High-Dimensional Binary Variates: Maximum Likelihood Estimation with Nonstationary Covariates and Factors

Abstract

This paper introduces a high-dimensional binary variate model that accommodates nonstationary covariates and factors, and studies their asymptotic theory. This framework encompasses scenarios where single indices are nonstationary or cointegrated. For nonstationary single indices, the maximum likelihood estimator (MLE) of the coefficients has dual convergence rates and is collectively consistent under the condition , as both the cross-sectional dimension and the time horizon approach infinity. The MLE of all nonstationary factors is consistent when , where depends on the link function. The limiting distributions of the factors depend on time , governed by the convergence of the Hessian matrix to zero. In the case of cointegrated single indices, the MLEs of both factors and coefficients converge at a higher rate of . A distinct feature compared to nonstationary single indices is that the dual rate of convergence of the coefficients increases from to . Moreover, the limiting distributions of the factors do not depend on in the cointegrated case. Monte Carlo simulations verify the accuracy of the estimates. In an empirical application, we analyze jump arrivals in financial markets using this model, extract jump arrival factors, and demonstrate their efficacy in large-cross-section asset pricing.

Keywords: Binary Response; Non-stationary Factors; Maximum Likelihood Estimation; Jump Arrival Factors.

1 Introduction

Since Chamberlain and Rothschild (1983)’s introduction of the linear approximate factor model, factor models have been the focus of extensive research. Seminal contributions include those by Bai (2003), Fan et al. (2013), Pelger (2019), and He et al. (2025). In recent years, attention has increasingly turned toward nonlinear factor models. For example, Chen et al. (2021) developed estimation methods and asymptotic theory for quantile factor models. In particular, considerable works have addressed nonlinear binary factor models, c.f., Chen et al. (2021), Ando et al. (2022), Wang (2022), Ma et al. (2023), and Gao et al. (2023). Binary factor models have diverse applications in fields such as engineering (data compression, visualization, pattern recognition, and machine learning), economics and finance (credit default analysis, macroeconomic forecasting, jump arrival analysis), and biology (gene sequence analysis). However, the aforementioned studies assume that both the factors and covariates are stationary processes—an assumption that may not hold in practice. For instance, daily jump frequencies in financial markets often exhibit aggregation in jump occurrence probabilities (see Bollerslev and Todorov 2011a, b), suggesting nonstationarity, which is also justified in our empirical studies. This paper addresses this gap by investigating a general class of binary factor models where both covariates and factors are generated by integrated processes.

Specifically, consider the following single-index general factor model:

| (1) |

Here, is a -dimensional covariate with coefficient vector , and is an -dimensional factor with factor loading vector . The binary outcome is modeled through a known nonlinear link function (such as logit or probit). Both and are integrated of order one, i.e., processes. It is certainly that can be extended to other types of variate like counts. We consider two cases for the single index , one is nonstationary index and one is cointegrated index. In the nonstationary univariate regression setting (i.e., and ), Park and Phillips (2000) provide the relevant asymptotic theory. However, in high-dimensional settings with a factor structure, the asymptotic properties remain unexplored. Furthermore, when is cointegrated, the associated asymptotic theory is also missing.

This paper develops a theoretical framework for binary factor models with nonstationary covariates and factors, modeled as integrated time series. Specifically, we model the covariates and factors as integrated time series and consider scenarios where the single index is either nonstationary or cointegrated. Our approach builds on earlier work on the asymptotics of nonlinear functions of integrated time series (c.f., Park and Phillips 1999, 2000, 2001; Dong et al. 2016; Zhou et al. 2024) and on MLE methodologies for high-dimensional stationary factor models (c.f., Bai and Li 2012; Chen et al. 2021; Gao et al. 2023; Yuan et al. 2023; Xu et al. 2025). There are also studies involving nonstationary time series in high-dimensional linear models, such as Zhang et al. (2018), Dong et al. (2021), Trapani (2021), and Barigozzi et al. (2024). Our main theoretical contribution lies in establishing the asymptotic properties of the MLEs for both coefficients and factors within the class of general binary factor models.

The findings of this paper are summarized below. In the model (1) with a nonstationary single-index, the convergence rate of the estimated () is characterized by two distinct rates along different axes in a new coordinate system where defines one axis. Along the axis of , the estimated (denoted by ) converges at a rate of , while along axes orthogonal to , it converges at a faster rate of . This dual-rate convergence is consistent with findings in binary regression models, such as the univariate case documented in Park and Phillips (2000). Collectively, exhibits a convergence rate of . The convergence rate of to is , where is determined by the property of the link function. The normalized estimator converges to at a rate of , faster than that of . In the model (1) with a cointegrated single index, the convergence rates of are faster. Along the axis of , the convergence rate improves to , and along axes orthogonal to , it improves to . Consequently, achieves an overall convergence rate of . Moreover, the convergence rate of to is , aligning with conventional estimation rates of factors, as discussed in prior studies (c.f., Bai 2003; Chen et al. 2021; Gao et al. 2023). The normalized estimator converges to at an accelerated rate of , surpassing the convergence rate of . It is worth noting that the asymptotic distributions of the coefficient estimates are significantly different under the cointegrated single index from that under the nonstationary single index.

The modeling framework of this paper has a wide range of applications; we apply it specifically to jump arrival events in financial markets. We find that the model captures well the potential jump arrival factor, which is nonstationary. Additionally, we find that the jump arrival factor effectively explains the asset panel data, which contains information not captured by the Fama–French–Carhart five factors. The jump arrival factor—which benefits from our nonstationary binary model—is effectively applicable in empirical financial asset pricing and is distinct from jump size factors (e.g., li2019jump; Pelger 2020).

The rest of the paper is organized as follows. In Section 2, we introduce the model, outline the underlying assumptions, and describe the estimation procedure. Section 3 presents the asymptotic properties of the proposed estimators. In Section 4, we report Monte Carlo simulation results to assess the accuracy of estimation. Section 5 offers an empirical application of the model, and Section 6 concludes the paper.

Notation. denotes the Euclidean norm of a vector or the Frobenius norm of a matrix. For any matrix with real eigenvalues, let be its largest eigenvalue. Convergence in probability and in distribution are denoted by and , respectively. denotes a mixture normal distribution with conditional covariance matrix . For any function , the notation , , and refer to the first, second, and third derivatives of at , respectively. The indicator function is written as . We write to mean that there exist positive constants and , independent of and , such that . Similarly, means that for some positive . The symbol denotes the Kronecker product. The phrase “w.p.a.1” stands for“ with probability approaching to 1”.

2 Models and Estimation Procedure

2.1 Model Setup

Model (1) can be rewritten in a form equivalent to

The term captures unobserved components of individual ’s utility. The error term is independently and identically distributed (i.i.d.) with distribution function (e.g., standard normal or standard logistic). The dependent variable is latent, and the observed outcome is binary, taking values of either 0 or 1.

In our framework, both the explanatory variable and the factor are nonstationary processes, integrated of order one (denoted as ). We first assume that there exist neighborhoods around the true parameters and such that and always lie within these neighborhoods, ensuring that and remain processes. In Section 3.1, we treat as an process. In Section 3.3, we allow for cointegration between and , i.e., . These two settings encompass both stationary and nonstationary single indices and are broadly applicable.

The assumptions regarding and are outlined below for the subsequent development of the theory.

Assumption 1.

(Integrated Processes)

-

(i)

The covariate series follow and the factor series follow , with initial conditions and , where and are linear processes defined as and , where with the lag operator for , and are nonsingular, and and . Additionally, we assume . The vector are i.i.d. with mean zero and satisfies for some . The distribution of is absolutely continuous with respect to the Lebesgue measure and has a characteristic function such that as for some .

-

(ii)

Define , , and . We assume that there exist -dimensional Brownian motion such that in for all .

These conditions are standard in nonstationary model estimation. In particular, Assumption 1(ii) is widely used in related studies, such as Park and Phillips (2000), Dong et al. (2016), and Trapani (2021). We define .

Assumption 2.

(Covariate Coefficients, Factors, and Factor Loadings)

-

(i)

There exists a positive constant , such that and for all .

-

(ii)

As , , where is a vector of Brownian motions with a positive definite covariance matrix.

-

(iii)

with , and as for , where .

Assumption 2(i) means that the loadings are in compact set. Sufficient conditions for Assumption 2(ii) can be found in Hansen (1992). The assumption of positive definiteness in Assumption 2(ii) precludes cointegration among the components of . Similar assumptions are made in Bai (2004). Assumption 2(iii) is a version of the strong factors assumption, which is commonly used in the literature, such as in Bai (2003) and Chen et al. (2021). The requirement that are distinct is similar to the assumption in Bai (2003), which provides a convenient way to identify and order the factors.

2.2 Estimation Procedure

Let , , , , , , and . Let , , , , and be the true parameters.

Given the stochastic properties of , the log-likelihood function is

| (2) |

Due to the rotational indeterminacy of the factor loadings and the factors , we impose identification constraints, following standard approaches:

| (3) |

The estimators for are then defined as:

| (4) |

Direct optimization of this expression is challenging due to the absence of closed-form solutions for our estimators, unlike in principal component analysis (PCA). To address this, we propose an iterative optimization algorithm.

Define the serial and cross-section averages as

where . The iterative optimization algorithm proceeds as follows:

-

Step 1:

Randomly select the initial parameter .

-

Step 2:

Given , solve for ; given , solve for .

-

Step 3:

Repeat Step 2 until a convergence criterion is met.

-

Step 4:

Let and be the final estimators after the iteration process. Normalize and to satisfy the constraints in (3).

In Step 3, various tolerance conditions can be employed, such as those based on parameter changes or the objective function. In this paper, we terminate the iteration when the change in the objective function is below a threshold , i.e., , where and denote the current and previous values of the log-likelihood function, respectively. In Step 4, we compute

where is a diagonal matrix. We then sort the diagonal elements of in descending order to obtain . Similarly, we sort according to the same order to obtain .

Remark 1.

If the covariate component is absent, the binary probability simplifies to , reducing the model to a pure binary factor model. Although the likelihood function remains non-convex in , the limit of becomes globally convex for each given , and the limit of becomes globally convex for each given . Consequently, these two optimization problems can be efficiently solved, as demonstrated in prior research, e.g., Chen et al. (2021). To illustrate this, consider the logit model. The leading terms in the Hessian matrices are:

where is the logistic function, a nonlinear integrable function of .

When appropriately normalized, the Hessian matrix converges weakly to a random limit matrix, rather than a constant matrix (see Park and Phillips 2000). Additionally, the Hessian matrix may converge to a neighborhood of zero when is large (due to is integrable and outside the effective range of this function), making the consistency of more challenging to ensure. However, when is adjusted with respect to (see Section 3), it also converges weakly to a stochastic limit matrix. Both Hessian matrices are almost surely negative definite, ensuring that the limit functions are globally concave.

3 Main Results

In this section, we delve into the theoretical foundations of the maximum likelihood estimation presented in (4). To facilitate understanding, we introduce the class of regular functions.

Definition 1.

A function is termed regular if it satisfies the following conditions: (i) for some and all ; (ii) ; (iii) is differentiable with a bounded derivative. Let be the set of functions that are bounded and integrable, and be the set of bounded functions that vanish at infinity. Clearly, the inclusions hold.

Next, we define the leading terms in score and Hessian as follows.

For the Logit case, and . For the Probit case, and , where is the probability density function of standard normal variable, and is the cumulative distribution function of the standard normal distribution.

3.1 Theoretical Results for Nonstationary Models

In this subsection, we assume that the process is integrated and of full rank, indicating the absence of cointegrating relationships among its component time series. To develop an asymptotic theory for the estimators defined in (4), we impose several assumptions on the functions , , and .

Assumption 3.

(Function Categories) The function is three times differentiable on . Additionally, the following conditions hold: (i) ; (ii) , , , , ; (iii) , .

These assumptions are mild and are satisfied by common models such as logit and probit. For notational convenience in the subsequent derivations, we define and .

To facilitate the analysis, we introduce block matrices for the score and Hessian. Define , , , and . The score function with respect to is expressed as . The corresponding Hessian is . Similarly, the score function with respect to is , and the Hessian is . The diagonal structure of the Hessian is straightforward to verify. For ,

For ,

Due to the unit root behavior of , its probability mass spreads out in a manner similar to a Lebesgue type. Given that is integrable (as per Assumption 3), outside the effective range of . This indicates that only moderate values of prevent from diminishing. Unlike , the sum varies with time , reflecting the spread of at specific time points. Therefore, to normalize the Hessian appropriately, it is crucial to analyze the convergence behavior of and select a suitable normalizing sequence concerning . Based on this analysis, we introduce the following assumptions.

Assumption 4.

(Integrable Functions)

-

(i)

For a normally distributed random variable , we assume . Additionally, for and .

-

(ii)

The variance as for all .

-

(iii)

For each , as , , where the covariance matrix .

-

(iv)

The sequences satisfy and for some , where .

-

(v)

For functions defined in Assumptions 3(i) and (ii), , where .

Assumption 4(i) is mild. To illustrate its plausibility, simulations (reported in the Supplementary Material) indicate that is approximately 0.5 in both the logit and probit models. Assumption 4(ii) ensures that the sum appropriately utilizes the properties outlined in Assumption 4(i). In the degenerate case, where is independent across and takes moderate values, the variance satisfies . In the stationary case, the in Assumption 4(iii) should be 0. Assumption 4(iv) imposes a constraint on the sample size and the dimensionality. Assumption 4(v) addresses information overflow in the cross-section and therefore requires a slightly stronger condition than Assumption 3.

As is standard, we have the following Taylor expansions.

| (5) |

where denotes the th block of the matrix , and denotes the th block of the matrix . Additionally, is some point between and .

The asymptotic theory for can be derived from Equation (5). To aid in the development of this theory, we rotate the coordinate system based on the true parameter using an orthogonal matrix , where and .111Because estimators converge at different rates in both the parallel and orthogonal directions relative to , performing a rotation enables a more comprehensive theoretical examination. This matrix will be used to rotate all vectors in for . Specifically, we define the following quantities:

In the general case, we define and . With these definitions, we can rewrite the model as . By Assumption 1 and applying the continuous mapping theorem, we obtain the following convergence results for ,

It is important to note that the rotation is not required in practice, and indeed, is conceptually impossible since is unknown. The rotation serves only as a tool for deriving the asymptotic theory for the proposed estimators.

If is the maximum likelihood estimator of , then we have . The score function and Hessian for the parameter can be expressed in terms of as follows: and . Using this relationship, we can derive the following Taylor expansion:

| (6) |

Define , , and .

Assumption 5.

(Covariance) , , , , and are finite, where , , , , with the th block of given by , the th block of given by , and the th block of given by .

Assumption 5 is used to deriving results related to the inverse of the Hessian matrix. It is a mild assumption because both and are diagonal matrices.

We now present the average rate of convergence for and .

Theorem 3.1 shows that the estimator exhibits dual convergence rates.

-

(i)

Along the coordinates parallel to (i.e., ), the average rate of convergence is .

-

(ii)

Along the coordinates orthogonal to (i.e., ), the average rate of convergence is .

For , the rate of convergence depends on , with the difference scaled by . If , the estimators for are consistent. Otherwise, only a subset of are consistent. It is noteworthy that the estimation of becomes less accurate for larger . This is intuitive, as , meaning that the uncertainty increases as grows. To the best of our knowledge, this is the first time such a phenomenon has been observed in the context of factor estimators. The explanation lies in the fact that for larger .

After performing a rotation , we present the convergence rates for in Corollary 3.2 below.

Corollary 3.1 demonstrates the collective consistency of the estimator . The subsequent theorem provides the asymptotic distributions of and .

Theorem 3.2.

The asymptotic behavior of the estimator varies with , influenced by the Hessian matrix. Recall the notation of , two distinct limiting distributions for emerge.

| (7) |

where

with and .

The dual convergence rates presented in Equation (7) are not surprising; similar results have been observed in various problems involving nonlinear functions, such as Park and Phillips (2000) and Dong et al. (2016). This implies that, in multivariate cases (), modest values of significantly influence a nonlinear function along . In contrast, there are no such restrictions on in the direction orthogonal to , allowing larger values of to contribute.

We introduce the normalized estimators and , derived from and . Specifically, . The following corollary characterizes the asymptotic behavior of and .

After normalization, the convergence rate along the direction increases to , while in the orthogonal direction, it remains at . By leveraging the linear relationship between and (and similarly between and ), we can derive the following asymptotic distribution.

Here, the normalization of scales it to the unit sphere, focusing on angular convergence rather than magnitude. Consequently, the convergence rate is accelerated due to the differing rates for . This suggests that imposing the constraint on the binary probability allows to serve as a more precise estimator of .

Estimating binary event probabilities is a crucial aspect of statistical analysis. The following corollary presents the corresponding theoretical result.

Corollary 3.3 indicates that the convergence rate is . If is observable, the convergence rate for is ; If is observable, the rate for is . Therefore, when estimating both parameters simultaneously, the best rate for is the minimum of and .

To extend the previous results to the plug-in version, we first derive estimators for the quantities of interest. According to Theorems 3.2 and 3.3, the estimators and . Based on these distributions, we define two estimators for the inverse Hessian of : and . Similarly, for the inverse Hessian of , we define: and . Specifically, we define the dominant terms for the Hessians as:

where and . The following corollary establishes the consistency of the proposed estimators:

Based on Corollary 3.4 and Slutsky’s theorem, we replace the limiting distribution of in Theorem 3.3 and that of in Theorem 3.2 to obtain the following plug-in version of the limiting distribution:

Next, we provide the local time estimator for :

| (8) |

This estimator is intuitive because, by consistency, . Finally, we define the mean squared error (MSE) for the observations to assess the accuracy of the model estimates:

The following proposition establishes the consistency of the proposed estimators:

The local time estimator in Equation (8) is not unique; it suffices that the nonlinear function within it is integrable and integrates to 1 over . Additionally, serves as an approximation of in (2) (see Gao et al. 2023 for this insight) assessing the model’s goodness of fit.

Remark 2.

When allowing for partial cointegration in —where the cointegration rank is smaller than —in the series , while maintaining the nonstationarity of , similar results can be obtained. For instance, if is stationary for all , the primary characteristics of the model remain largely unchanged, except for and , since continuous to be nonstationary. In this scenario, the local time corresponds to the Brownian motion , rather than , leading to a modification in . To uphold the asymptotic theory under these conditions, it is essential that remains nonstationary and that the cointegration rank of each is less than , thereby ensuring the persistence of dual convergence rates.

3.2 Selecting the Number of Factors

In this section we introduce a rank minimization method to select the number of factors.

Assume is a positive integer larger than . We solve the optimization problem in Equation (4) using factors, resulting in estimators , and . Define . The estimator for the number of factors is then given by

where is a sequence approaching zero as . In other words, counts the number of diagonal elements in that exceed the threshold . To elucidate, decompose into , where comprises the first columns of , and includes the remaining columns. It can be shown that for , and for . Consequently, converges in probability to a matrix with rank at certain rates. By selecting a suitable threshold , which is greater than this rate and less than , we can accurately determine .

3.3 Cointegrated Single Index

In this subsection, we examine the case where a linear cointegration happens among components of for all . In other words for every .

Within this context, we solve the optimization problem in Equation (4) under the assumption that is a -dimensional process and that the single index is . In Remark 3 below, we relax the assumption to accommodate nonstationarity in the single indices for some .

To derive the asymptotic properties of the estimators , we first rotate the coordinate system using a orthogonal matrix , where defines the primary axis. This transformation enables us to express the single index as

where and . In contrast to Section 3.1, here the component is a stationary scalar process, while is a -dimensional nonstationary process. Because the series is concentrated within the effective range of , some aspects of the original asymptotic theory must be revised, and we update the assumptions.

Assumption 6.

(Cointegrated Single Indices)

-

(i)

There exists a set such that belongs to w.p.a.1. Moreover, and .

-

(ii)

, , , , , , and all belong to the class .

-

(iii)

and are nonsingular. has rank and , where . All other conditions remain as in Assumption 1.

-

(iv)

Let be a strictly stationary process that is -mixing over with mixing coefficient satisfying , , and for some .

-

(v)

Assume that and for some positive constant .

-

(vi)

For each , as , , where the covariance matrix .

Assumption 6(i) ensures that the support of is bounded, which is reasonable when is a stationary scalar. Assumption 6(ii) relaxes the function class in Assumption 4. Assumption 6(iii) follows from the requirement only is stationary. Assumptions 6 (iv) and (v) ensure the -mixing for and the boundedness of , such as Trapani (2021).

We first give results for the average rate of convergence and the number of factors under the cointegrated single-index case. Define . The estimation of the number of factors is fully consistent with Section 3.2 except for the choice of thresholds .

Theorem 3.5.

We find that the convergence rates of both the coefficients and the factors are improved, suggesting that estimating the model in the cointegrated single-index case is more accurate. In addition, the threshold selection for the number of estimated factors is less demanding.

We now study the asymptotic distribution of the estimators . Unlike in Section 3.1, where is a nonstationary process, here is stationary. This change may affect the convergence rate of , which lies in the direction of . Similarly, the convergence rate of in the orthogonal direction may also differ. The following theorem addresses these questions.

Theorem 3.6 shows that the convergence rates for and differ from those in Theorem 3.2. Specifically, when the single indices are cointegrated, the convergence rates of the parameter estimators improve, and the asymptotic results resemble those observed in linear models. For , the conventional asymptotics hold, owing to a constant lower bound on for all and .

Rewrite and the inverse matrix , where

Leveraging the linear relationship between and , we can derive the asymptotic results for . The following theorem presents the asymptotic distributions of both and .

The convergence rates of the estimators and , as presented in Theorem 3.7, are influenced by the convergence rates of and , respectively, as detailed in Theorem 3.6. Notably, these convergence rates for and differ markedly from those in Theorem 3.3, primarily due to the impact of cointegration. Consequently, the asymptotic distributions undergo significant alterations.

Remark 3.

In practice, the time series may have both stationary and nonstationary series for different . We can partition the indices into two exclusive sets, and , such that is stationary for and nonstationary for . In this scenario, it is necessary to integrate the asymptotic theories in Sections 3.1 and 3.3.

For the estimators and , the asymptotic distributions remain consistent within their separate sets. However, the estimation of becomes more intricate. When is large, the asymptotic behavior of is predominantly influenced by the stationary components in . While for moderate values of , the asymptotic properties are determined by the combined contributions of both and . Identifying and is not easy, we leave it to our future research works.

4 Simulation

In this section, we perform simulations to verify the accuracy of the estimation results.

4.1 Simulation Design

To do so, we consider a model with the following data generating process (DGP).

-

Case 1.

Non-stationary probabilities: , , with , with , , and . The error term is linked to the binary response via either the logit or probit function. The covariate is observable, while the remaining parameters are unobservable.

-

Case 2.

Cointegrated probabilities: , , with , , , and with , where and represent the th value of and , respectively. As in Case 1, the binary response is modeled using either the logit or probit function. The covariate is observable, while all other parameters remain unobservable.

For each generated dataset, we first determine the number of factors. Then, we evaluate the parameter estimates by measuring the error according to the following criteria, where denotes the number of iterations.

| (9) |

where represents the th replication for . We set the number of simulations to 200.

4.2 Simulation Results

| Nonstationary | Cointegration | |||||||||||||||

| Logit | Probit | Logit | Probit | |||||||||||||

| \ | 100 | 300 | 500 | 100 | 300 | 500 | 100 | 300 | 500 | 100 | 300 | 500 | ||||

| 100 | 1.6985 | 1.9426 | 1.8013 | 1.2055 | 1.1410 | 1.2543 | 1.3652 | 1.4218 | 1.8149 | 1.1323 | 1.6886 | 1.7258 | ||||

| 300 | 1.7983 | 1.9894 | 1.9878 | 1.8142 | 1.9827 | 1.9352 | 1.7935 | 1.9209 | 1.9919 | 1.5960 | 1.9142 | 1.9827 | ||||

| 500 | 1.8030 | 1.9958 | 2.0065 | 1.8930 | 1.9948 | 2.0843 | 1.8428 | 1.9252 | 2.0013 | 1.7025 | 1.924- | 2.0110 | ||||

| MAE 1 | 100 | 0.8970 | 0.5798 | 0.6709 | 5.3008 | 7.8874 | 3.3996 | 2.5923 | 1.7338 | 0.7315 | 1.4395 | 0.5834 | 0.3640 | |||

| 300 | 0.6199 | 0.4216 | 0.4242 | 0.4841 | 0.3922 | 0.4350 | 0.8119 | 0.3842 | 0.3126 | 0.6141 | 0.2840 | 0.2278 | ||||

| 500 | 0.5752 | 0.4016 | 0.3749 | 0.4138 | 0.4053 | 0.3981 | 0.6687 | 0.3827 | 0.2943 | 0.5216 | 0.2721 | 0.2131 | ||||

| MAE 2 | 100 | 0.4975 | 0.3781 | 0.3739 | 0.4672 | 0.6724 | 0.7863 | 0.6519 | 0.3581 | 0.2545 | 0.8636 | 0.4060 | 0.2398 | |||

| 300 | 0.4525 | 0.3511 | 0.4166 | 0.4120 | 0.4145 | 0.6068 | 0.5178 | 0.2584 | 0.1964 | 0.4985 | 0.2033 | 0.1537 | ||||

| 500 | 0.4367 | 0.3256 | 0.3347 | 0.3765 | 0.4612 | 0.4688 | 0.4912 | 0.2524 | 0.1909 | 0.4293 | 0.1972 | 0.1461 | ||||

| MAE 3 | 100 | 0.7428 | 0.4868 | 0.5682 | 5.2045 | 7.8320 | 3.4389 | 2.3198 | 1.6066 | 0.6587 | 1.0169 | 0.4231 | 0.2851 | |||

| 300 | 0.4488 | 0.3740 | 0.4312 | 0.3126 | 0.3646 | 0.5679 | 0.5505 | 0.2768 | 0.2366 | 0.3416 | 0.1944 | 0.1645 | ||||

| 500 | 0.4236 | 0.3187 | 0.3430 | 0.3008 | 0.3901 | 0.4119 | 0.4247 | 0.2726 | 0.2163 | 0.2869 | 0.1763 | 0.1502 | ||||

| MAE 4 | 100 | 0.8308 | 0.3090 | 0.2095 | 0.6284 | 0.3405 | 0.2460 | 0.3611 | 0.1947 | 0.1355 | 0.4901 | 0.2273 | 0.1293 | |||

| 300 | 0.7769 | 0.2802 | 0.2064 | 0.5800 | 0.2443 | 0.2104 | 0.2821 | 0.1367 | 0.1034 | 0.2746 | 0.1081 | 0.0813 | ||||

| 500 | 0.7459 | 0.2762 | 0.1880 | 0.5371 | 0.2526 | 0.1857 | 0.2682 | 0.1350 | 0.1010 | 0.2361 | 0.1062 | 0.0776 | ||||

Table 1 presents the simulation outcomes. We observe that the estimated number of factors is consistent when both and are sufficiently large.

In the nonstationary scenario, when is relatively small, increasing can actually lead to larger errors and less stable results for parameter estimation. This finding aligns with Theorem 3.1, which states that the rate of convergence is ; thus, when is small, a larger decreases the convergence rate.

5 Empirical Application

In this section, we apply our nonstationary binary factor model to high-frequency financial data. By treating daily higher frequency is also possible jumps as binary events and acknowledging that their dynamic is nonstationary (see, for example, Bollerslev and Todorov 2011a and Bollerslev and Todorov 2011b), we extract the corresponding jump arrival factor and incorporate them into our asset pricing framework:

where indicates whether or not asset undergoes jumps on day , with 1 representing presence of jumps and 0 representing absence of jumps.

5.1 Data

We collected intraday observations of S&P 500 index constituents from January 2004 to December 2016.222We used the publicly available database provided by Pelger (2020), which includes 332 constituents; see https://doi.org/10.1111/jofi.12898. Using these high-frequency data, we identify daily jumps with robust detection methods. In particular, we employ the MINRV method proposed by Andersen et al. (2012). Additional results regarding the link function and jump detection methods are provided in the Supplementary Material. We set the confidence level for the jump test as 95%.

Moreover, the overall jump probability (or intensity) trajectory is strongly influenced by volatility (see, for example, Bollerslev and Todorov 2011b). For our covariates, we use the historical volatility of each stock, with daily volatility calculated from high-frequency data.

5.2 Estimation Results

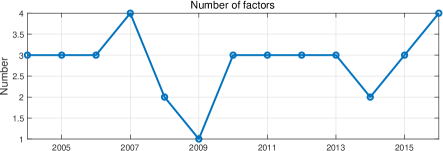

For the period from 2004 to 2016, we estimate three jump arrival factor. To capture dynamic changes, we compute the number of factors for each year, as illustrated in Figure 1.

Figure 1 shows that the number of factors is typically three, increases by one during the financial crisis, and then drops to one afterward.

Since our jump arrival factor captures the relationship between jump events (such as jump arrivals)—akin to the mutually exciting jumps described in Dungey et al. 2018—it differs significantly from the high-frequency continuous factors in Pelger (2020). While Pelger (2020) also constructs jump arrival factors, they rely on sparse jump size data and typically yield only a single factor. In contrast, we extract jump arrival information using a nonlinear factor model that leverages the complete dataset—including both jump occurrence and occurrence rate.

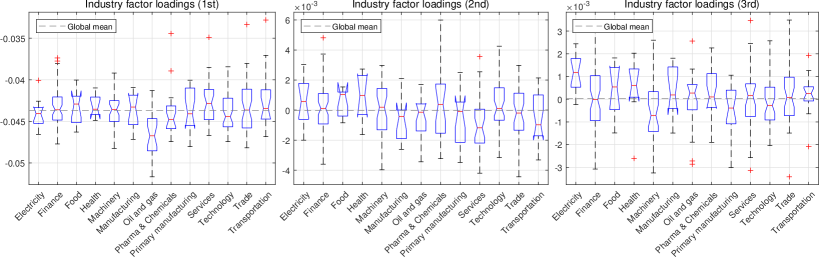

Figure 2 shows the distribution of factor loadings across various industries. Our analysis reveals that the first factor’s loadings are predominantly negative, with particularly large magnitudes for oil industry. In contrast, the second and third factors fluctuate around zero. Unlike Pelger (2020), which finds that the first four continuous factors are dominated by the financial, oil, and electricity sectors, our results indicate that the industry factor loadings contribute more uniformly to the jump arrival factors.

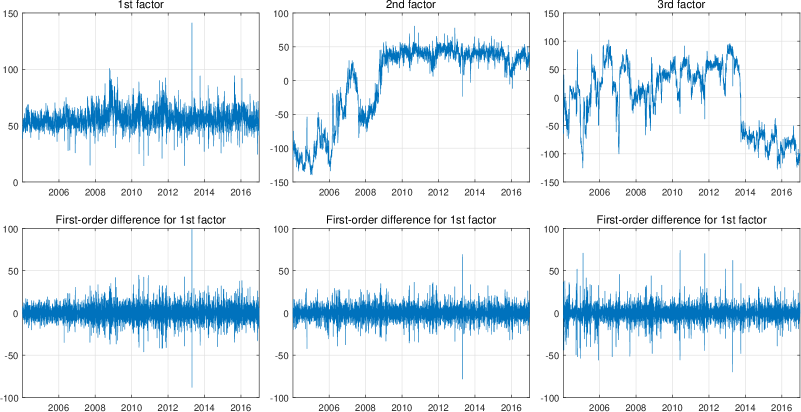

In addition, we show estimation results for the three jump arrival factors, as well as first-order difference results for the factors.

The top panel of Figure 3 displays the three jump arrival factor sequences, which appear to be nonstationary. However, their first-order differences are nearly stationary, aligning well with our model assumptions. To further validate these findings, we conduct an ADF test on the factor series of each year, as presented in Table 2.

| Year | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

| 1st factor | 0.6002 | 0.4890 | 0.4523 | 0.3966 | 0.4905 | 0.3886 | 0.3605 | 0.4488 | 0.4279 | 0.4736 | 0.4722 | 0.3644 | 0.3734 |

| 2nd factor | 0.6082 | 0.4302 | 0.0527 | 0.3833 | 0.1840 | 0.4706 | 0.4682 | 0.5151 | 0.4812 | 0.2984 | 0.4239 | 0.3021 | 0.5256 |

| 3rd factor | 0.0224 | 0.0252 | 0.2689 | 0.1107 | 0.0017 | 0.4234 | 0.2987 | 0.4244 | 0.5268 | 0.3136 | 0.5261 | 0.5718 | 0.5770 |

| 1st factor diff | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 |

| 2nd factor diff | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 |

| 3rd factor diff | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0010 |

Table 2 indicates that the first two factors are nonstationary in every year, while the third factor is nonstationary in almost all years. This confirms that the jump arrival factors are predominantly nonstationary. Furthermore, after applying first-order differencing, all factors pass the stationarity test.

Our model has diverse applications. In finance, for instance, we extract jump arrival factors that can be used to screen portfolios, explain asset pricing, and more. The next section demonstrates how our estimated jump arrival factors help explain excess returns, using asset pricing as an example.

5.3 Applications in Asset Pricing

In this section, we investigate the impact of jump arrival factors on pricing models. We analyze each year separately and choose the maximum number of factors observed across all years (i.e., ) to ensure that variations in the number of factors across periods do not affect the final results.

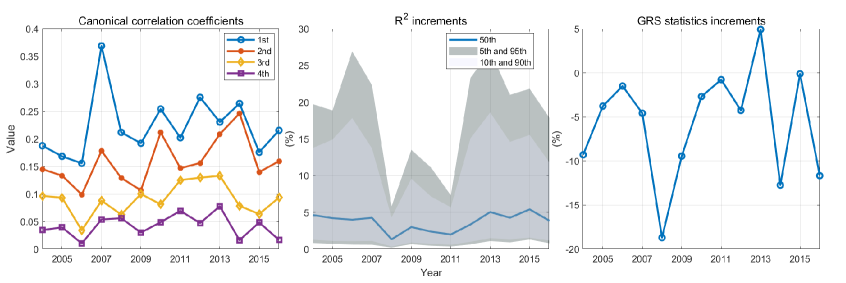

First, to assess whether the identified jump arrival factors can be explained by established financial factors, we compute the canonical correlations between the four jump arrival factors and the Fama–French–Carhart five factors over the entire sample period. The left panel of Figure 4 displays these canonical correlation coefficients.

Figure 4 reveals that most correlation coefficients are relatively low—except for the first coefficient, which shows a modest increase during the financial crisis. This observation suggests that the jump arrival factors are not fully captured by the Fama–French–Carhart five factors.

Motivated by the Fama–French–Carhart five factors model (e.g., Fama and French 2015), we incorporate the jump arrival factors to form the following six-factor model:

| (10) |

where represents the excess return of asset at time (with as the risk-free rate), is the market excess return, captures the size effect, represents the value factor, reflects profitability, measures investment, and denotes the set of jump arrival factors.

We evaluate the contribution of the jump arrival factors from two perspectives. First, by comparing the values from regressions based on the six-factor model (10) and the original Fama–French–Carhart five factors model, we determine whether including the jump arrival factors improves the explanation of excess returns. Second, we test the null hypothesis using the Gibbons–Ross–Shanken (GRS) test to assess the validity of the six-factor model relative to the Fama–French–Carhart five factors model.

The middle panel of Figure 4 plots the annual increases in for all assets. This panel displays the median, as well as the 5th/95th and 10th/90th percentiles of the increments. Larger improvements indicate that the jump arrival factors enhance the model’s ability to explain asset pricing. On average, the inclusion of jump arrival factors results in nearly a improvement in , with some assets exhibiting gains of more than .

Similarly, the right panel of Figure 4 presents the annual changes in the GRS statistic. A lower GRS statistic suggests that the joint alphas are statistically indistinguishable from zero, implying that the model effectively explains excess returns. Negative increments in the GRS statistic indicate that the jump arrival factors enhance the model’s performance. As observed, the GRS statistic decreased in almost every year, reinforcing the effectiveness of the jump arrival factors in explaining asset returns.

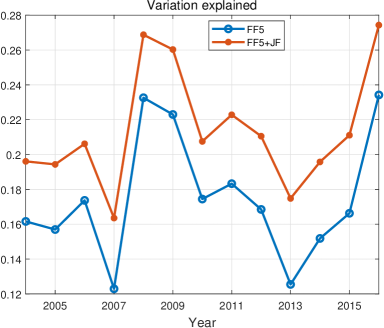

To further demonstrate that the jump arrival factors have incremental explanatory power, we examine how the proportion of variation explained by jump arrival factors varies over time. We adopt the two-stage regression framework of Fama and MacBeth (1973). Figure 5 illustrates the temporal dynamics using local-regression analysis over a rolling one-year window. The addition of jump arrival factors to the Fama–French–Carhart five factors significantly increases the explained variation by nearly 30%.

6 Conclusion

This paper considers a single-index general factor model with integrated covariates and factors, considering two distinct cases: nonstationary and cointegrated single indices. The estimators are obtained via maximum likelihood estimation, and new asymptotic properties have been established. First, the convergence rates differ between the two cases, with an elevated rate when the single index is cointegrated. Second, while the convergence rate for factor estimators depends on time in the nonstationary case—necessitating a larger sample size —but is independent of in the cointegrated case. Third, in a transformed coordinate system, the coefficient estimates exhibit two distinct convergence components. Finally, the limiting distributions of the coefficient estimates are entirely different across the two single-index scenarios. Monte Carlo simulations validate these theoretical results, and empirical studies demonstrate that the extracted nonstationary jump arrival factors play a crucial role in asset pricing. Future research could extend our modelling framework to matrix factor structures, such as Yuan et al. (2023), He et al. (2024), and Xu et al. (2025), or to the high-frequency econometrics, such as Pelger (2019) and Chen et al. (2024).

Supplementary Material

The Supplementary Material contains the proofs of the main theoretical results, additional numerical studies, and more details in the empirical analysis.

References

- Andersen et al. (2012) Andersen, T. G., D. Dobrev, and E. Schaumburg (2012). Jump-robust volatility estimation using nearest neighbor truncation. Journal of Econometrics 169(1), 75–93.

- Ando et al. (2022) Ando, T., J. Bai, and K. Li (2022). Bayesian and maximum likelihood analysis of large-scale panel choice models with unobserved heterogeneity. Journal of Econometrics 230(1), 20–38.

- Bai (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica 71(1), 135–171.

- Bai (2004) Bai, J. (2004). Estimating cross-section common stochastic trends in nonstationary panel data. Journal of Econometrics 122(1), 137–183.

- Bai and Li (2012) Bai, J. and K. Li (2012). Statistical analysis of factor models of high dimension. The Annals of Statistics 40(1), 436–465.

- Barigozzi et al. (2024) Barigozzi, M., G. Cavaliere, and L. Trapani (2024). Inference in heavy-tailed nonstationary multivariate time series. Journal of the American Statistical Association 119(545), 565–581.

- Bollerslev and Todorov (2011a) Bollerslev, T. and V. Todorov (2011a). Estimation of jump tails. Econometrica 79(6), 1727–1783.

- Bollerslev and Todorov (2011b) Bollerslev, T. and V. Todorov (2011b). Tails, fears, and risk premia. The Journal of Finance 66(6), 2165–2211.

- Chamberlain and Rothschild (1983) Chamberlain, G. and M. Rothschild (1983). Arbitrage, factor structure in arbitrage pricing models. Econometrica 51(5), 1281–1304.

- Chen et al. (2024) Chen, D., P. A. Mykland, and L. Zhang (2024). Realized regression with asynchronous and noisy high frequency and high dimensional data. Journal of Econometrics 239(2), 105446.

- Chen et al. (2021) Chen, L., J. J. Dolado, and J. Gonzalo (2021). Quantile factor models. Econometrica 89(2), 875–910.

- Chen et al. (2021) Chen, M., I. Fernández-Val, and M. Weidner (2021). Nonlinear factor models for network and panel data. Journal of Econometrics 220(2), 296–324.

- Dong et al. (2021) Dong, C., J. Gao, and B. Peng (2021). Varying-coefficient panel data models with nonstationarity and partially observed factor structure. Journal of Business & Economic Statistics 39(3), 700–711.

- Dong et al. (2016) Dong, C., J. Gao, and D. B. Tjostheim (2016). Estimation for single-index and partially linear single-index integrated models. Annals of Statistics 44(1), 425–453.

- Dungey et al. (2018) Dungey, M., D. Erdemlioglu, M. Matei, and X. Yang (2018). Testing for mutually exciting jumps and financial flights in high frequency data. Journal of Econometrics 202(1), 18–44.

- Fama and French (2015) Fama, E. F. and K. R. French (2015). A five-factor asset pricing model. Journal of Financial Economics 116(1), 1–22.

- Fama and MacBeth (1973) Fama, E. F. and J. D. MacBeth (1973). Risk, return, and equilibrium: Empirical tests. Journal of Political Economy 81(3), 607–636.

- Fan et al. (2013) Fan, J., Y. Liao, and M. Mincheva (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society Series B: Statistical Methodology 75(4), 603–680.

- Gao et al. (2023) Gao, J., F. Liu, B. Peng, and Y. Yan (2023). Binary response models for heterogeneous panel data with interactive fixed effects. Journal of Econometrics 235(2), 1654–1679.

- Hansen (1992) Hansen, B. E. (1992). Convergence to stochastic integrals for dependent heterogeneous processes. Econometric Theory 8(4), 489–500.

- He et al. (2024) He, Y., Y. Hou, H. Liu, and Y. Wang (2024). Generalized principal component analysis for large-dimensional matrix factor model. arXiv preprint arXiv:2411.06423.

- He et al. (2025) He, Y., L. Li, D. Liu, and W.-X. Zhou (2025). Huber principal component analysis for large-dimensional factor models. Journal of Econometrics 249, 105993.

- Ma et al. (2023) Ma, T. F., F. Wang, and J. Zhu (2023). On generalized latent factor modeling and inference for high-dimensional binomial data. Biometrics 79(3), 2311–2320.

- Park and Phillips (1999) Park, J. Y. and P. C. Phillips (1999). Asymptotics for nonlinear transformations of integrated time series. Econometric Theory 15(3), 269–298.

- Park and Phillips (2000) Park, J. Y. and P. C. Phillips (2000). Nonstationary binary choice. Econometrica 68(5), 1249–1280.

- Park and Phillips (2001) Park, J. Y. and P. C. Phillips (2001). Nonlinear regressions with integrated time series. Econometrica 69(1), 117–161.

- Pelger (2019) Pelger, M. (2019). Large-dimensional factor modeling based on high-frequency observations. Journal of Econometrics 208(1), 23–42.

- Pelger (2020) Pelger, M. (2020). Understanding systematic risk: A high-frequency approach. The Journal of Finance 75(4), 2179–2220.

- Trapani (2018) Trapani, L. (2018). A randomized sequential procedure to determine the number of factors. Journal of the American Statistical Association 113(523), 1341–1349.

- Trapani (2021) Trapani, L. (2021). Inferential theory for heterogeneity and cointegration in large panels. Journal of Econometrics 220(2), 474–503.

- Wang (2022) Wang, F. (2022). Maximum likelihood estimation and inference for high dimensional generalized factor models with application to factor-augmented regressions. Journal of Econometrics 229(1), 180–200.

- Xu et al. (2025) Xu, S., C. Yuan, and J. Guo (2025). Quasi maximum likelihood estimation for large-dimensional matrix factor models. Journal of Business & Economic Statistics 43(2), 439–453.

- Yu et al. (2024) Yu, L., P. Zhao, and W. Zhou (2024). Testing the number of common factors by bootstrapped sample covariance matrix in high-dimensional factor models. Journal of the American Statistical Association, 1–12.

- Yuan et al. (2023) Yuan, C., Z. Gao, X. He, W. Huang, and J. Guo (2023). Two-way dynamic factor models for high-dimensional matrix-valued time series. Journal of the Royal Statistical Society Series B: Statistical Methodology 85(5), 1517–1537.

- Zhang et al. (2018) Zhang, B., G. Pan, and J. Gao (2018). Clt for largest eigenvalues and unit root testing for high-dimensional nonstationary time series. The Annals of Statistics 46(5), 2186–2215.

- Zhou et al. (2024) Zhou, W., J. Gao, D. Harris, and H. Kew (2024). Semi-parametric single-index predictive regression models with cointegrated regressors. Journal of Econometrics 238(1), 105577.