A Mean Field Game for Capacity Expansion Modeling

Abstract

This paper studies the optimal investment behavior of renewable electricity producers in a competitive market, where both prices and installation costs are influenced by aggregate industry activity. We model the resulting crowding effects using a mean field game framework, capturing the strategic interactions among a continuum of heterogeneous producers. The equilibrium dynamics are characterized via a coupled system of Hamilton–Jacobi–Bellman and Fokker–Planck equations, which describe the value function of a representative producer and the evolution of the distribution of installed capacities over time. We analyze both deterministic and stochastic versions of the model, providing analytical insights in tractable cases and developing numerical methods to approximate the general solution. Simulation results illustrate how aggregate investment responds to changing market conditions, cost structures, and exogenous productivity shocks.

Keywords. Mean field games, optimal control, renewable investments.

AMS 2020 subject classifications. 91A16; 49L12; 91B74.

1 Introduction

As nations accelerate their transition towards low-carbon economies, the expansion of renewable energy sources, particularly solar and wind, has become a critical priority. However, this shift also brings substantial new challenges for electricity systems. A striking illustration occurred in April 2025, when much of Spain and parts of Portugal experienced a massive power outage affecting millions of households (see, for instance Bajo-Buenestado (2025) [6]). Although investigations are ongoing at time of writing, the incident highlights how increasing reliance on weather-dependent generation can amplify vulnerabilities to unexpected disturbances. More broadly, the growing prevalence of negative electricity prices in countries with deep renewables penetration further exemplifies the economic and operational stresses induced by this transition.

These phenomena underline the urgent need for careful planning of capacity expansion, not only to meet decarbonization targets but also to ensure system resilience. A variety of complementary solutions have been explored, such as demand-side response programs, investments in grid-scale storage, reinforcement of transmission networks, and dynamic pricing mechanisms. Yet, long-term investment decisions by competing firms remain central to the evolution of electricity markets, shaping both the pace and the stability of renewables integration. Capacity expansion planning must therefore balance the twin goals of promoting rapid deployment and preserving economic and operational robustness. In this context, mathematical modeling—including dynamic games, mean-field approximations, and stochastic control approaches—plays a crucial role in understanding strategic interactions between firms and guiding the design of efficient policy interventions (see for example Cacciarelli, Pinson, Panagiotopoulos, Dixon, and Blaxland (2025) [9]).

When modeling investment decisions in general, and in particular in energy systems, a common approach is to formulate dynamic control or stopping problems, often under uncertainty. In such frameworks, a central planner or a representative agent optimizes a long-term objective, accounting for evolving technological, market, and regulatory conditions (see, for example, Aïd, Campi, Nguyen Huu, and Touzi (2009) [1], Carmona and Ludkovski (2010) [10], Ludkovski and Sircar (2016) [27]). However, when considering renewable energy installations, such as solar panels which can be deployed relatively easily and at varying scales by a multitude of actors, it becomes essential to explicitly model the decentralized and competitive nature of investment. The price of electricity, which depends on the aggregate level of installed capacity, becomes a key channel of interaction between these agents. Directly analyzing multi-player dynamic games, however, quickly leads to computational intractability as the number of participants grows. To overcome this difficulty, it is common to study the limiting regime where the number of players tends to infinity, leading to more tractable mean field approximations that capture the aggregate effect of individual behaviors.

Mean field games (MFGs) study the limiting behaviour of stochastic differential games as the number of (exchangeable) players tends to infinity (see, for instance, Guéant, Lasry, and Lions (2011) [24] for an early review article). In this framework, each agent optimizes their objective function, taking as given the aggregate behavior of the population, which is itself determined in equilibrium as a fixed point of the collective dynamics of the individual strategies. The MFG formulation has since been widely adopted to analyze decentralized decision-making in large populations, providing both analytical and numerical tractability, and insight into emergent macro-level behavior.

In recent years, MFGs have been increasingly applied to a wide range of problems in energy systems. These include renewable investment decisions by Aïd, Dumitrescu, and Tankov (2021) [2], Alasseur, Basei, Bertucci, and Cecchin (2023) [5], Escribe, Garnier, and Gobet (2024) [20] or Aïd, Federico, Ferrari, and Rodosthenous (2025) [3], electricity storage optimization by Alasseur, Ben Taher, and Matoussi (2020) [4], and the design of demand-response programs by Élie, Hubert, Mastrolia, and Possamaï (2021) [19]. MFGs have also been used to study energy mix transitions by Chan and Sircar (2017) [15] and carbon emissions regulation by Carmona, Dayanıklı, and Laurière (2022) [13], Hernández Santibáñez, Jofré, and Possamaï (2023) [25], Bichuch, Dayanıklı, and Lauriere (2024) [8], Dayanikli and Laurière (2024) [16], as well as market design and electricity price formation by Firoozi, Shrivats, and Jaimungal (2022) [21] or Bassière, Dumitrescu, and Tankov (2024) [7]. More recently, the framework has been extended to analyze broader aspects of the energy transition, by Dumitrescu, Leutscher, and Tankov (2024) [18], and energy expenditure from cryptocurrency mining by Li, Reppen, and Sircar (2024) [26]. This list is far from exhaustive, but illustrates the growing role of MFGs in understanding the complex dynamics of modern energy systems.

Among the aforementioned papers, we motivate our work from [5], which develops a deterministic mean-field-type model for capacity expansion in solar energy with an infinite time horizon. In this model, identical producers optimize solar production capacity, and interact through the electricity price, which depends of the total installed capacity. This framework captures the trade-off between investment rewards, costs and the price-depressing effects of overcapacity. This paper characterizes the steady-state equilibrium using Pontryagin’s maximum principle, and provides a study of the effects of subsidies for solar production from a central planner’s point of view.

The model we propose can be seen as a finite-horizon reformulation of [5], with two key extensions. First, we allow for heterogeneity in initial capacities across producers. This extension is particularly relevant in the context of solar energy, where small-scale residential investors may compete with large-scale solar farms. Second, we include interaction not only through the state (installed capacity) but also through the control (installation rate), introducing a crowding effect. Indeed, while producers naturally interact through the market price of electricity, which depends on total installed capacity, installation costs may also be influenced by the aggregate speed of investment across the market, for instance, due to supply-chain congestion or labor constraints.

We employ an approximation where aggregates (or sums) are replaced by a continuum mean multiplied by the number of agents in the sum. This has been used in models of cryptocurrency mining in [26] and Garcia, Sircar, and Soner (2025b) [23], and its error is analyzed in Garcia, Reppen, and Sircar (2025a) [22]. It allows finite agent games with interaction through aggregates to benefit from mean field game technology, in particular reduction of dimension. In the current model, the aforementioned features lead naturally to a mean field game of both state and control, allowing us to study dynamic investment behavior, threshold effects, and the evolution of aggregate capacity over time.

Finally, unlike [5], we consider a finite time horizon, which better reflects the long but bounded planning horizons of investors in the energy sector. For example, investors may anticipate changes in technology or policy over the next two or three decades, such as the emergence of alternative energy sources or regulatory shifts, and may thus optimize over a finite investment window. Nevertheless, the approach we develop here could be naturally reduced to the infinite-horizon setting.

Our analysis is based on characterizing the mean field game equilibrium via a system of coupled Hamilton–Jacobi–Bellman (HJB) and Fokker–Planck (FP) equations. In an homogeneous setting, where all producers start with the same initial capacity, our model reduces to a deterministic control problem similar to [5], but with a finite-time horizon, for which we prove existence and uniqueness of solutions to a forward-backward ODE system and identify threshold behavior in optimal investment. In the heterogeneous case, we study the full mean field game of state and control, establish the structure of the equilibrium using partial differential equation (PDE) methods, and analyze the resulting distribution of installed capacities. In the case of a linear price function, we propose a numerical method based on a quadratic ansatz in the non-installation region and a finite difference scheme in the installation region. We also extend the model to include idiosyncratic randomness in the capacity dynamics, showing that our framework remains tractable under stochastic perturbations.

The remainder of the paper is organized as follows. In Section 2, we introduce our model and its main features. In Section 3, we analyze the homogeneous agents case and derive explicit characterizations of the equilibrium. In Section 4, we turn to the heterogeneous setting, study the associated HJB–FP system, and present our numerical scheme. Finally, in Section 5, we show how our framework extends to include randomness in capacity dynamics. We conclude in Section 6 with a discussion of extensions and policy implications.

2 Model formulation

The formulation of our model echoes that of [5], but is adapted to a finite time horizon (in years) and designed to account for potential heterogeneity in the initial capacities of investors.

We first consider the finite-player model with renewable producers, indexed by . Each producer is characterized by their installed capacity in MW at time . In the absence of new investment, installed capacity is assumed to depreciate exponentially at rate , reflecting a gradual loss in production efficiency over time. A producer can invest in new capacity by choosing an installation rate at each time , which represents the rate in MW/year at which new capacity is added. The dynamics of installed capacity for producer then follow:

| (1) |

starting from a fixed initial installed capacity , and where is the depreciation rate as above. The total (or aggregate) installed capacity is denoted by

| (2) |

Note that since the installation rate is assumed to be non-negative, we necessarily have

| (3) |

The aggregate installed capacity impacts the price at which all producers sell electricity. More precisely, we assume that the common market price at time is given by (in $/MWh), for a (strictly) decreasing price function , reflecting the idea that higher total capacity depresses the market price of electricity due to an abundance of cheap renewable production. The parameter represents the fraction of installed capacity that is effectively producing electricity at time , and thus accounts for the intermittency of renewable energy sources, such as variability in wind or sunlight. For simplicity, we assume is constant over time and we absorb this constant to .

Following [5], the marginal cost of production is constant, denoted by (in $/MWh), and represents operational expenses associated with running the installed capacity. This may include maintenance, insurance and other ongoing management costs of operating a renewable energy asset such as a solar or wind installation. We also model the cost of installing new capacity through two distinct mechanisms that curb rapid expansion:

-

(in $/MW) is the marginal installation cost;

-

(in ($ year)/MW2) is a crowding sensitivity parameter, capturing the additional cost per MW of capacity that arises from increased installation activity in the market. This reflects market frictions such as limited contractor availability, supply chain bottlenecks, or permitting delays that become more pronounced when many producers are simultaneously expanding.

However, contrary to [5], we assume that the installation cost is not constant, but instead increases with the total installation rate due to crowding effects. More precisely, the instantaneous cost of installing new capacity is defined as follows:

| (4) |

Finally, given a fixed initial installed capacity , the individual producer’s objective is defined by the following maximization problem

| (5) |

where is the number of production hours per year, and is a discount rate.

As is well known, this type of multi-agent non-zero sum differential game is difficult to solve, even for the two-player case. For analytical and computational tractability, we will instead study a continuum approximation by a type of mean field game, where a continuum mean multiplied by the number of players proxies for the aggregate quantities and , respectively defined in (2), (4). We first consider in the next section the simpler case of homogeneous producers; the study of the general mean field game is postponed to Section 4.

3 Homogeneous producers

In this section, we assume that all producers start with the same initial installed capacity, for all . This simplification, which makes our model a finite-horizon counterpart of [5] and thus facilitates comparison, will be relaxed in the next section.

In this setting, producers are indistinguishable, and their optimal actions can be derived using Pontryagin’s maximum principle, as in [5].

More precisely, we first focus on the th producer’s optimization problem, , for fixed capacity and effort of other producers. The Hamiltonian corresponding to the objective function (5) is given by

where is the adjoint variable, or costate. Recalling that defined in (4) depends on , the maximization of the previous Hamiltonian leads to the following installation rate

Under the assumption of homogeneous producers, all adjoint variables , , actually coincide, as well as the corresponding optimal investment rates, which can thus be derived by solving the previous equation, leading to

Furthermore, the costate satisfies the following ordinary differential equation (ODE):

We will subsequently drop the dependence on the index , since all producers are identical.

As the number of producers is assumed to be large, we follow here the standard mean field game convention by assuming that the impact of an individual producer to the total capacity is negligible, i.e.

Replacing in the above ODE for the costate, we derive the following simplified ODE,

Still under the assumption that is large, the natural approximation leads to the following formula for the total installation rate defined in (4),

highlighting in particular that installation of new capacity occurs at time if and only if . Finally, summing (1) over and using the previous equation, we derive the following ODE for the total installed capacity defined in (2),

In summary, when is sufficiently large, the original multi-player non-zero-sum game with homogeneous producers can be asymptotically approximated by a mean field game, characterized by the following forward-backward system:

| (6a) | ||||

| (6b) | ||||

The previous system is the finite-horizon analogue of the one derived in [5]. In the next section, we first prove existence and uniqueness for the system (6a)–(6b) under some regularity assumptions for the price function . We then highlight some interesting properties of the solution and the associated optimal installation rate. These theoretical results offer preliminary insights into the investment problem, which are further developed and illustrated by the numerical simulations presented at the end of this section.

3.1 Theoretical results

As mentioned above, the first main result establishes existence and uniqueness of the forward-backward system (6a)–(6b).

Proposition 3.1.

To prove the previous result, we first study the forward system analogous to (6). More precisely, we consider the following system of ODEs,

| (7) |

with initial condition .

Lemma 3.1.

Proof of Lemma 3.1.

Letting , we can rewrite the system (7) of two ODEs as , starting from . Since the price function is assumed to be Lipschitz continuous, the generator is also Lipschitz, so existence and uniqueness holds on by the Picard–Lindelöf theorem for this initial value problem. Note that, in particular, the solution satisfies for ,

| (8a) | ||||

| (8b) | ||||

Let then and be solutions to (7), starting from and respectively, with . To establish the comparison result, we proceed by contradiction: let be the smallest time for which , meaning that for . From (8a), we have , and using further that is decreasing, we deduce , for all . Using this in (8b), we obtain

which leads to a contradiction, since we assumed . In other words, for all we have , implying by (8a) that . ∎

By the previous lemma, it suffices to show existence and uniqueness of such that the solution to (7) starting from satisfies to prove Proposition 3.1.

Proof of Proposition 3.1.

Let and be solutions to (7), starting from and respectively, and assume without loss of generality that . Define then which is positive by Lemma 3.1 for all . Recall that we also have , implying , . Starting from (8b), and using in addition that is -Lipschitz continuous for , we obtain,

Using now (8a), we have

and substituting into the previous inequality, we deduce

where is a constant depending on and . Then, by Gronwall’s Lemma, we deduce

As the case can be treated similarly, we conclude that the map is Lipchitz continuous.

In addition, we can show that this continuous map is negative for sufficiently small, and positive for sufficiently large. Indeed, on the one hand, if

which is non-positive, so in particular smaller than , then the forward system (7) admits the following solution

By the condition on above, we have for all , so in particular as wanted. On the other hand, recall that for all by (3), implying since is decreasing that , which is a positive constant. We then have

and thus taking

we obtain .

From the previous reasoning, we deduce that the continuous map has values of opposite sign on , and thus has a root by Bolzano’s theorem. In other words, there exists such that , which concludes the existence part. Uniqueness follows directly from Lemma 3.1. Indeed, by the comparison principle, one necessarily needs to ensure . ∎

To ensure existence and uniqueness of the solution to the forward-backward system (6a)–(6b), we now work under the assumption that the strictly decreasing price function is Lipschitz continuous. In addition to this main result, we can establish some properties of the total installed capacity over time. We begin by constructing a trivial solution under a specific condition on the model parameters.

Lemma 3.2.

Proof.

The previous result highlights that if or are sufficiently small, or conversely if , , or are sufficiently large, then there will be no new capacity installed at any time. As such model will be less interesting to study, we are led to make the following assumption, which will be verified in the numerical experimentation in Section 3.3, in particular for the parameters chosen in (13).

Assumption 3.1.

The model parameters and the price function are such that and there exists a time for which

Under the previous assumption, the unique solution to the system (6a)–(6b) is not trivial, and exhibits some interesting properties, as stated in the following lemmas.

Lemma 3.3.

Under 3.1, there exists such that for and for .

Proof.

First, if for all , then the corresponding optimal installation rate is , leading to the solution derived in (9). In particular, we have

which contradicts 3.1. Thus, there exists at least one such that .

We then prove by contradiction that . In particular, we assume that and take the first for which , which exists by the above reasoning. In this case, we have , and for . This gives for all , implying . Using in addition that the price function is strictly decreasing, we derive from (6b) the following inequality

However, by 3.1, the right hand side is negative, leading to a contradiction.

To summarize, we necessarily have and . Then by continuity, there exists a time such that . It remains to show that on and on . We also proceed by contradiction, assuming that there exists an interval such that and for . On this interval, the installation rate is zero and the capacity decays at rate . Mathematically, , and thus . Using again (6b), we obtain

and since , we necessarily have , which contradicts the fact that for . Therefore, such interval cannot exist. In other words, if drops strictly below at some point, it cannot cross back to afterwards. Since and , this concludes the proof of existence of as required in the lemma. ∎

We can now prove that the price will stay above the production cost.

Lemma 3.4.

Under 3.1, we have for all .

Proof.

Let given by Lemma 3.3. We first prove that for all . At time , we have by definition and , implying using (6b) that

In particular, . Moreover, for , we have , and therefore satisfies the ODE . In other words, decay at rate starting from , and thus for .

We now prove the inequality for , assuming by contradiction that for some . Note that by 3.1 and the previous reasoning, we have

Therefore, there must exist an interval for , on which and , with being decreasing near and increasing near . More precisely, there exists such that for , while for . Since is strictly decreasing, we have , where denotes the inverse of , and . Moreover, since , we have by Lemma 3.3 that for . The system of equations satisfied by the solution on the interval is thus

Since for , we have , and thus . However, this is in contradiction with the fact that and , since

This concludes the proof that for all .∎

Under 3.1, and thanks to Lemma 3.3, we have for and for . In particular, on , the ODE (6a) for becomes

Differentiating the previous ODE and replacing using (6b) yields the following two-point boundary value problem,

| (10) |

with boundary conditions fixed and , since . Then, for , we have , implying in particular that there is no installation after time . We deduce that for ,

3.2 Linear price function

In this section, we focus on the price being a linear decreasing function, i.e.

and assume 3.1 is satisfied. Under this linear specification for the price, we can obtain a semi-explicit formula for the optimal capacity.

Proposition 3.2.

For a linear price function as above, we have

| (11) | ||||

and where is solution to the following transcendental equation,

| (12) |

Proof.

Recall that is defined in Lemma 3.3. As already mentioned, there is no installation after time , thus for as stated in (11). For , using the linear price in (10) we derive

with boundary conditions fixed and . Straightforward, albeit lengthy, computations show that the candidate solution defined in (11) is indeed solution to this second-order linear ODE boundary-value problem. In particular, are the two solutions of the quadratic equation , with . The constants and are derived from the boundary conditions. We further verify that the denominator in the definition of is not zero, because . Finally, we find from , which leads to (12). Finding from this equation fully determines , and thus , which describe the solution . ∎

Since the linear price is Lipschitz continuous, the previous solution is unique by Proposition 3.1, implying in particular that there exists a unique solution to Equation (12). This will also be observed numerically in the following section.

3.3 Numerical solution

In this section, we numerically solve (6a)–(6b) for two different price functions , linear—as in the previous section—and inverse, and for the parameters used in [2, 5]:

| (13) |

The comparison principle in Lemma 3.1 suggests a shooting method to numerically solve the forward-backward system (6a)–(6b): starting from an arbitrary value , one can solve the forward system (7) to obtain , and then update the choice of depending on the sign of . More precisely, by the comparison principle, one should increase the guess for if , and decrease otherwise. Since both the linear and inverse price functions are assumed to be Lipschitz continuous, this shooting method is guaranteed to converge to the unique solution.

Linear price function.

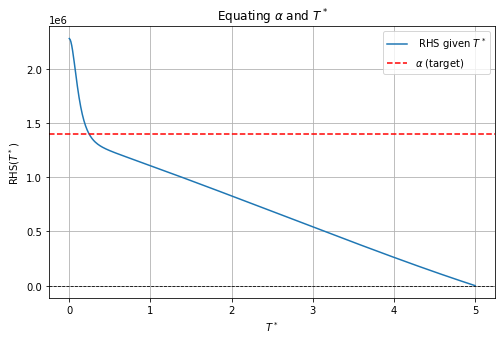

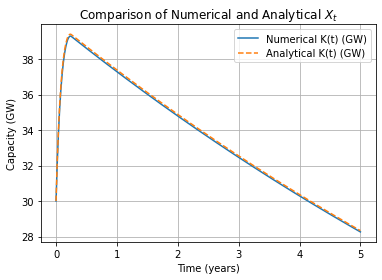

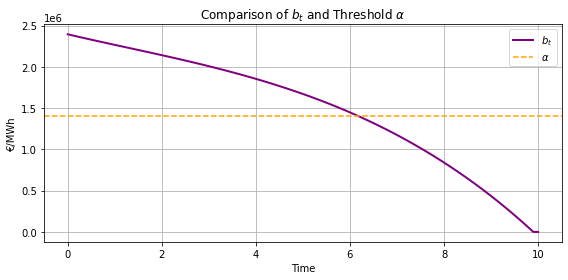

The previous numerical scheme is first implemented for a linear price function of the form with $/MWh, $/MW2h, and compared with another numerical method, consisting of computing by numerically solving (12) and then replacing in the explicit formulas established in Proposition 3.2. The results are displayed in Figure 1 for a fixed time horizon . More precisely, Figure 1 illustrates how to find such that (12) is satisfied. Then, Figure 1 confirms that the solution obtained with the shooting method coincides on with the semi-explicit solution.

The main economic observation from the numerical results illustrated in Figure 1 is the decay of capacity at the natural rate after the critical time . More precisely, the total installed capacity initially increases rapidly, reflecting the strong early incentives to invest. However, due to the finite planning horizon, a critical threshold time emerges, beyond which further investment is no longer profitable. This behavior contrasts sharply with the infinite-horizon results of [5], where investment incentives remain constant over time. Indeed, in our finite time horizon setting, since no profits can be generated after time , producers find it optimal to cease installing new capacity sufficiently in advance of the terminal date to avoid incurring costs that cannot be recouped. In other words, once the remaining time falls below a certain threshold, the opportunity cost of investment outweighs any remaining benefits. Consequently, investment stops, and capacity decays passively at the rate , in line with the theoretical predictions established in Lemma 3.3. This numerical example thus provides a clear illustration of how finite-horizon considerations fundamentally alter investment dynamics compared to the infinite-horizon benchmark.

Inverse price function.

We then consider as in [5] an ‘inverse’ price function of the form , for and the parameters previously described in (13). We first emphasize that, although the price function is not Lipschitz continuous on , this does not cause issues for the dynamics. Indeed, the installed capacity satisfies the lower bound , where is the initial capacity. Thus, remains bounded away from for all , and is effectively Lipschitz on the reachable set . This guarantees the well-posedness of the solution.

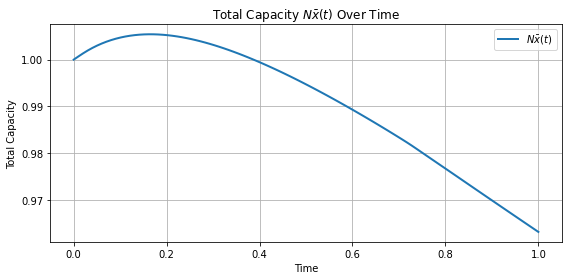

Figure 2 presents the dynamics of the total capacity over time in the case of an inverse price function, for three different finite time horizons (, , and years). We first observe that the solution satisfies Lemma 3.3: as in the previous case with a linear price, there is an initial increase in total capacity, followed by decay at the natural rate .

For the longest time horizons ( years), the total capacity rapidly approaches the infinite-horizon stationary state studied in [5], and remains near this steady state for most of the planning horizon. This illustrates a form of turnpike effect (see, for e.g. [12]): for sufficiently large maturity, the optimal policy drives the system close to the long-run equilibrium early on and maintains it there as long as ‘possible’, i.e. here until it is no longer profitable to invest. Interestingly, when the horizon is larger than years, the simulations indicate that the cessation of investment occurs approximately years before the terminal date, suggesting that the critical time for the given parameters.

In contrast, when the planning horizon is short (e.g., ), the total capacity increases briefly but remains below the infinite-horizon steady state, before decaying at the natural rate , as also seen in Figure 1 for the linear price case with the same maturity. This behavior reflects the fact that producers anticipate the approaching horizon and adjust their decisions to avoid incurring installation costs that cannot be recovered.

4 Heterogeneous producers

We now approximate the finite player game by one in which there is a continuum of producers whose capacities at time are distributed according to the continuous density function on , which smooths out the actual discrete (empirical) distributions of initial installed capacities .

In the approximating MFG, we consider the installed capacity of a representative producer at time . Analogous to (1), we have

| (14) |

where is their installation rate at time . We then let and denote, respectively, the mean installed capacity and mean installation rate at time . We adopt the following approximations of the aggregate quantities and ,

| (15) |

which restore the individual impacts on the aggregates, in the sense that now

This continuum aggregate game approximation was used in the cryptocurrency-mining model in [26], and is further analyzed in [22]. This can also be related to what is called -interpolated mean field games, introduced in [14] and generalized in [17]. As we will see in Lemma 4.1, under the preceding approximations and the additional concavity assumption on the function , producers with smaller installed capacity achieve a higher profit per unit of new energy installed than producers with larger capacity. This, in turn, results in a higher installation rate for smaller producers.

Using the approximations (15) in the original objective (5), we are led to consider the following dynamic value function, for ,

| (16) |

For fixed continuum mean quantities and , the representative producer’s Hamiltonian is

from which we derive the associated optimal response

| (17) |

The value function defined in (16) then satisfies the following Hamilton-Jacobi-Bellman (HJB) equation:

| (18) |

for , with terminal condition . The associated Fokker-Planck (FP) equation for the density of installed capacities at time is

| (19) |

with given initial condition . The preceding system of equations (18)–(19) characterizes a mean field game of state and control, approximating the original -player game. Integrating (17) over and rearranging yields to the following fixed-point condition for the mean installation rate at equilibrium,

| (20) |

The dynamics of the mean state at the mean field equilibrium is then given by

with initial condition .

In Section 4.1 we will explain how this mean field approximation generalize the case of homogeneous producers studied in Section 3. Then, in Section 4.2, we will prove some preliminary results on the value function that will be helpful to solve in Section 4.3 the HJB–FP system (18)–(19).

4.1 Connection to the homogeneous producers case

Under the following simplifications, one recovers the specific setting studied in Section 3:

-

All producers start with the same capacity.

-

There is no direct individual impact on the price.

First, by , the producers remain indistinguishable at all times, in the sense that their individual capacities are all identical, and in particular is a Dirac delta function for every . Moreover, their optimal controls coincide, and we thus deduce from (17)

which coincide with (20) because either the measure of is positive in or it is zero and on . Using this in the dynamic of the mean state at the mean field equilibrium, with the approximation , we derive the required dynamics for the total capacity , namely

| (21) |

It remains to compute the dynamics of defined above, the marginal value along the optimal trajectory, in the spirit of Hotelling’s rule for the economics of exhaustible resources (see [15] for a MFG version). First, by , an individual producer has no direct impact on the price, meaning that its impact is only through the mean capacity. This boils down to replacing by , or for fixed total capacity , . Using this in (18), and differentiating with respect to the individual capacity , we obtain

Noticing that and , the above PDE becomes

Finally, by definition of in (21) and using the chain rule , we deduce

| (22) |

with since . Therefore, under the two simplications –, the general HJB–FP system (18)–(19) boils down to the ODE system (22)–(21), which coincides with the system (6a)–(6b) studied in Section 3. The two methods, Pontryagin maximum principle and HJB, are thus consistent in this setting.

4.2 Properties of the value function

In this section, we establish several properties of the value function, which will guide the numerical resolution of (18)–(19). The following result highlights that producers with smaller capacity install at a larger rate. In fact, we will prove that the optimal strategy for producers with large capacity is to stop installing new capacity.

Lemma 4.1.

Assuming that the revenue is concave, then for all , is also concave, and is non-increasing.

Proof.

Let , and consider two processes and satisfying (14), respectively starting from , at time , and driven by two possibly different controls , . In particular

Let , define the process , starting from at time , and driven by the admissible control . Note that we have

Let now . From the concavity assumption on , we deduce

| (23) |

Moreover, since the cost is linear-quadratic, we also have

| (24) |

Denoting by the running reward in the definition of the value function in (16), namely

| (25) |

we obtain, by summing (23) and (24), the following inequality,

for all . Multiplying by and integrating from to , we deduce

The RHS of the previous inequality is upper bounded by . Finally, taking the supremum over the arbitrary controls and , we deduce

Since and are arbitrary, this completes the proof that the value function is concave.

The fact that is decreasing in is a direct consequence of the concavity of . Indeed, since is concave, is decreasing in , implying that is non-increasing in . ∎

In the following, we will work under the standing assumption stated in the previous lemma, namely that the mapping is concave. This assumption is satisfied in the examples of price functions we will consider, in particular the linear and inverse cases, discussed in Sections 4.3 and 4.4 respectively.

Lemma 4.2.

Suppose that . Then, there exists such that, for all and for any process with dynamics defined by (14) and starting from , the associated optimal control is for all .

Proof.

Since , there exists such that , and we can thus define . Let then . For any process starting from at time , the non-negativity of both the capacities and the admissible control imply

and since is decreasing with , we deduce that for all . Since the revenue at any time , namely , is negative, and the cost of installing new capacity is always non-negative, it is straightforward to conclude that no capacity should be installed on . More precisely, let as above, driven by a non trivial control , and starting from , and let the corresponding uncontrolled process, i.e. , . We clearly have , and by the previous remark on the negative revenue and non-negative cost, we deduce that

recalling that is the running reward defined in (25). Multiplying by and integrating over , it follows that any nonzero control yields a strictly smaller total reward than applying no control. Consequently, the optimal control is . ∎

By the previous lemma, we have that at any time , for sufficiently large, namely . From Equation (17), we deduce that for . Since is concave, the mapping is decreasing. As a result, we define for and fixed mean installation rate ,

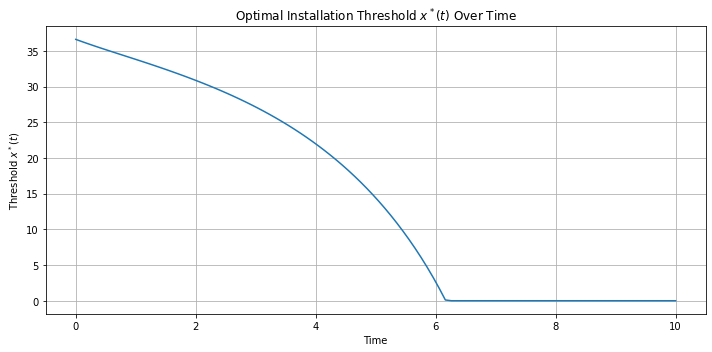

The previous quantity defines a threshold capacity: producers with installed capacity at time will invest to increase their capacity, whereas producers with capacity already exceeding this threshold will not invest. In addition, since , we deduce , and we can define , which is the analogue of in Lemma 3.3 for the homogeneous case. Note that at , since , no producer should install new capacity, i.e. . Using this in the definition of above, we deduce . Since , we conclude that . Note that after , will stay at , meaning that no producer will install new capacity for the remaining time. This is illustrated in Figure 3 and confirmed by the numerical results in Section 4.3.

In the following proposition, we provide a semi-explicit formula for the value function in the non-installation region, as illustrated in Figure 3. In particular, this result shows that if a producer does not install new capacity at some time , they will not invest at any later time . In other words, once a producer’s capacity belongs to the non-installation region, it will remain in that region.

Proposition 4.1.

In the non-installation region , is given by

| (26) |

Proof.

First, in the non-installation region, the HJB equation (18) simplifies to

with terminal condition , which is a linear PDE for which existence and uniqueness holds. It is then straightforward to see that the candidate solution in (26) indeed satisfies the above PDE. Clearly, is also the value obtained under the trajectory , which coincides with the strategy of no installation between and . ∎

4.3 Linear price function

In this section, we revisit the case of a linear price function with , previously studied in Section 3.2 for the homogeneous case.

Corollary 4.1.

In the non-installation region , the value function is given by with

| (27) |

and the threshold curve is

| (28) |

Proof.

Under the linear price specification, we can make the linear quadratic ansatz . From Proposition 4.1, we directly deduce that the pair is solution to the following system of ODE,

and thus given by (27). Finally, Equation (28) is derived from the fact that satisfies when . ∎

From the previous result, note that is only a function of , while is expressed as a function of the trajectory of the mean installed capacity, namely for . Unfortunately, such explicit derivation is not possible in the installation region. More precisely, on , we have by definition that , and the HJB equation (18) satisfied by the value function becomes

| (29) |

However, to our knowledge, no explicit solution exists for the previous HJB equation when the boundary condition is determined by the solution in the non-installation region, given by Corollary 4.1. Nevertheless, in the following, we suggest two numerical approaches to approximate the value function, the corresponding optimal strategy, and the solution to (19) in that region. The first approach uses a quadratic ansatz for approximation, while the second employs a finite difference scheme.

4.3.1 Linear-quadratic approximation

For the first numerical approach, we approximate the solution to PDE (29) by a quadratic function. More precisely, using the ansatz in (29), we obtain that the functions should be solution to the system

| (30a) | ||||

| (30b) | ||||

| (30c) | ||||

By (30a), solves a Riccati equation, and therefore it will be of the form

with solutions to the quadratic equation and a constant to be determined. Similarly, from (30b), depends on a constant , which is the value of at and is similarly not known yet. We choose the above constants and so that , since concavity of requires , and , to ensure that matches at the point with the solution in the non-installation region. Note that we do not impose the smooth pasting conditions along the entire threshold boundary , but only at ; this is precisely what makes the solution an approximation. In fact, if we attempted to match both and continuously along the entire threshold , we would arrive at a contradiction, which is the reason why this is not an exact solution but an approximation. Since the optimal control depends only on , we do not need to need to compute the solution to (30c) for approximating the mean field equilibrium.

Using this quadratic approximation for , we first solve the Fokker–Planck equation (19) by finite differences, as described below, approximating by in the installation region. Next, we update the mean installation rate via the fixed-point equation (20), which becomes under the quadratic approximation

and use this updated value to iterate the algorithm until convergence is achieved.

Summary of the algorithm.

-

1.

Initialization. Start with an initial guess for , for example .

-

2.

Mean state dynamics. Solve numerically starting from to obtain the average capacity .

- 3.

-

4.

Installation region. Use the quadratic ansatz introduced above where , , and are computed by backward integration from terminal conditions , of the associated ODEs (30).

-

5.

Fokker–Planck equation. Starting from the known repartition at time , solve forward in time

which corresponds to the FP equation in (19), to obtain the density . Here we use an explicit Euler finite differences scheme with upwinding for the derivative.

-

6.

Update and iterate. Use the density computed at the previous step in (20) to update . Return to step 2 with the updated and iterate until convergence.

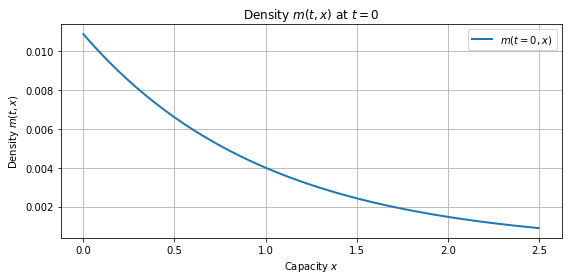

We present a numerical example in which we use the same parameter values as in Section 3.3, see (13), together with $/MWh, $/MW2h specifying the linear price function. For the initial distribution of installed capacities, we consider a truncated exponential distribution. More precisely, we define discrete capacity levels for , where and denotes a maximum capacity. We assign exponential weights of the form , which reflect the fact that smaller producers are more common in renewable electricity markets. We then normalize and rescale these weights to define each so that the total initial capacity equals . This yields a discrete approximation of a truncated exponential distribution over the grid , with mass concentrated near small capacities and a long tail toward larger producers.

The resulting capacity trajectories are presented in Figures 4(a) and 4(b), for horizons and years, respectively. Based on the numerical computations, we identify the times at which all producers cease installing new capacity: in the first case () and in the second (). Beyond these thresholds, no capacity is installed, and the total capacity declines at the natural rate .

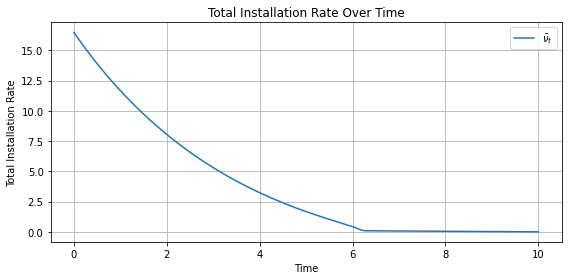

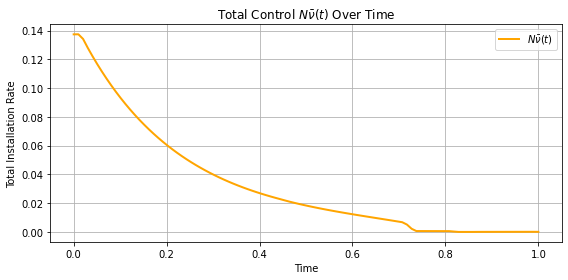

For the second case , we also graphically represent in Figure 5(a) the threshold between the installation and non-installation regions, and observe that its behavior is similar to the illustration in Figure 3. As shown in Figure 5(b), the mean installation rate drops to zero for , confirming that no capacity is installed beyond this time. Finally, still considering , we also plot in Figure 5(c) the function given by (27) in Corollary 4.1. We observe that , as expected. Indeed, this follows from the fact that , and the characterization of the threshold curve in (28).

4.3.2 Finite differences method

The other method relies on a classical finite difference scheme. Specifically, we discretize the HJB equation (18) backward in time on a uniform grid over both time and capacity. At each time step, the spatial derivatives are approximated using central differences, which leads to a nonlinear system of equations for the unknown values at the current time layer. This system is then solved using a root-finding algorithm (e.g., fsolve).

More precisely, given a uniform grid in time and space with step sizes and , we approximate:

Accordingly, the discretized HJB equation at each grid point takes the form:

At each time step, the system is solved backward in time, using to compute . We further impose the following boundary conditions at the boundaries of the domain:

The results are illustrated in Figure 6 for the following parameters:

| (31) |

The linear price function is further characterized by and .

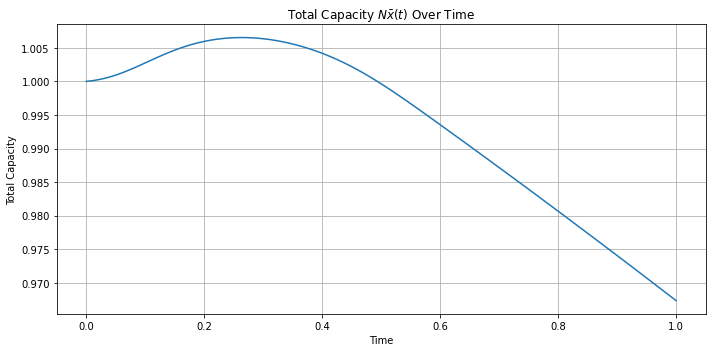

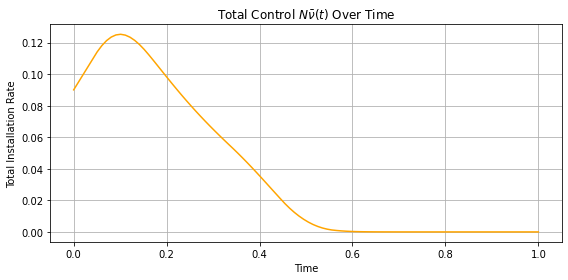

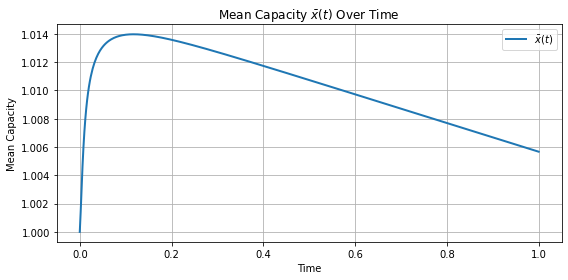

Figures 6(a) and 6(b) display the trajectories of the mean capacity and the optimal control over time. For comparison, we also solve the system numerically using the alternative method that approximates by two quadratic functions. As shown in Figures 6(d) and 6(e), this approach produces results that are very similar to those obtained with the finite difference scheme. This agreement verifies that both numerical methods are accurate and consistent with each other.

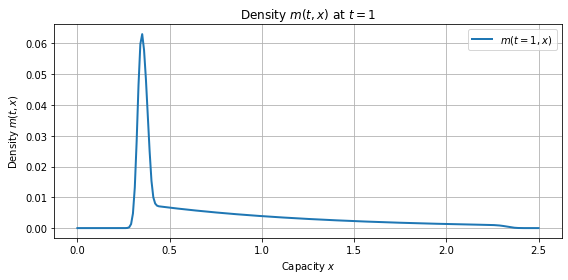

In addition, Figures 6(c) and 6(f) show the distribution of capacities at and . As intended, the initial distribution is exponential, and over time it becomes more concentrated around higher capacities, since producers with smaller initial capacities tend to invest more rapidly.

4.4 Inverse price function

We conclude this section by returning to the inverse price case, examined in [5] and previously in Section 3.3 for the homogeneous case. The main theoretical result presented below directly follows from Proposition 4.1, using the specification for the price function.

Corollary 4.2.

In the non-installation region , is given by

Therefore, in the non-installation region, we can further compute

which is strictly decreasing in , confirming that is indeed concave. Then, should be determined as the solution, if it exists, to , . However, contrary to the results for the linear price case in Corollary 4.1, no explicit analytic expression for the threshold function can be derived here. Nevertheless, can be approximated numerically. Moreover, since there is no obvious ansatz to approximate the solution to the HJB equation in the installation region, we focus here on the second numerical method, based on finite differences. Numerical results are presented for the same parameter values used in the previous section, as specified in Equation 31, but with to characterize the inverse price function. This value of is chosen so that the inverse price is of the same order as the linear price for near , the initial total capacity, ensuring that the results remain comparable in terms of dynamics and price levels. The trajectories of the mean capacity and the mean installation rate are shown in Figures 7(a) and 7(b) respectively.

The simulation shows that the inverse price function leads to a strong incentive for early installation: when aggregate capacity is low, the electricity price becomes very high, resulting in steep marginal rewards for producers. This creates a pronounced front-loading in installation behavior, as producers seek to take advantage of the initially high prices before crowding drives them down. Consequently, total production ramps up sharply in the early part of the horizon.

5 Production intermittency

In this section, we briefly study a version of the model with randomness. Specifically, suppose that evolves according to

where is a Brownian Motion. Introducing randomness in the installed capacity indirectly generates volatility in the instantaneous profit . In this sense, incorporating stochastic fluctuations in the state variable could serve to model the intermittency of renewable energy sources—such as variations in solar or wind output—which leads to uncertain revenue streams. The variability from intermittency of renewables (see, for instance Carmona and Yang (2024) [11]) increases the sensitivity of grids to fluctuations. Large-scale expansions, without corresponding flexibility measures, can make systems more exposed to operational risks (see Shrivats, Sircar, and Yang (2024) [28]).

The value function should now be defined as follows,

for all . The form of the optimal control remains the same as (17), and the corresponding HJB equation is similar to (18),

with terminal condition . More precisely, if we let in the above HJB equation, we recover (18). Similarly, the Fokker-Planck becomes

Finally, the fixed point condition coincides with (20). Intuitively, this model is expected to yield outcomes that closely resemble those of the deterministic setting studied in the previous sections. For conciseness, we limit ourselves in this section to presenting a numerical example that illustrates this resemblance. Specifically, when the price is linear and , the two numerical methods described earlier can be implemented.

The analogue of the first method discussed in Section 4.3.1 is to approximate by a quadratic function in each of the two regions, namely

with solutions to the same equations (27, 30b, 30c) as before, but now solve

Then, we can apply the numerical method of Section 4.3.1 and solve these two equations.

Alternatively, we can directly discretize the HJB equation using a central finite difference scheme, following the approach described in Section 4.3.2. The resulting discretized HJB equation takes the form

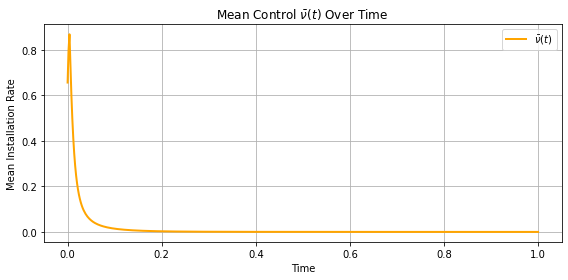

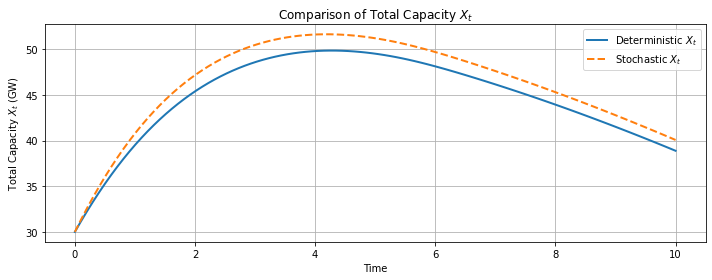

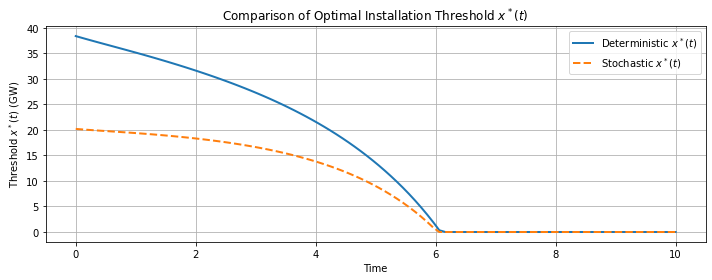

For illustration, we apply the first method with the same parameters as in Section 4.3.1, with and . The resulting capacity is shown in Figure 8(a), and the threshold is presented in Figure 8(b). We observe that the capacity trajectory with randomness (orange dotted curve) closely resembles the deterministic trajectory (blue curve). However, is noticeably smaller compared to Figure 5(a). This difference arises because becomes much larger when , since .

This reduction reflects agents’ increased caution under uncertainty. In particular, the stochastic component in the dynamics introduces a precautionary effect, where firms may delay or reduce investments to hedge against downside risks. This behavior is consistent with real-world observations, where firms facing high uncertainty (e.g., due to variable output from renewables or policy instability) often exhibit more conservative expansion strategies.

6 Conclusion

We conclude with a few modeling comments that suggest possible extensions or refinements of the current setup.

While we model the electricity price as a function of total installed capacity only, a more general formulation could allow the price to depend explicitly on time, i.e. , to capture external seasonal effects, regulatory interventions, or trends in demand that are not driven solely by supply. Incorporating such time dependence could be particularly relevant for settings where electricity prices exhibit strong periodic or structural trends.

Another possible extension is to introduce heterogeneity across firms in terms of cost structures, risk preferences, or technologies. For instance, the marginal installation cost could be modeled as a decreasing function of installed capacity , reflecting economies of scale. Similarly, the crowding sensitivity parameter could also be specified as , decreasing in , to capture the idea that larger firms may face lower relative frictions due to better access to contractors, permits, or supply chains. This would allow larger producers to install capacity more efficiently than smaller ones, capturing realistic differences in incentives between incumbents and new entrants.

Taking into account storage investment decisions and flexible resources (e.g. demand response, dispatchable backup) into the model would allow to assess their interaction with intermittent renewable deployment. Recent events—such as the major power outage in Spain and Portugal triggered by grid imbalances and a lack of short-term flexibility [6]—highlight the critical role of these mechanisms in ensuring system stability during high-renewable penetration.

Finally, it could be relevant to study the impact of various policy tools—such as carbon taxes, renewable subsidies, or capacity remuneration mechanisms—on long-term investment decisions within the mean field framework. For instance, as in [5], one could model subsidies that reduce the marginal cost of production or the installation cost , and examine how these interventions shift the equilibrium and accelerate renewable deployment.

References

- Aïd et al. [2009] R. Aïd, L. Campi, A. Nguyen Huu, and N. Touzi. A structural risk–neutral model of electricity prices. International Journal of Theoretical and Applied Finance, 12(7):925–947, 2009.

- Aïd et al. [2021] R. Aïd, R. Dumitrescu, and P. Tankov. The entry and exit game in the electricity markets: a mean-field game approach. Journal of Dynamics and Games, 8(4):331–358, 2021.

- Aïd et al. [2025] R. Aïd, S. Federico, G. Ferrari, and N. Rodosthenous. Regulation in a mean-field investment game with climate damage. Preprint SSRN 5235340, 2025.

- Alasseur et al. [2020] C. Alasseur, I. Ben Taher, and A. Matoussi. An extended mean field game for storage in smart grids. Journal of Optimization Theory and Applications, 184(2):644–670, 2020.

- Alasseur et al. [2023] C. Alasseur, M. Basei, C. Bertucci, and A. Cecchin. A mean field model for the development of renewable capacities. Mathematics and Financial Economics, 17(4):695–719, 2023.

- Bajo-Buenestado [2025] R. Bajo-Buenestado. The Iberian Peninsula blackout — Causes, consequences, and challenges ahead. Technical report, Rice University’s Baker Institute for Public Policy, 2025.

- Bassière et al. [2024] A. Bassière, R. Dumitrescu, and P. Tankov. A mean-field game model of electricity market dynamics. In F. E. Benth and A. E. D. Veraart, editors, Quantitative Energy Finance: Recent Trends and Developments, pages 181–219. Springer Nature Switzerland, 2024.

- Bichuch et al. [2024] M. Bichuch, G. Dayanıklı, and M. Lauriere. A stackelberg mean field game for green regulator with a large number of prosumers. Preprint SSRN 4985557, 2024.

- Cacciarelli et al. [2025] D. Cacciarelli, P. Pinson, F. Panagiotopoulos, D. Dixon, and L. Blaxland. Do we actually understand the impact of renewables on electricity prices? A causal inference approach. Preprint arXiv:2501.10423, 2025.

- Carmona and Ludkovski [2010] R. Carmona and M. Ludkovski. Valuation of energy storage: an optimal switching approach. Quantitative Finance, 10(4):359–374, 2010.

- Carmona and Yang [2024] R. Carmona and X. Yang. Joint granular model for load, solar and wind power scenario generation. IEEE Transactions on Sustainable Energy, 15(1):674–686, 2024.

- Carmona and Zeng [2024] R. Carmona and C. Zeng. Leveraging the turnpike effect for mean field games numerics. IEEE Open Journal of Control Systems, 3:389–404, 2024.

- Carmona et al. [2022] R. Carmona, G. Dayanıklı, and M. Laurière. Mean field models to regulate carbon emissions in electricity production. Dynamic Games and Applications, 12(3):897–928, 2022.

- Carmona et al. [2023] R. Carmona, G. Dayanikli, F. Delarue, and M. Lauriere. From Nash equilibrium to social optimum and vice versa: a mean field perspective. Preprint arXiv:2312.10526, 2023.

- Chan and Sircar [2017] P. Chan and R. Sircar. Fracking, renewables, and mean field games. SIAM Review, 59(3):588–615, 2017.

- Dayanikli and Laurière [2024] G. Dayanikli and M. Laurière. Multi-population mean field games with multiple major players: application to carbon emission regulations. In 2024 American Control Conference, pages 5075–5081, 2024.

- Dayanikli and Lauriere [2025] G. Dayanikli and M. Lauriere. Cooperation, competition, and common pool resources in mean field games. Preprint arXiv:2504.09043, 2025.

- Dumitrescu et al. [2024] R. Dumitrescu, M. Leutscher, and P. Tankov. Energy transition under scenario uncertainty: a mean-field game of stopping with common noise. Mathematics and Financial Economics, 18(2):233–274, 2024.

- Élie et al. [2021] R. Élie, E. Hubert, T. Mastrolia, and D. Possamaï. Mean-field moral hazard for optimal energy demand response management. Mathematical Finance, 31(1):399–473, 2021.

- Escribe et al. [2024] C. Escribe, J. Garnier, and E. Gobet. A mean field game model for renewable investment under long-term uncertainty and risk aversion. Dynamic Games and Applications, 14(5):1093–1130, 2024.

- Firoozi et al. [2022] D. Firoozi, A. V. Shrivats, and S. Jaimungal. Principal agent mean field games in REC markets. Preprint arXiv:2112.11963, 2022.

- Garcia et al. [2025a] N. Garcia, M. Reppen, and R. Sircar. Continuum aggregate games. In preparation, 2025a.

- Garcia et al. [2025b] N. Garcia, R. Sircar, and M. Soner. Mean field games of control and cryptocurrency mining. Preprint, 2025b.

- Guéant et al. [2011] O. Guéant, J.-M. Lasry, and P.-L. Lions. Mean field games and applications. In Paris-Princeton Lectures on Mathematical Finance 2010, volume 2003, pages 205–266. Springer Berlin Heidelberg, Berlin, Heidelberg, 2011.

- Hernández Santibáñez et al. [2023] N. Hernández Santibáñez, A. Jofré, and D. Possamaï. Pollution regulation for electricity generators in a transmission network. SIAM Journal on Control and Optimization, 61(2):788–819, 2023.

- Li et al. [2024] Z. Li, A. M. Reppen, and R. Sircar. A mean field games model for cryptocurrency mining. Management Science, 70(4):2188–2208, 2024.

- Ludkovski and Sircar [2016] M. Ludkovski and R. Sircar. Technology ladders and R&D in dynamic Cournot markets. Journal of Economic Dynamics and Control, 69:127–151, 2016.

- Shrivats et al. [2024] A. Shrivats, R. Sircar, and X. Yang. Quantifying renewables reliability risk in modern and future electric grids. The Journal of Energy Markets, 2024. To appear.