AAppendix References

Explaining Sustained Blockchain Decentralization with Quasi-Experiments:

Resource Flexibility of Consensus Mechanisms

Abstract

Decentralization is a fundamental design element of the Web3 economy. Blockchains and distributed consensus mechanisms are touted as fault-tolerant, attack-resistant, and collusion-proof because they are decentralized. Recent analyses, however, find some blockchains are decentralized, others are centralized, and that there are trends towards both centralization and decentralization in the blockchain economy. Despite the importance and variability of decentralization across blockchains, we still know little about what enables or constrains blockchain decentralization. We hypothesize that the resource flexibility of consensus mechanisms is a key enabler of the sustained decentralization of blockchain networks. We test this hypothesis using three quasi-experimental shocks—policy-related, infrastructure-related, and technical—to resources used in consensus. We find strong suggestive evidence that the resource flexibility of consensus mechanisms enables sustained blockchain decentralization and discuss the implications for the design, regulation, and implementation of blockchains.

1 Introduction

Blockchains offer an alternative to centralized systems through a model of trust built on distributed consensus (Ammous, 2018). While they were originally conceived as a time-stamping mechanism to prevent back- or forward-dating digital documents (Haber and Stornetta, 1991), in their modern incarnation, blockchain implementations are designed to remove centralized institutions from the process of tracking electronic cash (Nakamoto, 2008) and to execute generalized software programs without intermediaries (Buterin, 2014). Decentralization is fundamental to the ability of blockchains to operate without centralized intermediaries while maintaining resistance to attacks, faults, and collusion (Buterin, 2017). While too much decentralization can be bad for blockchain governance (Chen et al., 2021), failure to sustain decentralization in blockchain consensus mechanisms can cause catastrophic failures that lead to the loss of billions of dollars of economic value and data integrity regarding asset ownership. For example, the Ronin blockchain was hacked in 2022 for $625 million because of centralized points of failure (Thurman, 2022) and 51% attacks occur frequently and have significant and lasting negative effects on token prices (Shanaev et al., 2019). Since 2009, with blockchains growing rapidly and cryptocurrencies surpassing a 3.7 trillion-dollar market capitalization,111CoinMarketCap Accessed February 18, 2025. and with institutions, including governments, increasingly tokenizing hundreds of billions of dollars of bonds and other assets on blockchains, understanding and sustaining decentralization is becoming increasingly critical (Bank, 2021; Securitize, 2024).

While many tout the decentralized nature of blockchain technology, it is still unclear whether blockchains are actually becoming more centralized or decentralized over time and, perhaps more importantly, what drives blockchain centralization or decentralization. Indeed, decentralization faces powerful economic headwinds, including economies of scale and coordination costs (Hui and Tucker, 2023). It also faces economic trade-offs with blockchain’s other goals, such as net neutrality and permissionlessness (Halaburda and Obermeier, 2024; Bakos et al., 2021). Recent empirical work also estimates that several key subsystems of blockchain ecosystems are becoming more centralized (Ju et al., 2025). In this paper, we explore potential enablers of sustained blockchain decentralization in consensus mechanisms, an key element of this technology critical to establishing trust and fault tolerance without centralization.

By relying on technical virtualization theory, we hypothesize that the flexibility of resources required for consensus mechanisms is an important causal enabler of sustained blockchain decentralization (see Section 2). We define resource flexibility as the ease with which participants can acquire and deploy the resources needed for consensus mechanisms, which includes the initial acquisition and the ongoing operation and maintenance of resources. Many blockchains require the use of costly resources to verify transactions for proof-based consensus mechanisms, including hardware and electricity for Proof-of-Work (PoW) and native blockchain tokens for Proof-of-Stake (PoS). Causal examination of the implications of technical resource flexibility on sustained blockchain decentralization can therefore inform design decisions in the pursuit of decentralization at the heart of blockchain technologies.222The Proof-of-Authority consensus mechanism, which relies on a small number of validators selected by a central authority, is an exception to this requirement, though its inclusion in the validator set, determined by centralized authorities, is also a costly resource.

We leverage quasi-experimental variation across six blockchains (i.e., Bitcoin, Ethereum, Solana, Gnosis, BNB, Ronin) to investigate how resource flexibility, proxied by differences in blockchain designs, influences blockchain decentralization in the context of three independent shocks: a policy-related shock (China’s crypto mining ban on May 15, 2021), an infrastructure-related shock (Hetzner’s shutdown of Solana validators on November 2, 2022), and a technical shock (the Ethereum Merge on September 15, 2022). China’s ban shows the impact of resource flexibility (i.e., ASICs vs. GPUs) in response to a policy shock; Hetzner’s shutdown contrasts with China’s ban by revealing the impact of an even more flexible resource (i.e., tokens in PoS vs. hardware in PoW) in response to an infrastructure shock; and the Ethereum Merge assesses the effect of increased resource flexibility as Ethereum upgraded from PoW to PoS. To measure these effects, we employ event studies, difference-in-difference (DiD) estimation, and synthetic DiD (SDiD) methods and use five different measures of decentralization: Shannon entropy, the number of validating nodes, the Gini coefficient, the Nakamoto coefficient, and the Herfindahl–Hirschman Index.

Our analysis provides strong evidence suggesting that the resource flexibility of distributed consensus mechanisms enables sustained blockchain decentralization. We find that China’s ban reduced Bitcoin’s decentralization in comparison to Ethereum’s by around 0.21 bits of Shannon entropy from around 3.7 bits, that Hetzner’s shutdown reduced Solana’s decentralization by around 0.35 bits and that the dynamics of the recovery from the initial shocks varied widely across the two shocks. Bitcoin’s decentralization took over 6 months to recover from China’s ban, while Solana’s decentralization fully recovered from the Hetzner shutdown in approximately one month. Our analysis also decomposes the entropy into the number of nodes in the network and the distribution of block production across those nodes. We discuss why the difference in recovery rates between Bitcoin and Ethereum in response to the China ban and Solana’s rapid recovery from the Hetzner shutdown together support our hypothesis. We also find that the Ethereum Merge, which transitioned Ethereum from a Proof-of-Work (PoW) consensus mechanism (which is less flexible) to a Proof-of-Stake (PoS) mechanism (which is more flexible), provides a natural proxy for increased resource flexibility, thereby increasing Ethereum’s decentralization by 0.52 bits. Collectively, our findings offer strong suggestive evidence that variation in the level of resource flexibility in consensus mechanisms—from ASICs to GPUs and from PoW to PoS—is associated with sustained levels of blockchain decentralization.

To the best of our knowledge, ours is the first study to empirically quantify the impact of consensus mechanism design on sustained blockchain decentralization and our work contributes to several areas of research. First, our study is related to the literature on blockchain consensus mechanisms and their economic and technical implications (Bamakan et al., 2020; Halaburda et al., 2022). Consensus predicates many of the unique features of blockchains, including permissionlessness and trustlessness, which in turn support ownership, native payments, DeFi, and arbitrary smart contracts without central authorities (Catalini and Gans, 2016; Cong and He, 2019; Harvey et al., 2021; John et al., 2022). While previous studies illustrated the benefits of the technology, our paper is among the first to empirically demonstrate whether and how the consensus mechanism supports blockchain technology’s promise of a decentralized network.

Our work also contributes to the literature on the decentralization of blockchains (Gencer et al., 2018; Hoffman et al., 2020; Wu et al., 2020; Cong et al., 2021; Sai et al., 2021; Jia et al., 2022). Many studies have pointed out the centralized nature of blockchain consensus mechanisms (Srinivasan and Lee, 2017), especially in permissionless blockchains (Bakos et al., 2021). Cong et al. (2022) recently causally identified off-chain computation (in Layer 2 “roll-ups”) as a driver of decentralization in data providers for oracles, though not for the central mechanism of blockchain consensus. Capponi et al. (2023) theoretically demonstrate how hardware-based consensus mechanisms can support decentralization. Interestingly, our work complements that of Garratt and van Oordt (2023) who show that fixed costs in crypto mining increase resilience against 51% attacks when there are shocks to the price of crypto mining rewards. They argue fixed costs make it harder for miners to switch their hardware, or other resources, to other uses when mining rewards drop in price, thus improving resilience against attacks. Our results show the flip side of resource flexibility: when there are shocks to the resources required for mining (versus the rewards from mining), it is harder for miners or validators to obtain or migrate the resources to keep mining. Given the raison d’être of blockchains of forgoing centralized intermediaries and resisting external shocks, it is essential to understand the conditions under which blockchains are or are not decentralized and shock resistant, especially as more economic activity occurs on blockchains, including trading in government bonds (Bank, 2021) and stock exchanges (Meichler, 2023). We believe our work reveals the nuanced, causal role of resource flexibility in sustaining decentralization in the consensus mechanisms at the heart of blockchains.

2 Theory: Decentralization and Virtualization

2.1 Decentralization

The underlying integrity of blockchains depends, in theory and in practice, on their decentralization. Yet, empirical evidence reveals that decentralization is neither guaranteed and face economic headwinds like economies of scale and coordination costs (Hui and Tucker, 2023; Bakos et al., 2021). The decentralization of blockchain consensus mechanisms theoretically ensures transaction validity without trusted intermediaries by preventing faults, attacks, and collusion in transaction validation (Buterin, 2017). Beyond ledger integrity, the decentralized consensus of blockchains offers key sociotechnical primitives that are not commonly available in traditional systems and form the basis of the so-called Web3 movement (Dixon, 2021), though risks like the Ronin hack and 51% attacks underscore its fragility (Shanaev et al., 2019; Thurman, 2022).333Some decentralized systems, such as BitTorrent, offer similar primitives but without consensus among distributed nodes, which is a fundamental feature of blockchains.

We define decentralization as the distribution of decision-making authority and control across independent entities. In organizational theory, this emphasizes communication and coordination dispersion, while in computer science and economics, it often refers to how control over infrastructure and governance is spread (Vergne, 2020; Garratt and van Oordt, 2023; Cong et al., 2021). While higher participation can promote greater decentralization (Mueller-Bloch et al., 2024), decentralization is ultimately a question of how power and control are distributed. Thus, we use multiple measures of decentralization to capture meaningful shifts in the decentralization of the consensus layer, not participation alone.

Among the primitives enabled by blockchains, decentralization first reduces or entirely eliminates the role of trusted intermediaries and thus enables trustlessness as a foundational feature. Trustlessness not only allows for secure, direct peer-to-peer transactions but also alternative currencies (which can serve as a financial refuge from economic volatility), ownership records in digital ledgers outside of trusted institutions (from digital art to government bonds),444See Bank (2021). and smart contracts that can both codify and enforce arbitrary rules (Halaburda, 2016; Iansiti and Lakhani, 2017; Ammous, 2018; Cong and He, 2019; Halaburda et al., 2022). Second, decentralization enables participation and innovation without permission from gatekeepers, forming a permissionless ecosystem that fosters open access. Blockchain operators can participate in validation without permission (Cong et al., 2021), and any software developer can build applications on blockchains without permission (Halaburda, 2018). Third, when consensus is decentralized, blockchain data is immutable and censorship-resistant (Nakamoto, 2008; Wahrstätter et al., 2023). Despite the foundational benefits of decentralization, empirical evidence shows significant variation in its application across different blockchains and over time (Gencer et al., 2018; Sai et al., 2021). Given the importance of decentralization to blockchain integrity and the broader potential of decentralized systems, the empirical variations underscore the need to examine the factors driving these variations.

At the theoretical limit, full decentralization is impossible in a permissionless system without an identity management system that gives one vote to each person (Kwon et al., 2019; Bakos et al., 2021). However, even in permissionless systems, Cong and He (2019) and Cong et al. (2022) show that technological innovations that reduce frictions inherent in participation can increase competition in mining and decentralization in automated “oracles” that enable blockchains to seek and append information from off-chain sources. Among many innovations in computing networks more broadly, virtualization stands out as highly relevant and instrumental in reducing friction in deployment, disaster recovery, and operation on heterogeneous physical computing resources (Chowdhury and Boutaba, 2010).

2.2 Virtualization

Technical virtualization refers to the abstraction of physical computing resources, enabling them to be flexibly allocated and managed across different environments (Ameen and Hamo, 2013; Chowdhury and Boutaba, 2010). Rather than eliminating the need for hardware, virtualization enhances its flexibility by decoupling computational processes from specific physical machines. This principle is widely applied in cloud computing, where it supports more flexible resource allocation. Virtualization transforms heterogeneous computing resources into a flexible and unified resource pool, thereby enhancing the agility and scalability of information technology (IT) (Ameen and Hamo, 2013; Shirinbab, 2019).555Not only does virtualization affect IT flexibility for firms, it also influences how consumers use technologies. For example, cloud document editing services, such as Google Docs or Overleaf, allow users to access and collaborate on any document on any computer that has an Internet browser without needing to download applications or set up and maintain LaTeX environments. Server virtualization also improves resource availability (van Cleeff et al., 2009), and these improvements are particularly crucial for systems like the blockchain, where efficiency, flexibility, and availability are key to promoting and sustaining decentralization. While it has been shown that server virtualization has certain negative impacts on network stability and confidentiality (van Cleeff et al., 2009; Wang and Ng, 2010), these effects are largely mitigated on blockchains, which operate with secure cryptography at orders of magnitude less throughput and higher latency than traditional cloud services and are designed to be resilient to network instability. Technical virtualization also enables rapid deployment and flexibility in contexts beyond cloud computing. In manufacturing, for example, the virtualization and decentralization of supply chains transform manufacturing firms into integrated networks that allow them to flexibly alter and rapidly innovate on products (Brettel et al., 2014).

We define resource flexibility as the capacity for resources—such as computational power, storage, or blockchain tokens—to be deployed adaptively in response to changes in operational conditions, thereby reducing the cost of entry and avoiding operational disruption. This flexibility is distinct from resource efficiency: while some blockchains may require higher computational resources, their ability to reallocate these resources in response to shocks is what determines their flexibility, not their absolute efficiency. As virtualization theory illustrates, computing networks, which include blockchains, can achieve more resource flexibility by leveraging technical virtualization. Thus, resource flexibility may explain sustained blockchain decentralization by allowing them to be easily deployed and adaptively managed to shocks to the nodes of the blockchain network. This concept underpins our hypothesis that increased resource flexibility, facilitated by technical virtualization, can contribute to the robust decentralization of blockchain systems, thereby addressing some of the economic challenges such as economies of scale and coordination costs.

To understand the potential role of virtualization in blockchain decentralization, we examine two key contributions of virtualization to decentralization: 1) offering resource flexibility for rapid deployment and disaster recovery, and 2) democratizing participation by reducing barriers to entry. First, virtualization technologies facilitate flexible and rapid node deployment, which is critical for disaster recovery and operational resilience. Virtualization would theoretically allow blockchains to adapt and recover swiftly from disruptions, thereby promoting sustained decentralization. Second, by leveraging diverse computing resources and lowering participation costs, virtualization democratizes access to blockchain networks. In permissionless blockchain networks, it is essential to prevent control concentration and mitigate centralization risks (Hui and Tucker, 2023). These contributions collectively seem to support a more robust, decentralized blockchain ecosystem and motivate our hypothesis to empirically test the role of resource flexibility in responding to policy, infrastructure, and technical shocks.

3 Methodology

3.1 Experimental Setting

We examine three events that represent different dimensions of how resource flexibility influences blockchain decentralization. While the China ban provides a test of mining flexibility under a policy shock, the Hetzner shutdown and Ethereum Merge allow us to explore how infrastructure constraints and technical upgrades, respectively, affect decentralization through varying degrees of resource flexibility. Table 1 outlines the three events, the types of shocks, and the resources used in the consensus mechanisms in the events.

| Event | Type of Shock | Date | Resource | Method |

|---|---|---|---|---|

| China bans crypto | Policy | May 15, 2021 | Hardware | Diff-in-diff |

| mining | (ASIC, GPU) | |||

| Hetzner shuts down | Infrastructure | Nov 2, 2022 | Tokens (SOL) | Synthetic diff-in-diff |

| Solana nodes | ||||

| Ethereum Merge | Technical | Sep 15, 2022 | Hardware (GPU) to | Event study |

| Tokens (ETH) |

China’s ban on crypto mining.

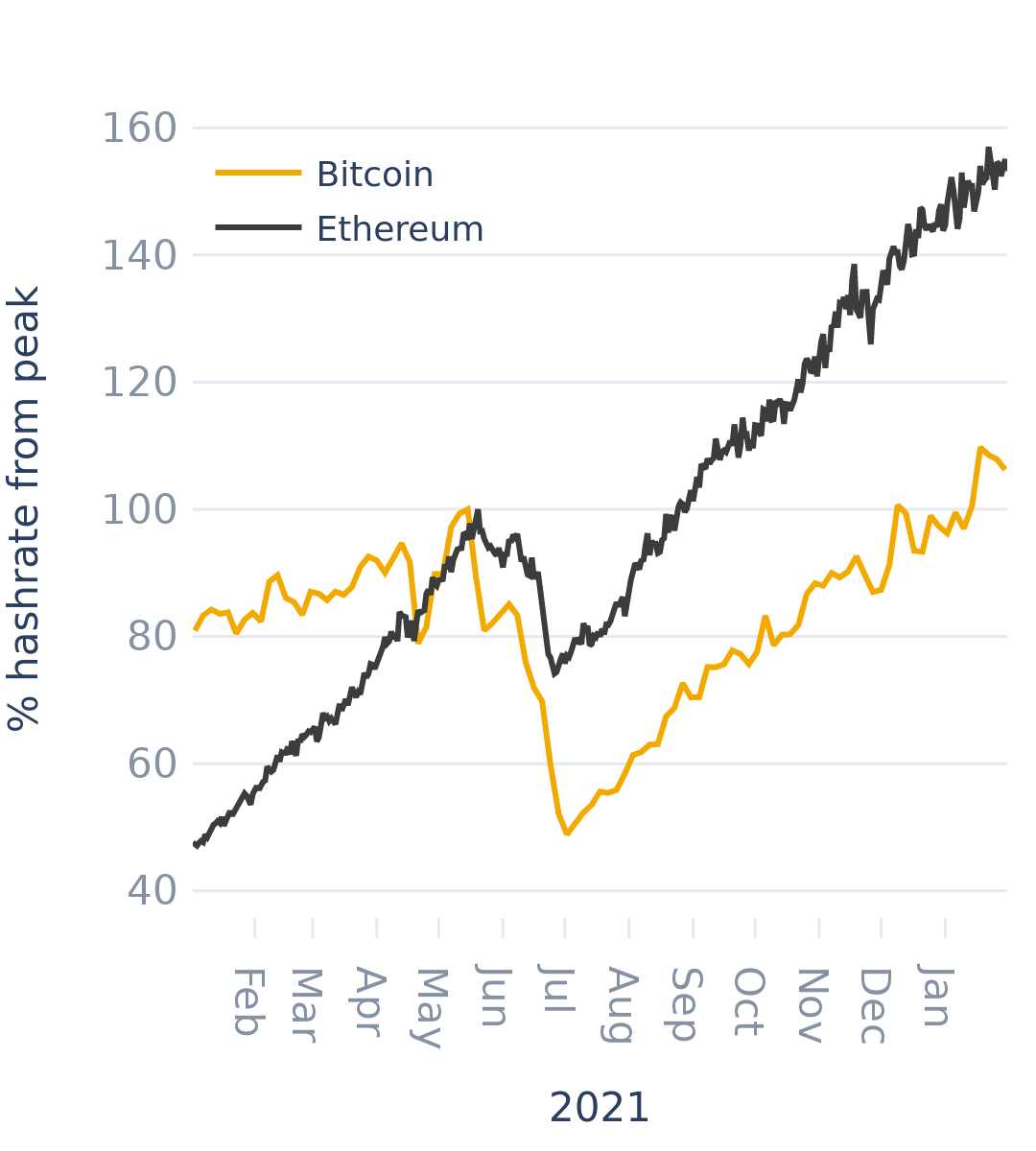

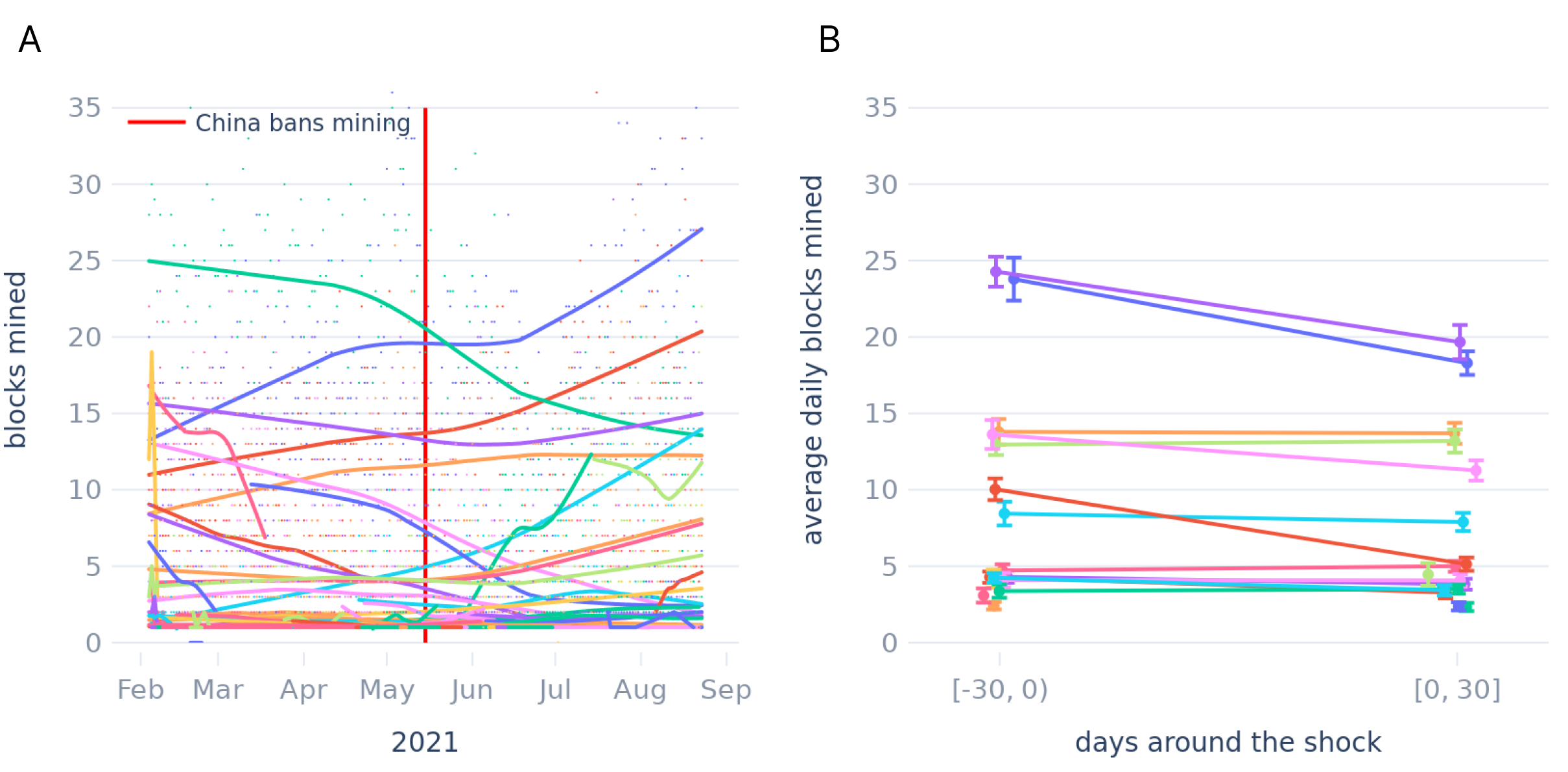

First, we study the policy shock of China’s ban on crypto mining on May 15, 2021, analyzed in Section 4.1 (Shen and Galbraith, 2021). This official Chinese policy established a blanket ban on all mining activities, including Bitcoin and Ethereum, both of which used PoW validation at the time. Both blockchains were relatively mature when the ban was enacted, with Bitcoin online since January 2009, with a market cap of over $809 billion, and Ethereum online since July 2015, with a market cap of $349 billion.666See coingecko.com Accessed August 21, 2023. This policy was a rolling ban starting around May 15, 2021, and enforced by local authorities in the next months (Shen and Galbraith, 2021). While the exact dates of the enforcement are not public, the hashrates dropped to a trough at the start of July 2021 (Figure 2).

While the ban applied to both Bitcoin and Ethereum, the key difference between the chains was the hardware used to achieve consensus, which was directly related to their resource flexibility and, in turn, affected their recovery from the shock. Apart from the hardware requirements, Bitcoin and Ethereum both used PoW for consensus. We use this quasi-experimental variation in the shock to mining for Bitcoin and Ethereum to identify the impact of virtualization in response to a large policy shock on blockchain decentralization. The technical specification underlying the variation was that Bitcoin used (and still uses) the SHA-256 hash function (Nakamoto, 2008) and Ethereum used Ethash.777See a detailed explanation of Ethash on ethereum.org. Accessed October 13, 2023. Bitcoin’s SHA-256 function was primarily mined using application-specific integrated circuits (ASICs), while Ethereum’s Ethash was designed to be ASIC-resistant and thus was mined primarily using graphical processing units (GPUs).\@footnotemark Because ASICs are highly specialized and physically constrained to a single function, they limit adaptability in response to disruptions. In contrast, GPUs are more general-purpose, allowing for greater virtualization—miners could reallocate their computational power dynamically, including leveraging cloud-based resources. Given this variation in the inherent resource flexibility of the technologies supporting the consensus mechanisms underlying Bitcoin and Ethereum, the China ban provides an excellent natural experiment with which to test the impacts of virtualization on blockchain decentralization. For this shock, we analyze data from July 19, 2020, to March 11, 2022.888Note that the Bitcoin halving occurred on May 11, 2020, which does not confound our analysis.

While Bitcoin and Ethereum differ in the types of applications used on them, we focus here on the consensus mechanisms used by the blockchains. Bitcoin was primarily used as a store of value and a medium of exchange, and Ethereum had those and additional use cases, such as decentralized finance and fungible and non-fungible tokens. However, the application layer is largely agnostic to the consensus layer; i.e., the PoW consensus mechanisms, which were used at the time by both blockchains, simply manage the creation of blocks (Nakamoto, 2008; Buterin, 2014). The PoW consensus mechanism secures the network by requiring computational work to add new blocks, indirectly influencing economic incentives such as mining rewards and transaction fees that maintain blockchain functionality and integrity. Importantly, this mechanism is agnostic to the type of data stored in the blocks—whether they are transactional records, smart contracts, or token information—and focuses solely on ensuring data integrity and network security. Thus, the economic incentive structure is equivalent for both Bitcoin and Ethereum apart from the different hash functions and hence the differences in required mining hardware.

Given the focus of our analysis on the consensus layer, we test the robustness of our results with key metrics of the consensus layer in Section C of the Appendix. First, the metrics that capture the computational work to add new blocks include the number of transactions, the amount of data stored, and the estimated hashrates. Next, metrics that capture the indirect economic incentives of mining include the token prices of BTC and ETH, transaction fees, and miner rewards. We find that our results were robust to these potential confounders.

Hetzner’s shutdown of Solana nodes.

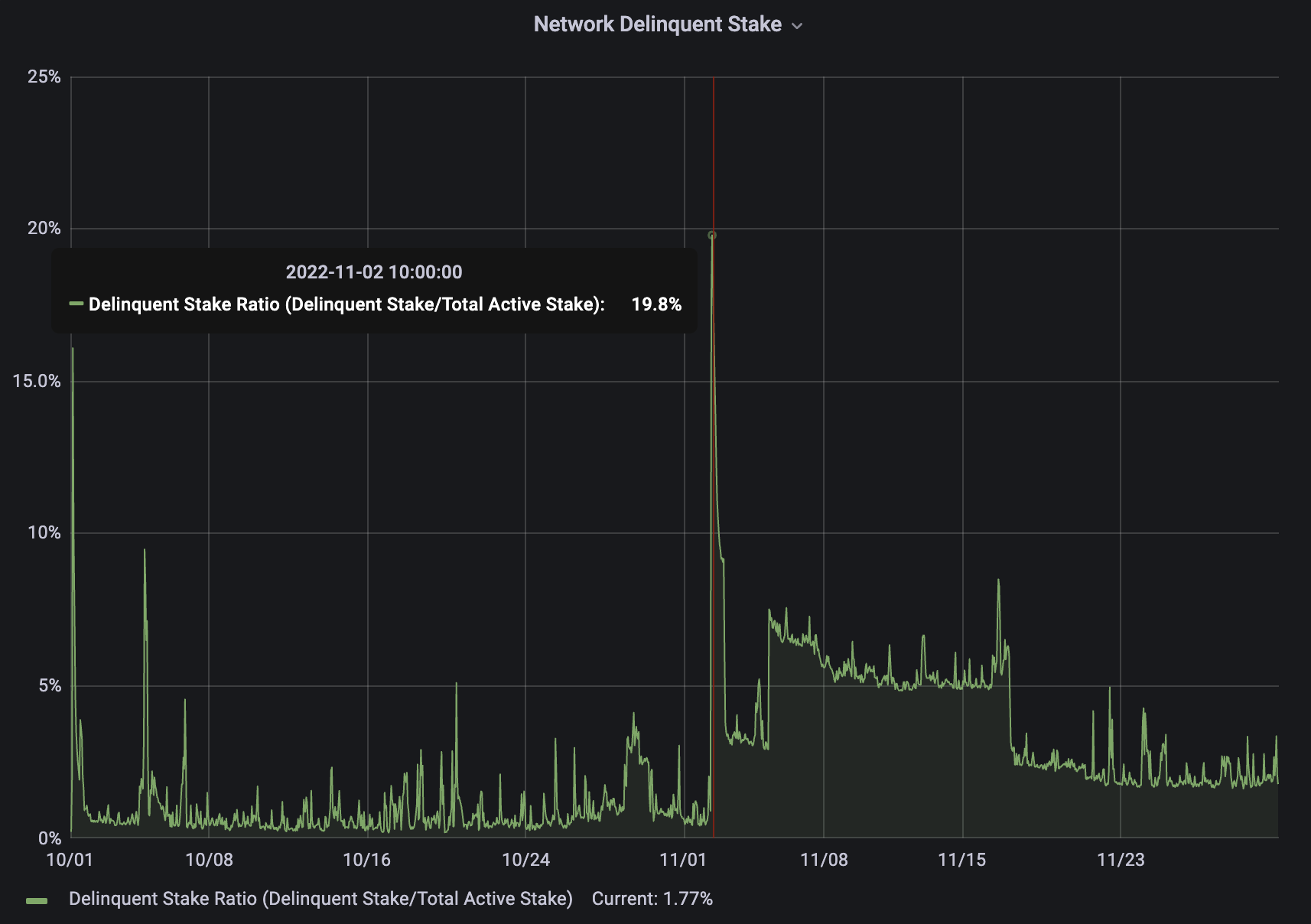

Second, we study Hetzner’s shutdown of Solana nodes on November 2, 2022, as described in Section 4.2 (Avan-Nomayo, 2022). Hetzner is a cloud service provider based in Gunzenhausen, Germany. Operators of PoS validators often run their validators on cloud services because of their ease of deployment, high uptime, and low maintenance. Hetzner, a German cloud service provider, had explicitly prohibited any cryptocurrency-related activities on its platform as of August 23, 2022.999 Hetzner’s official statement: “Using our products for any application related to mining, even remotely related, is not permitted. This includes Ethereum. It includes proof of stake and proof of work and related applications. It includes trading.” See their official statement and X post. Accessed April 14, 2024. Despite this general ban, Hetzner specifically targeted and shut down Solana nodes, while not applying the same measure to other blockchains like Ethereum. On the day of the shutdown, the delinquency rate among Solana validators spiked to 19.8%, indicating that validators representing nearly a fifth of actively staked SOL could not validate.101010RockawayX Solana Dashboard. Accessed August 22, 2023. Hetzner’s shutdown of Solana nodes serves as a test of how infrastructure-level constraints interact with resource flexibility in a proof-of-stake system. Unlike the China ban, which targeted mining hardware, this event highlights how validator decentralization is affected when centralized service providers restrict access, underscoring the role of infrastructure flexibility in blockchain resilience. We leverage synthetic difference-in-difference, using a synthetic control of other PoS blockchains, and event study methods to aid relevant comparisons and support identification. For this shock, we analyzed data from September 13, 2022, to December 22, 2022, 50 days before and after the shock on November 2, 2022.

This selective enforcement by an infrastructure provider represents an exogenous shock to the Solana network, offering a valuable perspective on infrastructure dependency and the risks posed by centralized cloud services to blockchain decentralization. However, the reasons behind Hetzner’s selective enforcement against Solana nodes, as opposed to nodes from other blockchains, remain unexplained by the company. Hetzner’s public communications state a broad prohibition against the use of their services for any crypto-related activities, encompassing both PoW and PoS mechanisms, as well as indirectly related activities such as cryptocurrency trading.\@footnotemark The absence of similar actions against other chains during the same period suggests a potentially unique issue with Solana’s relatively high resource usage that triggered enforcement. For example, Solana nodes require 256GB of RAM, while Ethereum nodes require just 8 GB of RAM.111111See hardware requirements for Solana and Ethereum. Accessed April 14, 2024. If indeed Solana was targeted due to its excessive resource usage, this would support the role of resource efficiency of consensus mechanisms in enabling sustained blockchain decentralization.

The Ethereum Merge.

Third, we study the Ethereum Merge on September 15, 2022, as described in Section 4.3 (The Ethereum Foundation, 2023). The Paris Upgrade, as it is also known, merged Ethereum’s original blockchain with the new PoS consensus mechanism (Beiko, 2022). At that point, each new block was no longer mined by PoW miners but was from then on validated by PoS validators. While in PoW, miners used servers with graphical processing units (GPUs) to mine new blocks through energy-intensive computations, anyone after the PoS upgrade could start validating on any server using 32 ETH. This upgrade is perhaps the biggest technical shock to Ethereum’s consensus mechanism to date. We analyze this shock as an event study to identify the effect of a major software upgrade from PoW to PoS on blockchain decentralization. For this shock, we analyze data from January 1, 2022, to April 1, 2023.

We have a few reasons to believe the exogeneity of the Merge as a technical shock. First, the Merge was a literal merging of Ethereum’s execution layer with a new, external Proof-of-Stake consensus layer, called the Beacon chain, which has been live and rewarding validators since December 1, 2020, but without validating any transactions on Ethereum.121212See more on the Beacon chain on ethereum.org. Accessed April 22, 2024. The Merge simply replaced the Proof-of-Work consensus layer with the existing PoS Beacon chain. The Merge occurred literally in the span of less than 20 seconds and did not require changes to the network before or after the Merge.131313See block 15,537,394 on etherscan.io. Accessed April 22, 2024. Second, while the Merge had been announced in advance, it has been delayed five times since 2017 across five forks: Byzantium in 2017, Muir Glacier in 2020, London in August 2021, Arrow Glacier in December 2021, and finally Gray Glacier in June 2022.141414See the forks of Ethereum on ethereum.org. Accessed April 22, 2024. Third, the Merge was a technical upgrade of nearly unprecedented scale or complexity in the blockchain ecosystem. Together, these factors highlight the difficulty of anticipating any effect on the Ethereum ecosystem on September 15, 2022, by participants.

3.2 Data

We used node-level data from six different blockchains to study the drivers of blockchain decentralization. A blockchain is a linked list of blocks, each containing a list of transactions. A node is a server that operates as a validator in PoS consensus or a miner in PoW consensus. In general, around every seconds, depending on the blockchain specifications, a node produces a block that is appended to the blockchain.

The data we use consists of the daily number of blocks produced by each node. Here, we focus on six blockchains—Bitcoin, Ethereum, Solana, BNB, Ronin, and Gnosis—that facilitate causal identification. Bitcoin, Ethereum, Solana, and Gnosis are all permissionless blockchains in the sense that anyone can operate a node and join the network to produce blocks on the blockchains. However, the four blockchains vary in their designs, which allowed us to tease apart potential drivers of decentralization. Bitcoin is still PoW and uses specialized hardware (i.e., application-specific integrated circuits ASICs) and energy-intensive computations to achieve consensus. Ethereum relied on PoW until September 15, 2022, when it was upgraded to PoS, which uses staked native tokens (i.e., ETH) to achieve consensus. Solana also uses PoS along with Proof-of-History (PoH), which scales transaction throughput while maintaining transaction sequences.151515While important, we do not take into account potential Sybil attacks in our analysis, as no scalable anti-Sybil systems exist for blockchains or are in development (Mohan et al., 2024). See Vitalik Buterin’s blogs on hard problems in cryptocurrency and proof of personhood. Hence, our measures of decentralization are technically the best-case approximations of decentralization. See Section 5.2 for further discussion on Sybil concerns. Gnosis previously used Proof of Authority (PoA) but transitioned to PoS on December 8, 2022.

In contrast to the other chains, Ronin and BNB are permissioned blockchains that have both centrally designated and elected validators.161616Ronin used Proof of Authority (PoA), which has a limited number of validators chosen by a central entity (often a company), but transitioned to Delegated Proof of Stake (DPoS), which has a limited number of elected and centrally designated validators, in April 2023. Importantly, permissioned blockchains can be affected by policy-related or infrastructure-related shocks. Hence, we use the permissioned PoS blockchains as control units for Solana in the analysis of Hetzner’s shutdown (an infrastructure shock) and not for the technical shock of the Ethereum Merge, where permissioned blockchains may be less relevant.

The data for Bitcoin and Ethereum hashrates were obtained from blockchain.com and etherscan.io, respectively. The hashrate is a measure of the collective computing power in a Proof-of-Work blockchain network; specifically, it is the total number of hash functions that all nodes in a network compute per second. While it cannot be directly measured, it is estimated from the number of blocks currently being mined and the current block difficulty. The computational power of an individual node can be affected by gradual hardware degradation, hardware upgrades, changes in efficiency due to electricity or cooling, or, most importantly for our context, changes in the amount of resources used by the node, which can be hash power or blockchain tokens.171717Most crypto miners are profit-maximizing and thus operate at maximum efficiency given the high costs of ASICs and GPUs, even in geographic regions with cheap electricity. See compassmining.io.

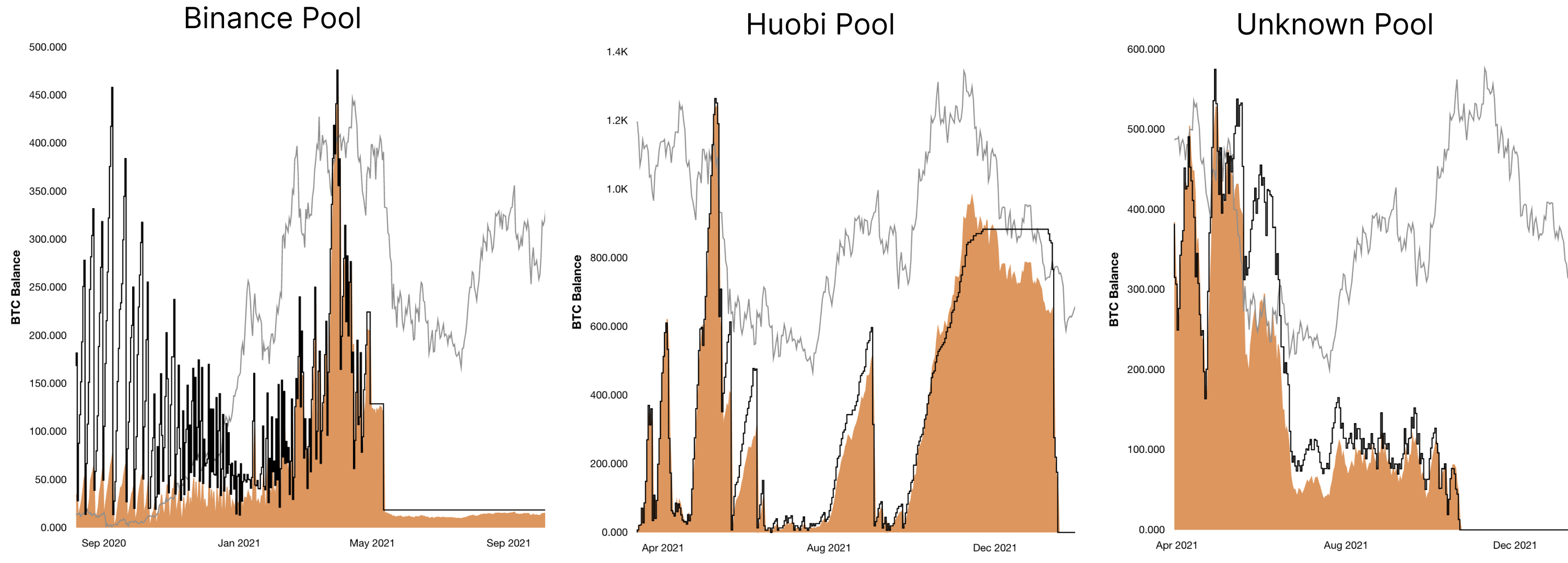

We aggregate daily counts of miners per day for Bitcoin, Ethereum, BNB, Gnosis, and Solana on Dune Analytics (dune.com). Table 2 shows a summary of the blockchains and data used in our study. We obtained the same data for Ronin from Moku (moku.gg). For Bitcoin, we divided the attribution of the block proportionally among the recipients of the block reward to account for mining pools that distribute rewards in the coinbase transaction; for all others, we attributed each block to a single node.181818The coinbase transaction is the first transaction in a block on a blockchain network such as Bitcoin, not to be confused with the eponymous cryptocurrency exchange Coinbase. This transaction is unique because it creates new coins and awards them to the miner who successfully added the block to the blockchain. It also typically includes the distribution of transaction fees collected from other transactions in the block, which are likewise awarded to the miner. In the context of mining pools, the coinbase transaction distributes these rewards proportionally among all pool participants, based on their contributed computational power. For Ethereum, we correct the identification of validators for proposer-builder separation (PBS), as explained further in Section D, thus fully accounting for the coincidence of the implementation of MEV-Boost on the same day as the Ethereum Merge. Further, we report the prevalence of MEV blocks and test for robustness in Section E. In PBS, the builder of a block, who orders the transactions within the block, first receives the block reward and then transfers the block reward to the proposer of the block, which is another name for the validator. Thus, one cannot simply use the block reward recipient data contained in the block and must find the proposer within the transactions of the block.

| Blockchain | Permissionless | Start date | Block time | Number of blocks | Number of nodes |

|---|---|---|---|---|---|

| Bitcoin | yes | Jan 3, 2009 | 10 min | 2,359,386 | 84,017 |

| Ethereum | yes | July 30, 2015 | 13 sec | 17,930,827 | 17,680 |

| Solana | yes | Mar 16, 2020 | 800 ms | 31,372,393 | 3,363 |

| BNB | no | Aug 29, 2020 | 5 sec | 31,372,303 | 60 |

| Gnosis | yes† | Oct 8, 2018 | 3 sec | 30,315,947 | 1168 |

| Ronin | no†† | Jan 25, 2021 | 3 sec | 22,973,856 | 39 |

-

•

†Gnosis upgraded from Proof-of-Authority to Proof-of-Stake in December 2022.

††Ronin upgraded from a Proof-of-Authority to Delegated Proof-of-Stake in April 2023.

3.3 Variable Construction

Decentralization Variables:

We use multiple measures of decentralization for the robustness and interpretability of our estimated effects: Shannon entropy, the number of nodes, the Gini coefficient, the Nakamoto coefficient, and the Herfindahl–Hirschman index (HHI).

We define the measures as follows. The number of nodes, which we refer to as , is simply the number of nodes of blockchain that produced at least one block on day .

Shannon entropy, which we refer to as , is a measure of the unpredictability or randomness in the distribution of blocks among nodes. Formally, it is defined as

where is the set of the number of blocks produced by each node in blockchain on day (Lin et al., 2021; Jia et al., 2022). It has units of bits (as in gigabit) and is bounded by . A higher entropy means more decentralization. Importantly, Shannon entropy captures and can be decomposed into the number of nodes and the distribution of block production over those nodes. The distribution of block production can subsequently be measured by the Gini coefficient, the Nakamoto coefficient, and HHI. Thus, Shannon entropy is a holistic measure of decentralization. An intuition for entropy is that any system with an entropy of (e.g., an entropy of 8) is equivalent in measure to a system with equally contributing entities (e.g., 3 nodes with the same number of blocks validated in a day).

The Gini coefficient is a measure of inequality within a distribution and quantifies the disparity in block production across nodes in blockchain on day . Formally, it is defined as

where and are values from and is the average of all in . It is unitless and is bounded by . A higher Gini coefficient means less decentralization.191919The Gini coefficient can be misleading without also considering the number of nodes. For example, consider the case when there is only one node (e.g., a dictatorship is one-man-one-vote). The Gini coefficient would then be zero, indicating full decentralization, but it is merely “fully equal” for only the single node. Hence, we consider it important to use multiple metrics when possible and Shannon entropy when one requires a single metric to encapsulate both the number of entities and the distribution of power over those entities.

The Nakamoto coefficient measures the minimum number of nodes required to collectively control over 51% of the block production on a given day. Formally, it is defined as

where is the fraction of blocks produced by the node on day (Srinivasan and Lee, 2017). The Nakamoto coefficient is a key measure for assessing the resilience of the blockchain against potential collusion or majority attacks. It has units of nodes and is bounded by . A higher Nakamoto coefficient means more decentralization.202020The threshold to take control over the consensus layer varies by blockchain. For example, Bitcoin requires 51% of the network, while Ethereum and Solana require 66.7%. To simplify our comparative analysis, we used 51% as the threshold for the Nakamoto coefficient.

Finally, indicates the concentration of block production among nodes in blockchain on day . Formally, it is defined as

is calculated as the sum of the squares of individual market shares of all participants. It is unitless and is bounded by . A higher HHI means less decentralization.

Treated Blockchain Variable:

The treated blockchain variable is a binary indicator variable for blockchain . equals one if the observation is from the blockchain that receives the treatment or zero if the observation is from the compared blockchain that does not. For example, in our analysis of China’s mining ban, , and . For simplicity, the tables display as Bitcoin for China’s mining ban and as Solana for Hetzner’s shutdown.

Post-Treatment Variable:

The post-treatment variable is a binary indicator variable for date . It is zero if the observation is before the treatment date and one if the observation is on or after the treatment date.

Treatment Variable:

The variable is the combination of both the post-shock and blockchain variables. It is formulated as the cross-term and is shown as for convenience and clarity. This variable is used to estimate the average treatment effects on the treated (ATT) . For example, in our analysis of China’s mining ban, the coefficient of the treatment variable represents the difference in Bitcoin’s and Ethereum’s entropy after the ban.

Exposure Variable:

China’s mining ban disproportionately impacted Bitcoin’s network compared to Ethereum’s, as evidenced by the drop in hashrates starting at the time of the ban (Figure 2). To control for the difference in exposure to the shock, we included the variable as a covariate in our analysis of China’s mining ban. It is formulated as the cross-term , where is the fractional decrease in the hashrate of blockchain from its peak hashrate at around the time of the ban to the minimum hashrate in the months following the ban.212121Because the exposure lasts for months after the peak, we also perform multi-period difference-in-difference estimation in Section F of the Appendix (Callaway and Sant’Anna, 2021).

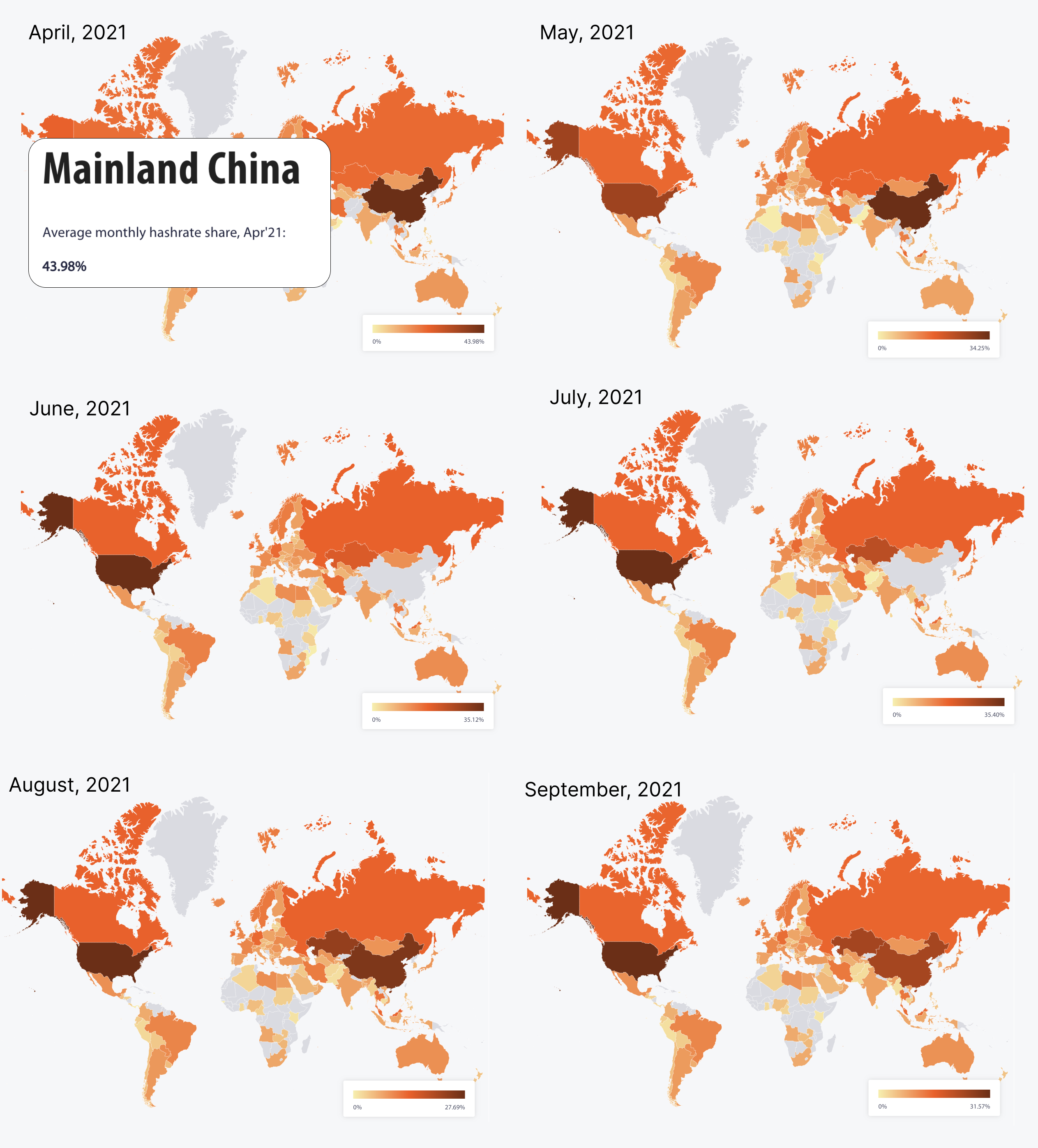

Non-random exposure to exogenous shocks can bias estimates, and methods have been devised to avoid such omitted variable bias (Borusyak and Hull, 2020). These methods involve estimating the expected exposure by simulating the process by which a unit receives the shock and constructing a recentered instrumental variable based on that estimate. Fortunately, we can directly measure the exposure for both Bitcoin and Ethereum by estimating the drawdown of the total daily hashrate from the peak around May 15th (Figure 2).222222This direct measurement is a clear feature of our identification strategy as simulated exposure methods are considerably noisier than directly measured exposure proxies. We find that and , and we use these estimates as control and treatment exposure covariates. We use the date of the peak hashrate for Bitcoin on May 15, 2021, as the date for the shock. As a robustness check, we validate our exposure measures using country-level geographic monthly hashrates for Bitcoin, serving as a proxy for both chains, in Section G of the Appendix.

Time Variable:

The time variable is a running variable used in our event study. It is the number of days after the treatment date and is set to zero at the treatment date.

3.4 Model Specifications

To identify causal effects in our analysis of the three shocks, we employ three empirical methods: difference-in-difference estimation (DiD), synthetic difference-in-difference (SDiD), and an event study.

Difference-in-Difference (DiD) Estimation

We use DiD for the policy shock of China’s mining ban and the infrastructure shock of Hetzner’s shutdown of Solana nodes. The DiD model was specified as follows:

| (1) |

where is a measure of decentralization (i.e., , , , , or ) of blockchain on day and is the error term. Including the exposure variable as a covariate yields:

| (2) |

For China’s ban, the variable is one for Bitcoin and zero for Ethereum. The variable is the cross-term and indicates one for Bitcoin after the ban or zero for Bitcoin before the ban and for Ethereum before and after the ban. For Hetzner’s shutdown of Solana nodes, the variable is one for Solana or zero for the synthetic control, which is explained below. The variable indicates one for Solana after the shutdown or zero for Solana before the shutdown and for the synthetic control before and Post the ban, or simply . The coefficient of the treatment variable represents the difference in the treated chain and control chain following the shock.232323For China’s ban on mining, we perform multi-period difference-in-difference analysis in Section F of the Appendix to account for the months-long exposure to the shock (Callaway and Sant’Anna, 2021).

In addition to estimating the treatment effects before and after the shocks, we aimed to estimate the dynamics of decentralization after the shocks by identifying the leading and lagging treatment effects. In our context, this analysis reveals if the blockchain recovered from the shock and, if so, how quickly. Thus, we modified Equation 1 by summing over the time-shifted treatment effects as specified by

| (3) |

where is the lead and lag effects for and , respectively and is the maximum lead and lag.

Synthetic Difference-in-Difference (SDiD) Estimation

For the infrastructure shock of Hetzner’s shutdown of Solana nodes, Solana exhibited no comparable control due to its unique entropy measures, which were significantly higher than those of other blockchains. Thus, we employ a synthetic difference-in-difference (SDiD) estimation approach using a synthetic control (Arkhangelsky et al., 2021). This control is constructed as a weighted sum of the entropy values from four other Proof-of-Stake blockchains: Ethereum, Gnosis, BNB, and Ronin. The purpose of the synthetic control is to create an optimally estimated counterfactual to Solana’s decentralization scenario in the absence of Hetzner’s shutdown.

The SDiD model is specified as follows:

| (4) |

where represents the decentralization of blockchain at time (see Section 3.3), is the treatment effect of Hetzner’s shutdown on the unit at time , is a binary indicator which equals 1 for Solana post-shutdown and 0 otherwise, is the blockchain fixed effects, and is the error term. To estimate the average treatment effect where the treatment was applied, we calculate as the average of over the observations with . All treated units begin treatment simultaneously. We computed the synthetic DiD estimators using the R package synthdid (Arkhangelsky et al., 2021).

Event Study

We use an event study to estimate the effect of the software shock of the Ethereum Merge and to test the robustness of the difference-in-difference estimation for Hetzner’s shutdown. For the Ethereum Merge, we could not find parallel trends between the decentralization of Ethereum and other blockchains around the event (as this was an Ethereum-only shock). The Event Study model was specified as follows:

| (5) |

where the superscripts, subscripts, and variables are the same as in Equation 1 and explained in Section 3.3. We do not include the subscript in Equation 5 because it is estimated for only a single blockchain at a time.

We use an event study and not regression discontinuity in time to implement this causal estimation strategy because the effect was not localized around a specific time frame. In our case, the running variable, time, only moves forward and does not allow for a local comparison around the event to isolate a causal effect. The effect of the Ethereum Merge was not localized at a specific time frame immediately around the event but was persistent after the event. This made an event study more suitable than regression discontinuity in time for our analysis, as we are capturing both the immediate impact of the Ethereum Merge and the longer-term trends associated with the Ethereum Merge (Hausman and Rapson, 2017).

4 Results

In this section, we present the empirical results quantifying the causal impact of resource flexibility, proxied by differences in blockchain design, on the decentralization of blockchain consensus in response to three shocks—policy, infrastructure, and technical. For each shock, we first present model-free evidence highlighting the pre- and post-shock values of decentralization. Then, we present DiD, SDiD, and event study estimates of the impact of the shock on decentralization. Taken together, the dynamics of the shocks and the comparisons between the three shocks provide strongly suggestive evidence that virtualization plays a role in influencing blockchain decentralization.

4.1 China Bans Crypto Mining

First, we study the effect of resource flexibility on the decentralization of the consensus of Bitcoin versus Ethereum in response to China’s ban on crypto mining on May 15, 2021, as explained in Section 3.1. Figure 3 shows the decentralization of Bitcoin and Ethereum as measured by entropy in bits (as used to measure the quantity of digital information). Since our empirical analyses are based on DiD estimates, they rely on the parallel trends assumption. First, we show visual proof of the parallel trends assumption before the shock in Figure 3. While the entropy measures seem to display some seasonality (perhaps due to varying electricity costs for nodes across geographies), the decentralization metrics are similar in absolute terms as well as parallel in trends.

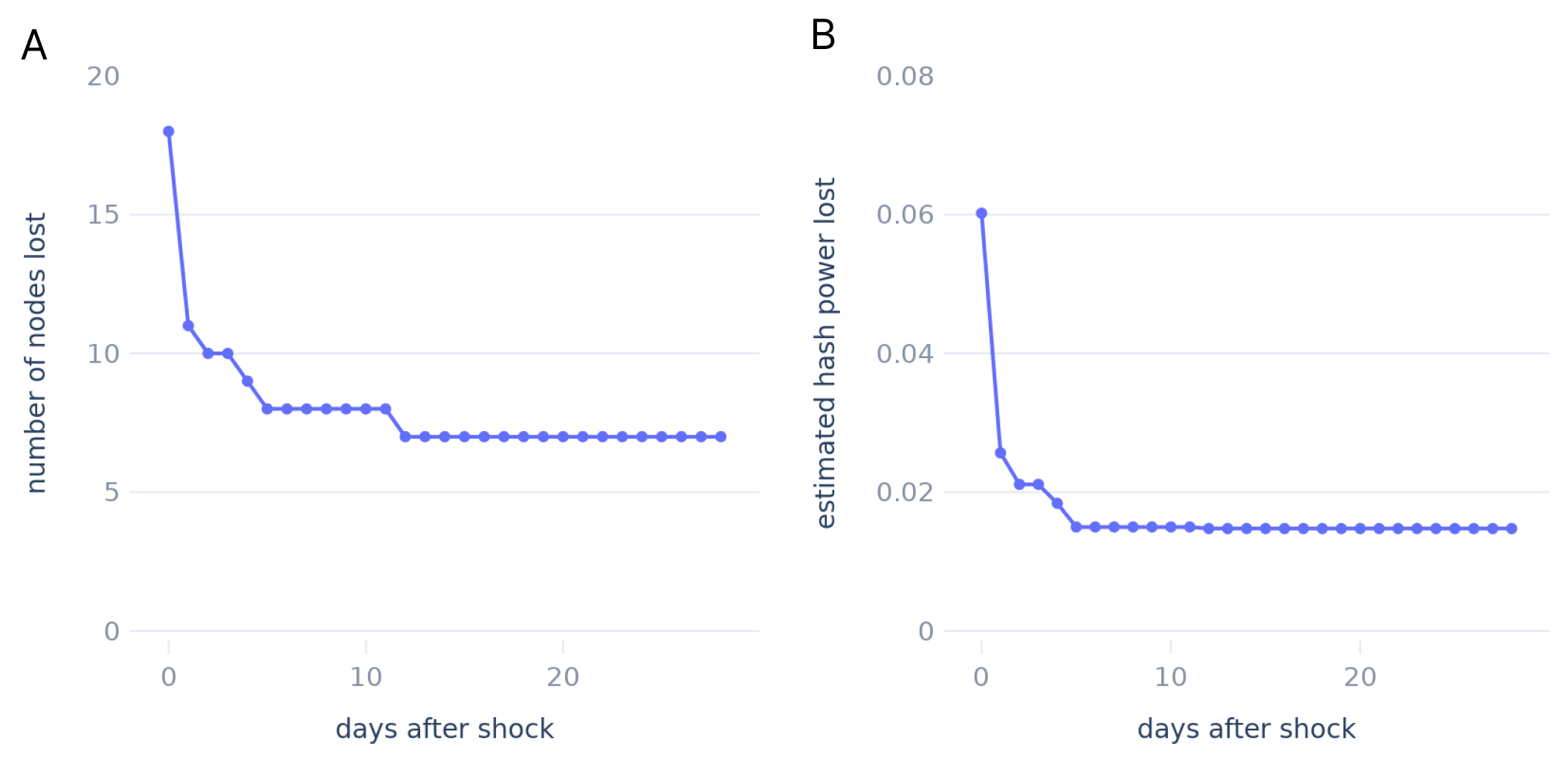

After China’s ban on crypto mining, we observe a significant decline in entropy for Bitcoin over many months (Figure 3). In contrast, we see little to no decline in entropy for Ethereum. To quantify the effect, we analyzed the results of the DiD specifications in Equation 1 to estimate the impact of resource flexibility on decentralization in response to the shock, by using the variation in hardware requirements as a proxy for resource flexibility, as explained in Section 3.1. We denote for simplicity. In our analysis, we find that Bitcoin’s entropy was reduced by 0.209 bits from 3.688 bits (by around 5.7%) before the ban in comparison with Ethereum’s entropy (Table 3). To further explore this effect, we present case studies in Section H of the Appendix where we can observe individual nodes and mining pools known to be based in China that experience declines in block production.

| Dependent | Entropy | Nodes | Gini | Nakamoto | HHI | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| variable | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) |

| Treatment | -0.209∗∗∗ | -0.198∗∗∗ | 5.050∗∗∗ | 5.207∗∗∗ | 0.047∗∗∗ | 0.047∗∗∗ | -0.414∗∗∗ | -0.384∗∗∗ | 0.012∗∗ | 0.011∗∗ |

| (0.054) | (0.052) | (1.319) | (1.293) | (0.010) | (0.010) | (0.105) | (0.103) | (0.004) | (0.004) | |

| Exposure | -0.044∗∗∗ | -0.620∗∗∗ | 0.002 | -0.118∗∗∗ | 0.003∗∗∗ | |||||

| (0.011) | (0.187) | (0.002) | (0.017) | (0.001) | ||||||

| Bitcoin | 0.020 | 0.020 | -33.980∗∗∗ | -33.980∗∗∗ | -0.327∗∗∗ | -0.327∗∗∗ | 1.577∗∗∗ | 1.577∗∗∗ | -0.037∗∗∗ | -0.037∗∗∗ |

| (0.024) | (0.024) | (1.123) | (1.124) | (0.009) | (0.009) | (0.062) | (0.062) | (0.003) | (0.003) | |

| After | 0.014 | 0.025 | -7.663∗∗∗ | -7.503∗∗∗ | -0.036∗∗∗ | -0.037∗∗∗ | -0.111 | -0.080 | 0.001 | 0.001 |

| (0.030) | (0.030) | (1.059) | (1.057) | (0.006) | (0.006) | (0.080) | (0.079) | (0.003) | (0.003) | |

| Intercept | 3.688∗∗∗ | 3.688∗∗∗ | 53.357∗∗∗ | 53.357∗∗∗ | 0.800∗∗∗ | 0.800∗∗∗ | 3.040∗∗∗ | 3.040∗∗∗ | 0.134∗∗∗ | 0.134∗∗∗ |

| (0.047) | (0.047) | (0.808) | (0.809) | (0.007) | (0.007) | (0.083) | (0.083) | (0.003) | (0.003) | |

| Monthly FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 1202 | 1202 | 1202 | 1202 | 1202 | 1202 | 1202 | 1202 | 1202 | 1202 |

-

•

Notes: ∗p0.05; ∗∗p0.01; ∗∗∗p0.001. Standard errors are clustered by blockchain and month. Monthly fixed effects (FE) are included.

It is important to note that Bitcoin and Ethereum experienced different exposures to the mining ban, which could have led to omitted variable bias (Borusyak and Hull, 2020). We therefore controlled for exposure by including the covariate , described by Equation 2. Then, we observed that the magnitude of the effect size for Treatment decreased slightly to while the Exposure covariate saw a small but significant effect of (Table 3, Column 2). The slight decrease in the effect size after controlling for exposure underscores the robustness of our findings, suggesting that the observed decline in Bitcoin’s decentralization is not solely attributable to differences in exposure to the mining ban but also likely influenced by the underlying virtualization characteristics of the blockchain.

We also estimated the effects for the other metrics (Table 3). Surprisingly, we observed that the number of nodes increased for Bitcoin after the shock by around 5 nodes.242424This positive effect on the number of nodes is possibly due to the dissolution of mining pools in China due to the ban. See Section H for case studies of China’s mining pools. Despite the increase in the number of nodes, all other metrics, which measure the distribution of block production among nodes, indicate that Bitcoin became more centralized after the shock. The Gini coefficient increased by 0.047, the Nakamoto coefficient decreased by around 0.414, and HHI increased by 0.012, all of which indicate the post-shock centralization of Bitcoin.252525Note that Gini and HHI are bounded between 0 and 1. The units are in bits for Entropy and nodes for Nodes and Nakamoto. Taken together, the results suggest that the addition of around 5 nodes were nodes with low block production and overall show a significant negative impact of the mining ban on the decentralization of Bitcoin.

4.2 Hetzner Shuts Down Solana Validators

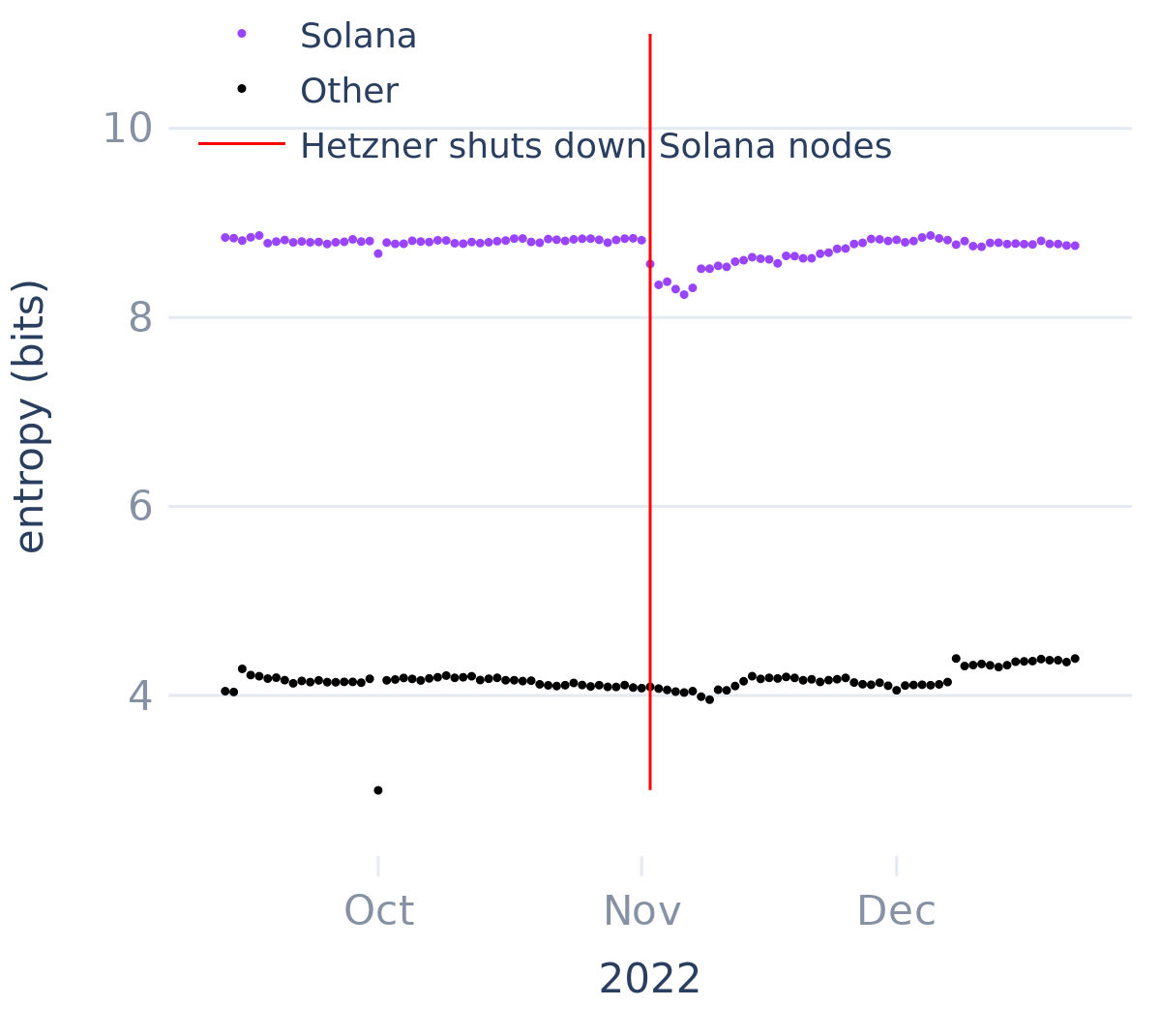

Second, we study the effect of Hetzner shutting down Solana validators on November 2, 2022, on the decentralization of Solana’s consensus mechanism, as explained in Section 3.1. We compare Solana to a synthetic control constructed from a weighted average of the other blockchains which can all experience infrastructure shocks. We note that this difference-in-difference estimation does not estimate the causal effect of virtualization, as does our analysis of China’s mining ban, but the effect of the shock itself on decentralization. As such, we can compare the dynamics of the recovery in blockchain decentralization between this and the previous shock. Figure 4 shows the entropy values of Solana and the synthetic control. Before estimating DiD effects, we visually demonstrate the parallel trends assumption between Solana and the synthetic control by showing the daily entropy of the blockchains over the period before the shock.

On the day of and following Hetzner’s shutdown of Solana validators, we observe an immediate, visible drop in the entropy of Solana. By comparison, we saw no shock to the entropy of the synthetic control. To quantify this effect, we estimate the synthetic difference-in-difference model in Equation 4 with Solana and a synthetic control of four other Proof-of-Stake blockchains. We denote as Solana for clarity. We find that the shutdown reduced 0.345 bits of entropy (around 3.93% from a pre-shock average of 8.787) of Solana ten days before and after the shock, in comparison with the synthetic control (Table 4, Column 1). Then having decomposed the entropy measure into the nodes and measures of the distribution of block production across nodes, we find that around 316 nodes went offline in this period (Table 4, Column 2). This decline was accompanied by an increase in the Gini coefficient of 0.042 and a decrease in the Nakamoto coefficient of -6.105 nodes but no significant change in HHI (Table 4, Columns 3, 4, and 5). These findings demonstrate a substantial negative impact of the infrastructure disruption on the decentralization of Solana.

| Dependent | Entropy | Nodes | Gini | Nakamoto | HHI |

|---|---|---|---|---|---|

| variable | (1) | (2) | (3) | (4) | (5) |

| Treatment | -0.345∗∗∗ | -316.8∗∗∗ | 0.042∗∗∗ | -6.105∗∗∗ | -0.001 |

| (0.090) | (3.8) | (0.006) | (0.064) | (0.005) | |

| Observations | 42 | 42 | 42 | 42 | 42 |

-

•

Notes: ∗p0.05; ∗∗p0.01; ∗∗∗p0.001. Standard errors are derived from placebo tests.

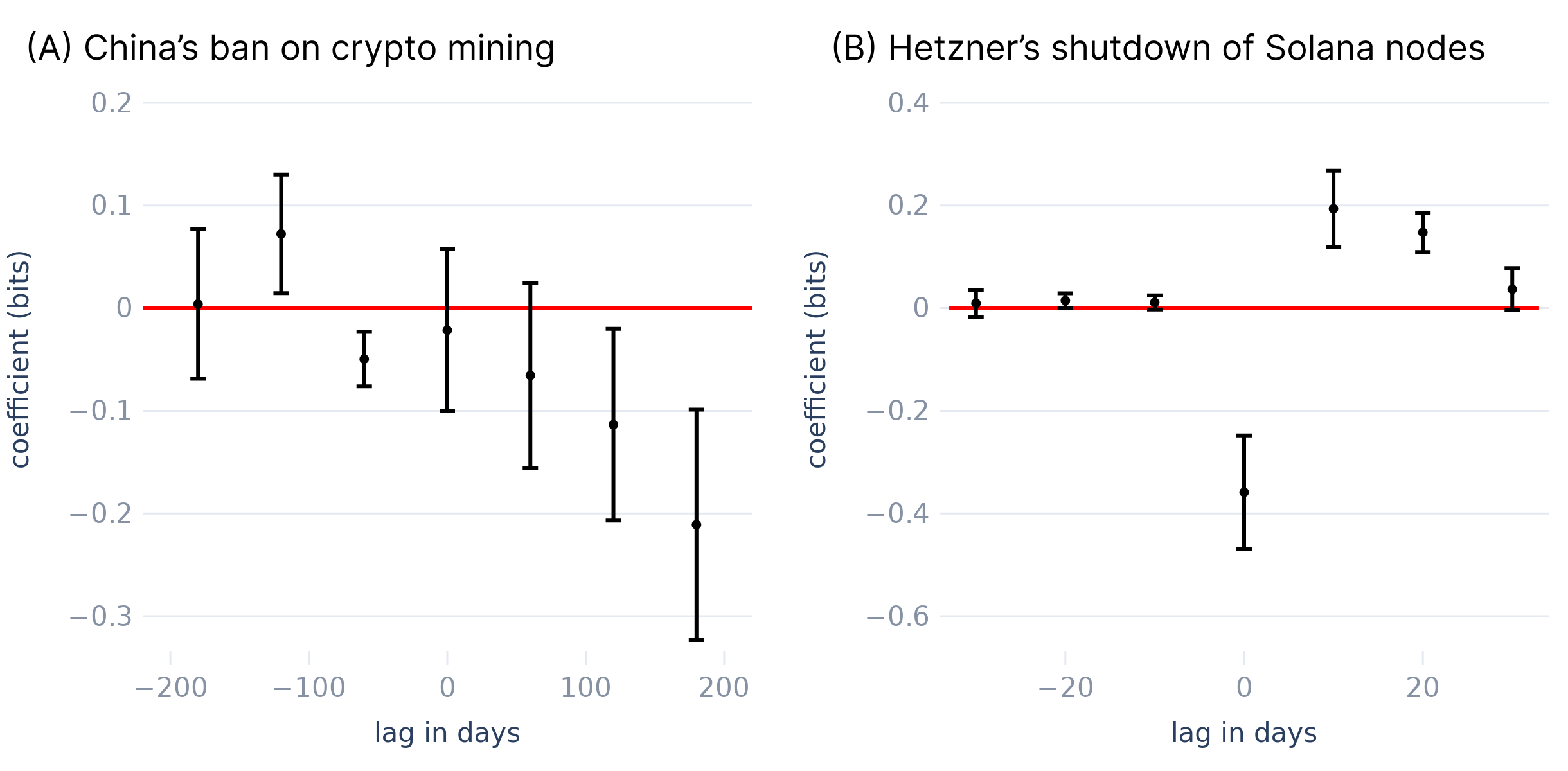

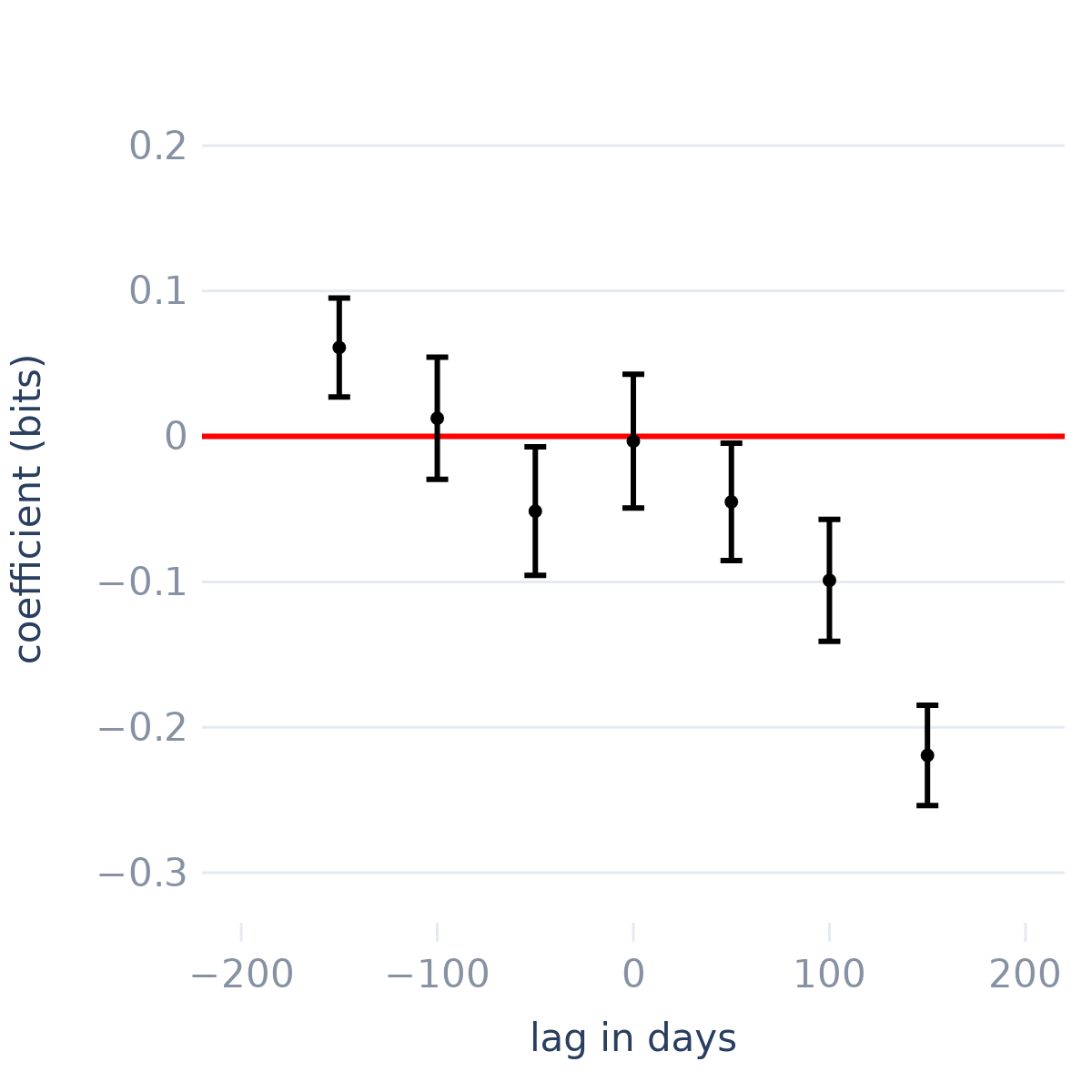

To compare Hetzner’s shutdown to China’s mining ban, we contrast distinct disruptions to examine how resource flexibility shapes decentralization. The China ban constrained mining via policy, while Hetzner’s shutdown was an infrastructure shock affecting validators. This comparison highlights how blockchains with varying resource flexibility respond to external pressures. Indeed, we can observe in Figures 3 and 4 that Bitcoin did not fully recover from the shock in the months following the shock while Solana recovered in a few weeks. To quantify the anticipatory and post-treatment effects of the China ban and the Hetzner shutdown, we estimate lagged effects using Equation 3.262626Note that we used blockchain fixed effects instead of a synthetic control in SDiD since we wanted to estimate multiple treatment effects, unlike in Table 4. In Figure 5, the Hetzner ban reduced Solana’s entropy by 0.359 bits immediately after the shock, but entropy increased in the 40 days following the shock.272727Note that the post-shock positive lagged effects in Figure 5B are measuring the increase in entropy following the initial large dip in response the shock; Table 4 shows the average post-shock effect. In contrast, the treatment lag for the China ban lasts for over 180 days after the shock. The coefficients for all metrics for the China ban and the Hetzner shutdown are displayed in Section I and Section J of the Appendix, respectively. Moreover, for the Hetzner shutdown, we estimate the DiD specification in Equation 1 at 10 to 50 days before and after the shock in Section K of the Appendix. We see that the effect at 50 days is not statistically significant and only 63% of the effect at 10 days. These results highlight the difference in the dynamics of a policy shock on a PoW blockchain versus an infrastructure shock on a PoS blockchain.

To further test robustness, we estimate Equation 5 of Solana’s entropy as an event study which revealed results consistent with our difference-in-difference estimation. Our results, shown in Table 5, demonstrate that the shutdown had a negative effect of 0.344 bits before the shock. All other metrics also show centralizing effects after the shutdown, with the number of nodes decreasing by around 338, the Gini coefficient increasing by 0.028, the Nakamoto coefficient decreasing by -7.919, and HHI increasing by 0.001. Then, the slope of the entropy after the shock is small but positive and significant at bits per day 60 days after the shock. By dividing the shock of 0.344 bits by the positive slope post-shock of 0.008 bits per day, we calculate that Solana took 43 days to fully recover from the shock. These results are again consistent with our DiD estimation.

| Dependent variable | Entropy | Nodes | Gini | Nakamoto | HHI |

|---|---|---|---|---|---|

| After | -0.344∗∗∗ | -338.330∗∗∗ | 0.028∗∗∗ | -7.919∗∗∗ | 0.001∗∗∗ |

| (0.033) | (32.535) | (0.005) | (0.608) | (0.000) | |

| Days | 0.000 | 3.608∗∗∗ | 0.000∗∗∗ | 0.005 | 0.000∗∗ |

| (0.000) | (0.095) | (0.000) | (0.010) | (0.000) | |

| (Days Post) | 0.008∗∗∗ | -1.789 | -0.001∗∗∗ | 0.243∗∗∗ | -0.000∗∗∗ |

| (0.001) | (0.958) | (0.000) | (0.022) | (0.000) | |

| Intercept | 8.812∗∗∗ | 2065.837∗∗∗ | 0.721∗∗∗ | 55.878∗∗∗ | 0.006∗∗∗ |

| (0.006) | (2.595) | (0.001) | (0.237) | (0.000) | |

| Observations | 121 | 121 | 121 | 121 | 121 |

-

•

Notes: ∗p0.05; ∗∗p0.01; ∗∗∗p0.001. Standard errors are clustered by blockchain and month.

The difference in the dynamics of China’s ban and Hetzner’s shutdown can be attributed to two key factors: the first in the nature of the shock and the second in the design of the blockchains. First, China’s ban was a policy ban while Hetzner’s shutdown was an infrastructure shutdown. Policy changes take time to comply with and enforce, especially for distributed networks such as Bitcoin.282828We show more evidence of this rolling ban of Bitcoin miners in Sections F, G, and H of the Appendix. In contrast, Hetzner themselves locked the servers that were validating for Solana.292929See tweets of Hetzner’s notice by @foldfinance and @solblaze_org. Accessed August 23, 2023. So the impact of an infrastructure shock may be more immediate, as we have seen in the data.

Second, Bitcoin and Solana differ in their consensus mechanisms. Bitcoin uses specialized hardware (i.e., application-specific integrated circuits ASICs) and energy-intensive computation to achieve PoW consensus. ASICs are, by definition, specific to Bitcoin mining and are not readily available in other cloud facilities. By comparison, Solana uses staked native tokens, SOL, to achieve PoS consensus. In Solana, one can relatively easily create new validators by transferring their tokens to another cloud server or even a home server.\@footnotemark Our results thus show that the flexibility of resources used in the consensus mechanism—i.e., tokens versus hardware—appears to have reduced frictions in recovering from shocks, suggesting a role in influencing sustained decentralization.

4.3 The Ethereum Merge

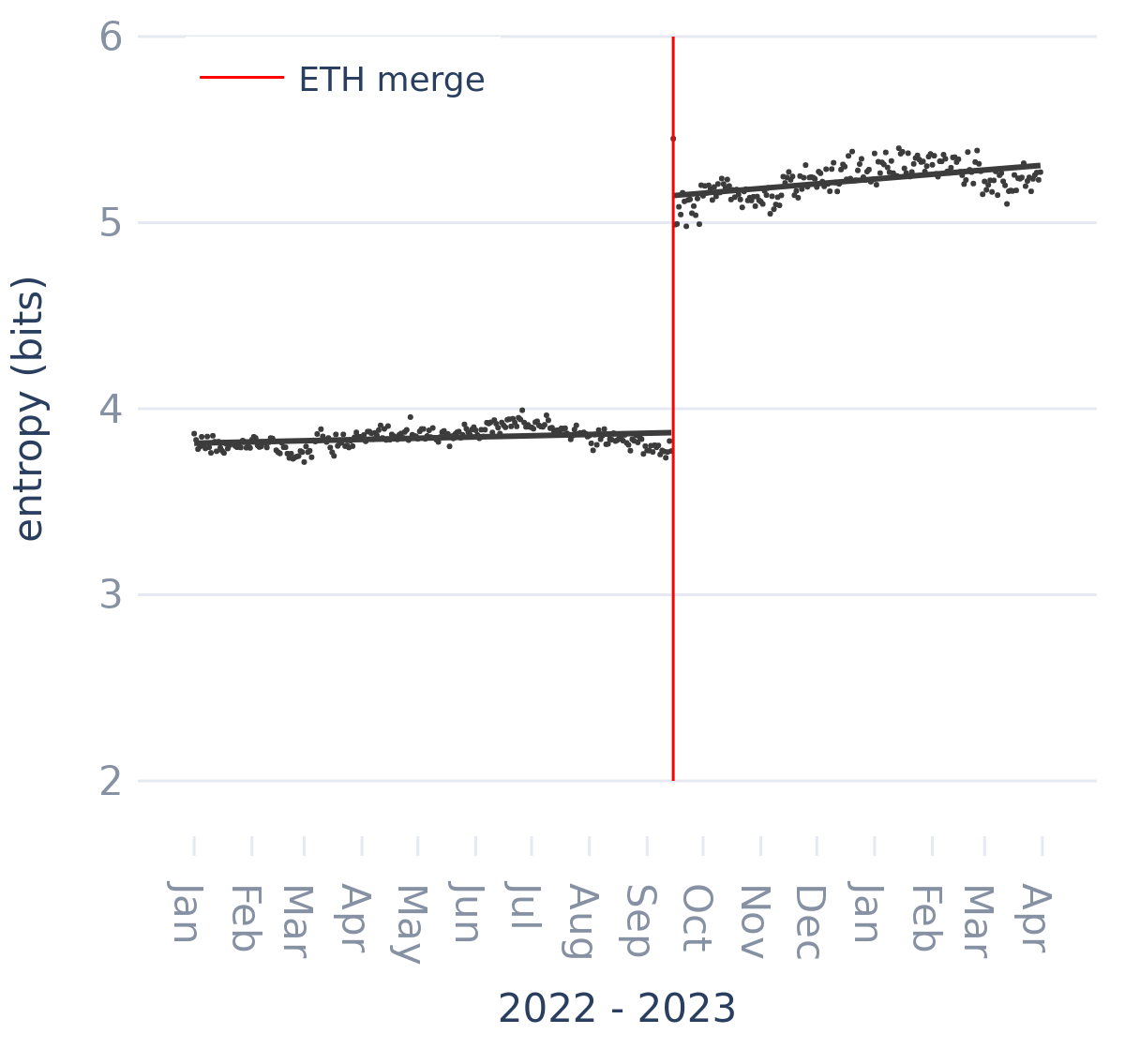

In the two previous natural experiments, we examine the effects of virtualization on decentralization in response to shocks across blockchains that differed in their level of virtualization. In this section, we investigate the effect of a technical upgrade—the Ethereum Merge on September 15—on the decentralization of a single blockchain over time, as explained in Section 3.1. The Merge was a software upgrade that changed Ethereum’s consensus mechanism from PoW to PoS. Thus, the Merge removed the need for physical hardware, thereby making Ethereum more virtualized by definition, and allowed anyone with 32 ETH and even consumer-grade computers to participate in Ethereum’s consensus. By lowering barriers to participation and decoupling consensus from specialized hardware, the Merge exemplifies how increased resource flexibility can contribute to decentralization. Figure 6 shows the entropy of Ethereum’s consensus before and after the shock. Before estimating the effects of the event study, we can visually observe the stepwise increase in both the means and the variance of decentralization specifically at the time of the Merge.

To quantify this impact on Ethereum’s decentralization, we estimate the specification for the Event Study in Equation 5. We find that the Merge increased Ethereum’s decentralization by 1.27 bits of entropy from 3.872 bits (Table 6). This increase in entropy can be attributed to the addition of around 680 new nodes and an increase in the Gini coefficient of 0.088, which indicates a rise in the inequality of the distribution of block production. Interestingly, the analyses show no significant change in the Nakamoto coefficient or the HHI. This implies that the number of nodes that control 51% of the network remained similar despite the increase in the broader base of the network, consisting mainly of smaller new entrants. Despite the insignificant change in Nakamoto and HHI, the overall results add to the evidence that resource flexibility plays a role in influencing decentralization, since PoS, by not relying on hardware for validation unlike PoW, offers a form of virtualization that allows for broader participation. The transition to Proof of Stake (PoS) facilitates an increase in validator numbers due to its lower barriers to entry, which diversifies participation and enhances network entropy.

| Dependent variable | Entropy | Nodes | Gini | Nakamoto | HHI |

|---|---|---|---|---|---|

| After | 1.274∗∗∗ | 679.980∗∗∗ | 0.088∗∗∗ | 0.080 | 0.000 |

| (0.032) | (11.791) | (0.003) | (0.088) | (0.003) | |

| Days | 0.000 | 0.023∗∗∗ | 0.000∗∗∗ | 0.000 | -0.000∗∗ |

| (0.000) | (0.004) | (0.000) | (0.000) | (0.000) | |

| Days Post | 0.001 | 0.213 | -0.000∗∗∗ | 0.000 | 0.000 |

| (0.000) | (0.137) | (0.000) | (0.001) | (0.000) | |

| Intercept | 3.872∗∗∗ | 52.104∗∗∗ | 0.774∗∗∗ | 3.028∗∗∗ | 0.122∗∗∗ |

| (0.030) | (0.617) | (0.002) | (0.026) | (0.003) | |

| Observations | 455 | 455 | 455 | 455 | 455 |

-

•

Notes: ∗p0.05; ∗∗p0.01; ∗∗∗p0.001. Standard errors are clustered by blockchain and month.

5 Discussion and Conclusions

We use data from major blockchain networks to investigate the impact of significant shocks to blockchain consensus decentralization. Specifically, we analyze three policy-related, infrastructure-related, and technical shocks in the blockchain industry, and our findings strongly suggest that resource flexibility plays a significant role in the decentralization dynamics of blockchains and enables sustained blockchain consensus decentralization.

The results indicate a statistically and economically significant influence of resource flexibility on the sustained decentralization of blockchain consensus. The difference is apparent when we juxtapose the time-lagged effects of the natural experiments in Figure 5. The China crypto mining ban led to a notable decline in Bitcoin’s decentralization, while the Hetzner shutdown of Solana nodes illustrated the greater resilience of more resource-flexible consensus mechanisms. Our results suggest that the nature of the shocks, combined with the inherent design of the blockchains, played a crucial role in determining their decentralization trajectories. In particular, Bitcoin, with its reliance on specialized hardware for PoW consensus, faced challenges in adapting to policy shocks, whereas Solana’s PoS mechanism allowed for a more agile response to infrastructure disruptions. While we have robust evidence on the immediate effects of these shocks, further analysis may elucidate the long-term implications and user behaviors in response to these events.

5.1 Implications for Blockchains

Our study provides empirical insights into the factors affecting blockchain decentralization, which informs various stakeholders in the blockchain ecosystem. First, the data suggests that design elements emphasizing resource flexibility are associated with a blockchain’s ability to maintain decentralization in the face of external shocks. However, this flexibility may come with trade-offs in other aspects such as security or efficiency. Second, operational decisions appear to have a measurable impact on a blockchain’s decentralization. These decisions could either enhance or compromise a blockchain’s structural integrity, contingent on its specific design. Lastly, policy decisions targeting blockchains have the potential for broader, systemic effects. Therefore, if the goal is to maintain a balance between innovation and safety, policymakers should consider the unintended consequences of their regulations on the decentralization and overall stability of multiple blockchains.

Blockchain Design

Our study provides empirical evidence that suggests design choices in blockchain architecture have implications for how these systems respond to external shocks. For instance, our data, as shown in Figure 3 and Table 3, indicates that Bitcoin’s decentralization was more adversely affected by China’s crypto mining ban compared to Ethereum’s. This observed difference can be linked to their respective architectural designs; Bitcoin’s reliance on specialized hardware could make it more vulnerable to policy-induced shocks. Conversely, Solana’s quicker recovery after the Hetzner shutdown could be indicative of the benefits of a more virtualized architecture.

Furthermore, alternative design approaches like stateless nodes and blobs could potentially increase participation in blockchain consensus, as suggested by our findings and supported by existing literature (Rustgi, 2023).303030See ethereum.org’s explanation on statelessness and EIP-4844 for details on blobs. Accessed April 15, 2024. Traditional full nodes often require substantial storage and computing power, typically necessitating centralized servers. Stateless nodes, by contrast, could lower these requirements, possibly enabling operation on less powerful devices like smartphones. If the goal is to enhance resilience against external shocks, designs that lower barriers to participation while maintaining the integrity of the system could be considered. For example, our analysis of the Merge shows that despite the increase in network entropy and participation, there remains a concentration of power among the largest validators, highlighting the ongoing challenges in achieving further decentralization. This emphasizes the need for further refinement of consensus mechanisms for further decentralization.

Blockchain Operations

The empirical evidence from the three types of shocks—policy, infrastructure, and technical—provides insights into the operational dynamics of blockchain consensus. In this context, we define blockchain operators as individuals or entities involved in the management of validators, either directly or indirectly, through activities like monitoring, coordination, or infrastructure development (Dunbar, 2023). Our findings indicate that reliance on a limited number of infrastructure providers could expose blockchains to vulnerabilities, as evidenced by the prolonged impact on Bitcoin’s decentralization following China’s ban. This suggests that if resilience against regulatory changes is a priority, operators might consider diversifying their infrastructure across multiple jurisdictions.

Similarly, the recovery dynamics observed in Bitcoin and Solana after the respective shocks point to the role of the consensus mechanism in determining a blockchain’s resilience to external factors. Depending on the consensus mechanism in use, different operational strategies can be more or less effective in mitigating the impact of such shocks. For instance, operators of PoW blockchains might need to consider factors like hardware supply, while those managing PoS blockchains could focus on the geographic distribution of nodes. Monitoring efforts by organizations like the Solana Foundation indicate that ongoing scrutiny of decentralization metrics can provide valuable data for operational decision-making.313131See the Solana Foundation’s March 2023 Report and nakaflow.io. Accessed September 6, 2023.

Blockchain Policy

Our findings indicate that policy changes can exert a significant influence on the level of decentralization in blockchain networks, as evidenced by the significant centralization of Bitcoin in response to China’s policy change (Figure 3, Table 3). This suggests that policymakers should be cognizant of the potential ripple effects that their decisions could have on the blockchain ecosystem, particularly in areas like decentralization and network security. While clear regulatory guidance could facilitate a more stable environment for blockchain-related services, it is important to note that such policies also come with trade-offs that could affect the broader financial ecosystem. As an increasing number of financial assets, including securities and government bonds, are being recorded on blockchains, understanding the implications of policy decisions on both the integrity and the decentralization of these platforms becomes increasingly important. However, it should be noted that the adoption of blockchain for financial assets is still a subject of ongoing debate and scrutiny.

5.2 Limitations and Future Research

While our study offers insights into the dynamics of blockchain design, operations, and policy, there are some limitations to consider. Our biggest limitation is that our analyses are of natural experiments in which we cannot vary just the resource flexibility of different blockchains. To better understand this limitation, we consider alternative hypotheses to ours. First, the type of event varied across shocks, which include policy-related, infrastructure-related, and technical shocks. For example, the lasting effect of China’s mining ban compared to the short-lived effect of Hetzner’s shutdown could be because China’s mining ban was a policy shock and Hetzner’s shutdown was an infrastructure shock. Intuitively, policy changes take days to weeks to implement and months to enforce, whereas infrastructure shocks can occur within days. However, we observe that Ethereum experienced the same shock as Bitcoin, but that Ethereum, whose consensus mechanism was inherently more virtualized and thus more flexible, saw little to no negative effect on its decentralization. Moreover, we perform multi-period difference-in-difference estimation and node-level decomposition in Sections F and H of the Appendix, respectively, to test for robustness of the results at finer resolutions of both time and units, further providing strong evidence for our virtualization hypothesis.

Second, public perception and market sentiment may impact a blockchain’s ability to recover from shocks. Though BTC and ETH prices are highly correlated (see Section L), positive market sentiment may lead to quicker recovery as participants are more likely to reinvest, stake, or engage in the network, thereby bolstering its decentralization and resilience. To test this “market sentiment” hypothesis, we estimate Equation 5 on the price of BTC 60 days around China’s ban, SOL 60 days around Hetzner’s shutdown, and ETH 60 days around the Ethereum Merge. We find that the shocks had either no effect or even negative effects on the cryptocurrencies’ prices, indicating that market sentiment did not facilitate a rapid recovery. The price of BTC hardly dropped around the ban by $1,288.26 from $49,350 (), and the price of SOL and ETH dropped by $7.25 from $30.41 () and by $350.02 from $1686.78 (), respectively. The coefficients for the estimation are displayed in Section M of the Appendix. The zero to negative price effects suggest that, if anything, Bitcoin should have recovered faster than Ethereum or Solana, again suggesting virtualization is the more likely explanation for the decentralization effects we estimated.

Third, Sybil attacks are possible on blockchains, as pseudonymity is a feature of most blockchains. That is, one individual or institution may operate multiple validators or miners. As mentioned previously, we do not take into account potential Sybil attacks in our analysis, as no scalable anti-Sybil systems exist for blockchains.323232See Vitalik Buterin’s blogs on hard problems in cryptocurrency and proof of personhood. Hence, our measures of decentralization are technically the best-case approximations of decentralization. However, substantial Sybil-ing is improbable, especially for the large blockchains that we study here since blockchains, by design, require resources to participate in consensus.33333351% attacks have occurred in the past for some other blockchains. See an article for Ethereum Classic’s 51% attack on August, 2020, on coindesk.com and a report for Bitcoin Gold on January, 2020, on github.com. Accessed April 22, 2024. For Proof-of-Stake blockchains, as an example, Sybil costs are scaled by the market capitalization of the tokens, which are in the trillions to tens of trillions of dollars. Moreover, even if Sybil-ing were present in blockchains, our estimations of treatment effects are unlikely to be affected since Sybil vulnerabilities should be the same across pre- and post-treatment periods and across the treatment and control blockchains. One possible weakness of our event study analysis of the Ethereum Merge is that there may be differences in Sybil-resistance pre- and post-Merge due to slashing penalties. However, ETH transfer fees make Sybil-ing costly and thus should not be a significant concern for our analyses. Ultimately, Sybil vulnerabilities remain an unsolved problem in blockchains but are unlikely to affect our analyses.

Beyond the primary limitation surrounding our hypothesis, our study has some other limitations to consider. First, our research focus on specific aspects of blockchain architecture, such as consensus mechanisms. A comprehensive understanding would require investigating other facets like smart contract design, interoperability, and scalability (Sai et al., 2021; Cong et al., 2022). Second, the quasi-experimental nature of our study might have overlooked potential behavioral patterns of forward-looking blockchain participants or the potential framing effects of initial blockchain adoption phases. Third, our observations do not span the entirety of the vast space of blockchains and their ecosystems, and it is essential to recognize that blockchain ecosystems evolve rapidly. Future research should aim to assess the long-term implications of design choices on blockchain adoption and decentralization. It would be particularly valuable to determine if the observed benefits of certain consensus mechanisms, such as PoS or PoH, remain consistent over extended periods. Fourth, our study mainly centered on well-established blockchains, potentially overlooking the dynamics of emerging or less popular blockchain platforms. We anticipate that future research will address these gaps, further refining our understanding of the virtualization hypothesis, optimal blockchain design, and the effects of blockchain policies in various global contexts.

References

- Ameen and Hamo (2013) Ameen, Radhwan Y., Asmaa Y. Hamo. 2013. Survey of server virtualization. URL http://arxiv.org/abs/1304.3557.

- Ammous (2018) Ammous, Saifedean. 2018. The Bitcoin Standard: The Decentralized Alternative to Central Banking. John Wiley & Sons.

- Arkhangelsky et al. (2021) Arkhangelsky, Dmitry, Susan Athey, David A. Hirshberg, Guido W. Imbens, Stefan Wager. 2021. Synthetic difference-in-differences. American Economic Review 111(12) 4088–4118.

- Avan-Nomayo (2022) Avan-Nomayo, Osato. 2022. 1,000 solana validators go offline as hetzner blocks server access. TheBlock URL https://www.theblock.co/post/182283/1000-solana-validators-go-offline-as-hetzner-blocks-server-access. Accessed: August 21, 2022.

- Bakos et al. (2021) Bakos, Yannis, Hanna Halaburda, Christoph Mueller-Bloch. 2021. When permissioned blockchains deliver more decentralization than permissionless. Commun. ACM 64(2) 20–22. doi:10.1145/3442371.

- Bamakan et al. (2020) Bamakan, Seyed Mojtaba Hosseini, Amirhossein Motavali, Alireza Babaei Bondarti. 2020. A survey of blockchain consensus algorithms performance evaluation criteria. Expert Systems with Applications 154 113385.

- Bank (2021) Bank, European Investment. 2021. Eib issues its first ever digital bond on a public blockchain. URL https://www.eib.org/en/press/all/2021-141-european-investment-bank-eib-issues-its-first-ever-digital-bond-on-a-public-blockchain. Accessed: August 28, 2023.

- Beiko (2022) Beiko, Tim. 2022. Paris upgrade specification. https://github.com/ethereum/execution-specs/blob/master/network-upgrades/mainnet-upgrades/paris.md. GitHub repository.

- Borusyak and Hull (2020) Borusyak, Kirill, Peter Hull. 2020. Non-random exposure to exogenous shocks: Theory and applications. Working Paper 27845, National Bureau of Economic Research. doi:10.3386/w27845. URL http://www.nber.org/papers/w27845.

- Brettel et al. (2014) Brettel, Malte, Niklas Friederichsen, Michael Keller, Marius Rosenberg. 2014. How virtualization, decentralization and network building change the manufacturing landscape: An industry 4.0 perspective. World Academy of Science, Engineering and Technology, International Journal of Mechanical, Aerospace, Industrial, Mechatronic and Manufacturing Engineering 8 37–44.