Probabilistic closed-form formulas for pricing nonlinear payoff variance and volatility derivatives under Schwartz model with time-varying log-return volatility

Department of Statistics

Faculty of Science, Kasetsart University

Bangkok 10900, Thailand

nontawat.bunch@ku.th

&

Department of Mathematics

Faculty of Science, Kasetsart University

Bangkok 10900, Thailand

udomsak.ra@ku.th

&

Department of Mathematics

Faculty of Science, Kasetsart University

Bangkok 10900, Thailand

phiraphat.sut@ku.th

Abstract

This paper presents closed-form analytical formulas for pricing volatility and variance derivatives with nonlinear payoffs under discrete-time observations. The analysis is based on a probabilistic approach assuming that the underlying asset price follows the Schwartz one-factor model, where the volatility of log-returns is time-varying. A difficult challenge in this pricing problem is to solve an analytical formula under the assumption of time-varying log-return volatility, resulting in the realized variance being distributed according to a linear combination of independent noncentral chi-square random variables with weighted parameters. By utilizing the probability density function, we analytically compute the expectation of the square root of the realized variance and derive pricing formulas for volatility swaps. Additionally, we derive analytical pricing formulas for volatility call options. For the payoff function without the square root, we also derive corresponding formulas for variance swaps and variance call options. Additionally, we study the case of constant log-return volatility; simplified pricing formulas are derived and sensitivity with respect to volatility (vega) is analytically studied. Furthermore,we propose simple closed-form approximations for pricing volatility swaps under the Schwartz one-factor model. The accuracy and efficiency of the proposed methods are demonstrated through Monte Carlo simulations, and the impact of price volatility and the number of trading days on fair strike prices of volatility and variance swaps is investigated across various numerical experiments.

Keywords Schwartz one-factor model Time-varying volatility Noncentral chi-square Volatility swaps Volatility options Vega

1 Introduction

Commodity price volatility has become a focal point for academics, investors, and economists due to its critical role in volatility trading and risk management. Unlike stocks, bonds, and other traditional financial instruments, commodities exhibit exceptionally large price swings around a long-term equilibrium [1], driving demand for volatility-based instruments such as variance and volatility swaps. These forward contracts allow traders to take pure positions on volatility through a simple payoff: at maturity, the long pays a fixed variance strike and receives any realized variance above that level, while the short pays the realized variance and receives the fixed strike. Investor interest in these swaps surged in 1998 following the collapse of Long-Term Capital Management (LTCM) and the ensuing spike in market turbulence; initially dominated by hedge funds selling volatility to dealers [19], the market has since grown into a vibrant arena with extensive research on pricing and hedging these contracts.

Research on variance swap pricing has overwhelmingly focused on equity markets, where a series of foundational studies has established robust valuation and replication methods. Demeterfi et al. [8] demonstrated that, under continuous price paths, variance swaps can be statically replicated using portfolios of vanilla options and that volatility swaps follow by dynamically trading those positions, also deriving an analytical fair-value formula that accounts for realistic volatility skews. Windcliff, Forsyth and Vetzal [35] applied numerical partial integro-differential equation methods to price volatility products and explored delta and delta-gamma hedging strategies for volatility swaps. Javaheri, Wilmott and Haug [13] valued and hedged volatility swaps within a GARCH(1,1) stochastic volatility framework by determining the first two moments of realized variance through a PDE approach and approximating expected realized volatility via Brockhaus and Long’s second-order convexity djustment [2]. Théorét, Zabré and Rostan [33] then provided an analytical solution for pricing volatility swaps under the same GARCH model and applied it to the S&P60 Canada index. Subsequent work by Carr and Madan [15] confirmed exact replication of variance swaps through vanilla options, Ma and Xu [18] incorporated control variate techniques in stochastic volatility settings, Zhu and Lian [37] derived closed-form solutions under Heston’s two-factor model, Rujivan and Zhu [24] offered a simplified analytical approach for discretely sampled variance swaps, Zheng and Kwok [36] extended pricing to generalized swaps with simultaneous jumps in price and variance, Shen and Siu [28] included stochastic interest rates and regime switches, and Chan and Platen [4] developed explicit formulas under the modified constant elasticity of variance model. Despite this extensive equity-focused literature, commodity markets have received little attention; the sole exception is Swishchuk [32], who used the Brockhaus–Long approximation to derive variance and volatility swap formulas for energy assets following a continuous-time GARCH(1,1) process.

In the context of volatility and variance derivatives for commodities, models for stochastic commodity price dynamics differ from those for other asset classes because they explicitly account for the convenience yield and allow for multiple sources of uncertainty. Schwartz [25] introduced three such models. In the first model the log of the spot price follows a mean reverting process around a constant convenience yield. The second model treats the convenience yield itself as stochastic. The third model further extends uncertainty by allowing interest rates to evolve randomly over time. In 2016, Chunhawiksit and Rujivan [6] proposed an analytical closed-form solution for pricing discretely-sampled variance swaps on commodities under the one-factor Schwartz model, defining realized variance via squared percentage returns, validating its financial meaningfulness, and demonstrating substantial computational efficiency gains over Monte Carlo (MC) methods. In the same year, Weraprasertsakun and Rujivan [34] extended this method by deriving a closed-form formula for pricing discretely-sampled variance swaps on commodities, now defining realized variance in terms of squared log returns, showing that their solution produces financially meaningful fair delivery prices throughout the model’s parameter space and dramatically reduces the computational burden compared to MC simulations, thereby offering market practitioners a highly efficient and implementable analytical tool.

However, the results proposed in [6, 34] and also [5, 9, 31] are limited to variance swaps because the closed-form formulas were derived by solving the Feynman–Kac formula to obtain conditional moments of the one-factor Schwartz model, whereas volatility swaps cannot be obtained through conditional moments and instead require half moments of log return. And, of course, the closed-form formula for the half moments of the log returns under the one-factor Schwartz model is not currently available, so a new technique must be introduced to address this issue.

In this paper, we derive closed-form analytical formulas for pricing discretely sampled volatility and variance derivatives under the one-factor Schwartz model with time-varying log-return volatility by expressing the realized variance as a linear combination of independent noncentral chi-square random variables and using their probability density function (PDF) to compute the expectation of its square root. As a result, we obtain explicit pricing formulas for volatility swaps, volatility call options, variance swaps and variance call options (with simplified expressions and analytical vega in the constant-volatility case), propose simple closed-form approximations for volatility swaps, and demonstrate the accuracy and efficiency of our methods through extensive MC simulations.

The remainder of this paper is organized as follows. Section 2 reviews the one-factor Schwartz model. Section 3 introduces variance and volatility swaps. In Section 4, we derive the probability density function of the realized variance and present its conditional moments. Section 5 uses these results to obtain closed-form pricing formulas for volatility and variance swaps and their corresponding options, and provides sensitivity analyzes. Section 7 validates our analytical findings with numerical experiments and discussion. Finally, Section 8 summarizes our contributions and suggests avenues for future research.

2 Schwartz model

In this section we recall Schwartz one-factor model [25] for commodity price dynamics, which we adopt under the risk-neutral probability space to ensure absence of arbitrage in variance swap pricing. Under , the commodity spot price follows the stochastic differential equation (SDE)

| (1) |

where is the speed of mean reversion to the long-run log-price level , is the volatility, and is a standard Brownian motion on . Defining the log-price process and applying Itô’s lemma to (1) yields the Ornstein–Uhlenbeck (OU) process

| (2) |

where is the instantaneous convenience yield at time and

It is important to note that, unlike the original OU process sense, a commodity does not behave like a conventional asset, and its spot price (or equivalently the logarithm of the spot price) serves as the state variable on which contingent claims are written.

3 Variance and volatility swaps

Following the collapse of LTCM in late 1998, when implied stock-index volatility reached unprecedented levels, the market for variance and volatility swaps began to expand. Unlike traditional stock options, these swaps provide pure exposure to future volatility [8] and have attracted investment banks and other financial institutions. Investors use them to speculate on future volatility, to trade the spread between realized and implied volatility or to hedge volatility exposure in other positions. Today, variance and volatility swaps are actively quoted across a broad range of assets such as stock indices, currencies and commodities. In the remainder of this chapter, we provide a comprehensive overview of their definitions, valuation strategies and practical implementations.

In a mathematical context, we define discretely sampled volatility and variance based on the log-returns of the underlying asset price. The primary objective of this paper is to estimate the log-return realized variance, commonly referred to as the realized variance, which is defined as

| (3) |

for , where is the underlying asset’s closing price at time for the -th observation belonging to the total number of observations . The term is the annualization factor, used to standardize the realized variance over the time horizon .

3.1 Variance swaps

Under a risk-neutral martingale measure , and assuming that is the time-varying risk-free interest rate at time , the value of a variance swap at time can be expressed as the expected present value of its future payoff:

where denotes the notional amount of the swap, measured in dollars per annualized variance point. More specifically, represents the amount received by the holder at maturity for each unit by which the realized variance exceeds the strike .

Because there is no upfront cost to enter into a variance swap, we have . Therefore, the fair strike price of a variance swap is given by

| (4) |

where denotes the conditional expectation of a random variable with respect to the filtration under the risk-neutral martingale measure . Thus, the valuation problem for a variance swap reduces to computing the expected value of the future realized variance in the risk-neutral world.

3.2 Volatility swaps

Similar to the valuation of a variance swap, the value of a volatility swap at time can be expressed as the expected present value of the future payoff,

where is the notional amount of the swap, denominated in dollars per annualized volatility point. Specifically, represents the amount that the holder of the contract receives at maturity if exceeds the strike by one unit.

Since there is no upfront cost to enter into a volatility swap, we set . Consequently, the fair strike price of a volatility swap is given by

| (5) |

3.3 Practical applications

Volatility exhibits several attractive features for trading. First, it rises with risk and uncertainty and tends to increase more after bad news than after good news. Second, it follows a mean reverting process so high volatility levels decrease and low levels increase. Finally, there is a negative correlation between volatility and asset prices so volatility remains high after large downward moves in the market [8]. Variance and volatility swaps allow investors to profit from or hedge against changes in future volatility. For example, a dealer who writes an option can face losses if volatility spikes and the option must be repurchased at a higher price. To transfer this risk, the dealer can enter a volatility swap with a hedge fund. The hedge fund takes the opposite position because it expects volatility to fall and seeks to earn a profit. As the most direct instruments for trading volatility, variance and volatility swaps are central to modern financial markets and will continue to play a key role.

4 The PDF of the realized variance

Consider follows the OU stochastic process (2) with mean and variance . Moreover, a covariance of and is denoted by . Let also known as the log-return. We obtain

| (6) |

where

| (7) |

and

| (8) |

at time for . So this means that is a normally distributed random variable with mean and variance for all .

By the definition of the noncentral chi-square random variables, we have

| (9) |

for all where is a noncentral chi-square distribution with degrees of freedom and noncentrality parameter where then

| (10) |

and

| (11) |

for . The log-return realized variance defined in (3) can be shown in terms of a linear combination of noncentral chi-square random variables, by applying (6)–(11), as

| (12) |

where the weighted parameter can be defined by

| (13) |

for .

4.1 Laguerre expansions for the PDF of

Over the past several decades, the distribution of linear combinations of noncentral chi-square random variables, or equivalently, quadratic forms in normal random variable vectors, has been the subject of extensive research. The PDFs associated with the distribution have been expressed in various representations, accompanied by many proposed methods for their efficient computation. For instance, in 1961, Shah and Khatri [27] introduced the distribution for the definite case using power series expansions. In 1962, Ruben [22] proposed a representation for the infinite case in terms of chi-squared series. Subsequently, in 1963, Shahe [26] extended their approach to the infinite case and compared their results with those of Ruben. Then, in 1967, Kotz et al. [16] represented the distribution in terms of various expressions including power series expansions, Laguerre series expansions, chi-squared series, and noncentral chi-squared series. Furthermore, in 1977, Davis [7] presented percentage point approximation tables for the distribution under a differential equation approach. To represent the PDF of a linear combination of independent noncentral chi-square random variables with positive weights, as given in (12), one of the most efficient computational methods is developed from the work of Kotz et al. (1967) and Davis (1977), and is represented in terms of Laguerre series expansions proposed by Castaño-Martínez and López-Blázquez in 2005 [3].

For our study, we apply the presented approach by Castaño-Martínez and López-Blázquez [3] to obtain the PDF of , as shown in the following theorem. The generalized Laguerre function is given by the following series representation

where the parameter and the fractional order for some .

Theorem 1.

Let . The PDF of written as , satisfying

and can be illustrated as

| (14) |

with three parameters , , and , where is the gamma function. The coefficient , for , depends on time-varying log-return volatility and mean for , satisfying the following recurrent relation,

| (15) | |||

| (16) | |||

| (17) |

Proof.

We will derive , i.e. the PDF of , by applying the presented approach by Castaño-Martínez and López-Blázquez [3] in Section 3 as follows.

Firstly, we consider a solution of the mean-reverting OU process (2),

We know that is normally distributed with mean

| (18) |

for given , and variance

| (19) |

at time for . In addition, since and are jointly distributed normal random variables, we then obtain that its covariance can be expressed as

| (20) |

where (see Franco [11]). According to the second term on RHS of the log-return in (6), the increments and for all and , are independent by using the property of a standard Brownian motion. Therefore, for , is the sequence of independent and identically distributed (i.i.d) random variables. Thus, a result of a random variable as illustrated in (3) is a linear combination of independent noncentral chi-square random variables with weighted parameters as defined in (12), for .

Secondly, in Section 3 of [3], the constants and the parameters, , and , are replaced by the following: . Consequently, by applying equations (3.2), (3.3), (3.4)a, and (3.4)b in [3], the PDF of can be constructed as shown in (14) where the recurrent coefficient for , can be calculated by using (15) and (16) as well as the coefficient for , can be calculated by using (17). ∎

4.2 The explicit formula for

By utilizing the Laguerre expansion (14) along with some properties of the generalized hypergeometric function

| (21) |

where denotes the usual Pochhammer symbol [29], the explicit formula for the -th conditional moment of is derived in the following theorem.

Theorem 2.

Proof.

We define

for where ’s, , are given in Theorem 1. Employing the symbolic computing package in MATHEMATICA yields

| (23) |

According to the uniformly convergent series derived in Theorem 1, we obtain that the series converges uniformly to i.e.,

| (24) |

By using the property of uniformly convergent series and applying (23), (24) yields

This completes the proof. ∎

4.3 Approximates for truncation errors of

On a computation of by machine, we have to estimate the error from substituting an infinite sum with a finite sum which is a method known as truncation error. An approximation for the truncation errors of will be derived in this subsection by applying the approaches stated in Subsection 3.1 of Castaño-Martínez and López-Blázquez (see [3]).

we define

for any , , such that . Thus, a truncation error of order of is denoted by . To approximate our truncation error, bounds of for , given in (15)–(17), can be derived below.

Lemma 1.

The coefficient , , satisfies

| (25) |

for , where and

| (26) |

where is a positive integer and . In addition,

Proof.

We will derive bounds of coefficient , , by applying the presented approach in Lemma 3.1 written by Castaño-Martínez and López-Blázquez (see [3]) as follows. The constants and parameter , and , are placed by the following: . Then, by applying Lemma 3.1, bounds of coefficient , , can be constructed as shown in (25) where the mention at the end can be derived by using Remark 3.1 given by Castaño-Martínez and López-Blázquez [3]. ∎

According to Lemma 1, we further define

| (27) |

for all , , such that and , where

| (28) |

Due to Lemma 1, our bound for truncation error can be derived as the following theorem.

Theorem 3.

Suppose that and . Then

| (29) |

for all and .

5 Pricing volatility and variance swaps

By applying Theorem 1 which introduces the PDF of , the fair strike price of volatility and variance swaps, defined in (5) and (4) respectively, can be expressed as

| (30) |

and

| (31) |

respectively.

Although and can be enumerated by using several techniques of numerical integration for both improper integrals above ,(30) and (31), those numerical techniques can lead to complications. To avoid those complications, we simplify the integral into a series of an infinite summation of a generalized hypergeometric function. It is obtained by analyzing the conditional expectation order of known as a raw moment proposed in Theorem 2.

In this section, the fair strike price of a volatility swap and variance swap is derived by setting and in (22), respectively. Additionally, we analyze the closed-form formulas for the fair strike price of both swaps in two scenarios, depending on the variance of the log-return: one where the variance changes over time, and another where it remains constant.

5.1 Pricing formulas for volatility and variance swaps: Time-varying log-return volatility

Due to the solution of the SDE in (2), , for , is a normally distributed random variable with time-varying log-return volatility. The difference between and , denoted as in (6), for , also follows a normal distribution with mean given by (18) and variance given by (19). The covariance of this difference is provided by (20).

In this subsection, these time-varying log-return volatility is used to analyze the explicit formulas for volatility and variance swaps, where is considered as a linear combination of independent noncentral chi-square random variables with weighted parameters for .

5.1.1 Volatility swaps price:

By using the probabilistic approach based on the PDF 14, the following theorem provides a closed-form formula for pricing a volatility swap under time-varying log-return volatility. The corresponding result for the case of constant log-return volatility is presented in the subsequent corollary.

Theorem 4.

Corollary 1.

5.1.2 Variance swaps price:

Closed-form formulas for pricing variance swaps under both time-varying and constant log-return volatility are presented in the following theorem and corollary.

Theorem 5.

Corollary 2.

5.2 Pricing formulas for volatility and variance swaps: Constant log-return volatility

In this subsection, we explore the other explicit solutions of volatility and variance swaps by assuming that the variances of log-returns are set to be the same.

Referring to (6), we assume that is a normally distributed random variable with mean and given variance for , where and are computed by (7) and (8) respectively. In other words, for , we choose the variance at i.e. at time , to represent the variance of log-returns for all -th observations. Since for forms a sequence of i.i.d. random variables as shown in the proof of Theorem 1, we can define a random variable

| (36) |

where follows the noncentral chi distribution with degrees of freedom and noncentrality parameter . Furthermore, a random variable defined by

| (37) |

is distributed according to the noncentral chi-square distribution with degree of freedom and noncentrality parameter where

| (38) |

and

| (39) |

The interesting results are discussed in the following theorems when is a random variable that can be written in terms of a linear combination of independent noncentral chi-square distributions without weighted parameters.

5.2.1 Volatility swaps price:

Since can be represented in terms of , the following theorems provide closed-form formulas for pricing volatility swaps under constant log-return volatility, in the cases where the sum of time-varying log-return means is greater than zero and equal to zero, respectively.

Theorem 6.

Proof.

Due to (36), we have the following explicit form (see Johnson et al. [14])

| (41) |

where is given in (39). We note that the conditional expectation above is always positive by the property of the explicitly of the Laguerre function (see Mirevki and Boyadiiev [20]). Thus, the realized volatility can be expressed as

Theorem 7.

Suppose that and for all . The fair strike price of a variance swap can be shown as

| (42) |

where is defined in (38).

Proof.

We proceed with the same approach as in the proof of the previous Theorem 6, but now we replace . We then obtain that

| (43) |

where with , and (see Mirevki and Boyadiiev [20]). Hence, we obtain (42) by substituting (43) on the RHS of (41). Note that the proof can be completed by considering that is distributed according to the central chi distribution with degrees of freedom when . ∎

5.2.2 Variance swaps price:

The following theorems are closed-form formulas for pricing variance swaps under constant log-return volatility, in the cases where the sum of time-varying log-return means is greater than zero and equal to zero, respectively.

Theorem 8.

Proof.

Theorem 9.

Suppose that and for all . The fair strike price of a variance swap can be shown as

| (46) |

where is defined in (38).

Proof.

According to Corollary 1 and 2, if we choose the arbitrary constant , we will get Theorem 6 and 8 respectively. Besides, in [23] written by Rujivan and Rakwongwan, both corollaries can be implied to Theorem 2.3 when and , and Theorem 2.7 when , and , respectively. In their work, the parameters are obtained by using the Black-Scholes model with a time-varying risk-free interest rate.

5.2.3 Vega of and

In financial mathematics, to measure the sensitivity of a derivative instrument’s value, we commonly study its partial derivative with respect to the parameter of interest. In this third-level section, we focus on the first-order partial derivative with respect to the price volatility , known as vega, denoted by (see Hull [12]). In other words, vega can be interpreted as the amount of money invested in the derivative instrument per share, indicating the profit or loss resulting from a one percentage point increase or decrease in volatility. We note that an increase in volatility suggests a higher chance of the underlying asset reaching extreme price levels, leading to a corresponding rise in the derivative instrument’s value. Conversely, reduced volatility tends to lower the derivative instrument’s value.

In the following corollaries, exact formulas for vega of volatility and variance swaps, and , are produced by using Theorems 6–9.

Corollary 3.

Proof.

Utilizing (8), (19), and (20), the variance of the log-return at time can be expressed as

We then obtain its partial derivative as

| (49) |

From Theorem 6, we consider the case that , we obtain the following partial derivative:

| (50) | ||||

By applying the property of the Laguerre function (see Mirevski and Boyadjiev [20]), we get

| (51) |

where . Then the derivative of with respect to can be found as

| (52) |

The result shown in (47), is simplified by substituting (52) into (51) and (50). Under the condition that , by Theorem 7, it is easy to get that

which implies (48). ∎

6 Pricing volatility and variance options

As indicated in the put-call parity relations described by Hull in [12], this section presents only an analytical formula for pricing volatility and variance options on calls.

A payoff for a volatility call buyer at expiration time on with a -strike can be written as

| (54) |

and a payoff for a variance call buyer at expiration time on with a -strike can be written as

| (55) |

for where is the realized variance given in (3).

Under the risk-neutral martingale measure with respect to filtration , we focus on calculating the conditional expectations of both call option yields given in (54) and (55) above. In particular, volatility and variance calls can be expressed as

| (56) |

where is a strike volatility call and

| (57) |

where is a strike variance call and is a time-varying risk-free interest rate, respectively. The challenge of this part is that we need to compute both expectations on the RHS of calls (56) and (57), given as follows:

| (58) |

and

| (59) |

respectively, where is the PDF given in (14) from Theorem 1. To obtain the RHS of (58), we apply a Jacobian transformation, which gives the relation .

As the same problem with Section 3, to avoid the complication of numerical integration for the improper integral in (59) and (58), both integrals can be expressed as an infinite summation series through a generalized Laguerre expansion derived by Dufresne [10] in Theorem 2.4. The conditional expectations can then be simplified as

| (60) |

for where and are real numbers satisfying . The coefficient on the RHS of (60) is defined in terms of a finite summation series of the conditional moment of order for , as follows:

| (61) |

for , where where can be specified based on call options’ type. By setting , we obtain the coefficient for the volatility call, and for the variance call, we set .

In the following subsection, an analytical formula for pricing volatility and variance options is presented in two cases by setting the variance of the log-return: one with time-varying variances and the other with a constant variance.

6.1 Pricing formulas for volatility and variance options: Time-varying log-return volatility

In this subsection, the variances of log-returns are assumed to change over time, similar to the setup introduced in Subsection 5.2. Then, is considered as derived in (12). Its conditional moment can be computed by using Theorem 2 to evaluate the RHS of (61) and complete the coefficient .

6.1.1 Volatility call option prices:

By using the PDF (14), the following theorem provides a closed-form formula for pricing a volatility call option under time-varying log-return volatility.

Theorem 10.

6.1.2 Variance call option prices:

The following theorem is a closed-form formula for pricing a variance call option under time-varying log-return volatility.

Theorem 11.

6.2 Pricing formulas for volatility and variance options: Constant log-return volatility

The interesting results of this subsection are other explicit solutions of volatility and variance call options, obtained by assuming that the variance of log-returns remains the same. Specifically, we set , following the approach introduced in Subsection 5.2. Under this assumption, the realized variance is expressed as a linear combination of independent noncentral chi-square random variables, and its conditional moment is derived below.

Since defined in (37), its conditional moment order , for , is obtained from Stuart et al. [30] in explicit form as

| (64) |

where degrees of freedom and noncentrality parameter are given in (38) and (39), respectively. Hence, a conditional moment of order , for , is defined as

| (65) |

For , is distributed according to the central chi-square distribution with degrees of freedom . By using a property of the generalized hypergeometric function (21), it is clear that a conditional moment of order for , can be simplified as

| (66) |

6.2.1 Volatility call option prices:

Since can be represented in terms of , the following theorem provides a closed-form formula for pricing a call volatility option under constant log-return volatility by applying (64).

Theorem 12.

Proof.

By using (56), we obtain its conditional expectation on the RHS of (56) by setting and in (60) with coefficients for , defined in (61). To obtain (61), if , , then we calculate the conditional moment of of order by setting for , in (65). On the other hand, for the case that , which implies , we calculate it using (66). We then obtain the result in (67). ∎

6.2.2 Variance call option prices:

The following theorem is a closed-form formula for pricing a variance call option under constant log-return volatility by applying (64).

Theorem 13.

Proof.

6.2.3 Vega of and

To obtain vega of call options presented in Theorems 12 and 13, we focus on its partial derivative on the RHS with respect to . We have that the parameter appears only in , where is an argument in , as defined in Subsection 6.2. For a given for and , we have coefficients for , as defined in (61). Then, the partial derivatives of and can be expressed as an infinite summation series of , which is defined as

| (69) |

In the following theorems, we present for two cases, characterized by the value of .

Theorem 14.

According to (65), if , then the partial derivative of the conditional moment of order for , is defined as

| (70) | ||||

Proof.

Suppose that . Then, there exists such that the partial derivative of the conditional moment of order , given in (65), can be expressed as

| (71) | ||||

From the above equation (71)), firstly, we consider the partial derivative of the hypergeometric function, by using its differentiation formula, see [21, Chapter 13], we have

| (72) | ||||

where . By applying (52), we get . Secondly, we consider the partial derivative of the second term on the RHS of (71), we have

| (73) |

where

| (74) |

where is derived in (52), and

| (75) |

where is derived in (49). Thus, the result (70) can be simplified by substituting (74) and ((75)) into (73) which (72) and (73) are substituted into (71). ∎

Theorem 15.

According to (65), if , then the partial derivative of the conditional moment of order for is defined as

| (76) |

Proof.

According to vega defined in the third-level Section 5.2.3, the derivative instruments are considered as volatility and variance call options. In the following corollaries, exact formulas for vega of volatility and variance call options, and , are derived by using Theorems 12 and 13, respectively.

Corollary 5.

Proof.

Due to Theorem 12, the partial derivative of with respect to can be illustrated as an infinite summation series of coefficients , , as defined in (69). For a given in (69), if , we compute using Theorem 14. On the other hand, if , we compute it using Theorem 15. Finally, we obtain a result in (77) by setting for . ∎

Corollary 6.

7 Numerical results and discussion

As demonstrated in Section 4, the theoretical frameworks developed in this paper yield new explicit formulas for computing the PDF of , as defined in equation (3), along with its conditional moments. This includes an analytical formula for pricing volatility and variance swaps and options under Schwartz one-factor model, as derived in Section 5 and 6 respectively. In practice, we automatically question whether these newly derived explicit formulas are accurate and efficient, especially considering that an infinite sum has to be truncated. To ensure that there are no algebraic errors in the derivation process, we thoroughly examine the accuracy of our explicit formulas. Additionally, to demonstrate the efficiency of our explicit formulas compared to MC simulations, we conduct a series of numerical examples coded in MATHEMATICA 13 and MATLAB R2024b, performed on a computer notebook with the following specifications: Processor: 2 GHz Quad-Core Intel Core i5, Memory: 16 GB 3733 MHz LPDDR4X, Operating system: macOS 14.2.1 (23C71).

7.1 Accuracy of the PDF of realized variance

To show the accuracy for our explicit formula of the PDF of , denoted by , as defined in (14), we choose and then . We set to hold for all our numerical experiments.

Example 1.

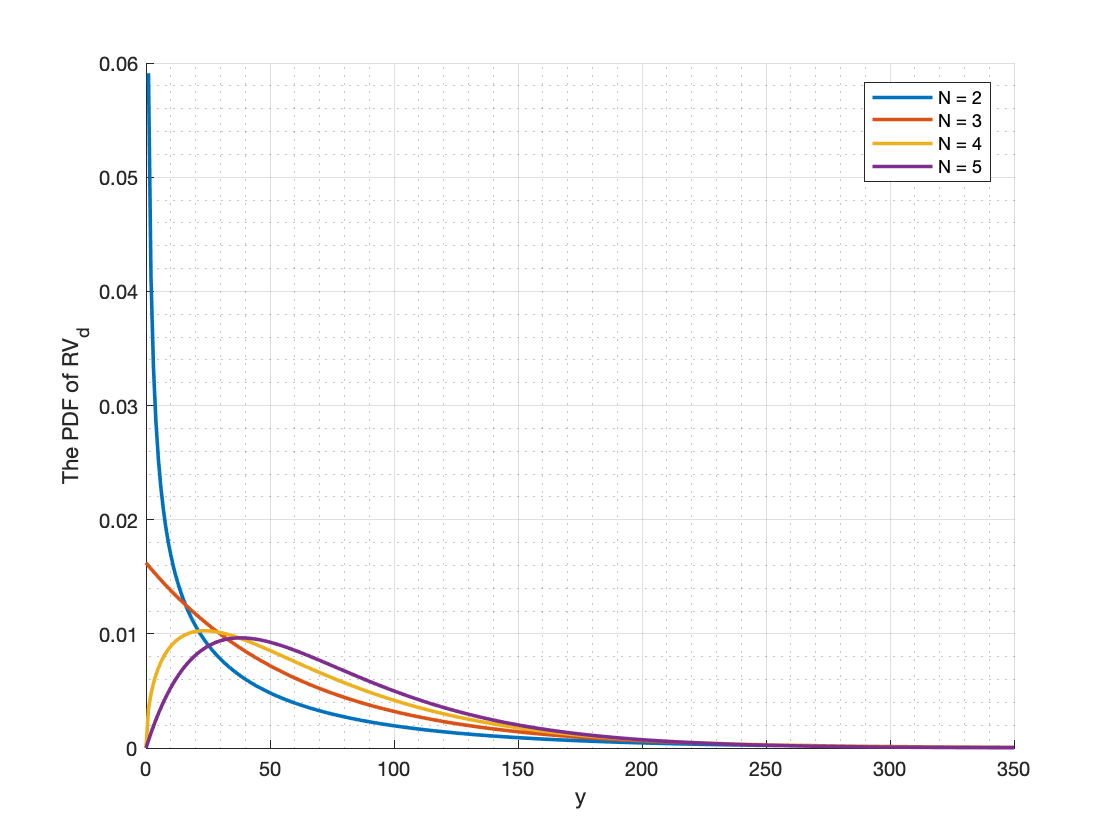

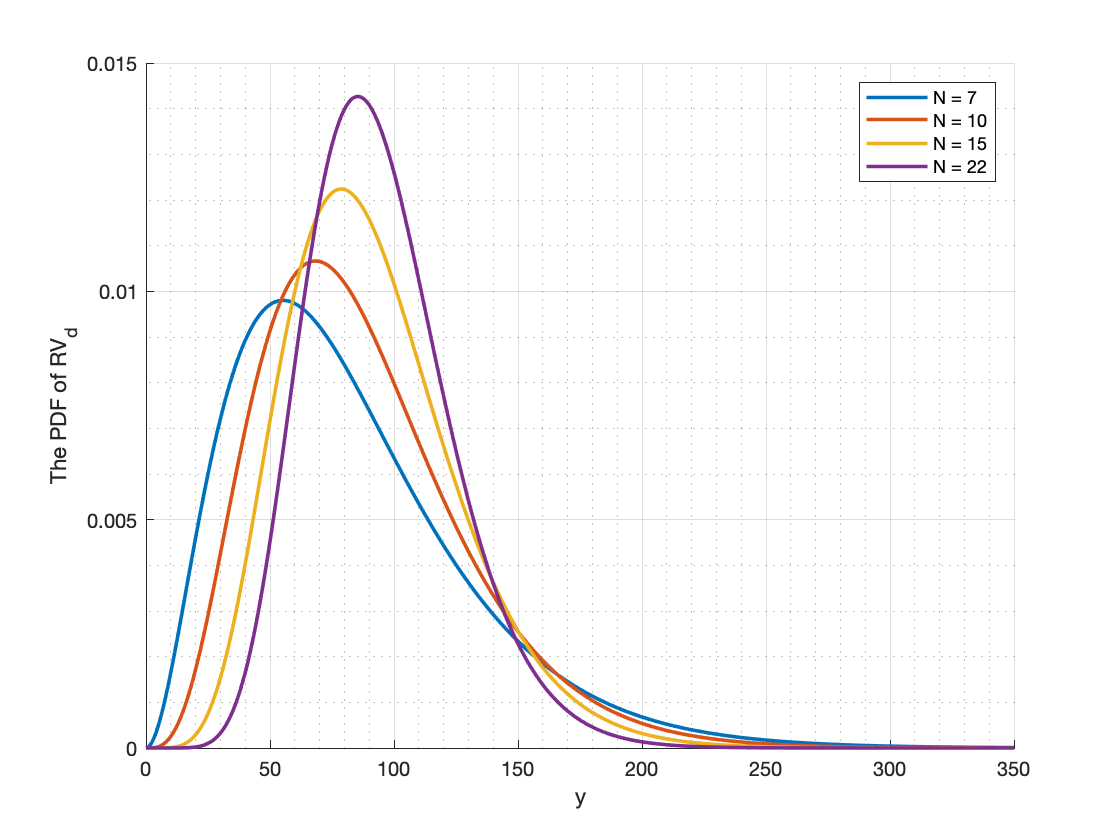

In this example, we illustrate the shapes of our explicit formula for the PDFs of by plotting , which are varied by the number of observations .

By setting , the shapes of the PDFs of differ across ten observation cases: . Let and for . We assume that the parameters of the SDE in (2) are given by the following: and , and is then computed using (2). The parameters and are then computed using (7), (8), (10) and (11), respectively. The value of is obtained from (13), which implies the value of . By using these values, the coefficients can be computed via the recurrence relations given in (16)–(17). We then obtain the various shapes of the PDFs of as shown in the following Figure 1a–1b.

Example 2.

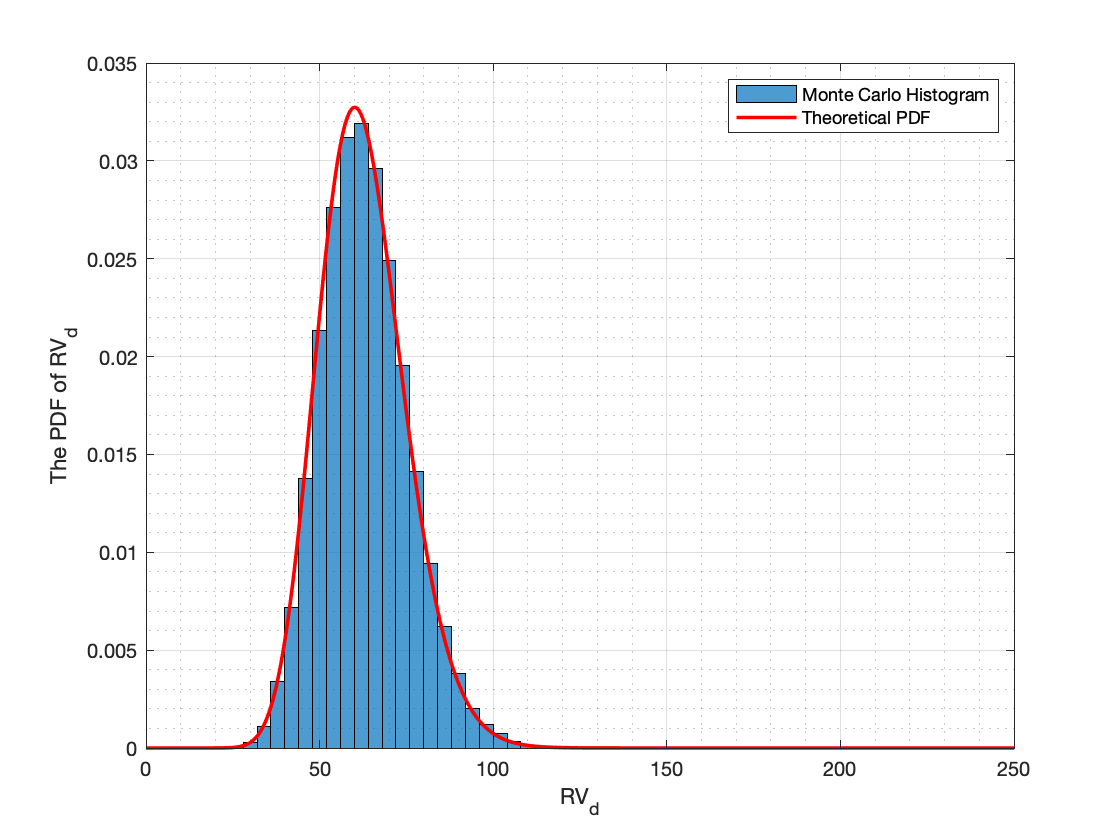

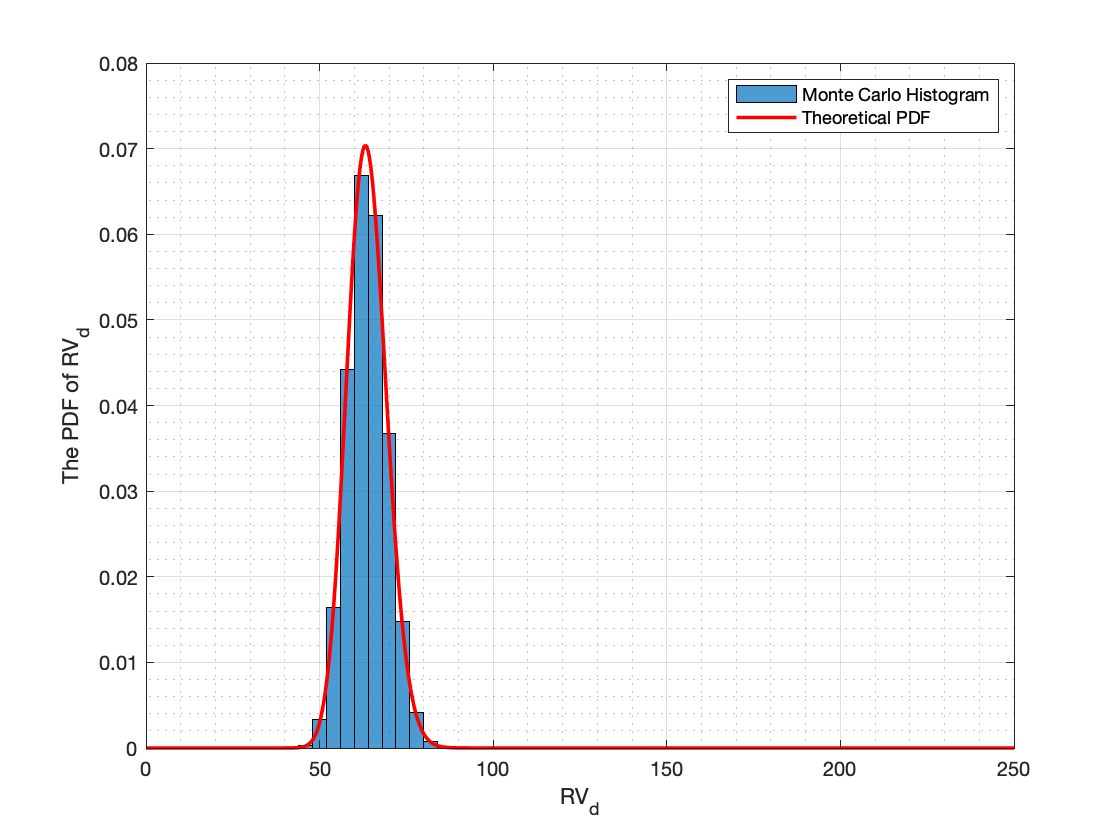

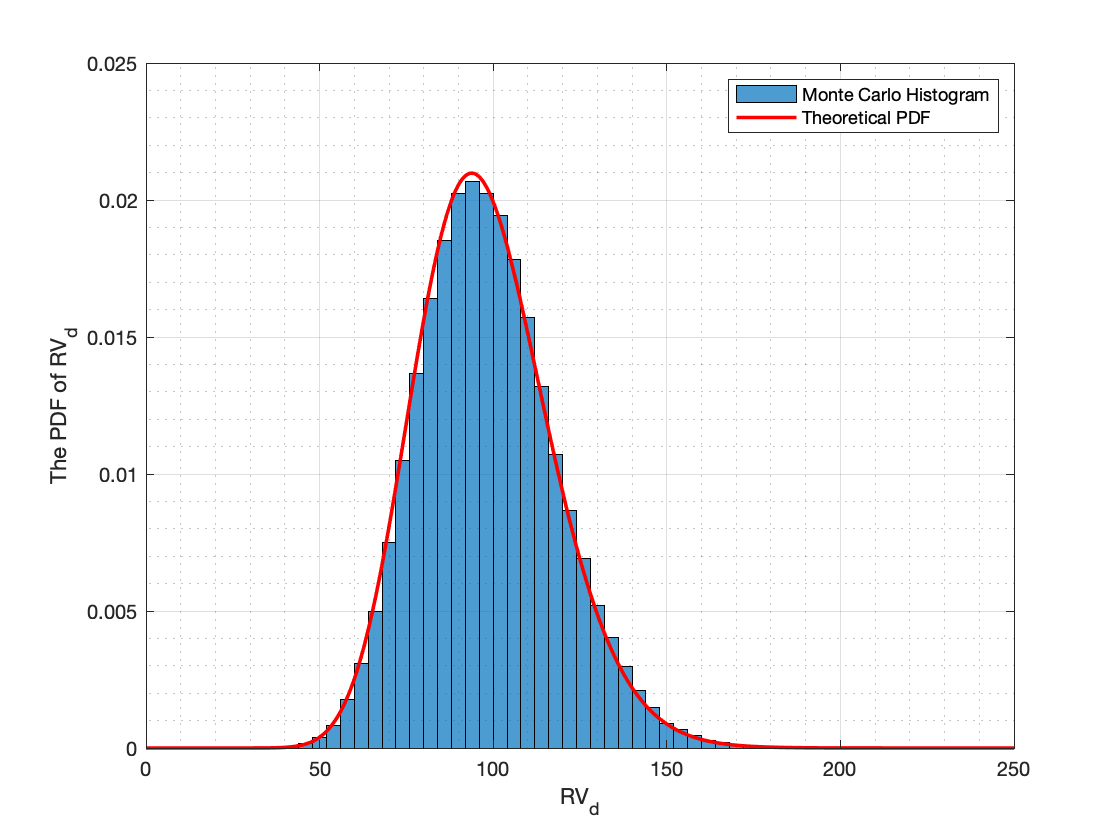

To demonstrate the accuracy and efficiency of the Laguerre expansions for the PDFs of as defined in (14), we compare the analytical expression with the approximate PDFs of obtained from MC simulations. In this example, the approximate PDFs are constructed from sample paths generated by simulating the SDE (2). To ensure high accuracy in the MC-based approximation, we set .

To compare the analytical and approximate PDFs of , we set all parameters to the same values as in Example 1, except for the price volatility , which is set to , and , and the number of observations , which is set to , and . The results are presented in the following figure.

It is clearly observed that the PDFs of obtained from the Laguerre expansions (14) are consistent with those corresponding histograms obtained from MC simulations for all and , as shown in Figure 2a–2d.

Example 3.

By setting all parameters to the same values as in Example 1, except for and varying which are set to , , , , , and , we evaluate the accuracy and efficiency of . Specifically, five sequences of truncation errors are computed for three different values of the degree of mean reversion , i.e. , and , using equation (29), as summarized in Table 1. By choosing , we obtain

for all values of and , indicating that yields sufficiently accurate results. Therefore, we adopt in our subsequent experiments.

| 0.5 | 0 | 5.0621E-03 | 4.0908E-03 | 3.3784E-03 | 2.8286E-03 | 2.3877E-03 | 2.0238E-03 |

|---|---|---|---|---|---|---|---|

| 1 | 2.4812E-06 | 1.3472E-06 | 7.8533E-07 | 4.7996E-07 | 3.0264E-07 | 1.9458E-07 | |

| 2 | 2.3443E-09 | 8.5308E-10 | 3.4989E-10 | 1.5546E-10 | 7.2847E-11 | 3.5296E-11 | |

| 3 | 2.6654E-12 | 6.4748E-13 | 1.8563E-13 | 6.0396E-14 | 1.9540E-14 | 7.1054E-15 | |

| 1.5 | 0 | 2.2769E-02 | 1.8416E-02 | 1.5221E-02 | 1.2749E-02 | 1.0760E-02 | 9.1092E-03 |

| 1 | 5.0288E-05 | 2.7367E-05 | 1.5987E-05 | 9.7862E-06 | 6.1741E-06 | 3.9644E-06 | |

| 2 | 2.1434E-07 | 7.8326E-08 | 3.2261E-08 | 1.4386E-08 | 6.7571E-09 | 3.2735E-09 | |

| 3 | 1.1008E-09 | 2.6957E-10 | 7.8065E-11 | 2.5270E-11 | 8.7965E-12 | 3.1957E-12 | |

| 3.0 | 0 | 4.8567E-02 | 3.9763E-02 | 3.3365E-02 | 2.8470E-02 | 2.4577E-02 | 2.1387E-02 |

| 1 | 2.2947E-04 | 1.2806E-04 | 7.7190E-05 | 4.9107E-05 | 3.2476E-05 | 2.2088E-05 | |

| 2 | 2.0955E-06 | 7.9627E-07 | 3.4435E-07 | 1.6308E-07 | 8.2467E-08 | 4.3744E-08 | |

| 3 | 2.3101E-08 | 5.9702E-09 | 1.8497E-09 | 6.5101E-10 | 2.5122E-10 | 1.0367E-10 |

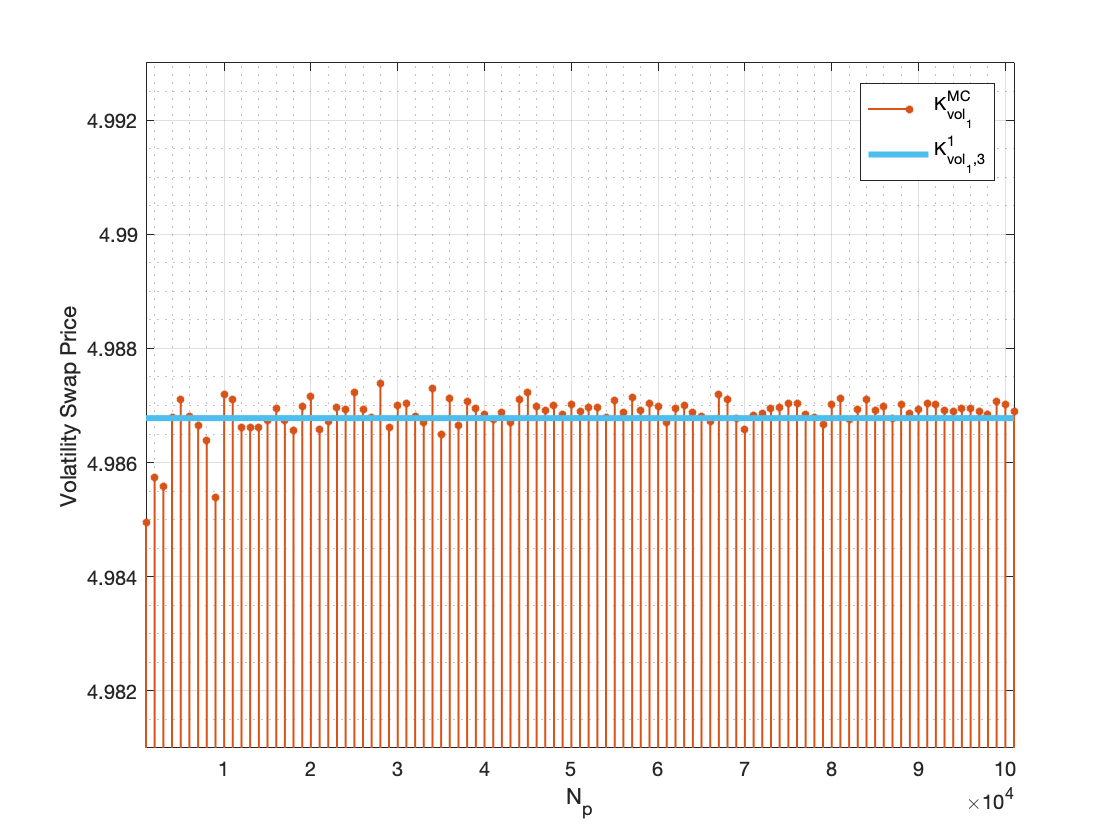

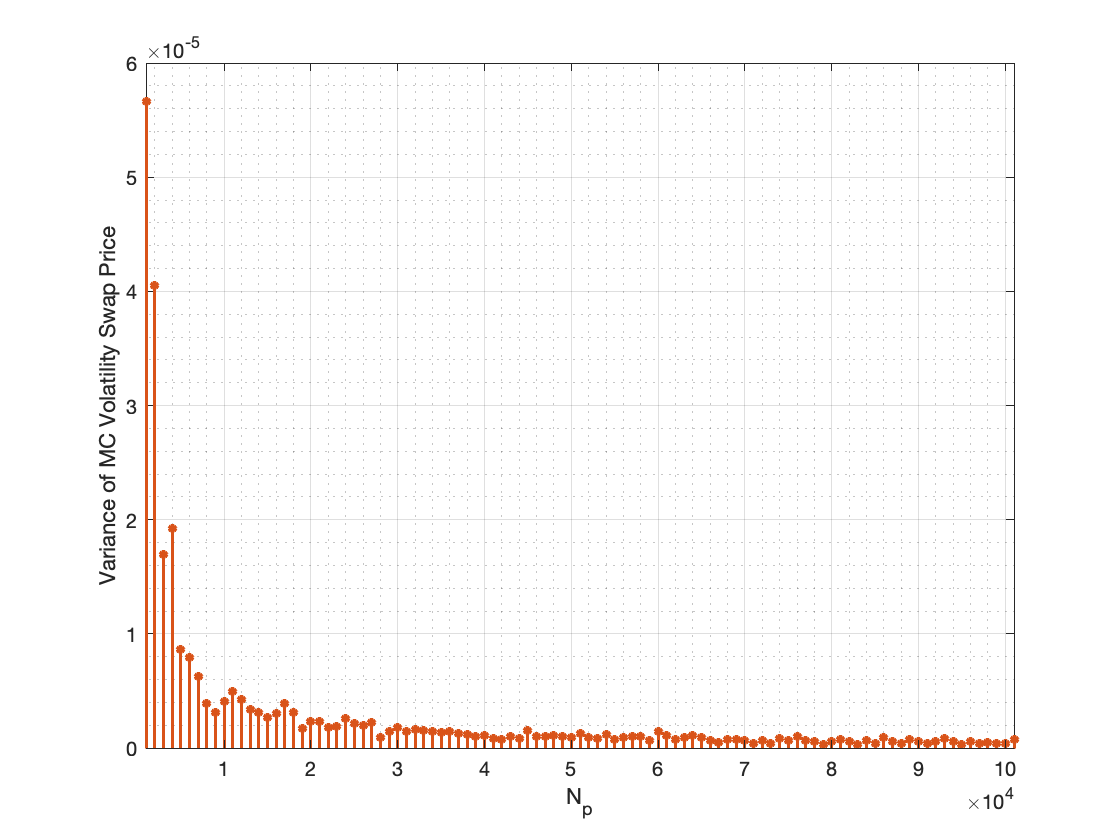

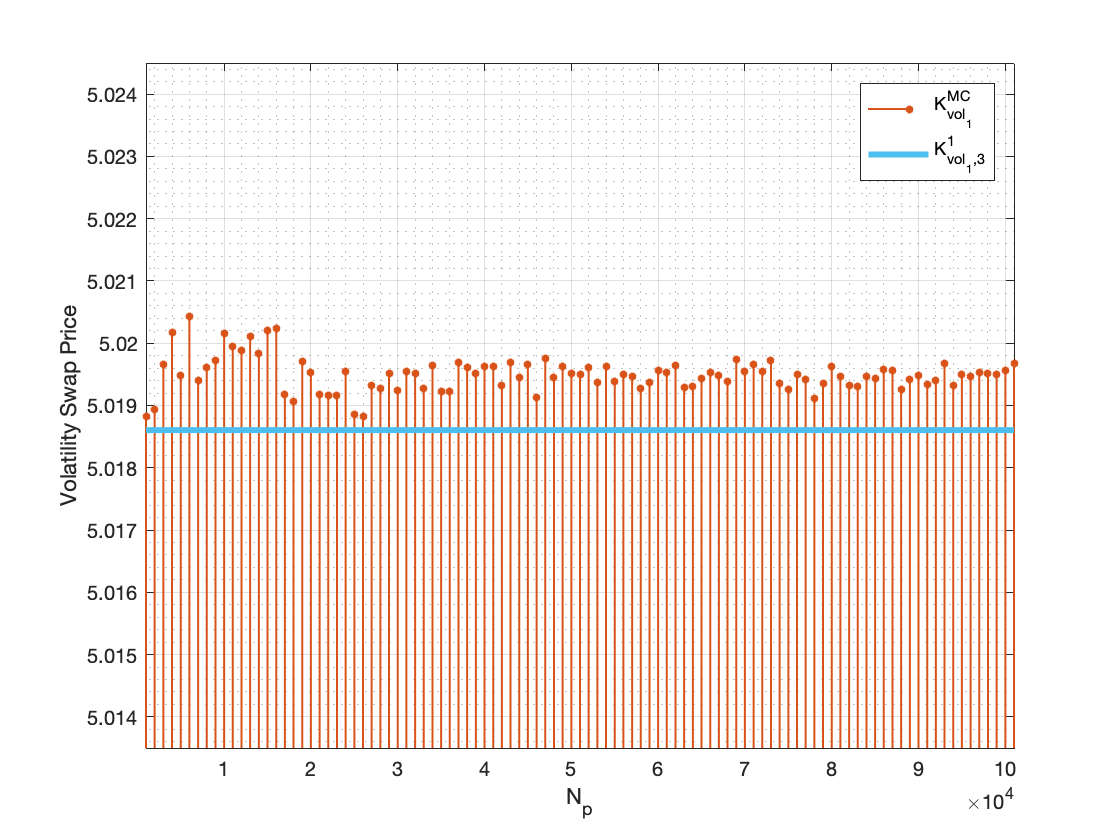

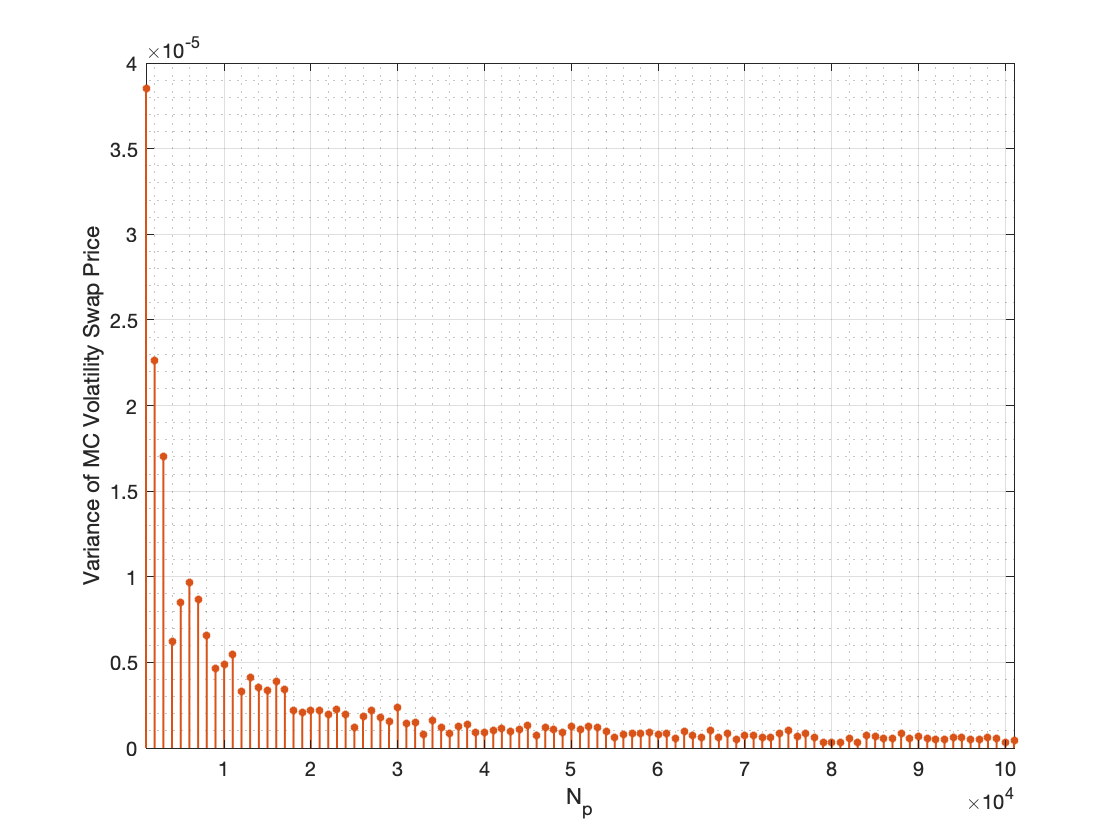

By setting , we plot the convergence of MC volatility swap prices to for , . Three sequences of MC volatility swap prices, with varying from to , are plotted against for each value of , as shown in Figures 3a, 3c, and 3e, respectively. Additionally, we plot the corresponding sequences of variances of the MC volatility swap prices for , , in Figures 3b, 3d, and 3f, respectively.

As shown in Figures 3a–3b, the MC volatility swap prices converge to , and the variances of the MC volatility swap prices approach zero, confirming that the MC estimates are very close to the true value of . Similar convergence behavior is observed for and , as illustrated in Figures 3c–3d and Figures 3e–3f, respectively. Moreover, as shown in Figures 3a, 3c, and 3e, it can be observed that increasing the value of results in slower convergence of the MC simulation results toward the analytical values.

7.2 Effects on fair strike prices of volatility and variance swaps

Example 4.

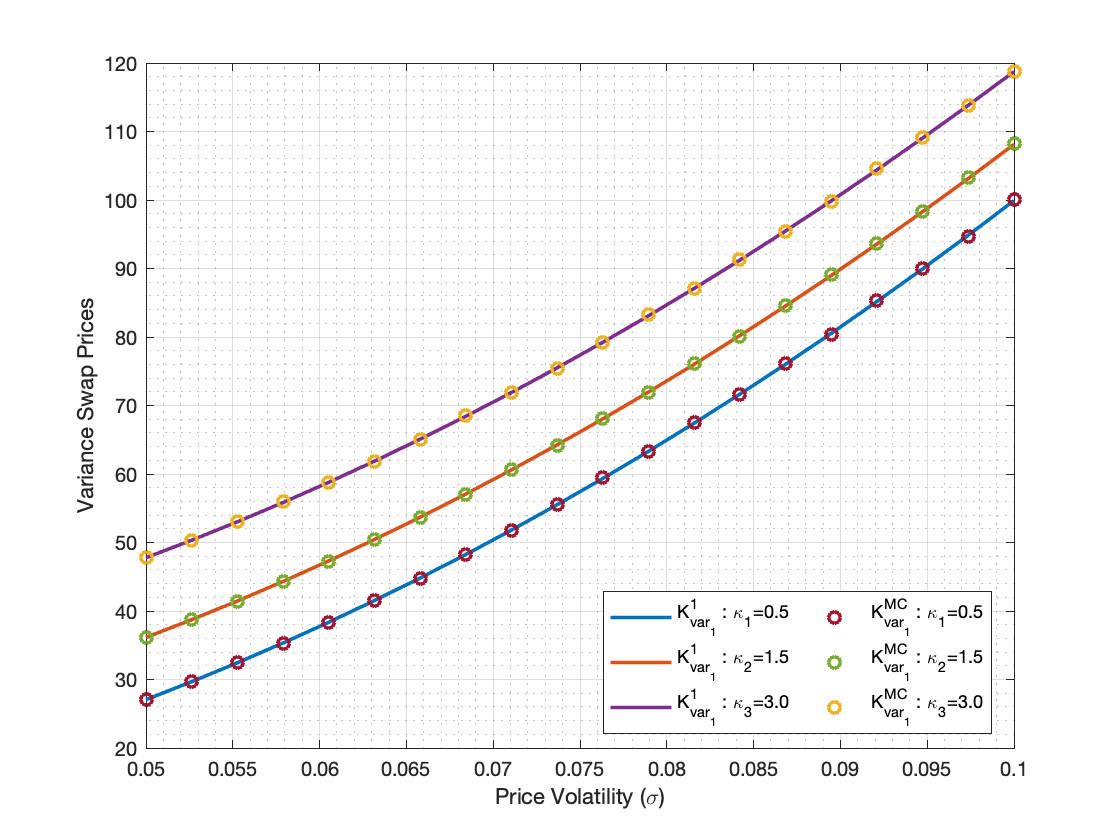

Let and for . To measure the effects of the price volatility on fair strike prices of volatility and variance swaps changing in the closed interval of time , we set and . We then obtain a variation of under , for while is varied over the interval . With this parameter setting, we let and then we plot the volatility swap obtained from (32) against those obtained from MC simulations with sample paths denoted by . Similarly, the variance swap , obtained from (34), is compared with the MC simulation results using the same number of paths.

The numerical results clearly demonstrate that the closed-form pricing formulas (34) and (32) yield values that perfectly match the results from MC simulations. Moreover, Figure 4a shows that an increase in price volatility results in the fair strike prices of volatility swaps increasing for each all . For the fair strike prices of variance swaps, similar results are shown in Figure 4b.

Example 5.

To study the effects of the number of trading days on fair strike prices of volatility and variance swaps, all parameters are set to be the same values as used in Example 4, except that we fix and consider three values of price volatility , and . The number of observations is varied from to . We compare the results by plotting against and against as shown in the following figure.

Figure 5a illustrates that as the number of trading days increases, the fair strike prices of the volatility swap obtained from our closed-form pricing formula (32) are consistent and converge to the results obtained from MC simulations for all for . A similar convergence pattern is observed for the variance swap prices, as shown in Figure 5b, where the prices are computed by (34).

8 Conclusion

In this paper, we first derived the distribution of the realized variance of log-returns with time-varying volatility for pricing volatility swaps under discrete-time observations, assuming the underlying asset follows the Schwartz one-factor model. We demonstrated that the realized variance is in the class of generalized noncentral chi-square distributions, as introduced by Koutras [17] in 1986, and can be expressed as a linear combination of independent noncentral chi-square random variables with weighted parameters. Based on this result, we derived the first analytical pricing formulas for volatility and variance swaps, as well as for volatility and variance options, under both time-varying and constant volatility cases. To support practical implementation, we provided an error analysis and proposed simple closed-form approximations for pricing volatility derivatives under the Schwartz model. Numerical experiments were conducted, clearly demonstrating the accuracy and computational efficiency of the proposed formulas and their consistency with Monte Carlo simulations. Finally, we analyzed the effects of price volatility and the number of trading days on the fair strike prices of volatility and variance swaps. The results show that increasing price volatility leads to higher fair strike prices, while increasing the number of trading days causes the fair strike prices to converge to their true values. Overall, the newly derived analytical formulas significantly enhance computational efficiency, particularly for pricing volatility derivatives with square-root payoffs. This contributes a practical and effective tool for both researchers and practitioners in the financial derivatives market.

Acknowledgement

We would like to express our sincere gratitude to the Development and Promotion of Science and Technology Talents Project (DPST) for supporting this research. We also thank the anonymous reviewers for their valuable comments and recommendations, which have helped to improve the quality and clarity of this work. Any remaining errors are solely our own.

References

- [1] Blanco, Carlos and Soronow, David. Mean reverting processes-energy price processes used for derivatives pricing & risk management. Commodities now , 5(2):68–72, 2001.

- [2] Brockhaus, Oliver and Long, Douglas. Volatility swaps made simple. Risk-London-Risk Magazine Limited , 13(1):92–95, 2000.

- [3] Castaño-Martínez, Antonia and López-Blázquez, Fernando. Distribution of a sum of weighted noncentral chi-square variables. Test, 14(2):397–415, 2005.

- [4] Chan, Leunglung and Platen, Eckhard. Pricing volatility derivatives under the modified constant elasticity of variance model. Operations Research Letters, 43(4):419–422, 2015.

- [5] Chumpong, Kittisak and Mekchay, Khamron and Thamrongrat, Nopporn. Analytical formulas for pricing discretely-sampled skewness and kurtosis swaps based on Schwartz’s one-factor model. Songklanakarin J. Sci. Technol, 43(2):1–6, 2021.

- [6] Chunhawiksit, Chonnawat and Rujivan, Sanae Pricing discretely-sampled variance swaps on commodities. Thai Journal of Mathematics, 14(3):711–724, 2016.

- [7] Davis, AW. A differential equation approach to linear combinations of independent chi-squares. Journal of the American Statistical Association, 72(357):212–214, 1977.

- [8] Demeterfi, Kresimir, Derman, Emanuel, and Kamal, Michael. A guide to volatility and variance swaps. Journal of Derivatives, 6(4):9–32, 1999.

- [9] Duangpan, Ampol, Boonklurb, Ratinan, Chumpong, Kittisak, and Sutthimat, Phiraphat. Analytical formulas for conditional mixed moments of generalized stochastic correlation process. Symmetry, 14(5):897, 2022.

- [10] Dufresne, Daniel. Laguerre series for Asian and other options. Mathematical Finance, 10(4):407–428, 2000.

- [11] García Franco, José Carlos. Maximum likelihood estimation of mean reverting processes. Technical Report, Citeseer, 2023. https://www2.stat.duke.edu/˜scs/Projects/StructuralPhylogeny/OUprocess.pdf

- [12] Hull, John C. and Basu, Sankarshan. Options, Futures, and Other Derivatives. Pearson Education India, 2016.

- [13] Javaheri, Alireza, Wilmott, Paul, and Haug, Espen G. GARCH and volatility swaps. Quantitative Finance, 4(5):589–595, 2004.

- [14] Johnson, Norman L., Kotz, Samuel, and Balakrishnan, Narayanaswamy. Continuous Univariate Distributions, Volume 2. John Wiley & Sons, 1995.

- [15] Jouini, Elyès, Cvitanić, Jakša, and Musiela, Marek. Option Pricing, Interest Rates and Risk Management. Cambridge University Press, 2001.

- [16] Kotz, Samuel, Johnson, Norman L., and Boyd, D. W. Series representations of distributions of quadratic forms in normal variables II. Non-central case. The Annals of Mathematical Statistics, 38(3):838–848, 1967.

- [17] Koutras, Markos. On the generalized noncentral chi-squared distribution induced by an elliptical gamma law. Biometrika, 73(2):528–532, 1986.

- [18] Ma, JunMei and Xu, Chenglong. An efficient control variate method for pricing variance derivatives. Journal of Computational and Applied Mathematics, 235(1):108–119, 2010.

- [19] Mehta, Nina. Equity vol swaps grow up. Derivatives Strategy Magazine, 1999.

- [20] Mirevski, S. P. and Boyadjiev, L. On some fractional generalizations of the Laguerre polynomials and the Kummer function. Computers & Mathematics with Applications, 59(3):1271–1277, 2010.

- [21] Olver, Frank W. J. NIST Handbook of Mathematical Functions Hardback and CD-ROM. Cambridge University Press, 2010.

- [22] Ruben, Harold. Probability content of regions under spherical normal distributions, IV: The distribution of homogeneous and non-homogeneous quadratic functions of normal variables. The Annals of Mathematical Statistics, 33(2):542–570, 1962.

- [23] Rujivan, Sanae and Rakwongwan, Udomsak. Analytically pricing volatility swaps and volatility options with discrete sampling: Nonlinear payoff volatility derivatives. Communications in Nonlinear Science and Numerical Simulation, 100:105849, 2021.

- [24] Rujivan, Sanae and Zhu, Song-Ping. A simplified analytical approach for pricing discretely-sampled variance swaps with stochastic volatility. Applied Mathematics Letters, 25(11):1644–1650, 2012.

- [25] Schwartz, Eduardo S. The stochastic behavior of commodity prices: Implications for valuation and hedging. The Journal of Finance, 52(3):923–973, 1997.

- [26] Shah, B. K. Distribution of definite and of indefinite quadratic forms from a non-central normal distribution. The Annals of Mathematical Statistics, 34(1):186–190, 1963.

- [27] Shah, B. K. and Khatri, C. G. Distribution of a definite quadratic form for non-central normal variates. The Annals of Mathematical Statistics, pages 883–887, 1961.

- [28] Shen, Yang and Siu, Tak Kuen. Pricing variance swaps under a stochastic interest rate and volatility model with regime-switching. Operations Research Letters, 41(2):180–187, 2013.

- [29] Slater, Lucy Joan. Generalized Hypergeometric Functions. Cambridge University Press, UK, 1966.

- [30] Stuart, Alan, Ord, J. Keith, and Arnold, Steven. Kendall’s advanced theory of statistics. vol. 2a: Classical inference and the linear model. Kendall’s Advanced Theory of Statistics. Vol. 2A: Classical Inference and the Linear Model, 1999.

- [31] Sutthimat, Phiraphat and Mekchay, Khamron. Closed-form formulas for conditional moments of inhomogeneous Pearson diffusion processes. Communications in Nonlinear Science and Numerical Simulation, 106:106095, 2022.

- [32] Swishchuk, Anatoliy V. Variance and volatility swaps in energy markets. Available at SSRN 1628178, 2010.

- [33] Théoret, Raymond, Zabré, Lydie, and Rostan, Pierre. Pricing volatility swaps: empirical testing with Canadian data. [Université du Québec à Montréal], Centre de recherche en gestion, 2002.

- [34] Weraprasertsakun, Anurak and Rujivan, Sanae. A closed-form formula for pricing variance swaps on commodities. Vietnam Journal of Mathematics, 45(1-2):255–264, 2017.

- [35] Windcliff, Heath, Forsyth, Peter A., and Vetzal, Kenneth R. Pricing methods and hedging strategies for volatility derivatives. Journal of Banking & Finance, 30(2):409–431, 2006.

- [36] Zheng, Wendong and Kwok, Yue Kuen. Closed form pricing formulas for discretely sampled generalized variance swaps. Mathematical Finance, 24(4):855–881, 2014.

- [37] Zhu, Song-Ping and Lian, Guang-Hua. A closed-form exact solution for pricing variance swaps with stochastic volatility. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 21(2):233–256, 2011.