Catoni-Style Change Point Detection for Regret Minimization in Non-Stationary Heavy-Tailed Bandits

Abstract

Regret minimization in stochastic non-stationary bandits gained popularity over the last decade, as it can model a broad class of real-world problems, from advertising to recommendation systems. Existing literature relies on various assumptions about the reward-generating process, such as Bernoulli or subgaussian rewards. However, in settings such as finance and telecommunications, heavy-tailed distributions naturally arise. In this work, we tackle the heavy-tailed piecewise-stationary bandit problem. Heavy-tailed bandits, introduced by bubeck2013bandits, , operate on the minimal assumption that the finite absolute centered moments of maximum order are uniformly bounded by a constant , for some . We focus on the most popular non-stationary bandit setting, i.e., the piecewise-stationary setting, in which the mean of reward-generating distributions may change at unknown time steps. We provide a novel Catoni-style change-point detection strategy tailored for heavy-tailed distributions that relies on recent advancements in the theory of sequential estimation, which is of independent interest. We introduce Robust-CPD-UCB, which combines this change-point detection strategy with optimistic algorithms for bandits, providing its regret upper bound and an impossibility result on the minimum attainable regret for any policy. Finally, we validate our approach through numerical experiments on synthetic and real-world datasets.

1 Introduction

In a Multi-Armed Bandit (MAB, for short, lattimore2020bandit, ), a decision-maker (also called learner) is faced with a sequence of repeated decisions among a fixed number of options (or actions or arms), observing a reward drawn from a probability distribution after each decision. MABs gained popularity over the last two decades, as they allow for strong theoretical guarantees over algorithms’ performance while maintaining the model’s generality. However, the most traditional MAB model relies on demanding assumptions that are rarely met in the real world. The majority of the research effort in the MAB literature focused on progressively overcoming these limitations to cover richer scenarios. Examples include non-stationary (besbes2014stochastic, ), linear (abbasi2011improved, ), and heavy-tailed (bubeck2013bandits, ) MABs.

In this work, we focus on a broad class of problems that relaxes, at the same time, two core assumptions of the standard MAB problem. In particular, we focus on heavy-tailed non-stationary MABs. Our framework allows for a general class of reward-generating probability distributions without relying on parametric assumptions and with a possibly infinite variance, called heavy-tailed distributions. This setting gained popularity over the last decade due to its applications in finance and telecommunications. Moreover, it extends the assumption of sub-gaussian reward distributions, which is customary in the MAB literature. In such application domains, the assumption that reward-generating distributions are fixed along the whole time horizon is too limiting. It is natural to consider settings, such as finance, characterized by non-stationary processes. We address, with a single algorithm named Robust-CPD-UCB, the problem of learning in non-stationary environments where the noise of the observations can be heavy-tailed. We prove theoretical guarantees over the performance of R-CPD-UCB and show that they are nearly optimal under some mild assumptions. To the best of the authors’ knowledge, this is the first work to address the problem of regret minimization in non-stationary bandits under infinite-variance reward distributions. In particular, we face the technical challenge of developing the first change-point detection strategy with proven theoretical guarantees for such types of distributions. The contributions are organized as follows:

-

•

In Section 2, we introduce the definition of the heavy-tailed piecewise-stationary MAB setting. We define the learning problem and introduce a lower bound on the expected regret for this setting.

-

•

In Section 3, we recall some notions and results from the existing literature on mean estimation for heavy-tailed random variables and on change-point detection.

-

•

In Section 4, we introduce Robust-CPD-UCB, an algorithm from regret minimization in our setting. We provide theoretical guarantees on its expected regret and insights on choosing its parameters.

- •

2 Problem Formulation

In this section, we recall the definitions of heavy-tailed and piecewise-stationary bandit. Then, we introduce the heavy-tailed piecewise-stationary bandits, the focus of this work. We formally define the problem of regret minimization and provide a novel regret lower bound for the problem.

2.1 Bandit Settings

Every round , a decision is undertaken (possibly at random) and a reward is sampled from a probability distribution . We call the set of reward-generating distributions an instance of the MAB (from now on, just MAB). Most of the literature deals with reward-generating distributions either sub-gaussian or with bounded supports.

Heavy-Tailed Bandits. In heavy-tailed bandits bubeck2013bandits , the probability distributions are heavy-tailed. In this work, we use the same definition of heavy-tailed MAB (HT MAB, for short).

Definition 2.1 (Heavy-Tailed MAB).

Let be a random variable with support on . Then, we call a heavy-tailed random variable if it satisfies

| (1) |

for and . Let be a MAB. Then, if , where is the set of probability distributions satisfying Equation (1), we call a heavy-tailed bandit (HT MAB, for short).

Note that Equation (1) implies that the variance of the rewards-generating distributions may be infinite (when ). Most of the technical tools employed for sub-gaussian rewards are ineffective for HT MABs. We address readers to genalti2024varepsilon for a recent literature review on HT MABs.

Piecewise-Stationary Bandits. In standard MABs, the reward-generating distributions are assumed to never change during learning. In non-stationary bandits, instead, the reward-generating distributions are dynamic in time, i.e., the rewards of the same arm are sampled from different distributions depending on the pull time . However, if there is no constraint on how many times the distributions may change, then the problem may quickly become non-tractable. Thus, in this work, we consider the most popular non-stationary MAB setting, i.e., the piecewise-stationary bandit (PS MAB) from yu2009piecewise , where the distributions of rewards remain constant for a certain period, called epoch, and then abruptly change at some unknown time points, called breakpoints. We assume that the total number of breakpoints is fixed before the trial. We define a PS MAB as follows.

Definition 2.2 (Piecewise-Stationary Bandit).

Let be a set of MABs. Then, let be a set of timesteps and call the set of indices , where and , by convention. If is the reward-generating distribution of arm when , then defines a piecewise-stationary bandit (PS MAB, for short).

is the -th epoch of the PS MAB, and to the -th breakpoint. To simplify notation, we define as the mean of the reward-generating distribution of action during epoch . Note that the reward-generating distribution of an action is fixed during an epoch, and so is the mean reward (and every other distribution parameter). We call the magnitude of the change in the mean of arm from epoch to the next one, . By convention, and for every . In Appendix A, we review the literature on PS MABs.

Piecewise Non-stationary Heavy-Tailed Bandits. The general definition of piecewise non-stationary MABs allows for any family of reward-generating distributions, including heavy-tailed ones. In this work, we deal with piecewise non-stationary bandits where the reward-generating distributions satisfy Equation (1). We call this setting the heavy-tailed piecewise-stationary setting (HTPS, for short).

Definition 2.3 (Heavy-Tailed Piecewise-Stationary Bandits).

Let be a PS bandit. If for every , we call it a heavy-tailed piecewise-stationary bandit (HTPS MAB, for short). We denote the set of such HTPS MABs as , where .

Definition 2.3 introduces the novel bandit setting, as the intersection between HT and PS MABs. To the best of the authors’ knowledge, this setting has not been studied in previous literature.

2.2 Learning Goal

A policy is a (possibly randomized) map that receives the filtration up to time (composed of past actions and rewards) and returns an action to play. We define as the sub-optimality gap of arm during epoch , i.e., and as the number of times action has been chosen during epoch by policy up to time . The goal of a learner is to minimize the expected cumulative regret , i.e., the cumulative performance gap w.r.t. to the best policy over a learning horizon.

Definition 2.4 (Expected Cumulative Regret).

Given a policy , we define the expected cumulative regret of as:

where the expectation accounts for both the randomness of policy and reward generation.

This performance index is also called dynamic regret and is the standard choice for PS MABs. The optimal policy corresponds to choosing the best action in every epoch , i.e., . We also define some quantities that govern the statistical complexity of the instance. is the minimum change between any two breakpoints, and are the minimum and maximum sub-optimality gap during an epoch , respectively. Intuitively, the smaller is, the more difficult it is to detect breakpoints, and the smaller is, the more difficult it is to distinguish the best action. On the other hand, the larger these quantities are, the larger the regret potentially incurred with an error. When is omitted, we refer to the quantity minimized/maximized over all epochs.

2.3 Lower Bound

In this section, we provide a lower bound to the expected cumulative regret that any policy must incur in an HTPS bandit.

Theorem 2.5 (Regret Lower Bound for the HTPS Bandit Problem).

For any fixed policy , we have

| (2) |

Results of this type are known as minimax lower bounds. Indeed, the result states that, for every policy, there exists at least one instance in which the expected regret grows at a certain rate. The bound is consistent with the known lower bounds for the HT and PS MAB problems. Indeed, in HT MABs every policy has its expected regret lower bounded by (bubeck2013bandits, ), while in PS MABs the lower bound is (garivier2011upper, ). Thus, Equation (2) is a natural combination of these two results that can be recovered by either setting or . We refer to Appendix B for the proof.

3 Technical Preliminaries

In this section, we introduce the technical tools we employ in our proposed solution. First, we discuss the mean estimation for HT random variables and describe the Catoni estimator. Then, we formalize the change-point detection (CPD) problem and discuss a technique based on confidence sequences.

3.1 Mean Estimation for Heavy-Tailed Random Variables with Catoni Estimator

Mean estimation for HT variables can be quite a delicate task. Empirical mean has been proved to achieve a sub-optimal concentration (bubeck2013bandits, ). However, alternative estimators enjoying optimal rates have been proposed. We focus on the elegant Catoni estimator (catoni2012challenging, ), defined using a Catoni-type influence function . The Catoni estimator for a sequence of variables is the solution of:

| (3) |

and is a predictable process. Remarkably, for a proper choice of , this estimator enjoys an optimal concentration of order with probability bhatt2022catoni .

3.2 Confidence Sequences and Change Point Detection

The PS MAB is often addressed by resorting to change-point detection (CPD) strategies, e.g., CUSUM-UCB (liu2018change, ). The idea is to actively adapt to environmental changes and tackle the problem as a sequence of stationary MABs. These strategies are often restricted to sub-gaussian rewards and do not scale on heavy-tailed variables. We propose an alternative approach to tackle this family of problems using a CPD strategy based on confidence sequences.

Confidence Sequences. Suppose for some where is the set of distributions on such that for each , where is the filtration. A confidence sequence (CS) for the mean is a sequence of confidence intervals holding at arbitrary data-dependent stopping times. Formally:

| (4) |

The random intervals that satisfy property (4) are called -CS, where is the confidence level. For a CS defined on , we formally introduce its width after samples defined as , for all and .

Change-Point Detection. Consider a data-generating process composed of infinitely-countable distributions and let be an unknown breakpoint, i.e., for every and for every . The goal of a CPD algorithm is to detect, as soon as possible after , that a change in the data-generating distribution happened. In other words, given the (stochastic) stopping time in which the CPD system detects a change, the objective is to minimize the detection delay , where the expectation is taken over an environment having a change-point after rounds. A trivial CPD system yielding a signal at every round would minimize this quantity. On the other hand, we also desire to reduce the false alarm rate (FAR), i.e., the probability that a signal is produced when no change happens. This translates into minimizing , where is the probability measure of the environment where there is no change-point. Moreover, the average run length (ARL), defined as , represents the expected number of rounds before a change is erroneously detected. However, when ARL is too large (e.g., the trivial CPD that never yields a signal), the system is too conservative, impacting the detection delay. This highlights a crucial trade-off between detection delay and ARL. Recent literature (shekhar2023sequential, ; shekhar2023reducing, ) shed light on the possibility of reducing CPD to a sequential estimation, i.e., producing sequential testing via confidence sequences. We focus on the repeated-FCS-detector framework, introduced in shekhar2023reducing . repeated-FCS-detector is a meta-algorithm that requires a CS computation strategy and uses it as a black-box tool, defined as:

Definition 3.1 (repeated-FCS-detector, shekhar2023reducing ).

Let be a sequence of observations. At every round , we receive a new sample and initialize a new -CS for the mean , formed using samples , , , and onwards. Moreover, we update all previously initialized CS using . We define the stopping time, , as the first time at which the intersection of all initialized CS becomes empty, i.e., .

Provided an oracle capable of computing a -CS at every round, this strategy is distribution agnostic, as it requires no additional information about the data-generating distribution nor the change point. In shekhar2023reducing , theoretical guarantees on both the ARL and the detection delay of repeated-FCS-detector are provided expressed in terms of the width of the -CS provided to the detector. We now report the theoretical guarantees of repeated-FCS-detector.

Theorem 3.2 (Guarantees of repeated-FCS-detector, shekhar2023reducing ).

Consider a CPD problem with observations i.i.d. from for and from for . Let . Suppose we can construct -confidence sequences with pointwise width and for pre- and post-change mean, respectively. Then, we have: (i) When there is no changepoint, the repeated-FCS-detector satisfies ; (ii) Suppose and large enough to ensure that . Introduce the event , and note that by construction. Then, for , we have , where .

Point (i) provides a lower bound on the ARL of repeated-FCS-detector, while (ii) upper bounds the expected detection delay. While ARL only depends on the desired confidence level, the detection delay depends on the width of the CSs. Indeed, the width of the CS must decrease fast enough to make the change detectable. This assumption is standard in CPD, as enough samples before the change are needed to model the null hypothesis correctly.

4 Robust Regret Minimization in Piecewise-Stationary Heavy-Tailed Bandits

In this section, we describe our strategy for regret minimization in HTPS MABs. We start by providing a CPD strategy suited for heavy-tailed random variables together with its theoretical guarantees. Then, we leverage this tool to build a meta-algorithm named Robust-CPD-UCB, which uses a regret minimizer for the stationary setting and the CPD strategy to tackle non-stationarity.

4.1 Catoni-FCS-detector

We start by introducing a novel CPD strategy for HT random variables, which we name Catoni-FCS-detector, based on a repeated-FCS-detector using a special type of CS. We can define Catoni-FCS-detector as a special instantiation of repeated-FCS-detector.

Definition 4.1 (Catoni-FCS-detector).

An instance of repeated-FCS-detector is a Catoni-FCS-detector if the -CS is defined as:

| (5) |

where is the Catoni-type influence function (Equation 3).

From now on, we call Catoni CS the confidence sequence defined as in Equation (5). Catoni CS have been introduced for the first time in wang2023catoni . While a Catoni CS does not admit a trivial closed-form representation, it can be proven (see Appendix B) that Equation (5) represents a proper -CS for the mean, attaining an optimal width (bhatt2022catoni, ). To use Catoni-FCS-detector in a bandit problem, however, we need specific types of guarantees, different than the ones provided for the general repeated-FCS-detector framework. We now provide two novel contributions of independent interest. First, we show how the width of the Catoni CS can be narrowed further w.r.t. to the one presented in previous works in the case of infinite variance. Second, we provide a finite-time bound on the detection delay of Catoni-FCS-detector, a crucial property for using a CPD in a bandit.

Proposition 4.2 (Detection Delay of Catoni-FCS-detector).

Consider a CPD problem with observations drawn i.i.d. from for and from for . Let . Suppose that there exists a known upper bound of the change point (). Let and suppose large enough s.t. . Set . Then, there exists a predictable sequence s.t. Catoni-FCS-detector enjoys (i) and (ii) .

We point out the importance of this specialized result. Since the guarantees of Theorem 3.2 are very general, this result is aimed at providing a finite-time, high-probability bound on the detection delay when using Catoni CS. In particular, we make the term from Theorem 3.2 explicit by using the properties of Catoni CS. Due to space reasons, the proof is postponed to Appendix B. Note that the rate of this detection delay cannot be improved as the lower bound for the detection delay of any distribution change is (lorden1971procedures, ), where the confidence parameter that we set to . Moreover, the dependencies on , and may also be tight, as they embed the log-likelihood ratio of the test for the means of heavy-tailed random variables. We leave the answer to this question for further investigations. We conclude this section with two important remarks.

Remark 4.3 (Comparison with Existing CPDs).

Catoni-FCS-detector is, to the best of authors’ knowledge, the first CPD strategy for the mean of HT random variables with infinite variance enjoying such guarantees. Thus, we consider our analysis an interesting standalone contribution. In bandit literature, however, many CPD strategies have been employed, (e.g., CUSUM (liu2018change, ) and GLR Test (besson2022efficient, )). However, they do not cover the HT scenario and often rely on strong parametric assumptions on the sample-generating distribution, e.g., only working on Bernoulli variables.

Remark 4.4 (On the a priori knowledge of Catoni-FCS-detector).

Catoni-FCS-detector does not rely, in principle, on any prior knowledge of the magnitude of the change or on the means. The confidence parameter is set based on the time horizon , which is standard in MABs. Moreover, the sequence can be set in advance for every , only relying on the knowledge of .

4.2 Robust-CPD-UCB

In this section, we introduce Robust-CPD-UCB (R-CPD-UCB for short, Algorithm 1), an algorithm for PS HT bandits. R-CPD-UCB actively adapts to the changes in the reward-generating distribution. The algorithm has three components: a sub-algorithm suited for the stationary HT MAB problem, that aims to minimize the regret in the stationary segments, we call this policy ; the Catoni-FCS-detector strategy for CPD; and a cyclic uniform exploration that ensures the availability of enough samples for every action to perform the CPD test. Algorithm 1 proceeds as follows: roughly every rounds it tries all the actions once (lines 4-5), this ensures that CPD can happen efficiently even when underrepresented actions in the history are the only ones changing. In the other rounds, a bandit sub-routine (e.g., Robust-UCB) plays according to all the history since the last reset (lines 8-9); once the new reward is obtained, it is fed to the Catoni-FCS-detector that verifies if a change point occurred (lines 12-14), in this case, everything is reset (line 15-16).

Remark 4.5.

(Connection to Monitored-UCB from cao2019nearly ) Robust-CPD-UCB borrows the idea of cyclic uniform exploration from the Monitored-UCB cao2019nearly . Moreover, as most of the algorithms for the PS setting, ours share the usage of a stationary bandit sub-routine. However, a crucial difference relies on the type of CPD strategy employed. Monitored-UCB leverages a sliding-window type of CPD strategy that checks if the average of the first half of the sliding-window is significantly different from that of the second half. This type of CPD strategy requires two hyper-parameters, the window size and the threshold, respectively. Tuning these parameters may be difficult, even though, in practice, the algorithm works well even under misspecification. Finally, Monitored-UCB only deals with rewards bounded in , while Robust-CPD-UCB deals with HT rewards.

Remark 4.6.

(Priori Knowledge of R-CPD-UCB) Algorithm 1 receives as inputs the time horizon , the uniform exploration coefficient , and a regret minimizer for the stationary setting only. Assuming that it is possible to choose a regret minimizer that does not require additional parameters other than (which is, as we will show in the next section, rather natural), then the only knowledge that R-CPD-UCB requires on the environment is the time horizon . Thus, in principle, our algorithm requires knowledge of only. In practice, this property ensures that no tuning must happen.

4.3 Theoretical Guarantees of Robust-CPD-UCB

As customary in the literature of PS MABs, we introduce a technical assumption regarding the length of any epoch ensuring that exploration is frequent enough to detect for every action.

Assumption 4.7.

For every epoch , let , and let be its length and . The learner can select such that, for every , it holds that .

This assumption ensures that proper learning can be performed in such an environment Indeed, we enforce that every epoch is large enough so that, due to the forced exploration only, the algorithm chooses every action at least times. This kind of assumption is ubiquitous in the piecewise-stationary bandits literature. Notable examples include Assumptions 4 and 7 in (besson2022efficient, ), Assumptions 1 and 2 in (cao2019nearly, ) and Assumption 1 in (liu2018change, ). Some are equivalent to ours, while others are neither weaker nor stronger. Alternative assumptions, such as the monotonicity of the mean change, also allow for theoretical tractability, e.g., Assumption 1 in (seznec2020single, ), which forces expected rewards to evolve in a decreasing manner. Note that Assumption 4.7 is a technical assumption aimed at the theoretical analysis of the algorithm. Algorithm 1 can operate regardless of this assumption, as shown in Section 5. We are now ready to present our main result.

Theorem 4.8 (Regret Upper Bound of R-CPD-UCB).

Under Assumption 4.7, R-CPD-UCB suffers an expected cumulative regret bounded as:

| (6) |

The regret can be decomposed into three contributions due to: the detection delay (part (A)), the regret-per-epoch of the stationary policy (part (B)), and the rounds of uniform exploration (part (C)).

Uniform Exploration Trade-off. The uniform exploration parameter appears in both (A) and (C). Setting aside part (B), it is clear that creates a trade-off between these two: the larger is, the quicker the algorithm can detect a change, and the smaller is (A); on the other hand, excessive uniform exploration inflates the regret of R-CPD-UCB and the contribution from (C). Finding the optimal value for would require extensive prior knowledge, which is, in general, not available. A good trade-off is to set , which impose both (A) and (C) to be . However, it is possible to define a forced exploration strategy that does not require any knowledge of , making the algorithm more versatile while keeping the same order of performance. In particular, we can leverage the methodology developed in besson2022efficient and obtain the following result.

Corollary 4.9.

Let where for some be an increasing sequence. R-CPD-UCB using after the -th detection satisfies:

| (A) | (7) |

Note that, if is known, setting can further reduce the regret bound.

Choosing . The choice of the inner regret minimizer determines the magnitude of part (B). The best choice is to select a policy that has a regret upper bound matching the known lower bound of . We can instantiate R-CPD-UCB using the Robust UCB policy with median-of-means estimator from (bubeck2013bandits, , Section 2.2). As a result, we get the following bounds.

Corollary 4.10.

Let be the Robust UCB policy with median-of-means estimator (bubeck2013bandits, , Section 2.2). Under Assumption 4.7, R-CPD-UCB suffers an expected cumulative regret bounded as:

| (8) |

Moreover, if for every , we have:

| (9) |

Equation (8) is a direct consequence of Theorem 4.8 and Theorem 3 of bubeck2013bandits . Equation (9) follows from Theorem 4.8, Proposition 1 of bubeck2013bandits , and Jensen’s inequality. Robust UCB enjoys both instance-dependent and instance-independent guarantees: part (B1) depends on the sub-optimality gaps and the individual lengths of the epochs, while part (B2) does not, as it accounts for a worst-case scenario of the sub-optimality gaps. We can now combine all and get the following.

Corollary 4.11.

Let be the Robust UCB policy with median-of-means estimator from (bubeck2013bandits, , Section 2.2). Let where for some . Under Assumption 4.7, R-CPD-UCB using after the -th detection suffers an expected cumulative regret bounded as:

| (10) |

Moreover, if for every , and , we have:

| (11) |

Equation (10), depends on both the minimum mean change , and the extreme sub-optimality gaps and , along the whole trial. We consider this bound an instance-dependent guarantee over the performance of R-CPD-UCB. Equation (11), instead, does not contain any of these quantities. The second assumption fundamentally states that can be assumed to be a constant w.r.t. the other quantities, in particular . In this case, an instance-independent bound can be obtained. Equation (11) matches, up to constants, the lower bound presented in Theorem 2.5. Thus, if we focus on the dependence on , , , and the performance guarantees of R-CPD-UCB are nearly-optimal.

5 Numerical Evaluation

We now provide a numerical evaluation of Robust-CPD-UCB ( chosen as Robust UCB with median-of-means estimator). We refer to Appendix C for additional details and experimental campaigns.

5.1 Casting Real-World Data to HTPS MABs

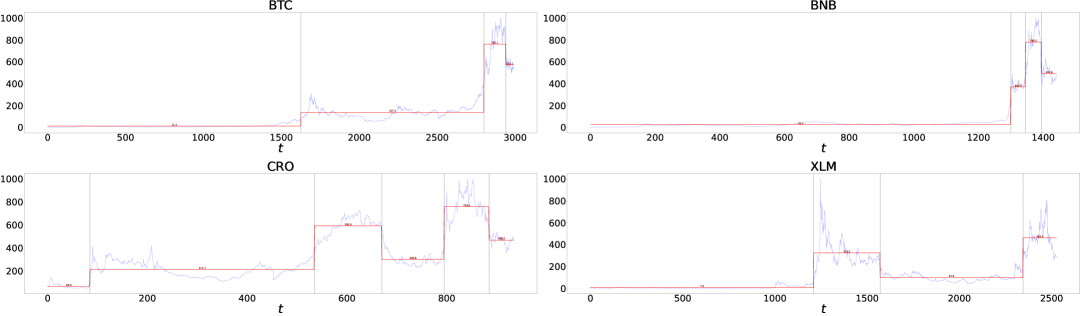

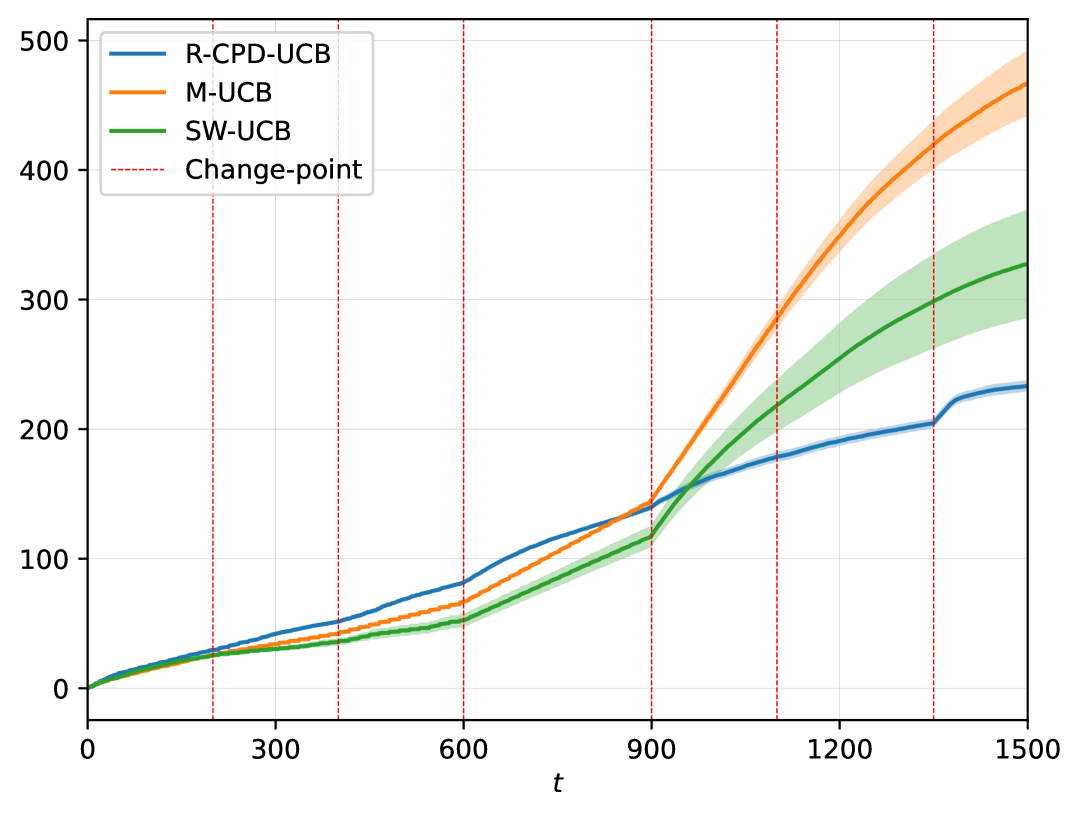

We model a real-world scenario as an HTPS MAB and, then, we leverage a real dataset to generate an HTPS MAB instance on which R-CPD-UCB is tested. Setting. We consider the problem of profit maximization in financial trading. As pointed out by panahi2016model , financial data exhibit heavy tails. A financial application of HT MABs is identifying the most profitable cryptocurrency among options. In fact, at the start of each day, an investor would like to invest a share of their money in the cryptocurrency with the highest closing price. This very same application has been studied, for example, in yu2018pure and lee2022minimax , both in the context of HT MABs. We use the same dataset (Kaggle link) employed in lee2022minimax . In Figure 1, we report the closing prices of four selected currencies among the top ten by market capitalization, along with a piecewise-constant fit of the data that minimizes the squared error. We observe two things: first, the piecewise constant approximation is a better fit than any constant approximation (in the previous works on HT MABs, the reward from a given currency was always considered stationary); second, this approximation suffers a high error in certain segments where the stochastic fluctuations are really strong. Following the existing literature panahi2016model , we fit the price distribution inside every segment with a Pareto distribution having its mean centered on the segment height, using and . Thus, the profit maximization problem in cryptocurrency trading can be treated as an HTPS MAB. Results. Starting from the piecewise-constant fit of the prices, we can build an HTPS MAB environment on which we test R-CPD-UCB, together with Sliding Window UCB garivier2011upper and MR-APE lee2022minimax , which was already tested on the same dataset when assuming stationarity. In Figure 2, we report the cumulative regrets obtained by the three algorithms averaged over trials (-axis is rescaled). R-CPD-UCB performs better than the two competitors, as it is the only algorithm tackling both heavy-tailedness and non-stationarity of the setting.

![[Uncaptioned image]](/html/2505.20051/assets/x2.png) Figure 2: Cumulative regrets on HTPS built from cryptocurrency dataset. trials, mean std.

Figure 2: Cumulative regrets on HTPS built from cryptocurrency dataset. trials, mean std.

(a) Gaussian rewards.

(a) Gaussian rewards.

(b) Pareto rewards.

Figure 3: Cumulative regrets. trials, mean std.

(b) Pareto rewards.

Figure 3: Cumulative regrets. trials, mean std.

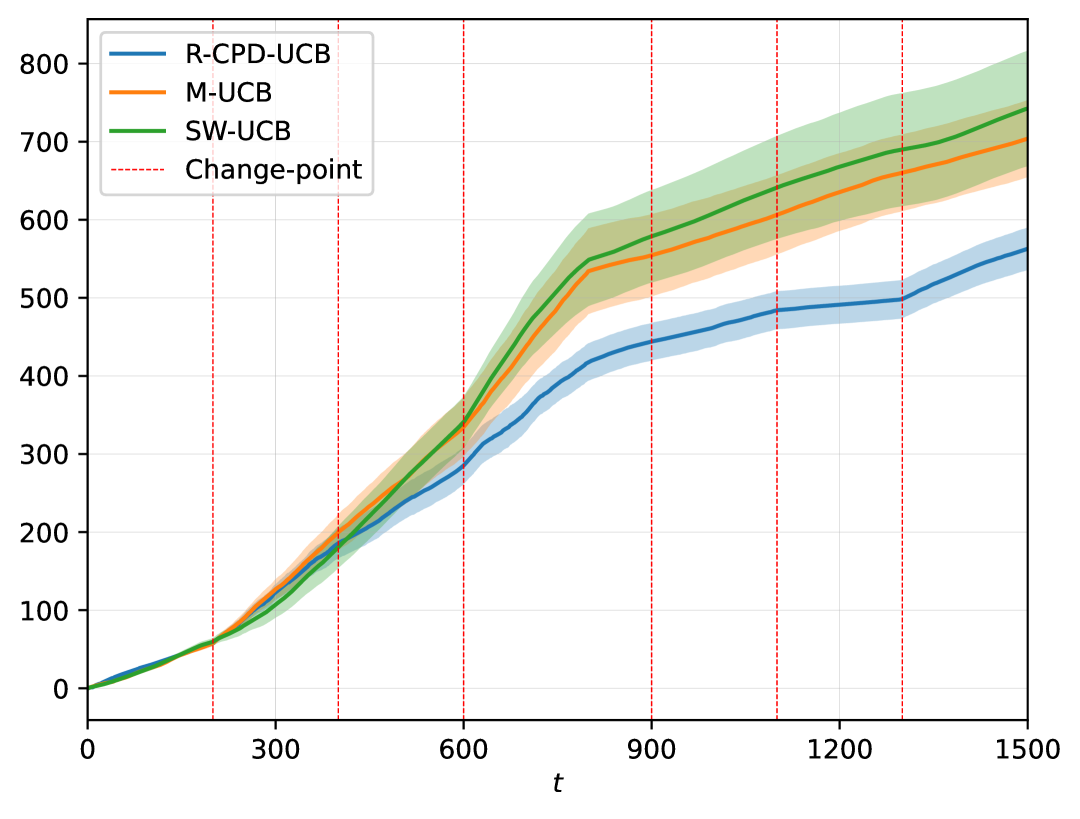

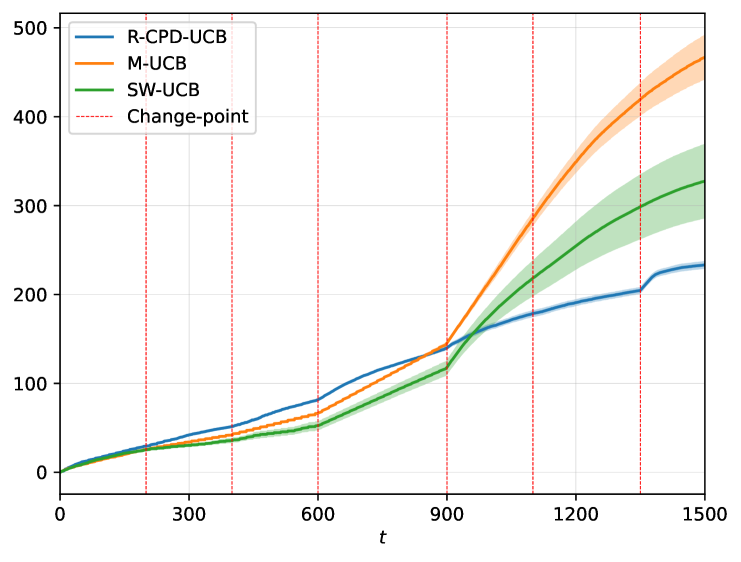

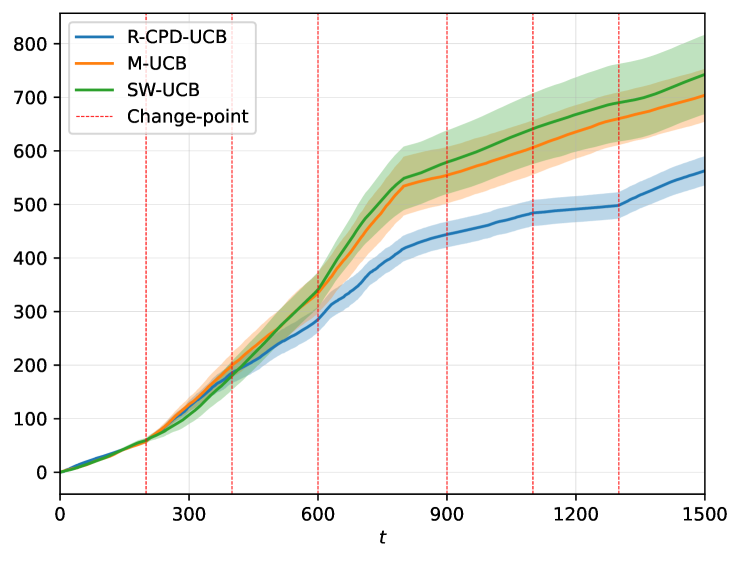

5.2 Regret Minimization in Highly Non-Stationary Environments

We now evaluate how R-CPD-UCB behaves in highly dynamic scenarios where changes are close.

Setting. We compare R-CPD-UCB with two of the most popular algorithms from the literature, Monitored UCB cao2019nearly and Sliding Window UCB garivier2011upper . We consider two PS MABs: Gaussian rewards with and Pareto rewards with . In both MABs, we have , and . Also, we have , i.e., and some actions may not change their means after a change point. However, at least one arm has its mean change, and the optimal action changes at least times. Interestingly, these instances violate Assumption 4.7. Results. In Figure 5, we report the cumulative regrets suffered by the considered algorithms. R-CPD-UCB achieves, in both instances, a smaller cumulative regret than competitors. Moreover, it shows a smaller uncertainty and more stable performances across the trials, especially when rewards have infinite variance (Figure 5(b)). Interestingly, R-CPD-UCB can outperform both Monitored UCB and Sliding Window UCB even when the rewards are Gaussian. This is because the change points are frequent and very close. Robust mean estimation using median-of-means stabilizes the algorithm’s behavior in data-scarce regimes. Finally, we remark that Assumption 4.7 is violated by these two instances; however, R-CPD-UCB performs well (and so is Monitored UCB, which relies on a similar hypothesis). This phenomenon was already observed in cao2019nearly , and shows how Assumption 4.7, in practice, is not very limiting.

6 Conclusions

In this work, we provided the first study on regret minimization in heavy-tailed piecewise-stationary bandits. We provided a lower bound on the performance of every algorithm and proposed Robust-CPD-UCB, a novel algorithm whose regret nearly matches the lower bound. We leverage novel advancements in the theory of change-point detection, building Catoni-FCS-detector, a general detection strategy suited for distributions with infinite variance. Finally, numerical evaluation shows that the performance of R-CPD-UCB is solid when compared to existing baselines. An interesting future direction would be to study the HTPS MAB problem when and are unknown.

References

- [1] Yasin Abbasi-Yadkori, Dávid Pál, and Csaba Szepesvári. Improved algorithms for linear stochastic bandits. Advances in neural information processing systems, 24, 2011.

- [2] Peter Auer, Pratik Gajane, and Ronald Ortner. Adaptively tracking the best bandit arm with an unknown number of distribution changes. In Conference on Learning Theory, pages 138–158. PMLR, 2019.

- [3] Omar Besbes, Yonatan Gur, and Assaf Zeevi. Stochastic multi-armed-bandit problem with non-stationary rewards. Advances in neural information processing systems, 27, 2014.

- [4] Lilian Besson, Emilie Kaufmann, Odalric-Ambrym Maillard, and Julien Seznec. Efficient change-point detection for tackling piecewise-stationary bandits. Journal of Machine Learning Research, 23(77):1–40, 2022.

- [5] Sujay Bhatt, Guanhua Fang, and Ping Li. Piecewise stationary bandits under risk criteria. In International Conference on Artificial Intelligence and Statistics, pages 4313–4335. PMLR, 2023.

- [6] Sujay Bhatt, Guanhua Fang, Ping Li, and Gennady Samorodnitsky. Catoni-style confidence sequences under infinite variance. arXiv preprint arXiv:2208.03185, 2022.

- [7] Sébastien Bubeck, Nicolo Cesa-Bianchi, and Gábor Lugosi. Bandits with heavy tail. IEEE Transactions on Information Theory, 59(11):7711–7717, 2013.

- [8] Yang Cao, Zheng Wen, Branislav Kveton, and Yao Xie. Nearly optimal adaptive procedure with change detection for piecewise-stationary bandit. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 418–427. PMLR, 2019.

- [9] Olivier Catoni. Challenging the empirical mean and empirical variance: a deviation study. In Annales de l’IHP Probabilités et statistiques, volume 48, pages 1148–1185, 2012.

- [10] Aurélien Garivier, Pierre Ménard, and Gilles Stoltz. Explore first, exploit next: The true shape of regret in bandit problems. Mathematics of Operations Research, 44(2):377–399, 2019.

- [11] Aurélien Garivier and Eric Moulines. On upper-confidence bound policies for switching bandit problems. In International conference on algorithmic learning theory, pages 174–188. Springer, 2011.

- [12] Gianmarco Genalti, Lupo Marsigli, Nicola Gatti, and Alberto Maria Metelli. -adaptive regret minimization in heavy-tailed bandits. In The Thirty Seventh Annual Conference on Learning Theory, pages 1882–1915. PMLR, 2024.

- [13] Gianmarco Genalti, Marco Mussi, Nicola Gatti, Marcello Restelli, Matteo Castiglioni, and Alberto Maria Metelli. Graph-triggered rising bandits. In Forty-first International Conference on Machine Learning, 2024.

- [14] Cédric Hartland, Nicolas Baskiotis, Sylvain Gelly, Michele Sebag, and Olivier Teytaud. Change point detection and meta-bandits for online learning in dynamic environments. In CAp 2007: 9è Conférence francophone sur l’apprentissage automatique, pages 237–250, 2007.

- [15] Hoda Heidari, Michael J Kearns, and Aaron Roth. Tight policy regret bounds for improving and decaying bandits. In IJCAI, pages 1562–1570, 2016.

- [16] Steven R Howard, Aaditya Ramdas, Jon McAuliffe, and Jasjeet Sekhon. Time-uniform, nonparametric, nonasymptotic confidence sequences. The Annals of Statistics, 49(2), 2021.

- [17] Levente Kocsis and Csaba Szepesvári. Discounted ucb. In 2nd PASCAL Challenges Workshop, volume 2, pages 51–134, 2006.

- [18] Tor Lattimore and Csaba Szepesvári. Bandit algorithms. Cambridge University Press, 2020.

- [19] Kyungjae Lee and Sungbin Lim. Minimax optimal bandits for heavy tail rewards. IEEE Transactions on Neural Networks and Learning Systems, 35(4):5280–5294, 2022.

- [20] Fang Liu, Joohyun Lee, and Ness Shroff. A change-detection based framework for piecewise-stationary multi-armed bandit problem. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 32, 2018.

- [21] Gary Lorden. Procedures for reacting to a change in distribution. The annals of mathematical statistics, pages 1897–1908, 1971.

- [22] Alberto Maria Metelli, Francesco Trovo, Matteo Pirola, and Marcello Restelli. Stochastic rising bandits. In International Conference on Machine Learning, pages 15421–15457. PMLR, 2022.

- [23] Hanieh Panahi. Model selection test for the heavy-tailed distributions under censored samples with application in financial data. International Journal of Financial Studies, 4(4):24, 2016.

- [24] Julien Seznec, Andrea Locatelli, Alexandra Carpentier, Alessandro Lazaric, and Michal Valko. Rotting bandits are no harder than stochastic ones. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 2564–2572. PMLR, 2019.

- [25] Julien Seznec, Pierre Menard, Alessandro Lazaric, and Michal Valko. A single algorithm for both restless and rested rotting bandits. In International Conference on Artificial Intelligence and Statistics, pages 3784–3794. PMLR, 2020.

- [26] Shubhanshu Shekhar and Aaditya Ramdas. Reducing sequential change detection to sequential estimation. arXiv preprint arXiv:2309.09111, 2023.

- [27] Shubhanshu Shekhar and Aaditya Ramdas. Sequential changepoint detection via backward confidence sequences. In International Conference on Machine Learning, pages 30908–30930. PMLR, 2023.

- [28] Hongjian Wang and Aaditya Ramdas. Catoni-style confidence sequences for heavy-tailed mean estimation. Stochastic Processes and Their Applications, 163:168–202, 2023.

- [29] Jia Yuan Yu and Shie Mannor. Piecewise-stationary bandit problems with side observations. In Proceedings of the 26th annual international conference on machine learning, pages 1177–1184, 2009.

- [30] Xiaotian Yu, Han Shao, Michael R Lyu, and Irwin King. Pure exploration of multi-armed bandits with heavy-tailed payoffs. In UAI, pages 937–946, 2018.

Appendix A Additional Related Works on Non-Stationary MABs

In this appendix, we discuss more in detail the related works on non-stationary MABs.

A.1 Piecewise-Stationary MABs

The most common definition of piecewise-stationary MABs in the literature is the one introduced by [29]. In this work, the authors deal with the PS MAB problem as it is defined in this work, and consider both a scenario in which side-observations are available, and an agnostic scenario in which they are not, which corresponds to the one that we study in this work. In the latter scenario, they show that every algorithm must suffer at least regret. In [11], the authors analyze two algorithms to tackle the PS MAB problem, namely Discounted UCB (introduced in [17]) and Sliding Window UCB. Contrary to ours, these algorithms don’t rely on any CPD strategy but rather passively adapt to the changes in the environment. In practice, actively adapting algorithm, e.g., algorithm based on CPD strategies like ours, hence show better performances. The idea of actively adapt to changes first appeared in [14]. More recent works, such as [20] and [8], paved the way for the analysis of actively adaptive algorithms, which were considered tougher to analyze from a theoretical perspective w.r.t. to their passive counterparts. Recently, with [2] and [4], there has been focus on removing the prior knowledge on from the algorithms. In the former, the AdSwitch algorithm they propose does not require any additional assumptions, but it is not optimized for tractability or numerical efficiency. Indeed, as shown in [4], AdSwitch enjoys poor empirical performance. In the latter, the authors propose an algorithm that performs well in practice and has tight theoretical guarantees without any need for to be known beforehand, however they rely on an assumption which is nearly the same as ours. All of the aforementioned works don’t account for the heavy-tailed setting, as their scope is restricted to rewards with bounded support or sub-gaussian. The only work that accounts for non-stationarity in heavy-tailed settings is [5], where the authors consider a general framework to allow for more general risk measures (linear being the case considered here), and consider the same setup of piecewise-stationary bandits and heavy-tailed rewards, and establish upper and lower bounds on the regret under special assumptions on the risk measures and distributions. However, there are multiple reasons for why our approach is better suited in the regret-minimization scenario:

-

•

Assumption 1 (Stability): since their paper focuses on achieving strong regret guarantees with heavy-tailed rewards, the stability assumption plays a crucial role in the analysis, where the rate functions on the decay of the empirical and truncated distributions are assumed to be known. While the assumption is not strong in and of itself, the knowledge of these parameters play a crucial role in the change detection and regret minimization procedures, and also appear in the regret bounds. Robust-CPD-UCB, on the other hand, requires no knowledge of such functions, relies on novel analysis of Catoni estimators that do not necessitate truncations, and is simpler to run online in practice.

-

•

The CPD routine used in [5] is based on a sliding window method requiring specification of both widow size and threshold. Robust-CPD-UCB is based on the newly developed CPD method based on Catoni estimator that runs online only with the same assumption on the distributions.

-

•

The regret minimization algorithm in [5] uses a data-driven truncation of the rewards that depends on the policy, and the knowledge of the decay rate functions to compute the exploration bias for the arm index. Our work, on the other hand, requires no such methods and uses a simple combination of the novel Catoni-CPD and any policy suited for the stationary heavy-tailed regret minimization.

For the most common case of linear risk/ regret in mean, Robust-CPD-UCB establishes stronger guarantees with the CPD procedure requiring weaker assumptions. Finally, it is easier to implement owing to not requiring distributional knowledge or thresholds.

A.2 Bounded Variation and Monotonically Non-stationary MABs

Another setting of interest is non-stationary MABs with bounded variations. In this setting, the rewards’ distributions changes are less restricted, and the focus moves from the number of changes to the total amount of change . In [3], the authors propose Rexp3, an algorithm that leverages tools from the adversarial MAB problem to deal with non-stationarity in stochastic settings. The regret upper bound that they provide is in the order of . Over the last years, there has been increasing interest in monotonically non-stationary MABs, i.e., non-stationary MABs where the mean rewards are only allowed to decrease (rotting bandits, [24, 25]) or to increase (rising bandits, [22]), some works focus on both settings [15, 13]. The monotonicity assumptions substitutes the need for piecewise-stationarity, as it is a strong enough assumption to allow for strong theoretical characterizations. In such settings, regret bounds depend in general on the total variation of the distributions’ means and instance-dependent-type of results are common in this literature. Moreover, the additional structure added by this assumption, put the accent on the difference between restless bandits (a proper non-stationary setting) and rested bandits, where the evolution of rewards depends on learner’s actions rather than just time.

Appendix B Proofs

See 2.5

Proof.

The proof of this theorem combines techniques from Lemma 5 of [25], Theorem 4 of [12], and Theorem 6 from [10].

Consider the following prototype of reward distribution, defined for and :

It is easy to verify that for every .

Consider a set of of instances belonging to indexed by a vector in a way that, for every and every , we have

It follows that for every and . Let for every , assuming w.l.o.g. that is divisible by . Thus, all epochs are of the same length. For every fixed policy , we write the average expected regret among the instances indexed by :

| (12) |

where equals to where the -th coordinate is set to and equals to where the -th coordinate is set to , for .

Let be the Kullback-Leibler divergence between and , then we have:

where the inequality follows by upper bounding the first addendum with . Using Pinsker Inequality and the previous bound on the KL divergence, for every , we get

that implies

| (13) |

Combining Equation (12) and Equation (13), we get

by setting . ∎

Remark B.1.

In the proof of Theorem 2.5, we do not impose any condition on . Moreover, the length of every epoch is equal to . This means that in principle one can choose a large enough , i.e., , such that Assumption 4.7 holds. This proves that our assumption does not make the problem easier from a regret minimization perspective.

See 4.2

Proof.

Due to its length, we divided this proof into several steps. In Steps 1-3 we extend Theorem 10 of [28] to the case of heavy-tailed random variables. In Step 4 we apply the sticthing technique to the resulting CS, tightening its width. Then, in Step 5 we define the CS hyper-parameters and define a set of good events, under which we are able to properly bound the detection delay in Step 7. The proof is concluded by showing that no false alarm occurs under the good event (Step 8).

Step 1 (Building a nonnegative supermartingale) First, we observe that

are nonnegative supermartingales. To prove this for (all steps are analogous for ), we bound

and, subsequently,

Step 2 (Building a CS for ) Then, we can leverage Ville’s inequality to construct a CS around :

which implies

Analogous calculations for and a union bound, yield a -CS where the intervals have the following form:

Step 3 (Bounding the width of the CS for ) We are now required to provide a bound on the width of the previously derived -CS. To do so, we derive high-probability lower and upper bounds over the random solution of . For all , let

then, with steps analogous to Step 1, we observe that is a nonnegative supermartingale. Note that , and an analogous definition leads to the nonnegative supermartingale . We define:

and using Markov’s ineqality we get:

Since upper bounds with probability at least , any s.t.

| (14) |

also satisfies

| (15) |

where is a non-random quantity as it’s the solution to a deterministic equation. As is a non-increasing function of , Equation (15) implies that:

Note that Equation (14) admits solutions if and only if

| (16) |

Finally, we conclude this step by bounding

which yields the upper CS on in the following form:

Repeating all the previous steps for , and by applying a union bound, yields a two-sided -CS for . The width of such CS concentrates as

| (17) |

Step 4 (Stitching) We now discuss the choice of the sequence . The idea is to partition time in an exponential grid, and then fix the same value of inside the same cell. Moreover, the confidence level is modified and set to a cell-specific value . This idea, called stitching, first appeared in [16]. In particular, set , , and . Then, for every , we set for every . Assume . For every , we have

Noting that , this yields a tight bound over the width of the -CS for .

Step 5 (Good event characterization) As the width derived in the previous steps is not deterministic, we now characterize a favorable event in which such bound hold simultaneously for all -CS. For any -CS of length , we have that

Thus, considering a stream of samples, the probability of this to be violated for at least one interval of the -CS is bounded as

The event , defined above, represents a good event in which the -CS starting from have the widths of the single CIs deterministically bounded up until horizon . Now, we note that if we have different -CS of lengths , we define . This event describe the scenario in which all -CS starting sequentially before have the widths of all of their CIs bounded. Using another union bound argument, we can see that . Finally, note that , for every and . Thus for every . Characterizing this event is necessary since Catoni-FCS-detector requires that CS widths well behave, i.e., they possess a deterministic upper bound.

We also introduce the event , that represents the scenario in which every -CS starting from a timestamp greater or equal than never miscovers the true mean up to time . By the definition of -CS, we have . From now on, we continue by setting .

Step 6 (Verifying condition (16))

For every , we use the previously defined values for , and , and solve inequality (16). We obtain that it is satisfied for every , which is always true under the theorem’s assumptions.

Step 7 (Bounding the detection delay) We are now ready to bound the detection delay of Catoni-FCS-detector after a change of magnitude happened after samples. Note that we assume to be large enough to satisfy Equation (16). To do so, we leverage the width of the -CS that has just been derived. Suppose, without loss of generality, that a change point is detected after at most overall samples. Thus, we work under the events , , and , defined in Step 5, which hold simultaneously with probability at least , and guarantee that the CS widths are always properly bounded and the pre-change mean and the post-change mean are never miscovered. By assumption, is large enough to ensure

and we have to find an s.t.:

We first bound , that holds under the trivial requirements that and . Moreover, we define and . Thus, we can find an upper bound on the expected detection delay by solving the following:

If , then . Else, for , we define

and note that . We can thus upper bound them separately. It is trivial to observe that

Upper bounding requires additional effort. We start by identifying a value which satisfies

Let , and , then

Since is an upper bound on the expected detection delay, we have

As a consequence, we can rewrite:

which immediately implies that

Under the events defined above and that hold with probability at least , the detection delay is bounded as

Step 8 (Bounding the probability of false alarm)

The bound on the probability of false alarm is a trivial consequence of the definition of event . Under this event, it is impossible by construction for the detector to raise a false alarm, as all the CS always intersect at least on . Thus, the probability of false alarm is bounded by . ∎

Lemma B.2.

Let be the event in which R-CPD-UCB restarts exactly times without false alarms and excessive delays. Then, we have .

Proof.

Note that, by construction of the algorithm, each action is sampled at least times after timesteps have passed since the last detection point. Thanks to Assumption 4.7, the length of every epoch is at least .

Let be the event in which all detections happened without false alarms and excessive delays up to the -th epoch. Then, by a union bound and by Proposition 4.2, we have:

∎

See 4.8

Proof.

Let be the event in which R-CPD-UCB restarts exactly times without false alarms and excessive delays.

We start by decomposing the regret in the following way:

where the second inequality follows from Lemma B.2. We can now focus on bounding the first addendum. We decompose it as follows:

where the inequality follows by upper bounding the contribution to the regret given by the forced exploration in the first rounds, the remaining term is the expected regret accrued by the policy up to . We prosecute by bounding the first addendum as follows:

where is the expectation according to an environment starting from the second segment. Putting all together, we can write

which yields, by a recursive application:

where the second inequality follows from the definition of . The proof is concluded by substituting with its definition. ∎

See 4.10

Proof.

See 4.11

Proof.

First, note that the proof of Theorem 4.8 can be conducted in the exact same way by substituting with the sequence . Note that, thanks to event the algorithm restarts exactly times. Equation (11) is a trivial consequence of the fact that for every , due to the monotonocity of the sequence. Moreover, we bound .

To prove Equation (10), we need an additional step. In particular:

Plugging this in (A), and bounding for every , concludes the proof. ∎

Appendix C Additional Numerical Evaluations

In this appendix, we provide additional details on the experimental evaluation of Section 5 and additional experimental campaigns in synthetic environments.

C.1 Detection Delay Analysis

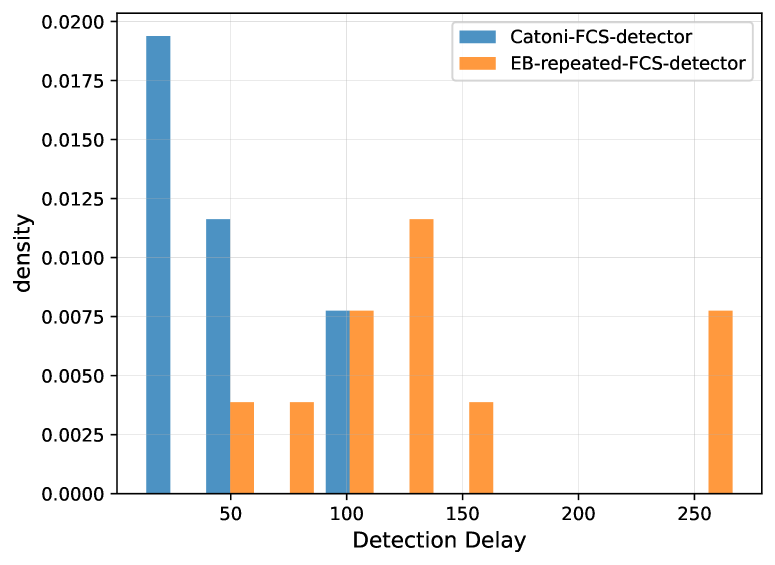

We evaluate how reactive is Catoni-FCS-detector to changes of data-generating distribution, and comparing it repeated-FCS-detector with Empirical Bernstein CSs from [26], Section 2.2, which is suited for distributions with finite variance. We consider two distribution-shift scenarios: Gaussian distributions with and Laplace distributions with scale equal to . The change happens after steps, and the total horizon is . The magnitude of change is . In Figure 4, we report the distribution of the detection delay of both algorithm over trials. We can see how, in general, Catoni-FCS-detector has a smaller detection delay w.r.t. repeated-FCS-detector. Moreover, no false alarm is raised along the trials.

C.2 Regret Minimization in Highly Non-Stationary Environments

In this section, we evaluate how R-CPD-UCB behaves in highly dynamic scenarios where change-points are close.

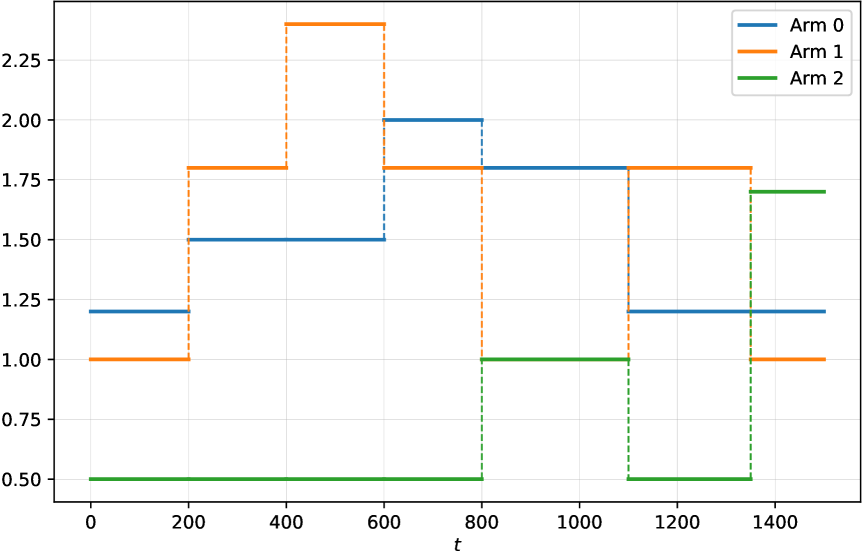

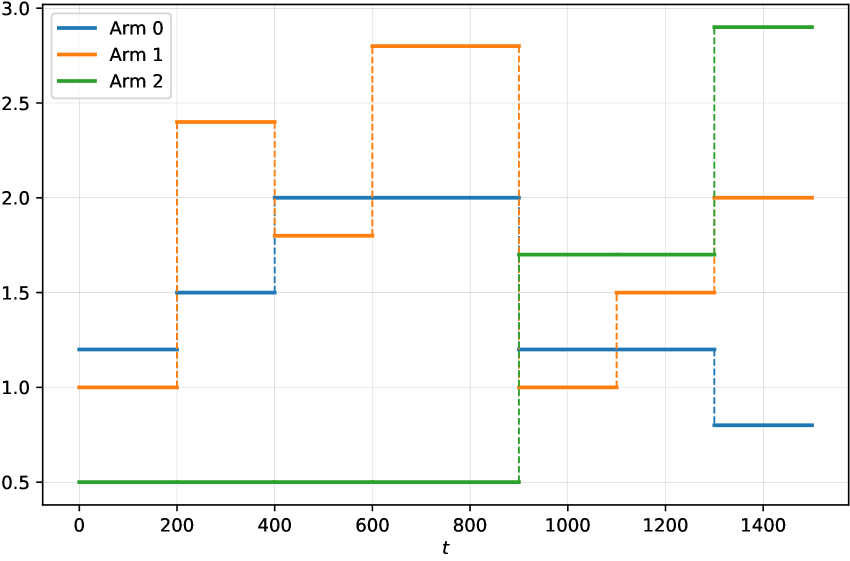

Setting We confront R-CPD-UCB with two of the most popular algorithms from the literature, Monitored UCB [8] and Sliding Window UCB [11]. We consider two PS MABs: Gaussian rewards with and Pareto rewards with and . In both MABs, we have , and . Also, we have , i.e., and some actions may not change their means after a change-point. However, at least one arm has its mean change, and the optimal action changes at least times. Interestingly, these instances violate Assumption 4.7. We use and the means reported in Table 1(a) for the Gaussian scenario. The optimal actions change times. For the Pareto scenario, we use , , and the means reported in Table 1(b). The optimal actions change times. In Figure 7 we report the means of every action in every epoch.

Results In Figure 5, we report the cumulative regrets suffered by the considered algorithms. For each instance and algorithm, we performed trials and reported the average cumulative regrets with their aleatoric uncertainties. R-CPD-UCB achieves, in both instances, a smaller cumulative regret than competitors. Moreover, it shows a smaller uncertainty and more stable performances across the trials, especially when rewards have infinite variance (Figure 5(b)). Interestingly, R-CPD-UCB can outperform both Monitored UCB and Sliding Window UCB even when the rewards are Gaussian. This is probably because the change-points are frequent and very close. Robust mean estimation using median-of-means stabilizes the algorithm’s behavior in data-scarce regimes. Finally, we remark that Assumption 4.7 is violated by these two instances; however, R-CPD-UCB performs well (and so is Monitored UCB, which relies on a similar hypothesis). This phenomenon was already observed in [8], and shows how Assumption 4.7 is, in practice, is not very limiting.

C.3 Sensibility to

In this section, we study the sensibility of R-CPD-UCB to different magnitudes of changes.

Setting

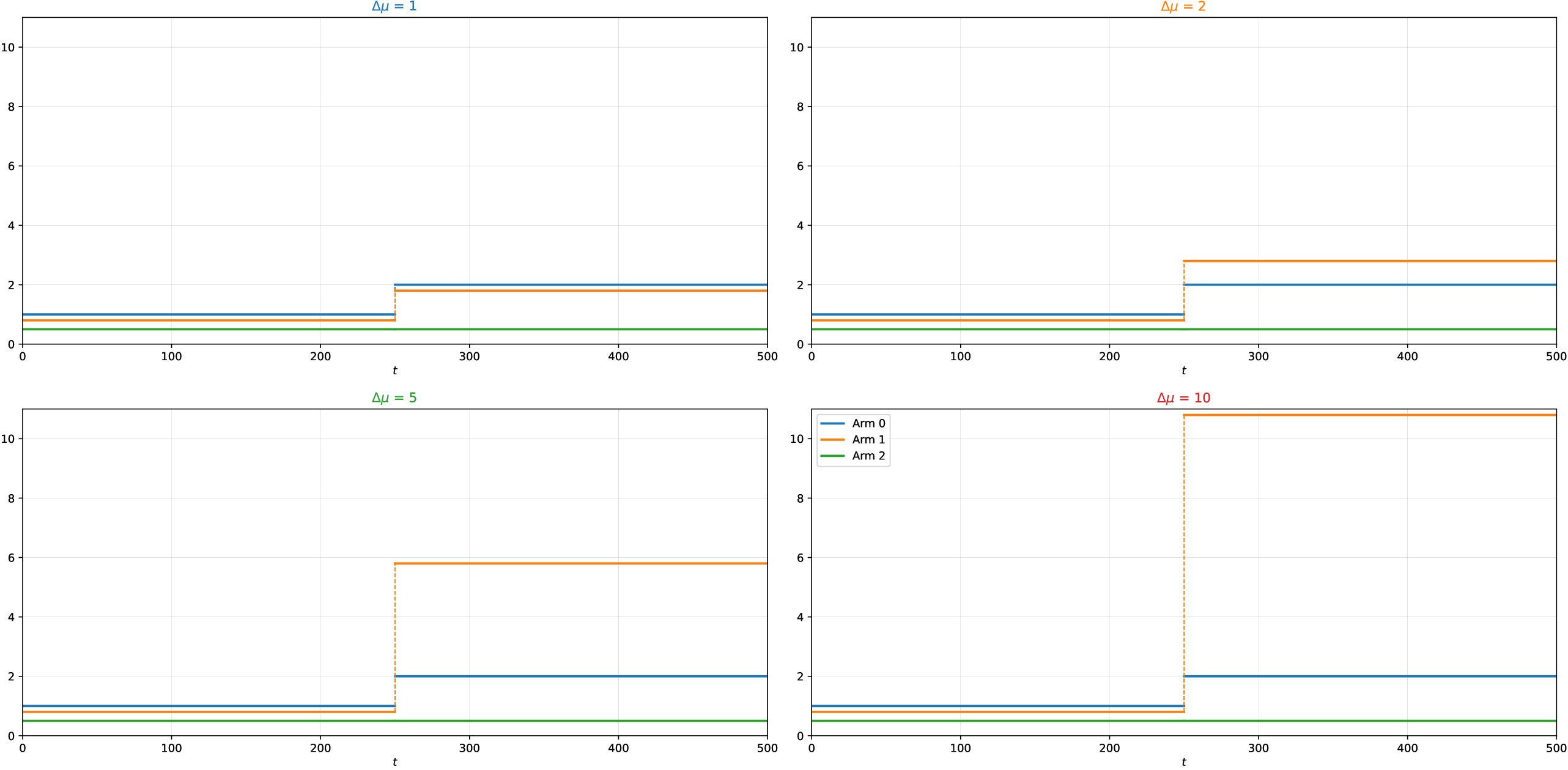

We consider four HTPS MABs with Pareto rewards (, ), , , and . The starting means are , and , and a change occurs at . We let , (thus, ) and , respectively. In the first PS MAB, the first action remains optimal from the start to the end of the trial; in the others, the second action becomes optimal after the change. In Figure 8, we report the means of every action in every epoch for the four HTPS MABs.

Results

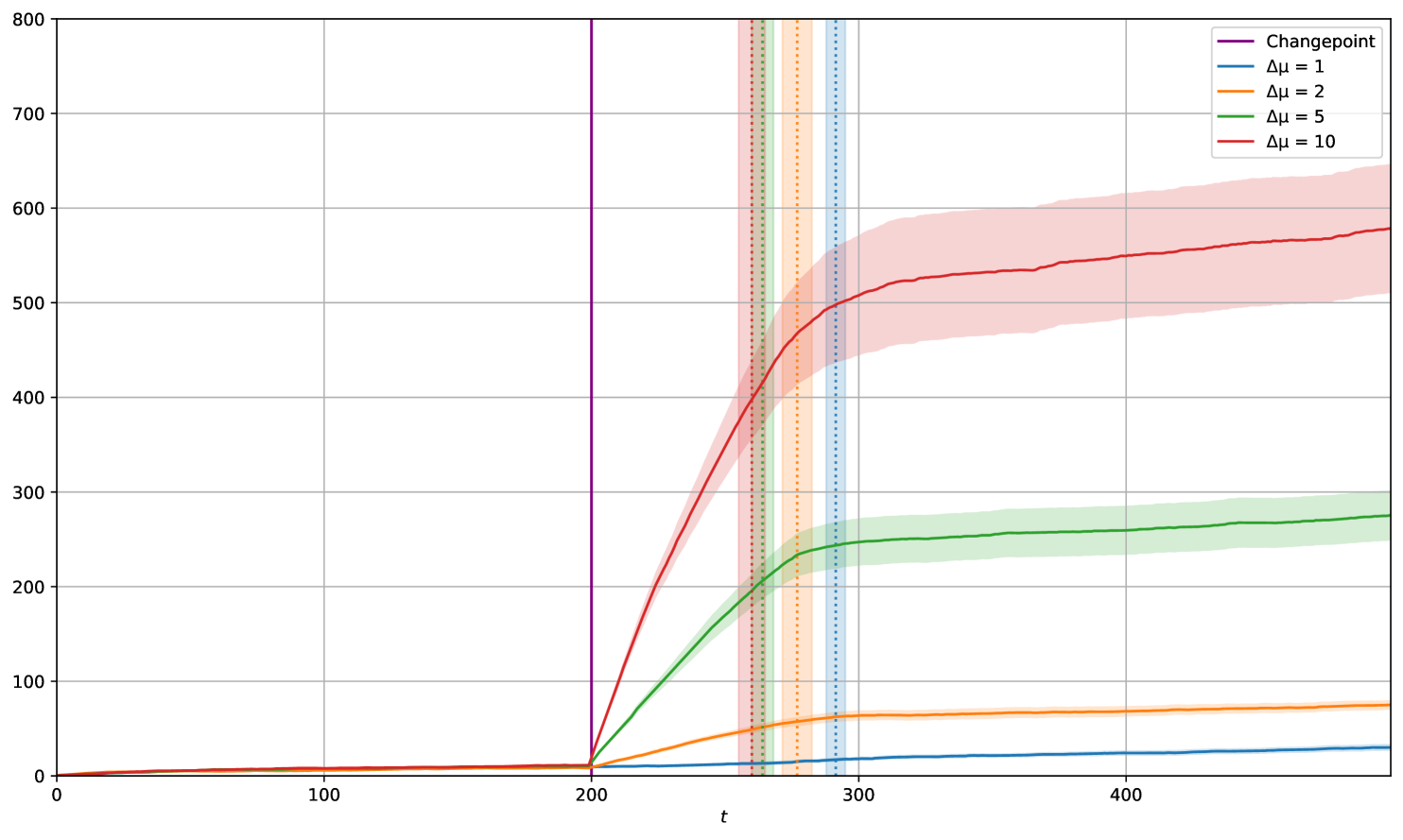

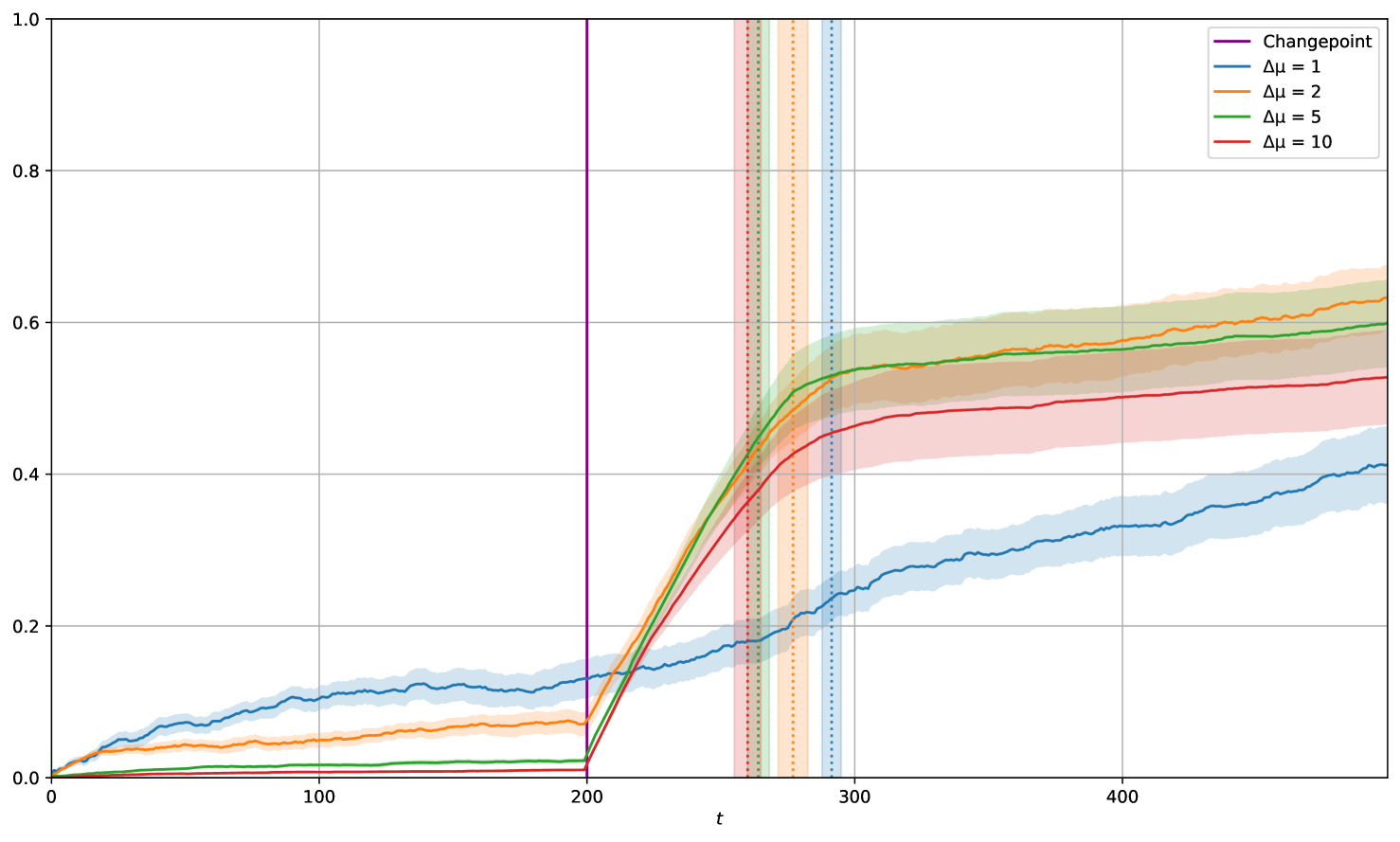

In Figure 9, we report the cumulative regrets suffered by R-CPD-UCB in the four HTPS MABs. For each instance, we performed trials and reported the average cumulative regret (on the right), together with its standard deviation. Moreover, the dashed vertical lines indicate the average detection time and their standard deviations. As the four instances differ in terms of magnitude (e.g., in the first instance, the maximum mean is , and in the fourth is ), we also reported the rescaled cumulative regrets (on the left). R-CPD-UCB can detect the change with a reasonable delay, and all cumulative regrets show sublinear growth. As grows, the cumulative regret is larger, but the detection delay decreases. Intuitively, a larger change yields a larger regret but is also easier to detect. From the rescaled cumulative regrets, we can observe how a large w.r.t. to the mean does not deteriorate the performance of R-CPD-UCB.

C.4 Stationary Environments

In this section, we study the empirical behavior of R-CPD-UCB in stationary HT MABs.

Setting

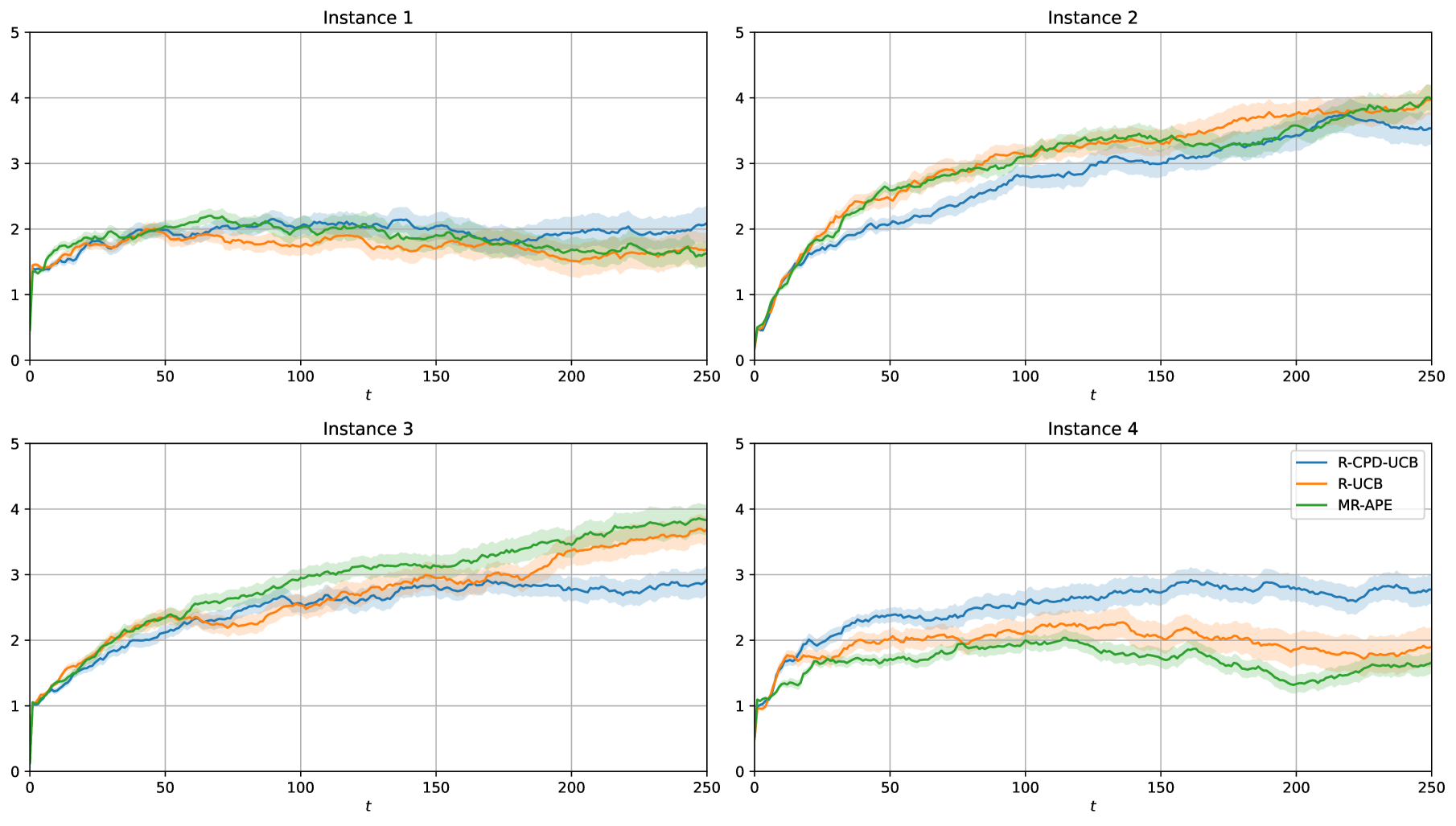

We consider four HT MABs with Pareto rewards (, ), , , and . We compare R-CPD-UCB with two gold standards from the literature: Robust UCB [7] and MR-APE [19].

| Instance | |||

| Instance | |||

| Instance | |||

| Instance |

Results

We remark that, in a stationary environment, the behavior of R-CPD-UCB diverges from the one of Robust UCB in only two cases: (i) when there is a false detection (happens with probability smaller than ) and (ii) R-CPD-UCB performs a forced exploration (once every rounds). In both cases, the contribution to the regret is small compared to the dominant term, adding a constant factor at most. In Figure 10, we report the cumulative regrets suffered by the algorithms in the four HT MABs. For each instance, we performed trials and reported the average cumulative regret, together with its standard deviation. R-CPD-UCB raises only one false alarm in one trial of the fourth instance, and the average cumulative regret is thus slightly larger than the one Robust UCB, which is suited for the stationary setting. R-CPD-UCB suffers cumulative regrets comparable to the ones of algorithms suited for the stationary case. All cumulative regrets show sublinear growth.

Appendix D Computational Complexity of Robust-CPD-UCB

In this section, we characterize the computational complexity of R-CPD-UCB and provide a simple modification to the algorithm that allows for quicker computation while keeping similar theoretical guarantees. For the sake of traceability, we assume that all means belong to the set . We start by upper bounding the computational complexity of R-CPD-UCB.

Proposition D.1.

Let . Let be the machine tolerance. Then, R-CPD-UCB takes at most steps with probability at least .

Proof.

Using the bisection method with a tolerance of , and searching in the interval , we can solve the two root-finding problems implied by Equation (5) in at most . Note that, by Theorem 3.2 from [6], the solution lies in the search interval with probability at least . Then, we observe that R-CPD-UCB, at each round , for every action , runs a step of the Catoni-FCS-detector which computes CS of lengths . Computing a CS of length requires to compute CIs, which requires steps at most for each of them. Note that a solution always exists as the number of samples is always greater than when the CPD routine is executed. The result follows by upper bounding . ∎

Proposition D.1 states that the computational complexity of R-CPD-UCB is polynomial in .