Multi-horizon optimization for domestic renewable energy system design under uncertainty

Abstract

In this paper we address the challenge of designing optimal domestic renewable energy systems under multiple sources of uncertainty appearing at different time scales. Long-term uncertainties, such as investment and maintenance costs of different technologies, are combined with short-term uncertainties, including solar radiation, electricity prices, and uncontrolled load variations. We formulate the problem as a multistage multi-horizon stochastic Mixed Integer Linear Programming (MILP) model, minimizing the total cost of a domestic building complex’s energy system. The model integrates long-term investment decisions, such as the capacity of photovoltaic panels and battery energy storage systems, with short-term operational decisions, including energy dispatch, grid exchanges, and load supply. To ensure robust operation under extreme scenarios, first- and second-order stochastic dominance risk-averse measures are considered preserving the time consistency of the solution. Given the computational complexity of solving the stochastic MILP for large instances, a rolling horizon-based matheuristic algorithm is developed. Additionally, various lower-bound strategies are explored, including wait-and-see schemes, expected value approximations, multistage grouping and clustering schemes. Extensive computational experiments validate the effectiveness of the proposed methods on a case study based on a building complex in South Germany, tackling models with over 20 million constraints, 5 million binary variables, and 6 million continuous variables.

keywords:

domestic renewable energy system; multi-horizon stochastic optimization; stochastic dominance; bounds.1 Introduction

Addressing climate change necessitates a coordinated effort to reduce global CO2 emissions, which are predominantly driven by the energy sector. According to the International Energy Agency (see Birol [2022]), the energy industry accounts for approximately 73% of global greenhouse gas emissions, making it the largest contributor to climate change. Within this sector, electricity and heat production alone account for roughly 40% of emissions, totaling 14.7 gigatonnes of CO2 in 2022 (see International Gas Union and Snam [2024]). This underscores the urgent need for changes in energy production and consumption practices.

In this context, domestic Renewable Energy Systems (RESs) emerge as a key solution for accelerating the transition to sustainable energy. These systems enable households to generate and use renewable energy, primarily solar, to meet their energy needs, thereby reducing the environmental footprint of energy production. A typical domestic RES consists of Photovoltaic (PV) panels, Battery Energy Storage Systems (BESS), and digital devices capable of implementing demand response programs by directly controlling household appliances. Beyond reducing CO2 emissions, domestic RES design contributes to preserving natural resources and ecosystems. Unlike coal or nuclear power plants, PV panels operate without water, making them particularly advantageous in regions facing water scarcity. Moreover, rooftop solar installations minimize land use and habitat disruption, providing an environmentally friendly alternative to large-scale energy projects.

However, the deployment of domestic RES faces several challenges. Sufficient roof space with optimal orientation is essential for effective solar energy capture, which may limit their feasibility for some buildings. Additionally, the high upfront costs of PV panels and BESS, even when partially mitigated by government incentives, remain a significant barrier for many households. The intermittent and stochastic nature of solar radiation further complicates the integration of RES into energy systems. These challenges highlight the need for advanced optimization models to design efficient and cost-effective domestic RES for residential complexes.

There is a broad literature on RES. We refer the readers to Rahani-Andelibi [2017], Zakaria al. [2020], Al-Shahri et al. [2021], Jasinski et al. [2023], Ukoba et al. [2024] for comprehensive reviews on the topic. Specifically, most of the works presented in the literature are focused on the very short-term, addressing the operations management of a domestic RES that has been already installed; see, for instance, AlSkaif et al. [2017], Rahani-Andelibi [2017], Luo et al. [2020], Olivieri and McConky [2020], Taghikhani and Zangeneh [2022]. Much fewer works are devoted to the RES design problem. For example, Milan et al. [2012] present a Linear Programming (LP) model for the design of a RES composed of PV panels, a solar thermal collector, and a heat pump over a yearly time horizon. In the work, no uncertainty is considered. Kucuksari et al. [2014] formulate a deterministic multistage Mixed Integer Linear Programming (MILP) model to optimally locate PV panels and design and maintain BESS, and handle the operational uncertainties in the system via a simulation phase that provides updates to the optimization model. Mohammadi et al. [2018] introduce an approach to designing a RES consisting of PV panels, wind turbines, and BESS for a single household over a yearly time horizon, where the uncertainty affecting the problem is considered in a post-optimality analysis to validate the solution.

Most studies on RES design adopt deterministic approaches; only a few papers in the literature incorporate uncertainty into the modeling framework. For example, an LP approach is presented in Zhu al. [2021], where the realizations of the wind and solar power output are considered as interval ranges, rather than single numbers, in a fuzzy optimization approach. Hemmati and Saboori [2017] propose a stochastic mixed integer non-linear programming model to integrate a BESS into an already installed PV system, while Lauinger et al. [2016] present a two-stage stochastic LP model to design a RES consisting of PV, fuel cell, heat pump, boiler, solar thermal generators, and BESS. Both works optimize jointly investment decisions on the RES infrastructure and operational decisions on RES components to satisfy an aggregated load under the uncertainty of renewable generation. The uncertainty of the load is considered in Aghamohamadi et al. [2019], where a robust optimization model is proposed to determine the optimal capacity of a residential PV-battery system while minimizing its operation costs.

The literature on RES also includes some examples of two-stage stochastic MILP models (see Schwarz et al. [2018], Cervantes et al. [2018], Keyvandarian and Saif [2024]). Specifically, Schwarz et al. [2018] develop a two-stage stochastic MILP model to decide, in the first stage, the design of a RES consisting of PV, air-water heat pump, hot water and BESS, and, in the second stage, the system operations in a yearly time horizon with 5 minutes resolution. Another two-stage stochastic multiperiod MILP model is presented in Cervantes et al. [2018] for PV and BESS design. In this paper, an aggregate electricity load is considered and the uncertainty of load, electricity import costs and solar radiation is modeled by means of independent scenarios. Another example of two-stage stochastic multiperiod MILP model can be found in Keyvandarian and Saif [2024], with application to a RES consisting of PV, wind turbines, BESS, and diesel generators.

As further discussed in Khezri et al. [2023] and from the literature review on RES models, we can identify some open challenges that need to be addressed:

-

1.

Combine different time scales in the problem: a medium-to-long-term time horizon to plan the installation of the RES infrastructure and a short-term horizon to evaluate how the system operates to supply the load.

-

2.

Provide a better representation of the load, which needs to be disaggregated at the household level, distinguishing also between controllable (e.g., air conditioning) and non-controllable loads (e.g., kitchen electricity needs).

-

3.

Consider accurately both the long-term uncertainty affecting the costs of the RES infrastructure and the short-term uncertainty on weather-based solar radiation and electricity loads.

-

4.

Consider the customer discomfort that may be caused by undelivered load in the short-term.

-

5.

Develop solution methods to provide RES configurations whose quality can be guaranteed with affordable effort.

To address these open challenges, in this paper we formulate the problem of designing a domestic RES under uncertainty as a multi-horizon stochastic optimization model. This class of problems has been introduced in Hellemo et al. [2012] and Kaut et al. [2014] to describe situations that include both long-term and short-term uncertainty. The multi-horizon approach has been widely utilized in the literature to address real-life problems involving strategic and operational decisions. To mention just a few: Skar et al. [2016] develop a multi-horizon model to plan long-term investments in the European power system considering the uncertainty of the intermittent energy production and the energy demand; Su et al. [2015] introduce a multistage multi-horizon stochastic equilibrium model to analyze multi-fuel energy markets, focusing on infrastructure development and renewable energy policies in both perfect and imperfect market structures; Werner et al. [2013] investigate the time consistency property in multi-horizon scenario trees; Seljom and Tomasgard [2015] incorporate short-term uncertainty into long-term energy system models, focusing on power systems with large shares of wind generation; Abgottspon and Andersson [2016] utilize the multi-horizon approach to support scheduling decisions for a pumped storage hydro power plant in a liberalized market environment; Seljom and Tomasgard [2017] investigate through a multi-horizon model the influence of policy actions and future energy prices on the cost-optimal development of energy systems in Norway and Sweden; Escudero and Monge [2018] present a MILP model for a multi-horizon capacity expansion planning, where a stochastic dominance risk averse functional is considered; Maggioni et al. [2020] extend the definition of the traditional Expected Value problem and Wait-and-See problem from stochastic programming in a multi-horizon framework, introducing new measures to quantify the importance of the uncertainty at both strategic and operational levels. Addressing problems with two time scales is computationally challenging, leading to recent research into efficient solution methods. Vojvodic et al. [2023] propose a multi-horizon model for generation capacity planning under electricity and natural gas demand uncertainty, leveraging a Benders-type algorithm to achieve near-optimal solutions. Zhang et al. [2024a] exploit the block-separable structure of multi-horizon stochastic LP models with Benders and Lagrangean decomposition methods. Similarly, Jacobson et al. [2023] tackle macro-energy systems planning by applying a Benders approach that separates investments from operations and decouples operational time steps via budgeting variables in the master problem. To address oscillations in Benders schemes, Zhang et al. [2024b] introduce a stabilized adaptive method, while Rigaut et al. [2024] propose a time-block decomposition scheme using recursive Bellman-like equations, demonstrating its effectiveness in a battery management problem.

In this paper, we propose a multi-horizon model to co-optimize long-term decisions on the installed capacity of PV panels and BESS and short-term decisions on the electricity generation from PV panels, the charge, discharge and energy level of BESS, the electricity exchanges with the power grid, and the supply of different types of load. Several sources of uncertainty affecting the problem at different time scales are considered: long-term uncertainty comprises the investment and maintenance costs of the different technologies, while short-term uncertainty includes solar radiation, import prices from the public power grid and non-controlled load. To prevent black swan operational scenarios with high discomfort for the users by undelivered load in the short-term, first- and second-order stochastic dominance risk-averse measures are considered at the operational level, preserving the time consistency of the solution (see Dentcheva and Ruszczyński [2003], Dentcheva and Ruszczyński [2024]). Given the computational burden of multistage multi-horizon stochastic models with risk measures, in this work, we also develop a heuristic method to compute feasible solutions and test the effectiveness of the proposed approach by implementing a variety of strategies for obtaining lower bounds.

To sum up, the contributions of our paper can be summarized as follows:

-

1.

We propose a novel multi-horizon optimization model for RES design under different sources of uncertainty. Our model includes both investment and expansion decisions on the RES infrastructure at the strategic level and considers in detail different types of loads at the operational level. Specifically, to the best of our knowledge, the formulation of the RES design problem as a multi-horizon optimization model has not been proposed before and represents a key contribution of this work.

-

2.

To control the discomfort that may be caused to the users by undelivered load in the short-term, we consider a coherent and time-consistent risk-averse measure by integrating in the model the first- and second-order stochastic dominance functional.

-

3.

We devise a rolling-horizon algorithm to provide high-quality feasible solutions to the problem, and we test a set of approaches for obtaining strong lower bounds to assess the quality of the solution method.

-

4.

To validate the proposed approaches, we provide extensive computational experiments based on a real building complex in South Germany, tackling models with over 20 million constraints, 5 million binary variables, and 6 million continuous variables.

The rest of the paper is organized as follows. Section 2 describes the RES design planning problem and provides its formulation as a multi-horizon MILP model. Section 3 describes the algorithm for providing feasible solutions to the RES design problem. Section 4 presents a variety of strategies for obtaining lower bounds. Section 5 reports the main results of the computational experiments for validating the proposed approach. Finally, Section 6 concludes the paper.

2 Optimal design of a domestic renewable energy system

We begin with a general description of the domestic RES design problem and leave relevant notation to the next subsection, followed by problem formulation.

2.1 Problem description

The problem consists in designing a domestic RES by planning investments in PV panels and BESS technologies to satisfy the electricity load of a building complex under several sources of uncertainty. Two types of decisions must be considered: strategic decisions for long-term planning and operational decisions for short-term planning. Strategic decisions are made at stages to plan the installation of new capacity for PV and BESS technologies, being seasons or years. Each stage is composed of a number of days that can differ from one stage to another. Each day is divided into daily periods, represented as blocks of consecutive hours, where the number of hours in each block can vary within the same day. Hours in the same daily periods are assumed to have the same electricity generation and load. To manage the operation of the designed RES, operational decisions are made at daily periods. In such a multi-horizon setting, the two planning horizons are affected by several sources of uncertainty: the strategic uncertainty (in the long-term) includes the investment and maintenance costs of the different PV and BESS technologies and their residual values, while the short-term uncertainty comprises solar radiation, electricity prices to sell and import from the power grid, load, and operating costs.

In a multi-horizon approach to modeling uncertainties, the realization of strategic and operational uncertain parameters is represented by discrete values in scenario trees across different time scales. Specifically, long-term uncertainty is captured through a set of strategic nodes organized in a multistage scenario tree (e.g., red circle nodes in Fig. 1), while operational uncertainty is modeled within operational sub-trees branching from each strategic node (e.g., sub-trees with blue diamond nodes in Fig. 1). Typically, operational sub-trees are designed as two-stage multi-period trees (see, e.g., Kaut et al. [2014], Escudero and Monge [2018], Kaut [2024], Rigaut et al. [2024], Zhang et al. [2024a]); however, they can also be represented as multistage trees, as demonstrated in Maggioni et al. [2020].

Figure 1(a) illustrates an example of a multi-horizon scenario tree with three stages and seven strategic nodes, represented by red circles. Each stage corresponds to a time interval within the long-term horizon where new information becomes available and decisions are made. Within each stage, there is a finite number of strategic nodes, each representing a specific decision or event. The strategic node at the first stage is known as the root, while those at the final stage are called leaves. Every strategic node, except the root, is linked to a unique node in the preceding stage, referred to as its ancestor. A strategic scenario is defined as a path through the sequence of strategic nodes from the root to a leaf, representing the realization of strategic uncertain parameters across the long-term horizon.

At the operational level, short-term uncertainty is modeled independently of strategic uncertainty. In the multi-horizon scenario tree shown in Fig. 1(a), short-term uncertainty is represented by two-stage multi-period scenario sub-trees branching from each strategic node. Each operational sub-tree contains six operational nodes, corresponding to three operational scenarios and two operational periods. It is important to note that the terminal leaves of these operational sub-trees are not connected to subsequent strategic or operational nodes. This representation of uncertainty is referred to as the traditional multi-horizon scenario tree, as it was introduced in the seminal works of Hellemo et al. [2012] and Kaut et al. [2014]. On the other hand, in this paper we consider the tactical representation introduced in Alonso-Ayuso et al. [2020], where terminal leaves of each operational sub-tree are connected to the immediate successor investment node, as shown in Fig. 1(b). Such a representation allows the transfer of aggregated information on short-term operations to the successor investment and operational nodes, thus providing a better representation of long-term dynamics of BESS.

In line with Milan et al. [2012], Haq et al. [2019], the modeling of PV technology assumes that each type consists of identical panels with a specified nominal capacity, representing the maximum hourly electricity output achievable by a single PV panel. At the strategic level, different PV panel types are associated with distinct costs, including fixed preparation costs, installation costs, and maintenance costs, all of which are treated as strategic stochastic parameters. Additionally, at the end of the long-term planning horizon, each PV panel is assumed to have an unit residual value, which is also uncertain.

In terms of short-term operations, during the day-time, the electricity load of the domestic building complex can be supplied by the electricity generated from PV panels, which depends on the installed capacity of PV panels and the stochastic availability of solar radiation. Furthermore, electricity generation from PV panels involves stochastic operating costs.

To manage the variability of the solar power production, at each stage, investments in PV panels can be coupled with investments in different BESS technologies. Similarly to PV modeling, we consider BESS as composed of a number of identical battery units for each technology with a given nominal capacity, loss factor, and discharge/charge depths fractions. Loss factors tend to increase along the multistage time horizon. At the strategic level, different types of batteries are characterized by distinct fixed preparation costs, installation costs, maintenance costs, and residual values at the end of the planning horizon. At the operational level, they incur different operating costs.

If the RES production and storage is insufficient to meet the electricity demand, energy can be imported from the public power grid, incurring electricity purchase costs that are typically much higher than the costs of RES production. On the other hand, excess in the RES energy generation can be exported to the power grid.

The building complex consists of households and commercial offices, with different consumption profiles. Loads of the domestic building can be classified into two categories: non-controlled loads and controlled ones. The first group includes all types of consumption that cannot be controlled by the RES central operator and must be necessarily met. They include, for example, lighting, fridge, kitchen electricity loads, online computing, and communication. On the other hand, controlled loads are characterized by mechanisms that let the user to modulate its operation in terms of intensity and time scheduling. There are two types of controlled loads, namely, elastic and deferrable: while the set of elastic loads includes loads that can be partially curtailed, deferrable loads must be consumed inevitably, which however can be shifted from load peak hours to off-peak hours. More precisely, elastic loads have a reference level (a setpoint), as a target for each daily period in each household. They include, as an example, electricity load in function of the thermal one as HVAC—Heating, Ventilation and Air-Conditioning—system as well as the load from microwave, TV, and refrigerator. Negative deviations from the setpoints are allowed up to a maximum curtailment value, causing however a discomfort to the final user. On the other hand, deferrable loads have a reference period in the day as a target for the supply. The RES central operator, however, can decide to anticipate or delay the consumption, inducing a discomfort to the final user. Deferrable loads include, for example, electricity load for using the washing machine, dryer, dishwasher, oven, iron, battery of electricity vehicles, and vacuum cleaner. Some of the controlled load types may be incompatible at the same operational period, while others may have latency-based precedence relationships along the daily periods.

In such a framework, the decision maker wants to design domestic RES infrastructures able to meet the electricity loads of the domestic building complex at minimum total cost (i.e., investment and operational). Specifically, at the strategic level, the decisions to be taken concern the investments in PV and BESS technologies over the long-term planning horizon, subject to technical and budgeting constraints. On the other hand, at the operational level, the problem is to optimize in the short-term the production from the domestic RES, the load supply, and the power exchange with the grid.

2.2 Notation

Tables LABEL:tab:tree_stratLABEL:tab:risk_par provide the full notation of the multi-horizon model: Tables LABEL:tab:tree_strat and LABEL:tab:tree_oper show the sets and parameters of the multi-horizon scenario tree representation for the strategic and the operational uncertainty, respectively; Table LABEL:tab:sets provides the sets of the RES problem; in Table LABEL:tab:det_par the deterministic model parameters are listed; the uncertain strategic and operational model parameters are reported in Tables LABEL:tab:stra_par and LABEL:tab:oper_par, respectively; in Table LABEL:tab:stra_var the strategic decision variables defined for each strategic node of the scenario tree are reported; Table LABEL:tab:oper_var shows the operational decision variables defined for strategic node at stage (being the set of stages), and operational node ; finally Table LABEL:tab:risk_par provides sets, parameters and decision variables for discomfort modeling.

| Symbol | Description |

| set of strategic stages. | |

| set of strategic nodes of the scenario tree. | |

| set of strategic nodes of the scenario tree at strategic stage . | |

| set of strategic scenarios. | |

| set of strategic scenarios passing through strategic node . | |

| ancestor node of strategic node . | |

| stage to which strategic node belongs (i.e., ). | |

| probability of strategic scenario . | |

| probability of strategic node . Note that . | |

| number of days in stage . |

| Symbol | Description |

| set of operational nodes of stage . | |

| set of operational scenarios in stage . | |

| set of consecutive operational daily periods. | |

| set of operational daily periods at stage . | |

| first/last operational period of stage . | |

| probability of operational scenario . | |

| probability of operational node . | |

| daily period of operational node , with . | |

| operational scenario to which operational node belongs. | |

| operational ancestor node of operational node . For operational nodes belonging to the first daily period of stage (i.e., ) we set . | |

| number of hours in daily period . |

| Symbol | Description |

| set of PV technologies. | |

| set of battery technologies. | |

| set of controlled load types. | |

| subset of elastic load types. | |

| subset of deferrable load types. | |

| pairs of deferrable load types with incompatible satisfaction in the same operational period. | |

| pairs of deferrable load types with a time precedence relationship, where is the precedent one. | |

| set of daily periods at stage where electricity can be generated from the PV panels. | |

| set of daily periods in stage where the electricity consumption is allowed for elastic load type . | |

| set of daily periods in stage where the electricity consumption is allowed for deferrable load type . | |

| auxiliary set introduced to model the supply of deferrable load . For any stage and operational node , it gives the set of operational nodes such that starting the supply of load in would necessitate supplying the load in node as well. | |

| auxiliary set introduced to model the minimum latency constraint between the precedent load and the deferred load . For any operational node that is a candidate for starting the supply of load , it gives the set of operational nodes compatible with the start of the supply of load . |

| Symbol | Description |

| maximum number of PV panels of technology that can be installed in the building complex. | |

| maximum number of PV panels of all technologies that can be installed in the building complex. | |

| lower bound to the number of PV panels of any technology installed at each stage. | |

| capacity of a PV panel of technology . | |

| maximum number of battery units of technology that can be installed in the building complex. | |

| maximum number of battery units of all technologies that can be installed in the building complex. | |

| lower bound to the number of battery units of any technology installed at each stage. | |

| fraction of loss energy in a battery of type in daily periods of stage . | |

| capacity of a battery of type . | |

| discharge/charge depth fractions of capacity in a battery of type in daily periods of stage . | |

| unit operational cost of battery of type . | |

| upper bound on the decrease deviation from reference level of elastic load at operational period . | |

| upper bound on the difference of the reference levels of elastic load type between the operational daily periods and , . | |

| average hourly electricity requirement of deferrable load in stage . | |

| number of consecutive hours needed to satisfy the requirement of deferrable load at stage . | |

| number of consecutive daily periods that are required to satisfy the requirement of deferrable load by starting the supply at daily period . For any load and any period , parameter is computed by considering and . Notice that it could happen that the number of hours to assign to the last daily period is smaller than . In this case, by convention, it is assumed that all hours in period must satisfy the load. | |

| reference operational period for supplying deferrable load type in stage . | |

| minimum number of precedence periods for load type over type . |

| Symbol | Description |

| fixed (i.e., preparation) cost for the installation of PV technology of type in strategic node . | |

| unit installation cost of a PV panel of technology . | |

| unit maintenance cost of a PV panel of technology in strategic node . | |

| fixed (i.e., preparation) cost for battery technology in strategic node . | |

| unit installation cost for battery technology in strategic node . | |

| unit maintenance cost for battery technology in strategic node . | |

| residual value of a PV panel unit of technology at strategic node . | |

| residual value of a battery unit of technology at strategic node . | |

| budget for investment in RES components at strategic node . |

| Symbol | Description |

| hourly non-controlled electricity load (say kitchen, lighting, tv, fridge, refrigerator, circulation pump, electric vehicles) in the households at operational node | |

| hourly reference level for elastic load type at operational node . | |

| hourly fraction of the installed capacity of PV panel of technology converted into electricity at operational node . | |

| hourly unit revenue of the electricity sold to the public power grid at operational node . | |

| hourly unit cost of the electricity imported from the grid at operational node . | |

| hourly unit cost of the electricity generated by PV technology of type at operational node . |

| Symbol | Description |

| binary variable. if PV technology has been installed by strategic node , and otherwise. | |

| total number of PV panels of type installed by strategic node . | |

| binary variable. if new PV panels of technology are installed at strategic node , and otherwise. | |

| binary variable. if battery technology has been installed by strategic node , and otherwise. | |

| total number of battery units of type installed by strategic node . | |

| binary variable. if new battery units of technology are installed at strategic node , and otherwise. |

| Symbol | Description |

| hourly electricity generated from PV panels of type used to meet the load requirements of the households in strategic node in operational node . | |

| hourly amount of electricity purchased from the power grid in strategic node in operational node . | |

| total electricity accumulated in battery type at the end of daily period of operational node . | |

| hourly charge of the battery type in operational node . | |

| hourly discharge of the battery type in operational node . | |

| hourly decrease deviation from the reference level of elastic load in operational node . | |

| binary variable. if deferrable load is supplied starting from daily period of operational node , and otherwise. | |

| hourly amount of electricity purchased from the power grid in strategic node in operational node . |

| Symbol | Description |

| set of profiles for the total discomfort in operational scenarios . | |

| users discomfort for each unit curtailment of elastic load at period . | |

| users discomfort caused by the shift of the starting period of deferrable load from the reference period to the period . Note that means that daily period is a zero-discomfort penalized alternative to period . | |

| upper bound on the expected discomfort in stage . | |

| threshold for the total daily discomfort in profile . | |

| upper bound on the excess fraction of discomfort over the threshold that can be accepted in any operational scenario for profile . | |

| upper bound on the probability of violation of the threshold for profile . | |

| upper bound on the expected excess fraction of discomfort that can be accepted in any stage for profile . | |

| excess of discomfort for profile in operational scenario . | |

| binary variable. if the discomfort in operational scenario exceeds the threshold for profile , and otherwise. |

2.3 Problem formulation

Optimal decisions about the domestic RES design and its short-term management are determined by minimizing the objective function (1) given by the sum of the expected strategic and operational costs of the RES design, while respecting several types of constraints:

-

1.

Strategic constraints (2) related to the RES design and its budget.

-

2.

Operational constraints (3) modeling the short-term operations of PV and BESS technologies.

-

3.

Operational constraints (4) related to the supply of the loads.

-

4.

Tactical constraints (5) modeling the BESS flow balance between consecutive stages.

-

5.

Maximum expected discomfort constraint (6) to limit the expected discomfort caused to the users by reductions or shifts of the loads with respect to reference values.

-

6.

Risk-averse discomfort constraints (7) to protect the solution from the discomfort of black swan operational scenarios.

We now formulate the objective function and different types of constraints.

| Objective function (1) | ||||

| (1a) | ||||

| (1b) | ||||

| (1c) | ||||

| (1d) | ||||

In the objective function (1), the expression (1a) gives the strategic costs associated with PV technology, which are computed as the sum of fixed preparation costs (incurred only at the first installation of a PV technology), plus variable installation costs of PV panels, plus maintenance costs. Similarly, the term (1b) computes the strategic costs related to BESS by considering preparation, installation and maintenance costs. The expression (1c) computes the expected operational costs of the domestic RES as the import costs from the public power grid, plus the operating costs of BESS, plus PV electricity generation costs, minus revenues of exporting electricity to the public grid. Note that, in order to compute the total operational costs, the hourly cost of each operational node is multiplied by the number of hours in the corresponding daily period and the number of days in the corresponding stage . Finally, expression (1d) gives the expected residual value of the RES investments.

| Strategic constraints (2), | |||

| (2a) | |||

| (2b) | |||

| (2c) | |||

| (2d) | |||

| (2e) | |||

| (2f) | |||

| (2g) | |||

| (2h) | |||

| (2i) | |||

| (2j) | |||

| (2k) | |||

| (2l) | |||

| (2m) | |||

| (2n) | |||

| (2o) | |||

| Constraint (2a) defines as binary variables the step variable representing the installation of technology by strategic node (i.e., if technology is in use in node ) and the impulse variable representing the installation of new panels of technology in node . Constraint (2b) enforces the coherence between binary variables associated with PV technology stating that new PV panels of technology can be installed in the RES (i.e., ) only if technology is in use in node (i.e., ). Constraint (2c) imposes that, once installed in a given strategic node, a PV technology is in use in the successor nodes. Constraint (2d) states that the non-negative variable representing the number of PV panels of technology installed by strategic node is bounded from below by the number of PV panels installed by the ancestor node and from above by the maximum number of PV panels of type that can be installed. If PV technology is not in use in strategic node (i.e., ), constraint (2d) sets to zero the variable . Constraint (2e) prevents the installation of more than one PV technology at any strategic node. Constraint (2f) upper bounds the total number of PV panels in use at any strategic node. Constraint (2g) lower and upper bounds the number of PV panels of any technology to be installed at any strategic node. Constraints (2h)(2n) work similarly to equations (2a)(2g), but for the BESS case. Constraint (2o) forces the budget restrictions on the RES investments. | |||

| PV and BESS operational constraints (3), | |||

| (3a) | |||

| (3b) | |||

| (3c) | |||

| (3d) | |||

| (3e) | |||

| (3f) | |||

Equation (3a) states that the share of electricity generated from PV panels to supply the RES load is non-negative and it is bounded from above by the total electricity generated from PV panels. Constraint (3b) is the electricity balance equation for operational node , enforcing the equality between electricity sources and uses. Specifically, the left-hand-side of (3b) computes the total electricity available in operational node as the sum of the electricity generated from the PV panels, plus the import from public power grid, plus the electricity discharged from BESS, minus the electricity charged in BESS. The right-hand-side of (3b) gives the total electricity consumption in operational node , which is the sum of the non-controlled electricity load , plus the consumption of elastic loads , plus the electricity requirements of deferrable loads supplied in operational node . Specifically, in stage , each deferrable load , once started, needs to be supplied for the consecutive hours in order to fully satisfy the load. Knowing the number of hours of each daily period , we can construct parameters representing the number of consecutive daily periods that are required to fully meet the electricity requirement of load by starting to supply the load at daily period . So, the deferrable load must be supplied at the operational node if and only if the start time for satisfying the load falls within the interval . In constraint (3b) this is expressed by constructing for operational node and deferrable load the set of operational nodes that belong to the same operational scenario of node (i.e., ), are associated with daily periods that may be potential starting periods for load (i.e., ), and with associated daily periods falling in the interval . Constraint (3c) gives the net bounds of the electricity discharge of the BESS taking into account the loss and the discharge depth of the battery. Constraint (3d) bounds the electricity charge in the BESS to the product between the charge depth and the battery’s capacity. Constraint (3e) gives the flow balance in the BESS for any operational node whose operational period is not the first daily period. Constraint (3f) bounds the electricity storage in the BESS to the installed capacity.

| Load operational constraints (4), | |||

| (4a) | |||

| (4b) | |||

| (4c) | |||

| (4d) | |||

| (4e) | |||

| (4f) | |||

Constraint (4a) is a load ramp constraint, forcing an upper bound on the absolute difference in the net reference level to be satisfied for any elastic load between two consecutive operational nodes. Constraint (4b) bounds the decrease deviation from the reference level for each elastic load in the operational nodes. Constraint (4c) defines the domain of variables . Constraint (4d) enforces that in each operational scenario of the two-stage tree headed by strategic node exactly one operational period must be the starting period for satisfying the electricity requirement of deferrable load . Constraint (4e) imposes the incompatibility of the hourly electricity consumption between any of the daily periods with starting period , and any of the daily periods with starting one , . Constraint (4f) ensures that the minimum latency in the time precedence relationship is maintained between the preceding load and the deferred load , where . Specifically, this constraint states that if load is supplied starting at daily period , then load must be satisfied at any daily period no earlier than .

Tactical constraints modeling inter-stages BESS electricity flows (5)

| (5a) | ||||

| (5b) | ||||

Equation (5a) states that at the beginning of the planning period each battery is empty, by computing the storage level in battery in any operational node associated with the first operational period as the total electricity charged in operational node . Equation (5b) enforces the storage electricity balance for the first operational period of any subsequent stage . In order to represent the operation of long-term storage, the constraint allows for the electricity transfer between stages, by computing the storage level in the first operational period as the sum of the following terms:

-

1.

is the expected electricity level of the battery at the end of the last daily period of the previous stage , weighted by coefficient to represent the (unique) first day of stage .

-

2.

is the expected electricity level of the battery at the end of the last daily period of stage , weighted by coefficient to represent the remaining days of stage .

-

3.

is the total battery flow in operational node .

The proposed approximation of the electricity flows allows to model the dynamics of long-term storage, while keeping under control the dimensions of the multistage stochastic tree (see Fig. 1(b)).

Maximum expected discomfort constraint (6),

| (6) |

To limit the discomfort for the users arising from deviations in household electricity consumption from the elastic setpoints, as well as shifts in the supply of deferrable loads relative to the reference period, equation (6) establishes an upper bound on the expected discomfort at each strategic node. Equation (6) is referred to as a risk-neutral approach to discomfort.

While the risk-neutral approach limits the expected discomfort in each strategic node, it does not account for extreme discomfort scenarios that may arise, leaving the system unprotected from unusually high levels of discomfort. In order to protect the users from black swan operational scenarios with high deviations from the reference load, we consider the risk-averse measures named first-and second-order Stochastic Dominance (SD) (see e.g., Dentcheva and Ruszczyński [2003], Gollmer et al. [2008], Escudero et al. [2020], Dentcheva and Ruszczyński [2024] and references therein). The aim of the risk contention is to keep the discomfort within the bounds specified by the modeler, by ensuring that violations of predefined thresholds are controlled.

For each stage , let denote the set of profiles defined by the modeler for controlling the total discomfort in operational scenarios . The SD constraint system can be expressed as the following constraints system:

Risk-averse discomfort constraints (7),

| (7a) | |||

| (7b) | |||

| (7c) | |||

| (7d) | |||

| (7e) | |||

Constraint (7a) defines, for each operational scenario , the decision variable as the daily discomfort excess beyond the threshold . Constraint (7b) sets an upper bound to the discomfort excess and ensures consistency between the non-negative variable and the binary variable , which indicates whether the threshold is violated in scenario . Constraint (7c) defines the domain of the variables . Constraint (7d) bounds the probability of threshold violations, while constraint (7e) limits the expected violation of the threshold in each strategic node.

Specifically, the first-order SD constraints are given by equation (7a)–(7d), while the second-order SD measure is given by (7a)–(7b), (7e). It is worth to point that the first-order SD measure has a direct relationship with the time-honored chance-constrained approach where the probability of violating a profile threshold is upper bounded, see the seminal work of Charnes et al. [1958]. The SD measures are coherent and time consistent risk averse ones, according to the properties proposed in Artzner et al. [1999] for the former and the ones proposed in Shapiro et al. [2021] for the latter.

3 An algorithmic approach to compute feasible solutions

In real-life applications, the cardinality of the strategic and operational node sets in the RES model (1)(7) can be extremely high. As a result, solving large instances optimally using a state-of-the-art MILP solver is impractical due to the significant computational effort required. This section introduces a heuristic approach for obtaining feasible solutions to the RES problem. Specifically, the method we propose is a specialization of the constructive matheuristic algorithm SFR3, which stands for Scenario variables Fixing and Randomization of constraints / variables’ integrality Relaxation iterative Reduction. Details on its application to hub location and supply network design problems can be found in Escudero and Monge [2021, 2023].

In the SFR3 approach, the original multi-horizon model is replaced by smaller multi-horizon models, which are iteratively solved in a rolling horizon fashion. To keep the dimensions of the problems within affordable limits, each multi-horizon problem is restricted only to a subset of strategic nodes. Algorithm 1 provides a detailed description of the procedure designed to compute a feasible solution to the RES problem, with the corresponding notation reported in Table LABEL:tab:SFR3_par.

| Symbol | Description |

| number of non-relaxed stages, whose nodes are not subject to any relaxation at each iteration of the algorithm. | |

| number of relaxation stages, whose nodes can be randomly selected at each iteration of the algorithm. | |

| probability for the selection of the strategic nodes belonging to the relaxation stage . | |

| set of successor nodes of strategic node . | |

| vector of strategic decision variables defined in strategic node . | |

| vector of operational decision variables defined in operational node , for . | |

| vector of decision variables for discomfort modeling in operational scenario , for . | |

| dynamic set containing the successor nodes of strategic node belonging to a non-relaxed stage at each iteration of the algorithm. | |

| dynamic set containing strategic nodes at relaxation stage which are successors of node and are randomly selected to be included in the model at each iteration of the algorithm. | |

| dynamic set containing all successor nodes of strategic node belonging to relaxation stages that are randomly selected to be included in the model at each iteration of the algorithm. | |

| dynamic set containing all strategic nodes to be considered at a given iteration . | |

| updated probability of the selected strategic node at a given iteration . |

Specifically, at a given iteration of the algorithm, the set of stages is partitioned into the following three disjoint stage groups:

-

1.

Stages are the non-relaxed stages: all the strategic nodes belonging to these stages and the corresponding operational nodes will be considered in the model.

-

2.

Stages are the relaxation stages: only some strategic nodes randomly selected with probability and the corresponding operational nodes will be considered in the model.

-

3.

Stages are the removed stages: none of the strategic nodes belonging to these stages will be considered in the model.

Having fixed the values of decision variables up to stage , at iteration of the algorithm, the multi-horizon problem decomposes into a set of sub-problems, which can be independently solved. Denoting with any root node of a sub-tree in the stage group headed by , we refer to the correspondent sub-problem as -submodel. An -submodel is a replica of the RES problem (1)(7) restricted to a reduced set of nodes. For any node , the -submodel is obtained by constructing the following sets:

-

1.

is the set of successors of node belonging to a non-relaxed stage .

-

2.

is the set of successors of node at the relaxation stage selected to be included in the -submodel. Nodes are randomly selected with probability provided the caveat of keeping a Hamiltonian path from node to every node . For this reason, only nodes with ancestor node selected as well in the -submodel can be considered.

-

3.

is the set of the strategic nodes in all the relaxation stages to be included in the -submodel. Note that if , is the empty set.

-

4.

is the set of all strategic nodes to be considered in the -submodel.

In each -submodel, probabilities must be properly re-scaled. More precisely, node , being the root node of the -submodel, is assigned a probability . The updated probability of any selected successor node is computed by multiplying the original probability by the ratio between the updated probability of the ancestor node and the sum of the probabilities of children nodes of that are selected in the -submodel. Note that this re-scaling is necessary to guarantee that, in the reduced scenario tree associated with the -submodel, the probability of any node is the sum of the probabilities of its children nodes.

The -submodel is then solved in order to provide a value to strategic , operational and discomfort variables of the RES problem, for , and . Finally, adopting a rolling horizon approach, decision variables in node are fixed to the solution of the -submodel and a new iteration of the algorithm is performed. Note that when all the submodels have been solved and the procedure stops by fixing all decision variables associated with nodes in non-relaxed stages of the -submodels.

In the SFR3 approach, different choices for the values of parameters , and are possible. Special cases of the SFR3 approach include:

-

1.

The weak myopic strategy, with components , , . It is a one-stage rolling horizon approach, where the groups of non-relaxed stages are singleton, the groups of relaxed stages are empty and, then, any -submodel is composed of the constraints and variables only defined in node , as well as the related operational scenarios in set .

-

2.

The stronger myopic strategy, with components , , . It is a two-stage rolling horizon approach, where each -submodel includes all constraints and variables defined in node and in its children nodes , as well as the related operational scenarios in sets and .

-

3.

The even stronger myopic strategy, with components , , . It is a multi-stage rolling horizon approach, where each -submodel includes all constraints and variables defined in node and in its successors nodes up to stage , as well as the related operational scenarios.

4 Lower bounds for multi-horizon models

This section deals with methods for obtaining lower bounds for the RES model (1)(7). Specifically, we consider the following approaches:

-

1.

is the Strategic Wait-and-See approach, where the non-anticipativity constraints on the strategic decision variables are relaxed, see Subsection 4.1.

-

2.

is the Scenario Multistage Grouping approach, where the strategic scenarios are grouped in disjoint groups, with the non-anticipativity constraints that link one scenario group with any other being relaxed, see Subsection 4.2.

-

3.

is the Scenario Multistage Clustering approach, where the non-anticipativity constraints are relaxed up to a given stage, so as to obtain clusters of strategic scenarios, see Subsection 4.3.

-

4.

is the Multi Horizon Expected Value approach, where all strategic and operational uncertain parameters are replaced by their expected values, see Subsection 4.4.

-

5.

is the Multi Horizon Operational Expected Value approach, where operational uncertain parameters are replaced by their expected values, see Subsection 4.5.

For compactness purposes, let denote the strategic variables in strategic node and denote the operational variables in strategic node and operational node , where

Additionally, let the vector denote the operational scenario variables for risk averse discomfort modeling in strategic node and operational scenario :

Let and denote the vectors of the objective function coefficients for the elements of the vectors of variables and , respectively. The RES model (1)(7) can be expressed in a compact form as the following optimization model

| (8a) | |||||

| s.t. | (8b) | ||||

| (8c) | |||||

| (8d) | |||||

| (8e) | |||||

| (8f) | |||||

| (8g) | |||||

4.1 Strategic Wait-and-See (SWS) approach

In the SWS approach, the non-anticipativity constraints are relaxed exclusively for the strategic decision variables. This relaxation decomposes the original multi-horizon problem into a collection of independent subproblems. Let denote the subset of strategic nodes associated with the strategic scenario . The -submodel, derived by relaxing the non-anticipativity constraints in the RES model (1)–(7), is expressed as the following optimization problem

| s.t. | ||||

By weighting the objective function values of all -subproblems with scenarios probabilities , the resulting value, provides a lower bound for the optimal value of the RES model, as discussed in Maggioni et al. [2020].

4.2 Scenario Multistage Grouping (SMG) approach

The lower bound provided by the approach, , can be improved by grouping the strategic scenarios into disjoint groups. The grouping strategy is a widely employed technique for obtaining lower bounds in stochastic problems. For its application to multistage stochastic programs, we refer the reader to Maggioni et al. [2014], Maggioni and Pflug [2016], Maggioni et al. [2016], Maggioni and Pflug [2019]. For the multi-horizon case, we refer to the approach as the method that groups the scenarios of the original problem into independent subproblems. A smaller results in a stronger lower bound but comes at the cost of increased computational effort. Table LABEL:tab:SMG_par reports the notation needed to formulate the approach.

| Symbol | Description |

| set of groups of strategic scenarios. | |

| set of scenarios in group . | |

| set of nodes in group . | |

| weight of scenario group . | |

| weight of scenario in group , for . | |

| weight assigned to strategic node in group . | |

| replica of the vector of strategic decision variables in strategic node in scenario group , for . | |

| replica of the vector of operational decision variables in strategic node , operational node in scenario group , for . | |

| replica of the vector of variables for discomfort excess in strategic node , operational scenario in scenario group , for . |

For any scenario group , the elements of set can be randomly chosen from set , without repetition (i.e., ) and such that . For any , we define as -submodel the replica of the RES model (1)–(7) restricted to the set of strategic nodes associated with strategic scenarios . In any -submodel, the probabilities must be properly rescaled. Let denote the updated probability of scenario in the corresponding group , which can be computed as the ratio between the original probability of the scenario and the sum of the probabilities of all scenarios in group . Additionally, let denote the updated probability in group of a given node ; it is obtained by summing up the updated probabilities of all strategic scenarios passing through node . Thus, we can express any -submodel as the following optimization program

| s.t. | ||||

By combining the optimal values of the scenario groups with weights we can compute a lower bound of optimal value .

4.3 Scenario Multistage Clustering (SMC) approach

A second strategy to strengthen the lower bound provided by the method is by relaxing non-anticipativity constraints for strategic variables up to a given stage , which is referred to as breaking stage. By relaxing the non-anticipativity constraints up to the breaking stage , the multi-horizon problem decomposes into independent submodels. These submodels are referred to as the -submodels, for , where represents the set of strategic scenario clusters. The cardinality of equals . It is worth mentioning that each node in and its successors belong to just one scenario cluster in set . The approach is based on the solution of the - submodels. Table LABEL:tab:SMC_par reports the notation needed to formulate the approach

| Symbol | Description |

| breaking stage | |

| set of clusters of strategic scenarios. | |

| strategic node in stage associated with the scenario cluster . | |

| set of scenarios in cluster . | |

| set of nodes in cluster . | |

| weight of scenario cluster . | |

| weight of scenario in cluster , for . | |

| weight assigned to strategic node in cluster . | |

| replica of the vector of strategic decision variables in strategic node in scenario group , for . | |

| replica of the vector of operational decision variables in strategic node , operational node in scenario group , for . | |

| replica of the vector of variables for discomfort excess in strategic node , operational scenario in scenario cluster , for . |

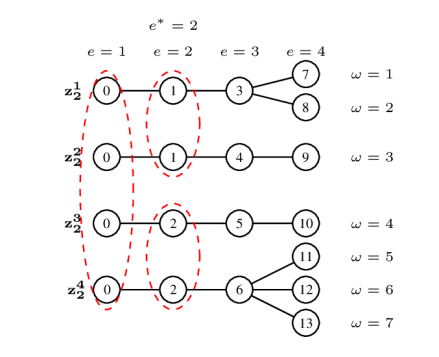

For any scenario cluster , let denote the unique node in stage belonging to cluster and let denote the set of strategic scenarios in group , which can be expressed as . Clearly, we have and . Fig. 2 provides a visual representation of this approach for a scenario tree consisting of 13 nodes and 7 scenarios.

By selecting the second stage as the breaking stage , the scenario tree decomposes into scenario clusters, with , , , and . In addition, note that nodes in stages 3 and 4 are included in only one scenario cluster, while the nodes in the early stages belong to more than one cluster.

For any , we define as -submodel the replica of the RES model (1)–(7) restricted to the set of strategic nodes associated with strategic scenarios . Similarly to the case, in any -submodel, probabilities must be properly rescaled. Let denote the updated probability of scenario in the corresponding cluster , which can be computed as the ratio between the original probability of the scenario and the sum of the probabilities of all scenarios in cluster . Additionally, let denote the updated probability in cluster of a given node ; it is obtained by summing up the updated probabilities of all strategic scenarios passing through node .

We can express any -submodel as the following optimization program

| s.t. | ||||

By combining the optimal values of the scenario clusters using as weights the sum of the probabilities of strategic scenarios in each cluster we obtain a lower bound of optimal value . It is worth mentioning that for the approach is equivalent to the scheme, as non-anticipativity constraints are fully relaxed and the problem decomposes into singleton scenario clusters, corresponding to the strategic scenarios of the problem.

4.4 Multi-Horizon Expected Value (MHEV) approach

An alternative way to obtain a lower bound for the original problem, especially useful for large-sized instances, is by replacing the stochastic processes by their expectations (see Maggioni et al. [2020]). In the approach, all the uncertain parameters (both the strategic and the operational ones) are replaced by their expected value:

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) |

Since no operational uncertainty is considered in this approach, the SD constraints (7) cannot be included in the model and the users discomfort can be controlled only by imposing constraint (6) to bound the expected discomfort at any stage . Let and denote the vectors of the objective function coefficients for the variables in the vectors and , respectively, for . Model is a deterministic program expressed as

| s.t. | ||||

4.5 Multi-Horizon Operational Expected Value (MHOEV) approach

An alternative approach to solving the deterministic program is to replace only the operational uncertain parameters in the RES model with their expected values, as done in (14) and (15), while considering the uncertainty of strategic stochastic parameters (see Maggioni et al. [2020]). Denoting with the vector of the objective function coefficients for the variables in vector , for , model can be expressed as follows

| s.t. | ||||

It can be shown, see Maggioni et al. [2020], that the solutions of problems and are lower bounds of the solution value . Those bounds are not stronger than bounds obtained with or approaches. However, much less computational effort is required, so that these schemes are very useful for large-sized instances.

5 Computational experiments

In this section, we present an extensive set of computational results to validate the proposed methodology. The analysis is based on a case study inspired by a building complex in southern Germany. Throughout the section, we report results obtained for three different multi-horizon scenario tree sizes: small, medium, and large. To evaluate the impact of discomfort modeling on system performance, we compare the outcomes of three models for each instance type: the RES model without user discomfort, the risk-neutral RES model, and the risk-averse RES model.

The section is organized as follows. Section 5.1 outlines the main features of the case study. Section 5.2 reports the results of solving the RES model as a monolithic problem, focusing on objective function values and computational time. Section 5.3 presents the lower bounds obtained using the schemes introduced in Section 4. Finally, Section 5.4 discusses the results of the heuristic approach introduced in Section 3.

5.1 The data

We consider a case study inspired by a building complex in southern Germany. The case study is constructed using publicly available data sources. Electricity prices are obtained from the ENTSOE’s Transparency Platform ENTSOE [2024], while PV production coefficients and load profiles are derived from the CoSSMic European project Open Power System Data [2020], which provides detailed consumption profiles, with resolutions reaching individual devices, for various small businesses and residential households.

To assess the performance of the RES model and its bounds, we analyze three types of instances: small, medium, and large. The problem dimensions for these instances are summarized in Table LABEL:pro-res-dimensions. Specifically, column 1 reports the instance size (i.e., small, medium or large). Columns from 2 to 5 describe the size of the strategic multistage scenario tree, including the number of stages , nodes , scenarios , and the branching degree . Columns 6 and 7 specify the dimensions of the operational two-stage scenario sub-trees rooted in each strategic node, detailing the number of operational scenarios and daily periods in each operational sub-tree. Finally, columns from 8 to 13 outline the size of the RES problem, reporting the number of PV technologies , BESS technologies , elastic loads , deferrable loads , pairs of incompatible consumptions , and pairs of loads subject to precedence constraints .

| Size | ||||||||||||

| Small | 3 | 13 | 9 | 3 | 10 | 12 | 3 | 2 | 25 | 25 | 10 | 10 |

| Medium | 4 | 40 | 27 | 3 | 20 | 12 | 3 | 2 | 40 | 35 | 15 | 15 |

| Large | 6 | 364 | 243 | 3 | 20 | 12 | 3 | 2 | 75 | 75 | 50 | 50 |

As shown in Table LABEL:pro-res-dimensions, the small instance represents strategic uncertainty with a three-stage tree, where each node (except for leaves) has three immediate successors, resulting in 13 nodes and 9 strategic scenarios. The medium instance includes an additional stage, while the large instance features a six-stage strategic tree with 364 nodes and 243 scenarios. In terms of operational uncertainty, the small instance models it using two-stage scenario trees with 12 daily periods and 10 operational scenarios rooted at each strategic node. Both the medium and large instances increase the number of operational scenarios to 20, providing a more refined representation of operational uncertainty for each strategic node.

All three instances include investments in three PV technologies (mono-crystalline, poly-crystalline, and thin-film panels) and two types of BESS (lead-acid and lithium-ion). Mono-crystalline panels are the most efficient but also the most expensive, while thin-film panels offer lower investment costs at the expense of reduced electricity production capacity. Regarding BESS, lithium-ion batteries have higher costs but greater storage capacity and higher charge/discharge depth limits. At the start of the planning period, investment costs are as follows: PV mono-crystalline 2.5 €, PV poly-crystalline 2.1 €, PV thin-film 1.95 €, lead-acid BESS 1.05 €, and lithium-ion BESS 1.3 €. In subsequent stages, investment costs in children nodes of each node are determined based on three trajectories: a stable cost trajectory, a cost reduction up to 30%, and a cost increase up to a 30% compared to the ancestor node . Maintenance costs are assumed to be 1.5% of the investment costs in each strategic node. A budget of 20,000 € for RES infrastructure investments is imposed at each strategic node.

The instances also differ in the number of controllable loads: 50 for the small instance, 75 for the medium instance, and 150 for the large instance. To analyze the impact of discomfort modeling on the optimal value of the problem, we evaluate three models for each instance type:

- 1.

- 2.

- 3.

In total, nine instances are tested. All computational experiments were conducted on an ASUS laptop equipped with a 3 GHz Intel Core i7-5500U processor and 4 GB of RAM, using the GAMS 24.7.4 environment and the Gurobi solver with GUSS (Gather-Update-Solver-Scatter). GUSS is a GAMS tool specifically designed to efficiently handle the batch processing of optimization problems with identical structure but varying data inputs (see Bussieck et al. [2012]). Instead of recompiling or recreating the model for each scenario or parameter set, GUSS utilizes the same model instance and iteratively updates its parameters. This approach eliminates the computational overhead associated with model initialization and compilation, which is particularly significant for complex problems. Moreover, by processing multiple scenarios within a single run, GUSS minimizes the overhead of repeatedly invoking the solver and managing input/output operations for each scenario. These features enable substantial reductions in computational time, especially in applications requiring the solution of multiple optimization problems with shared structure, such as the bounding schemes addressed in this paper.

5.2 Results of the direct solution of the RES model

Table LABEL:results-cpx provides the dimensions, the optimal objective function value and the CPU time for solving the nine instances derived from applying the three variations of the RES model to each instance type. Specifically, column 1 defines the size of the instance. The second column indicates the version of the RES model tested. Columns from 3 to 7 provide the dimension of the problem to be solved, reporting the number of constraints , integer variables , binary variables , continuous variables , and nonzero elements of the constraint matrix #Nze. Columns 8 and 9 report the results of solving the problem as a monolithic multi-horizon program, providing the optimal objective function value and the CPU time .

| Size | Model | |||||||

| Small | (1)–(5) | 158,266 | 26 | 46,930 | 46,840 | 515,425 | 5,093,382 | 24.09 |

| Small | (1)–(6) | 158,279 | 26 | 46,930 | 46,840 | 589,525 | 5,097,959 | 25.67 |

| Small | (1)–(7) | 158,565 | 26 | 47,060 | 46,970 | 664,275 | 5,746,672 | 35.05 |

| Medium | (1)–(5) | 1,400,591 | 80 | 432,400 | 384,121 | 4,869,757 | 7,520,072 | 447.46 |

| Medium | (1)–(6) | 1,400,631 | 80 | 432,400 | 384,121 | 5,553,757 | 7,967,872 | 671.32 |

| Medium | (1)–(7) | 1,402,311 | 80 | 433,200 | 384,921 | 6,241,757 | 13,627,470 | 1015.72 |

| Large | (1)–(5) | 21,590,651 | 728 | 5,245,240 | 6,116,293 | 56,961,232 | – | OOM |

| Large | (1)–(6) | 21,591,015 | 728 | 5,245,240 | 6,116,293 | 69,444,232 | – | OOM |

| Large | (1)–(7) | 21,606,345 | 728 | 5,252,540 | 6,123,593 | 81,989,647 | – | OOM |

Note that, for each instance size, the dimensional differences between models (1)–(5) and (1)–(6) stem solely from the inclusion of the additional constraints to bound the expected discomfort. Similarly, differences between the size of model (1)–(7) and model (1)–(6) are attributable to the additional decision variables and constraints required by the risk measure. Regarding computational performance, all RES models are solved efficiently for the small-size instance, with Gurobi achieving optimal solutions within CPU times on the order of tens of seconds. For medium-size instances, Gurobi successfully computes optimal solutions for all three RES models, although computational times increase significantly, particularly for the risk-averse model (1)–(7), which requires approximately 17 minutes. In contrast, solving the large-size instances directly proves computationally infeasible, underscoring the necessity of developing alternative methodologies to approximate or efficiently compute solutions for the RES model.

Regarding the objective function values, the results for both small- and medium-size instances clearly highlight the significance of incorporating discomfort modeling in the RES problem. The inclusion of discomfort considerations dramatically affects the model’s outputs. Specifically, protecting users from extreme discomfort scenarios can lead to a substantial increase in total system costs. In the small-size instances, the risk-averse solution incurs an additional 12.8% and 12.7% in costs compared to the solution that ignores discomfort and the risk-neutral model, respectively. The impact is even more pronounced in the medium-size instance, where the risk-averse solution results in costs that are 81.2% and 71.0% higher than the no-discomfort and risk-neutral models, respectively.

5.3 Results for the lower bound schemes

This section presents the lower bounds for all instances, as provided by the schemes outlined in Section 4. Specifically, Table LABEL:res-LB-b shows the value of the bounds and the corresponding CPU times for the , , and approaches. Table LABEL:res-LB-SMG provides the lower bounds for the approach, showing results for various choices of the number of groups . Finally, Table LABEL:res-LB-scm presents the outcomes of the approach for different values of the breaking stage .

| Size | Model | ||||||

| Small | (1)–(5) | 5,081,531 | (19.29) | 85,752 | (14.10) | 93,713 | (15.52) |

| Small | (1)–(6) | 5,081,531 | (20.23) | 652,034 | (15.03) | 692,540 | (16.56) |

| Small | (1)–(7) | 5,627,824 | (21.53) | ||||

| Medium | (1)–(5) | 7,481,041 | (58.32) | 253,623 | (25.12) | 253,770 | (27.21) |

| Medium | (1)–(6) | 7,919,379 | (65.71) | 5,320,846 | (25.46) | 5,372,962 | (33.67) |

| Medium | (1)–(7) | 13,606,112 | (69.11) | ||||

| Large | (1)–(5) | 41,066,993 | (723.51) | 2,256,139 | (39.87) | 2,322,285 | (188.61) |

| Large | (1)–(6) | 45,444,337 | (980.85) | 38,535,711 | (46.36) | 38,605,487 | (192.54) |

| Large | (1)–(7) | 60,499,195 | (983.18) | ||||

In all small- and medium-sized instances, the bounds obtained through the approach are very close to the optimal value of the corresponding RES problem. Conversely, the bounds generated by the and approaches are notably less tight, with the approach yielding marginally better results than .

The lower bounds derived from the approach can be further improved by grouping the strategic scenarios, as done in the method. Table LABEL:res-LB-SMG presents the resulting objective function approximations and the computational times required to compute these bounds for three distinct values of the parameter , representing the number of groups: 2, 5, and 10. In the small instances, where the total number of strategic scenarios is limited to 9, it is not feasible to partition the scenarios into 10 groups.

| Size | Model | ||||||

| Small | (1)–(5) | 5,086,860 | (23.03) | 5,086,581 | (25.69) | ||

| Small | (1)–(6) | 5,086,863 | (34.24) | 5,086,592 | (29.99) | ||

| Small | (1)–(7) | 5,742,359 | (40.02) | 5,740,937 | (30.37) | ||

| Medium | (1)–(5) | 7,499,313 | (78.50) | 7,481,360 | (80.99) | 7,481,060 | (90.54) |

| Medium | (1)–(6) | 7,930,194 | (91.55) | 7,919,984 | (91.54) | 7,919,679 | (95.01) |

| Medium | (1)–(7) | 13,615,408 | (82.77) | 13,609,282 | (77.49) | 13,608,111 | (91.24) |

| Large | (1)–(5) | – | OOM | 41,068,103 | (1641.13) | 41,067,634 | (1320.48) |

| Large | (1)–(6) | – | OOM | 45,767,974 | (2484.12) | 45,468,410 | (2078.91) |

| Large | (1)–(7) | – | OOM | 60,539,361 | (2610.22) | 60,499,254 | (2144.71) |

The parameter introduces a trade-off between the accuracy of the lower bound and the computational cost: smaller values of lead to tighter bounds but require greater computational effort to solve each sub-problem. Conversely, increasing reduces the computational burden of each sub-problem at the expense of bound quality. For large-scale instances, no feasible solutions can be obtained when the scenarios are grouped into only two groups, further illustrating the critical impact of on the applicability of the approach.

An alternative method to strengthen the lower bound provided by the approach is the method, where non-anticipativity constraints are relaxed up to a specific breaking stage, . Table LABEL:res-LB-scm presents the lower bounds obtained using the method for three distinct values of the breaking stage : , , and , where denotes the total number of stages in the problem. The case is excluded from Table LABEL:res-LB-scm since it corresponds to the bound. Furthermore, to ensure an approximation of the original problem, it is required that . As a result, for the small-size instances, where , only the case is considered. Similarly, for the medium-size instances, with , only the cases and are defined.

| Size | Model | ||||||

| Small | (1)–(5) | 5,088,391 | (22.10) | ||||

| Small | (1)–(6) | 5,088,391 | (30.12) | ||||

| Small | (1)–(7) | 5,634,860 | (27.41) | ||||

| Medium | (1)–(5) | 7,498,189 | (60.52) | 7,498,230 | (66.61) | ||

| Medium | (1)–(6) | 7,951,062 | (64.65) | 7,951,545 | (66.31) | ||

| Medium | (1)–(7) | 13,624,496 | (65.22) | 13,627,436 | (67.91) | ||

| Large | (1)–(5) | 41,117,245 | (533.81) | 41,118,301 | (494.04) | 41,119,221 | (660.23) |

| Large | (1)–(6) | 45,859,502 | (801.61) | 45,860,004 | (689.81) | 45,860,184 | (960.22) |

| Large | (1)–(7) | 60,562,808 | (721.13) | 60,563,201 | (705.23) | 60,565,811 | (840.47) |

Table LABEL:res-LB-scm demonstrates the effectiveness of the method in producing tight lower bounds. The quality of these bounds shows marginal improvements as the breaking stage , up to which non-anticipativity constraints are relaxed, is anticipated. This suggests that significant benefits are already captured at higher values of . The computational effort associated with reveals a trade-off: reducing lowers the number of sub-problems to solve but increases their complexity. Consequently, CPU times do not exhibit a monotonic trend. For example, in large-scale instances, the optimal computational performance is achieved when the breaking stage is set to .

Several conclusions can be drawn from the application of the lower-bound schemes. First, the weak bounds obtained through expectation-based methods (see Table LABEL:res-LB-b) highlight the necessity of incorporating short-term variability into the bounding schemes. Ignoring key factors such as solar energy intermittency and electricity price volatility results in significant underestimation of system costs. Hence, only methods that explicitly address operational uncertainty can provide reliable bounds for the RES problem. Second, the method provides tight lower bounds, which can be further enhanced by the and approaches, with generally yielding superior results (see Tables LABEL:res-LB-SMG and LABEL:res-LB-scm). Except for the small-size risk-averse discomfort instance and the medium-size no-discomfort instance, the method consistently outperforms , delivering tighter bounds with significantly reduced computational time. This demonstrates the robustness and efficiency of in tackling complex instances of the RES problem.

5.4 Performances of the proposed algorithm to compute feasible solutions

This section presents the main results of applying the heuristic approach described in Section 3 to various model instances, employing different strategies for assigning values to the parameters , , and . Table LABEL:res-sfr3-b available in Appendix A, reports the results for small- and medium-size instances. The first column specifies the size of the instance, while the second column identifies the tested version of the RES model. Columns 3 to 5 describe the heuristic strategy, detailing the number of non-relaxed stages , the number of relaxation stages , and the probability associated with node selection . Columns 6 and 7 compare the optimal objective function value with the cost of the feasible solution . Column 8 computes the gap between the feasible solution and the best lower bound, expressed as , where is the best lower bound, retrieved from Tables LABEL:res-LB-SMG and LABEL:res-LB-scm. Column 9 provides the gap between the feasible solution and the optimal value, defined as . The final column reports the CPU time required to compute the feasible solution.