[feb]organization=Faculty of Economics and Business, Universitas Indonesia, city=Depok, country=Indonesia \affiliation[bi]organization=Bank Indonesia, city=Jakarta, country=Indonesia

Export proceeds repatriation policies: A shield against exchange rate volatility in emerging markets?

Abstract

We examine the impact of mandatory export proceeds repatriation on exchange rate stability in three emerging markets, Iran, Sri Lanka, and Turkey, using the Generalized Synthetic Control framework. By modeling exchange rate stochastic volatility as our outcome of interest and controlling for interest rate differentials, exchange rate regime shifts, and inflation rate gaps, we address both unobserved time‐varying confounders and heterogeneous treatment effects. Our estimates reveal no statistically significant impact of repatriation mandates on exchange‐rate volatility across the three countries. We also find that we cannot reject the possibility of a non-zero impact. These results remain robust to an extensive range of sensitivity analyses, including alternative covariate specifications and placebo tests, thereby confirming their reliability.

keywords:

Export proceeds repatriation policy , Exchange rate volatility , Generalyzed synthetic control , Emerging marketsJEL:

E58 , F31 , G151 Introduction

Exchange rate volatility is a critical concern, especially for emerging economies, where fluctuations in currency values can significantly impact the performance of an economy (Krol, 2014). Greater exchange rate volatility slows productivity and gross domestic product growth (Aghion et al., 2009; Bush and López Noria, 2021). There is also evidence that higher exchange rate volatility affects the unemployment rate of a country (Feldmann, 2011), raises transaction risk related to international trade (Baum and Caglayan, 2010), and reduces consumption and investment (Grier and Grier, 2006). One of the key policy measures employed to stabilize exchange rate movements is the export proceeds repatriation (EPR) policy, which mandates that exporters bring their foreign exchange earnings back into the exporters’ country within a specified period.

We apply the generalized synthetic control (GSC) estimator of (Xu, 2017) to rigorously quantify the effectiveness of mandatory export proceeds repatriation in stabilizing exchange rate volatility. By integrating interactive fixed effects with a synthetic control framework, the GSC flexibly adjusts for both unobserved time‑varying confounders and heterogeneous treatment effects, delivering a credible counterfactual analysis path for each treated country. Because GSCs require single, non‐reversible treatments and sufficiently long pretreatment periods, our analysis focuses on Iran, Sri Lanka, and Turkey, three emerging economies that implemented continuous repatriation rules during our observation period, which is March 2008 to December 2021.

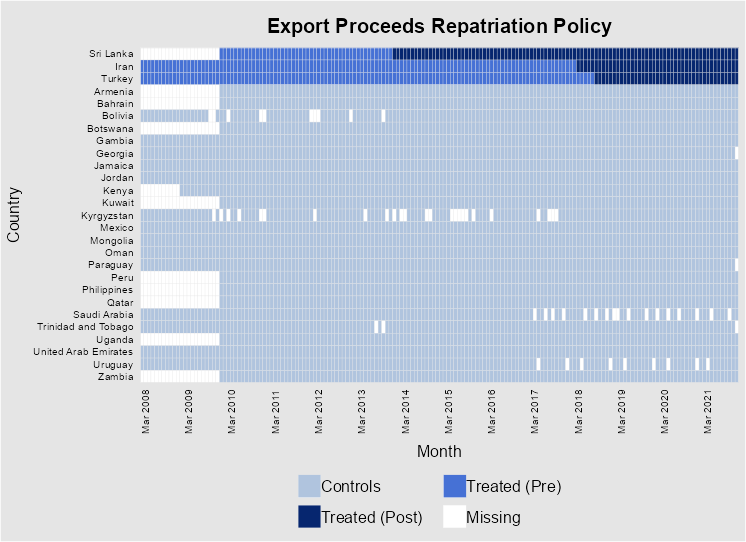

Iran began implementing an EPR policy in April 2018 with no requirement to convert export proceeds into local currency. The repatriation rules differ depending on the amount of funds received by exporters. The difference covers the maximum percentage of export proceeds that may be converted into Iranian rial based on an exporter’s foreign transaction, while the rest should be used for imports. In January 2014, Sri Lanka implemented an EPR policy requiring the conversion of the proceeds into Sri Lankan rupees. However, Sri Lankan exporters are still allowed to retain the proceeds abroad, provided that the fund is not used to buy properties or other capital assets abroad. On the other hand, Turkey has a long history of implementation. Turkey has implemented various iterations of its EPR policy over the years. The policy was initially introduced in the 1980s as part of broader economic liberalization measures aimed at integrating Turkey into global financial markets. However, as the country experienced recurrent currency crises, the policy underwent several modifications. By March 2008, the policy had been retracted, and there was no obligation to repatriate export proceeds. In September 2018, amid heightened exchange rate volatility and increasing external debt pressures, the government reinstated strict repatriation requirements, mandating that at least 80% of export earnings be brought back to Turkey within 180 days.

These regulations were introduced to channel exporters’ foreign-currency earnings back into the domestic market, limit speculative depreciation, and support macroeconomic stability. However, whether they succeed in reducing exchange-rate volatility, remains unclear. The outcomes are confounded by concurrent forces such as geopolitical shocks, COVID-19 pandemic, episodes of global risk aversion, and persistent domestic inflation. Therefore, the specific contribution of EPR rules to currency stability has received little systematic scrutiny. This study addresses that gap; to the best of our knowledge, it is among the first to provide a rigorous, policy-focused evaluation of EPR effects on exchange-rate volatility in an emerging-market setting.

We analyze monthly data for the three adopters and ask whether the EPR mandated dampened volatility or was overshadowed by broader macrofinancial conditions. Our empirical design tests the policy’s impact while explicitly controlling for interest-rate differentials, the prevailing exchange-rate regimes, and inflation gaps. By disentangling these channels, this study clarifies how capital flow regulations interact with domestic and external factors to shape currency dynamics. The findings inform policy debates on capital-flow management, highlighting the circumstances under which EPR rules can, or cannot, enhance exchange-rate stability in emerging economies. These findings could help policy makers formulate better policies regarding EPR that would have a greater impact on exchange rate stability.

The remainder of the paper is organized as follows. Section 2 summarizes the key literature on export proceeds and exchange rate volatility. Section 3 introduces the data and describes our empirical strategy. Section 4 presents the results and the empirical analysis. Section 5 discusses the robustness tests. Finally, Section 6 concludes the paper.

2 Literature Review on Export Proceeds and Exchange Rate Volatility

By 2021, 83 of 156 111Data source from The Annual Report on Exchange Arrangements and Exchange Restrictions by the IMF emerging countries had adopted EPR policies, yet research on export proceeds remains scarce. Early studies emphasized stabilizing export earnings amid commodity price and quantity fluctuations (Wallich, 1961; Powell, 1959; Massell, 1964; Macbean, 1962). Later work examined export proceeds as part of the trade balance (Guillaumont, 1980) and as a factor influencing foreign direct investment (Asiedu and Lien, 2004; Prayoga and Purnomo, 2024). This paper contributes to the limited body of literature by investigating how EPR policies affect exchange rate volatility.

The majority of exchange rate literature on developing economies focuses on how exchange rates influence growth. It also examines how institutional factors, such as international trade and financial openness or exchange rate regimes, shape exchange rate fluctuations. A consistent finding is the negative impact of exchange rate volatility on long-term economic performance (Devereux and Engel, 2002; Choudhri and Hakura, 2006; Grier and Grier, 2006; Lee-Lee and Hui-Boon, 2007; Aghion et al., 2009; Krol, 2014; Feldmann, 2011; Bush and López Noria, 2021; Aysun, 2024; Sukmawati and Ekananda, 2018). In contrast, this study examines EPR policies as drivers of exchange rate volatility.

By design, EPR requirements direct additional export earnings back into the domestic financial system, thereby expanding the supply of foreign exchange (Calvo et al., 1996) regardless of whether those receipts are subsequently converted into local currency. This transmission highlights the relationship between foreign exchange capital flows and exchange rate volatility, which is our outcome of interest. Some research indicates different volatility determinants in developing economies from determinants in developed countries (Grossmann and Orlov, 2014). For example, (Flood and Rose, 1999) argue that macroeconomic factors are less critical in developing economies, whereas (Rafi and Ramachandran, 2018) and (Caporale et al., 2017) emphasize the importance of foreign capital flows. Furthermore, (Gabaix and Maggiori, 2015) develop a theoretical model that also supports the importance of foreign capital flows, influenced by relative levels of interest rates, in determining exchange rate volatility. The model is also disconnected from traditional macroeconomic fundamentals. (Brunnermeier et al., 2008) and (Farhi and Gabaix, 2016) also describe exchange rate dynamics through changes in the interest rate differentials (IRD) that lead to movements in capital flows.

Furthermore, the intensity of exchange rate volatility is a direct consequence of exchange rate regimes (Flood and Rose, 1999; MacDonald, 2007; Sarno and Taylor, 2003) where pegged exchange rate regimes will produce lower exchange rates than floating regimes ((Ghosh et al., 2002), (Levy-Yeyati and Sturzenegger, 2003), inter alia). However, soft-pegged and managed floating regimes are still vulnerable to the volatility of exchange rates. Countries that adopted EPR policies also adopted soft-pegged and managed floating regimes as listed in Table 2.

Inflation differentials vis-à-vis the United States are also important in determining exchange rate volatility via purchasing power parity (PPP). In contrast to most studies that cite the impact of exchange rate volatility on inflation, (Farhi and Gabaix, 2016) develop a theoretical model that proves the influence of inflation on exchange rate volatility during rare disasters. The comovement between inflation and exchange rates is also empirically shown by (ŞEn et al., 2020). Moreover, because PPP prevails over time, a burst of inflation eventually weakens the currency, even though it might initially strengthen; in the classic overshooting model, where the central bank fixes the money-supply growth rate, an inflation surprise is therefore expected to end up pushing the exchange rate down or in words, a depreciation (Clarida and Waldman, 2008). (Ekananda and Suryanto, 2021) show that the effect of global inflation on domestic inflation may differ at different threshold levels, causing the effect of inflation on exchange rate volatility to also vary. In short, inflation (or similarly inflation differential) affects exchange rate volatility. (Clarida et al., 2002) also theoretically show that in a two-country Nash equilibrium under central bank discretion, inflation does affect exchange rate volatility. Similar results from empirical studies are also given by (Goldberg and Klein, 2005) and (Faust et al., 2007).

Furthermore, (Orlov, 2006) and (Orlov, 2009) show that studying volatility via a conventional time-domain approach (i.e., variance or standard deviation) may lead to spurious results if the effect on various components of volatility is not uniform. Among others, (Daníelsson, 1998), (Iseringhausen, 2020), and (Kim et al., 1998) show that given the choice of statistic volatility models and generalized autoregressive conditional heteroskedasticity (GARCH) models, stochastic volatility models are preferable, given their efficiency and better forecasting power. These properties are essential for both regulators and market players.

Prior evidence suggests that capital flow restrictions seldom dampen exchange rate fluctuations. (Glick and Hutchinson, 2005) and (Edwards and Rigobon, 2009) find little support for a volatility‑reducing effect of capital controls, while (Panggabean et al., 2024) report that Indonesia’s repatriated export proceeds leave short‑ and medium‑term exchange rate volatility unchanged. Guided by these findings, we propose the following hypothesis for the present study:

: Export‑proceeds repatriation (EPR) mandates in Iran, Sri Lanka, and Turkey have no measurable effect on monthly exchange‑rate volatility. The empirical analysis that follows tests this null against the alternative that EPR policies either increase or decrease volatility in the treated economies.

3 Data and empirical methodology

3.1 Data

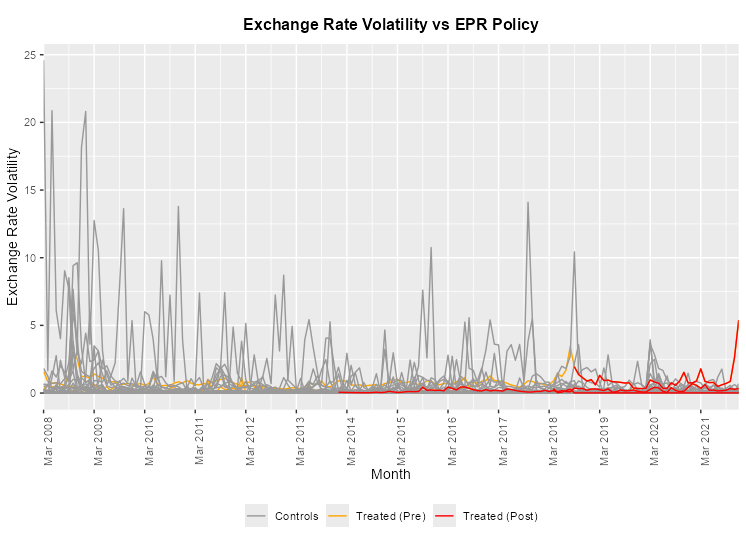

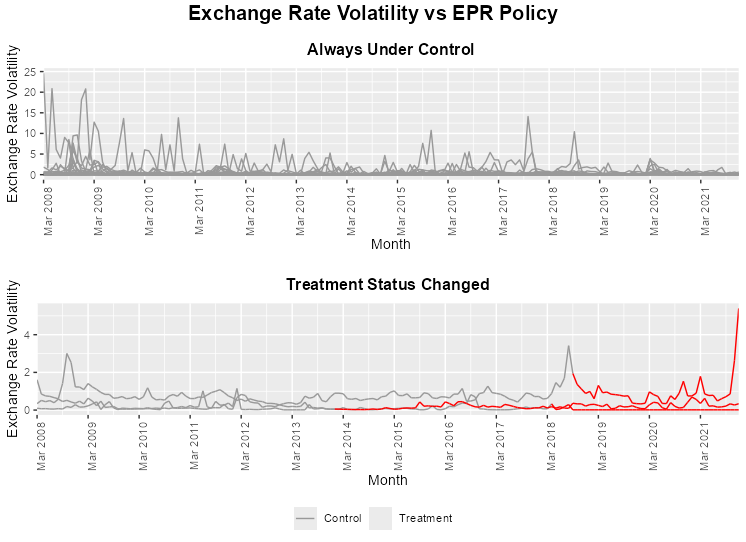

We retrieve data regarding the timing of the implementation of EPR policies in Iran, Sri Lanka, and Turkey from The Annual Report on Exchange Rate Arrangements and Exchange Restrictions (AREAER) database of the International Monetary Fund (IMF). Iran, Sri Lanka, and Turkey present an ideal case for analysis, given their consistent implementation of the policy without reversals since March 2008 to December 2021 and their adherence to a non-hard-pegged exchange rate regime as classified by the IMF during our observation period. We follow the general guidance proposed by (Abadie et al., 2015) to choose our treated and control units. First, the treated units should not experience large idiosyncratic shocks to exchange rate volatility (outcome of interest) as a result of the reform implementation of EPR policies (our treatment). We observe the absence of exchange rate volatility shocks caused by EPR policies implementation in Figure 1 and the second plot in Figure 2. Second, the analysis requires a large number of pretreatment and posttreatment observations. Table 1 summarizes the number of observations of the treated units.

Note: Exchange rate volatility is calculated by implementing the stochastic volatility model

Note: Exchange rate volatility is calculated by implementing the stochastic volatility model

| Treated Country | Number of Pretreatment Observations | Number of Posttreatment Observations |

| Iran | 121 | 45 |

| Sri Lanka | 70 | 96 |

| Turkey | 126 | 40 |

Third, the control units must have never received treatment, which, in our case, are the countries that never implemented EPR policies during our observation period. Finally, the control units should be structurally similar to the treated units. It is important to avoid bias resulting from comparing countries with different characteristics. Hence, we select only countries categorized as emerging countries by the IMF, which is consistent with our choice of data source for de facto exchange rate regimes 222(Anderson et al., 2009) gives the complete list and definition for de facto exchange rate regimes and countries implementing EPR policies. The countries that comply with the third and fourth requirements are twenty-four developing countries that never applied the export proceeds repatriation policy from March 2008 to December 2021. The countries have been additionally filtered by de facto exchange rate regimes, as defined by the IMF (Anderson et al., 2009), which excludes those countries that apply hard-pegged exchange rate regimes. We avoid countries that adopt hard-pegged exchange rate regimes since it is not relevant to analyze exchange rate volatility for such countries (Flood and Rose, 1999; MacDonald, 2007; Sarno and Taylor, 2003). The list of treated and control units, along with their exchange rate regimes in alphabetical order, is given in Table 2.

| No. | Country | Exchange Rate Regimes1 | Status |

|---|---|---|---|

| 1 | Armenia | 1, 2 | Control |

| 2 | Bahrain | 1 | Control |

| 3 | Bolivia | 1 | Control |

| 4 | Botswana | 1 | Control |

| 5 | Gambia | 0, 1, 2 | Control |

| 6 | Georgia | 0, 1, 2 | Control |

| 7 | Iran | 0, 1 | Treated |

| 8 | Jamaica | 1, 2 | Control |

| 9 | Jordan | 1 | Control |

| 10 | Kenya | 0, 1, 2 | Control |

| 11 | Kuwait | 0, 1 | Control |

| 12 | Kyrgyzstan | 0, 1, 2 | Control |

| 13 | Mexico | 2 | Control |

| 14 | Mongolia | 0, 1, 2 | Control |

| 15 | Oman | 1 | Control |

| 16 | Paraguay | 0, 1, 2 | Control |

| 17 | Peru | 1, 2 | Control |

| 18 | Philippines | 1, 2 | Control |

| 19 | Qatar | 1 | Control |

| 20 | Saudi Arabia | 1 | Control |

| 21 | Sri Lanka | 1, 2 | Treated |

| 22 | Trinidad and Tobago | 1 | Control |

| 23 | Turkey | 2 | Treated |

| 24 | Uganda | 2 | Control |

| 25 | United Arab Emirates | 1 | Control |

| 26 | Uruguay | 2 | Control |

| 27 | Zambia | 1, 2 | Control |

11=soft-pegged (2009 de facto system: conventional pegged arrangement, stabilized arrangement, pegged exchange rate within horizontal bands, crawling peg, crawl-like arrangement); 2=floating (2009 de facto system: floating, free floating); 0=other managed arrangements

To examine the impact of EPR policies on exchange rate volatility, this paper utilizes the GSC with four main covariates, namely interest rate differential (IRD), inflation differential, and exchange rate regime in the form of a categorical covariate. Since GSC does not allow treatment reversal, we began our monthly observation in March 2008 until December 2021, purposefully avoiding treatment reversal for Turkey while allowing sufficient time for a pretreatment period.

Exchange rate volatility is calculated via the stochastic volatility model following (Kim et al., 1998) with daily exchange rates retrieved from Refinitiv Eikon from 1 March 2008 to 31 December 2021. The daily exchange rate volatility is then converted into monthly volatility by taking the square root of the average of the sum of the squared daily stochastic volatility for each month. Interest rate differentials are calculated as the difference between the effective federal funds rate (EFFR) 333https://fred.stlouisfed.org/series/EFFR and a country’s short-term interest rates, both compounded into monthly rates. The interest rates are retrieved from several sources, depending on data availability, with preferences given to interbank short-term rates, as listed in Table 11 in the Appendix. Moreover, monthly inflation data are retrieved from the IMF database.

3.2 Methodology

3.2.1 Stochastic Volatility

The exchange rate volatility is estimated following the stochastic volatility model parameters. The model for regularly spaced data is

| (1) |

where is the mean-corrected exchange rate return with and .

The conditional variance of given is , implying that the conditional variance is time-varying. We assume that , the log-volatility of the exchange rate return at time , follows

| (2) |

where can be thought as the persistence in the volatility, is the volatility of the log-volatility, and and . For identifiability reasons, following (Kim et al., 1998), will be set to one when we estimate the model. Finally, and are uncorrelated standard normal noise shocks.

Equation 1 can be rewritten as

| (3) |

Thus, the estimation of stochastic volatility models requires the estimation of the parameters

| (4) |

We use an auxiliary mixture sampler following (Kim et al., 1998) to estimate them.

Since volatility is a latent variable, we need to compute for each value of by particle filtering. We employ the particle filtering algorithm following (Kim et al., 1998) and (Pitt and Shephard, 1999). We modify MATLAB codes from (Chan et al., 2019) using iterations and discard the first 1,000 iterations for convergence.

3.2.2 Generalized Synthetic Control

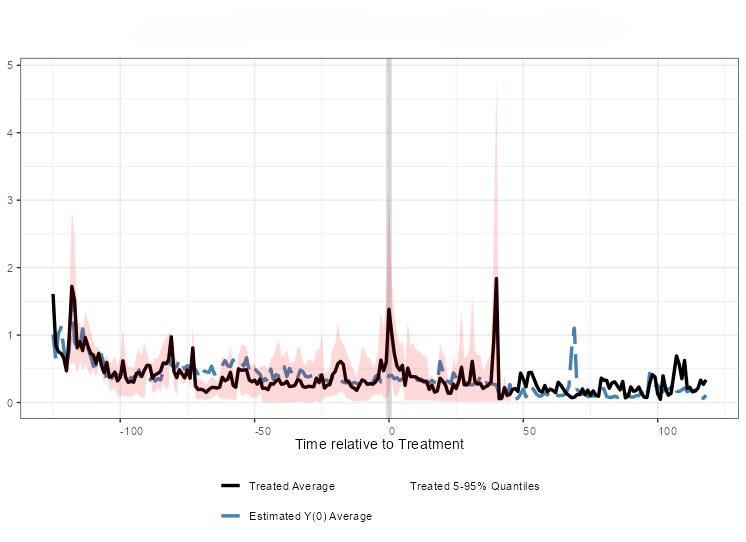

Our study applies GSC following (Xu, 2017), which relaxes the parallel trends assumption commonly required in Difference-in-Differences (DID) ((Card, 1990; Card and Krueger, 1994; Angrist and Pischke, 2009), inter alia) and simultaneously unifies the synthetic control method (Abadie et al., 2010, 2015). In a DID design, the parallel trends assumption requires that, had the treated units never received the intervention, their outcome of interest path would have shared the same baseline slope as that observed for the control group; hence any post-intervention divergence in slopes is attributed to the ATT. Although Figure 3 suggests that a conventional DID strategy could be applied to our three treated countries, the impact of export proceeds repatriation policy on exchange rate volatility is subject to unobserved, time varying confounders. These confounders violate the parallel trends assumption, making a DID specification including the staggered DID design proposed by (Wing et al., 2024), inter alia, unsuitable for this analysis. As our treated units are more than one, using the synthetic control method proposed by (Abadie et al., 2010) is also not feasible.

In order to handle the bias due to the existence of unobserved time-varying confounders, earlier research suggested the use of factor-augmented estimators (Bai, 2009; Gobillon and Magnac, 2016; Liu et al., 2024; Xu, 2017). The factor-augmented estimator we employ is the interactive fixed effect (IFE) model (Bai, 2009). The IFE model employs the interaction between unit-specific intercepts (factor loadings) with time-varying coefficients (latent factors). (Gobillon and Magnac, 2016) show the superiority of the IFE model over the synthetic control method in DID settings when unit-specific intercepts (factor loadings) do not share a common support. The GSC incorporates the IFE into the synthetic control model.

The GSC estimator is specifically designed to remain stable in the presence of limited observations (Xu, 2017). The robustness makes it an appropriate choice for our dataset, which contains just three treated countries and twenty‑four control countries, each observed over 166 monthly periods. Furthermore, the GSC does not discard any observations from the control group; thus, it uses more information from the control group, resulting in a more efficient procedure than the synthetic control method does. A cross-validation scheme is also embedded in the GSC model. This scheme automatically selects the number of factors of the IFE model with high probability, thereby reducing the risk of overfitting.

The framework of the GSC model relies on two main assumptions. First, it requires the treated and control units to be affected by the same set of factors, while the number of factors is fixed for the entire observed period. Thus, it cannot capture unobserved confounders that are independent across units. Second, it assumes that the error term of any unit at any time is independent of the treatment, observed covariates, and unobserved cross-sectional and temporal heterogeneities of all units (including itself) at all periods of observation (Xu, 2017; Liu et al., 2024).

In our study, the outcome of interest is exchange rate volatility, the observation unit is the country (treated and controlled), and the time is the month of observation. The covariates are IRD, inflation differential, and exchange rate regime. We do not include interactions with time and unit (country) since two-way fixed effects in our design absorb any common time-only shocks across units and unit-only shocks across time. Finally, our treatment is the implementation of EPR policies.

Let be our outcome of interest of unit at time , is the total number of units with where is the number of treated unit and is the number of control units. The control units are subscripted from to and the treated units from to . The number of periods of observations is with as the number of pretreatment periods of treated unit while is the period of observation at which pretreatment ends. Hence, we denote the time at which unit is first treated as and control units are never treated at all time . A summary of our observations is given in Table 3. In addition, let denotes the set of units in the treated group and denotes the set of units in the control group.

| Unit | N | |

|---|---|---|

| Treated unit 1 | 45 | |

| Treated unit 2 | 96 | |

| Treated unit 3 | 40 | |

| Control Unit | 166 |

The functional form of our design, following (Xu, 2017), is

| (5) |

where is the heterogeneous treatment effect on unit at time ; is the treatment indicator, which equals if unit is treated at time and equals otherwise; is a vector of observed covariates; is a vector of unknown parameters which, in this study, is assumed to be constant across space and time mainly for faster computation 444as noted by (Xu, 2017), this limitation can be further addressed by using random coefficient models in Bayesian multi-level analysis; however, in this study constant is fairly acceptable since any variation across unit and time are already absorbed by the fixed effects; is an vector of unknown factor loadings; is an vector of unobserved common factors with is the number of factors; and is an unobserved idiosyncratic shock for unit and time with mean zero.

Our main quantity of interest is the average treatment effect on the treated (ATT) at time when , given by

| (6) |

where and are potential outcome if unit is treated at time and potential outcome if unit is not treated at time , respectively. As in (Abadie et al., 2010), we do not incorporate the uncertainty of the treatment effects since we are making inferences about the ATT in the sample, not the ATT of the population. Finally, the model is implemented by using gsynth R package (Xu, 2017).

4 Empirical results and discussions

4.1 Results

Our cross‐validation procedure indicates that three factors () minimize the mean squared prediction error (MSPE), the outcomes of which are reported in Table 4. In reference to Equation 5, is then a vector of unknown factor loadings and is a vector of unobserved common factors.

| r | sigma2 | IC | PC | MSPE |

|---|---|---|---|---|

| 0 | 0.96516 | 0.38998 | 0.91520 | 0.13973 |

| 1 | 0.21216 | -0.71061 | 0.27316 | 0.09043 |

| 2 | 0.12944 | -0.79481 | 0.21065 | 0.08381 |

| 3* | 0.10236 | -0.62404 | 0.20142 | 0.08024 |

| 4 | 0.08534 | -0.40479 | 0.19703 | 0.08485 |

Note: r is the number of unobserved factors; sigma2 is the estimated variance of the error term; IC is the Bayesian Information Criterion; PC is the penalty criterion.

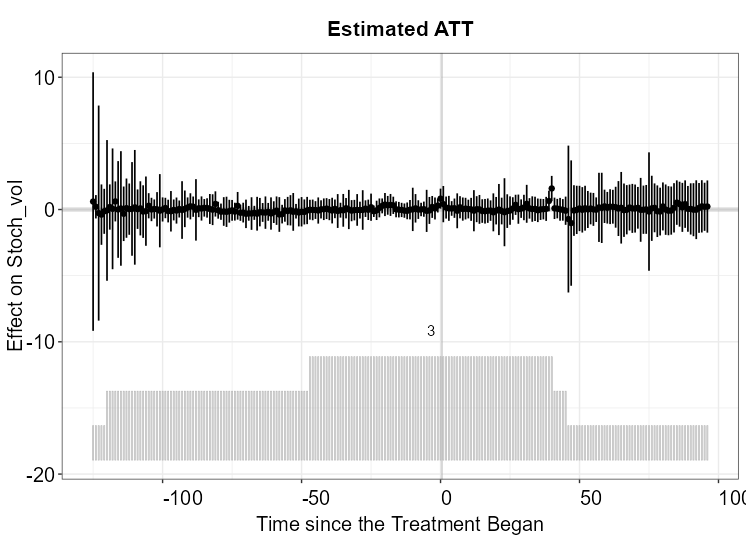

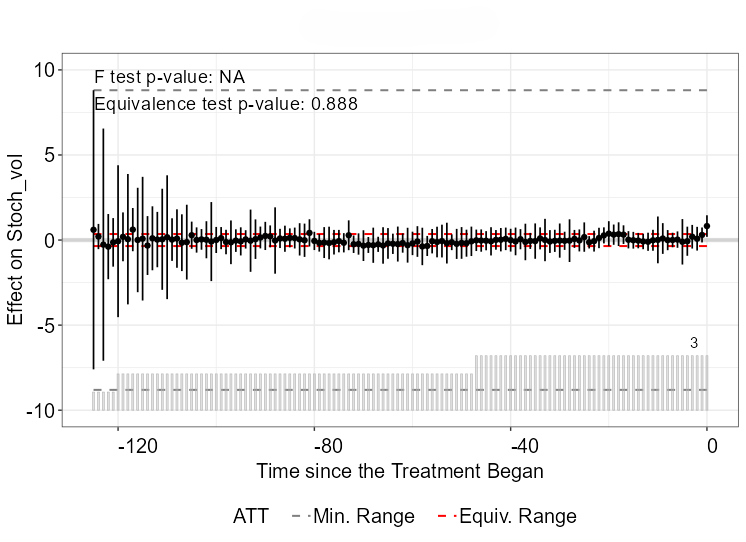

Table 5 and Figure 4 present the estimated ATT and its temporal evolution relative to the start of treatment. The estimated p‑value of , exceeds the conventional 5% threshold for statistical significance. Accordingly, we fail to reject the null hypothesis that the EPR policy has no effect on exchange rate volatility. Adopting a conservative stance that adheres to the 5% significance level (see (Benjamin and Berger, 2019)), we infer that the EPR policy does not exert a statistically robust influence on exchange‑rate volatility across the three treated countries. This inference is reinforced by the estimated ATTs, whose confidence intervals almost uniformly span zero, underscoring both the statistical imprecision and the lack of an economically meaningful effect. In sum, the available evidence remains insufficient to substantiate any substantive influence of the EPR policy on exchange‑rate volatility.

| Average ATT | Standard Error | Lower CI | Upper CI | p-value |

| 0.06939 | 0.15550 | -0.23538 | 0.37417 | 0.65541 |

Note: CI = 95% confidence interval

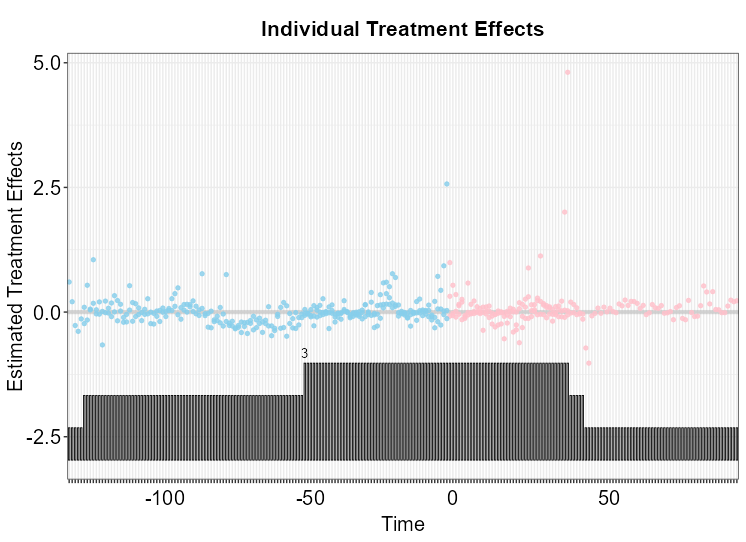

Figure 5 shows the estimated individual treatment effects for every treated unit and period, centered on the policy-adoption date (t = 0). Pretreatment estimates oscillate tightly around zero, with most points lying within ±0.5 standardized units and no discernible drift, indicating a good pre-fit and no anticipatory effects. After adoption, the cloud of points remains centered near zero and retains a similar vertical spread; only a handful of positive outliers peaking at approximately +5 appear several periods after the shock. These idiosyncratic spikes are sparse and do not shift the modal treatment effect, which remains statistically indistinguishable from zero. The accompanying histogram shows that most observations cluster between t = –50 and t = +30; within this dense window, the dot cloud still straddles the zero line, implying that a larger sample mass does not reveal a latent effect concealed by sampling noise. The plot suggests that the export-proceeds repatriation policy did not produce a systematic or economically meaningful change in exchange-rate volatility across treated units; any detectable impact is confined to a few outlying episodes rather than the typical experience. Thus, at the individual level, the policy’s impact is neither widespread nor uniformly strong.

With respect to Equation 5, Table 6 presents our estimates of the covariate coefficients, . By observing the covariates and the p-values, we conclude that both IRD and the exchange rate regime are statistically significant positive predictors of exchange rate volatility with robust standard errors. In contrast, the inflation differential is not statistically significant, as its coefficient is indistinguishable from zero, from our observation of the p-value and the confidence interval that crosses zero. These results suggest that for our sample countries, inflation differentials do not play an important role in determining exchange rate volatility.

| Covariate | Coefficient | Standard Error | Lower CI | Upper CI | p-value |

|---|---|---|---|---|---|

| IRD | 0.00773 | 0.00280 | 0.00225 | 0.01321 | 0.00571 |

| ER_Regime | 0.11504 | 0.01754 | 0.08066 | 0.14942 | 0.00000 |

| Inf_diff | 0.00023 | 0.00151 | -0.00274 | 0.00320 | 0.88093 |

Note: CI = 95% confidence interval

These results are in contrast with (Glick and Hutchinson, 2005), who view export proceeds as a form of restriction on international capital flows and are positively correlated with an exchange rate crisis. Another study that contrasts our results is (Edwards and Rigobon, 2009) which shows that a tightening of capital controls increases the volatility of exchange rates. However, these findings are consistent with (Panggabean et al., 2024), which likewise report no evidence of the impact of repatriated export proceeds on exchange rate volatility in Indonesia in the short and immediate terms.

5 Robustness and sensitivity analysis

5.1 Diagnostics

By examining the counterfactual estimation in Figure 6, we can conclude that the estimated counterfactuals reproduce the treated trajectory reasonably well, where exceptions are noted only for a handful of occasions. Figure 4 and Figure 5 can also be seen as a plot for dynamic treatment effects as defined by (Liu et al., 2024). From the figures, we observe that pretreatment residuals oscillate tightly around the zero line and show no discernible upward or downward drift; the figures provide little evidence of anticipatory behaviour or misspecified pre‑trends. The absence of systematic deviation confirms the strict exogeneity assumption.

Figure 7 reports an equivalence test whose high p-value confirms that the ATT is not statistically different from zero. However, statistical insignificance alone does not guarantee that the effect is practically irrelevant. The 95 % confidence bands repeatedly cross the pre-specified equivalence margins (red dotted lines); therefore, we cannot show that all ATTs fall inside the indifference zone. In summary, the test leaves us with two unresolved possibilities: the policy may exert a non-zero influence, or any influence may be too small to matter substantively. The overall evidence is therefore inconclusive.

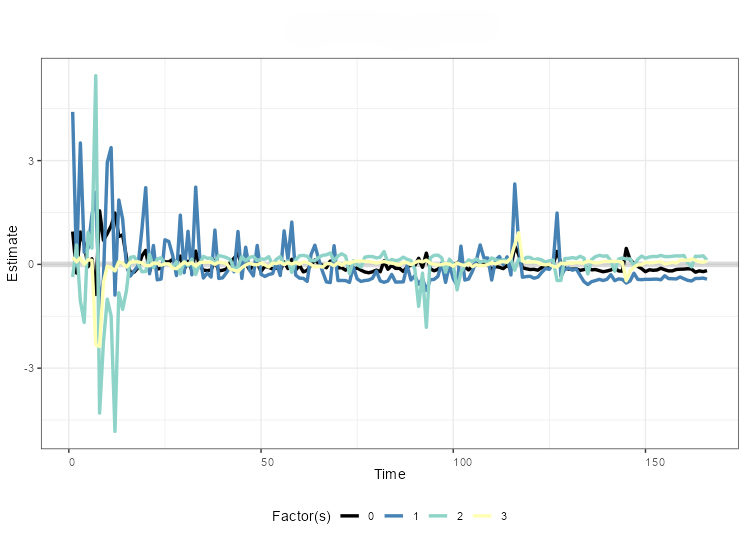

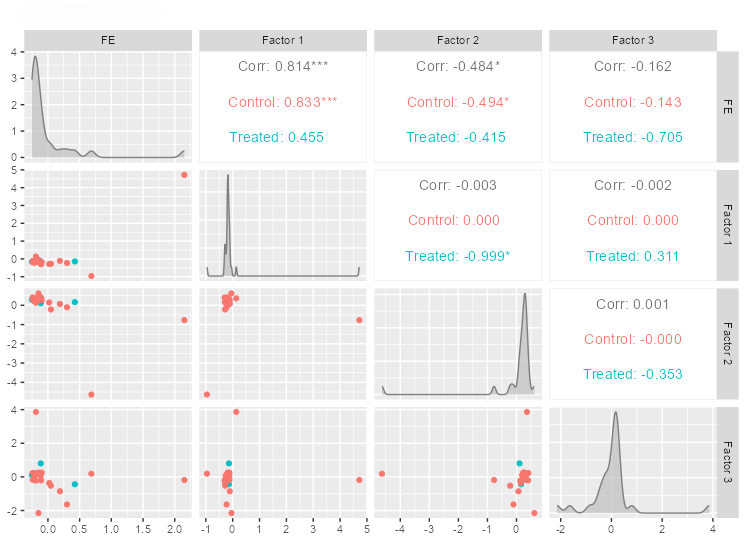

The three common factors we obtained in Subsection 4.1 influence exchange rate volatility and EPR policies, while unobserved and can capture unit-specific sensitivities. Figure 8 and Figure 9 show that the first factor exhibits pronounced early-sample volatility, which correlates strongly with the unit fixed effects, suggesting a global volatility shock that dissipates after the mid-sample. The second factor generates relatively greater volatility compared to the first factor at the beginning of the sample period and moderate, intermittent peaks around the mid-sample period. Moreover, the third factor captures only a one-off negative dip in the early period and minor fluctuations thereafter. After all factors hover close to zero, indicating that most systematic comovement is confined to the initial turbulence.

These heterogeneous loadings underscore the necessity of integrating the IFE into our GFC model. Cross-sectionally, the three factors display distinct loading distributions. Most treated loadings lie inside the control cloud, implying that the donor pool (control units) spans the treated units’ latent characteristics. The strongest relationship is between the unit fixed effect and Factor 1 ( for the whole sample): countries with higher average volatility also load more heavily on the global shock embedded in Factor 1. The correlations with Factors 2 and 3 are weak, which is consistent with these components capturing idiosyncratic, short-lived disturbances. Crucially, treated-unit loadings do not cluster at the extremes of any factor; hence, there is no evidence that the treated group is an outlier in the latent space. Therefore, the GSC should provide credible counterfactuals. In summary, the factor paths and loadings confirm that the model has isolated a small set of common shocks (mainly in the early sample) and that the treated economies are well represented within that latent-factor span.

5.2 Sensitivity analysis

Since the GSC works well even with a single treated unit, we employ the method for each treated unit separately but with the same covariates and the same control units. We then examine the results presented in Table 7. For Iran, Sri Lanka, and Turkey, there are very high p-values, indicating that there are no effect of EPR policies on exchange rate volatility, which is consistent with our results in Subsection 4.1. The MSPE remains low and the number of factors suggested by the cross validation procedures (3, 3, and 4), are similar to the number of factors that we used in our model. The significance of the coefficients of the covariates is also consistent with our results. All three countries show that the inflation differential is not statistically significant different from zero as a predictor of exchange rate volatility.

| Model | Response Variable: Exchange Rate Volatility | ||

|---|---|---|---|

| Iran | Sri Lanka | Turkey | |

| ATT | -0.02547 | 0.03486 | 0.27393 |

| (se: 0.17905) | (se: 0.19133) | (se: 0.35411) | |

| [p-value: 0.88686] | [p-value: 0.85544] | [p-value: 0.43917] | |

| MSPE | 0.04919 | 0.02911 | 0.12641 |

| sigma2 | 0.08534 | 0.10236 | 0.10236 |

| Covariates | IRD, ER_Regime, Inf_diff | ||

| Unobserved factors | 4 | 3 | 3 |

| Significant | IRD, ER_Regime | IRD, ER_Regime | IRD, ER_Regime |

| Fixed effects | two way | ||

| Observations | 166 | ||

| Treated country | Iran | Sri Lanka | Turkey |

| Control countries | Armenia, Bahrain, Bolivia, Botswana, Gambia, Georgia, Jamaica, Jordan, Kenya, Kuwait, Kyrgyzstan, Mexico, Mongolia, Oman, Paraguay, Peru, Philippines, Qatar, Saudi Arabia, Trinidad and Tobago, Uganda, United Arab Emirates, Uruguay, Zambia | ||

Note: sigma2 is the estimated variance of the error term

We also perform a sensitivity analysis of our model using an alternative covariate specification that includes IRD, prevailing exchange rate regime, and terms of trade (ToT). Since Iran, Sri Lanka, and Turkey do not rely heavily on exports, including ToT as a covariate is a way to disturb the model and check the reliability of our model. Our results using this set of covariates show that the ATT remains not significantly different from zero, whereas the same set of covariates, IRD and exchange rate regime, remain significant in determining exchange rate volatility. A summary of the results is presented in Table 8

| ATT | Standard Error | Lower CI | Upper CI | p-value |

| 0.08713 | 0.07644 | -0.06269 | 0.23695 | 0.25435 |

Note: CI = 95% confidence interval

5.3 Placebo Tests

To verify whether our GSC estimates are not driven by spurious fit, we perform both in-time and in-space placebo tests. Table 9 presents the results of the in-time placebo test when we pretend that the policy began for every treated country in January 2013, which is twelve periods before the earliest actual adoption. The placebo average treatment effect is small and its bootstrap p-value far exceeds the 95% significance thresholds, indicating that the GSC procedure does not generate false positives when no treatment has yet occurred.

| Placebo ATT | Standard Error | Lower CI | Upper CI | Placebo p-value |

| 0.05805 | 0.17686 | -0.28859 | 0.40469 | 0.74275 |

Following (Abadie et al., 2015), we perform in-space placebo tests in which we assign the policy, one at a time, to each control country, using the three actual start dates of Iran, Sri Lanka, and Turkey. For every such pseudo-treated unit, we re-estimate the model and record the placebo ATT. The empirical p-value is computed as the share of placebo ATTs whose value is at least as large as the true ATT. We discard placebo runs for which cross-validation selects r = 0 factors (i.e., ordinary two-way fixed effects) because in those cases the GSC specification is not applicable. Table 10 shows the placebo effects for each pseudo-treated unit, and that the empirical p-value is not statistically significant.

| Pseudo-treated Unit | First Treatment Time: Apr 2018 | First Treatment Time: Jan 2014 | First Treatment Time: Sep 2018 | |||

| Placebo ATT | p-value* | Placebo ATT | p-value* | Placebo ATT | p-value* | |

| Armenia | -0.00056 | 1 | -0.03748 | 1 | -0.05940 | 1 |

| Bahrain | -0.00688 | 1 | -0.00960 | 1 | -0.01305 | 1 |

| Bolivia | -0.00667 | 1 | 0.00113 | 1 | -0.01251 | 1 |

| Botswana | -0.15773 | 1 | -0.23320 | 1 | -0.16393 | 1 |

| Gambia | -2.25546 | 0 | -3.28953 | NA | -2.32469 | 0 |

| Georgia | 0.02534 | 1 | 0.25366 | 1 | 0.02604 | 1 |

| Jamaica | 0.27812 | 1 | -0.01902 | 1 | 0.27374 | 1 |

| Jordan | 0.00005 | 1 | 0.00534 | 1 | -0.00350 | 1 |

| Kenya | -0.13958 | 1 | -0.14343 | 1 | -0.15849 | 1 |

| Kuwait | -0.13324 | 1 | -0.08446 | 1 | -0.14757 | 1 |

| Kyrgyzstan | 0.24428 | 1 | 0.12806 | 1 | 0.25396 | 1 |

| Mexico | 0.07573 | 1 | -0.12681 | 1 | 0.05667 | 1 |

| Mongolia | -0.00852 | 1 | -0.03972 | 1 | 0.04329 | 1 |

| Oman | -0.00091 | 1 | -0.00175 | 1 | -0.00271 | 1 |

| Paraguay | -0.15717 | 1 | -0.25431 | 1 | -0.14856 | 1 |

| Peru | 0.10523 | 1 | 0.09762 | 1 | 0.12142 | 1 |

| Philippines | 0.00569 | 1 | -0.01584 | 1 | 0.01251 | 1 |

| Qatar | 0.02965 | NA | 0.11598 | 1 | 0.04394 | NA |

| Saudi Arabia | -0.01111 | 1 | -0.00547 | 1 | -0.01541 | 1 |

| Trinidad and Tobago | -0.06644 | 1 | 0.06387 | 1 | -0.07147 | 1 |

| Uganda | -0.11615 | 1 | -0.31584 | 1 | -0.11658 | 1 |

| United Arab Emirates | -0.00261 | 1 | -0.00051 | 1 | -0.00530 | 1 |

| Uruguay | -0.44698 | 0 | -0.37769 | 1 | -0.45942 | 0 |

| Zambia | -0.30535 | 1 | 0.53493 | NA | -0.28824 | 1 |

| ATT of in-sample placebo test: -0.10711 | ||||||

| p-value of in-sample placebo test: 0.94118 | ||||||

Note: p-value* is 1 if placebo ATT true ATT and 0 otherwise; p-value* is NA when , indicating the infeasibility of GSC implementation for such pseudo-treated unit.

Both placebo tests strengthen confidence in our baseline findings. That is, the non-existence of a robust impact of EPR policies on exchange-rate volatility is not caused by model overfitting or by chance correlations in the data.

6 Conclusions

This study investigates the impact of an export proceeds repatriation policy on exchange rate volatility in Iran, Sri Lanka, and Turkey from March 2008 to December 2021. Our results do support the hypothesis that the export proceeds repatriation policy does not have an impact on exchange rate volatility. However, we cannot reject the possibility that any impact is too small to be substantively meaningful. These conclusions are robust across several sensitivity analyses and placebo tests, attesting to their reliability. These results are in contrast with several studies on foreign capital flows that flag EPR policies as a form of restriction on international capital flows that increases exchange rate volatility. However, another former study on repatriated export proceeds shows similar results to ours.

Nevertheless, our results should be interpreted with caution. The absence of proprietary export proceeds volume data and central bank intervention may influence the results, given the different natures of regulations in each country. We suggest that further research include these data to gain deeper insights into each emerging country being analyzed.

Appendix A Data Source for Short-term Interest Rates

| No. | Country | Interest Rates | Data Sources |

|---|---|---|---|

| 1 | Armenia | Money market rates | CEIC |

| 2 | Bahrain | BHIBOR | Refinitiv Eikon |

| 3 | Bolivia | Interbank rates | CEIC |

| 4 | Botswana | Policy rates | CEIC |

| 5 | Gambia | T-bill rates and Policy rates | CEIC |

| 6 | Georgia | Money market rates | Bloomberg |

| 7 | Iran | Policy rates, Interbank rates, and Deposit rates | CEIC and central bank website |

| 8 | Jamaica | Money market rates and T-bill rates | CEIC |

| 9 | Jordan | Money market rates | CEIC |

| 10 | Kenya | Interbank rates | CEIC |

| 11 | Kuwait | Interbank rates | CEIC |

| 12 | Kyrgyzstan | Interbank rates | CEIC |

| 13 | Mexico | Money market rates and TIIE | CEIC and Refinitiv Eikon |

| 14 | Mongolia | Interbank rates | CEIC |

| 15 | Oman | Interbank rates | CEIC |

| 16 | Paraguay | Money market rates and Policy rates | CEIC |

| 17 | Peru | Interbank rates | Refinitiv Eikon |

| 18 | Philippines | Money market rates | CEIC |

| 19 | Qatar | Overnight Deposit rates and QIBOR | Refinitiv Eikon |

| 20 | Saudi Arabia | Policy rates, Money market rates, and SAIBOR | CEIC and Refinitiv Eikon |

| 21 | Sri Lanka | SLIBOR and Call market rates | CEIC |

| 22 | Trinidad and Tobago | Reverse Repo rates | Bloomberg |

| 23 | Turkey | Interbank rates and Money market rates | CEIC |

| 24 | Uganda | T-bill rates and Overnight Deposit rates | CEIC and Refinitv Eikon |

| 25 | United Arab Emirates | Interbank rates and EIBOR | CEIC and central bank website |

| 26 | Uruguay | Money market rates and Interbank rates | CEIC and Refinitv Eikon |

| 27 | Zambia | Policy rates and Overnight Deposit rates | CEIC and Refinitv Eikon |

Note: BHIBOR=Bahraini Interbank Offered Rate; TIIE=Tasa de Interes Interbancaria de Equilibrio (Interbank Equilibrium Interest Rate); QIBOR=Qatar Interbank Offered Rate; SAIBOR=Saudi Arabian Interbank Offered Rate; SLIBOR= Sri Lankan Interbank Offered Rate; EIBOR=The Emirates Interbank Offered Rate.

References

- Abadie et al. (2010) Abadie, A., Diamond, A., Hainmueller, J., 2010. Synthetic Control Methods for Comparative Case Studies: Estimating the Effect of California’s Tobacco Control Program. Journal of the American Statistical Association 105, 493–505. doi:10.1198/jasa.2009.ap08746.

- Abadie et al. (2015) Abadie, A., Diamond, A., Hainmueller, J., 2015. Comparative Politics and the Synthetic Control Method. American Journal of Political Science 59, 495–510. doi:10.1111/ajps.12116.

- Aghion et al. (2009) Aghion, P., Bacchetta, P., Rancière, R., Rogoff, K., 2009. Exchange Rate Volatility and Productivity Growth: The Role of Financial Development. Journal of Monetary Economics 56, 494–513. doi:10.1016/j.jmoneco.2009.03.015.

- Anderson et al. (2009) Anderson, H., Veyrune, R., Kokenyne, A., Habermeier, K., 2009. Revised System for the Classification of Exchange Rate Arrangements. IMF Working Papers 2009, 1. doi:10.5089/9781451873580.001.

- Angrist and Pischke (2009) Angrist, J.D., Pischke, J.S., 2009. Mostly Harmless Econometrics: An Empiricist’s Companion. Princeton University Press. doi:10.2307/j.ctvcm4j72.

- Asiedu and Lien (2004) Asiedu, E., Lien, D., 2004. Capital Controls and Foreign Direct Investment. World Development 32, 479–490. doi:10.1016/j.worlddev.2003.06.016.

- Aysun (2024) Aysun, U., 2024. Identifying the External and Internal Drivers of Exchange Rate Volatility in Small Open Economies. Emerging Markets Review 58, 101085. doi:10.1016/j.ememar.2023.101085.

- Bai (2009) Bai, J., 2009. Panel Data Models With Interactive Fixed Effects. Econometrica 77, 1229–1279. doi:10.3982/ecta6135.

- Baum and Caglayan (2010) Baum, C.F., Caglayan, M., 2010. On the Sensitivity of the Volume and Volatility of Bilateral Trade Flows to Exchange Rate Uncertainty. Journal of International Money and Finance 29, 79–93. doi:10.1016/j.jimonfin.2008.12.003.

- Benjamin and Berger (2019) Benjamin, D.J., Berger, J.O., 2019. Three Recommendations for Improving the Use of P-Values. American Statistician 73, 186–191. doi:10.1080/00031305.2018.1543135.

- Brunnermeier et al. (2008) Brunnermeier, M.K., Nagel, S., Pedersen, L.H., 2008. Carry Trades and Currency Crashes. NBER Macroeconomics Annual 23, 313–347. doi:10.1086/593088.

- Bush and López Noria (2021) Bush, G., López Noria, G., 2021. Uncertainty and Exchange Rate Volatility: Evidence From Mexico. International Review of Economics and Finance 75, 704–722. doi:10.1016/j.iref.2021.04.029.

- Calvo et al. (1996) Calvo, G.A., Leiderman, L., Reinhart, C.M., 1996. Inflows of Capital to Developing Countries in the 1990s. Modern Political Economy and Latin America: Theory and Policy 10, 217–223. doi:10.4324/9780429498893-28.

- Caporale et al. (2017) Caporale, G.M., Ali, F.M., Spagnolo, F., Spagnolo, N., 2017. International Portfolio Flows and Exchange Rate Volatility in Emerging Asian Markets. Journal of International Money and Finance 76, 1–15. doi:10.1016/j.jimonfin.2017.03.002.

- Card (1990) Card, D., 1990. The Impact of the Mariel Boatlift on the Miami Labor Market. Industrial and Labor Relations Review 43, 245–257. doi:10.1177/001979399004300205.

- Card and Krueger (1994) Card, D., Krueger, A.B., 1994. Minimum Wages and Employment: A Cast Study of the Fast-Food Industry in New Jersey and Pennsylvania. American Economic Review 84, 772–793. doi:10.1257/aer.90.5.1397.

- Chan et al. (2019) Chan, J., Koop, G., Poirier, D.J., Tobias, J.L., 2019. Time Series Models for Volatility, in: Bayesian Econometric Methods. Cambridge University Press, pp. 391–410. URL: Https://www.cambridge.org/highereducation/product/9781108525947/book, doi:10.1017/9781108525947.

- Choudhri and Hakura (2006) Choudhri, E.U., Hakura, D.S., 2006. Exchange Rate Pass-Through to Domestic Prices: Does the Inflationary Environment Matter? Journal of International Money and Finance 25, 614–639. doi:10.1016/j.jimonfin.2005.11.009.

- Clarida et al. (2002) Clarida, R., Gal, J., Gertler, M., 2002. A Simple Framework for International Monetary Policy Analysis. Journal of Monetary Economics 49, 879–904. doi:10.1016/S0304-3932(02)00128-9.

- Clarida and Waldman (2008) Clarida, R.H., Waldman, D., 2008. Is Bad News About Inflation Good News for the Exchange Rate? And, if So , Can That Tell Us Anything About the Conduct of Monetary Policy?, in: Campbel, J.Y. (Ed.), Asset Prices and Monetary Policy. University of Chicago Press. chapter 9, pp. 371–396. doi:10.7208/9780226092126-012.

- Daníelsson (1998) Daníelsson, J., 1998. Multivariate Stochastic Volatility Models: Estimation and a Comparison With VGARCH Models. Journal of Empirical Finance 5, 155–173. doi:10.1016/S0927-5398(97)00016-9.

- Devereux and Engel (2002) Devereux, M.B., Engel, C., 2002. Exchange Rate Pass-Through, Exchange Rate Volatility, and Exchange Rate Disconnect. Journal of Monetary Economics 49, 913–940. doi:10.1016/S0304-3932(02)00130-7.

- Edwards and Rigobon (2009) Edwards, S., Rigobon, R., 2009. Capital Controls on Inflows, Exchange Rate Volatility and External Vulnerability. Journal of International Economics 78, 256–267. doi:10.1016/j.jinteco.2009.04.005.

- Ekananda and Suryanto (2021) Ekananda, M., Suryanto, T., 2021. The Influence of Global Financial Liquidity on the Indonesian Economy: Dynamic Analysis with Thrreshold VAR. Economies 4, 162–182. doi:10.3390/economies9040162.

- Farhi and Gabaix (2016) Farhi, E., Gabaix, X., 2016. Rare Disasters and Exhange Rates. The Quarterly Journal of Economics 131, 1–52. doi:10.1093/qje/qjv040.

- Faust et al. (2007) Faust, J., Rogers, J.H., Wang, S.Y.B., Wright, J.H., 2007. The High-Frequency Response of Exchange Rates and Interest Rates to Macroeconomic Announcements. Journal of Monetary Economics 54, 1051–1068. doi:10.1016/j.jmoneco.2006.05.015.

- Feldmann (2011) Feldmann, H., 2011. The Unemployment Effect of Exchange Rate Volatility in Industrial Countries. Economics Letters 111, 268–271. doi:10.1016/j.econlet.2011.01.003.

- Flood and Rose (1999) Flood, R.P., Rose, A.K., 1999. Understanding Exchange Rate Volatility Without the Contrivance of Macroeconomics. The Economic Journal 109, F660–F672. doi:10.1111/1468-0297.00478.

- Gabaix and Maggiori (2015) Gabaix, X., Maggiori, M., 2015. International Liquidity and Exchange Rate Dynamics. The Quarterly Journal of Economics 130, 1369–1420. doi:10.1093/qje/qjv016.Advance.

- Ghosh et al. (2002) Ghosh, A.R., Gulde, A.M., Wolf, H.C., 2002. Exchange Rate Regimes: Choices and Consequences. The MIT Press. doi:10.7551/mitpress/2898.001.0001.

- Glick and Hutchinson (2005) Glick, R., Hutchinson, M., 2005. Capital Controls and Exchange Rate Instability in Developing Economies. Journal of International Money and Finance 24, 387–412. doi:10.1016/j.jimonfin.2004.11.004.

- Gobillon and Magnac (2016) Gobillon, L., Magnac, T., 2016. Regional Policy Evaluation: Interactive Fixed Effects and Synthetic Controls. Review of Economics and Statistics 98, 535–551. doi:10.1162/REST\_a\_00537.

- Goldberg and Klein (2005) Goldberg, L.S., Klein, M.W., 2005. Establishing Credibility : Evolving Perceptions of the European Central Bank. Technical Report 231. Federal Reserve Bank of New York.

- Grier and Grier (2006) Grier, R., Grier, K.B., 2006. On the Real Effects of Inflation and Inflation Uncertainty in Mexico. Journal of Development Economics 80, 478–500. doi:10.1016/j.jdeveco.2005.02.002.

- Grossmann and Orlov (2014) Grossmann, A., Orlov, A.G., 2014. A Panel-Regression Investigation of Exchange Rate Volatility. International Journal of Finance and Economics 326, 303–326. doi:10.1002/ijfe.

- Guillaumont (1980) Guillaumont, P., 1980. The Impact of Declining Terms of Trade and Inflation on the Export Proceeds and Debt Burden of Developing Countries. World Development 8, 763–768. doi:10.1016/0305-750X(80)90003-0.

- Iseringhausen (2020) Iseringhausen, M., 2020. The Time-Varying Asymmetry of Exchange Rate Returns: A Stochastic Volatility – Stochastic Skewness Model. Journal of Empirical Finance 58, 275–292. URL: Https://doi.org/10.1016/j.jempfin.2020.06.008, doi:10.1016/j.jempfin.2020.06.008.

- Kim et al. (1998) Kim, S., Shephard, N., Chib, S., 1998. Stochastic Volatility: Likelihood Inference and Comparison With ARCH Models. Review of Economic Studies 65, 361–393. doi:10.1111/1467-937X.00050.

- Krol (2014) Krol, R., 2014. Economic Policy Uncertainty and Exchange Rate Volatility. International Finance 17, 241–256. doi:10.1111/infi.12049.

- Lee-Lee and Hui-Boon (2007) Lee-Lee, C., Hui-Boon, T., 2007. Macroeconomic Factors of Exchange Rate Volatility: Evidence From Four Neighbouring ASEAN Economies. Studies in Economics and Finance 24, 266–285. doi:10.1108/10867370710831828.

- Levy-Yeyati and Sturzenegger (2003) Levy-Yeyati, E., Sturzenegger, F., 2003. To Float or to Fix: Evidence on the Impact of Exchange Rate Regimes on Growth. The American Economic Review 93, 1173–1193. doi:10.1257/000282803769206250.

- Liu et al. (2024) Liu, L., Wang, Y., Xu, Y., 2024. A Practical Guide to Counterfactual Estimators for Causal Inference With Time-Series Cross-Sectional Data. American Journal of Political Science 68, 160–176. doi:10.1111/ajps.12723, arXiv:2107.00856.

- Macbean (1962) Macbean, A.I., 1962. Causes of Excessive Fluctuations in Export Proceeds of Underdeveloped Countries. Bulletin of the Oxford University Institute of Economics & Statistics 27, 323–341. doi:10.1111/j.1468-0084.1964.mp27004003.x.

- MacDonald (2007) MacDonald, R., 2007. Exchange Rate Economics: Theories and Evidence. Routledge, London. doi:10.4324/9780203380185.

- Massell (1964) Massell, B.F., 1964. Export Concentration and Fluctuations in Export Earnings: A Cross-Section Analysis. The American Economic Review 54, 47–63.

- Orlov (2006) Orlov, A.G., 2006. Capital Controls and Stock Market Volatility in Frequency Domain. Economics Letters 91, 222–228. doi:10.1016/j.econlet.2005.09.014.

- Orlov (2009) Orlov, A.G., 2009. A Cospectral Analysis of Exchange Rate Comovements During Asian Financial Crisis. Journal of International Financial Markets , Institutions & Money 19, 742–758. doi:10.1016/j.intfin.2008.12.004.

- Panggabean et al. (2024) Panggabean, S., Ekananda, M., Gitaharie, B.Y., Djuranovik, L., 2024. Steadying the Ship: Can Export Proceeds Repatriation Policy Stabilize Indonesian Exchange Rates Amid Short-Term Capital Flows Fluctuations? SSRN Working Paper 5220907, SSRN. URL: Papers.ssrn.com/abstract=5220907.

- Pitt and Shephard (1999) Pitt, M.K., Shephard, N., 1999. Filtering via Simulation: Auxiliary Particle Filters. Journal of the American Statistical Association 94, 590–599. doi:10.1080/01621459.1999.10474153.

- Powell (1959) Powell, A.A., 1959. Export Receipts and Expansion in the Wool Industry. Australian Journal of Agricultural Economics 3, 64–74. doi:10.1111/j.1467-8489.1959.tb00260.x.

- Prayoga and Purnomo (2024) Prayoga, D.S., Purnomo, D., 2024. The Influence of Foreign Exchange Policy From Export Proceeds, Import Payments, Inflation Rate, and Rupiah Exchange Rate on Foreign Direct Investment in Indonesia. Indonesian Interdisciplinary Journal of Sharia Economics (IIJSE) 7, 4875–4901. doi:10.31538/iijse.v7i3.5467.

- Rafi and Ramachandran (2018) Rafi, O.P.C.M., Ramachandran, M., 2018. Capital Flows and Exchange Rate Volatility : Experience of Emerging Economies. Indian Economic Review 53, 183–205. doi:10.1007/s41775-018-0031-1.

- Sarno and Taylor (2003) Sarno, L., Taylor, M.P., 2003. The Economics of Exchange Rates. Cambridge University Press, Cambridge. doi:10.1017/CBO9780511754159.

- Sukmawati and Ekananda (2018) Sukmawati, I., Ekananda, M., 2018. Exchange Rate Volatility Effect on Indonesia’s Exports, in: Dartanto, T., Gitaharie, B.Y., Handayani, D., Shauki, E.R. (Eds.), Challenges of the Global Economy: Some Indonesian Issues. Nova Science Publishers. chapter 15, pp. 287–308. doi:10.7208/9780226092126-012.

- Wallich (1961) Wallich, H.C., 1961. Stabilization of Proceeds From Raw Material Exports, in: Ellis, H.S., Wallich, H.C. (Eds.), Economic Development for Latin America, Palgrave Macmillan UK. pp. 342–365. doi:10.1007/978-1-349-08449-4.

- Wing et al. (2024) Wing, C., Yozwiak, M., Hollingsworth, A., Freedman, S., Simon, K., 2024. Designing Difference-in-Difference Studies With Staggered Treatment Adoption: Key Concepts and Practical Guidelines. Annual Review of Public Health 45, 485–505. doi:10.1146/annurev-Publhealth-061022-050825.

- Xu (2017) Xu, Y., 2017. Generalized Synthetic Control Method: Causal Inference With Interactive Fixed Effects Models. Political Analysis 25, 57–76. doi:10.1017/pan.2016.2.

- ŞEn et al. (2020) ŞEn, H., Kaya, A., Kaptan, S., Cömert, M., 2020. Interest Rates, Inflation , and Exchange Rates in Fragile EMEs : A Fresh Look at the Long-Run Interrelationships. The Journal of International Trade & Economic Development 29, 289–318. doi:10.1080/09638199.2019.1663441.