Trading-R1: Financial Trading with LLM Reasoning via Reinforcement Learning

Abstract

Developing professional, structured reasoning on par with human financial analysts and traders remains a central challenge in AI for finance, where markets demand interpretability and trust. Traditional time-series models lack explainability, while LLMs face challenges in turning natural-language analysis into disciplined, executable trades. Although reasoning LLMs have advanced in step-by-step planning and verification, their application to risk-sensitive financial decisions is underexplored. We present Trading-R1, a financially-aware model that incorporates strategic thinking and planning for comprehensive thesis composition, facts-grounded analysis, and volatility-adjusted decision making. Trading-R1 aligns reasoning with trading principles through supervised fine-tuning and reinforcement learning with a three-stage easy-to-hard curriculum. Training uses Tauric-TR1-DB, a 100k-sample corpus spanning 18 months, 14 equities, and five heterogeneous financial data sources. Evaluated on six major equities and ETFs, Trading-R1 demonstrates improved risk-adjusted returns and lower drawdowns compared to both open-source and proprietary instruction-following models as well as reasoning models. The system generates structured, evidence-based investment theses that support disciplined and interpretable trading decisions. Trading-R1 Terminal will be released at https://github.com/TauricResearch/Trading-R1.

1 Introduction

Financial exchange predates written history, yet the founding of the Amsterdam Stock Exchange is commonly treated as the birth of the modern securities market Petram (2014). Since then, scholars and practitioners have proposed a wide range of theories to explain price formation and guide trading, spanning sociological and psychological accounts, econometric models, and technical paradigms such as Elliott Wave, Dow Theory, and price action Elliott (1938); Dow et al. ; Schwager (2012); Lefevre and Markman (2010); Brooks (2009). As time passes, the amount of available market data and computing power and technology have drastically changed and increased, quantitative methods have flourished, and advances in natural language processing have enabled large-scale analysis of unstructured sources of various modalities, including news, earnings disclosures, and macroeconomic reports, using tools such as sentiment analysis. Yet these signals are seldom integrated into a coherent decision framework but individually used as tools for analysts and firms. Instead, bespoke factors are typically engineered in isolation and left to human traders to interpret and combine.

Recent breakthroughs in large language models (LLMs) have transformed automated reasoning across domains. NLP has shifted from single-purpose models to promptable intelligence: general purpose systems augmented with chain-of-thought, self-verification, and reinforcement learning, that now can tackle complex reasoning tasks with increasing reliability and scope Bai et al. (2023); OpenAI et al. (2025); DeepSeek-AI et al. (2025); OpenAI et al. (2024). Yet their application to finance remains nascent. Markets are dynamic, noisy, and multi-factor, demanding adaptive and interpretable reasoning under uncertainty, requirements that differ markedly from the math, coding, and science tasks that have dominated recent LLM optimizations Lu et al. (2024); Hendrycks et al. (2021). Alternatives exist, notably purely quantitative approaches Ericson et al. (2024); Fjellström (2022), but they are often opaque and brittle across regimes; meanwhile, general-purpose reasoning LLMs struggle to ground their inferences in financial contexts, provide verifiable logic, and produce traceable decisions Liu et al. (2025b); Tatsat and Shater (2025); Lee et al. (2025). Progress is further hampered by sparse, fragmented public financial data, which complicates model training; moreover, there is a mismatch between open-ended financial QA benchmarks Qian et al. (2025); Liu et al. (2025b) and the structured, sequential reasoning that trading demands. Unlike QA, market decisions are inherently uncertain and path-dependent: even reasonable choices can yield divergent, unforeseen outcomes.

To address these gaps, we propose Trading-R1, a financial trading reasoning foundation model tailored for financial and specifically trading-oriented reasoning. We curate a high-quality dataset of over 100K publicly sourced financial reasoning samples and train Trading-R1 via supervised fine-tuning followed by a curriculum of reinforcement learning from easy to hard. This design directly tackles the core limitations of existing reasoning LLMs in finance, advancing models that are both grounded in market complexity and practically usable for trading. Our key contributions are as follows:

-

•

Tauric-TR1-DB: A large-scale, diverse financial reasoning corpus. We curate a comprehensive dataset spanning 18 months from January 1, 2024, to May 31, 2025, across 14 major tickers, integrating heterogeneous financial data used by real traders, such as technical market data, fundamentals, news, insider sentiment, and macroeconomic indicators. The final corpus contains 100k samples of filtered, high-quality financial information, paired with supervision via reverse reasoning distillation and volatility-aware reward labeling.

-

•

Supervised fine-tuning with reverse chain-of-thought distillation. Since proprietary LLMs provide only final answers without intermediate reasoning, we reconstruct hidden reasoning traces from high-performing but opaque API models and use them as supervision for reasoning-oriented training. This approach enables our model to generate concise, interpretable, and high-quality investment theses distilled from the insights of state-of-the-art reasoning systems.

-

•

Reinforcement learning for execution-grade decisions. Beyond thesis writing, we refine the model for actionable decision making. We cast trade recommendations as an RL problem, labeling assets on the standard five-tier investment scale (Strong Buy, Buy, Hold, Sell, Strong Sell). Ratings are volatility-adjusted and used as rewards to align model outputs with realistic trading objectives.

-

•

Trading-R1: A financial reasoning LLM for trading. We propose Trading-R1, a large-scale financial reasoning LLM trained across diverse assets and market conditions (bull and bear). The model demonstrates strong generalization in trading scenarios, producing both high-quality analyses and profitable trade recommendations.

2 Related Work

2.1 Large Language Models in Finance

Large Language Models (LLMs) have demonstrated impressive capabilities across many domains, including finance. To adapt them for financial tasks, researchers typically rely on three strategies: pretraining on domain-specific data, fine-tuning on task-specific datasets, and applying reinforcement learning to align model behavior with desired outcomes. Another line of work explores using pretrained models directly off the shelf as specialized experts within multi-agent systems. In these setups, LLMs are assigned distinct roles, and their coordinated interactions are designed to elicit more explicit financial reasoning and enhance the overall reasoning capabilities of the system.

Pretraining and Fine-tuning LLMs for Finance

Domain adaptation for LLMs in finance follows two main approaches: pretraining from scratch on financial corpora and fine-tuning existing models on financial data.

Models like BloombergGPT (Wu et al., 2023), XuanYuan 2.0 (Zhang et al., 2023b), and Fin-T5 (Lu et al., 2023) were trained on combined public and finance-specific datasets. BloombergGPT, leveraging proprietary Bloomberg data, outperforms general-purpose counterparts like BLOOM-176B in market sentiment classification and summarization tasks, while maintaining competitive general language understanding compared to similar-sized open-source models.

The fine-tuning approach is exemplified by models such as PIXIU (FinMA) (Xie et al., 2023), which fine-tuned LLaMA on 136K finance-related instructions; FinGPT (Yang et al., 2023), which used LoRA to adapt LLaMA and ChatGLM with approximately 50K finance-specific samples; and Instruct-FinGPT (Zhang et al., 2023a), fine-tuned on 10K instruction samples from financial sentiment analysis datasets. These models demonstrate stronger performance in finance classification tasks compared to their base versions and other open-source LLMs like BLOOM and OPT (Zhang et al., 2022), sometimes even surpassing BloombergGPT. However, their performance in generative tasks still lags behind powerful general-purpose models like GPT-4, indicating the need for higher-quality, domain-specific datasets.

Reinforcement Learning for LLMs

Reinforcement learning from human feedback (Ouyang et al., 2022; Kaufmann et al., 2023, RLHF) has emerged as a cornerstone technique for aligning LLMs with human preferences (Lambert et al., 2024). This approach ranges from Proximal Policy Optimization (Schulman et al., 2017, PPO) to Direct Preference Optimization (Rafailov et al., 2023, DPO) and Simple Preference Optimization (Meng et al., 2024, SimPO), which eliminate the need for explicit reward modeling and help stabilize training. Recent innovations such as Group Relative Policy Optimization (Shao et al., 2024a, GRPO) address computational challenges by optimizing group-wise comparisons and implementing batch-normalized rewards. Notable advancements include DeepSeek-R1’s multi-stage RL training (DeepSeek-AI et al., 2025) and personalized alignment via variational preference learning (Poddar et al., 2024). Despite significant progress, fundamental limitations persist, including risks of reward hacking, off-policy instability, and the need for pluralistic alignment to accommodate diverse human preferences (Casper et al., 2023; Kaufmann et al., 2024).

Multi-agent LLMs for Finance

While training models on financial data can improve performance, limited resources and data availability often make off-the-shelf LLMs an attractive alternative. Although not specialized in finance, large general-purpose models excel at reasoning and instruction following, which has fueled the rise of agent systems, frameworks that equip LLMs with memory, tools, and role specialization to achieve complex goals. This paradigm has spread rapidly across domains from coding to AI4Science to computer use agents Gottweis et al. (2025); Hong et al. (2024); Liu et al. (2025a). In finance, multi-agent systems are often designed to replicate real decision-making processes, such as hedge fund structures, by assigning agents distinct roles and tools (e.g., news retrieval, indicator calculation). Recent frameworks like TradingAgents explicitly model financial institutions, combining structured communication and debate to produce detailed reasoning reports segmented by information sources Xiao et al. (2025).

2.2 Large Language Models in Financial Trading

LLMs are employed in financial trading across four primary application paradigms: information processing, reasoning-based decision making, reinforcement learning optimization, and alpha factor generation.

Information-Driven Trading

Information-driven approaches process news and market data to generate trading signals. Studies evaluating both closed-source models (e.g., GPT-4.1, Claude 3.7) and open-source LLMs (e.g., Qwen (Bai et al., 2023)) have demonstrated the effectiveness of simple long-short strategies based on sentiment scores (Lopez-Lira and Tang, 2023). Fine-tuned LLMs like FinGPT show improved performance through domain-specific alignment (Yang et al., 2023; Zhang et al., 2024a; Kirtac and Germano, 2024). Advanced methods involve summarizing financial news and reasoning about their relationship with stock prices (Fatouros et al., 2024; Wang et al., 2024).

Reasoning-Enhanced Trading

Reasoning-enhanced approaches leverage LLMs’ analytical capabilities through reflection and multi-agent debate. Reflection-based systems, such as FinMem (Yu et al., 2023) and FinAgent (Zhang et al., 2024b), employ layered memorization and multimodal data to summarize inputs, inform decisions, and incorporate technical indicators, achieving better backtest performance while mitigating hallucinations (Ji et al., 2023). Multi-agent frameworks (Xing, 2024; Xiao et al., 2025) enhance reasoning and factual validity by employing LLM debates among specialized agents. Systems like TradingGPT (Li et al., 2023) demonstrate improved sentiment classification and increased robustness in trading decisions through this collaborative approach.

Reinforcement Learning Optimization

Reinforcement learning optimized trading systems use backtesting performance as rewards to refine decision-making processes. SEP (Koa et al., 2024) employs RL with memorization and reflection to refine LLM predictions based on market history. Classical RL methods are also integrated in frameworks that combine LLM-generated embeddings with stock features, trained via algorithms like Proximal Policy Optimization (PPO) (Ding et al., 2023; Schulman et al., 2017). These approaches systematically improve LLM trading capabilities through iterative feedback loops.

Alpha Factor Generation

Rather than directly making trading decisions, LLMs can generate alpha factors—signals that predict stock returns. QuantAgent (Wang et al., 2023) employs a dual-loop architecture: an inner loop where a writer agent generates code from trading ideas with feedback from a judge agent, and an outer loop where the code is tested in real markets to enhance the judging agent. Similarly, AlphaGPT (Wang et al., 2023) proposes a human-in-the-loop framework for alpha mining. These approaches leverage LLMs’ capabilities to automate and accelerate trading strategy development through systematic generation and refinement of predictive signals.

3 Trading-R1 Methodology

3.1 Motivations

Training a reasoning model for financial trading is uniquely challenging compared to other domains. Financial decisions are high-stakes, multifaceted, market-dependent, and highly sensitive to noise. Simply extending chains of thought through standard reasoning training does not necessarily improve model quality; instead, it can amplify hallucinations and degrade the reliability of generated trading decisions. Since language models are conditional autoregressive generators, the quality of the final action depends on two coupled priors: (i) the external prior, given by the input context that initiates generation, and (ii) the internal prior, shaped by the model’s own previously generated tokens during roll-out. These dynamics lead to two practical imperatives:

-

•

Input quality (external prior) If the prompting context is noisy, misaligned, or low signal-to-noise, the model’s analysis is anchored to poor evidence, degrading downstream reasoning regardless of decoding or prompting.

-

•

Reasoning scaffolding (internal prior) During generation, poorly structured intermediate thoughts accumulate and result in brittle theses and unreliable decisions. Trading requires a disciplined investment thesis with clear structure, defensible claims, explicit evidence, and careful attention to risk. Providing such scaffolding ensures that the reasoning process remains coherent and that the final action is grounded in sound logic.

These challenges motivate our methodology for Trading-R1. We control both what the model conditions on and how it reasons toward the decision. Specifically, we (1) implement a rigorous data collection, cleaning, and assembly pipeline to provide high signal-to-noise, finance-grounded context at training time, and (2) employ a multi-stage, easy-to-hard curriculum for supervised fine-tuning and reinforcement learning that first teaches the model to structure an investment thesis, then to construct logical, evidence-based arguments, and finally to make decisions grounded in market dynamics. This design enables Trading-R1 to reason like a professional trader, generating substantiated and transparent analyses that lead to coherent, actionable decisions rather than merely producing longer text.

3.2 Input Data Collection at Scale

To manage external priors and ensure high-quality training inputs, we implement a rigorous data collection process that spans diverse time periods, market conditions, sectors, and analytical modalities. In financial trading research, the main challenge is not gaining access to data, but selecting information that sharpens the signal-to-noise ratio and yields actionable insights. Our dataset is built from reliable sources capturing market dynamics, company fundamentals, and public sentiment. We define input data broadly, encompassing a holistic view of macroeconomic trends and firm-specific conditions—what companies do, how they perform, and how they are perceived. To build generalizable market intelligence and provide the model with the strongest possible priors for generating high-quality theses, three core objectives guide our collection process:

Breadth across companies

We include data from a diverse set of stocks spanning sectors and market capitalizations. By focusing on more than a dozen widely followed firms (e.g., NVDA, AAPL, JNJ) over the 18 months period from January 1, 2024, to May 31, 2025, we capture a broad range of market conditions and corporate developments.

Depth of information

For each day and for each given asset, we aggregate features spanning technical data, fundamentals, news, sentiment, and macroeconomic factors. Sources include Finnhub, SimFin, Google News scraping, and stockstats, yielding a dense, multi-perspective snapshot of each company.

Robustness to variation

Real-world data is often incomplete or unbalanced. To enhance resilience, we vary input composition during label generation by randomly sampling from market data, news, sentiment, fundamentals, and macroeconomic factors. This approach trains the model to reason effectively even when information is limited. It also enables the model to detect complex patterns across contexts while remaining adaptable to real-world variability, which is essential for success in dynamic financial environments. Further methodological details are provided in Appendix 7.

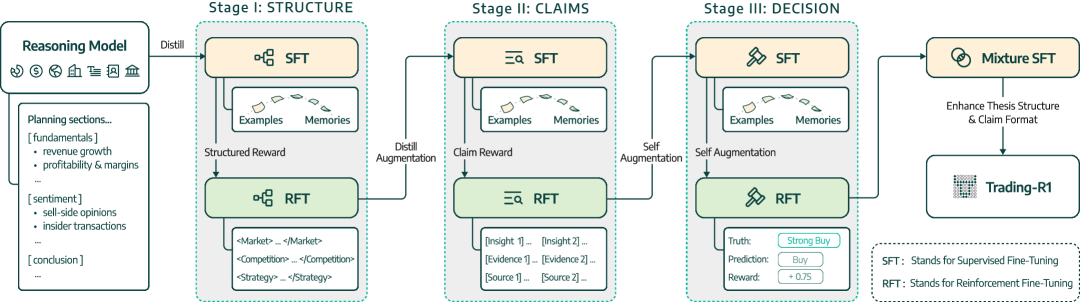

3.3 Trading-R1 Training Overview

Managing the internal priors of an LLM’s generation is critical for trading. Without proper structure, intermediate reasoning steps can compound errors, producing brittle theses and unreliable final decisions. To address this, we design a multi-stage, easy-to-hard curriculum that interleaves supervised fine-tuning (SFT) with reinforcement learning fine-tuning (RFT) as seen in Figure 1. This curriculum progressively teaches the model to (i) structure its outputs like a professional investment thesis, (ii) construct logical and evidence-backed arguments, and (iii) make decisions grounded in real market dynamics. The curriculum unfolds across three stages, each warm-started with SFT (Figure 3) to establish structural and stylistic priors, and refined with RFT to align behavior through task-specific rewards. This interleaving ensures that the model first acquires the general form of professional analysis before being guided toward evidence-grounded reasoning and, ultimately, market-aligned decision making. The staged progression stabilizes intermediate reasoning, mitigates error compounding, and builds the internal discipline required for coherent and actionable trading outputs.

| Stage | Training Phase | Method Description | Objective | ||

|---|---|---|---|---|---|

|

SFT | Supervised Fine-Tuning on massive Qwen and | Initial structured thinking and | ||

| OpenAI data (no reject sampling) | basic data organization | ||||

| RFT | Reinforcement Fine-Tuning on sections | Enable systematic analysis and | |||

| (introduction/claims/table/conclusion) | professional data categorization | ||||

| Augmentation | Self-Distill with reject sampling cases | Reinforce structured reasoning | |||

| with clear structure | patterns | ||||

|

SFT | Supervised Fine-Tuning for evidence-based | Basic claim structure and | ||

| reasoning foundation | evidence awareness | ||||

| RFT | Reinforcement Fine-Tuning on opinion + | Ground claims with quotes and | |||

| quote + source structure | sources, address hallucination | ||||

| Augmentation | Self-Distill with reject sampling cases | Reinforce evidence-based | |||

| with professional and faithful claims | professional reasoning | ||||

|

SFT | Supervised Fine-Tuning for investment | Basic decision-making structure | ||

| recommendation patterns | for investments | ||||

| RFT | Reinforcement Fine-Tuning with Equity | Generate market-aware | |||

| & Volatility & Smooth Adj | investment recommendations | ||||

| Augmentation | Self-Distill with reject sampling prediction | Reinforce accurate directional | |||

| (directional) correct cases | predictions |

In the formatting stage, the model is rewarded for following the professional structure of investment theses, systematically organizing technical, fundamental, and sentiment-based analyses. XML-tagged formatting is reinforced at this stage to promote consistent reasoning patterns and stable structured outputs. In the evidence-grounding stage, rewards encourage the model to support claims with direct citations and quotations from the input context, reducing hallucinations and fostering disciplined, evidence-based reasoning. Finally, in the decision stage, the model is trained with outcome-based rewards derived from the volatility-aware labels in Section 3.5, penalizing poor predictions and incentivizing decisions that align with verifiable market outcomes, as illustrated in Figure 4. Through this progression, Trading-R1 learns first to produce the correct form of professional analysis, then to anchor its reasoning in evidence, and ultimately to generate coherent, market-driven trading decisions.

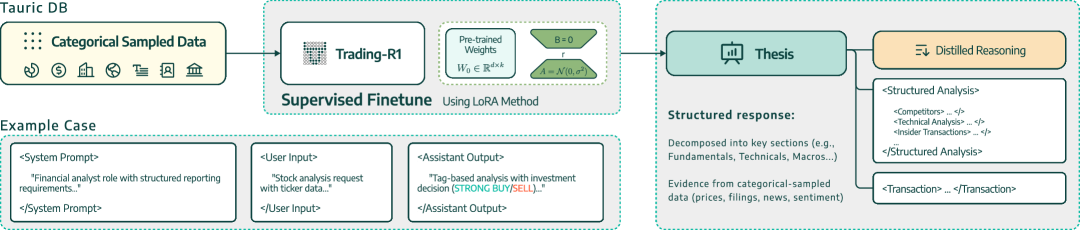

3.4 Supervised Investment Reasoning Distillation

To support the SFT warm-start stages in the interleaved easy-to-hard curriculum of Trading-R1 (Figure 1), high-quality reasoning traces are required as supervised targets. Yet obtaining such labels for large language models (LLMs) is notoriously costly, and the difficulty is magnified in the financial domain, where ground truth is often ambiguous, unavailable, or prohibitively expensive to produce. To address this, we leverage the volatility-driven labeling method introduced in Section 3.5 to automatically construct input-to-investment-thesis pairs for SFT. Each investment thesis provides a detailed reasoning trace that logically supports a trading decision consistent with the volatility-aware label assigned for that day.

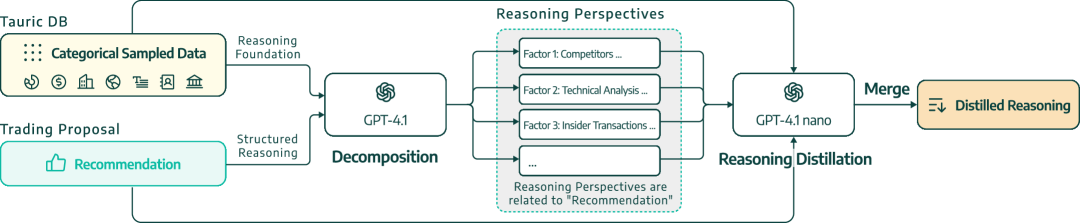

Reverse Reasoning Distillation

To overcome the difficulty of sourcing such detailed reasoning traces, we introduce a novel technique we call reverse reasoning distillation. While commercial LLMs accessed via APIs (e.g., OpenAI’s o1, o3) consistently outperform most open-source models in reasoning quality, they typically do not expose their full chain-of-thought (CoT) outputs for easy full distillation, returning only final conclusions without explanatory steps. To extract high-quality, long-form reasoning without hosting massive models ourselves, we propose a method for synthetically reconstructing reasoning paths from these black-box models.

As illustrated in Figure 2(a), we begin by inputting structured financial data for a specific ticker on a given date into proprietary reasoning models, such as o3-mini or o4-mini, and retrieve its final trading recommendation (i.e., a front-end response). Next, as shown in Figure 2(b), we pass this final response, along with the original input, into a dedicated planner LLM tasked with inferring the key reasoning steps required to arrive at the given conclusion. To simulate the full reasoning process, we then use a lightweight LLM (e.g., GPT-4.1-nano) to elaborate how each data modality (e.g., market data, news, social media, fundamentals) contributes to the investment decision. These segments are then programmatically stitched into a coherent reasoning trace. The end result is a high-quality, synthetic dataset of structured financial inputs paired with plausible, step-by-step investment theses, suitable for use in SFT pipelines.

3.5 Volatility-Driven Discretization for Label Generation

Once a broad and diverse input corpus is assembled, the next step is to define a reliable target label. This serves as a clear indicator of the optimal trading action at a given point in time and supports market-verifiable, reward-driven reinforcement learning. Instead of attempting to predict exact future price movements, which are noisy, unstable, and especially difficult for language models to capture, we discretize the output space into five intuitive actions: strong sell, sell, hold, buy, and strong buy. This design serves two purposes. First, it mirrors real-world trading, where decisions are expressed as actions rather than precise price forecasts. Second, it provides a natural mapping from outputs to portfolio allocation weights that can be tailored to user-specific risk preferences.

Labels are generated using a principled, multi-horizon volatility-aware procedure. For each training instance, we sample inputs across all modalities (market, news, sentiment, fundamentals, and macroeconomic information) and construct a composite signal from multiple time horizons. Specifically, we compute exponential moving average (EMA) prices and calculate forward returns over 3, 7, and 15-day periods. Each return series is normalized by its rolling 20-period volatility to create Sharpe-like signals. These signals are then combined using empirically-determined weights (0.3, 0.5, 0.2 respectively) to form a composite weighted signal. Finally, labels are assigned based on percentile thresholds computed from the distribution of valid weighted signals, using asymmetric quantiles (85%, 53%, 15%, 3%) that reflect market dynamics. The full procedure is described in Algorithm 1 and Appendix 8. This multi-horizon volatility-aware design provides four advantages. (i) Signals capture both short-term momentum and medium-term trends through multiple time horizons. (ii) Volatility normalization ensures consistent signal strength across different market regimes. (iii) The weighted combination balances immediate price action with broader trend information. (iv) Asymmetric quantile cutoffs preserve the market’s long-term upward drift while maintaining class diversity for robust training.

The resulting proxy labels are highly valuable for downstream learning. They supply a natural reward signal for reinforcement learning (Section 3.7) and enable the scalable creation of high-quality targets for supervised fine-tuning (Section 3.6). This significantly lowers the cost of reasoning-based supervision, which would otherwise depend on manual or expert annotation.

3.6 Supervised Fine-Tuning for Structured Analysis

SFT Warm-Start for Structured Reasoning

Using high-quality investment theses generated through reverse reasoning distillation, we perform SFT to warm-start each stage of the easy-to-hard curriculum (Figure 3). Each training instance pairs structured market data with a detailed investment thesis, teaching the model to analyze, synthesize, and decide in ways that mirror expert financial workflows. Because the distillation process is controllable, stage-specific SFT targets can be designed to establish the correct reasoning priors before RFT refinement.

Stage-Wise Targets

In Stage I (Structure), SFT emphasizes the professional organization of theses, instilling structured thinking and systematic data organization. In Stage II (Claims), SFT introduces evidence-based reasoning, guiding the model to build claims anchored in data. In Stage III (Decision), SFT focuses on investment recommendation patterns, preparing the model to structure outputs around actionable decisions. This staged warm-start stabilizes intermediate reasoning, reduces compounding errors, and ensures that RFT operates on strong structural and evidential priors.

Backbone Model and Stability

We adopt Qwen3-4B as the backbone model, since it is already optimized for reasoning tasks. This prior accelerates convergence during both SFT and RFT, while improving the model’s ability to generate structured, interpretable outputs. Without this warm-start, models tended to overfit to superficial heuristics, forget structures from earlier stages, and produce brittle, incoherent theses. Staged SFT initialization instead provides disciplined scaffolding that preserves prior knowledge and allows reinforcement learning to refine rather than overwrite the model’s analytical capabilities.

3.7 Reinforcement Learning Fine-Tuning for Market-Aligned Decisions

RFT Fine-Tuning after SFT Warm-Start

While SFT equips the model with structured and interpretable reasoning, it often overfits to superficial patterns and falls short of producing decisions that are both robust and actionable. Directly transitioning from SFT to outcome-based RL is unstable, as the model lacks the discipline to balance structured reasoning with verifiable market performance. To address this, our interleaved easy-to-hard curriculum applies RFT after each SFT warm-start, reinforcing the stage-specific priors with outcome-based feedback. In this way, RFT refines the model’s reasoning so that quality analyses translate into coherent, market-aligned actions. Detailed reward specifications for each stage are provided in Appendix 10.

Action Space and Labeling

We define a five-class action space—strong sell, sell, hold, buy, strong buy—mapped to portfolio weights. This design reflects varying degrees of conviction and enables finer-grained position control compared to the traditional buy/hold/sell triad. Labels are asset-specific, constructed from the multi-horizon volatility-aware procedure described in Section 3.5. To better capture market dynamics, we project returns onto asymmetric quantiles, producing a skewed distribution that reflects both the equity market’s long-term upward drift and the growth-oriented characteristics of our blue-chip training universe, while maintaining sufficient class diversity for robust training:

| Strong Buy | Buy | Hold | Sell | Strong Sell |

| 15% | 32% | 38% | 12% | 3% |

This distribution encourages the model to learn realistic, market-consistent policies while preserving class diversity for robust training. The asymmetric allocation reflects both empirical equity market behavior and established analyst practices, with a bias toward positive actions that is particularly justified by our training universe composition. Our portfolio focuses on large-cap and mega-cap blue-chip companies—including technology leaders like NVIDIA, Microsoft, and Apple, established financials like Berkshire Hathaway and JPMorgan Chase, healthcare giants like Eli Lilly and Johnson & Johnson, and broad market ETFs like SPY and QQQ. These companies collectively represent over $11 trillion in market capitalization and are characterized by solid fundamentals, robust cash flows, dominant market positions, and strong competitive moats within their respective sectors. Given the inherent quality and growth orientation of this blue-chip universe, a structural bullish bias in the action distribution aligns with the long-term appreciation potential of these market-leading assets. Importantly, because Trading-R1 trades with long–short strategies, a sell or strong sell signal implies initiating short positions rather than merely closing longs. While shorting introduces practical feasibility challenges, incorporating it during training provides a richer action space and sharper signal discrimination for tactical positioning around these fundamentally strong companies.

Time Horizon

We target medium-term strategies with holding periods on the order of one week. This horizon balances actionability with feasibility: excluding high-frequency trading (limited by LLM inference latency) while avoiding long-horizon investing, which requires macroeconomic foresight beyond the current capabilities of language models. Medium-term trading provides a natural setting where structured reasoning, evidence grounding, and outcome alignment can be most effectively combined.

Policy Optimization

To optimize the policy during reinforcement learning, we adopt Group Relative Policy Optimization (GRPO), a recent variant of Proximal Policy Optimization (PPO) that eliminates the need for a separate value model Schulman et al. (2017); Shao et al. (2024b). Whereas PPO estimates per-token advantages with a learned value function, GRPO derives the baseline directly from a group of sampled trajectories for the same input. This relative scoring stabilizes training and reduces memory overhead. Concretely, for each input , we sample candidate outputs from the old policy and assign each output a reward from the reward model. The group-relative advantage normalizes each candidate by its peers:

The GRPO objective is then:

| (1) |

where controls clipping, scales the KL penalty to the reference SFT model , and is the normalized group-relative advantage.

For Trading-R1 training, the reward integrates the structure, evidence, and decision components (Section 10). Each sampled output is thus judged not only on the correctness of its trading decision, but also on the coherence of its thesis structure and the grounding of its claims. This holistic scoring aligns naturally with GRPO’s group-relative framework. Together, GRPO provides stable optimization without requiring a critic model, while our three-stage reward system supplies task-specific shaping signals that progressively refine structured reasoning, evidence-backed claims, and market-aligned trading decisions. Full reward formulations are deferred to Appendix 10.

4 Experiments

4.1 Training Details

Training Trading-R1 involved processing multi-dimensional financial inputs (20–30k tokens) and generating comprehensive investment theses (6–8k tokens). The supervised fine-tuning stage with LoRA Hu et al. (2021) was conducted on one 8×H100 server (96GB), while the reinforcement learning stage utilized one 8×H200 server (141GB). This RL stage enhances the model’s ability to transition from analytical reasoning to high-confidence trading decisions, completing the full pipeline from insight to action.

Our training portfolio encompasses a strategically selected universe of large-cap equity assets representing diverse market sectors and investment vehicles. The portfolio concentrates on mega-cap technology leaders including NVIDIA, Microsoft, and Apple, which collectively represent over $11 trillion in market capitalization and serve as primary drivers of modern equity market dynamics. Beyond technology, the selection spans communication services (Meta), consumer discretionary (Amazon, Tesla), financials (Berkshire Hathaway, JPMorgan Chase), healthcare (Eli Lilly, Johnson & Johnson), and energy (Exxon Mobil, Chevron). Additionally, two major ETFs (SPY and QQQ) provide exposure to broader market beta and technology sector concentration, respectively. This curated selection ensures Trading-R1 encounters the full spectrum of market regimes, sector dynamics, and volatility patterns that characterize modern institutional trading environments. The complete portfolio breakdown by sector and market capitalization is detailed in Appendix 7.

4.2 Data, Prompts, and Reward Structure

Inputs are standardized across models to ensure comparability. Each prompt provides a structured snapshot of market data, fundamentals, social sentiment, and recent news headlines for a given asset-day. Models are required to generate an investment thesis followed by a trading decision mapped to a five-class discrete action space (Strong Sell, Sell, Hold, Buy, Strong Buy).

Rewards are derived from the volatility-adjusted, percentile-based labeling scheme introduced in Section 3.5. Labels are calibrated to each asset’s return distribution, reflecting differences in volatility and drift. The resulting asymmetric target distribution (detailed in Table 2) mirrors both empirical equity market behavior and established analyst practices. By tailoring label distributions per asset, we ensure that both training rewards and evaluation outcomes are realistic, risk-aware, and aligned with professional financial analysis.

4.3 Experimental Design and Evaluation Methodology

We evaluate Trading-R1 using a comprehensive historical backtesting framework on a curated set of high-volume equities, including Apple (AAPL), Google (GOOGL), and Amazon (AMZN), along with widely traded ETFs such as SPY. The backtest covers June 1 to August 31, 2024, a held-out period excluded from the training data that reflects diverse market conditions and provides a realistic benchmark for assessing generalization and robustness.

Baseline Models

We compare Trading-R1 against a broad range of LLM-based analysis tools spanning small, medium, and large model classes. For small language models (SLMs), we evaluate Qwen-4B, GPT-4.1-nano, and GPT-4.1-mini. For larger LLMs, we include GPT-4.1, LLaMA-3.3, LLaMA-Scout, and Qwen3-32B. For reinforcement learning–enhanced models (RLMs), we consider DeepSeek, O3-mini, and O4-mini. In addition, we conduct an ablation study on Trading-R1 variants: one initialized with SFT warm-start and another trained with RL only, to better understand the contributions of each training stage to overall performance.

Evaluation Metrics

We evaluate model performance using standard finance metrics that capture both profitability and risk characteristics. Our evaluation framework includes Cumulative Return (CR) to measure total returns, Sharpe Ratio (SR) to assess risk-adjusted performance, Hit Rate (HR) to evaluate prediction accuracy, and Maximum Drawdown (MDD) to quantify downside risk. These metrics provide a comprehensive assessment of trading strategy effectiveness across different market conditions. Detailed mathematical definitions and calculation procedures for all metrics are provided in Appendix 8.

Backtesting Simulation

We adopt a standard backtesting setup based on historical market data, collecting multi-dimensional inputs for Trading-R1 such as daily news, price data, and derived indicators, like Tauric-TR1-DB. Trades are executed using only information available up to each trading day, eliminating look-ahead bias and ensuring strictly causal evaluation in a fully out-of-sample setting. This controlled design isolates the effect of model quality on trading performance.

5 Results

Our experimental results demonstrate a clear hierarchy in trading performance across different model categories. Tables 3 and 4 present the performance metrics for Trading-R1.

| NVDA | AAPL | MSFT | |||||||||||

| Category | Model | CR(%) | SR | HR(%) | MDD(%) | CR(%) | SR | HR(%) | MDD(%) | CR(%) | SR | HR(%) | MDD(%) |

| SLM | Qwen-4B | -1.59 | -1.62 | 52.2 | 2.80 | -0.81 | -0.92 | 41.7 | 3.76 | -1.45 | -1.28 | 50.0 | 4.38 |

| GPT-4.1-nano | 0.76 | -0.09 | 56.0 | 3.82 | 0.44 | -0.31 | 51.9 | 3.52 | -0.01 | -0.95 | 39.3 | 1.60 | |

| GPT-4.1-mini | 0.29 | -0.53 | 58.8 | 2.47 | -2.14 | -1.92 | 40.0 | 3.69 | -2.34 | -1.74 | 27.3 | 4.00 | |

| LLM | GPT-4.1 | 3.15 | 0.85 | 65.5 | 2.81 | 4.02 | 1.24 | 50.0 | 2.89 | 2.30 | 0.97 | 63.9 | 1.92 |

| LLaMA-3.3 | 0.65 | -0.16 | 62.2 | 2.78 | 6.73 | 1.78 | 63.6 | 2.40 | 1.58 | 0.54 | 58.1 | 1.59 | |

| LLaMA-Scout | -1.96 | -1.64 | 31.8 | 2.90 | 2.03 | 0.58 | 59.4 | 3.21 | -0.29 | -1.33 | 36.8 | 1.44 | |

| Qwen3-32B | 1.74 | 0.27 | 64.5 | 2.80 | 0.62 | -0.12 | 33.3 | 3.39 | 2.14 | 1.29 | 65.6 | 0.82 | |

| RLM | DeepSeek | -0.79 | -0.66 | 50.0 | 3.66 | 0.68 | -0.13 | 55.3 | 4.78 | -0.38 | -1.01 | 33.3 | 2.06 |

| O3-mini | -2.97 | -1.48 | 46.9 | 5.33 | -1.89 | -1.13 | 50.0 | 3.72 | 1.19 | 0.15 | 47.4 | 1.19 | |

| O4-mini | -0.99 | -0.83 | 43.2 | 3.61 | -3.19 | -1.36 | 50.0 | 7.88 | -1.72 | -1.77 | 48.5 | 2.35 | |

| Ours | Supervise Finetune | 7.42 | 2.72 | 72.5 | 2.01 | -2.37 | -1.27 | 45.2 | 5.20 | -0.24 | -0.64 | 56.1 | 3.87 |

| Reinforcement Learning | 3.27 | 1.25 | 62.5 | 2.73 | 4.04 | 1.14 | 57.1 | 3.02 | -0.18 | -0.81 | 45.7 | 1.66 | |

| Trading-R1 | 8.08 | 2.72 | 70.0 | 3.80 | 5.82 | 1.80 | 63.6 | 3.68 | 2.38 | 0.87 | 60.4 | 1.90 | |

Small Language Models (SLMs) perform the weakest, struggling with profitability due to their limited parameter capacity and shallow reasoning, which leads to unstable analyses, weak argumentation, and poor overall decision quality. Reasoning Language Models (RLMs) achieve modest improvements over SLMs but face significant challenges: their limited instruction-following ability sometimes prevents them from producing decisions in the required format, and their lengthy reasoning paths often drift away from market-relevant data. Large Language Models (LLMs) outperform both categories, demonstrating stronger consistency and decision quality even without domain-specific training.

Interestingly, despite their advanced reasoning capabilities, off-the-shelf RLMs often underperform LLMs on trading tasks. This underperformance stems from their unguided reasoning processes, which can drift away from financial analysis and result in unfocused outputs. In contrast, the Trading-R1 series (SFT, RFT, and full Trading-R1) highlights the importance of specialized training: SFT enforces professional output formats and consistent decision-making patterns, while RFT progressively aligns reasoning with market outcomes.

| AMZN | META | SPY | |||||||||||

| Category | Model | CR(%) | SR | HR(%) | MDD(%) | CR(%) | SR | HR(%) | MDD(%) | CR(%) | SR | HR(%) | MDD(%) |

| SLM | Qwen-4B | -2.90 | -1.13 | 46.2 | 6.05 | 1.32 | 0.14 | 51.7 | 3.80 | -1.33 | -3.37 | 42.3 | 1.71 |

| GPT-4.1-nano | -4.88 | -2.34 | 40.7 | 6.20 | -3.07 | -1.69 | 47.8 | 5.19 | 0.04 | -1.23 | 47.6 | 1.38 | |

| GPT-4.1-mini | 2.24 | 0.81 | 50.0 | 2.01 | 1.21 | 0.16 | 56.5 | 1.70 | -1.03 | -2.47 | 43.5 | 1.44 | |

| LLM | GPT-4.1 | 3.80 | 1.15 | 64.3 | 2.44 | 5.63 | 1.59 | 68.8 | 1.91 | 0.35 | -0.74 | 43.3 | 1.21 |

| LLaMA-3.3 | -0.89 | -0.61 | 58.6 | 6.02 | 3.21 | 1.01 | 62.5 | 2.55 | 1.27 | 0.27 | 64.7 | 1.35 | |

| LLaMA-Scout | -3.47 | -1.48 | 35.7 | 5.95 | 3.51 | 0.92 | 53.1 | 2.78 | -1.34 | -3.36 | 36.0 | 1.65 | |

| Qwen3-32B | 5.61 | 2.12 | 64.3 | 1.89 | -1.23 | -0.58 | 46.2 | 6.61 | 2.32 | 1.87 | 70.4 | 0.65 | |

| RLM | DeepSeek | -1.15 | -1.14 | 50.0 | 3.00 | 1.26 | 0.12 | 40.5 | 2.80 | -1.15 | -1.82 | 36.4 | 2.00 |

| O3-mini | -3.15 | -1.37 | 38.2 | 5.50 | 2.05 | 0.53 | 73.1 | 2.64 | 0.80 | -0.25 | 57.6 | 0.62 | |

| O4-mini | -2.48 | -1.28 | 51.6 | 4.83 | -0.45 | -0.80 | 53.6 | 2.68 | -0.30 | -1.34 | 36.8 | 1.72 | |

| Ours | Supervise Finetune | 1.93 | 0.36 | 60.6 | 4.28 | 2.52 | 0.54 | 55.9 | 2.93 | 1.78 | 0.86 | 58.1 | 1.15 |

| Reinforcement Learning | -0.05 | -0.29 | 52.5 | 4.84 | -0.18 | -0.36 | 44.4 | 5.11 | 1.85 | 1.00 | 67.6 | 0.69 | |

| Trading-R1 | 5.39 | 1.72 | 63.0 | 3.20 | 5.12 | 0.86 | 50.0 | 4.65 | 3.34 | 1.60 | 64.0 | 1.52 | |

We believe this trend reflects differences in training focus. General-purpose LLMs, exposed to a massive variety of user instructions during instruction tuning, remain flexible and open-ended in how they approach problems. RLMs, by contrast, have recently been optimized for narrow domains such as coding, mathematics, and scientific reasoning. This specialization yields strong performance in those fields but limits generalization, making them less effective for financial reasoning tasks. Although finance overlaps with mathematics and science, financial data differs in key ways: it is noisy, ambiguous, and filled with mixed signals, which makes step-by-step, verifiable rewards difficult to define. As a result, purely RFT-based approaches are not feasible off the shelf for financial LLM training. Our Trading-R1 addresses these challenges by combining the strengths of both paradigms. Through SFT, it integrates structured thesis writing and consistent decision-making patterns, while RFT progressively reinforces stage-specific behaviors. This design stabilizes reasoning, prevents drift, and enables coherent, market-aligned trading decisions.

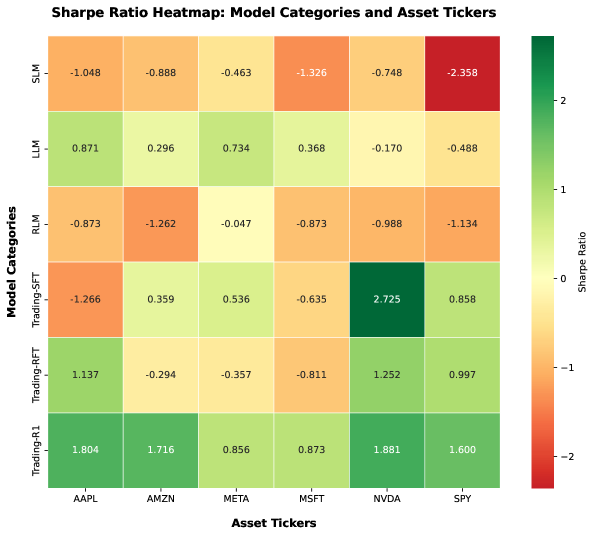

Our Trading-R1 approach achieves the strongest overall performance by combining SFT and RFT to capture market dynamics effectively. Across all evaluated assets, Trading-R1 delivers improvements over baseline models. It achieves a Sharpe ratio of with returns on NVDA, and outperforms GPT-4.1 on AAPL with a Sharpe of versus , while maintaining lower drawdowns ( vs. RLMs’ ). The model also attains leading hit ratios, including on NVDA and on SPY. By contrast, small LLMs such as Qwen-4B and GPT-4.1-nano often yield negative Sharpe ratios, and RLMs like O3-mini and O4-mini incur significant losses due to unguided reasoning processes. Overall, the performance hierarchy (SLM RLM LLM Trading-SFT Trading-RFT Trading-R1) underscores the importance of both model scale and specialized reasoning in algorithmic trading, with our approach achieving the best balance between profitability and risk management. Figure 5 shows this performance hierarchy across all evaluated assets, demonstrating the consistent improvements achieved by our Trading-R1 series over baseline approaches.

These results suggest that RFT-enhanced reasoning allows the model to adapt quickly to market fluctuations. The planning capabilities enable Trading-R1 to compose structured, professional theses that evaluate assets from comprehensive aspects, providing high-quality context for final trading recommendations. Trading-R1 not only generates more profitable trading signals but also sustains lower maximum drawdowns, demonstrating strong potential for real-world trading applications.

Observations

Trading-R1 consistently ranks among the top models across all evaluated assets, demonstrating a good balance between performance and reliability. The stability and interpretability of its outputs distinguish it from baseline models, many of which either collapse into poor profitability or produce erratic, unreadable theses. Beyond competitive metrics, Trading-R1 generates structured, facts-grounded investment theses that provide clear analytical reasoning. This combination of consistent performance with professional thesis generation makes the model particularly valuable for practical applications where both accuracy and interpretability are essential for decision-making support.

This outcome reflects a deliberate design choice. Our model’s training with both SFT and RFT produces more stable reasoning and coherent, professional investment theses. We deliberately prioritize enhanced readability, interpretability, and structured argumentation over marginal performance gains. This trade-off aligns with established precedents in the field: recent work on reasoning models has similarly documented that optimizing purely for performance metrics can compromise output coherence and practical utility. For instance, DeepSeek-R1’s developers found that their reinforcement learning approach led to language mixing issues, ultimately requiring additional alignment mechanisms that reduced raw performance to restore usability. Our design philosophy embraces this fundamental trade-off from the outset. In practical applications, investors and practitioners require not only accurate predictions but also clear, well-structured rationales that support decision-making. A model that consistently delivers professional, market-aligned analyses provides greater real-world value than one that maximizes performance metrics at the expense of interpretability and user trust.

6 Conclusion

We introduced Trading-R1, a framework for aligning large language models with financial decision-making through supervised fine-tuning and reinforcement learning. By integrating volatility-aware label generation and reasoning-based supervision, Trading-R1 generates actionable, risk-aware trading decisions while maintaining analytical rigor and interpretability.

Trading-R1 offers key advantages over existing approaches through its transparent, scalable pipeline that can be applied to proprietary data and research generation. Unlike general-purpose LLMs that rely on zero-shot prompting, our approach produces consistent, structured analytical reports and enables local deployment. Evaluation on historical market data shows Trading-R1 achieves the best balance of risk-adjusted returns and drawdowns compared to instruction-following and reasoning models, while generating structured, facts-grounded investment theses that support interpretable decision-making.

Trading-R1 is best suited for research support and structured analysis generation for financial professionals. The framework shows promise for institutional applications including data vendors, sell-side research generation, and buy-side decision support with customizable policies. We recommend its use as a tool to augment human decision-making in high-throughput scenarios where structured reasoning and interpretability are valued. Future work will focus on real-time deployment capabilities, scalable offline RL variants for improved sample efficiency, and integration of additional data modalities to enhance robustness and domain adaptability.

Industrial Applications and Future Work

Here, we outline the strengths and limitations of Trading-R1 and highlight potential applications for the financial industry.

Strengths and Contributions

Our Trading-R1, trained entirely on publicly available data curated as Tauric-TR1-DB, offers a transparent, modular, and easily modifiable pipeline for training, observation, and processing. This makes it accessible to researchers who wish to develop their own financial trading reasoning models. The current version shows strong potential in thesis drafting and raw data processing, producing high-quality analytical reports that support trade decisions with reasonable returns and favorable Sharpe ratios. These results indicate that by leveraging open and public data, it is possible to train a market-grounded RL-LLM capable of generating professional-quality financial analyses. The model provides interpretability, robust backtested returns, and strong potential for practical downstream applications. Its key strengths include structured reasoning chains for investment analysis, the ability to denoise diverse data sources effectively, and the capacity to mine actionable insights from textual information.

General-purpose LLMs can process large amounts of financial data through prompting, but relying solely on zero-shot performance is often inefficient. Outputs from such methods do not consistently guarantee fidelity, preferred formatting, or comprehensive coverage of relevant viewpoints. Our approach, by contrast, scales effectively with larger volumes of high-quality input data, combining open datasets with curated internal thesis reports that maintain stronger analytical standards.

All of this is packaged into a 4B-parameter form factor that can run on standard commercial GPUs without the need for massive or expensive servers. This makes deployment more affordable, inference faster on large datasets, and ensures the system can run locally and privately. As a result, sensitive information is protected while maintaining customizability and independence from the internet, which is essential for secure large-scale processing.

Limitations and Challenges

Despite promising results, Trading-R1 faces several important limitations. Trading decision-making itself remains highly challenging, as financial markets are inherently difficult to predict in terms of direction, timing, and portfolio management. Data quality further complicates this task: even after filtering and cleaning, noisy and conflicting information persists, and higher-quality sources remain costly and difficult to obtain. A significant thesis-to-decision gap also exists, since companies with strong fundamentals may still be poor short-term trades, while overvalued firms can continue to rise despite weak financials. Moreover, Trading-R1 is best used as a research and thesis-generation tool, not as a substitute for independent due diligence, since traders with different risk tolerances and strategies can hold opposite yet profitable positions.

From a technical standpoint, our hybrid reward function can introduce training instability, while excessive reinforcement learning may erode the structured reasoning format established during supervised fine-tuning. Hallucinations also persist, particularly in smaller models handling long and noisy contexts, where outputs averaging 32K tokens make token-by-token dependencies fragile. To mitigate this, we penalize overly long generations to preserve conciseness and clarity. Another limitation lies in the training universe, which has been biased toward blue-chip and large-cap companies, especially in AI-related sectors during the bullish 2024–2025 cycle. This introduces a structural long bias. Customization would require incorporating longer historical data, expanding coverage to small- and mid-cap companies, and enabling flexible trading intervals aligned with client needs. Despite these constraints, our approach demonstrates how large language models can improve the consistency, quality, and throughput of financial data processing, offering particular value for data vendors and analysts who must manage large volumes of market information in standardized formats.

Recommended Applications

Given the strengths and limitations of Trading-R1, we recommend its use primarily as a tool for data cleaning, data generation, and research support for human analysts and traders. The model is particularly effective for producing daily key points, structured research summaries, and large-scale data processing that can assist decision-making. Despite encouraging backtesting results, Trading-R1 is not suited for high-stakes scenarios, since even advanced LLMs remain prone to hallucinations and nondeterministic behavior. Backtesting performance should therefore be viewed as evidence of the model’s ability to generate well-grounded reports, rather than as a guarantee of trading success. Reward design and citation mechanisms can improve faithfulness and grounding, but users must still exercise caution. The most appropriate applications are high-throughput tasks where efficiency gains outweigh the need for perfect accuracy. The best users are professionals with sufficient domain expertise to recognize and correct potential errors. For instance, we observed one data source incorrectly reporting the P/E ratio of the S&P 500 as 38, illustrating the importance of pre-filtering input data rather than expecting the model to self-correct without internet access.

Key advantages of Trading-R1 include faster and effective processing, local and private deployment, customization flexibility, and the ability to perform reasoning and thesis generation locally without relying on proprietary external models. This makes it particularly valuable for three key institutional applications:

-

•

Data vendors can process large amounts of raw financial data into structured feeds and standardized formats more cost-effectively than using proprietary models, while maintaining full control over output structure and thesis granularity through in-house deployment.

-

•

Sell-side institutions can train models that understand their investment thesis frameworks and consistently produce research reports in their preferred analytical formats.

-

•

Buy-side institutions can fine-tune the model’s decision-making policy to align with firm-specific investment preferences. For instance, adjusting RFT label ratios to increase long exposure to preferred sectors like technology, or modifying hold ratios during training to reduce trading frequency and match the firm’s investment horizon.

This customization capability enables Trading-R1 to adapt to diverse institutional requirements while ensuring data privacy and analytical consistency across all deployment scenarios.

References

- Bai et al. (2023) J. Bai, S. Bai, Y. Chu, Z. Cui, K. Dang, X. Deng, Y. Fan, W. Ge, Y. Han, F. Huang, B. Hui, L. Ji, M. Li, J. Lin, R. Lin, D. Liu, G. Liu, C. Lu, K. Lu, J. Ma, R. Men, X. Ren, X. Ren, C. Tan, S. Tan, J. Tu, P. Wang, S. Wang, W. Wang, S. Wu, B. Xu, J. Xu, A. Yang, H. Yang, J. Yang, S. Yang, Y. Yao, B. Yu, H. Yuan, Z. Yuan, J. Zhang, X. Zhang, Y. Zhang, Z. Zhang, C. Zhou, J. Zhou, X. Zhou, and T. Zhu. Qwen technical report, 2023. URL https://arxiv.org/abs/2309.16609.

- Brooks (2009) A. Brooks. Reading Price Charts Bar by Bar: the Technical Analysis of Price Action for the Serious Trader. John Wiley & Sons, Inc., Hoboken, New Jersey, USA, 2009. ISBN 978-0-470-44395-8.

- Casper et al. (2023) S. Casper, X. Davies, C. Shi, T. K. Gilbert, J. Scheurer, J. Rando, R. Freedman, T. Korbak, D. Lindner, P. Freire, T. Wang, S. Marks, C.-R. Segerie, M. Carroll, A. Peng, P. Christoffersen, M. Damani, S. Slocum, U. Anwar, A. Siththaranjan, M. Nadeau, E. J. Michaud, J. Pfau, D. Krasheninnikov, X. Chen, L. Langosco, P. Hase, E. Bıyık, A. Dragan, D. Krueger, D. Sadigh, and D. Hadfield-Menell. Open problems and fundamental limitations of reinforcement learning from human feedback, 2023. URL https://arxiv.org/abs/2307.15217.

- DeepSeek-AI et al. (2025) DeepSeek-AI, D. Guo, D. Yang, H. Zhang, J. Song, R. Zhang, R. Xu, Q. Zhu, S. Ma, P. Wang, X. Bi, X. Zhang, X. Yu, Y. Wu, Z. F. Wu, Z. Gou, Z. Shao, Z. Li, Z. Gao, A. Liu, B. Xue, B. Wang, B. Wu, B. Feng, C. Lu, C. Zhao, C. Deng, C. Zhang, C. Ruan, D. Dai, D. Chen, D. Ji, E. Li, F. Lin, F. Dai, F. Luo, G. Hao, G. Chen, G. Li, H. Zhang, H. Bao, H. Xu, H. Wang, H. Ding, H. Xin, H. Gao, H. Qu, H. Li, J. Guo, J. Li, J. Wang, J. Chen, J. Yuan, J. Qiu, J. Li, J. L. Cai, J. Ni, J. Liang, J. Chen, K. Dong, K. Hu, K. Gao, K. Guan, K. Huang, K. Yu, L. Wang, L. Zhang, L. Zhao, L. Wang, L. Zhang, L. Xu, L. Xia, M. Zhang, M. Zhang, M. Tang, M. Li, M. Wang, M. Li, N. Tian, P. Huang, P. Zhang, Q. Wang, Q. Chen, Q. Du, R. Ge, R. Zhang, R. Pan, R. Wang, R. J. Chen, R. L. Jin, R. Chen, S. Lu, S. Zhou, S. Chen, S. Ye, S. Wang, S. Yu, S. Zhou, S. Pan, S. S. Li, S. Zhou, S. Wu, S. Ye, T. Yun, T. Pei, T. Sun, T. Wang, W. Zeng, W. Zhao, W. Liu, W. Liang, W. Gao, W. Yu, W. Zhang, W. L. Xiao, W. An, X. Liu, X. Wang, X. Chen, X. Nie, X. Cheng, X. Liu, X. Xie, X. Liu, X. Yang, X. Li, X. Su, X. Lin, X. Q. Li, X. Jin, X. Shen, X. Chen, X. Sun, X. Wang, X. Song, X. Zhou, X. Wang, X. Shan, Y. K. Li, Y. Q. Wang, Y. X. Wei, Y. Zhang, Y. Xu, Y. Li, Y. Zhao, Y. Sun, Y. Wang, Y. Yu, Y. Zhang, Y. Shi, Y. Xiong, Y. He, Y. Piao, Y. Wang, Y. Tan, Y. Ma, Y. Liu, Y. Guo, Y. Ou, Y. Wang, Y. Gong, Y. Zou, Y. He, Y. Xiong, Y. Luo, Y. You, Y. Liu, Y. Zhou, Y. X. Zhu, Y. Xu, Y. Huang, Y. Li, Y. Zheng, Y. Zhu, Y. Ma, Y. Tang, Y. Zha, Y. Yan, Z. Z. Ren, Z. Ren, Z. Sha, Z. Fu, Z. Xu, Z. Xie, Z. Zhang, Z. Hao, Z. Ma, Z. Yan, Z. Wu, Z. Gu, Z. Zhu, Z. Liu, Z. Li, Z. Xie, Z. Song, Z. Pan, Z. Huang, Z. Xu, Z. Zhang, and Z. Zhang. Deepseek-r1: Incentivizing reasoning capability in llms via reinforcement learning, 2025. URL https://arxiv.org/abs/2501.12948.

- Ding et al. (2023) Y. Ding, S. Jia, T. Ma, B. Mao, X. Zhou, L. Li, and D. Han. Integrating stock features and global information via large language models for enhanced stock return prediction, 2023. URL https://arxiv.org/abs/2310.05627.

- (6) C. H. Dow, W. P. Hamilton, R. Rhea, and E. G. Schaefer. The Dow Theory on Stock Price Movement. Based on 255 editorials in The Wall Street Journal by Charles H. Dow.

- Elliott (1938) R. N. Elliott. The Wave Principle. 1938.

- Ericson et al. (2024) L. Ericson, X. Zhu, X. Han, R. Fu, S. Li, S. Guo, and P. Hu. Deep generative modeling for financial time series with application in var: A comparative review, 2024. URL https://arxiv.org/abs/2401.10370.

- Fatouros et al. (2024) G. Fatouros, K. Metaxas, J. Soldatos, and D. Kyriazis. Can large language models beat wall street? unveiling the potential of ai in stock selection, 2024. URL https://arxiv.org/abs/2401.03737.

- Fjellström (2022) C. Fjellström. Long short-term memory neural network for financial time series, 2022. URL https://arxiv.org/abs/2201.08218.

- Gottweis et al. (2025) J. Gottweis, W.-H. Weng, A. Daryin, T. Tu, A. Palepu, P. Sirkovic, A. Myaskovsky, F. Weissenberger, K. Rong, R. Tanno, K. Saab, D. Popovici, J. Blum, F. Zhang, K. Chou, A. Hassidim, B. Gokturk, A. Vahdat, P. Kohli, Y. Matias, A. Carroll, K. Kulkarni, N. Tomasev, Y. Guan, V. Dhillon, E. D. Vaishnav, B. Lee, T. R. D. Costa, J. R. Penadés, G. Peltz, Y. Xu, A. Pawlosky, A. Karthikesalingam, and V. Natarajan. Towards an ai co-scientist, 2025. URL https://arxiv.org/abs/2502.18864.

- Hendrycks et al. (2021) D. Hendrycks, C. Burns, S. Basart, A. Zou, M. Mazeika, D. Song, and J. Steinhardt. Measuring massive multitask language understanding, 2021. URL https://arxiv.org/abs/2009.03300.

- Hong et al. (2024) S. Hong, M. Zhuge, J. Chen, X. Zheng, Y. Cheng, C. Zhang, J. Wang, Z. Wang, S. K. S. Yau, Z. Lin, L. Zhou, C. Ran, L. Xiao, C. Wu, and J. Schmidhuber. Metagpt: Meta programming for a multi-agent collaborative framework, 2024. URL https://arxiv.org/abs/2308.00352.

- Hu et al. (2021) E. J. Hu, Y. Shen, P. Wallis, Z. Allen-Zhu, Y. Li, S. Wang, L. Wang, and W. Chen. Lora: Low-rank adaptation of large language models, 2021. URL https://arxiv.org/abs/2106.09685.

- Ji et al. (2023) Z. Ji, T. Yu, Y. Xu, N. Lee, E. Ishii, and P. Fung. Towards mitigating hallucination in large language models via self-reflection, 2023. URL https://arxiv.org/abs/2310.06271.

- Kaufmann et al. (2023) T. Kaufmann, P. Weng, V. Bengs, and E. Hüllermeier. A survey of reinforcement learning from human feedback. arXiv preprint arXiv:2312.14925, 10, 2023.

- Kaufmann et al. (2024) T. Kaufmann, P. Weng, V. Bengs, and E. Hüllermeier. A survey of reinforcement learning from human feedback, 2024. URL https://arxiv.org/abs/2312.14925.

- Kirtac and Germano (2024) K. Kirtac and G. Germano. Sentiment trading with large language models. Finance Research Letters, 62:105227, 2024. ISSN 1544-6123. https://doi.org/10.1016/j.frl.2024.105227. URL https://www.sciencedirect.com/science/article/pii/S1544612324002575.

- Koa et al. (2024) K. J. Koa, Y. Ma, R. Ng, and T.-S. Chua. Learning to generate explainable stock predictions using self-reflective large language models, May 2024. URL http://dx.doi.org/10.1145/3589334.3645611.

- Lambert et al. (2024) N. Lambert, V. Pyatkin, J. Morrison, L. Miranda, B. Y. Lin, K. Chandu, N. Dziri, S. Kumar, T. Zick, Y. Choi, et al. Rewardbench: Evaluating reward models for language modeling. arXiv preprint arXiv:2403.13787, 2024.

- Lee et al. (2025) J. Lee, N. Stevens, and S. C. Han. Large language models in finance (finllms). Neural Computing and Applications, Jan. 2025. ISSN 1433-3058. 10.1007/s00521-024-10495-6. URL http://dx.doi.org/10.1007/s00521-024-10495-6.

- Lefevre and Markman (2010) E. Lefevre and J. D. Markman. Reminiscences of a stock operator: With new commentary and insights on the life and times of Jesse Livermore. John Wiley & Sons, 2010.

- Li et al. (2023) Y. Li, Y. Yu, H. Li, Z. Chen, and K. Khashanah. Tradinggpt: Multi-agent system with layered memory and distinct characters for enhanced financial trading performance. arXiv preprint arXiv:2309.03736, 2023.

- Liu et al. (2025a) H. Liu, X. Zhang, H. Xu, Y. Wanyan, J. Wang, M. Yan, J. Zhang, C. Yuan, C. Xu, W. Hu, and F. Huang. Pc-agent: A hierarchical multi-agent collaboration framework for complex task automation on pc, 2025a. URL https://arxiv.org/abs/2502.14282.

- Liu et al. (2025b) Z. Liu, X. Guo, F. Lou, L. Zeng, J. Niu, Z. Wang, J. Xu, W. Cai, Z. Yang, X. Zhao, C. Li, S. Xu, D. Chen, Y. Chen, Z. Bai, and L. Zhang. Fin-r1: A large language model for financial reasoning through reinforcement learning, 2025b. URL https://arxiv.org/abs/2503.16252.

- Lopez-Lira and Tang (2023) A. Lopez-Lira and Y. Tang. Can chatgpt forecast stock price movements? return predictability and large language models, 2023. URL https://arxiv.org/abs/2304.07619.

- Lu et al. (2023) D. Lu, H. Wu, J. Liang, Y. Xu, Q. He, Y. Geng, M. Han, Y. Xin, and Y. Xiao. Bbt-fin: Comprehensive construction of chinese financial domain pre-trained language model, corpus and benchmark, 2023. URL https://arxiv.org/abs/2302.09432.

- Lu et al. (2024) P. Lu, H. Bansal, T. Xia, J. Liu, C. Li, H. Hajishirzi, H. Cheng, K.-W. Chang, M. Galley, and J. Gao. Mathvista: Evaluating mathematical reasoning of foundation models in visual contexts, 2024. URL https://arxiv.org/abs/2310.02255.

- Meng et al. (2024) Y. Meng, M. Xia, and D. Chen. Simpo: Simple preference optimization with a reference-free reward. Advances in Neural Information Processing Systems, 37:124198–124235, 2024.

- OpenAI et al. (2024) OpenAI, :, A. Jaech, A. Kalai, A. Lerer, A. Richardson, A. El-Kishky, A. Low, A. Helyar, A. Madry, A. Beutel, A. Carney, A. Iftimie, A. Karpenko, A. T. Passos, A. Neitz, A. Prokofiev, A. Wei, A. Tam, A. Bennett, A. Kumar, A. Saraiva, A. Vallone, A. Duberstein, A. Kondrich, A. Mishchenko, A. Applebaum, A. Jiang, A. Nair, B. Zoph, B. Ghorbani, B. Rossen, B. Sokolowsky, B. Barak, B. McGrew, B. Minaiev, B. Hao, B. Baker, B. Houghton, B. McKinzie, B. Eastman, C. Lugaresi, C. Bassin, C. Hudson, C. M. Li, C. de Bourcy, C. Voss, C. Shen, C. Zhang, C. Koch, C. Orsinger, C. Hesse, C. Fischer, C. Chan, D. Roberts, D. Kappler, D. Levy, D. Selsam, D. Dohan, D. Farhi, D. Mely, D. Robinson, D. Tsipras, D. Li, D. Oprica, E. Freeman, E. Zhang, E. Wong, E. Proehl, E. Cheung, E. Mitchell, E. Wallace, E. Ritter, E. Mays, F. Wang, F. P. Such, F. Raso, F. Leoni, F. Tsimpourlas, F. Song, F. von Lohmann, F. Sulit, G. Salmon, G. Parascandolo, G. Chabot, G. Zhao, G. Brockman, G. Leclerc, H. Salman, H. Bao, H. Sheng, H. Andrin, H. Bagherinezhad, H. Ren, H. Lightman, H. W. Chung, I. Kivlichan, I. O’Connell, I. Osband, I. C. Gilaberte, I. Akkaya, I. Kostrikov, I. Sutskever, I. Kofman, J. Pachocki, J. Lennon, J. Wei, J. Harb, J. Twore, J. Feng, J. Yu, J. Weng, J. Tang, J. Yu, J. Q. Candela, J. Palermo, J. Parish, J. Heidecke, J. Hallman, J. Rizzo, J. Gordon, J. Uesato, J. Ward, J. Huizinga, J. Wang, K. Chen, K. Xiao, K. Singhal, K. Nguyen, K. Cobbe, K. Shi, K. Wood, K. Rimbach, K. Gu-Lemberg, K. Liu, K. Lu, K. Stone, K. Yu, L. Ahmad, L. Yang, L. Liu, L. Maksin, L. Ho, L. Fedus, L. Weng, L. Li, L. McCallum, L. Held, L. Kuhn, L. Kondraciuk, L. Kaiser, L. Metz, M. Boyd, M. Trebacz, M. Joglekar, M. Chen, M. Tintor, M. Meyer, M. Jones, M. Kaufer, M. Schwarzer, M. Shah, M. Yatbaz, M. Y. Guan, M. Xu, M. Yan, M. Glaese, M. Chen, M. Lampe, M. Malek, M. Wang, M. Fradin, M. McClay, M. Pavlov, M. Wang, M. Wang, M. Murati, M. Bavarian, M. Rohaninejad, N. McAleese, N. Chowdhury, N. Chowdhury, N. Ryder, N. Tezak, N. Brown, O. Nachum, O. Boiko, O. Murk, O. Watkins, P. Chao, P. Ashbourne, P. Izmailov, P. Zhokhov, R. Dias, R. Arora, R. Lin, R. G. Lopes, R. Gaon, R. Miyara, R. Leike, R. Hwang, R. Garg, R. Brown, R. James, R. Shu, R. Cheu, R. Greene, S. Jain, S. Altman, S. Toizer, S. Toyer, S. Miserendino, S. Agarwal, S. Hernandez, S. Baker, S. McKinney, S. Yan, S. Zhao, S. Hu, S. Santurkar, S. R. Chaudhuri, S. Zhang, S. Fu, S. Papay, S. Lin, S. Balaji, S. Sanjeev, S. Sidor, T. Broda, A. Clark, T. Wang, T. Gordon, T. Sanders, T. Patwardhan, T. Sottiaux, T. Degry, T. Dimson, T. Zheng, T. Garipov, T. Stasi, T. Bansal, T. Creech, T. Peterson, T. Eloundou, V. Qi, V. Kosaraju, V. Monaco, V. Pong, V. Fomenko, W. Zheng, W. Zhou, W. McCabe, W. Zaremba, Y. Dubois, Y. Lu, Y. Chen, Y. Cha, Y. Bai, Y. He, Y. Zhang, Y. Wang, Z. Shao, and Z. Li. Openai o1 system card, 2024. URL https://arxiv.org/abs/2412.16720.

- OpenAI et al. (2025) OpenAI, :, S. Agarwal, L. Ahmad, J. Ai, S. Altman, A. Applebaum, E. Arbus, R. K. Arora, Y. Bai, B. Baker, H. Bao, B. Barak, A. Bennett, T. Bertao, N. Brett, E. Brevdo, G. Brockman, S. Bubeck, C. Chang, K. Chen, M. Chen, E. Cheung, A. Clark, D. Cook, M. Dukhan, C. Dvorak, K. Fives, V. Fomenko, T. Garipov, K. Georgiev, M. Glaese, T. Gogineni, A. Goucher, L. Gross, K. G. Guzman, J. Hallman, J. Hehir, J. Heidecke, A. Helyar, H. Hu, R. Huet, J. Huh, S. Jain, Z. Johnson, C. Koch, I. Kofman, D. Kundel, J. Kwon, V. Kyrylov, E. Y. Le, G. Leclerc, J. P. Lennon, S. Lessans, M. Lezcano-Casado, Y. Li, Z. Li, J. Lin, J. Liss, Lily, Liu, J. Liu, K. Lu, C. Lu, Z. Martinovic, L. McCallum, J. McGrath, S. McKinney, A. McLaughlin, S. Mei, S. Mostovoy, T. Mu, G. Myles, A. Neitz, A. Nichol, J. Pachocki, A. Paino, D. Palmie, A. Pantuliano, G. Parascandolo, J. Park, L. Pathak, C. Paz, L. Peran, D. Pimenov, M. Pokrass, E. Proehl, H. Qiu, G. Raila, F. Raso, H. Ren, K. Richardson, D. Robinson, B. Rotsted, H. Salman, S. Sanjeev, M. Schwarzer, D. Sculley, H. Sikchi, K. Simon, K. Singhal, Y. Song, D. Stuckey, Z. Sun, P. Tillet, S. Toizer, F. Tsimpourlas, N. Vyas, E. Wallace, X. Wang, M. Wang, O. Watkins, K. Weil, A. Wendling, K. Whinnery, C. Whitney, H. Wong, L. Yang, Y. Yang, M. Yasunaga, K. Ying, W. Zaremba, W. Zhan, C. Zhang, B. Zhang, E. Zhang, and S. Zhao. gpt-oss-120b and gpt-oss-20b model card, 2025. URL https://arxiv.org/abs/2508.10925.

- Ouyang et al. (2022) L. Ouyang, J. Wu, X. Jiang, D. Almeida, C. Wainwright, P. Mishkin, C. Zhang, S. Agarwal, K. Slama, A. Ray, et al. Training language models to follow instructions with human feedback. Advances in neural information processing systems, 35:27730–27744, 2022.

- Petram (2014) L. Petram. The world’s first stock exchange. Columbia University Press, 2014.

- Poddar et al. (2024) S. Poddar, Y. Wan, H. Ivison, A. Gupta, and N. Jaques. Personalizing reinforcement learning from human feedback with variational preference learning. In The Thirty-eighth Annual Conference on Neural Information Processing Systems, 2024. URL https://openreview.net/forum?id=gRG6SzbW9p.

- Qian et al. (2025) L. Qian, W. Zhou, Y. Wang, X. Peng, H. Yi, Y. Zhao, J. Huang, Q. Xie, and J. yun Nie. Fino1: On the transferability of reasoning-enhanced llms and reinforcement learning to finance, 2025. URL https://arxiv.org/abs/2502.08127.

- Rafailov et al. (2023) R. Rafailov, A. Sharma, E. Mitchell, C. D. Manning, S. Ermon, and C. Finn. Direct preference optimization: Your language model is secretly a reward model. Advances in Neural Information Processing Systems, 36:53728–53741, 2023.

- Schulman et al. (2017) J. Schulman, F. Wolski, P. Dhariwal, A. Radford, and O. Klimov. Proximal policy optimization algorithms, 2017. URL https://arxiv.org/abs/1707.06347.

- Schwager (2012) J. D. Schwager. Market Wizards: Interviews with Top Traders. Wiley, updated edition, February 2012. ISBN 978-1-118-27305-0.

- Shao et al. (2024a) Z. Shao, P. Wang, Q. Zhu, R. Xu, J. Song, X. Bi, H. Zhang, M. Zhang, Y. Li, Y. Wu, et al. Deepseekmath: Pushing the limits of mathematical reasoning in open language models. arXiv preprint arXiv:2402.03300, 2024a.

- Shao et al. (2024b) Z. Shao, P. Wang, Q. Zhu, R. Xu, J. Song, X. Bi, H. Zhang, M. Zhang, Y. K. Li, Y. Wu, and D. Guo. Deepseekmath: Pushing the limits of mathematical reasoning in open language models, 2024b. URL https://arxiv.org/abs/2402.03300.

- Tatsat and Shater (2025) H. Tatsat and A. Shater. Beyond the black box: Interpretability of llms in finance, 2025. URL https://arxiv.org/abs/2505.24650.

- Wang et al. (2024) M. Wang, K. Izumi, and H. Sakaji. Llmfactor: Extracting profitable factors through prompts for explainable stock movement prediction, 2024. URL https://arxiv.org/abs/2406.10811.

- Wang et al. (2023) S. Wang, H. Yuan, L. Zhou, L. M. Ni, H.-Y. Shum, and J. Guo. Alpha-gpt: Human-ai interactive alpha mining for quantitative investment. arXiv preprint arXiv:2308.00016, 2023. URL https://arxiv.org/abs/2308.00016.

- Wu et al. (2023) S. Wu, O. Irsoy, S. Lu, V. Dabravolski, M. Dredze, S. Gehrmann, P. Kambadur, D. Rosenberg, and G. Mann. Bloomberggpt: A large language model for finance, 2023. URL https://arxiv.org/abs/2303.17564.

- Xiao et al. (2025) Y. Xiao, E. Sun, D. Luo, and W. Wang. Tradingagents: Multi-agents llm financial trading framework, 2025. URL https://arxiv.org/abs/2412.20138.

- Xie et al. (2023) Q. Xie, W. Han, X. Zhang, Y. Lai, M. Peng, A. Lopez-Lira, and J. Huang. Pixiu: A large language model, instruction data and evaluation benchmark for finance, 2023. URL https://arxiv.org/abs/2306.05443.

- Xing (2024) F. Xing. Designing heterogeneous llm agents for financial sentiment analysis, 2024. URL https://arxiv.org/abs/2401.05799.

- Yang et al. (2023) H. Yang, X.-Y. Liu, and C. D. Wang. Fingpt: Open-source financial large language models, 2023. URL https://arxiv.org/abs/2306.06031.

- Yu et al. (2023) Y. Yu, H. Li, Z. Chen, Y. Jiang, Y. Li, D. Zhang, R. Liu, J. W. Suchow, and K. Khashanah. Finmem: A performance-enhanced llm trading agent with layered memory and character design, 2023. URL https://arxiv.org/abs/2311.13743.

- Zhang et al. (2023a) B. Zhang, H. Yang, and X.-Y. Liu. Instruct-fingpt: Financial sentiment analysis by instruction tuning of general-purpose large language models, 2023a. URL https://arxiv.org/abs/2306.12659.

- Zhang et al. (2024a) H. Zhang, F. Hua, C. Xu, H. Kong, R. Zuo, and J. Guo. Unveiling the potential of sentiment: Can large language models predict chinese stock price movements?, 2024a. URL https://arxiv.org/abs/2306.14222.

- Zhang et al. (2022) S. Zhang, S. Roller, N. Goyal, M. Artetxe, M. Chen, S. Chen, C. Dewan, M. Diab, X. Li, X. V. Lin, T. Mihaylov, M. Ott, S. Shleifer, K. Shuster, D. Simig, P. S. Koura, A. Sridhar, T. Wang, and L. Zettlemoyer. Opt: Open pre-trained transformer language models, 2022. URL https://arxiv.org/abs/2205.01068.

- Zhang et al. (2024b) W. Zhang, L. Zhao, H. Xia, S. Sun, J. Sun, M. Qin, X. Li, Y. Zhao, Y. Zhao, X. Cai, L. Zheng, X. Wang, and B. An. A multimodal foundation agent for financial trading: Tool-augmented, diversified, and generalist, 2024b. URL https://arxiv.org/abs/2402.18485.

- Zhang et al. (2023b) X. Zhang, Q. Yang, and D. Xu. Xuanyuan 2.0: A large chinese financial chat model with hundreds of billions parameters, 2023b. URL https://arxiv.org/abs/2305.12002.

7 Data Collection

Training a financial reasoning model that is both useful and auditable requires data that captures the diverse information channels traders and firms rely on in practice. To this end, we assemble a large, time-stamped corpus spanning assets, market regimes, and horizons, with multiple modalities and data dimensions. Each reasoning artifact (corporate filings, earnings commentary, reputable news, and technical signals) is aligned with price series under strict pre/post ordering to prevent lookahead bias.

This diversity and temporal discipline are essential for two reasons. First, the format objectives require high-quality exemplars of market analysis so the model can learn reasoning patterns that are coherent, verifiable, and well structured. Second, the outcome objectives require clean data of heterogeneous inputs from technical indicators, news, and sentiment to discrete trading actions and benchmarked excess returns over fixed horizons so that the model can learn meaningful connections of the data to trends in the market. This ensures that the learned reward captures directional accuracy, signal strength, and trading frictions. In short, the quality of the input data directly determines whether the model produces reasoning that is coherent, logical, and grounded in real market conditions.

The dataset is built in two stages. In the first stage, we collect large-scale raw inputs consisting of textual sources and numerical technical indicators. These inputs form the contextual foundation provided to the reasoning model. In the second stage, we integrate and structure these raw inputs into temporally grounded samples. For each trading day and ticker, we assemble the relevant documents and signals into a single input prompt that reflects the information available at that time. Each structured sample can then be paired with downstream labels for both supervised fine-tuning (SFT) and reinforcement learning (RL).

To ensure fairness and reproducibility, all data are sourced from publicly available providers with documented provenance and are collected through transparent, versioned pipelines.

7.1 Large-Scale Raw Data Collection

To ensure the training data captures a broad and meaningful diversity of inputs, we draw from five major categories of financial information: news related to the asset, technical indicators for both the asset and the broader market, fundamental financial data, sentiment surrounding the company or asset, and macroeconomic factors. Together, these categories provide comprehensive coverage of sources and data types, allowing the model to identify reliable patterns that reflect both market conditions and asset-specific dynamics. The collection process for each category is detailed below.

7.1.1 News

| Time Horizon | Date Range (relative to ) | Max Samples |

|---|---|---|

| Last 3 days | days to | 10 |

| Last 4–10 days | days to days | 20 |

| Last 11–30 days | days to days | 20 |

To construct a robust news dataset, we implemented two complementary pipelines: structured financial APIs and broader web sources. This dual-source design balances timeliness with diversity, exposing the model to both precise market-moving signals and a wide range of narrative perspectives. All news was segmented into temporal buckets (Table 5), enabling the model to distinguish between recent developments, medium-term narratives, and older but still relevant context. This captures the natural decay of informational value over time, aligning the dataset with real-world trading dynamics. Finnhub was chosen for its structured, real-time financial coverage, while Google News was used to aggregate heterogeneous media perspectives, mitigating source bias and capturing broader narrative context. Integrating both sources preserves temporal precision while enriching coverage breadth, supporting downstream tasks that depend on both hard financial events and softer sentiment-driven dynamics.

Finnhub API