe, H. ((2015)). Factor copula models for item response data. Psychometrika, 80:126–150.

- Oh and Patton, (2017) Oh, D. and Patton, A. ((2017)). Modeling dependence in high dimensions with factor copulas. Journal of Business and Economic Statistics, 35(1):139–154.

- Qu and Yin, (2012) Qu, L. and Yin, W. ((2012)). Copula density estimation by total variation penalized likelihood with linear equality constraints. Computational Statistics and Data Analysis, 56(2):384–398.

- R Core Team, (2023) R Core Team (2023). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Scott, (1992) Scott, D. W. ((1992)). Multivariate density estimation: Theory, practice, and visualization. Hoboken, NJ, USA: Wiley.

- Sklar, (1959) Sklar, A. ((1959)). Fonctions de répartition à n dimensions et leurs marges. Publ. Inst. Stat. Univ. Paris, 8:229–231.

- Sánchez, (2003) Sánchez, V. ((2003)). Advanced support vector machines and kernel methods. Neurocomputing, 55:5–20.

- Wang et al., (2023) Wang, W., Wang, B., Chau, K., and Xu, D. ((2023)). Monthly runoff time series interval prediction based on woa-vmd-lstm using non-parametric kernel density estimation. Earth Science Informatics, 16:2373–2389.