The Scaling Behaviors in Achieving High Reliability via Chance-Constrained Optimization

Abstract.

We study the problem of resource provisioning under stringent reliability or service level requirements, which arise in applications such as power distribution, emergency response, cloud server provisioning, and regulatory risk management. With chance-constrained optimization serving as a natural starting point for modeling this class of problems, our primary contribution is to characterize how the optimal costs and decisions scale for a generic joint chance-constrained model as the target probability of satisfying the service/reliability constraints approaches its maximal level. Beyond providing insights into the behavior of optimal solutions, our scaling framework has three key algorithmic implications. First, in distributionally robust optimization (DRO) modeling of chance constraints, we show that widely used approaches based on KL-divergences, Wasserstein distances, and moments heavily distort the scaling properties of optimal decisions, leading to exponentially higher costs. In contrast, incorporating marginal distributions or using appropriately chosen

-divergence balls preserves the correct scaling, ensuring decisions remain conservative by at most a constant or logarithmic factor. Second, we leverage the scaling framework to quantify the conservativeness of common inner approximations and propose a simple line search to refine their solutions, yielding near-optimal decisions. Finally, given

data samples, we demonstrate how the scaling framework enables the estimation of approximately Pareto-optimal decisions with constraint violation probabilities significantly smaller than the -barrier that arises in the absence of parametric assumptions.

Keywords: High reliability, Service level agreements, Chance constrained optimization, Distributionally Robust Optimization, Extreme Value Theory, CVaR approximation, Large deviations

1. Introduction

Consider a service provider striving to meet a target level of service in the face of uncertainty. For instance, a distributor of a commodity like electricity needs to fulfill uncertain demands at different nodes of a distribution network. The distribution firm must allocate supply capacities to various nodes in such a way that excessive demand shedding occurs in no more than an fraction of the service instances, where is a pre-specified service level agreement, typically close to 1. Similarly, an emergency response service provider might seek to minimize the costs of positioning and dispatching ambulances while ensuring that the uncertain spatially distributed demand for emergency services is met with probability . What is the minimum cost the service provider will incur in meeting such high service level agreements? Specifically, how large must this minimum cost and the optimal resource allocations be if the provider aims to ensure very high levels of service availability, as required in contexts like electricity distribution, cloud computing, or emergency medical response? This paper focuses on analytically treating this question, as gaining a more explicit understanding of how various cost parameters and the uncertainty influence this minimum cost is a crucial first step towards gaining insights into the economics of high reliability.

1.1. Chance constrained optimization

For several decades, chance constrained optimization has served as a typical starting point for modeling the above class of problems; see Charnes & Cooper, (1959), Prékopa, (1970), Shapiro et al., (2021). A generic chance-constrained optimization formulation can be stated abstractly as,

| (1) |

where the goal is to find a decision from a set that minimizes a cost function while ensuring that the service/reliability constraints, modeled via are satisfied with high probability despite the parameters affecting the constraints being random. In this paper, we will be primarily interested in the case where is a continuous -valued random vector admitting a probability density function. For any decision choice constraint violation models an undesirable disruption event such as excessive demand shedding or a failure to dispatch an ambulance within a 15-minute window.

To gain a comprehensive view into how the formulation (1) serves as a powerful vehicle for modeling high service availability or high reliability requirements in various contexts, refer sample applications in power systems and electricity markets (Bienstock et al., 2014, Wu et al., 2014, Pena-Ordieres et al., 2020), cloud computing (Cohen et al., 2019, Kwon, 2022), emergency medical service (ReVelle & Hogan, 1989, Beraldi et al., 2004), portfolio selection (Agnew et al., 1969, Ghaoui et al., 2003, Bonami & Lejeune, 2009), healthcare management (Deng & Shen, 2016, Wang et al., 2021), project management (Shen et al., 2010), telecommunication networks (Li et al., 2010), supply chain and logistics (Wang, 2007, Li et al., 2017), humanitarian relief operations (Özgün Elçi & Noyan, 2018), and staffing call centres (Gurvich et al., 2010).

While the formulation in (1) is conceptually attractive and conducive for quantitatively modeling contractual service-level agreements, it does not lend itself readily to tractable solution procedures. To begin with, observe that the potential non-convexity of the collection of decisions satisfying the probability constraint renders (1) computationally intractable, generally speaking. Beyond a narrow collection of problems (see, eg., Prékopa et al., 1998, Dentcheva et al., 2000, Lagoa et al., 2005), it is well-known that instances of (1) where both (i) the efficient computation of the probability and (ii) the convexity of the feasible set hold simultaneously are rare. Therefore, clever algorithmic inventions have been necessary to computationally handle the formulation (1) in general. These include the use of convex inner approximations (see, eg., Nemirovski & Shapiro, 2007), scenario approximation (Calafiore & Campi, 2006), strengthening mixed-integer program formulations (see, eg., Luedtke et al., 2010), among many notable algorithmic developments for tackling (1). Despite the broader computational challenges, chance-constrained optimization remains a widely used model for decision-making under uncertainty.

1.2. Research questions and our contributions

Diverging from the above discussed methodological research thrusts, this paper aims to develop a qualitative understanding of the properties of the optimal value and optimal solutions to when aiming for a high degree of reliability, specified via a target reliability level close to one in (1). To illustrate this pursuit concretely, consider the question: “By how much should an electricity distribution firm increase the generator/supply capacities at different nodes of a network if it aims to halve the likelihood of excess demand shedding, say, from to ?” Alternatively, how steeply does the capital expenditure increase as a function of the target level with which we wish to avoid network failures due to excess demand shedding? Currently, aside from methods—which become computationally demanding and less accurate under stringent reliability requirements—we lack a means to qualitatively understand how different cost parameters and uncertainties influence the answers to such questions. However, gaining a qualitative understanding into these questions is equally crucial from an operations and risk management perspective.

In this paper, we aim to alleviate this challenge by analytically examining the chance-constrained formulation in the high reliability regime where With large deviations theory (see, eg., Dembo & Zeitouni, 2009) providing a systematic framework for studying how significant deviations in the behaviour of the random vector leads to atypical events, we propose to treat the probability constraint in under the lens of large deviations approximations. When the target service level approaches one, this approximation allows us to view as a perturbed and scaled version of a limiting optimization problem that we can explicitly write. Leveraging the rich literature on perturbation analysis of optimization models (Rockafellar & Wets, 2009, Bonnans & Shapiro, 2013), we uncover a remarkable regularity in the behavior of optimal values and solutions to when the distribution of and the constraint functions in (1) admit sufficient regularity. Besides offering qualitative insights, this regularity has several algorithmic implications. The rest of this section is dedicated to describing these contributions and discussing related literature.

1.2.1. Scaling of optimal costs and decisions under high reliability requirements.

Let denote the optimal value of and denote an optimal solution to As our first main contribution, we explicitly identify a suitable scaling function which increases to infinity and a constant such that,

| (2) |

as the permissible probability of service disruption, denoted by in , is decreased to zero. Here the notation is used to indicate concisely that and as decreases to zero. The precise limiting notion, the choice of the scaling function constant and the non-zero limits and are identified in Theorem 3.1. A key observation here is that it is possible to explicitly characterize the rate at which the optimal value and the optimal solution of scale as a function of the target level approach one, and it depends on the probability density of primarily via the marginal distribution of its components

The observation that the rate at which the optimal cost of meeting high reliability scales, is free of the dependence structure across the components might offer a degree of relief for decision-makers who may have to estimate the joint distribution of from data. Estimating the joint distribution well in the tail regions where constraint violations happen typically is a formidable statistical challenge. The results reveal that although misspecifying the copula may yet affect the constraint satisfaction, its impact on the prescribed decisions and their costs remains bounded when viewed as a function of .

1.2.2. Algorithmic implications of the scaling phenomenon (2).

Similar to how analyzing the scaling of computational effort with problem size aids in discriminating and developing efficient algorithms in computer science, the novel approach of analyzing the optimization instances as a function of the target level carries the following novel algorithmic implications.

Application 1: Delineating chance-constrained DRO models with sharp characterizations of their conservativeness. Given a collection of plausible probability distributions for the random vector the distributionally robust optimization (DRO) approach towards tackling chance constraints involves replacing the probability constraint in (1) with the uniform requirement Motivated by considerations of tractability and finite-sample guarantees, the distributional ambiguity set is formulated typically via moment constraints (see, eg., Ghaoui et al., 2003, Natarajan et al., 2008, Hanasusanto et al., 2017), -divergence balls (see, eg., Jiang & Guan, 2016), or Wasserstein balls (see Xie, 2021, Ho-Nguyen et al., 2022, Chen et al., 2024); see also the survey article Küçükyavuz & Jiang, (2022). While the uniform requirement is conceptually a conservative approach, some choices of are intuitively considered more conservative that others. With the performance of a DRO model relying crucially on the choice of the ambiguity set can we characterize the cost scaling of the optimal decisions prescribed by the DRO models for different choices of so that we can precisely delineate them based on their conservativeness?

Employing the aforementioned large-deviations machinery, another key contribution in this paper is to characterize the scaling of the optimal decisions prescribed by some prominent DRO formulations together with their costs. The results reveal that commonly used DRO approaches based on KL-divergences, Wasserstein distances, and moments heavily distort the scaling properties of optimal decisions and result in exponentially higher costs. On the other hand, incorporating marginal distributions (or) employing suitably chosen -divergence balls preserves the correct scaling and ensures that their solutions remain conservative by at most a constant or logarithmic factor.

Application 2: Quantifying and reducing the conservativeness of inner approximations based on CVaR and Bonferroni inequality. In computationally handling the joint probability constraints in (1), solving inner approximations based on conditional value-at-risk (CVaR) and Bonferroni inequality have served as two widely used approaches (eg., Nemirovski & Shapiro, 2007). While solutions from the inner approximations remains feasible for the extent of optimality loss is less understood—specifically, how much more expensive are their solutions? Using our large deviations-based scaling framework, we develop sharp characterizations akin to (2), providing key insights into their conservativeness. The results reveal that both CVaR- and Bonferroni-based inner approximations exhibit negligible relative loss in optimality when the underlying random variables are light-tailed. In the presence of heavy-tailed random variables, both methods yield decisions that are more expensive by a constant factor. Notably, CVaR-based approximations score better by producing decisions proportionate to those of : Specifically, we establish

| (3) |

where constant and denote the optimal value and solution of the CVaR-constrained approximation of and are the same as in (2). Although the conservativeness, quantified by increases with heavier-tailed distributions, we propose an elementary line-search (see Algorithm 1) that can strictly improve the solution into near-optimal decisions for irrespective of tail heaviness.

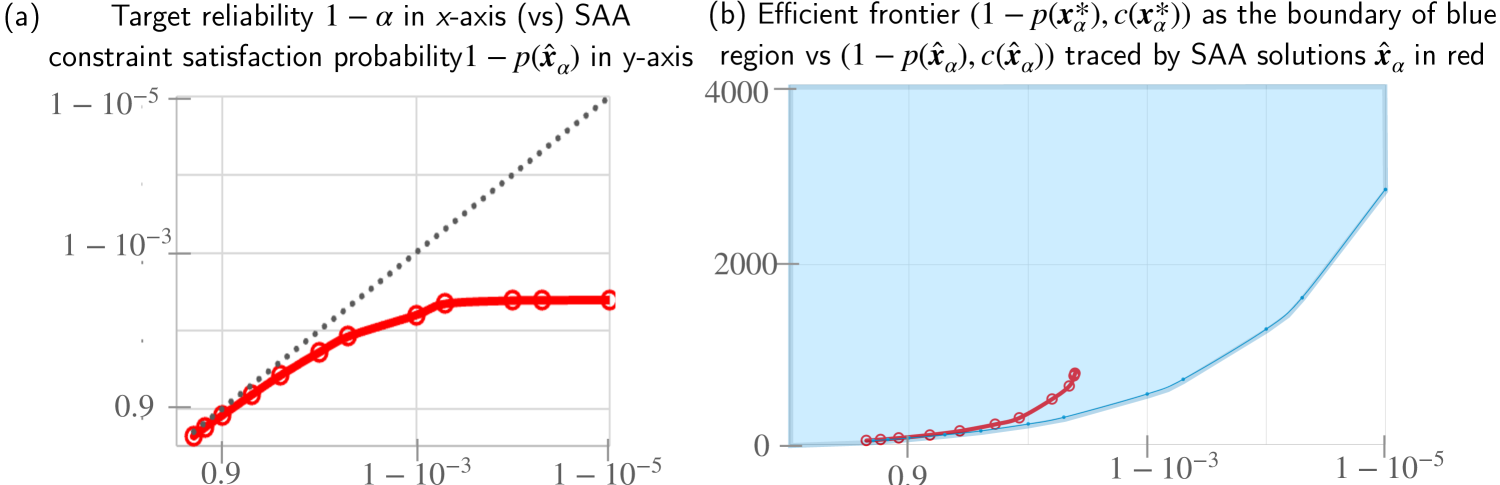

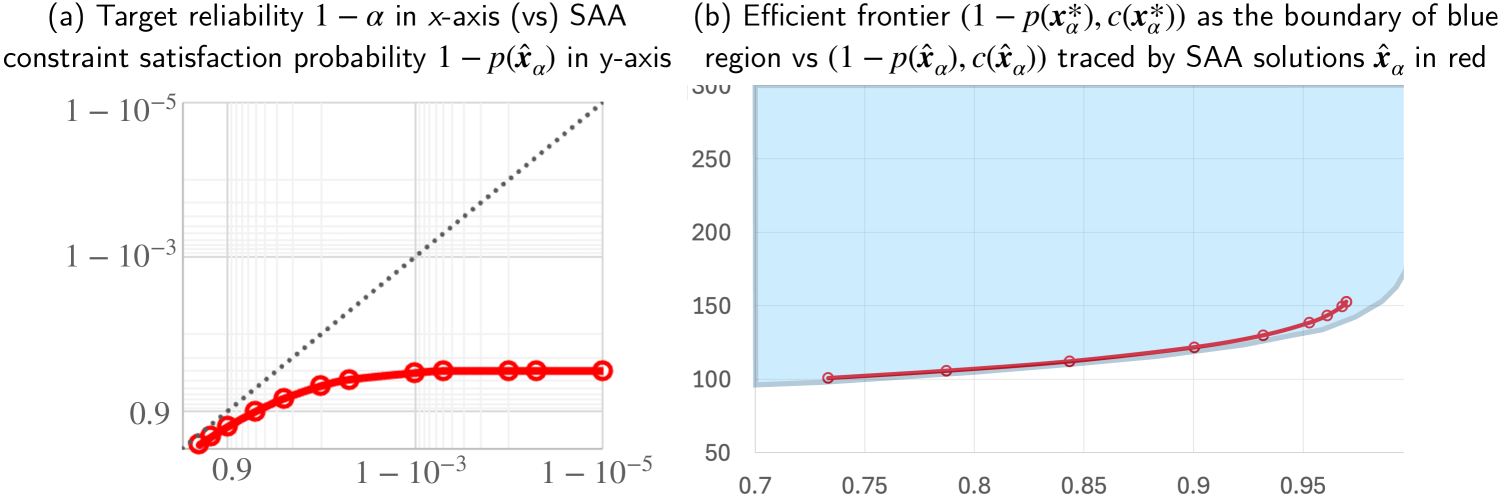

Application 3: Estimating Pareto efficient decisions from limited data. In data-driven applications, the choice of the distribution in the formulation is informed typically by a limited number of independent observations of Given such samples and a target constraint violation probability , observe that it is statistically impossible to nonparametrically identify a decision whose constraint violation probability is smaller than unless additional assumptions are made about the distribution of This is manifestly observed in any sample average approximation (SAA) of the chance constraint in which target as illustrated via a numerical example in Figure 1 below with observations. In Fig 1(a), we see that an SAA optimal solution falls significantly short of satisfying the target reliability level for all Next, we also observe from both the panels in Fig 1 that SAA is not able to arrive at a solution whose constraint violation probability is smaller than the level regardless of how large we set the target to be.

The underestimation reported in Figure 1 happens because for any patently infeasible decision whose constraint violation probability is in the range we have samples falling, on an average, in the constraint violation region. As a result, SAA is prone to dangerously underestimating the constraint violation probability to be zero and declare such an to be feasible, at least 50% of the times. This is a fundamental statistical bottleneck which limits the use of nonparameteric estimation approaches in applications requiring high reliability levels where In an attempt to overcome this bottleneck, at least partially, we ask, “can we develop a nonparametric estimation procedure that, under minimal assumptions, can yield decisions that are Pareto efficient in balancing the cost and the constraint violation probability even when ?”

As our final illustration of the utility of the large-deviations scaling framework, we demonstrate how (2) can serve as a basis for addressing the above ambitious question, much like how the field of extreme value theory in statistics provides a rigorous framework for estimating quantiles at levels far beyond what is feasible with finite data (see, eg., De Haan & Ferreira, 2007, Chap. 1, 4). Specifically, under a minimal nonparametric assumption on the distribution of we show in Section 6 that a suitably extrapolated trajectory of solutions, grounded in (2), is nearly optimal in minimizing the constraint violation probability for any given cost target, even when the cost target is sufficiently large to allow

1.3. Related literature utilizing large deviations theory in optimization modeling

While large deviations theory is frequently used to analyze the quality of solutions from sampled approximations (see, eg., Shapiro & Homem-de Mello, 2000), its direct application in formulating or studying optimization models is relatively limited. Van Parys et al., (2021), Sutter et al., (2024), Li et al., (2021) apply Sanov’s theorem–a key result in large deviations theory–to identify data-driven formulations that optimally balance conservativeness of solutions with out-of-sample performance. More closely related to our pursuit are Mainik & Rüschendorf, (2010), Nesti et al., (2019), Tong et al., (2022), and Blanchet et al., (2024). For linear portfolios comprising assets with heavy-tailed losses, Mainik & Rüschendorf, (2010) seek to minimize their extremal risk index, a notion arising from large deviations approximation of the excess losses probabilities. Nesti et al., (2019), Tong et al., (2022) approximate chance-constraints using large deviations heuristics for suitably light-tailed random vectors, focusing on the computational aspects of solving the resulting bi-level problems.

The recent independent study by Blanchet et al., (2024), made public in arXiv about a month before the first version of this paper, shares our objectives of (i) characterizing the scaling of the optimal value in chance-constrained models and (ii) assessing the conservativeness of CVaR approximations. Their analysis focuses on a specific case of (1), where for and additionally quantifies the quality of solutions provided by scenario approximation (Calafiore & Campi, 2006). We now outline the key differences: Fundamentally, in the model studied by Blanchet et al., (2024), both the optimal value and the optimal resource allocation decisions shrink to zero as the target reliability level is raised to 1, implying that the scaling in (2) must satisfy . This qualitative phenomenon contrasts sharply with those in common resource provisioning tasks such as in commodity distribution networks, emergency response, or cloud servers, etc., where resource allocations must scale up to meet stricter service level requirements. One of the contributions of our paper lies in identifying minimal structural assumptions on the constraint functions under which both these qualitative phenomena can manifest. In particular, our abstraction provides the flexibility to study both the setting considered by Blanchet et al., (2024) and the more common setting where the optimal value of must scale up as the target level is raised. Our framework is versatile enough to accommodate a wider variety of chance constraints, including those with nonlinearities and uncertainties on either the left- or right-hand side quadratic constraints, and more. Additionally, the results characterizing the conservativeness of DRO models, the algorithmic breakthrough of data-driven estimation of Pareto-optimal decisions even when and the line-search procedure for reducing the conservativeness of CVaR approximation, are all novel and unique to this paper.

Organization of the paper. Section 2 introduces the precise chance-constrained model assumptions under which we derive our results. Section 3 is devoted to discussing the first main result on the scaling of optimal values and decisions. Section 4 delves into the implications of the scaling framework for DRO modeling. Sections 5 - 6 are devoted, respectively, to the applications relating to quantifying the conservativeness of inner approximations and data-driven estimation of Pareto optimal solutions. Numerical illustrations are provided shortly after the key results to quantitatively complement their understanding. Proofs are furnished in the appendix.

2. Model description and assumptions

Notational Conventions. Vectors are written in boldface to enable differentiation from scalars. For any and let and denote the respective component-wise operations. Let be the extended real-line, denote the positive orthant, and denote its interior. For and , let denote the distance between and the set . For real-valued sequences and , we write as if if and if For any Borel measurable set , denote the set of all Borel probability measures on as . For any positive integer we use to denote

2.1. Assumptions on the constraints and illustrative examples

Recall the chance constrained optimization model (1), which we labeled as in the introduction. A key ingredient in the model is the collection of constraints where is a positive integer, and are lower semicontinuous functions specified suitably for a problem at hand. With denoting an -valued random vector modeling all the uncertain factors affecting the decision problem, the constraints typically model critical requirements such as meeting demands in commodity supply networks or disaster relief networks (see Examples 1-2 below), or regulatory capital requirements in insurance-reinsurance networks (eg., Blanchet et al., 2023). In applications where it is either infeasible or unduly expensive to ensure that the requirements are always satisfied, the decision-maker strives to ensure that they are met, at least, with a pre-agreed target probability level In line with this goal, the chance-constrained optimization model seeks to find a decision from the set that minimizes the cost function while meeting the service level agreement

Throughout the paper, we shall assume that the random vector has a probability density supported on a closed cone In applications, we typically have as either the positive orthant or the euclidean space the cost function is linear in the decision , and the service requirements are often specified via functions which are linear or bilinear in In more sophisticated instances, the functions may be non-linear (or) may get specified by means of the value of an optimization problem; see, for eg., Yang & Xu, (2016), Blanchet et al., (2023), Pena-Ordieres et al., (2020). Without restricting to a specific functional form, our assumptions below specify requirements on the constraint functions that bestow sufficient regularity while allowing broader use. We first introduce the notion of “safe set” for any decision which is helpful towards this end. For any let

| (4) |

denote the set of scenarios for which the constraints hold for all Observe that is a set-valued map. Let

Definition 1 (Non-vacuous set-valued mapping).

We call a set-valued map to be non-vacuous for the support and the decision set if for every the “unsafe set” is (i) non-empty, and (ii) bounded away from for every

Equipped with these notions, we are now ready to introduce the regularity required for our analysis.

2.1.1. Homogeneous safe-set model.

We first present the simpler model based on homogeneity here, before moving to the more general assumption in Section 2.1.2.

Assumption 1.

There exists a constant such that for any and we have and Further, the map defined in (4), is continuous on and non-vacuous for the support and decision set

Assumption 1 allows for an easy interpretation as follows: Given any and suppose that a decision-maker wishes to identify a decision that makes scenarios to be safe (that is, ). Satisfaction of Assumption 1 means that they can achieve this by choosing In other words, As it will become evident from the first main result (Theorem 3.1) in Section 3, non-vacuousness of the safe-sets will ensure that the value of in (1) is not trivially zero or infinite.

Example 1 (Joint capacity sizing and probabilistic transportation).

Consider the formulation,

which includes the classical transportation problem as an instance with applications in commodity distribution and emergency response; see, eg., Luedtke et al., (2010), Beraldi et al., (2004). In this joint capacity sizing and transportation problem, we have factories producing a single commodity, distribution centers, and a distribution center connected with a factory only if lies in the edge set The goal is to identify factory supply capacities and a transportation plan jointly such that the cumulative capacity allocation and transportation costs is minimized while ensuring the factories are resourced sufficiently to meet the demand at the distribution centers with probability

To verify Assumption 1, observe that is a cone. Further, Since the graph of the map given by

is polyhedral, the map is continuous (Rockafellar & Wets, 2009, Eg. 9.35). Further, note that whenever for we have for any As a result, and due to the convexity of we have that the map is non-vacuous for the support and decision set

Note that the reasoning in Eg. 1 does not rely on the network structure, and Assumption 1 can be verified to hold with more broadly for linear chance constraints of the form featuring right-hand uncertainty.

Example 2 (Network design).

Consider the problem

| (5) | ||||

in which a network designer aims to locate outposts at suitable vertices of a given network, equip those vertices with supply capacities and arcs with flow capacities such that the following requirement is met: The stochastic demands arising in different nodes of the network, captured by the random vector should be met with a feasible flow with probability at least Here is the node-arc incidence matrix. Network design formulations of this nature arise in disaster relief (Hong et al., 2015) and emergency medical response (Boutilier & Chan, 2020); see also Atamtürk & Zhang, (2007). If we take then note that is finite if and only if there is a feasible flow. Further, if is finite. Therefore, the chance constraint in (5) can be equivalently written as Note that for any and we have and An immediate implication of this homogeneity is as

Since the graph of the map given by is polyhedral, the map is continuous (see Rockafellar & Wets, 2009, Eg. 9.35). Exactly following the same reason in Example 1, we have to be non-vacuous for the support and the decision set Therefore Assumption 1 is satisfied with

2.1.2. Non-homogeneous safe-set model.

We next present an alternative requirement on the constraint functions that holds more broadly than the homogeneous case in Section 2.1.1.

Assumption 2.

There exist constants and a function such that the following are satisfied:

-

i)

for any and we have

-

ii)

for any sequence

(6) -

iii)

given any sequence and we have

(7) for some sequence

-

(iv)

the set-valued map defined by is non-vacuous for the support and the decision set

Observe that (6)-(7) are readily satisfied if for any sequence The weaker notion of convergence in (6) - (7) is related to the well-known notion of epi-convergence in the optimization literature (Rockafellar & Wets, 2009, Prop. 7.2). Specifically, if we let as suitably scaled versions of the constraint functions, then (6) - (7) are equivalent to saying that the sequence of functions are epi-converging to whenever . Another sufficient condition for (6) - (7) is the epi-convergence of when is convex for every and (Rockafellar & Wets, 2009, Prop. 7.48).

Example 3 (Linear portfolio selection).

Consider the problem,

which aims to select a minimum cost portfolio weight vector whose resulting portfolio return is above a prescribed minimal level with probability at least see, example, Bonami & Lejeune, (2009), Pagnoncelli et al., (2009a). Here is the risk-free return and is the random vector modeling returns of risky assets. One may take signifying average portfolio return, as taken in Pagnoncelli et al., (2009a), (or) combine it with a risk measure signifying portfolio variance as in Bonami & Lejeune, (2009). Note that satisfies

whenever As a result, Assumption 2 holds with and The resulting is non-vacuous for the support and decision set when

Note that if we had alternatively taken the scaling constants in (6) - (7) to be in Example 3, we would obtain which would lead to vacuous On the other hand, if we had taken we would obtain which would again lead to a vacuous Proposition 2.1 below asserts that an appropriate choice of scaling constants in Assumption 2 that renders the resulting to be non-vacuous is unique.

Proposition 2.1.

If the collection of constants for which Conditions (ii) - (iv) of Assumption 2 are satisfied is non-empty, then it is unique.

2.2. Assumptions on the cost function

We next introduce a mild structure on the cost which can be readily verified in the examples in Section 2.1. To state the assumption, recall the definition and the constant for which the constraint functions satisfy Assumption 1 or 2.

Assumption 3.

The cost function is positively homogeneous, that is, for every and Further, the mapping is strictly increasing for every

Note that if is positively homogeneous with degree then one can simply take as the cost function satisfying Assumption 3. The results also extend to the case of approximately homogeneous costs where as uniformly over in compact subsets of not containing the origin. For the ease of exposition, we limit the treatment to Assumption 3.

2.3. Assumptions on the probability distribution of

We assume that the random vector satisfies either Assumption or Assumption below, with the former corresponding to multivariate light-tailed distributions and the latter capturing multivariate heavy-tailed distributions. For let denote the probability density of denote the complementary cumulative distribution function (CDF) of Let capture the marginal distribution with the heaviest tail. The following definition is useful for introducing Assumptions and

Definition 2.

A function is said to be regularly varying with index if for every

If is regularly varying with index we abbreviate this as Regularly varying functions offer a systematic and general approach for studying functions with polynomial growth/decay rates, and have served as a fundamental tool for modeling and studying distribution tails: see, example, Feller, (2008), De Haan & Ferreira, (2007), Resnick, (2007).

Assumption ().

[Lighter-tailed distributions] The joint probability density admits the following representation uniformly over in compact subsets of not containing the origin:

for a positive function and

Assumption ().

[Heavier-tailed distributions] The joint probability density admits the following representation uniformly over in compact subsets of not containing the origin:

for a positive function and

Lemma 2.1 (Marginal distributions under Assumption ).

Under Assumption

-

a)

the complementary CDFs possess an exponential decay rate as in as where the positive constants for

-

b)

the heaviest tail and

-

b)

consequently, one could have taken in Assumption () without loss of generality; in this case we will have

Lemma 2.2 (Marginal distributions under Assumption ).

Under Assumption

-

a)

the complementary CDFs possess a polynomial decay rate as in as where the positive constants for

-

b)

the heaviest tail and

-

b)

consequently, one could have taken in Assumption () without loss of generality; in this case we will have

Several commonly used multivariate distributions, including the Gaussian distributions, multivariate , several classes of elliptical distributions, Archimedean copulas, log-concave distributions and exponential families, satisfy Assumptions or ; please refer Deo & Murthy, (2023), Section E.C.2 for a more comprehensive list, their verification, and related properties. Note that the nonparametric nature of allows a great degree of flexibility in modeling various copula and tail dependence structures. Example 4 below serves as a pointer towards understanding how Assumptions and are natural for capturing light and heavy-tailed phenomena respectively. Further examples are available in Resnick, (2007) and references therein.

Example 4 (Elliptical distributions).

If is elliptically distributed on then its pdf is given by for some positive definite matrix mean vector and a suitable generator function (see, eg., Frahm, (2004), Corollary 4). As special examples, we have the generator for to be multivariate normal distributed, and for to possess multivariate -distribution with degrees of freedom.

In the multivariate normal case, note that Assumption is readily satisfied with as,

as , uniformly in compact sets, for a suitable constant Similarly, any generator function satisfying leads to the resulting as The parameter choice leads to distributions with tails heavier than the normal distribution and leads to Weibullian tails that are heavier than the exponential distribution.

For multivariate -distributions, the heavy-tailed Assumption holds with as,

3. Scaling of optimal value and solution in the high reliability regime

3.1. Large deviations characterizations for the probability of constraint violation

In order to understand the behavior of optimal value and solutions of we first derive novel characterizations of the probability of constraint violation, under the assumptions introduced in Section 2. To state the results governed by the cases in Assumption 1-2 in a unified manner, we take throughout the paper,

Proposition 3.1.

Proposition 3.2.

A well-known example of explicit characterizations of the constraint violation probability, similar to those in Propositions 3.1 - 3.2, is from the setting of linear chance constraint, under multivariate normal distribution for Here take to be a given constant, and is a positive definite covariance matrix. Since in this instance, we readily have where is the complementary CDF of the standard normal distribution. Due to this explicit expression, the chance constraint reduces to the deterministic equivalent in this case. Such deterministic equivalents, while pivotal in the earlier literature, are typically difficult to obtain beyond stylized examples. The probability characterizations in Propositions 3.1 - 3.2 above can be viewed as offering a pathway towards such deterministic characterizations much more broadly, with the caveat that the resulting deterministic constraints set we introduce next becoming equivalent to the chance constrained set only asymptotically.

3.2. Main result 1: Scaling of the optimal cost and solutions of

To ease the notational burden, define

| (8) |

where is the inverse function of In line with the notation in Lemma 2.1-2.2 and Propositions 3.1 - 3.2, assign for any

| (9) |

Theorem 3.1.

Suppose that the constraint functions satisfy either Assumption 1 or Assumption 2, the cost function satisfies Assumption 3, and satisfies Assumption () or (). Then, as

-

a)

the optimal value of , call it satisfies where is the optimal value of the deterministic optimization problem below in (10):

(10) -

b)

any optimal solution of call it satisfies where denotes the set of optimal solutions for In particular, if has a unique solution then

(11)

Example 5.

Consider the linear chance constraint with being elliptically distributed as in Example 4, matrices and for Here the constraint functions for readily satisfy Assumption 1 with If the generator for the elliptical distribution satisfies we have from Example 4 that Assumption is satisfied with and Let for Then from Lemma 2.1(b), we have as where and Further, from the definition of in (9), we have Since the constraints are linear in the variable a typical application of Lagrange duality leads to Then the resulting in Theorem 3.1 is given by,

| (12) |

Therefore the characterization in Theorem 3.1 translates to

where and denote the optimal value and solution of (12) and the target reliability level If the optimal solution set of (12) is not a singleton, then

3.2.1. A discussion on the scaling rate.

First, note that Theorem 3.1 precisely characterizes the rate at which an optimal solution and its respective cost vary with respect to the target reliability level Interestingly, this scaling rate is determinable entirely from (i) the constant in Assumptions 1 or 2 capturing a certain rate of growth of the constraint functions , and (ii) the function which captures the rate at which the complementary CDF of the marginal distributions of decay to zero. In the cases where as in Examples 1-2, greater reliability is attained by increasing the capacities of supplies (optimal ). On the other hand, in the case where as in the portfolio optimization setting, greater reliability is attained by decreasing the weights of the risky assets (optimal ). Further, the dependence on highlights that as the tails of the marginal distribution of become heavier, the corresponding value of increases. A more precise characterization of the growth rate of under Assumptions and stipulating light-tailed and heavy-tailed distributions, respectively, are given in Lemma 3.1 below.

Lemma 3.1.

As we have

-

(i)

under Assumption and

-

(ii)

under Assumption

Suppose and consider a reliability level sufficiently close to 1. Then it follows from the scaling rate characterization in Lemma 3.1 that that a decision-maker endowed with, for instance, twice as much budget as the optimal cost can reduce the probability of constraint violations at most by a factor if is heavy-tailed. Indeed, this is because (a) if and only if due to Theorem 3.1, and (b) is solved at when The heavier the tail, smaller is the index resulting in a less significant reduction in constraint violation probability. If is light-tailed on the other hand, Lemma 3.1 implies that the probability of constraint violations can be reduced to an exponentially smaller level when the decision-maker is allowed to select a decision whose cost is This can be verified similarly by solving for in for

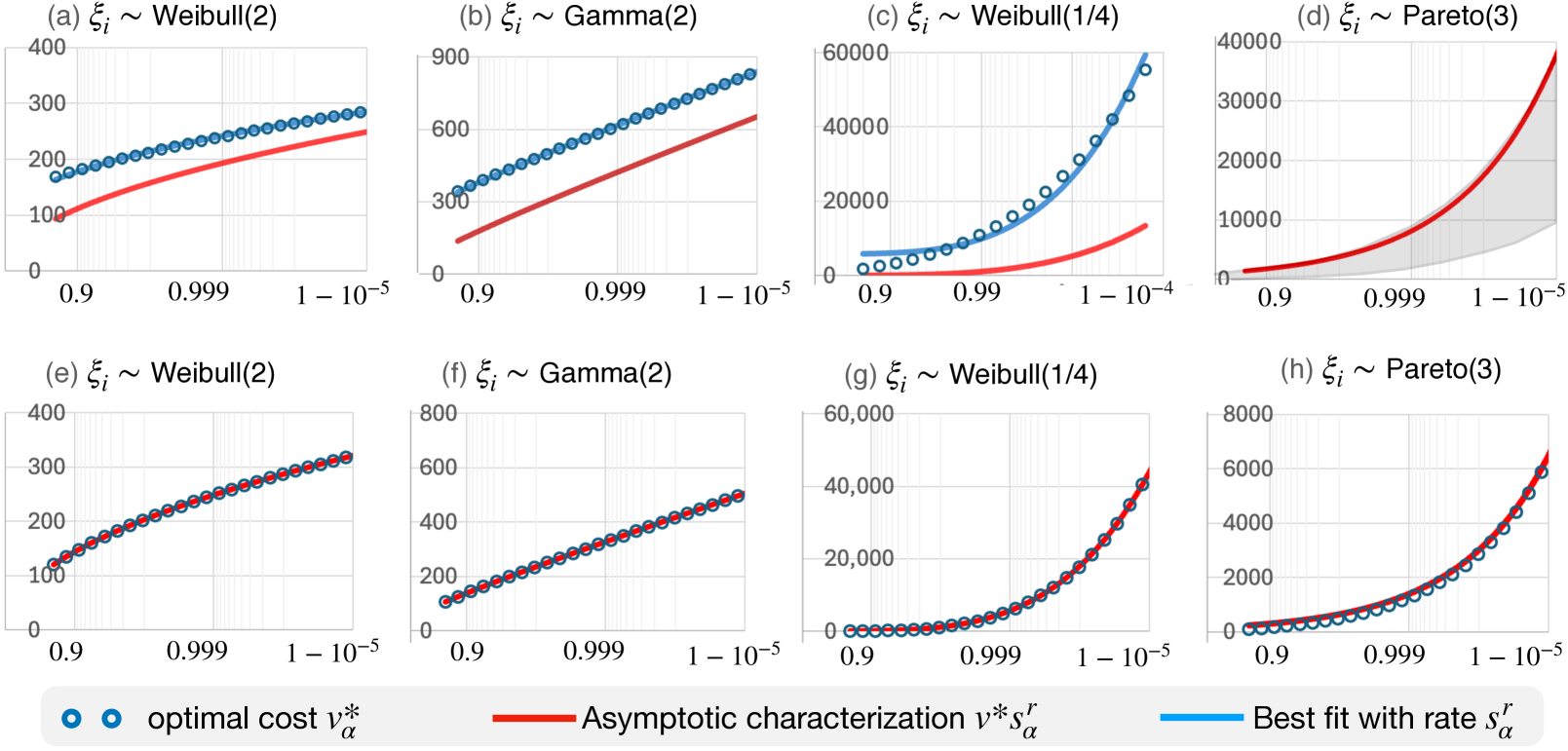

Numerical Illustration 1 (Scaling of optimal costs).

To quantitatively illustrate the scaling in Theorem 3.1, we consider the joint capacity sizing and transportation problem from Example 1 in a network with factories, distribution centers (DCs), and 100 edges. Each DC in the network is connected to a Factory only if or the cost incurred for transporting unit quantity in the respective edges are set by sampling uniformly at random from the intervals and The production cost parameters are drawn uniformly from the interval Demands for the commodity at the DCs are independent, with their expected values drawn uniformly from the interval

As in Example 1, we first consider the joint chance-constrained case where the decision-maker ensures that all DC demands are met with probability at least Figure 2 illustrates the optimal cost for different demand distributions, along with (i) the respective best-fitting functions with growth rate and (ii) the asymptotic characterization identified in Theorem 3.1.

The demand distributions in Panels (a)-(d) exhibit increasingly heavier tails from left to right and, correspondingly, the respective optimal costs are much larger in magnitude in the Panels (c)-(d). For example, if follows a Weibull distribution with shape parameter , then . Thus, the optimal cost grows more steeply for smaller . This trend is evident in Panels (a) and (c), where the observed cost growth aligns precisely with the identified rates and Panel (c) exhibiting a significantly faster growth of optimal costs compared to Panel (a). For Gamma-distributed demands with shape parameter 2 (Panel b), we have as . The optimal cost in Panel (b) reflects this, exhibiting linear growth when plotted on a log-scale. In Panel (d), the demands follow a Pareto distribution with for scale parameters . The corresponding scaling rate is , which matches the observed cost growth. Since solving the joint chance constraint problem exactly turns out to be intractable for this instance with common solvers, Panel (d) depicts a shaded region between upper and lower bounding individual chance constrained optimal values. Overall, we find that the scaling rate and the cost characterization effectively capture both the magnitude and growth trends under various distributions considered.

Furthermore, the gap between the optimal cost and its asymptotic counterpart narrows significantly when the decision maker is interested instead in individual chance constraints of the form for each DC This suggests that the observed gap in the joint chance constrained setting arises primarily from lower-order terms in the Bonferroni inequality, which are not captured in asymptotic analysis. While this gap may increase with larger in , the scaling rate remains accurate in characterizing the growth of both optimal decisions and costs, regardless of .

3.2.2. A discussion on the limiting constants

From Theorem 3.1, we find that the multiplicative constants in the relationships and are determined in by the joint distribution and the constraint functions , as informed via the limiting counterparts and in the assumptions. Although explicitly identifying the constraint function in and solving it to arrive at the limiting constants is not our focus, Proposition 3.3 below provides a characterization of which can be useful towards that end.

Proposition 3.3.

The constraint set in (13) is convex if is quasi-concave and is convex. The convexity of holds, for example, if the probability density satisfying the assumption is log-concave. Likewise, the constraint set in (13) can be written as a union of convex sets in the case of joint chance constraints with for quasi-concave functions Though not the focus of this paper, Proposition 3.3 may offer a new window into understanding the eventual convexity properties of chance constraints, which as a standalone topic, has been of great interest in the literature (see, e.g. van Ackooij, (2015), Van Ackooij & Malick, (2019) and references therein).

3.2.3. Impact of distribution mis-specification.

Regardless of how challenging it is to precisely compute the constants for a given setting, it is worthwhile to note that the asymptotic characterizations of the optimal value and solution depend on the target reliability level only via the scaling This highlights how the marginal distributions and the copula governing joint distributions decouple in influencing the scaling rate and the limiting constants respectively. As noted in Corollary 3.1 below, this decoupling has an interesting consequence on how mis-specifying the copula of leads to decisions which are expensive, at most, by a constant factor, even as the target reliability level is raised to 1. Mis-specifying the rate at which the marginal distributions decay, on the other hand, will distort the rate at which the resulting decisions scale. To formally state the former observation, let denote the collection of all joint distributions of for which the marginal CDF of is and the complementary CDF is for Additionally, let denote the optimal value of obtained by solving with a probability measure in place of

Corollary 3.1 (Impact of copula misspecification).

Under the assumptions in Theorem 3.1,

4. Application I: Characterizing the costs of distributional robustness

We devote this section towards examining the implications of Theorem 3.1 for the well-known Distributionally Robust Optimization (DRO) variants of the chance-constrained formulation

Given a collection of probability distributions defined on we consider the DRO formulation,

| (14) |

which seeks to identify an optimal decision whose probability of constraint violation continues to be smaller than when evaluated with any probability distribution in While chance-constrained DRO models of the form date back to Ghaoui et al., (2003), Erdoğan & Iyengar, (2005), Calafiore & Ghaoui, (2006), recent literature has witnessed a surge in their study primarily due to their ability to model and hedge against uncertainty or shifts in the underlying operational environment. Commonly used models for the distributional ambiguity set in chance-constrained setting include those specified using moment constraints (see, eg., Ghaoui et al., 2003, Natarajan et al., 2008, Hanasusanto et al., 2017), -divergence balls (see, eg., Jiang & Guan, 2016), or Wasserstein balls (see Xie, 2021, Ho-Nguyen et al., 2022, Chen et al., 2024). Please refer the survey article Küçükyavuz & Jiang, (2022) for a comprehensive account.

4.1. Scaling of costs under -divergence DRO

First we consider the well-known -divergence based distributional ambiguity set,

| (15) |

denotes the -divergence between and and the radius parameter captures the extent of distributional ambiguity.

Assumption 4.

The function specifying the -divergence in (15) is continuous, strictly convex, satisfies with its minimum attained at

Then, as a consequence of the characterizations in Theorem 3.1 above and the worst-case probability characterization in (Jiang & Guan, 2016, Theorem 1), we obtain Theorem 4.1 below on the scaling of optimal costs and decisions of Recall and define

| (16) |

Theorem 4.1 (Scaling of optimal value and solution for -divergence DRO).

Suppose that the constraint functions satisfy either Assumption 1 or 2 and Assumptions 3-4 hold. Further assume that the ambiguity set in is defined via the -divergence ball in (15), for some and a distribution satisfying either Assumption () or (). Then, as

-

a)

the optimal value of , call it satisfies where is the optimal value of the deterministic optimization problem in (10); and

-

b)

any optimal solution of call it satisfies where denotes the set of optimal solutions for If has a unique solution then

| -divergence | scaling rate | asymptotic for under | ||

|---|---|---|---|---|

| Assump. | Assump. | |||

| KL-divergence | ||||

| -divergence | ||||

| Polynomial | ||||

| divergences | ||||

Theorem 4.1 reveals that while the limiting multiplicative constants and in Theorems 3.1-4.1 are identical, the scaling rate arising with -divergence DRO can be substantially different from that of the baseline distribution Utilizing the definition of in (16), Table 1 below furnishes (i) the scaling rate arising in Theorem 4.1, and (ii) an asymptotic for the cost incurred by deploying -divergence DRO optimal decisions. To facilitate comparison, the latter is expressed in terms of the baseline scaling rate witnessed in Theorem 3.1. The constant in Table 1.

Suppose the parameter in Assumptions 1 or 2 is positive. Then the first striking observation from Table 1 is that the well-known KL-divergence DRO yields decisions which are exponentially more expensive than those of regardless of the radius To see this, recall that optimal cost for grows only at the rate as (see Thm. 3.1). As we shall see in the Numerical Illustration 2 below, the extreme conservativeness of KL-divergence DRO is observed even at not-so-stringent reliability levels, say, when is and the radius is taken as small as In contrast to DRO employing KL-divergences, we learn from Table 1 that DRO employing alternative divergence measures such as and polynomial divergences are conservative only by a constant factor in light-tailed settings. In the presence of heavy-tailed random variables however, they yield decisions which are more expensive by a factor growing polynomially in .

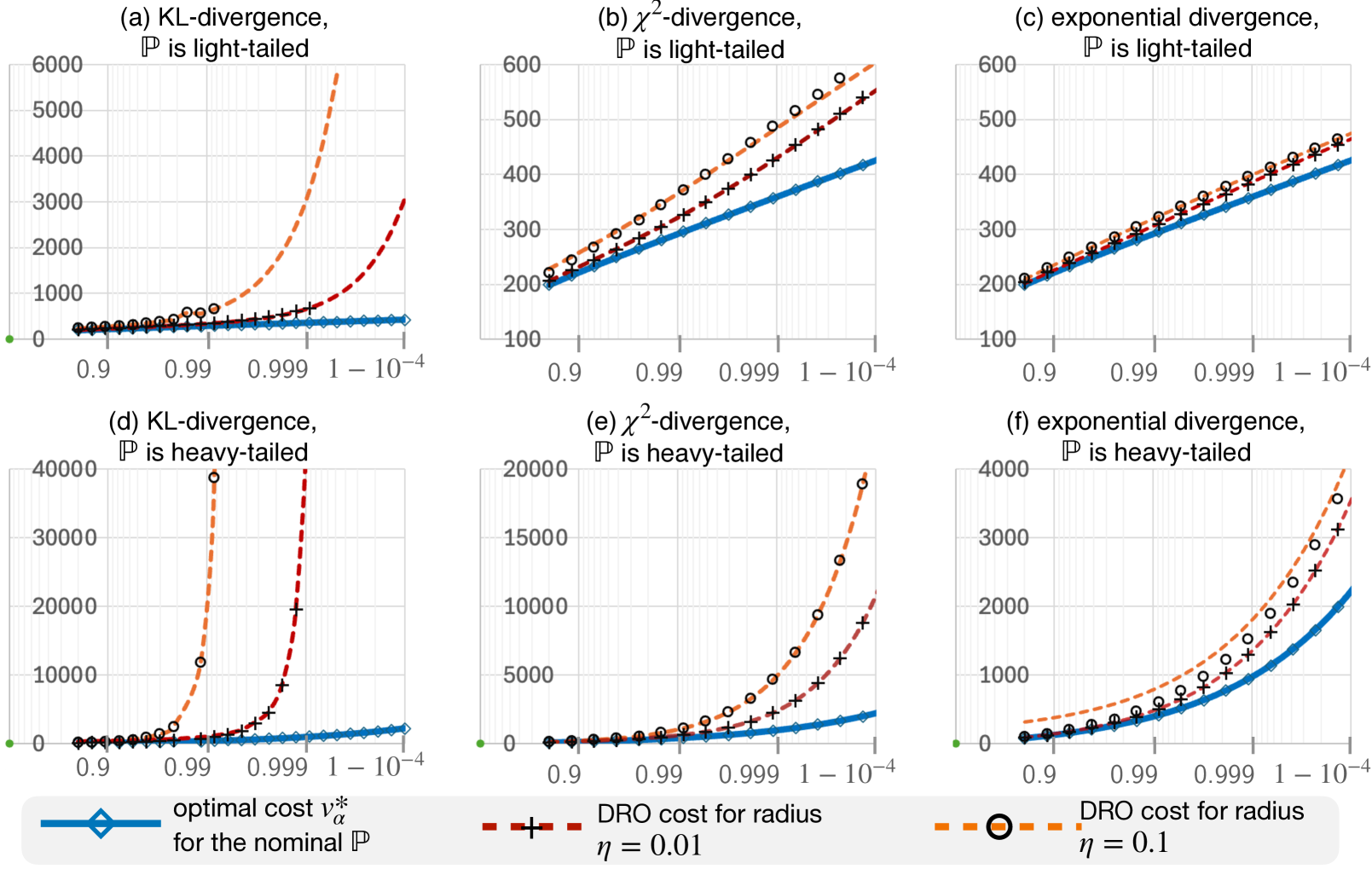

Numerical Illustration 2 (Scaling of DRO decisions).

Considering the same transportation problem setting in Numerical Illustration 1, we empirically explore in Figure 3 the impact of -divergence choice on the optimal decisions prescribed by the respective DRO formulations.

The markers in Fig 3 indicate the actual costs and the dashed lines illustrate the best fitting functions with rate predicted by Theorem 4.1. The exponentially high costs brought about by KL-divergence DRO decisions is immediately apparent from Panels (a) and (d): When is light-tailed, the KL-divegence formulation with radius results in decisions which are and more expensive when the reliability targets are set at 95% and 120% respectively (that is, when and ). The same formulation produces decisions which are, respectively, and more expensive when is heavy-tailed. Thus, KL-divergence DRO can be seen to yield prohivitively expensive decisions even at not so-stringent reliability targets.

DRO employing -divergence, on the other hand, produces decisions which, in Panels (b) and (e), grow at the same scaling rate when is light-tailed and at a polynomially faster rate when is heavy-tailed. Besides empirically illustrating the results in Table 1, Fig 3 brings out that the extent of conservativeness has a complex, often prohibitive, dependence on the target reliability level the radius and the tails of the baseline distribution under KL and -divergences.

In the right-most panels Panels (c) and (f), we take and examine the effect of exponentially growing on the cost of optimal decisions. This choice of is in contrast to the logarthmic growth for KL-divergence and for -divergence. For such an exponential divergence measure, we find in Panels (c) and (f) that the resulting decisions are conservative within the same orders of magnitude of the optimal costs of uniformly for all target reliability levels In particular, tuning the choice of radius allows one to fulfil its role as a knob controlling conservativeness, without letting the target reliability level and the tails of the baseline distribution render the resulting decisions unduly expensive.

The observations in Table 1, and Numerical Illustration 2 reinforce the extreme conservativeness of KL-divergence DRO observed in the specific example of quantile estimation in Blanchet et al., (2020), Birghila et al., (2021). Building on the empirical observation in Numerical Illustration 2, Proposition 4.1 below rigorously establishes the desirable scale-preserving nature of -divergences defined via growing exponentially in

Proposition 4.1.

Summarizing, Table 2 below precisely delineates the -divergence DRO formulations which preserve the scaling from those whose cost grow much faster than the nominal counterpart Please refer A.4 in the appendix for a proof for the properties in Table 2.

| Growth rate of as | |||

|---|---|---|---|

| satisfies | logarithmically growing | polynomially growing | exponentially growing |

| Assumption | No | SP | SP |

| Assumption | No | No | w-SP |

4.2. Distortion of scaling under Wasserstein DRO

Suppose that the ambiguity set in is given by

| (17) |

is the Wasserstein distance of order between any two probability measures supported on and is the collection of all joint distributions with marginals and . Let be an optimal solution of the resulting distributionally robust formulation.

Theorem 4.2 (Conservativeness of Wasserstein DRO).

Suppose that the constraint functions satisfy either Assumption 1 or 2 and Assumption 3 holds. Let the ambiguity set in be the Wasserstein ball in (17) for some and distribution satisfying either (i) Assumption () holds, or (ii) Assumption () holds with Then for any the cost of the optimal decision prescribed by denoted by satisfies

for all sufficiently small and some positive constant that does not depend on As a result, when satisfies Assumption and when satisfies Assumption

An immediate implication of Theorem 4.2 is that the decisions prescribed by Wasserstein DRO formulations are exponentially more expensive than its non-robust counterpart when is light-tailed and polynomially more expensive when is heavy-tailed. Intuitively speaking, this behavior arises because there always exist probability distributions within the distributional ambiguity set whose marginal tail distributions are as heavy as that of a Pareto (power law) distribution with tail parameter for any Thus, regardless of whether the baseline distribution is light-tailed or heavy-tailed, the cost of decisions prescribed by Wasserstein DRO grows at a drastically different rate from its non-robust counterpart as the target service level is raised to 1.

4.3. Scaling of optimal costs under inclusion of marginal distributions in

When equipped with the knowledge of marginal distributions of the random vector it is natural to define the distributional ambiguity set via recall that is the collection of all joint distributions of under which the CDF of equals for The use of ambiguity sets based on marginal distributions is well-known in the broader DRO literature: see Rachev & Rüschendorf, (2006b, a), Natarajan, (2021), Wang & Wang, (2016), Ennaji et al., (2024) and references therein for detailed accounts of its tractability and desirable properties in broader operations and risk management applications.

To describe the scaling of optimal decisions prescribed by marginal distributions based DRO formulations, define for any on the unit sphere Letting further define

Theorem 4.3 (Preservation of scaling under marginal distribution based DRO).

Suppose that the constraint functions satisfy either Assumption 1 or 2 and Assumption 3 holds. Let the ambiguity set in be where the marginal complementary CDFs for satisfy either Assumption () or (). Then, as

-

a)

the optimal value of , call it satisfies where is the optimal value of the deterministic optimization problem in which the constraint function is obtained by setting the specific choice of below in the definition of in (9):

-

b)

any optimal solution of call it satisfies where denotes the set of optimal solutions for the respective In particular, if has a unique solution then as

Corollary 4.1.

Consider any distributional ambiguity set contained in where the marginal complementary CDFs for satisfy either Assumption () or (). Then the resulting DRO formulation is scale-preserving in the sense that

Thus a modeler seeking to utilize marginal information, when available, in can arrive at a decision that is more expensive only by a constant factor irrespective of the target level While the use of marginals based ambiguity sets is well-known in the broader DRO literature (see, eg., Natarajan, 2021), its effectiveness in chance-constrained formulations compared to the more commonly used DRO counterparts is a relatively novel observation, albeit intuitive in light of the scaling rate depending fundamentally only on marginal distributions. Coincidentally, estimating marginal distributions of from data does not suffer from curse of dimensions unlike the estimation of joint distribution, which reinforces the effectiveness of marginals based DRO.

4.4. Distortion of scaling under moments-based DRO

Consider a mean-dispersion based distributional ambiguity set of the form

| (18) |

treated in Hanasusanto et al., (2017), where is the set of all Borel probability distributions on with a given mean vector and is an upper bound on the dispersion measure corresponding to a suitable dispersion function Here is a proper cone which depends on the dispersion measure chosen by the modeler, and the notation means The choice is related to the well-known Chebyshev ambiguity set constraining the mean and covariance of Indeed in this case, and is the cone of positive semidefinite matrices. For any other common choices of the dispersion function include (i) for which bounds the component-wise mean absolute deviations or its higher moment counterparts, (ii) the choice which bounds the component-wise upper and lower mean semi-deviations, (iii) among others. Please refer Ghaoui et al., (2003), Hanasusanto et al., (2017), Küçükyavuz & Jiang, (2022) and references therein for additional information on choices for dispersion function

Theorem 4.4 below provides a lower bound of the cost of an optimal decision prescribed by mean-dispersion based DRO formulations. For uniformity in notation, take if

Theorem 4.4 (Conservativeness of moment based DRO).

Suppose that the constraint functions satisfy either Assumption 1 or 2 and Assumption 3 holds. Let the collection in be the mean-dispersion distributional ambiguity set in (18), and the dispersion function is one among or defined above. Then for any the cost of the optimal decision prescribed by satisfies

for all sufficiently small and some positive constant depending on the problem instance. The conclusion remains the same even if

Thus, among the prominent DRO formulations we have considered in this section, we find only the marginal distribution based DRO to be scale-preserving unconditionally. Excluding this choice, we find -divergence DRO in which is growing at an exponential rate to be weakly scale-preserving unconditionally. Due to the express availability of tractable reformulations, we find this particular family of -divergence DRO formulations to be blending tractability with a desirable scale-preserving property which ensures that the optimal decisions produced by the DRO formulation are not unduly conservative.

5. Application II: Quantifying & reducing the conservativeness of safe approximations

Inner approximations to chance constraints, based on Conditional Value at Risk (CVaR) and Bonferroni inequality, have served as prominent vehicles for tackling the computational challenges in solving . In this section, we demonstrate how the scaling machinery developed in this paper leads to a thoroughly novel approach for quantifying and reducing the conservativeness of these popular inner approximations of

5.1. CVaR-based inner approximations

We begin by recalling the definition of CVaR: For any random variable its CVaR at level is defined as is the -th quantile of If a constraint function is convex in , then retains the convexity (Rockafellar et al., 2000). In this case, it is well-known that the constraint serves as the tightest convex inner approximation to the chance constraint see, example, Nemirovski & Shapiro, (2007).

For the generic formulation in (1), one may similarly consider the following inner approximation (see Chen et al., 2010):

| (19) |

where are positive constants. Indeed in this case, when a decision satisfies the constraints in (19), and hence This, in turn, is equivalent to the probability constraint in as are positive constants. Consequently, any solution to (19) satisfies the probability constraint in and hence can be considered to be prescribing “safe” decisions. Though the constants may seem superfluous, the flexibility of tuning these parameters has been found to be helpful in improving the quality of subsequent approximations: see Chen et al., (2010), Zymler et al., (2011). The variational representation of CVaR due to Rockafellar & Uryasev, (2002) renders the following to be a computationally attractive way of rewriting the formulation in (19):

As CVaR-based approximations involve computation of expectations, they may become vacuous if the constraint functions are extended real-valued and can take with positive probability. To avoid this, it is natural to restrict the constraint functions to be real-valued and work with an assumption slightly less general than the epigraphical convergence in Assumption 2.

Assumption 5.

There exist constants and a function such that the following are satisfied:

-

i)

for any and we have

-

ii)

for any sequence and

-

iii)

the set-valued map defined by is non-vacuous for the support and the decision set

Theorem 5.1 (Scaling of the optimal value and solution of CVaR approximation).

Suppose Assumption 3, Assumption 5, and either Assumption () or () hold. Let and denote, respectively, the optimal value and an optimal solution to the CVaR approximation in (19). Further assume that Then, as

-

a)

the optimal value satisfies where and is the optimal value of the deterministic optimization problem in (10);

-

b)

any optimal solution satisfies where denotes the set of optimal solutions for In particular, if has a unique solution then

-

c)

the conservativeness of the CVaR approximation relative to for all values of sufficiently small, is thus essentially determined by the constant which is given by,

Theorem 5.1 reveals that the extent of conservativeness introduced by CVaR-based approximations remains bounded, irrespective of the target reliability level Notably, the conservativeness is determined fundamentally by the heaviness of the tails of the distribution of and is larger for heavier-tailed random variables. In particular, the gap in approximation is inversely proportional to when the distribution of has polynomially decaying heavy-tails, such as, as Conversely, for light-tailed distributions meeting Assumption , two key observations emerge: (i) the conservativeness vanishes, and (ii) the solutions of the CVaR approximation and the target solution of the formulation coincide asymptotically.

Under both Assumptions and we have componentwise, where is optimal for the original formulation (1). Refer the Panels (c) and (f) in Figure 4 for an empirical demonstration of this finding. As we shall see in Section 5.3, this property can be used to develop an elementary algorithm capable of improving into a nearly optimal solution for

5.2. Inner approximations based on Bonferroni inequality

As joint constraints are computationally more challenging than individual chance constraints, Bonferroni inequality has served as an intuitive and popular approach towards breaking up multiple constraints, such as in (1), into individual probability constraints as below: For any positive constants satisfying consider

| (20) |

Indeed, for any satisfying the individual probability constraints in (20), we have due to the Bonferroni’s inequality. Consequently, any solution to (20) in turn satisfies the probability constraint in

Theorem 5.2 (Scaling for Bonferroni inequality based approximation).

Suppose Assumption 3, Assumption 5, and either Assumption () or () hold. Let and denote, respectively, the optimal value and an optimal solution to the Bonferroni inequality based approximation in (20). Then the following hold as :

-

a)

Under Assumption the optimal value and any optimal solution satisfy and where and are the optimal value and optimal solutions of the deterministic optimization problem in (10);

-

b)

Under Assumption the optimal value and any optimal solution satisfy and where and are the optimal value and optimal solutions of

(21) with

Theorem 5.2 reveals that the inner approximation based on Bonferroni inequality features the same scaling as . Hence the extent of conservativeness introduced by the formulation (20) remains bounded even as the problem becomes more challenging with the target level approaching 1. Similar to CVaR approximation, the conservativeness of (20) vanishes if the distribution of is light-tailed and the resulting solution coincides with a target solution of the formulation asymptotically. However, in the case of heavy-tailed distributions, the limiting deterministic optimization problem in (21) does not match with (10). In particular, note that the constraint sets and are of very different nature even when we set Hence one cannot expect the solution to be proximal to the scaled solution set which was a nice feature of CVaR-based inner approximations that cannot be guaranteed with Bonferroni inequality based inner approximations.

5.3. A line-search procedure to obtain asymptotically optimal solutions for

Consider a target reliability level and a solution obtained by solving either the CVaR-based inner approximation in (19) or the Bonferroni inequality based inner approximation in (20). Assuming the ability to evaluate the probability of constraint violation at any Algorithm 1 below outlines an elementary line search procedure which returns a strictly improved feasible solution to This strict improvement is guaranteed by the observations in Lemma 5.1 below.

Lemma 5.1.

Suppose is a cone and is continuous. Then under the assumptions of Thm. 5.1,

-

a)

the cost of the decisions parameterized by is strictly increasing in

-

b)

the decision is feasible for for any where

-

c)

we have and consequently for the assignment

Despite the simplicity of the line-search in Algorithm 1, Proposition 5.1 below demonstrates that the improved solution returned by Algorithm 1 is asymptotically optimal for . In Proposition 5.1 below, recall that denotes the optimal value of in (1).

Proposition 5.1.

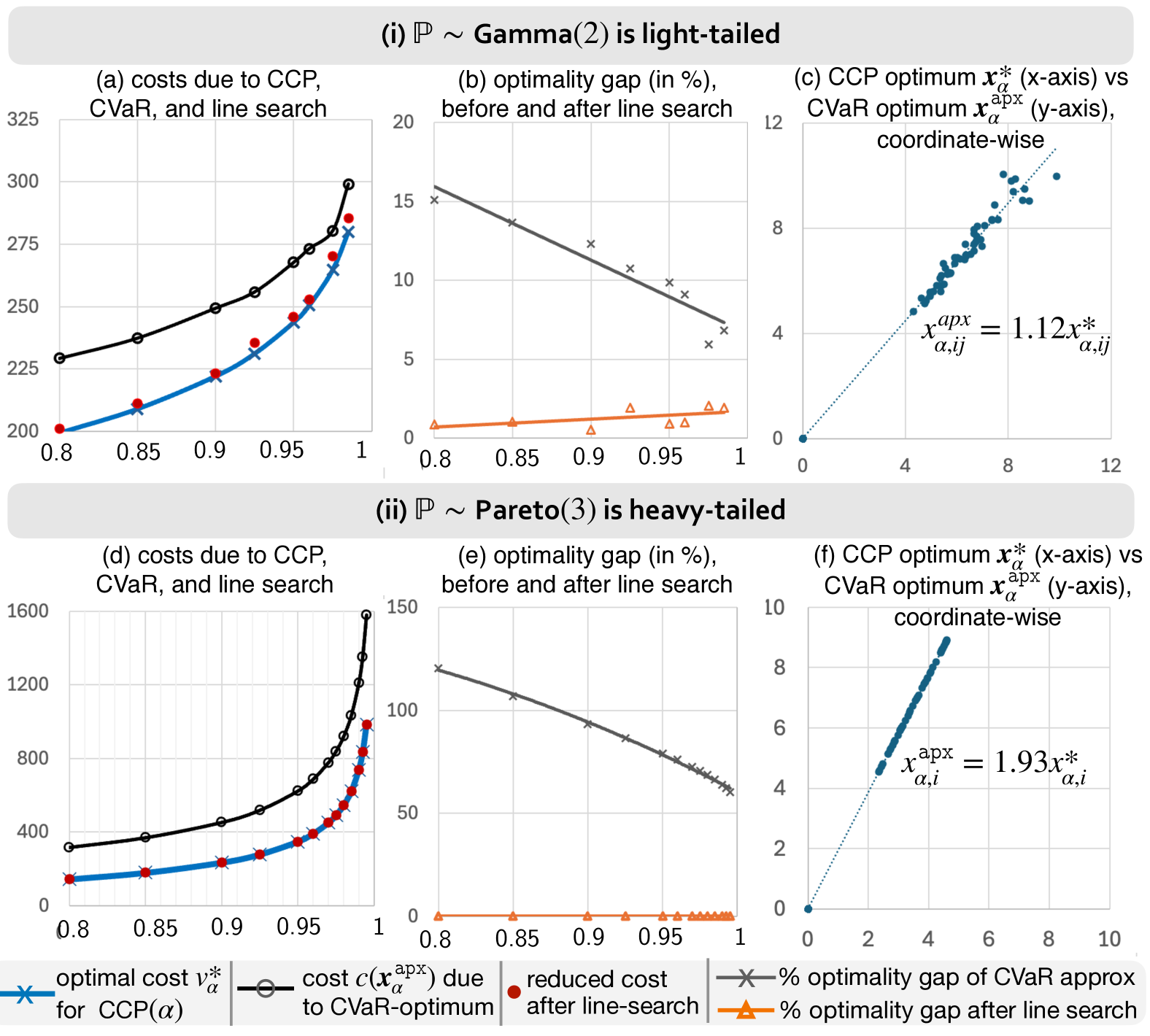

Numerical Illustration 3 (Effectiveness of Algorithm 1).

Considering the same transportation example in Numerical Illustration 1, we compare in Figures 4(a) and 4(d) the following optimal costs at various target levels : (i) the cost due to the optimal solution of (ii) the cost due to the CVaR inner approximation (19) obtained by setting for and (iii) the cost due to the solution returned by the line search in Algorithm 1.

Besides illustrating the near-optimality of pictorially in Panels (a) and (d), we find from Panels (b) and (e) that the optimality gap gets reduced by as much as 50 to 120 percentage points in the heavy-tailed setting and 5 - 15 percentage points in the light-tailed setting. Panels (c) and (f) illustrate the reason behind the effectiveness of the line search: As predicted by Theorem 5.1, we see that component-wise, which is brought about vividly by the scatter plots between the components of the solutions output by and its respective CVaR inner approximation.

At a conceptual level, the near-optimality of the line search in Algorithm 1 is primarily due to the observation that componentwise, where and is a solution to in (1). As a result, conducting a line search for a less-expensive feasible solution along the ray passing through turns out to be sufficient for obtaining a solution with vanishing relative optimality gap even though may be sub-optimal by a constant factor.

6. Application III: Estimation of Pareto-efficient solutions from limited data

In this section, we use the scaling in Theorem 3.1 as the basis to develop a novel semiparametric method for estimating approximately Pareto-optimal decisions from limited data.

6.1. The estimation barrier in handling constraint violation probabilities

In practice, the underlying probability distribution with which the problem of interest, in (1), should be solved is seldom known and is informed only by independent realizations from In this case, one of the most basic approaches towards solving is to approximate the probability of constraint violation in (1) via its average computed from the samples as below:

| (22) |

See example, Ahmed & Shapiro, (2008), Pagnoncelli et al., (2009b) for the considerations pertinent to approximating with this Sample Average Approximation (SAA) approach. Recalling the notation we have the following due to Chebyshev’s inequality:

| (23) |

Hence, we need at least samples in order to well-approximate the constraint violation probability at a boundary point satisfying with at least confidence. Similar sample requirement arises with the well-known scenario approximation approach as well, see Calafiore & Campi, (2006). Consequently, both SAA and scenario approximation approaches are well-suited for solving only when the number of available samples and the considered constraint violation probability level are such that is not small. Conversely, if as constraint violations are rarely observed in-sample, leading to hazardous underestimation of the probability of constraint violation.

Numerical Illustration 4.

Here we consider the joint capacity sizing and transportation example in Numerical Illustration 1 with distribution centers. Taking independent observations of the demands realized at the 30 distribution centers as our dataset, we first illustrate the properties of the SAA optimal solutions obtained by solving at different target reliability levels The out-of-sample reliability levels met by the SAA solutions for the joint chance-constrained formulation and their respective costs are presented for the case of independent light-tailed Gamma(2) distributed demands in Figure 5 and Table 3 below. Corresponding results for the individual chance-constrained heavy-tailed counterparts are presented in Figure 1 in the Introduction and Table 3. The costs and constraint violation probabilities are reported together with their respective 95% confidence intervals computed from 32 independent experiments.

From Panels (a) of both Figures 1 and 5, we observe that the SAA optimal solutions fall significantly short when the target reliability level is such that The shortfall is severely more pronounced when as typically zero samples fall in the constraint violation regions for the identified SAA optimal decisions. Insufficient in-sample constraint violations often leads the SAA to incorrectly conclude a decision whose to be feasible, even though it patently violates the requirement . As a result, we see from Panels (a)-(b) of Figures 1 and 5 that the cost and reliability offered by SAA solutions taper and do not improve for This example serves to illustrate why SAA cannot be relied upon to yield a decision satisfying

| is light-tailed | is heavy-tailed | |||

|---|---|---|---|---|

| Target | ||||

| 0.8 | 0.733 0.005 | 100.720 0.422 | 0.772 0.003 | 44.184 0.170 |

| 0.85 | 0.787 0.004 | 105.687 0.484 | 0.826 0.002 | 54.923 0.172 |

| 0.9 | 0.843 0.004 | 112.072 0.591 | 0.878 0.002 | 71.831 0.241 |

| 0.95 | 0.900 0.004 | 121.650 0.815 | 0.933 0.002 | 106.432 0.451 |

| 0.975 | 0.932 0.003 | 129.775 1.023 | 0.963 0.001 | 149.790 0.970 |

| 0.99 | 0.953 0.003 | 138.345 1.307 | 0.981 0.001 | 223.545 1.529 |

| 0.961 0.002 | 143.199 1.456 | 0.988 0.0007 | 294.528 3.710 | |

| 0.968 0.002 | 149.483 1.601 | 0.994 0.0005 | 503.952 15.540 | |

| 0.970 0.002 | 152.612 1.685 | 0.996 0.0005 | 648.958 34.310 | |

| 0.970 0.002 | 152.612 1.685 | 0.995 0.0005 | 764.963 53.252 | |

| 0.970 0.002 | 152.612 1.685 | 0.996 0.0005 | 779.464 55.678 | |

| 0.970 0.002 | 152.612 1.685 | 0.996 0.0005 | 791.064 57.624 | |

The statistical bottleneck demonstrated in Numerical Illustration 3 is acute in applications requiring very high levels of reliability, such as power distribution and telecommunication networks (where , regulatory risk management (where ), etc. Due to the low tolerance for constraint violation (specified via small ) in these settings, obtaining sufficient number of representative samples to ensure becomes often an impossible proposition unless additional parametric distributional assumptions are made. The need for effective data-driven algorithms that perform well even when the target has been widely acknowledged, particularly in the example of quantile estimation. Note that estimating quantile of a random variable at a level can, in fact, be seen as one of the simplest instances of via its definition

| (24) |

The field of Extreme Value Theory (EVT) in Statistics (see, eg., De Haan & Ferreira, 2007, Resnick, 2013) has bridged this critical need in the particular context of estimation of quantiles when is small, corresponding to levels far beyond those captured via the empirical distribution from the data samples.

6.2. Basis for extrapolation of solution trajectories inspired from EVT

The central ingredient in extreme value theory (EVT) which enables estimation of quantile at levels is a limiting characterization of the form,

| (25) |

akin to (11), which allows the extrapolation of extreme tail quantile from an intermediate quantile which is observed sufficiently in the available data; see (De Haan & Ferreira, 2007, Thm. 1.1.6). Here is a positive constant, is a scaling function depending on the underlying distribution, and one takes to facilitate an extrapolation via (25). The enduring appeal of this extrapolation, revolving around the limiting relationship (25), stems from the fact it does not require the modeler to make parametric assumptions about distribution tail regions which are not sufficiently witnessed in data. Its practical effectiveness and minimally assuming semiparametric nature have made this approach a cornerstone for estimating quantiles in diverse engineering and scientific disciplines.

Momentarily viewing our chance-constrained formulation as a sophisticated generalization of the quantile estimation task in (24), we propose to utilize the following consequence of Theorem 3.1 in a similar way the limiting relationship (25) has powered quantile extrapolation in EVT. In particular, Proposition 6.1 below serves as the counterpart of (25) that allows direct data-driven estimation of solutions at constraint violation probability levels far below without requiring the modeler to make parametric assumptions on the distribution of To state Proposition 6.1, let denote the optimal solution set of at any

Proposition 6.1.

Suppose the assumptions in Theorem 3.1 are satisfied. Suppose also that is singleton.Then for any we obtain

as .

Suppose, for a moment, we have access to an optimal solution obtained by solving at an appropriate base constraint violation probability level Then Proposition 6.1 brings out a desirable property of the extrapolated trajectory of decisions, for constructed from the optimal solution at the base level. In particular, Proposition 6.1 asserts that such an extrapolated trajectory gets vanishingly close, in a relative sense, point-wise to the trajectory of optimal solution sets in the case of light-tailed distributions and in the case of heavy-tailed distributions. Thus, even when is such that is small and constraint violations at that level are observed insufficiently in the dataset as a consequence, the extrapolated trajectory and Proposition 6.1 can be seen as empowering us with a pathway for approximating the solutions of to which have no access otherwise in the statistically challenging setting where .

6.3. Estimation of weakly Pareto-efficient solutions which breach the barrier

Given a dataset comprising i.i.d. samples of consider the trajectory,

| (26) |

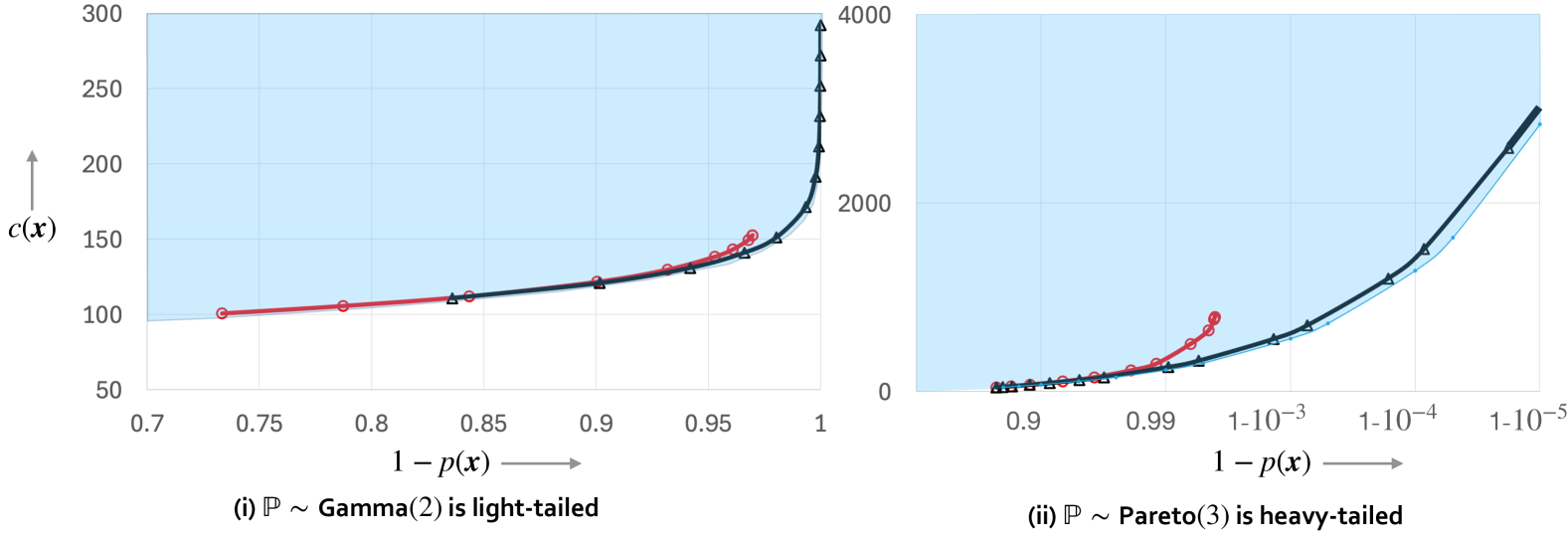

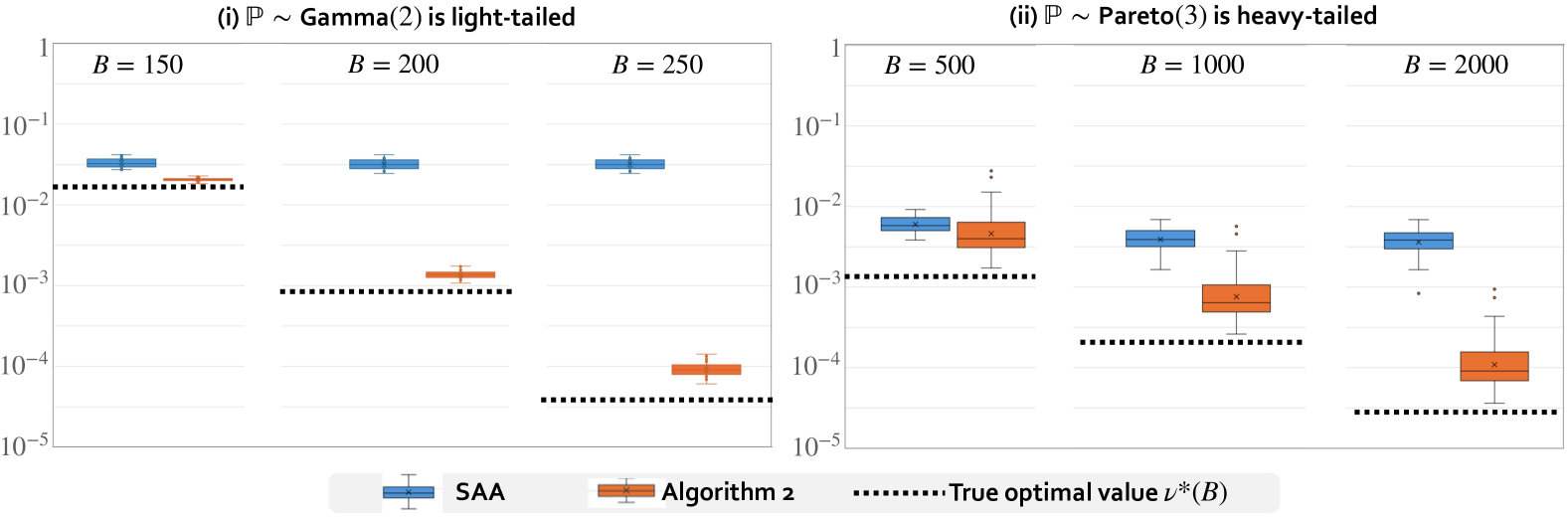

where is an optimal solution estimate obtained either from the sample average approximation (or) the scenario approximation of constructed using the dataset For the base SAA solution to be accurate, it is necessary from the application of Chebyshev’s inequality in (23) that as With defined in (26) serving as the key construct enabling estimation of approximately Pareto optimal decisions, we first empirically bring out its properties in Numerical Illustration 3 below before proceeding to its theoretical properties in Theorem 6.1 and the following Section 6.4.

Numerical Illustration 3 continued. Taking the base constraint violation probability level Figure 6 and Table 4 below present the trajectory of (out-of-sample constraint satisfaction probability cost ) pairings traced by the decisions Unlike the tapering of constraint satisfaction probabilities and costs observed with SAA in Table 3 and Figure 1, we observe from Figure 6 that the extrapolated trajectory is able to produce decisions whose constraint satisfaction probabilities can be significantly larger than the empirically observed barriers of in the light-tailed joint chance-constrained setting and in the heavy-tailed individual chance-constrained setting. In particular, even when equipped with only samples, the trajectory is able to produce decisions whose constraint violation probabilities can be as small as or even smaller when larger values of are used. We also observe that the associated confidence intervals in Table 4 to be significantly narrower than those reported for SAA in Table 3. More interestingly in Figure 6, the extrapolated decisions in offer reliability, cost pairings that lie close to the efficient frontier capturing the best possible (reliability, cost) pairings attainable for the problem.

| is light-tailed | is heavy-tailed | ||||

|---|---|---|---|---|---|

| 1.0 | 0.733 0.005 | 100.720 0.422 | 1.0 | 0.772 0.003 | 44.184 0.170 |

| 1.1 | 0.836 0.003 | 110.792 0.465 | 1.1 | 0.797 0.003 | 48.631 0.189 |

| 1.2 | 0.902 0.002 | 120.864 0.506 | 1.3 | 0.829 0.002 | 55.669 0.217 |

| 1.3 | 0.942 0.002 | 130.936 0.549 | 1.6 | 0.877 0.002 | 70.139 0.273 |

| 1.4 | 0.966 0.001 | 141.008 0.591 | 2.0 | 0.915 0.001 | 88.369 0.344 |

| 1.5 | 0.980 0.0006 | 151.080 0.634 | 2.7 | 0.951 0.001 | 119.936 0.467 |

| 1.7 | 0.993 0.0003 | 171.224 0.718 | 3.4 | 0.969 0.0006 | 151.109 0.589 |

| 1.9 | 0.998 0.0001 | 191.368 0.803 | 5.9 | 0.991 0.0002 | 258.393 1.006 |

| 2.1 | 0.00004 | 211.512 0.887 | 7.4 | 0.995 0.0001 | 325.555 1.268 |

| 2.3 | 0.00002 | 231.656 0.972 | 12.6 | 0.999 0.00003 | 556.691 2.168 |

| 2.5 | 0.000007 | 251.800 1.056 | 15.9 | 0.00002 | 701.387 2.732 |

| 2.7 | 0.000003 | 271.944 1.141 | 27.1 | 0.000005 | 1199.355 4.671 |

| 2.9 | 0.000001 | 292.088 1.225 | 34.2 | 0.000002 | 1511.092 5.886 |

Numerical Illustration 3 empirically demonstrates the ability of the trajectory to produce approximately Pareto optimal decisions whose reliability levels can be significantly smaller than the barrier. This empirically observation can be quite surprising when viewed from the following standpoint: If note that it is statistically impossible to even just verify the hypothesis that , when one is, say, presented with a decision satisfying Theorem 6.1 and Corollary 6.1 below examine the above intriguing empirical observation on approximate Pareto optimality and argue that it is not a coincidence: In particular, Theorem 6.1 below and Corollary 6.1 and the following section establish the weak Pareto efficiency of the solutions traced by the trajectory and its optimality for the well-known -model (see Charnes & Cooper, 1963, He et al., 2019).

Definition 3 (Weak Pareto efficiency).

A sequence of decisions is weakly Pareto efficient in balancing the cost and constraint violation probability if, for any given there exists and such that the following holds for all :

| (27) |