Anonymous

Continuum-armed Bandit Optimization with Pairwise Comparisons

Continuum-armed Bandit Optimization with Batch Pairwise Comparison Oracles

Xiangyu Chang ††thanks: Author names listed in alphabetical order. \AFFDepartment of Information Systems and Intelligence Business, Xi’an Jiaotong University, Xi’an 710049, China \AUTHORXi Chen \AFFStern School of Business, New York University, New York, NY 10012, USA \AUTHORYining Wang \AFFNaveen Jindal School of Management, University of Texas at Dallas, Richardson, TX 75080, USA \AUTHORZhiyi Zeng \AFFDepartment of Information Systems and Intelligence Business, Xi’an Jiaotong University, Xi’an 710049, China

This paper studies a bandit optimization problem where the goal is to maximize a function over periods for some unknown strongly concave function . We consider a new pairwise comparison oracle, where the decision-maker chooses a pair of actions for a consecutive number of periods and then obtains an estimate of . We show that such a pairwise comparison oracle finds important applications to joint pricing and inventory replenishment problems and network revenue management. The challenge in this bandit optimization is twofold. First, the decision-maker not only needs to determine a pair of actions but also a stopping time (i.e., the number of queries based on ). Second, motivated by our inventory application, the estimate of the difference is biased, which is different from existing oracles in stochastic optimization literature. To address these challenges, we first introduce a discretization technique and local polynomial approximation to relate this problem to linear bandits. Then we developed a tournament successive elimination technique to localize the discretized cell and run an interactive batched version of LinUCB algorithm on cells. We establish regret bounds that are optimal up to poly-logarithmic factors. Furthermore, we apply our proposed algorithm and analytical framework to the two operations management problems and obtain results that improve state-of-the-art results in the existing literature.

This version: June 5, 2025

Bandit optimization, inventory control, local polynomial regression, pairwise comparison, regret analysis

1 Introduction

We consider an important question of noisy continuum-armed bandit (CAB) optimization, where the goal is to maximize of an unknown -dimensional smooth function over consecutive time periods, where is a certain convex compact domain. In the standard noisy CAB setting, at each time period an optimization algorithm takes an action and observes a noisy feedback of the function value . In this paper, we study a weaker feedback oracle: the algorithm at each time period should offer two actions , and a noisy evaluation of the difference of the function values will be provided. In this way, the algorithm no longer has noisy evaluation of function values directly, and can only perform optimization by (noisily) comparing two hypothetical solutions and at each time period. A formal definition of the pairwise comparison oracle is given in Sec. 2 later in the paper.

The weaker pairwise comparison oracle is relevant in many business application scenarios in which the direct observation of feedback or rewards is not possible or unbiased. Below we list several important applications of the CAB optimization problem when only pairwise comparison evaluations can be reliably made:

-

1.

Joint pricing and inventory replenishment with censored demand and lost sales. Consider the standard news-vendor inventory control model with a pricing component: at the beginning of review period with an amount of carry-over inventory, the retailer makes a joint price decision and an inventory order-up-to level decision . The instantaneous reward is formulated as

(1) where is a realized demand depending on the price decision . Because the observed demand realization is censored (since the maximum fulfilled demand during review period is at most ), the retailer cannot directly observe the instantaneous reward (the lost-sales part is unobservable). On the other hand, the recent work of Chen et al. (2023) shows that in the censored demand setting, pairwise comparisons or expected rewards between two inventory decisions can still be reliably obtained. In Sec. 5.1 we give a formal description of how the algorithms in this paper can be applied to this important supply chain management problem, with extensions to multiple products too.

-

2.

Network revenue management with non-parametric demand learning. Network Revenue Management (NRM) is a classical problem in operations management. In NRM, the retailer sells types of products over consecutive time periods, by posting a -dimensional vector at the beginning of each time period. The realized demands at time , , depend on the price being posted. The sale of a unit of product type also consumes certain amounts of resources, which have types and the retailer has amount of non-replenishable inventory for resource type initially. The objective for the retailer is to carry out price optimization so that the expected cumulative revenue is maximized, while keeping track of resource inventory constraints because once a resource type is depleted no product that uses that particular resource type could be solved.

The question of NRM, especially its learning-while-doing version in which the demand curve is not known a priori and must be learnt on the fly (which is nicknamed “blind” NRM in many cases), has been studied extensively in the literature (Besbes and Zeevi 2012, Chen et al. 2019). However, when the demand curve is nonparametric, tight regret bounds especially in terms of dependency on the number of products/resource types are challenging; see for example the summary in (Miao and Wang 2021) for a literature survey.

In full-information, offline optimization settings in which is known in advance, the conventional approach when the demand curve is invertible is to optimize the problem with the expected demand rates as optimization variables, leading to an optimization problem with concave objectives and linear constraints. Under the bandit setting, this approach can still be used as showcased in (Miao and Wang 2021), with two additional complexities: 1) the inverse demand curve must be estimated, which introduces bias into the observation of the objective function, and 2) the feasible region must be dealt with in an approximate manner, as the expected demand of a price vector is not exactly known. In this paper, we use the pairwise comparison oracle as an abstraction that captures the first challenge and the aggregated penalty term in Assumption 2.3 and Eq. (2) to capture the second challenge. More technical details are given in Example 2.6 and Sec. 5.2 to cover this example.

1.1 Our contributions

In this paper, focusing on the a weaker pairwise comparison oracle that is intrinsically biased and only consistent when many time periods are involved, we make a number of methodological and theoretical contributions:

-

•

When the objective function is very smooth but not necessarily concave, we propose an algorithm that achieves sub-linear regret. The regret scaling with time horizon also matches existing lower bounds in the simpler setting where unbiased function value observations are available. To achieve such results, our proposed algorithms contain several novel components such as successive tournament eliminations and local polynomial regression with biased pairwise comparisons. Our approach improves on several existing results, including those that apply only to unbiased function value observations or only moderately smooth objectives. We discuss related works in details in the next section.

-

•

When the objective function is moderately smooth and strongly concave, we propose an algorithm to achieve regret, which is a significant improvement compared with the case where the objective function is merely smooth but without additional structures. The proposed algorithm is based on the idea of gradient descent with fixed step sizes. While such an idea looks simple, its implementation must be very carefully designed because only inexact gradients resulting from biased pairwise comparison oracles are available. In our algorithm, we use epochs with geometrically increasing number of time periods for each epoch to properly control the error in inexact gradient estimates, so that when they are coupled together with fixed step sizes the optimal rate of convergence is attained.

In addition to the above contributions specific to the pairwise comparison oracle model, we also connect the oracle model with learning-while-doing problems in important operations management questions, and show that our proposed methods and analysis have the potential to improve existing state-of-the-art results on these problems:

-

•

We mention two important operations management problems: network revenue management and joint pricing and inventory replenishment. We explain how our proposed algorithms could be applied to these problems with carefully designed pairwise comparison oracles, and demonstrate that in both cases, our algorithms and analysis improve existing results in terms of dependency on time horizon when the objective is smoother, or several dimensional factors that are important in problems with many product or resource types.

1.2 Related works

The dueling bandit is a related thread in bandit research that also features observational models involving pairwise comparisons of two arms. Yue et al. (2012) pioneered this line of research, studying a bandit problem with finite number of arms under strong stochastic transitivity assumptions. The works of Urvoy et al. (2013), Saha and Gaillard (2022), Saha et al. (2021), Dud´ık et al. (2015) extended the dueling bandit model to pure-exploration, gap-dependent, adversarial and/or contextual settings, retaining a finite number of arms/actions. Sui et al. (2018) provides a survey of results in this direction. The works of Argarwal et al. (2022), Agarwal et al. (2022) studied batched dueling bandit problems, which remotely resemble our setting where many time periods must be devoted to extract meaningful pairwise comparison signals. (Argarwal et al. 2022, Agarwal et al. 2022) nevertheless adopt feedback models different from our biased pairwise comparison oracle, and focus exclusively on multi-armed bandit settings. It should be pointed out that very few existing works on dueling bandit allows for an infinite number of actions (see next paragraph for some exceptions), or adopts a flexible budget of time periods devoted to each query, with consistency only achieved over many time periods and a single time period being not informative (see e.g. Definition 2.1).

Our research is also connected with the literature on continuum-armed bandit, involving an infinite (in fact, uncountable) number of arms with non-parametric reward functions. In the classical setting of continuum-armed bandit, every time period a single action is taken, and an unbiased reward observation is received. Agrawal (1995) pioneered the research in this area, with extensive follow-up studies in (Bubeck et al. 2011, Locatelli and Carpentier 2018, Wang et al. 2019) focusing on adaptivity and optimality. The work of (Kumagai 2017) studies dueling bandit settings for continuum-armed bandit. Compared to our settings, the work of Kumagai (2017) assumes the probability of seeing a binary output is closely related to the difference between function values at two actions being compared against, which is a special case of our comparison oracle and cannot be applied to our studied OM problems that only deliver consistent comparisons with a large number of time periods.

Two important contributions this paper make are to apply the algorithmic framework (together with its analysis) to important operations management problems to obtain improved results. Here we review related works specific to the operations management applications studied in this paper, and compare them with results obtained in this paper:

Note: references: HR09 (Huh and Rusmevichientong 2009); YLS21 (Yuan et al. 2021); CWZ23 (Chen et al. 2023); CSWZ22 (Chen et al. 2022).

denotes the number of produces whose inventory and pricing are managed.

In all regret bounds, polynomial dependency on and other problem parameters other than time horizon is dropped.

| pricing model | demand censoring | fixed costs | upper bound | lower bound | |

| HR09 | None | Yes | No | N/A | |

| YLS21 | None | Yes | Yes | N/A | |

| CSWZ22 | parametric | No | Yes | N/A | |

| CWZ23 | non-parametric | Yes | No | ||

| This paper | non-parametric | Yes | No |

When demand distribution is equipped with a PDF that is uniformly bounded away from below, the regret upper bound could be improved to . Such improvement cannot happen when there is a pricing model with at least two parameters, as established in (Broder and Rusmevichientong 2012).

Applicable to only.

Not proved in this paper but obtained by invoking existing lower bound results (Wang et al. 2019).

-

•

Joint pricing and inventory management with demand learning. Table 1 summarizes the most related existing results on joint pricing and inventory management with demand learning. Compared with these results, application of the proposed algorithm and analytical frameworks in this paper yields improved regret bounds for smoother pricing functions in with . (The case of would reduce to the regret upper bound obtained in (Chen et al. 2023).)

In addition to the works listed in Table 1, other related works on joint pricing and inventory control with demand learning include (Katehakis et al. 2020, Chen et al. 2021) focusing on specialized settings/algorithms such as discrete demands/inventory inflating policies. We also remark that, as far as we know, there has been no works formally analyzing the problem when both censored demands and fixed ordering costs are present (corresponding to two “Yes” in columns 3 and 4 of Table 1), which would be an interesting future research direction to pursue. More broadly, the problem originates from the studies of Chen and Simchi-Levi (2004a, b), Huh and Janakiraman (2008), Petruzzi and Dada (1999), Chen and Simchi-Levi (2012) focusing primarily on full-information settings.

-

•

Blind network revenue management (NRM). Table 2 summarizes the most related existing results on blind network revenue management. Compared with these results, applications of our porposed algorithms and anlytical framework yields improved regret upper bounds. More specifically, compared with the most related work of Chen et al. (2023) (CWZ23), our obtained regret bounds impose the same set of assumptions and achieve the same asymptotic rate of , but has much improved dependency on the number of product/resource types, improving a factor of to in the dominating regret terms. Other results summarized in Table 1 either impose stronger assumptions on the demand function (parametric assumptions or very smooth non-parametric assumptions, with ), or achieve weaker regret upper bounds such as or for any .

Table 2: Summary of results on blind network revenue management. Additional references are given in the main text. Note: references: BZ12 (Besbes and Zeevi 2012); FSW18 (Ferreira et al. 2018); CJD19 (Chen et al. 2019); MWZ21 (Miao et al. 2021), MW21 (Miao and Wang 2021). denotes the number of product types, which is also the dimension of pricing vectors offered to customers at each time period. In all regret bounds, polynomial dependency on problem parameters other than time horizon or is dropped. refers to the expected revenue as a function of demand rates.

demand model assumptions upper bound lower bound BZ12 non-parametric, , FSW18 parametric * N/A CJD19 non-parametric, , N/A MWZ21 parametric N/A MW21 non-parametric, N/A This paper non-parametric, Bayesian regret and finite numbe () of price candidates.

Hiding additional terms depending polynomially on and growing slower than .

Not proved in this paper but obtained by invoking lower bound results in existing literature (Agarwal et al. 2010).

In addition to works summarized in Table 2, other relevant works include (Wang et al. 2014, Besbes and Zeevi 2009, Wang et al. 2021, Besbes and Zeevi 2015, Cheung et al. 2017, Nambiar et al. 2019, Bu et al. 2022) studying simplified or variants of the NRM model, such as multi-modal demand functions, power of linear models, model mis-specification and incorporation of offline data. More broadly, the problem originates from the seminal works of Gallego and van Ryzin (1994) analyzing optimal dynamic pricing strategies and fixed-price heuristics with stochastic, multi-period demands.

2 Problem formulation and assumptions

2.1 The pairwise comparison oracle

We first give a formal definition of the pairwise comparison oracle that will be studied in this paper. To ensure smooth applications to important OM and business questions, we will state the comparison oracle in full technical generality so that the results derived in this paper are as general as possible.

Definition 2.1

A pairwise comparison oracle associated with an underlying function is -consistent if the following holds: for any , , , the oracle consumes time periods and returns an estimate that satisfies

In Definition 2.1, we define a pairwise comparison oracle that can be used to indirectly obtain information about an unknown objective functrion that is to be optimized. This oracle is in general biased, only conferring meaning information of when invoked with a sufficiently large number of time periods , making it significantly different from most stochastic/noisy feedback or dueling bandit oracles that contains unbiased information of objective functions with only a single query/arm pull. Throughout the rest of this paper, we use the notation to denote the output of the pairwise comparison oracle when it is invoked to compare and with time periods.

The pairwise comparison oracle defined in Definition 2.1 encompasses several important feedback structures as special cases, as we enumerate below:

Example 2.2 (The standard bandit feedback)

In the standard bandit feedback setting the algorithm supplies and observes , with and almost surely. The oracle can be easily constructed using the difference of the sample averages at and . The standard Hoeffding’s inequality (Hoeffding 1963) implies that the constructed oracle is -consistent with and .

Example 2.3 (The continuous dueling bandit)

In the continuous dueling bandit setting (Kumagai 2017), at time the algorithm supplies and observes a binary comparison feedback such that for some known link function . Using the Hoeffding’s inequality this implies that, with samples, the sample average satisfies with probability . Subsequently, if is invertible and is -Lipschitz continuous, then satisfies Definition 2.1 with and .

In addition to the above examples, it is also common that (noisy) pairwise comparison oracles could be constructed for more complex operations management problems. In later Sec. 5 of this paper we mention two important operations management problems for which pairwise comparison oracles could be rigorously constructed, albeit through quite complex algorithms and procedures.

2.2 Function classes and assumptions

It is clear that, if the underlying, unknown function does not satisfy any regularity properties, it is mathematically impossible to design any non-trivial optimization algorithms. In this section, we introduce two standard function classes that impose certain smoothness and shape constraints on the underlying objective function so that the optimization problem is tractable.

Definition 2.4 (The Hölder class)

For and , the Hölder function class over is defined as

where is the set of all -times continuously differentiable functions on .

The Hölder function class is a popular function class that measures the smoothness of a function with higher orders and/or smaller constants indicating smoother functions. In the most general definition of the Hölder class the order could be further extended to any strictly positive real numbers. We shall however restrict ourselves to only integer-valued orders to make our analysis simpler.

We also consider functions that are strongly concave on , as specified in the following definition:

Definition 2.5 (Strongly concave functions)

For , the strongly concave function class over is defined as

Definition 2.5 above captures strongly concave functions that are at least twice continuously differentiable, by constraining the Hessian matrices of to be negative definite with all eigenvalues uniformly bounded away from zero on . Strongly concave functions naturally arise in many application problems and we show in this paper that for strongly concave and smooth functions there is an improved algorithm with improved performance guarantees as well.

2.3 Domain and knapsack constraints

We make the following assumption on the domain of the objective function : {assumption}[Interior maximizer] There exists a constant such that , where . Such interior properties of the maximizer are common assumptions imposed for stochastic zeroth-order or bandit optimization problems (Besbes et al. 2015).

In addition to optimizing an unknown objective function stipulated in Definition 2.1 and hard domain constraints , in many applications such as network revenue management, an “averaging” knapsack constraint is also important, preventing the algorithm from making too many decisions that are far away from a certain feasibility region dictated by initial inventory constraints. To this end, we introduce an averaging “penalty” function satisfying the following condition: {assumption}[Knapsack penalty function] The penalty function is convex and satisfies for some convex compact feasible region containing . Furthermore, there exists a constant such that for all .

Example 2.6 (Network revenue management)

In NRM, the opitmization variable is the expected demand rates for product types, , and the feasible region is where is the resource consumption matrix and is the normalized initial inventory levels. For this particular example, the penalty function could be defined as which penalizes over-selling of products with depleted resource types, where is the maximum price that could be offered and is the smallest non-zero entry in the resource consumption matrix . This penalty function satisfies Assumption 2.3 with respect to the feasible region with parameter .

2.4 Admissible policies and regret

In this section we give a rigorous definition of an admissible policy (that is, policies that are non-anticipating and only use past observations to guide future actions). An admissible policy consists of a variable sequence of conditional distributions such that for ,

Furthermore, with probability 1 there exists such that .

The cumulative regret of an admissible policy is defined as the expectation of the differences between the optimal (maximum) objective value and the actions the policy takes:

| (2) |

where is the unique integer such that which exists almost surely, and . Eq. (2) is a natural definition of the regret. To see this, each query of the pair generates a reward of . As the maximum possible reward for querying a pair is , the regret for this query is . Recall that the pair will be queried for periods, which gives a natural regret definition in (2).

3 Algorithm for smooth functions

We now give an overview of our algorithm for smooth functions, that is, those functions that belong to Hölder smoothness classes but may not be strongly concave or have other particular structures/shapes. The main algorithm, pseudocode displayed in Algorithm 3, is based on the following two main ideas:

-

1.

The entire solution space is partitioned into multiple smaller cubes; in each cube, a iterative LinUCB method is applied to figure out the approximately best solution within that cube;

-

2.

For competitions across tubes, a successive tournament elimination idea is applied, eliminating nearly half the small cubes every iteration via the noisy pairwise comparison oracle, until a unique winner is selected.

The first idea (iterative UCB method to find an approximate best solution within a small cube) is further decomposed into two sub-routines, elaborated in Secs. 3.1 and 3.2. The procedure relies on local polynomial regression to exploit the smoothness of the objective function, and an iterative application of batched LinUCB algorithm so that the standard LinUCB algorithm could be adapted to our setting where only a noisy pairwise comparison oracle is available, instead of noisy but unbiased function value observations.

3.1 Local polynomial approximation

To exploit the smoothness of the objective function , it is conventional to use local polynomial approximation schemes to approximate across multiple smaller cubes (Wang et al. 2019, Fan and Gijbels 2018, Wang et al. 2021, den Boer et al. 2024). More specifically, let be an algorithm parameter and divide into cubes, each of size . For any vector , let

be a cube corresponding to the indicator vector . Let be an arbitrary point in . For any and the smoothness level , define the local polynomial map , , as

For example, with and , the feature map can be explicitly written as .

The following lemma upper bounds the error of using local polynomial mapping as an approximation of .

Lemma 3.1

Let . Then for any , there exists , , such that

Lemma 3.1 shows that the approximation error of using local polynomial regression decreases as the number of small partitioning cubes increases, leading to more local approximations. Furthermore, the order of smoothness also plays an important role in the upper bound of approximation errors, as smoother functions admit smaller approximation errors. Lemma 3.1 can be proved by multi-variate Taylor expansion with Lagrangian remainders, which we place in the supplementary material.

3.2 Linear bandit with batched updates and biased rewards

Algorithm 1 gives a pseudo-code description of the LinUCB algorithm that will output approximate best solutions in a small cube. From Lemma 3.1, we know that locally could be well approximated by a linear function with respect to the polynomial map of centered solution vectors: this gives the foundation of using LinUCB and linear bandit methods.

At a higher level, Algorithm 1 resembles the LinUCB algorithm with infrequent policy updates, analyzed in (Abbasi-Yadkori et al. 2011). However, given our problem structure, there are several important differences:

-

1.

In our problem we only have access to a (biased) pairwise comparison oracle, instead of noisy unbiased observation of rewards for a given action. In Algorithm 1, we use a “baseline solution” to support pairwise comparisons, motivated by the observation that remains a linear model for locally thanks to Lemma 3.1.

The use of such a baseline also requires that is not too sub-optimal, because otherwise invocations of would incur large regret on the part. The near-optimality of is ensured in Algorithm 2 via an iterative procedure with double epochs, which we discuss in details in the next section.

-

2.

In our problem, because of the intrinsic bias in the pairwise comparison oracle, the observed feedback is not unbiased. This requires us to take extra care in the setting of the parameter in confidence terms to make sure the optimal solution is not overlooked.

-

3.

The output of Algorithm 1 is a single solution in so that it can be compared against (near-optimal) solutions from other cubes in a successive tournament elimination procedure. This is in contrast to standard linear bandit which only needs to ensure low cumulative regret from a sequence of solutions/actions. In our algorithm, we use the solution that lasts for the longest amount of time as the final output, which serves as an approximate good solution thanks to the pigeon hole principle.

Our next lemma analyzes Algorithm 1.

Lemma 3.2

Let and . Suppose Algorithm 1 is run with and . Then with probability the following properties hold:

-

1.

;

-

2.

;

-

3.

.

Lemma 3.2 contains three results, each serving an important purpose. The first result upper bounds the sub-optimality gap between the optimal objective value in cube and the solution , the final output of Algorithm 1, showing that is an approximate optimizer of in cube . The second result upper bounds the total number of iterations in Algorithm 1, which is important in establishing that the algorithm makes infrequence updates to solutions. The third result upper bounds the cumulative regret incurred throughout the entire algorithm. Notably, it only upper bounds half of the regret incurred by the pairwise comparison oracle on the parts of : the other half of the regret will be upper bounded in the next section after we introduce an iterative invocation procedure to ensure the near-optimality of solutions.

Due to space constraints, the complete proof of Lemma 3.2 is placed in the supplementary material.

Remark 3.3

For theoretical analysis, the values of several algorithm parameters require knowledge of the smoothness parameters and . Unfortunately, such prior knowledge is mathematically necessary in order to design and analyze effective algorithms, as demonstrated by the negative result of Locatelli and Carpentier (2018). In practice, we recommend the use of for reasonably smooth functions, for very smooth functions, and the value of for the derivative upper bounds.

Remark 3.4

The constants in the definition of in Algorithm 1 are for theoretical analytical purposes and are therefore conservative for practical use. When implementing the algorithm, together with the recommendation made in the previous remark, we recommend the choice of , with and .

3.3 Iterative applications of batched linear bandit

The BatchLinUCB routine introduced and analyzed in the previous section requires a fixed anchoring point to facilitate pairwise comparisons. Clearly, if is small the cumulative regret incurred by BatchLinUCB would be large regardless of how well it learns the maximum of in . This is evident from the last property of Lemma 3.2, where only half the regret incurred in BatchLinUCB is upper bounded. In this section we introduce an iterative application of the BatchLinUCB routine (pseudocode description in Algorithm 2), which controls the other half of the total regret incurred in the LinUCB procedure from .

The basic idea behind Algorithm 2 is simple: we use a doubling trick in the outer iteration to make sure that the solution provided is directly from the optimal solution output by Algorithm 1 in the previous iteration. This ensures that for later iterations that are longer, the quality of is also higher because it is obtained as an approximate optimizer in the previous iteration.

Lemma 3.5

3.4 Main algorithm: tournament successive eliminations

We are now ready to present our main algorithm, with pseudo-code in Algorithm 3.

* If is odd then transfer one arbitrary directly to ;

Algorithm 3 is built upon the idea of successive tournament eliminations. More specifically, each cube is regarded as a “competitor” and the competitors are paired with each other to play a hypothetical tournament; those cubes who “won” pairwise competitions are advanced to the next round, where each round is indicated by a variable and the “active” cubes/competitors at the beginning of round is denoted as a set (Lines 11 and 12). Finally, the winner of this tournament is used to determine whether other competitors should be kept for the next outer iteration, as shown on Line 18.

The following lemma is a structural lemma that plays a crucial in our understand and analysis of Algorithm 3.

Lemma 3.6

Suppose Algorithm 3 is run with and . Let also . Define also . Then with probability the following hold for all :

-

1.

;

-

2.

For every , .

Lemma 3.6 is proved in the supplementary material. It outlines the most important structures and properties of Algorithm 3. The first property, , indicates that (with high probability) the algorithm will never eliminate the cube with the optimal solution during any rounds of the tournament elimination phase. The second property states that, with high probability, all competitors who are still active at outer iteration after the tournament and elimination steps are nearly optimal, especially for later outer iterations that last longer.

We are now ready to present the main theoretical results upper bounding the cumulative regret of Algorithm 3:

Theorem 3.7

Theorem 3.7 shows that for objective functions of dimension that belong to the Hölder smoothness class of order , the asymptotic regret scaling is as time horizon increases. The regret upper bound is minimax optimal in time horizon up to poly-logarithmic terms, because it matches existing lower bound on continuum-armed bandit in which unbiased function value observations are available (Wang et al. 2019), a special case of the setting studied in this paper.

Remark 3.8

The large constants in the parameters in Algorithm 3 is for theoretical analysis only and in practical implementations they should be replaced with constants of one.

4 Algorithm for strongly concave functions

In this section, we design algorithms for a special case of the general bandit question with noisy pairwise comparison oracles, in which the objective function to be maximized is strongly concave. The (strong) concavity of objective functions is a common condition in operations management practice, such as “regularity” of demand/revenue functions in dynamic pricing (Chen et al. 2019), and the strong concavity of inventory holding/lost-sales costs when demand distributions are non-degenerate (Huh and Rusmevichientong 2009).

Mathematically, throughout this section we assume that

| (3) |

for some constants and , where the function classes and are defined in Sec. 2.2.

4.1 Proximal gradient descent with inexact gradients

The additional shape constraint calls for new algorithmic procedures that could exploit the strong concavity of . To this end, we design a proximal gradient descent algorithm with batch inexact gradient evaluations, as described in Algorithm 4.

In the outer iterations of Algorithm 4, we implement a projected (inexact) gradient ascent approach. Fixed step sizes are used to exploit strong concavity of the objective function, and the the iterations have geometrically increasing number of time periods dedicated for inner iterations in order to properly maintain gradient estimation error in the finite-difference approach (Lines 7 and 8). The inner iteration is then a finite-difference method to estimate the gradient of the objective function, utilizing the (biased) pairwise comparison oracles studied in this paper.

4.2 Regret analysis

We establish the following theorem upper bounding the regret of Algorithm 4, maximizing strongly concave functions with noisy pairwise comparison oracles.

Theorem 4.1

Remark 4.2

Dropping polynomial dependency on problem parameters other than the problem dimension and the time horizon , as well as all poly-logarithmic factors, the upper bound in Theorem 4.1 is on the asymptotic order of .

5 Application to operations management problems

In this section we show how the pairwise comparison oracle discussed in this paper is common in the solution to important operations management questions with demand learning. As a clarification, all algorithms and analysis in this section are not new; however, reformulating the existing results into pairwise comparison oracles allows us to use the new algorithms and analysis derived in this paper to yield new or improved results for these classical learning-while-doing problems in operations management.

5.1 Example: joint pricing and inventory control with censored demand

5.1.1 Problem formulation.

This example primarily follows (Chen et al. 2023, Sec. EC.6). Consider a multi-period joint pricing and inventory replenishment problem for a firm with different types of products. At the beginning of a time period , the firm makes two sets of decisions: the price decision and the inventory decision consisting of inventory order-up-to levels for each product type. Given , the demands for all products are modeled as where are demand curves and are centered noise random variables such that for some unknown joint distribution on . The firm does not know either or . The instantaneous rewards and inventory level transitions are then the same as in Eq. (1) for each product type.

At each time period , the firm observes censored demand , where the max operator is applied in an element-wise fashion. With full information of and under the asymptotic regime of , the near-optimal solution is myopic which solves

where is the marginal distribution of induced by and . The question is then to carry out bandit optimization of in -dimension with pairwise comparison oracle, to be introduced in the next section.

5.1.2 Pairwise comparison oracle.

While or an unbiased estimate of it cannot be directly accessed due to demand censoring, it is possible to obtain, when given a pair of price vectors , an unbiased estimate of

where . Such a pairwise comparison oracle is constructed in (Chen et al. 2023, Algorithm 8), with the following guarantee summarizing (Chen et al. 2023, Lemma EC.6.2) adapted to the notation of this paper:

Lemma 5.1

Given and time periods, (Chen et al. 2023, Algorithm 8) is a pairwise comparison oracle that outputs that satisfies with probability that

5.1.3 Improved regret analysis.

One major improvement, which is a direct consequence of the algorithm and analysis of this paper, is to incorporate the pairwise comparison oracle in Lemma 5.1 into Algorithm 3 to deliver an improved regret bound when the partially optimized objective function is smoother. More specifically, we have the following result:

Corollary 5.3

Compared with the regret upper bound obtained in (Chen et al. 2023), Corollary 5.3 improves the existing bound for . This is because for smoother functions our Algorithm 3 can better exploit the additional smoothness in contrast to the simplified tournament elimination approach adopted in (Chen et al. 2023). See also Table 1 for comparisons against additional existing results.

5.2 Example: network revenue management

5.2.1 Problem formulation.

This example follows (Miao and Wang 2021) and, to a lesser extent, the setting studied in (Chen and Shi 2019). Consider multi-period pricing of types of products using types of resources over time periods with non-replenishable initial inventory levels of the resources which also scale linearly with . The demand curve which is an map is unknown, non-parametric and must be learnt on the fly. Regret is measured against the fluid approximation with the expected revenue as objective and subject to linear feasibility constraints on demand rates. More specifically, on the demand domain, the fluid approximation is defined as the following constrained optimization problem:

| (4) |

where is the known resource consumption matrix, is a known vector of normalized inventory levels for all resource types, and is the expected revenue as a function of the demand rate vector , where is the inverse function of the demand curve mapping from to .

It is a common assumption in the literature that is both smooth and strongly concave, essentially implying for some and . This together with the convexity of the feasible region (which is actually a polytope) makes Algorithm 4 and Theorem 4.1 good candidates for obtaining results under this setting of the problem.

5.2.2 Pairwise comparison oracle.

While Eq. (4) is a concave maximization problem in , in the bandit setting where (and therefore ) is unknown it is difficult to directly optimize it because it is unknown which price vector is leading to a target demand rate vector . This means that if we use optimization methods to obtain a sequence of , it is difficult to either evaluate or check whether the solution is feasible because both involve the unknown demand curve or its inverse .

In Miao and Wang (2021) a two-step procedure is proposed which can serve as a pairwise comparison oracle as defined in this paper. More specifically, the algorithm first uses inverse batch gradient descent type methods similar to the one designed in (Chen and Shi 2019) to find a price that converges to a neighborhood of . Afterwards, the algorithm uses Jacobian iteration steps to converge to at a much faster pace. The following lemma establishes the theoretical property of the two-step procedure in (Miao and Wang 2021), which is adapted from (Miao and Wang 2021, Lemma 3, property 3).

Lemma 5.4

Given satisfying , and time periods, (Miao and Wang 2021, Algorithm 2) applied to separately is a pairwise-comparison oracle that outputs that satisfies with probability that

where in the notation we omit polynomial dependency on other problem parameters.

5.2.3 Improve regret analysis.

Incorporating the pairwise comparison oracle in Lemma 5.4 into Algorithm 4 for objective functions, we obtain the following result which improves the result in (Miao and Wang 2021) without imposing additional assumptions or conditions:

Corollary 5.5

6 Numerical Results

In this section, we provide three different streams of experimental studies to demonstrate the effectiveness of the proposed pairwise comparison algorithms. We report numerical results on both synthetic objective functions, and also synthetic problem instances arising from inventory management problems.

6.1 Bandit Optimization with Smooth Objective Functions

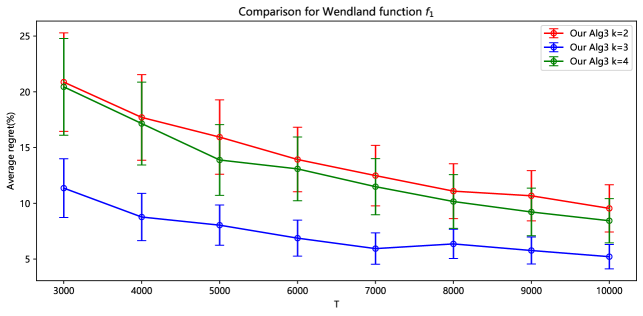

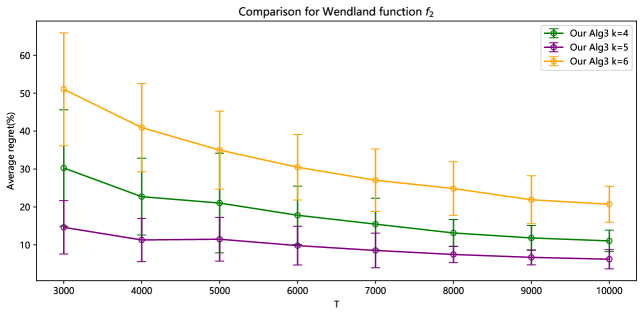

To mimic the scenario considered in this paper, we conduct two simple bandit optimization problems with smooth objective functions to evaluate the proposed Algorithm 3’s finite sample performance. We construct the following objective functions:

| (5) |

We follow conventional settings of noises in continuum-armed bandit problems. That is, for and every , an optimization algorithm takes an action and observes where , , with . and are the so-called Wendland functions that satisfy and respectively (Chernih et al. 2014). We then apply Algorithm 3 to both functions with smoothness levels for and for .

Throughout our numerical experiments we report the percentage of relative regret, defined as

| (6) |

where . Then, the percentage of relative regret is utilized to evaluate the effectiveness of the proposed pairwise comparison algorithms. Other parameters for implementing Algorithm 3 are shown in Appendix 12.

Figures 1 and 2 depict the simulation results of the proposed Algorithm 3 with different smooth levels, with 50 runs, respectively. From Figure 1 and 2, we can find that as , all the average regrets of Algorithm 3 decrease dramatically. An interesting result is that the average regret of with the input smooth level is always smaller than others at the same periods. The reason may be the selected smooth level , which is the same as the smoothness of . The same phenomenon can also be observed for the average regret of with the input smooth level . All the above results are consistent with our proposed theorems, which provide more evidence to demonstrate the correctness and effectiveness of the proposed pairwise comparison algorithms.

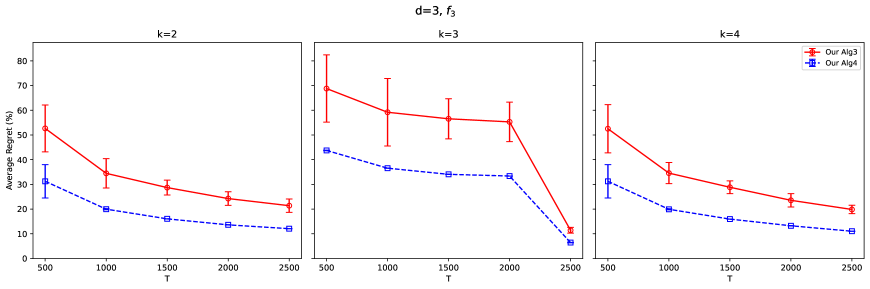

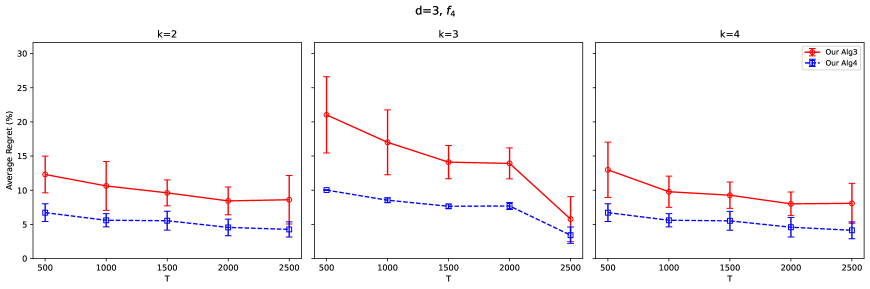

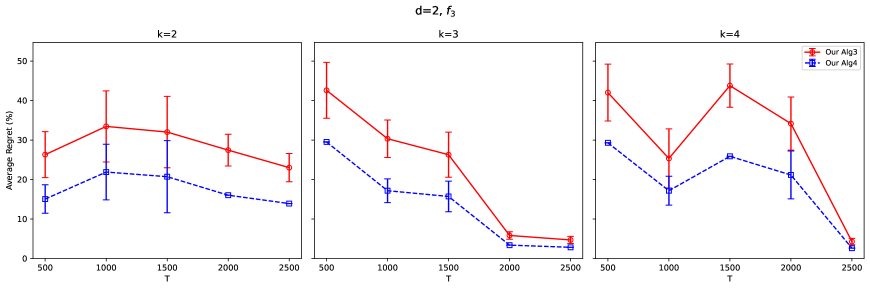

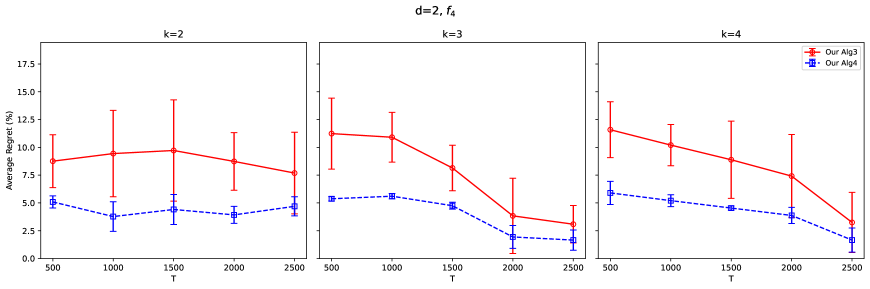

6.2 Bandit Optimization with Concave Objective Functions

Following almost the same setting as the above subsection, we conduct two simple bandit optimization problems with the concave objective functions to compare Algorithm 3 and 4’s finite sample performance. We consider four objective functions:

-

•

;

-

•

;

Obviously, the objective functions are concave and smooth in infinite dimensions. We set and for this example, and Algorithms 3 and 4 both can apply to the two objective functions.

Figures 3 and 4 show the simulation results of proposed Algorithms 3 and 4 for and with , with 50-time runs, respectively. The results for can be found in Appendix 11.2. According to the figures, we can find two interesting facts. First, all the average regrets of Algorithms 3 and 4 decrease dramatically as . Second, the average regrets of Algorithm 4 are always smaller than those of Algorithm 3 at the same periods and smoothness . The reason may be that Algorithm 4 is designed for concave objective functions. Thus, the simulation example is well-suited to the setting of Algorithm 4.

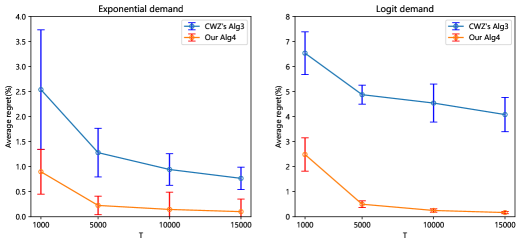

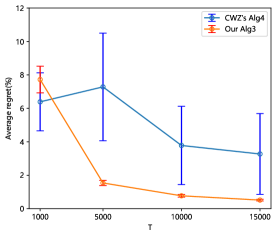

6.3 Example: Inventory Management with Censored Demand

6.3.1 Problem formulation

Let us consider a firm selling one type of product over a time horizon of periods. At period, the firm can observe the inventory level before replenishment and need to make a pricing decision and inventory order-up-to decision with zero ordering lead time and zero ordering cost. Suppose that the unknown demand is influenced by the price , namely, , where is a deterministic demand function and is a noise random variable. We further assume the unsatisfied demands are lost and unobservable. Thus, the lost-sales quantity is not observable. At the end of period , the firm incurs a profit of

| (7) |

where and are the per-unit holding and lost-sales penalty costs, respectively. Note that because the lost-sales cost is not observable, neither is the realized profit .

It is well known that the optimal pricing and inventory replenishment policy with known and noise distribution of has been investigated by Sobel (1981) (called Clairvoyant optimal policy), taking the form of

| (8) |

where . Denote that and . Therefore, the performance of an admissible policy is measured by the cumulative regret compared against the Clairvoyant policy , i.e.,

| (9) |

In the next part, we test Algorithm 3 under smooth and non-concave and Algorithm 4 under smooth and concave , respectively, then compare the performance with corresponding algorithms proposed by Chen et al. (2023). For the noisy pairwise comparison oracle, we adopt the same designed and analyzed in (Chen et al. 2023, Algorithm 2, Lemma 2). The percentage of relative regret, defined as

| (10) |

is adopted as the measurement, where is the Clairvoyant optimal reward.

6.3.2 Settings under different types of

We test our algorithms using the same settings as in the numerical section of Chen et al. (2021, 2023). Because the concavity and non-concavity of the objective function have been conducted by Chen et al. (2023).

To obtain the concave objective function , we set

-

•

Cost parameters: and .

-

•

Two demand functions: (i) Exponential function ; (ii) Logit function .

-

•

Random error distribution: (i) Uniform distribution on and normal distribution with mean 0 and standard deviation 2 for the exponential demand function. (ii)Uniform distribution on and normal distribution with mean 0 and standard deviation 0.2 for the logit demand function.

To obtain the non-concave objective function , we set

-

•

Cost parameters: and .

-

•

Demand functions: , where is the CDF of standard normal distribution.

-

•

Random error distribution: Uniform distribution on and normal distribution with mean 0 and standard deviation 2 for the exponential demand function.

Combining the cost parameters, demand functions, and error distributions, it shows 24 distinct simulations. We run the proposed Algorithms 3 and 4 for 50 times and compare the average with the results of corresponding methods in Chen et al. (2023), respectively. The detailed parameter settings of Algorithms 3 and 4 are given by Appendix 12.

6.3.3 Performance under different types of

Figure 5 reports the results of overall average regrets with the comparison between the proposed Algorithms 3 and 4 with CWZ’s Algorithm 4 and 3 (Chen et al. 2023) for concave and non-concave , respectively. As it can be seen, Algorithms 3 and 4 significantly outperform CWZ’s Algorithms 4 and 3, especially . The error bars demonstrate that our algorithm is more stable than CWS’s. These results corroborate our theoretical findings that the proposed algorithm is superior on smoother objectives.

7 Conclusion and future directions

In this paper, we study a biased pairwise comparison oracle abstracted from several important operations management problems. We proposed bandit algorithms that operate under two different sets of smoothness and/or concavity assumptions, and derive improved results for two important OM problems (joint pricing and inventory control, network revenue management) applying our proposed algorithms and their analysis.

To conclude our paper, we mention the following two future directions, one from the bandit optimization perspective and the other one from applications to OM problems.

Incorporating growth conditions in function classes.

In this paper, we studied two types of function classes: Hölder smoothness class and strongly concave function class , which is one form of shape constraints. It would be interesting to extend our results to other important function classes, such as those equipped with growth conditions that regulate how fast the Lesbesgue measure of level sets of objective functions could grow. Existing results in continuum-armed bandit show that such growth conditions have significant impacts on the optimal regret of bandit algorithms (Locatelli and Carpentier 2018, Wang et al. 2019), and it would be interesting to explore extensions of these results to biased pairwise comparison oracles.

Joint pricing and inventory replenishment with censored demands and fixed costs.

In this paper, we apply our algorithms and analytical frameworks to a joint pricing and inventory replenishment problem with demand learning settings, where demands are censored and inventory ordering is subject to variable, linear costs. In pracice, however, it is common that inventory ordering is also subject to fixed costs that are incurred regardless of ordering amounts. It is an interesting yet challenging question to extend algorithms and analysis in this paper to problem settings with both demand censoring and inventory ordering costs, which remains as far as we know an open question in the field.

References

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori, Yasin, Dávid Pál, Csaba Szepesvári. 2011. Improved algorithms for linear stochastic bandits. Proceedings of the Advances in Neural Information Processing Systems (NIPS). 2312–2320.

- Agarwal et al. (2010) Agarwal, Alekh, Ofer Dekel, Lin Xiao. 2010. Optimal algorithms for online convex optimization with multi-point bandit feedback. Conference on Learning Theory (COLT).

- Agarwal et al. (2022) Agarwal, Arpit, Rohan Ghuge, Viswanath Nagarajan. 2022. An asymptotically optimal batched algorithm for the dueling bandit problem. Advances in Neural Information Processing Systems (NeurIPS).

- Agrawal (1995) Agrawal, Rajeev. 1995. The continuum-armed bandit problem. SIAM Journal on Control and Optimization 33(6) 1926–1951.

- Argarwal et al. (2022) Argarwal, Arpit, Rohan Ghuge, Viswanath Nagarajan. 2022. Batched dueling bandits. International Conference on Machine Learning (ICML).

- Besbes et al. (2015) Besbes, Omar, Yonatan Gur, Assaf Zeevi. 2015. Non-stationary stochastic optimization. Operations research 63(5) 1227–1244.

- Besbes and Zeevi (2009) Besbes, Omar, Assaf Zeevi. 2009. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57(6) 1407–1420.

- Besbes and Zeevi (2012) Besbes, Omar, Assaf Zeevi. 2012. Blind network revenue management. Operations research 60(6) 1537–1550.

- Besbes and Zeevi (2015) Besbes, Omar, Assaf Zeevi. 2015. On the (surprising) sufficiency of linear models for dynamic pricing with demand learning. Management Science 61(4) 723–739.

- Broder and Rusmevichientong (2012) Broder, Josef, Paat Rusmevichientong. 2012. Dynamic pricing under a general parametric choice model. Operations Research 60(4) 965–980.

- Bu et al. (2022) Bu, Jinzhi, David Simchi-Levi, Yunzong Xu. 2022. Online pricing with offline data: Phase transition and inverse square law. Management Science 68(12) 8568–8588.

- Bubeck et al. (2011) Bubeck, Sébastien, Rémi Munos, Gilles Stoltz, Csaba Szepesvári. 2011. X-armed bandits. Journal of Machine Learning Research 12(5).

- Chen et al. (2021) Chen, Boxiao, Xiuli Chao, Cong Shi. 2021. Nonparametric learning algorithms for joint pricing and inventory control with lost sales and censored demand. Mathematics of Operations Research 46(2) 726–756.

- Chen et al. (2022) Chen, Boxiao, David Simchi-Levi, Yining Wang, Yuan Zhou. 2022. Dynamic pricing and inventory control with fixed ordering cost and incomplete demand information. Management Science 68(8) 5684–5703.

- Chen et al. (2023) Chen, Boxiao, Yining Wang, Yuan Zhou. 2023. Optimal policies for dynamic pricing and inventory control with nonparametric censored demands. Management Science 70(5) 3363–3380.

- Chen et al. (2019) Chen, Qi, Stefanus Jasin, Izak Duenyas. 2019. Nonparametric self-adjusting control for joint learning and optimization of multiproduct pricing with finite resource capacity. Mathematics of Operations Research 44(2) 601–631.

- Chen and Simchi-Levi (2004a) Chen, Xin, David Simchi-Levi. 2004a. Coordinating inventory control and pricing strategies with random demand and fixed ordering cost: The finite horizon case. Operations Research 52(6) 887–896.

- Chen and Simchi-Levi (2004b) Chen, Xin, David Simchi-Levi. 2004b. Coordinating inventory control and pricing strategies with random demand and fixed ordering cost: The infinite horizon case. Mathematics of Operations Research 29(3) 698–723.

- Chen and Simchi-Levi (2012) Chen, Xin, David Simchi-Levi. 2012. Pricing and inventory management, R. Philips and O. Ozer, eds.. Oxford University Press, Oxford.

- Chen and Shi (2019) Chen, Yiwei, Cong Shi. 2019. Network revenue management with online inverse batch gradient descent method. Available at SSRN 3331939 .

- Chernih et al. (2014) Chernih, Andrew, Ian H Sloan, Robert S Womersley. 2014. Wendland functions with increasing smoothness converge to a gaussian. Advances in Computational Mathematics 40 185–200.

- Cheung et al. (2017) Cheung, Wang Chi, David Simchi-Levi, He Wang. 2017. Dynamic pricing and demand learning with limited price experimentation. Operations Research 65(6) 1722–1731.

- den Boer et al. (2024) den Boer, Arnoud V., Boxiao Chen, Yining Wang. 2024. Pricing and positioning of horizontally differentiated products with incomplete demand information. Operations Research 72(6) 2446–2466.

- Dud´ık et al. (2015) Dudík, Miroslav, Katja Hofmann, Robert E Schapire, Aleksandrs Slivkins, Masrour Zoghi. 2015. Contextual dueling bandits. Conference on Learning Theory (COLT). PMLR, 563–587.

- Fan and Gijbels (2018) Fan, Jianqing, Irene Gijbels. 2018. Local polynomial modelling and its applications. Routledge.

- Ferreira et al. (2018) Ferreira, Kris Johnson, David Simchi-Levi, He Wang. 2018. Online network revenue management using thompson sampling. Operations Research 66(6) 1586–1602.

- Gallego and van Ryzin (1994) Gallego, Guillermo, Garrett van Ryzin. 1994. Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management Science 40(8) 999–1020.

- Hoeffding (1963) Hoeffding, Wassily. 1963. Probability inequalities for sums of bounded random variables. Journal of the American Statistical Association 58(301) 13–30.

- Huh and Janakiraman (2008) Huh, Woonghee Tim, Ganesh Janakiraman. 2008. (s, s) optimality in joint inventory-pricing control: An alternate approach. Operations Research 56(3) 783–790.

- Huh and Rusmevichientong (2009) Huh, Woonghee Tim, Paat Rusmevichientong. 2009. A nonparametric asymptotic analysis of inventory planning with censored demand. Mathematics of Operations Research 34(1) 103–123.

- Katehakis et al. (2020) Katehakis, Michael N, Jian Yang, Tingting Zhou. 2020. Dynamic inventory and price controls involving unknown demand on discrete nonperishable items. Operations Research 68(5) 1335–1355.

- Kumagai (2017) Kumagai, Wataru. 2017. Regret analysis for continuous dueling bandit. Advances in Neural Information Processing Systems 30.

- Locatelli and Carpentier (2018) Locatelli, Andrea, Alexandra Carpentier. 2018. Adaptivity to smoothness in x-armed bandits. Conference on Learning Theory. PMLR, 1463–1492.

- Miao and Wang (2021) Miao, Sentao, Yining Wang. 2021. Network revenue management with nonparametric demand learning:sqrt T-regret and polynomial dimension dependency. Available at SSRN 3948140 .

- Miao et al. (2021) Miao, Sentao, Yining Wang, Jiawei Zhang. 2021. A general framework for resource constrained revenue management with demand learning and large action space. available at SSRN 3841273 .

- Nambiar et al. (2019) Nambiar, Mila, David Simchi-Levi, He Wang. 2019. Dynamic learning and pricing with model misspecification. Management Science 65(11) 4980–5000.

- Petruzzi and Dada (1999) Petruzzi, Nicholas C., Maqbool Dada. 1999. Pricing and the newsvendor problem: A review with extensions. Operations research 47(2) 183–194.

- Saha and Gaillard (2022) Saha, Aadirupa, Pierre Gaillard. 2022. Versatile dueling bandits: Best-of-both world analyses for learning from relative preferences. International Conference on Machine Learning (ICML). PMLR, 19011–19026.

- Saha et al. (2021) Saha, Aadirupa, Tomer Koren, Yishay Mansour. 2021. Adversarial dueling bandits. International Conference on Machine Learning (ICML). PMLR, 9235–9244.

- Sobel (1981) Sobel, Matthew J. 1981. Myopic solutions of Markov decision processes and stochastic games. Operations Research 29(5) 995–1009.

- Sui et al. (2018) Sui, Yanan, Masrour Zoghi, Katja Hofmann, Yisong Yue. 2018. Advancements in dueling bandits. International Joint Conference on Artificial Intelligence (IJCAI). 5502–5510.

- Urvoy et al. (2013) Urvoy, Tanguy, Fabrice Clerot, Raphael Féraud, Sami Naamane. 2013. Generic exploration and k-armed voting bandits. International Conference on Machine Learning (ICML). PMLR, 91–99.

- Wang et al. (2019) Wang, Yining, Sivaraman Balakrishnan, Aarti Singh. 2019. Optimization of smooth functions with noisy observations: Local minimax rates. IEEE Transactions on Information Theory 65(11) 7350–7366.

- Wang et al. (2021) Wang, Yining, Boxiao Chen, David Simchi-Levi. 2021. Multi-modal dynamic pricing. Management Science 67(10) 6136–6152.

- Wang et al. (2014) Wang, Zizhuo, Shiming Deng, Yinyu Ye. 2014. Close the gaps: A learning-while-doing algorithm for single-product revenue management problems. Operations Research 62(2) 318–331.

- Yuan et al. (2021) Yuan, Hao, Qi Luo, Cong Shi. 2021. Marrying stochastic gradient descent with bandits: Learning algorithms for inventory systems with fixed costs. Management Science 67(10) 6089–6115.

- Yue et al. (2012) Yue, Yisong, Josef Broder, Robert Kleinberg, Thorsten Joachims. 2012. The k-armed dueling bandits problem. Journal of Computer and System Sciences 78(5) 1538–1556.

Supplementary material: additional proofs

8 Proofs of results in Sec. 3

8.1 Proof of Lemma 3.1

Because , by Taylor expansion with Lagrangian residuals, there exists such that

With

we have that

The norm of can be upper bounded as

This proves Lemma 3.1.

8.2 Proof of Lemma 3.2

We first prove the second inequality. Let be the matrix at the end of iteration . By definition, and each iteration the determinant of the matrix doubles. Hence, . On the other hand, , and therefore . Consequently, .

We next prove the third inequality in Lemma 3.2. Let be the estimated linear model at the beginning of iteration . Let also . By definition, we have

| (11) |

Re-arranging terms on both sides of Eq. (11) and noting that and thanks to Lemma 3.1, we have

| (12) |

Note that satisfies with probability , following Definition 2.1 and Lemma 3.1. Subsequently, by the Cauchy-Schwarz inequality,

| (13) |

Here, Eq. (14) holds because and . Because since , dividing both sides of Eqs. (12,13) by we obtain

| (14) |

Using Hölder’s inequality, it holds for all that

| (15) |

On the other hand, Lemma 3.1 implies that for all . Consequently, we have for all that

| (16) |

Eq. (16) demonstrates that, with probability , the estimate constructed in Line 4 of Algorithm 1 is a uniform upper bound on , or more specifically for all . Subsequently, with probability it holds that

| (17) | ||||

| (18) | ||||

| (19) | ||||

| (20) |

Here, Eq. (17) holds because by the definition of , and hence thanks to (Abbasi-Yadkori et al. 2011, Lemma 4); Eq. (18) holds by the Cauchy-Schwarz inequality and the fact that ; Eq. (19) holds because for any and , .

8.3 Proof of Lemma 3.5

The first property holds by directly invoking Lemma 3.2 and noting that and the definition of .

To prove the second property, note that for any iteration of length , Algorithm 2 invokes the BatchLinUCB with . The first and third properties of Lemma 3.2 show that, with probability , the total regret cumulated in the time periods (accounting for both and in Algorithm 1) is upper bounded by

Subsequently,

which is to be proved.

8.4 Proof of Lemma 3.6.

We use induction to prove the first property. The inductive hypothesis for is trivially true because . Now assume holds, we shall prove that holds as well with probability .

Fix arbitrary and let . By Lemma 3.5 and Definition 2.1, we have with probability that

| (21) |

The elimination steps (Line 18) then satisfy the following properties: with Eq. (22), the feedback satisfies with probability that

where the second inequality holds because thanks to the definition of . This shows that , which is to be proved.

We next prove the second property of Lemma 3.6. Because almost surely, Eq. (21) and the tournament mechanism in Algorithm 3 imply that

| (22) |

On the other hand, according to Line 18 of Algorithm 3, for any , the satisfies . Subsequently, applying Eqs. (21,22), we obtain

| (23) |

This completes the proof of Lemma 3.6.

8.5 Proof of Theorem 3.7

To simplify notations, throughout this proof we shall drop numerical constants and polynomial dependency on . Let be the last complete iteration in Algorithm 3 and fix arbitrary . The cumulative regret incurred by all operations during iteration can be upper bounded, with probability , by

| (24) |

Using Lemmas 3.5 and 3.6, and a union bound over all hypercubes, it holds with probability that

| (25) |

Using the same analysis, can also be upper bounded by

| (26) |

Using Lemma 3.5 and a union bound over all hypercubes, it holds with probability that

| (27) |

Define the following constants:

Summing over and noting that , we have that

| (28) |

Finally, note that and therefore because . Expanding all definitions of constants in Eq. (28), the regret of Algorithm 3 is upper bounded by

which is to be proved. Note that in this algorithm the implemented solutions are always feasible; that is, for all . Therefore, the regret of the term is exactly zero.

9 Proof of Theorem 4.1

The first part of the proof analyzes the estimation error of the gradient estimate as well as the regret incurred in the gradient estimation procedure, by establishing the following lemma:

Lemma 9.1

Proof 9.2

Proof of Lemma 9.1. We first prove the second property of Lemma 9.1. By Taylor expansion and the fact that , it holds for every that

| (29) | |||

| (30) |

We next turn to the first property. Eqs. (29,30) together yield that

| (31) |

On the other hand, the definition of the noisy pairwise comparison oracle combined together with the union bound yield that, with probability , the following hold for all :

| (32) | ||||

| (33) |

Combining Eqs. (31,32,33) and noting that , we complete the proof of Lemma 9.1.

Our next lemma establishes convergence rate of the proximal gradient descent/ascent approach adopted in Algorithm 4, using fixed step sizes and inexact gradient estimates .

Lemma 9.3

Let , which is convex on thanks to the condition that . For each epoch , let . Then for every until time periods are elapsed,

where .

The technical proof of Lemma 9.3 is involved and therefore deferred to the end of this section.

We are now ready to complete the proof of Theorem 4.1. The first property of Lemma 9.1 implies that, with high probability, , where the second inequality holds because almost surely. Incorporating this into Lemma 9.3, we have with probability that

| (34) |

where the last inequality holds because a complete epoch lasts for periods, and therefore . Because and which implies , Eq. (34) yields

| (35) |

Combining Eq. (35) with the second property of Lemma 9.1, and noting that the regret incurred by the term is zero because the violation constraints from and are symmetric and cancel out each other, we would complete the proof of Theorem 4.1. More specifically, the regret arising from the second property of Lemma 9.1 can be upper bounded by

| (36) |

9.1 Proof of Lemma 9.3

By Line 12 of Algorithm 4, it holds for every epoch that

| (37) |

Because is continuously differentiable with -Lipschitz continuous gradients, it holds that

| (38) |

Additionally, using the definition that and the Cauchy-Schwarz inequality, we have for every that

| (39) |

Combining Eqs. (37,38,39) and using the fact that , we have for every that

| (40) |

Let be a coefficient associated with epoch , so that and . By Eq. (40) setting , we have that

| (41) |

Now let be the sub-optimality gap at the solution of epoch . Summing both sides of Eq. (41) through and telescoping, we obtain for every that

| (42) |

We next present and prove a technical lemma that is helpful for our recursive analysis:

Lemma 9.4

Let and be nonnegative real sequences. If for all and , then for any , we have

Proof 9.5

10 Parameter setting of Experiment one

10.1 Setting for bandit optimization with smooth objective functions

The parameter setting for is in Table 3 and Table 4, respectively. Only the parameters with updated values compared to Table 3 are reported in Table 4.

| Parameter Symbol | Explanation | Value | ||

| parameter in Algorithm 1 | ||||

| parameter in Algorithm 1 | ||||

| parameter in | ||||

| parameter in upper bound in Lemma 3.1 | ||||

| parameter in | 0.01 | |||

| parameter in | 0.005 | |||

| parameter in Algorithm 3 | ||||

| parameter in Algorithm 3 | ||||

| parameter in Algorithm 3 | ||||

| control parameter of Hölder class | ||||

| smoothness level | ||||

| cube count per dimension | 3 | |||

| dimensions used for analysis | ||||

|

|

|

3000-10000(step=1000) | ||

| noise in the oracle function |

-

*

In practical implementations, we suggest scaling by constants.

-

**

Since we use in the definition of , a second-degree polynomial is actually used for fitting by setting .

| Parameter Symbol | Explanation | Value |

| control parameter of Hölder class | ||

| smoothness level | ||

| noise in the oracle function |

11 Parameter setting and results of Experiment two

11.1 Setting for bandit optimization with concave objective functions

The parameters used in Algorithm 3 and Algorithm 4 for concave objective functions are demonstrated in Table 5.

| Parameter Symbol | Explanation | Value |

| parameter in Algorithm 1 | ||

| parameter in Algorithm 1 | ||

| parameter in | ||

| parameter in upper bound in Lemma 3.1 | ||

| parameter in | 0.01 | |

| parameter in | 0.01 | |

| parameter in Algorithm 3 | ||

| parameter in Algorithm 3 | ||

| parameter in Algorithm 3 | ||

| control parameter of Hölder class | ||

| smoothness level | ||

| cube count per dimension | 3 | |

| dimensions used for analysis | ||

| total time steps | ||

| parameter in Algorithm 4 | 1 | |

| parameter in Algorithm 4 | 1 | |

| parameter in Algorithm 4 | 10 |

-

*

In practical implementations, we suggest scaling by constants.

-

**

Since we use in the definition of , a second-degree polynomial is actually used for fitting by setting .

11.2 Results of Experiment two