Learning Explainable Stock Predictions with Tweets Using Mixture of Experts

Abstract

Stock price movements are influenced by many factors, and alongside historical price data, textual information is a key source. Public news and social media offer valuable insights into market sentiment and emerging events. These sources are fast-paced, diverse, and significantly impact future stock trends. Recently, LLMs have enhanced financial analysis, but prompt-based methods still have limitations, such as input length restrictions and difficulties in predicting sequences of varying lengths. Additionally, most models rely on dense computational layers, which are resource-intensive. To address these challenges, we propose the FTS-Text-MoE model, which combines numerical data with key summaries from news and tweets using point embeddings, boosting prediction accuracy through the integration of factual textual data. The model uses a Mixture of Experts (MoE) Transformer decoder to process both data types. By activating only a subset of model parameters, it reduces computational costs. Furthermore, the model features multi-resolution prediction heads, enabling flexible forecasting of financial time series at different scales. Experimental results show that FTS-Text-MoE outperforms baseline methods in terms of investment returns and Sharpe ratio, demonstrating its superior accuracy and ability to predict future market trends.

Learning Explainable Stock Predictions with Tweets Using Mixture of Experts

Wenyan Xu1††thanks: Equal contribution Dawei Xiang211footnotemark: 1 Rundong Wang3 Yonghong Hu1 Liang Zhang4 Jiayu Chen5 Zhonghua Lu6 1Central University of Finance and Economics 2University of Connecticut 3Nanyang Technological University 4The Hong Kong University of Science and Technology (Guangzhou) 5Hong Kong University 6University of Chinese Academy of Sciences

1 Introduction

Stock price prediction is inherently a time series problem, and time series regression models have long been central to financial valuation. Traditional methods such as linear regressionMontgomery et al. (2021), ARIMAAriyo et al. (2014), and GARCHFrancq and Zakoian (2019) typically assume long-term market stability and rely on predefined assumptions. However, these methods are limited in their ability to capture complex market dependencies and adapt to sudden market events (Malkiel, 1999). Recent studies have highlighted the advantages of machine learning techniques, which excel at modeling long-term dependencies and detecting market volatility, overcoming the reliance on prior assumptions typical of traditional methodsKumar et al. (2024).

Unlike traditional models that rely solely on numerical data, deep learning modelsKoa et al. (2023) can integrate multi-dimensional, heterogeneous information to improve prediction accuracy. Harry Markowitz’s Modern Portfolio TheoryKonstantinov et al. (2020) emphasizes the importance of market correlations, while research by Hsu et al. (2021) demonstrates a positive correlation between emotions in news, blogs, and social media and stock market trendsHsu et al. (2021). However, relying solely on sentiment scores may overlook key details in text content, failing to fully tap into its potential. Therefore, integrating richer and more comprehensive text data into stock prediction models has become increasingly important.

Recent cross-modal time series prediction methods based on large language models (LLMs) have demonstrated outstanding performance. In the latest portfolio optimization applications, SocioDojoCheng and Chin and SEPKoa et al. (2024) use knowledge-aligned text prompts to help LLMs make more accurate decisions. However, these methods are limited by the input context length, processing only a limited amount of text, and have a restricted prediction horizon. Furthermore, they typically perform binary classification to predict stock price trends rather than accurately forecasting the next value in the time series. Additionally, the computational cost of invoking LLMs is significant. Unlike the aforementioned prompt-based methods, we sort news and tweet data by time and extract 1-2 key factual summaries at each time point, aligning them with numerical time series via point embeddings. Additionally, we predict the actual stock price value, rather than just the trend.

Most time series prediction models rely on dense layers, requiring the computation of all parameters for each input token. Although these methods are computationally accurate, they consume substantial resources. Sparse techniques, such as the Mixture of Experts (MoE), improve computational efficiency and model performance under fixed inference constraints. Based on this, we propose the Financial Time Series-Text-MoE (FTS-Text-MoE) model, a decoder-only transformer architecture specifically designed for stock price prediction. The model uses a sparse transformer decoder, selectively activating parameters to significantly reduce computational costs. Additionally, we design multi-resolution prediction heads to enable more flexible predictions for time series of varying lengths.

Key contributions of this study include:

-

•

We resolved technical issues in crawling public news data and updated the Nasdaq news dataset in the FNSPID project 111https://github.com/Zdong104/FNSPID_Financial_News_Dataset to January 19, 2025 (the original dataset was until 2023), detailed in Appendix B.3.

-

•

We introduced the FTS-Text-MoE model , specifically designed for stock price prediction, which effectively aligns time series data with text data, improving prediction accuracy.

-

•

We demonstrated through experiments that FTS-Text-MoE outperforms traditional benchmark methods in accurately predicting financial time series trends, with significant improvements in investment returns and Sharpe ratio.

2 Related Works

Early studies on stock prediction using text analysis employed support vector machines (SVM) to extract basic features from text, such as bag-of-words, noun phrases, and named entities Schumaker and Chen (2009). These shallow features were later replaced by structured tuples (e.g., subject, action, object) extracted by deep neural networks Ding et al. (2015); Deng et al. (2019). Additionally, Xu and Cohen (2018) extracted implicit text vectors and used variational autoencoders (VAE) to model stock price prediction as a binary classification problem. As understanding of text complexity grew, Xu and Cohen (2018); Yang et al. (2020); Deng et al. (2019) began extracting richer implicit information from pre-trained text embeddings. Recent studies, such as Wang et al. (2025); Liu et al. (2025), used text as prompts to further enhance the accuracy of LLMs in time-series prediction. Unlike these methods, our research couples text sentences at each time point with corresponding time series data, predicting the next time series value, providing clearer analysis and exploring the specific impact of text on stock price fluctuations.

Sparse Deep Learning for Time Series. Deep learning models are typically large-scale and parameter-intensive Hoefler et al. (2021), requiring significant memory and computational resources. Sparse networks, such as MoE Jacobs et al. (1991), use dynamic routing to specialized experts, improving efficiency while maintaining or exceeding generalization performance Fedus et al. (2022). Traditional time series models, like DLinear Zeng et al. (2023) and SparseTSF Lin et al. (2024), are usually smaller and have less focus on sparse methods. After large-scale pretraining, studies such as MoLE Ni et al. (2024) and IME Ismail et al. explore sparsity but are not fully sparse models, as they route inputs to all attention heads before aggregation. The recent study Time-MoE Shi et al. (2024) uses sparse foundational models for general time-series forecasting but does not consider the impact of real-world textual information on numerical features. We further investigate whether complex textual information can enhance the interpretability of numerical predictions.

3 Methodology

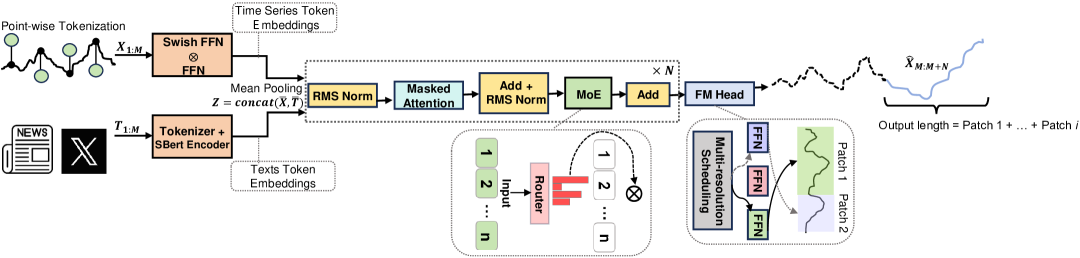

We propose FTS-Text-MoE (Figure 1), a decoder-only Transformer architecture utilizing an MoE framework. The model comprises three components: (1) input token embedding, (2) MoE Transformer module, and (3) multi-resolution forecasting.

Problem Formulation.

Given historical numerical observations and corresponding textual data over the past days, our goal is to predict the next days: where represents the proposed model. FTS-Text-MoE supports flexible context lengths () and forecasting horizons () during inference, unlike traditional fixed-horizon models. Following the channel independence principle from Nie et al. , multivariate series are decomposed into univariate series, enabling better generalization across tasks.

3.1 Input Token Embedding

Text Token Embedding

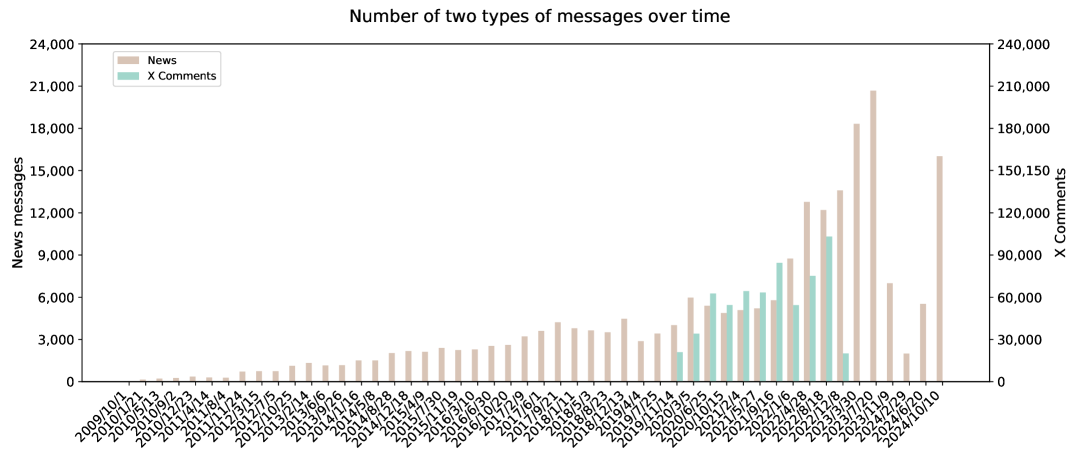

We present an efficient pipeline for converting raw text into high-quality embeddings. On a daily basis, we select the top news articles and X Comments (Figure 2), embedding them using a pretrained DistilBART-12-6-cnn model222https://huggingface.co/sshleifer/distilbart-cnn-12-6. The resulting summaries are tokenized using the MiniLM L3 v2 (para) tokenizer333https://huggingface.co/sentence-transformers/paraphrase-MiniLM-L3-v2 and subsequently transformed into semantic representations using the SBertEncoder.

Time Token Embedding

Each time point in the financial time series is embedded using SwiGLU Shazeer (2020):

| (1) |

where and and are learnable parameters, and denotes the hidden dimension.

Textual and numerical embeddings undergo mean pooling for aggregation before entering the subsequent MoE Transformer modules.

| Sector | Chronos | Moirai | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MSE () | MAE () | MSE () | MAE () | MSE () | MAE () | MSE () | MAE () | MSE () | MAE () | |

| Basic Materials | 0.6458 | 0.8112 | 0.8725 | 0.8399 | 0.5540 | 0.6591 | 0.1972 | 0.3849 | 0.3866 | 0.5505 |

| Financial Services | 0.7247 | 0.7549 | 0.7466 | 0.7644 | 0.5498 | 0.6429 | 0.2060 | 0.3913 | 0.2077 | 0.3914 |

| Consumer Defensive | 0.1946 | 0.4503 | 0.1533 | 0.3558 | 0.5717 | 0.6721 | 0.5717 | 0.6721 | 0.5700 | 0.6710 |

| Utilities | 0.7518 | 0.9498 | 0.2517 | 0.4080 | 0.2797 | 0.4188 | 0.2797 | 0.4188 | 0.0527 | 0.1698 |

| Energy | 0.2094 | 0.3878 | 0.3204 | 0.4979 | 0.4196 | 0.5835 | 0.4196 | 0.5835 | 0.1392 | 0.3615 |

| Technology | 0.8681 | 0.8893 | 0.5858 | 0.5920 | 0.7480 | 0.7412 | 0.8688 | 0.8279 | 0.1538 | 0.3643 |

| Consumer Cyclical | 0.3628 | 0.5345 | 0.8673 | 0.9623 | 0.3116 | 0.5074 | 0.1632 | 0.3486 | 0.1049 | 0.2252 |

| Real Estate | 0.2282 | 0.4495 | 0.3687 | 0.4488 | 0.3567 | 0.5419 | 0.3892 | 0.5461 | 0.3550 | 0.5420 |

| Healthcare | 0.3521 | 0.4199 | 0.5786 | 0.6337 | 0.2248 | 0.4226 | 0.0705 | 0.2162 | 0.1299 | 0.3057 |

| Communication Services | 0.2029 | 0.3351 | 0.7599 | 0.8566 | 0.3388 | 0.5166 | 0.0511 | 0.1817 | 0.0697 | 0.2225 |

| Industrials | 0.4708 | 0.5574 | 0.2126 | 0.5158 | 0.1226 | 0.2743 | 0.5829 | 0.6761 | 0.1224 | 0.2741 |

3.2 FTS-Text-MoE Transformer

Inspired by Shi et al. (2024), we utilize a decoder-only Transformer Vaswani et al. (2017); Chen et al. (2024), incorporating advancements from LLMs Touvron et al. (2023). To enhance training stability, we apply RMSNorm Zhang and Sennrich (2019) at each sub-layer input. Rotary Positional Embeddings Su et al. (2024) improve sequence flexibility and extrapolation. Following Chowdhery et al. (2023), we eliminate most biases, retaining them only in the QKV layers of self-attention for better extrapolation. Formally, the architecture is defined as follows:

|

|

(2) |

To introduce sparsity, we replace the standard FFN with a MoE layer, sharing a pool of sparsely activated experts. Each Mixture layer comprises multiple expert networks akin to standard FFNs, where each timestep routes inputs to either a single expert Fedus et al. (2022) or multiple experts Lepikhin et al. . One shared expert captures common knowledge across contexts. The Mixture function is defined as follows:

| (3) | |||

| (4) | |||

| (5) | |||

| (6) |

Here, are trainable parameters, is the number of non-shared experts, and denotes the activated non-shared experts per MoE layer.

FTS-Text-MoE boosts efficiency by activating only a subset of its 113M parameters, with just 50M active during operation. This selective activation enables the model to utilize specialized experts, boosting efficiency while preserving scalability.

3.3 Multi-resolution Prediction

Unlike existing foundational models, which typically output predictions at a fixed horizon, our model incorporates a multi-resolution prediction head followed by Shi et al. (2024). This prediction head consists of () output projections, each targeting a specific forecasting horizon , predicting future timesteps. During inference, we apply a greedy scheduling algorithm to concatenate these projections, enabling flexible, arbitrary-length forecasting and enhancing the adaptability of FTS-Text-MoE.

3.4 Loss Function

The multi-resolution prediction head comprises several single-layer FFN output projections, each dedicated to a specific forecasting horizon. The final loss combines autoregressive losses across multiple resolutions and an auxiliary balancing loss, as detailed in Appendix A.1:

| (7) | ||||

Where denotes the number of multi-resolution projections, and represents the horizon length of the -th projection. (autoregressive loss) quantifies the difference between actual and predicted values to optimize prediction accuracy, while (auxiliary loss) balances expert utilization, ensuring more even distribution and enhancing training efficiency.

4 Experiments

To evaluate the effectiveness of FTS-Text-MoE, we compared it with state-of-the-art language models designed for time series prediction. Details on datasets and metrics can be found in Appendix B.

4.1 Baselines

We use state-of-the-art models designed for long-term time series forecasting as baselines.

Chronos: Chronos Ansari et al. discretizes time series into intervals by scaling and quantizing real values. This enables training language models on the "language of time series" without altering the model architecture. We evaluate Chronos models (t5-small444https://huggingface.co/amazon/chronos-t5-small/base555https://huggingface.co/amazon/chronos-t5-base/large666https://huggingface.co/amazon/chronos-t5-large).

Moirai: Moirai Woo et al. (2024) concatenates multivariate time series into a single sequence with [MASK] tokens for prediction, and the model uses multi-granularity patching to handle different frequencies. We evaluate Moirai models (t5-small777https://huggingface.co/Salesforce/moirai-moe-1.0-R-small/base888https://huggingface.co/Salesforce/moirai-moe-1.0-R-base).

4.2 Performance Comparison

In this section, we quantitatively and qualitatively assess the predictive performance of our FTS-Text-MoE model against those baselines.

4.2.1 Effect of Text Source and Length on Prediction Accuracy

We compare performance using Mean Squared Error (MSE) and Mean Absolute Error (MAE) across 11 industry sectors, integrating stock time series data with various textual inputs—summarized news and summarized X comments. Lower MSE and MAE values indicate superior predictive accuracy.

Our analysis highlights that adding summarized news or tweet inputs significantly improves stock movement prediction accuracy (Table 1). Specifically, using summarized X comments results in consistently lower MSE and MAE compared to models using only news or other inputs. This indicates that distilled sentiment signals effectively reduce noise and enhance prediction accuracy. Industry-level analysis reveals that sectors like Healthcare, Consumer Cyclical, and Communication Services exhibit lower prediction errors, suggesting a strong reliance on textual signals and improved performance with text integration. In contrast, industries like Energy and Industrials, which experience higher volatility, show improved accuracy with textual inputs but still exhibit larger errors.

4.2.2 Prediction Performance of TS Models

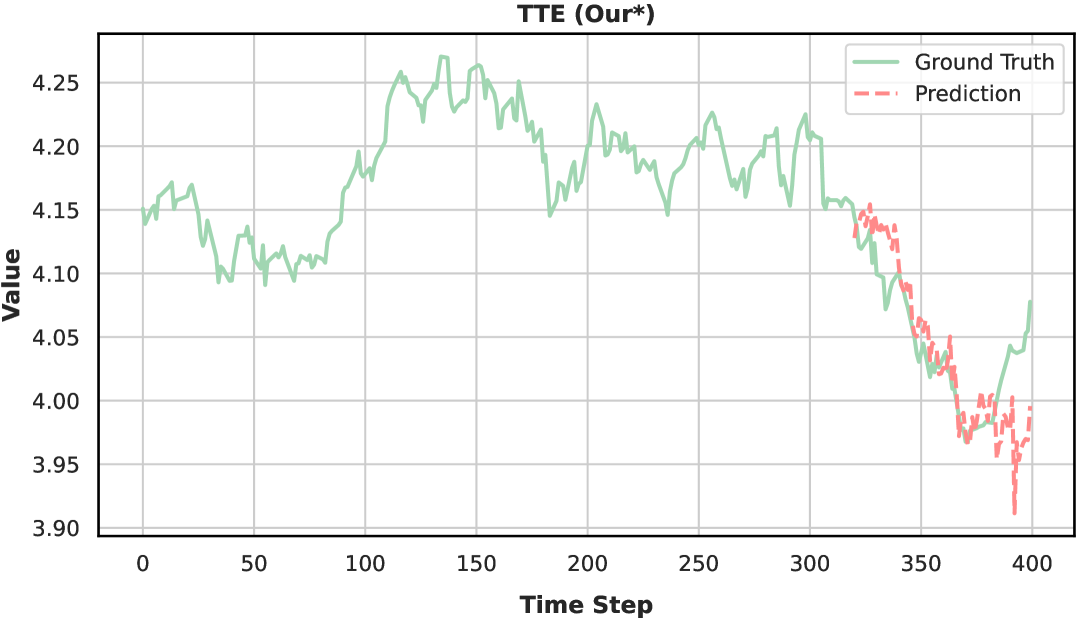

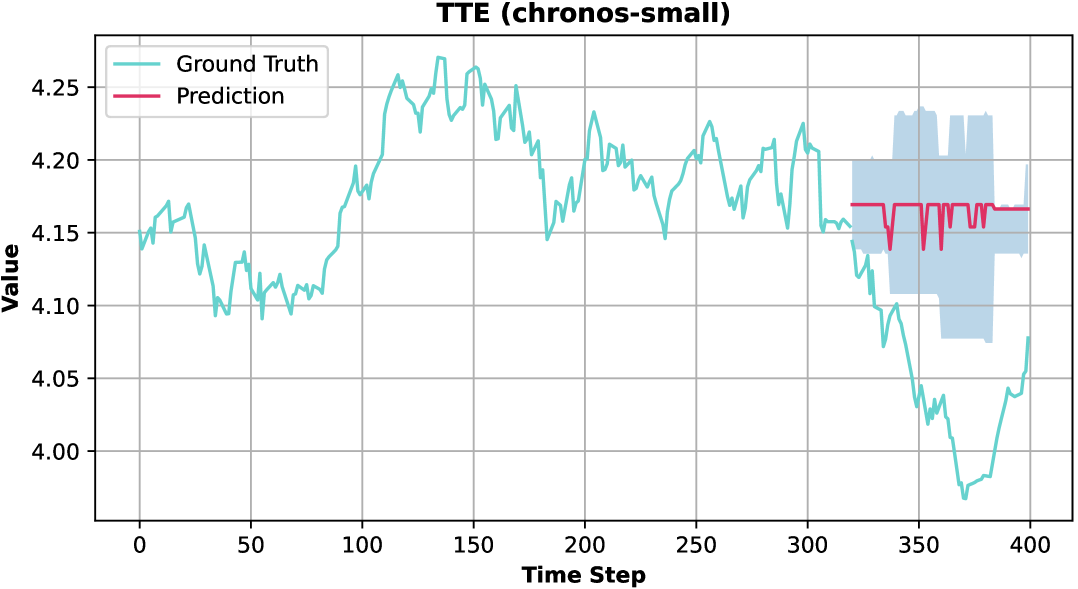

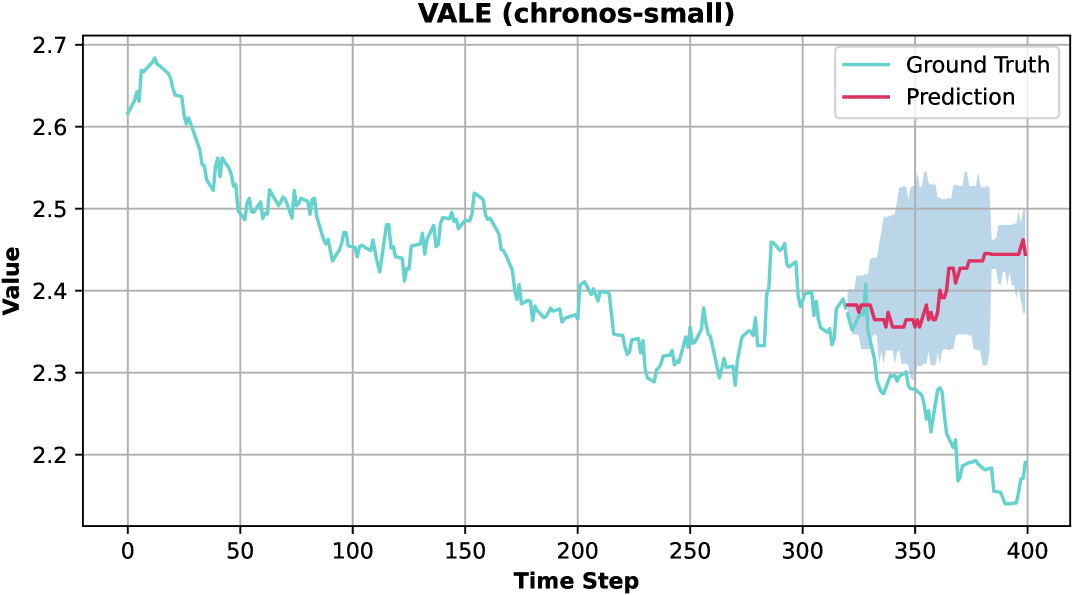

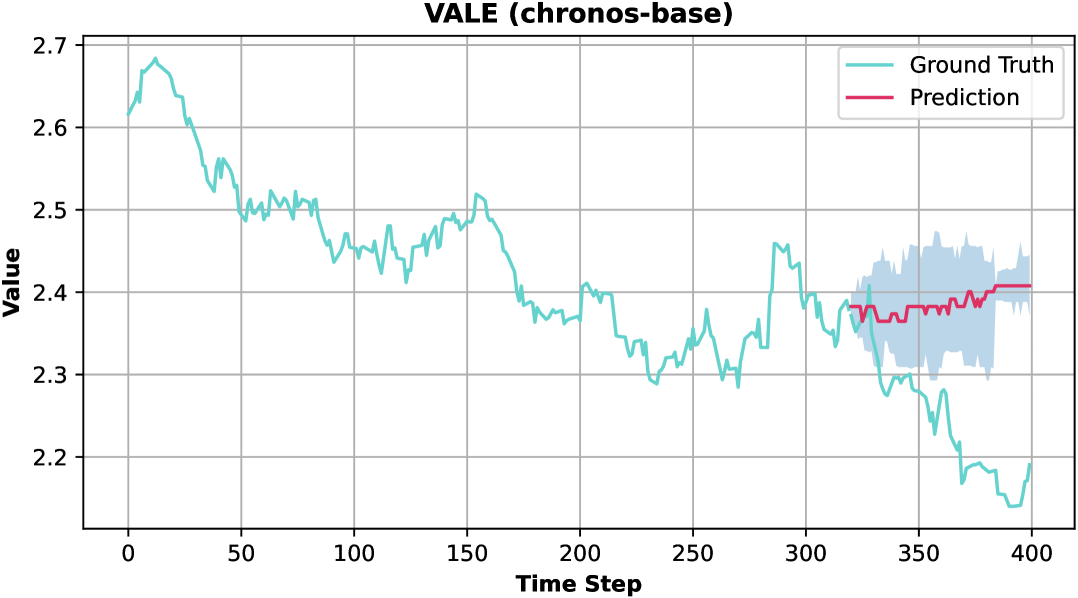

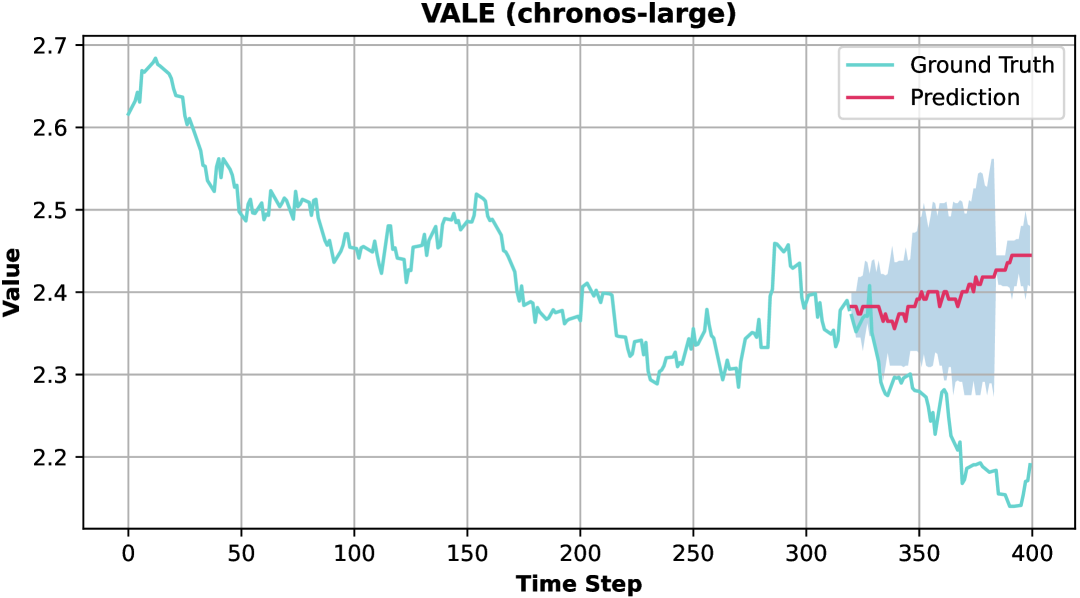

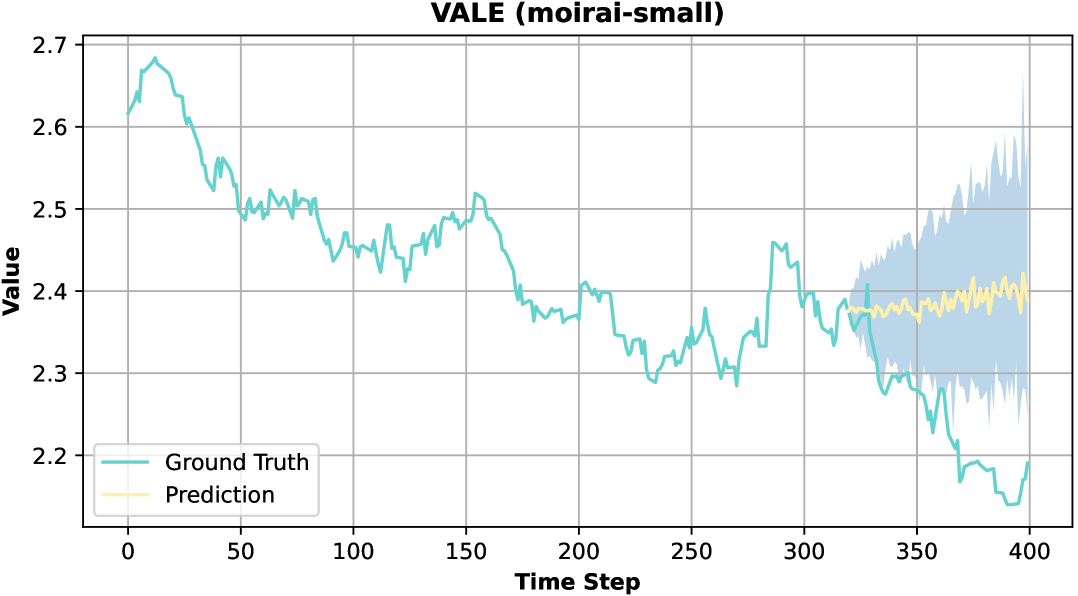

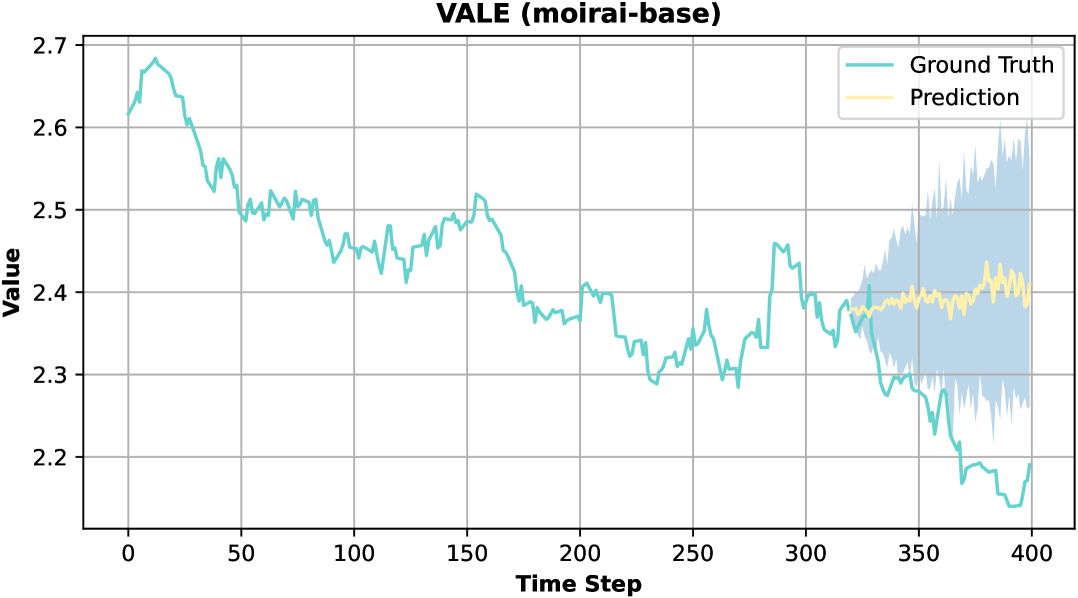

When compared to the baseline models, Chronos and Moirai, FTS-Text-MoE shows improved performance with the addition of text inputs (such as news and tweets), but still falls short of surpassing Chronos and Moirai in some industries and scenarios (Table 1). Chronos and Moirai models exhibit a more conservative prediction approach, especially under high uncertainty and market volatility, smoothing the curve to reduce errors and maintain lower MSE and MAE. In contrast, FTS-Text-MoE adopts a more proactive strategy, capturing short-term volatility, which benefits quick market shifts but increases prediction errors during periods of significant fluctuations3.

| Approach | Overall () | Std. Dev. () | Sharpe () |

|---|---|---|---|

| 1/N | 0.0570 | 5.132e-3 | 0.1725 |

| S&P500 Index | -0.0082 | 5.459e-3 | -0.3002 |

| Moirai | 0.0079 | 1.741e-3 | 0.3320 |

| Chronos | -0.0077 | 1.288e-3 | 0.1223 |

| Our | 0.1347 | 5.290e-3 | 1.0818 |

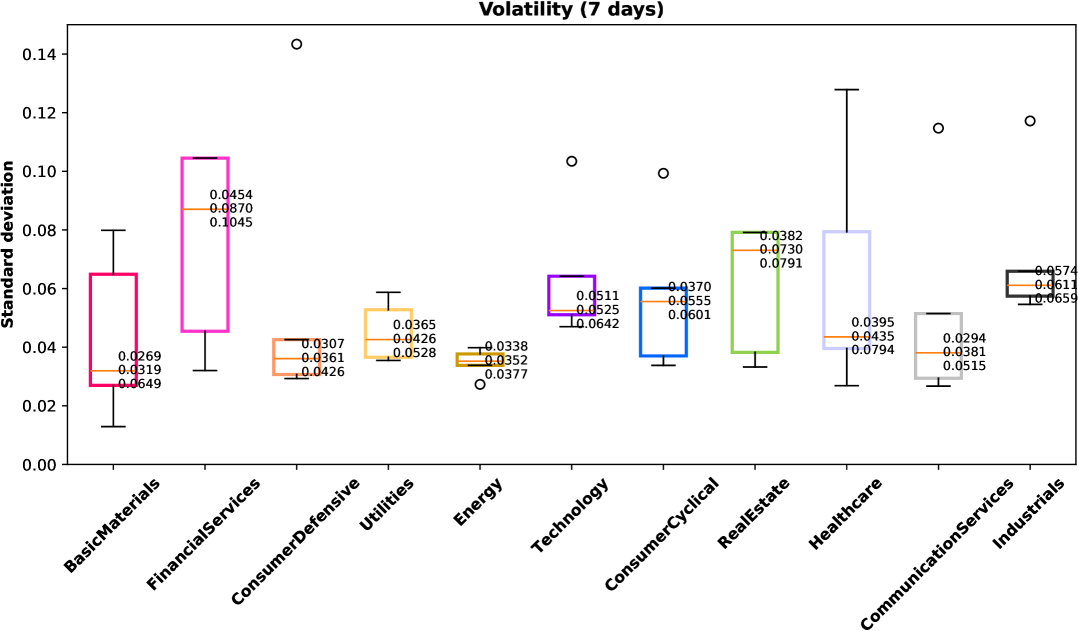

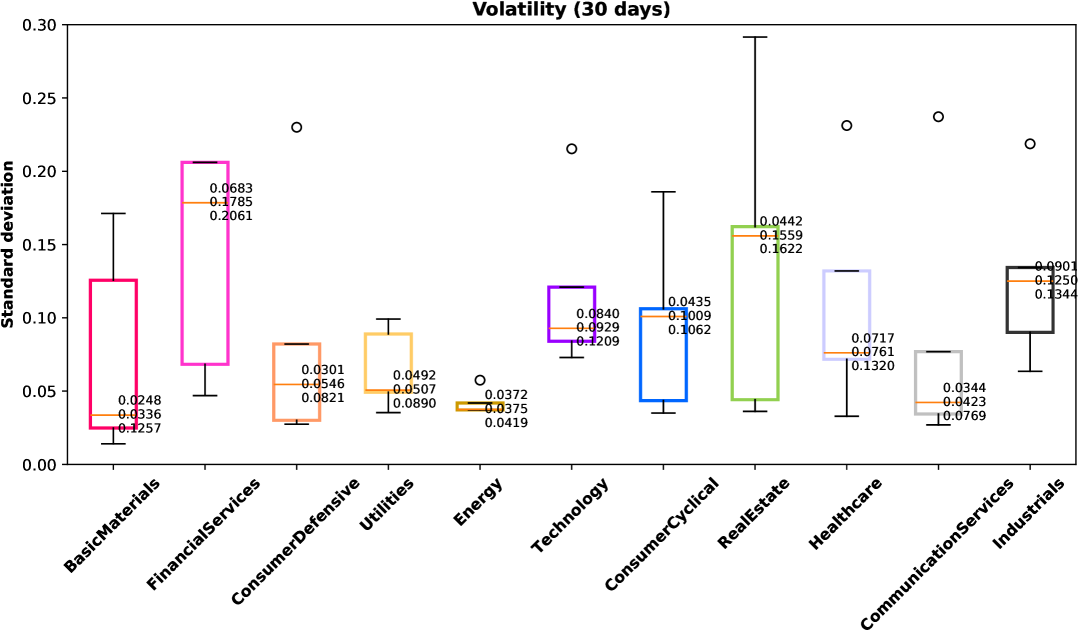

4.3 Robustness Analysis of FTS-Text-MoE

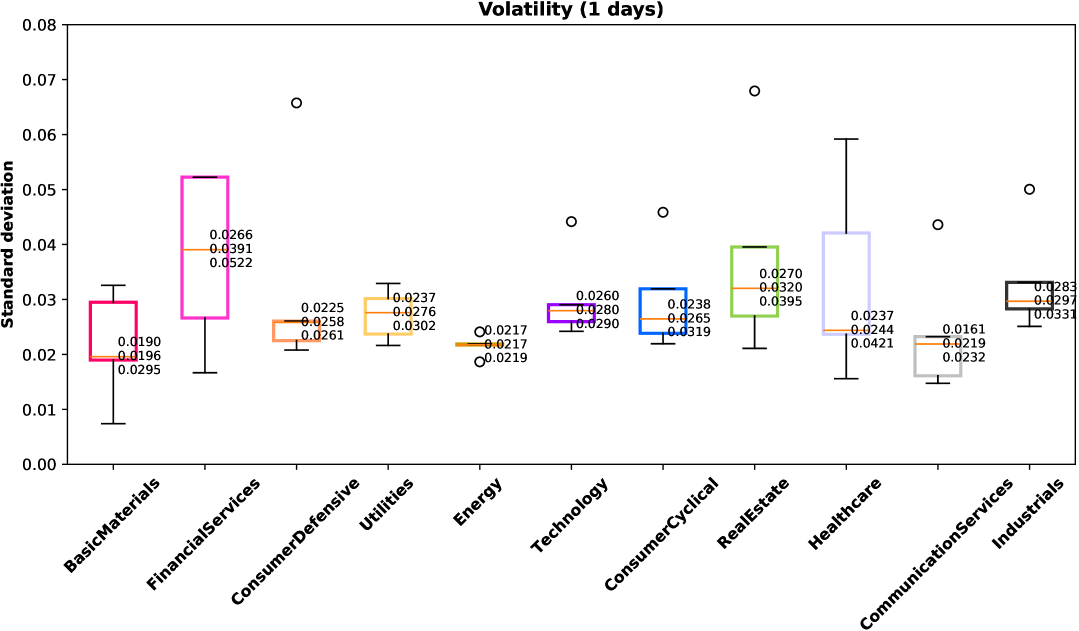

We analyzed stock price volatility across sectors (see Figure 5), measuring it as the standard deviation of changes over a given sampling period (): Higher volatility indicates greater risk, which generally increases with a longer sampling period .

| (8) |

where and are the first and last days, represents the value change over , and is the average change:

| (9) |

4.4 Comparison of Return and Loss Distributions

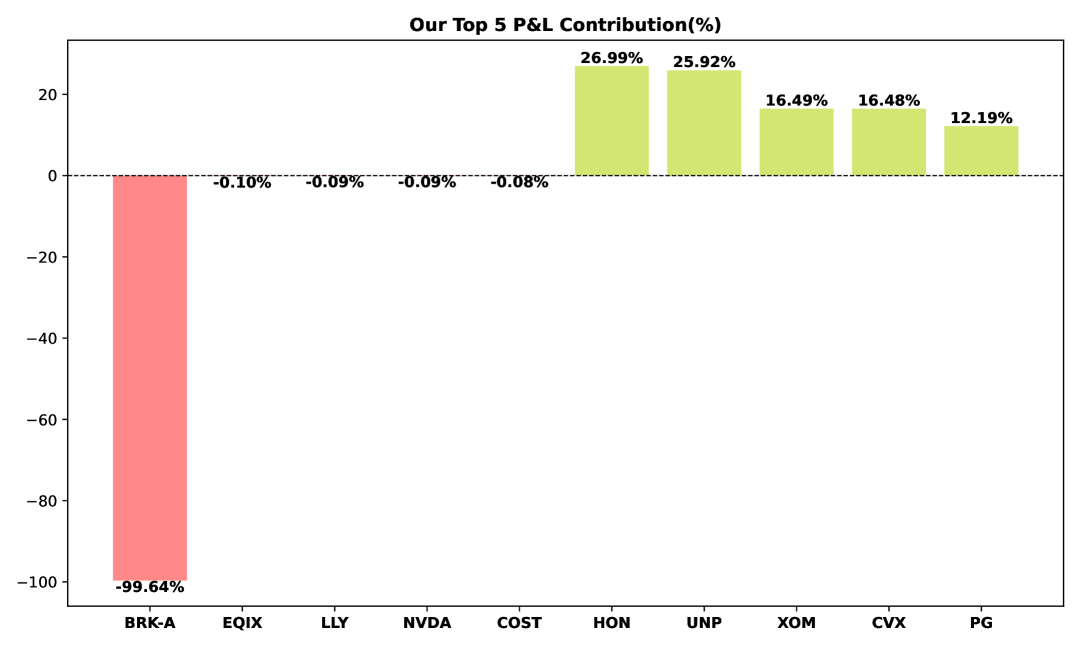

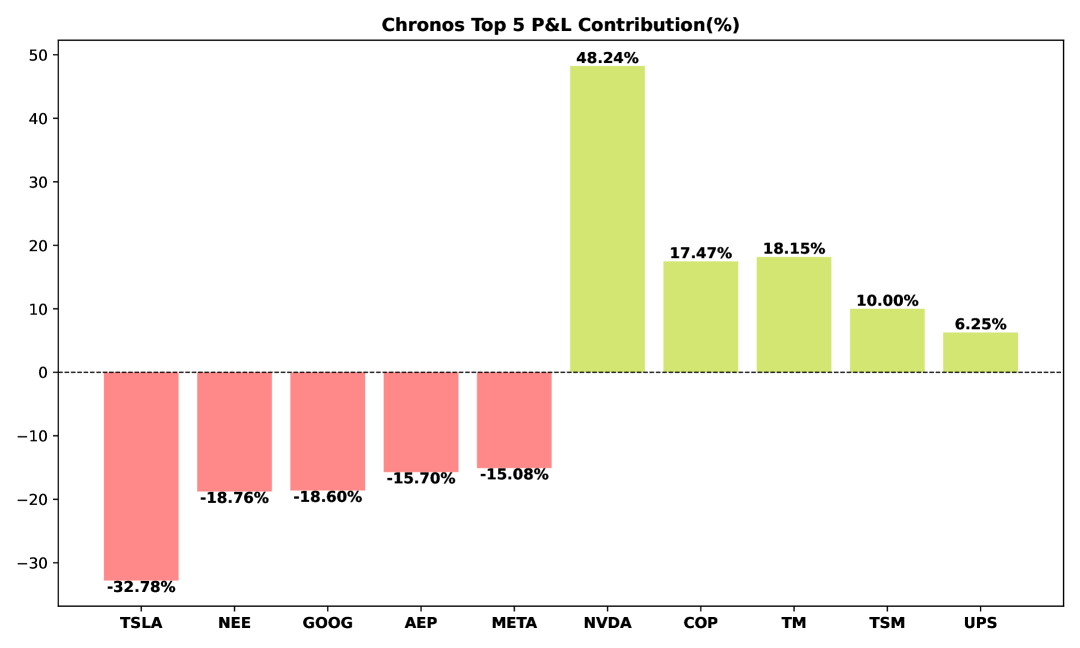

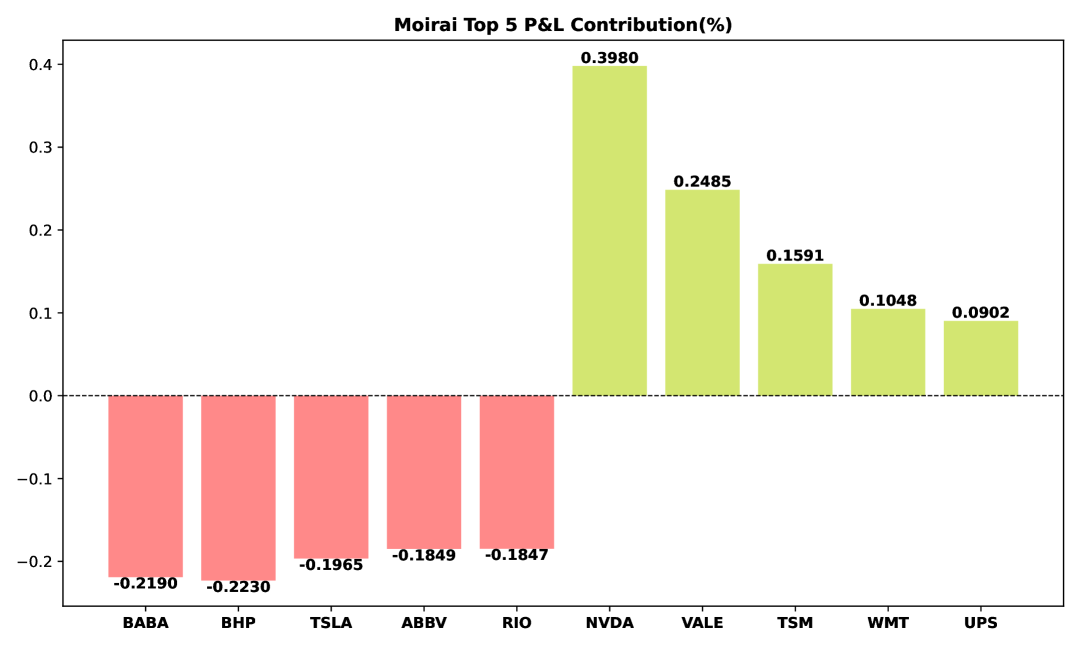

Compared to FTS-Text-MoE, Chronos and Moirai, which rely solely on historical time-series data, adopt a more passive prediction strategy. In contrast, FTS-Text-MoE integrates real-world textual information, resulting in a more aggressive forecasting approach. Figure 4 shows the top five gainers and losers for FTS-Text-MoE and the baseline models. The return distribution for FTS-Text-MoE is noticeably more uneven, indicating a more aggressive and concentrated investment strategy.

4.5 Portfolio Optimization

We evaluate portfolio performance using three key metrics across four baselines:

-

•

1/N Portfolio: Equally weighted across 11 stocks.

-

•

S&P 500 Index: Market benchmark.

-

•

Moirai/Chronos Positive Prediction Portfolios: Invests only in positively predicted stocks, equally weighted.

As shown in Table 2, FTS-Text-MoE, following the same investment approach, outperforms Moirai/Chronos, particularly in terms of overall returns and Sharpe ratio. With an Overall return of 0.1347, it demonstrates superior cumulative returns, while its Sharpe ratio of 1.0818 indicates better risk-adjusted performance. However, its higher standard deviation (Std. Dev. = 5.290e-3) suggests increased return volatility, likely due to the model’s responsiveness to time series fluctuations, making it more sensitive to short-term market dynamics.

5 Conclusion

This study proposes FTS-Text-MoE, which effectively integrates time series and textual data to overcome the input-output length limitations faced by existing large-scale financial forecasting models when processing multi-source data and performing long-sequence predictions. The proposed model employs a sparse Transformer decoder combined with an MoE mechanism, significantly enhancing computational efficiency, and utilizes multi-resolution prediction heads to enable flexible forecasting across different temporal scales. Experimental results demonstrate that FTS-Text-MoE achieves superior performance in financial time series prediction tasks, effectively integrating quantitative and sentiment data for a more comprehensive market analysis.

6 Limitations

The proposed FTS-Text-MoE integrates financial numerical data with textual information and reduces computational complexity using a sparse Transformer decoder, but it has limitations. Firstly, the model aligns textual and time-series data at the same time step, yet news and tweets often have a delayed impact on stock prices. This lag, where market information takes time to propagate, may affect prediction accuracy. Secondly, news and social media may contain false or misleading information, negatively influencing forecasts. Future research will focus on handling lag and improving text authenticity verification to enhance model robustness and accuracy.

References

- (1) Abdul Fatir Ansari, Lorenzo Stella, Ali Caner Turkmen, Xiyuan Zhang, Pedro Mercado, Huibin Shen, Oleksandr Shchur, Syama Sundar Rangapuram, Sebastian Pineda Arango, Shubham Kapoor, and 1 others. Chronos: Learning the language of time series. Transactions on Machine Learning Research.

- Ariyo et al. (2014) Adebiyi A Ariyo, Adewumi O Adewumi, and Charles K Ayo. 2014. Stock price prediction using the arima model. In 2014 UKSim-AMSS 16th international conference on computer modelling and simulation, pages 106–112. IEEE.

- Chen et al. (2024) Jiayu Chen, Bhargav Ganguly, Yang Xu, Yongsheng Mei, Tian Lan, and Vaneet Aggarwal. 2024. Deep generative models for offline policy learning: Tutorial, survey, and perspectives on future directions. Transactions on Machine Learning Research.

- (4) Junyan Cheng and Peter Chin. Sociodojo: Building lifelong analytical agents with real-world text and time series. In The Twelfth International Conference on Learning Representations.

- Chowdhery et al. (2023) Aakanksha Chowdhery, Sharan Narang, Jacob Devlin, Maarten Bosma, Gaurav Mishra, Adam Roberts, Paul Barham, Hyung Won Chung, Charles Sutton, Sebastian Gehrmann, and 1 others. 2023. Palm: Scaling language modeling with pathways. Journal of Machine Learning Research, 24(240):1–113.

- Dai et al. (2024) Damai Dai, Chengqi Deng, Chenggang Zhao, RX Xu, Huazuo Gao, Deli Chen, Jiashi Li, Wangding Zeng, Xingkai Yu, and 1 others. 2024. Deepseekmoe: Towards ultimate expert specialization in mixture-of-experts language models. arXiv preprint arXiv:2401.06066.

- Deng et al. (2019) Shumin Deng, Ningyu Zhang, Wen Zhang, Jiaoyan Chen, Jeff Z Pan, and Huajun Chen. 2019. Knowledge-driven stock trend prediction and explanation via temporal convolutional network. In Companion proceedings of the 2019 world wide web conference, pages 678–685.

- Ding et al. (2015) Xiao Ding, Yue Zhang, Ting Liu, and Junwen Duan. 2015. Deep learning for event-driven stock prediction. In Proceedings of the 24th International Conference on Artificial Intelligence, pages 2327–2333.

- Fedus et al. (2022) William Fedus, Barret Zoph, and Noam Shazeer. 2022. Switch transformers: Scaling to trillion parameter models with simple and efficient sparsity. Journal of Machine Learning Research, 23(120):1–39.

- Francq and Zakoian (2019) Christian Francq and Jean-Michel Zakoian. 2019. GARCH models: structure, statistical inference and financial applications. John Wiley & Sons.

- Hoefler et al. (2021) Torsten Hoefler, Dan Alistarh, Tal Ben-Nun, Nikoli Dryden, and Alexandra Peste. 2021. Sparsity in deep learning: Pruning and growth for efficient inference and training in neural networks. Journal of Machine Learning Research, 22(241):1–124.

- Hsu et al. (2021) Yen-Ju Hsu, Yang-Cheng Lu, and J Jimmy Yang. 2021. News sentiment and stock market volatility. Review of Quantitative Finance and Accounting, 57(3):1093–1122.

- (13) Aya Abdelsalam Ismail, Sercan O Arik, Jinsung Yoon, Ankur Taly, Soheil Feizi, and Tomas Pfister. Interpretable mixture of experts. Transactions on Machine Learning Research.

- Jacobs et al. (1991) Robert A Jacobs, Michael I Jordan, Steven J Nowlan, and Geoffrey E Hinton. 1991. Adaptive mixtures of local experts. Neural computation, 3(1):79–87.

- Koa et al. (2023) Kelvin JL Koa, Yunshan Ma, Ritchie Ng, and Tat-Seng Chua. 2023. Diffusion variational autoencoder for tackling stochasticity in multi-step regression stock price prediction. In Proceedings of the 32nd ACM International Conference on Information and Knowledge Management, pages 1087–1096.

- Koa et al. (2024) Kelvin JL Koa, Yunshan Ma, Ritchie Ng, and Tat-Seng Chua. 2024. Learning to generate explainable stock predictions using self-reflective large language models. In Proceedings of the ACM Web Conference 2024, pages 4304–4315.

- Konstantinov et al. (2020) Gueorgui Konstantinov, Andreas Chorus, and Jonas Rebmann. 2020. A network and machine learning approach to factor, asset, and blended allocation. Journal of Portfolio Management, 46(6):54–71.

- Kumar et al. (2024) Pulikandala Nithish Kumar, Nneka Umeorah, and Alex Alochukwu. 2024. Dynamic graph neural networks for enhanced volatility prediction in financial markets. arXiv preprint arXiv:2410.16858.

- (19) Dmitry Lepikhin, HyoukJoong Lee, Yuanzhong Xu, Dehao Chen, Orhan Firat, Yanping Huang, Maxim Krikun, Noam Shazeer, and Zhifeng Chen. Gshard: Scaling giant models with conditional computation and automatic sharding. In International Conference on Learning Representations.

- Lin et al. (2024) Shengsheng Lin, Weiwei Lin, Wentai Wu, Haojun Chen, and Junjie Yang. 2024. Sparsetsf: Modeling long-term time series forecasting with* 1k* parameters. In International Conference on Machine Learning, pages 30211–30226. PMLR.

- Liu et al. (2025) Chenxi Liu, Qianxiong Xu, Hao Miao, Sun Yang, Lingzheng Zhang, Cheng Long, Ziyue Li, and Rui Zhao. 2025. Timecma: Towards llm-empowered multivariate time series forecasting via cross-modality alignment. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 39, pages 18780–18788.

- Lo (2002) Andrew W Lo. 2002. The statistics of sharpe ratios. Financial analysts journal, 58(4):36–52.

- Montgomery et al. (2021) Douglas C Montgomery, Elizabeth A Peck, and G Geoffrey Vining. 2021. Introduction to linear regression analysis. John Wiley & Sons.

- Ni et al. (2024) Ronghao Ni, Zinan Lin, Shuaiqi Wang, and Giulia Fanti. 2024. Mixture-of-linear-experts for long-term time series forecasting. In International Conference on Artificial Intelligence and Statistics, pages 4672–4680. PMLR.

- (25) Yuqi Nie, Nam H Nguyen, Phanwadee Sinthong, and Jayant Kalagnanam. A time series is worth 64 words: Long-term forecasting with transformers. In The Eleventh International Conference on Learning Representations.

- Schumaker and Chen (2009) Robert P Schumaker and Hsinchun Chen. 2009. Textual analysis of stock market prediction using breaking financial news: The azfin text system. ACM Transactions on Information Systems (TOIS), 27(2):1–19.

- Shazeer (2020) Noam Shazeer. 2020. Glu variants improve transformer. arXiv e-prints, pages arXiv–2002.

- Shi et al. (2024) Xiaoming Shi, Shiyu Wang, Yuqi Nie, Dianqi Li, Zhou Ye, Qingsong Wen, and Ming Jin. 2024. Time-moe: Billion-scale time series foundation models with mixture of experts. arXiv preprint arXiv:2409.16040.

- Su et al. (2024) Jianlin Su, Murtadha Ahmed, Yu Lu, Shengfeng Pan, Wen Bo, and Yunfeng Liu. 2024. Roformer: Enhanced transformer with rotary position embedding. Neurocomputing, 568:127063.

- Touvron et al. (2023) Hugo Touvron, Thibaut Lavril, Gautier Izacard, Xavier Martinet, Marie-Anne Lachaux, Timothée Lacroix, Baptiste Rozière, Naman Goyal, Eric Hambro, Faisal Azhar, and 1 others. 2023. Llama: Open and efficient foundation language models. arXiv preprint arXiv:2302.13971.

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Łukasz Kaiser, and Illia Polosukhin. 2017. Attention is all you need. Advances in neural information processing systems, 30.

- Wang et al. (2025) Chengsen Wang, Qi Qi, Jingyu Wang, Haifeng Sun, Zirui Zhuang, Jinming Wu, Lei Zhang, and Jianxin Liao. 2025. Chattime: A unified multimodal time series foundation model bridging numerical and textual data. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 39, pages 12694–12702.

- Woo et al. (2024) Gerald Woo, Chenghao Liu, Akshat Kumar, Caiming Xiong, Silvio Savarese, and Doyen Sahoo. 2024. Unified training of universal time series forecasting transformers. In Proceedings of the 41st International Conference on Machine Learning, pages 53140–53164.

- Xu and Cohen (2018) Yumo Xu and Shay B Cohen. 2018. Stock movement prediction from tweets and historical prices. In Proceedings of the 56th Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers), pages 1970–1979.

- Yang et al. (2020) Linyi Yang, Tin Lok James Ng, Barry Smyth, and Riuhai Dong. 2020. Html: Hierarchical transformer-based multi-task learning for volatility prediction. In Proceedings of The Web Conference 2020, pages 441–451.

- Zeng et al. (2023) Ailing Zeng, Muxi Chen, Lei Zhang, and Qiang Xu. 2023. Are transformers effective for time series forecasting? In Proceedings of the AAAI conference on artificial intelligence, volume 37, pages 11121–11128.

- Zhang and Sennrich (2019) Biao Zhang and Rico Sennrich. 2019. Root mean square layer normalization. Advances in Neural Information Processing Systems, 32.

Appendix A Implementation Details

A.1 Loss Function

Integrating extensive textual information into financial time series data poses a challenge for training stability in FTS-Text-MoE. To enhance robustness against outliers and improve stability, we employ the Huber loss. The autoregressive loss, projected from a single-layer FFN, is defined as follows:

|

|

(10) |

where is a hyperparameter that balances the L1 and L2 loss components.

In MoE architectures, optimizing purely for accuracy often leads to uneven expert utilization, with the model favoring a small subset of experts, limiting broader training. To address this, inspired by Dai et al. (2024) and Fedus et al. (2022), we introduce an auxiliary loss for expert load balancing. This loss aligns the proportion of tokens assigned to each expert () with its routing probability (), ensuring a more balanced distribution.

| (11) | |||

where is an indicator function.

The multi-resolution forecasting heads utilize multiple output projections from a single-layer FFN, each corresponding to a different forecasting horizon. During training, errors across scales are aggregated into a composite loss. The final loss function combines the multi-resolution autoregressive loss and the auxiliary balancing loss:

| (12) |

where is the number of multi-resolution projections, and denotes the horizon of the -th projection.

A.2 Model Details

FTS-Text-MoE employs a 12-layer architecture with 12 attention heads per layer and integrates an MoE module with 8 experts per layer. For each token, the top-2 experts () are selected. The model features a hidden dimension () of 384, a feed-forward network dimension () of 1536, and each expert has a dimension of 192 (). This design results in 50M active parameters during inference, with a total parameter count of 113M.

A.3 Training Configuration

Each model is trained for 10,000 steps with a batch size of 64 and a maximum sequence length of 1,024. Each iteration processes 64 time steps. The output projection employs prediction horizons of {1, 8, 32, 64}, and the auxiliary loss coefficient is set to 0.02. Optimization is performed using the AdamW optimizer with hyperparameters: learning rate , weight decay , , and . The learning rate follows a schedule with a linear warm-up for the first 10,000 steps, after which cosine annealing is applied. Training is conducted on two NVIDIA A6000-48G GPUs with FP16 precision. To improve batch efficiency and handle variable-length sequences, we employ sequence packing to minimize padding overhead.

Appendix B Data Sources and Metrics

B.1 Time Series Data

Stock price data from Yahoo Finance includes 55 stocks across 11 industries with daily open, high, low, close prices, and trading volume. The adjusted closing price is used as the primary measure of stock value over 20 years, yielding 191,512 sample points. See Table 3 for details.

| Sector | Stock Symbol | Total Days | First Date | Last Date |

| Basic Materials | BHP | 5568 | 2009/10/21 | 2025/1/17 |

| RIO | 4461 | 2012/10/31 | 2025/1/16 | |

| SHW | 3390 | 2015/10/6 | 2025/1/15 | |

| VALE | 5465 | 2010/2/1 | 2025/1/17 | |

| APD | 4796 | 2011/12/2 | 2025/1/17 | |

| Financial Services | BRK-A | 5570 | 2009/10/19 | 2025/1/18 |

| V | 5392 | 2010/4/15 | 2025/1/19 | |

| JPM | 1840 | 2020/1/5 | 2025/1/17 | |

| MA | 1840 | 2020/1/5 | 2025/1/17 | |

| BAC | 1840 | 2020/1/5 | 2025/1/18 | |

| Consumer Defensive | WMT | 2240 | 2018/12/1 | 2025/1/19 |

| PG | 1840 | 2020/1/5 | 2025/1/18 | |

| KO | 5575 | 2009/10/14 | 2025/1/18 | |

| PEP | 5548 | 2009/11/10 | 2025/1/19 | |

| COST | 5449 | 2010/2/17 | 2025/1/18 | |

| Utilities | NEE | 1639 | 2020/7/24 | 2025/1/17 |

| DUK | 5381 | 2010/4/26 | 2025/1/17 | |

| D | 5387 | 2010/4/20 | 2025/1/18 | |

| SO | 5324 | 2010/6/22 | 2025/1/18 | |

| AEP | 5579 | 2009/10/9 | 2025/1/16 | |

| Energy | XOM | 1973 | 2019/8/25 | 2025/1/18 |

| CVX | 3090 | 2016/8/3 | 2025/1/18 | |

| SHEL | 1840 | 2020/1/5 | 2025/1/17 | |

| TTE | 1839 | 2020/1/5 | 2025/1/16 | |

| COP | 5541 | 2009/11/17 | 2025/1/17 | |

| Technology | AAPL | 1844 | 2020/1/1 | 2025/1/18 |

| MSFT | 1840 | 2020/1/5 | 2025/1/18 | |

| TSM | 5392 | 2010/4/15 | 2025/1/19 | |

| NVDA | 1615 | 2020/8/17 | 2025/1/20 | |

| AVGO | 1839 | 2020/1/6 | 2025/1/19 | |

| Consumer Cyclical | AMZN | 1844 | 2020/1/1 | 2025/1/19 |

| TSLA | 1841 | 2020/1/4 | 2025/1/19 | |

| HD | 1841 | 2020/1/4 | 2025/1/17 | |

| BABA | 3725 | 2014/11/7 | 2025/1/17 | |

| TM | 5465 | 2010/2/1 | 2025/1/18 | |

| Real Estate | AMT | 5526 | 2009/12/2 | 2025/1/17 |

| PLD | 5322 | 2010/6/24 | 2025/1/18 | |

| CCI | 5442 | 2010/2/23 | 2025/1/16 | |

| EQIX | 3469 | 2015/7/21 | 2025/1/17 | |

| PSA | 3286 | 2016/1/20 | 2025/1/17 | |

| Healthcare | UNH | 1839 | 2020/1/6 | 2025/1/20 |

| JNJ | 1836 | 2020/1/9 | 2025/1/18 | |

| LLY | 1840 | 2020/1/5 | 2025/1/18 | |

| PFE | 1839 | 2020/1/6 | 2025/1/18 | |

| ABBV | 4398 | 2013/1/3 | 2025/1/17 | |

| Communication Services | GOOG | 2173 | 2019/2/6 | 2025/1/19 |

| META | 1841 | 2020/1/4 | 2025/1/19 | |

| VZ | 1833 | 2020/1/12 | 2025/1/19 | |

| CMCSA | 2844 | 2017/4/6 | 2025/1/17 | |

| DIS | 2046 | 2019/6/13 | 2025/1/18 | |

| Industrials | UPS | 5538 | 2009/11/20 | 2025/1/18 |

| UNP | 5555 | 2009/11/3 | 2025/1/18 | |

| HON | 1837 | 2020/1/8 | 2025/1/18 | |

| LMT | 1841 | 2020/1/4 | 2025/1/18 | |

| CAT | 5554 | 2009/11/4 | 2025/1/17 |

B.2 Tweet Data

Given the vast number of daily tweets, we use a dataset clustered via the BERTopic pipeline. It includes tweets about the top 5 stocks in 11 sectors from 2020 to 2022, collected via the Twitter API. The dataset comprises 637,395 tweets. See Table 4 for details.

| Company | Total Days | Daily Tweet Count | First Date | Last Date |

| AAPL | 1090 | 83964 | 2020/1/1 | 2022/12/31 |

| ABBV | 914 | 3200 | 2020/1/4 | 2022/12/21 |

| AEP | 416 | 2156 | 2020/1/12 | 2022/12/28 |

| AMT | 546 | 2536 | 2020/1/10 | 2022/12/24 |

| AMZN | 1090 | 58193 | 2020/1/1 | 2022/12/31 |

| APD | 444 | 2283 | 2020/1/4 | 2022/12/16 |

| AVGO | 776 | 2466 | 2020/1/6 | 2022/12/24 |

| BABA | 978 | 18761 | 2020/1/4 | 2022/12/24 |

| BAC | 1046 | 7353 | 2020/1/5 | 2022/12/24 |

| BHP | 446 | 1433 | 2020/1/7 | 2022/12/23 |

| BRK-A | 414 | 1910 | 2020/1/4 | 2022/12/29 |

| CAT | 937 | 4823 | 2020/1/6 | 2022/12/24 |

| CCI | 339 | 1651 | 2020/1/5 | 2022/12/24 |

| CMCSA | 806 | 2412 | 2020/1/6 | 2022/12/24 |

| COP | 689 | 2027 | 2020/1/19 | 2022/12/24 |

| COST | 1003 | 4780 | 2020/1/7 | 2022/12/24 |

| CVX | 824 | 6907 | 2020/1/5 | 2022/12/24 |

| D | 462 | 1353 | 2020/1/12 | 2022/12/24 |

| DIS | 1064 | 14146 | 2020/1/8 | 2022/12/24 |

| DUK | 357 | 1688 | 2020/1/9 | 2022/12/24 |

| EQIX | 441 | 2505 | 2020/1/5 | 2022/12/28 |

| GOOG | 1085 | 12539 | 2020/1/4 | 2022/12/24 |

| HD | 923 | 4837 | 2020/1/4 | 2022/12/24 |

| HON | 464 | 1436 | 2020/1/8 | 2022/12/24 |

| JNJ | 884 | 6104 | 2020/1/9 | 2022/12/20 |

| JPM | 950 | 7783 | 2020/1/5 | 2022/12/24 |

| KO | 828 | 3915 | 2020/1/7 | 2022/12/24 |

| LLY | 745 | 2781 | 2020/1/5 | 2022/12/24 |

| LMT | 733 | 2620 | 2020/1/4 | 2022/10/17 |

| MA | 913 | 3408 | 2020/1/5 | 2022/12/24 |

| META | 965 | 44182 | 2020/1/4 | 2022/12/24 |

| MSFT | 963 | 31153 | 2020/1/4 | 2022/12/24 |

| NEE | 559 | 1637 | 2020/1/4 | 2022/12/24 |

| PEP | 669 | 2196 | 2020/1/15 | 2022/12/24 |

| PFE | 1031 | 12021 | 2020/1/6 | 2022/12/24 |

| PG | 727 | 2665 | 2020/1/5 | 2022/12/24 |

| PLD | 505 | 2362 | 2020/1/9 | 2022/12/24 |

| PSA | 499 | 2482 | 2020/1/11 | 2022/12/27 |

| RIO | 578 | 2005 | 2020/1/6 | 2022/12/24 |

| SHEL | 406 | 1688 | 2020/1/5 | 2022/12/23 |

| SHW | 398 | 1939 | 2020/1/4 | 2022/12/23 |

| SO | 365 | 1590 | 2020/1/4 | 2022/12/29 |

| TM | 560 | 2053 | 2020/1/5 | 2022/12/23 |

| TSLA | 973 | 181368 | 2020/1/4 | 2022/12/24 |

| TSM | 786 | 3850 | 2020/1/6 | 2022/12/24 |

| TTE | 404 | 1911 | 2020/1/5 | 2022/12/24 |

| UNH | 818 | 2550 | 2020/1/6 | 2022/12/24 |

| UNP | 398 | 1557 | 2020/1/4 | 2022/12/22 |

| UPS | 803 | 2805 | 2020/1/4 | 2022/12/23 |

| V | 936 | 5293 | 2020/1/4 | 2022/12/24 |

| VALE | 660 | 1937 | 2020/1/4 | 2022/12/24 |

| VZ | 745 | 3119 | 2020/1/12 | 2022/12/24 |

| WMT | 1076 | 11164 | 2020/1/4 | 2022/12/24 |

| XOM | 1060 | 7933 | 2020/1/5 | 2022/12/24 |

| NVDA | 1074 | 33965 | 2020/1/4 | 2022/12/24 |

B.3 News Data

We extract news data from the FNSPID dataset, focusing on articles related to 55 S&P 500 stocks listed on NASDAQ from 1999 to 2023. This dataset includes URLs, headlines, and full news texts.

To ensure up-to-date coverage, we addressed technical issues in the FNSPID project, like automating page navigation, filtering pop-ups, and recognizing new web elements. Using Selenium, we retrieved news headlines and full content from NASDAQ. This update extends coverage to January 19, 2025, compiling 216,308 high-quality news records. See Table 5 for details.

| Company | Total Days | Daily News Count | First Date | Last Date |

| AAPL | 595 | 9365 | 2022/6/3 | 2025/1/18 |

| ABBV | 2669 | 6198 | 2013/1/3 | 2025/1/17 |

| AEP | 1224 | 1945 | 2009/10/9 | 2025/1/16 |

| AMT | 2196 | 6532 | 2009/12/2 | 2025/1/17 |

| AMZN | 307 | 5282 | 2023/3/9 | 2025/1/19 |

| APD | 1410 | 2213 | 2011/12/2 | 2025/1/17 |

| AVGO | 61 | 507 | 2023/12/16 | 2025/1/19 |

| BABA | 2573 | 9262 | 2014/11/7 | 2025/1/17 |

| BHP | 2354 | 4810 | 2009/10/21 | 2025/1/17 |

| BRK | 2087 | 9288 | 2009/10/19 | 2025/1/18 |

| CAT | 2366 | 5685 | 2009/11/4 | 2025/1/17 |

| CCI | 1156 | 1676 | 2010/2/23 | 2025/1/16 |

| CMCSA | 1877 | 4762 | 2017/4/6 | 2025/1/17 |

| COP | 2702 | 5711 | 2009/11/17 | 2025/1/17 |

| COST | 2883 | 7281 | 2010/2/17 | 2025/1/18 |

| CVX | 2217 | 9188 | 2016/8/3 | 2025/1/18 |

| D | 1691 | 2936 | 2010/4/20 | 2025/1/18 |

| DIS | 1667 | 9211 | 2019/6/13 | 2025/1/18 |

| DUK | 1925 | 3202 | 2010/4/26 | 2025/1/17 |

| GOOG | 1742 | 9226 | 2019/2/6 | 2025/1/19 |

| KO | 3143 | 8140 | 2009/10/14 | 2025/1/18 |

| LLY | 87 | 507 | 2023/12/16 | 2025/1/18 |

| LMT | 131 | 507 | 2023/12/15 | 2025/1/18 |

| MSFT | 631 | 9237 | 2022/4/26 | 2025/1/18 |

| NEE | 2383 | 4993 | 2010/7/24 | 2025/1/17 |

| NVDA | 828 | 9216 | 2021/8/17 | 2025/1/20 |

| PEP | 2519 | 5462 | 2009/11/10 | 2025/1/19 |

| PLD | 1434 | 2152 | 2010/6/24 | 2025/1/18 |

| RIO | 238 | 436 | 2012/10/31 | 2025/1/16 |

| SHW | 798 | 1218 | 2015/10/6 | 2025/1/15 |

| SO | 1577 | 2534 | 2010/6/22 | 2025/1/18 |

| TM | 2420 | 4083 | 2010/2/1 | 2025/1/18 |

| TSLA | 626 | 9212 | 2022/5/2 | 2025/1/19 |

| TSM | 2079 | 4398 | 2010/4/15 | 2025/1/19 |

| UNP | 1821 | 3084 | 2009/11/3 | 2025/1/18 |

| UPS | 2177 | 4217 | 2009/11/20 | 2025/1/18 |

| V | 2949 | 7445 | 2010/4/15 | 2025/1/19 |

| VALE | 1431 | 2015 | 2010/2/1 | 2025/1/17 |

| WMT | 1753 | 9154 | 2018/12/1 | 2025/1/19 |

| XOM | 1440 | 7253 | 2019/8/25 | 2025/1/18 |

| BAC | 96 | 500 | 2024/10/9 | 2025/1/18 |

| EQIX | 188 | 324 | 2015/7/21 | 2025/1/17 |

| HD | 146 | 500 | 2024/8/19 | 2025/1/17 |

| HON | 188 | 500 | 2024/5/14 | 2025/1/18 |

| JNJ | 127 | 500 | 2024/8/30 | 2025/1/18 |

| JPM | 89 | 500 | 2024/10/15 | 2025/1/17 |

| MA | 152 | 500 | 2024/8/1 | 2025/1/17 |

| META | 45 | 500 | 2024/12/6 | 2025/1/19 |

| PFE | 57 | 500 | 2024/10/18 | 2025/1/18 |

| PG | 182 | 500 | 2024/6/25 | 2025/1/18 |

| PSA | 146 | 241 | 2016/1/20 | 2025/1/17 |

| SHEL | 230 | 482 | 2024/2/1 | 2025/1/17 |

| TTE | 143 | 218 | 2024/2/13 | 2025/1/16 |

| UNH | 120 | 500 | 2024/9/5 | 2025/1/20 |

| VZ | 139 | 500 | 2024/8/21 | 2025/1/19 |

B.4 Multimodal Data Alignment

To enhance stock prediction accuracy, we align time-stamped tweets, news articles, and stock prices as multimodal inputs. Integrating textual and numerical data improves predictive performance. For a comparison of daily tweet and news volumes, see Figure 2.

B.5 Text-Cleaning Pipeline

Earlier sections detailed dataset attributes, including sampling frequency, time series count, and total observations. Here, we provide the text-cleaning pipeline, which ranks raw text and extracts summaries (see Algorithms 1 and 2) before converting them into embeddings (see Algorithm 3). Tweets, being short, are not summarized.

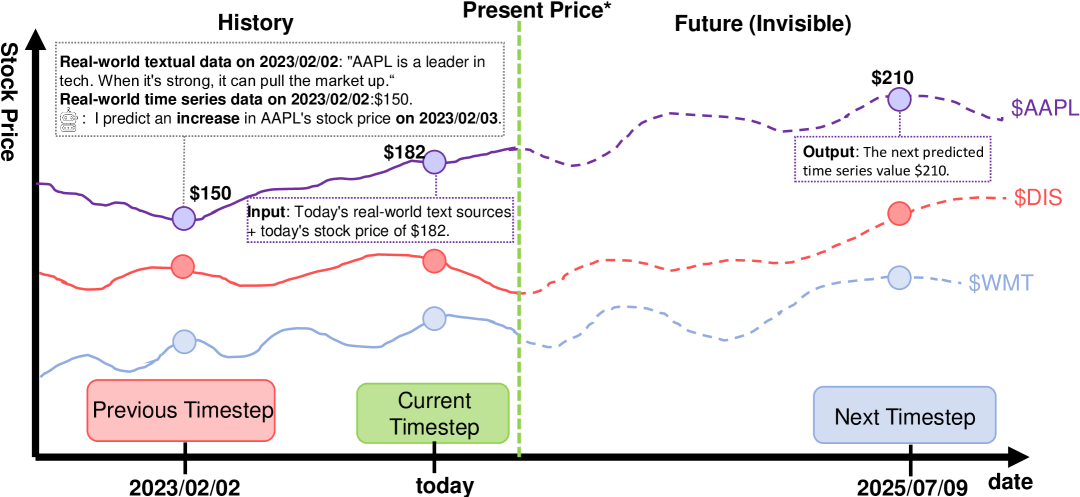

B.6 Input-Output Flow in FTS-Text-MoE for Time Series Forecasting

Figure 6 illustrates the input and output structure in time series forecasting using FTS-Text-MoE.

B.7 Evaluation Metrics

Error Metrics (Negative).

Model performance is evaluated using mean square error (MSE) and mean absolute error (MAE):

| MSE | ||||

| MAE | (13) |

where denote the ground truth and predicted values at time step .

Overall (Positive).

Cumulative daily returns:

| (14) |

Std. Dev. (Negative).

Standard deviation of returns, indicating risk:

| (15) |

where the mean return is:

| (16) |

Sharpe Lo (2002) (Positive).

Risk-adjusted return:

| (17) |

where is the portfolio’s average return, the risk-free rate, the return standard deviation, and 252 the annualization factor.

These metrics provide a comprehensive evaluation of predictive accuracy and financial performance.

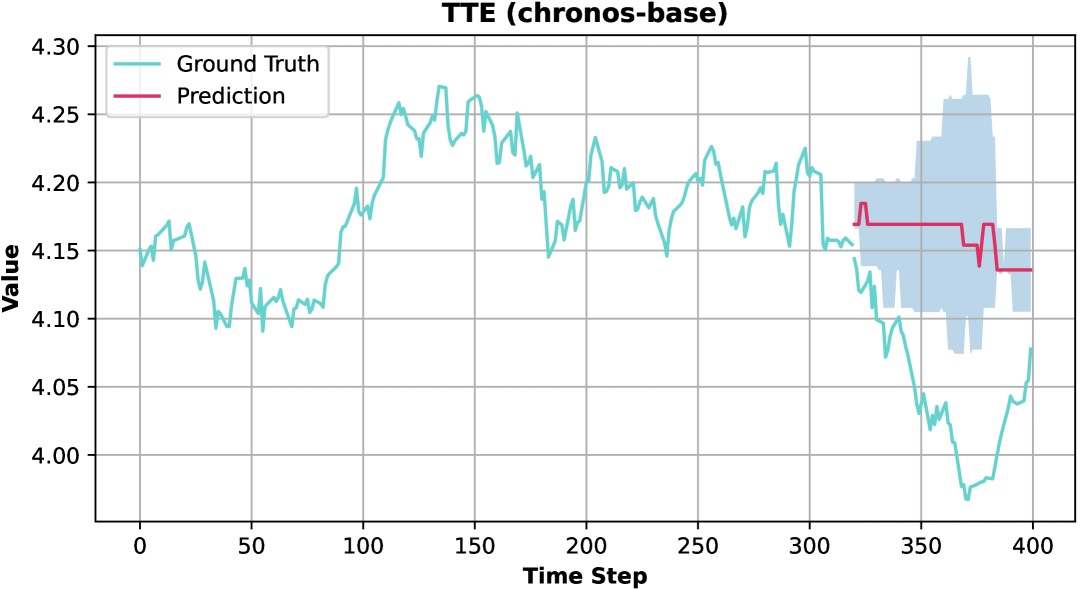

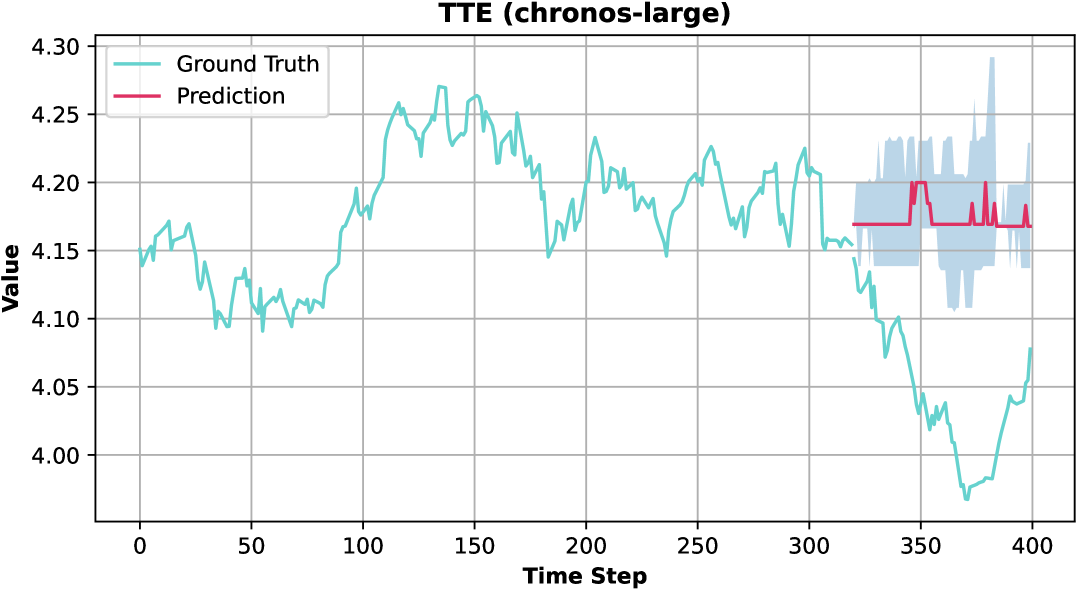

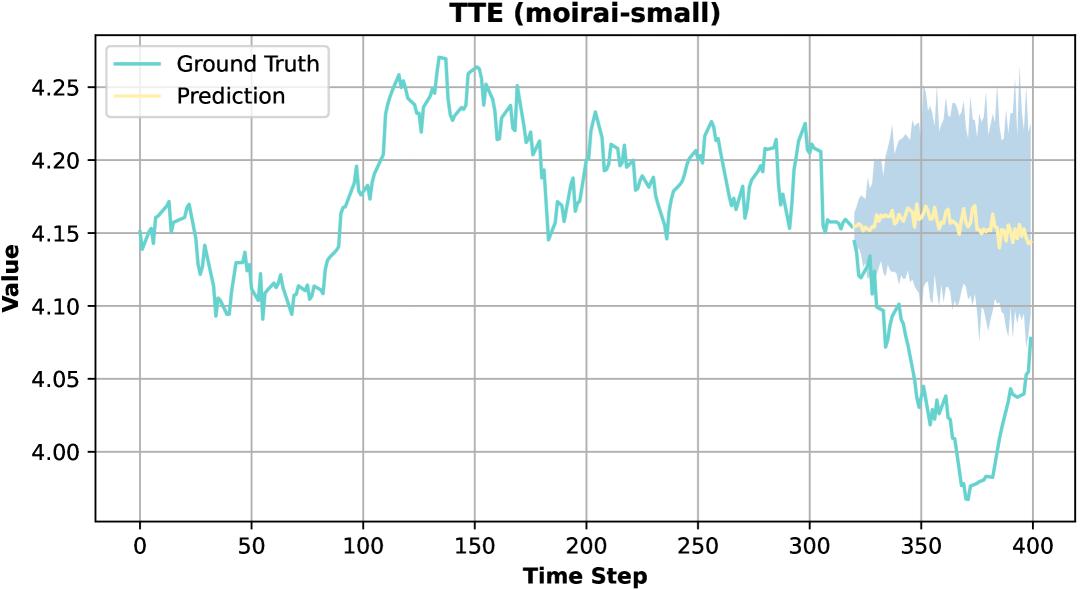

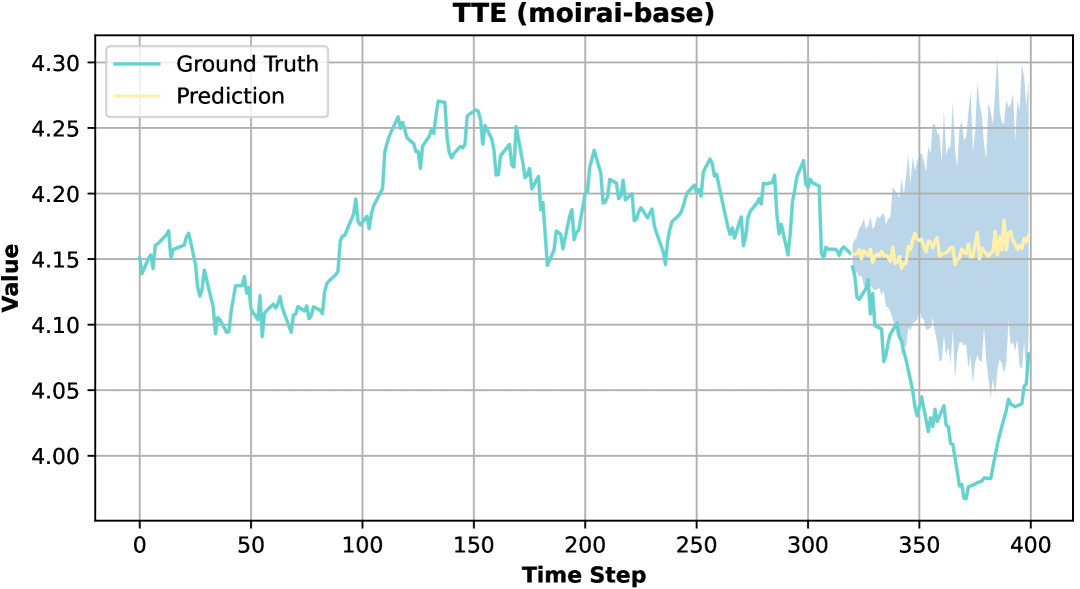

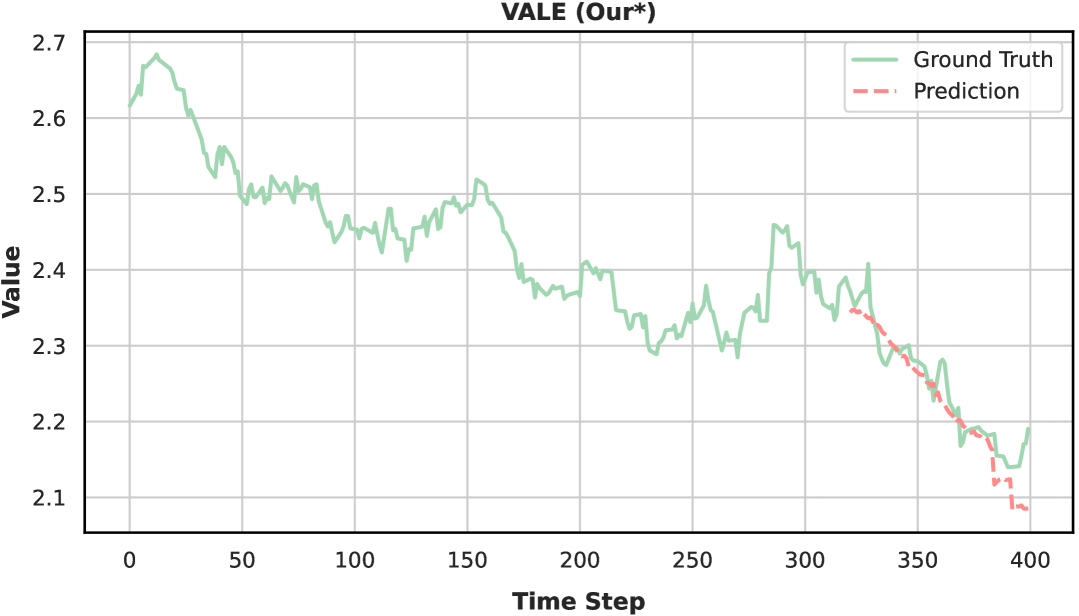

Appendix C Analysis of Financial Time-Series Results

As shown in Figure 7 (TTE stock time series data), Chronos and Moirai adopt a more conservative forecasting approach, with Moirai exhibiting the smoothest prediction curve. This suggests that Moirai prioritizes stability in high-uncertainty scenarios. In contrast, FTS-Text-MoE takes a more proactive approach, aiming to capture short-term fluctuations and better align with time series trends.