Scalable Fitting Methods for Multivariate Gaussian Additive Models with Covariate-dependent Covariance Matrices

Scalable Fitting Methods for Multivariate Gaussian Additive Models with Covariate-dependent Covariance Matrices

Abstract

We propose efficient computational methods to fit multivariate Gaussian additive models, where the mean vector and the covariance matrix are allowed to vary with covariates, in an empirical Bayes framework. To guarantee the positive-definiteness of the covariance matrix, we model the elements of an unconstrained parametrisation matrix, focussing particularly on the modified Cholesky decomposition and the matrix logarithm. A key computational challenge arises from the fact that, for the model class considered here, the number of parameters increases quadratically with the dimension of the response vector. Hence, here we discuss how to achieve fast computation and low memory footprint in moderately high dimensions, by exploiting parsimonious model structures, sparse derivative systems and by employing block-oriented computational methods. Methods for building and fitting multivariate Gaussian additive models are provided by the SCM R package, available at https://github.com/VinGioia90/SCM, while the code for reproducing the results in this paper is available at https://github.com/VinGioia90/SACM.

Keywords: Multivariate Gaussian Regression; Generalized Additive Models; Modified Cholesky Decomposition; Matrix Logarithm; Dynamic Covariance Matrices; Smoothing Splines.

1 Introduction

This paper proposes computationally efficient methods for fitting multivariate Gaussian regression models in which both the mean vector, , and the covariance matrix, , are allowed to vary with the covariates via additive models, based on spline basis expansions. A key challenge in this context is to ensure the positive definiteness of , which is achieved here by modelling the elements of an unconstrained parametrisation matrix, . While several alternative parametrisations are discussed in pinheiro1996, we focus on the matrix logarithm (logM) of (chiu1996) and the modified Cholesky decomposition (MCD) of (pourahmadi1999), which are widely used in applications.

Model fitting is performed in an empirical Bayesian framework, where maximum a posteriori (MAP) estimates of the regression coefficient are obtained via Newton optimisation methods as in wood2016, while prior hyperparameters are selected by maximising a Laplace approximation to the marginal likelihood (LAML) via the generalised Fellner-Schall (FS) iteration of woodfasiolo2017. Such methods require the first- and second-order derivatives of the log-likelihood w.r.t. the elements of and , hence the first contribution of this work is to provide efficient methods for evaluating them. In particular, we show that this can be achieved by exploiting sparsity, in the MCD case, and, under the logM model, by developing highly optimised derivative expressions. Note that the latter are more efficient than those provided by chiu1996 and are useful beyond the additive modelling context considered here. For example, the optimisation and sampling methods used by kawakatsu2006matrix and ishihara2016matrix to fit, respectively, GARCH and multivariate volatility models, require evaluating the derivatives of the logM parametrisation. The derivatives of the logM parametrisation are also used to fit the multivariate covariance GLMs via the software package discussed in bonat2018 and to aid model interpretability in the multivariate volatility models considered by bauer2011forecasting. Interestingly, Deng2013 proposed methods to fit logM-based covariance matrix models by maximum penalised likelihood methods, but avoided derivative computation by approximating the log-likelihood.

The only model-specific input of the fitting framework outlined above are the derivatives of the log-likelihood w.r.t. the response distributions parameters (here and ) so, in principle, no further modification is needed to fit the models considered here. However, given that the number of elements of grows quadratically with the dimension of the response vectors and that each element can be modelled via linear predictors containing several regression coefficients, the memory requirement can be substantial even for moderate . Hence, the second contribution of this paper is to propose a block-oriented computational framework that limits memory requirements, while not affecting the leading cost of computation. We also show how to further speed up computation in cases where many linear predictors are left unmodelled, with a realistic example of such scenarios being provided in the application to electricity load modelling considered here.

As discussed in woodfasiolo2017, the FS update is guaranteed to maximise the LAML only under linear-Gaussian models, which is not the case here due to the non-linear relation between and . Hence, the third contribution of this work is to consider an “exact” version of the FS update, which is guaranteed to provide an ascent direction on the LAML objective. Further, we provide methods for efficiently computing the update that are applicable to any non-linear or non-Gaussian additive model.

At the time of writing, we are not aware of other work focussing on the computational challenges that must be addressed when fitting regression models based on either the MCD or the logM parametrisation. However, the models considered here are closely related to the MCD-based multivariate Gaussian models considered by muschinski2024 and to the regression copula models of klein2025bayesian, which exploit the logM parametrisation for correlation matrices proposed by archakov2021. In the former, the covariance matrix is allowed to vary with covariates, as is the case in the unconstrained models considered by tastu2015space and bonat2016. Related models are also the fixed covariance, MCD-based regression models of cottet2003bayesian and the multivariate functional additive mixed models of volkmann2023multivariate.

The rest of the paper is structured as follows. In Section 2 we describe the model class considered here and the proposed fitting framework. In Section 3 we explain how to efficiently compute the log-likelihood derivative w.r.t. the elements of and under the MCD and logM parametrisations, comparing the proposed methods with automatic differentiation and assessing the relative performance of models based on either parametrisation. We discuss methods for limiting memory usage and for efficiently computing the exact FS update in, respectively, Section 4 and 5, while in Section 6 we consider an application to probabilistic electricity demand modelling.

2 Multivariate Gaussian Additive Models

This section defines additive mean and covariance matrix models, and details the corresponding fitting methods. Henceforth, is the vector-to-matrix diagonal operator, while and denote the trace and the determinant of a matrix , respectively.

2.1 Model Structure

Consider -dimensional, independent random vectors , , normally distributed with mean vector and covariance matrix , that is . Let be the matrix of linear predictors, where is the number of distributional parameters controlling the mean and covariance matrix, and indicate its -th row and -th column with, respectively, and . The mean vector is modelled via , , while , , model the unconstrained entries of a covariance matrix reparametrisation. By omitting the subscript , the latter can be formalised via a symmetric parametrisation matrix

| (1) |

The elements of are related to specific entries of the logM- and MCD-based covariance matrix regression models, as will be clarified in Section 3. Although such models can be defined without introducing , using this auxiliary matrix eases the notation.

In an additive modelling context, the elements of are modelled by

| (2) |

where the ’s can be linear or smooth effects of , that is the -th element of an -dimensional vector of covariates . However, the r.h.s. of (2) can be straightforwardly generalised beyond univariate effects. Assume that the smooth functions appearing in (2) are built using linear spline basis expansions, so that the linear predictors can be expressed as , , where is an model matrix and includes the regression coefficients of both linear and smooth effects. Let be the -dimensional vector of coefficients belonging to all the linear predictors. To avoid overfitting, assume that the effects’ complexity is controlled via an improper Gaussian prior, under which . Here is a Moore-Penrose pseudoinverse of , where is the vector of positive smoothing parameters, controlling the prior precision, and the ’s are positive semi-definite matrices. See Wood2017 for a detailed introduction to smoothing spline bases and penalties.

2.2 Model Fitting

Let be the posterior distribution of , conditional on . In this work, we consider maximum a posteriori (MAP) estimation of , that is

| (3) |

, with the -th log-likelihood contribution, and the prior log density. To do so, we use Newton’s algorithm, which requires the gradient and Hessian of w.r.t. . These are respectively

where and . Gradient and Hessian are formed by blocks depending on the parametrisation-specific log-likelihood derivatives w.r.t. , that is

| (4) |

where and . For fixed , the efficient computation of the log-likelihood derivatives w.r.t. is essential for fast model fitting. Hence, Section 3 focuses on computing and efficiently for both logM- and MCD-based models, while Section 4 proposes a bounded-memory strategy to compute the Hessian blocks .

However, the real challenge when fitting the GAMs is selecting the smoothing parameters. Here, we select by maximising a Laplace approximation to the marginal log-likelihood (LAML), , that is

| (5) |

where is the dimension of the null space of , is the product of its positive eigenvalues, is the maximiser of , and evaluated at . To maximise efficiently, we consider the generalised Fellner-Schall iteration proposed by woodfasiolo2017. This starts by considering the first derivatives of w.r.t.

| (6) |

for , where , , and with terms and being defined accordingly. woodfasiolo2017 show that , provided that is positive semi-definite (if it is not, then an appropriately perturbed or expected version can be used instead). Under the further assumption that , it is easy to see that the update (henceforth the Fellner-Schall update, FS) will increase (decrease) when (), thus providing a LAML ascent direction.

From a computational perspective, the FS update is attractive because it avoids the computation of the term which, as explained in Section 5, requires the third-order derivatives of the log-likelihood w.r.t. . However, the assumption does not hold under any of the models considered here, hence the FS iteration is not guaranteed to reach the LAML maximiser. Nonetheless, under the logM parametrisation the third derivatives are expensive to compute, hence the FS update is the most attractive option for scalable computation. Instead, under the MCD parametrisation such derivatives can be computed cheaply, which enables the adoption of the following iteration (Wood25GAM)

| (7) |

We call such update the “exact” FS (EFS) update because its direction agrees with the sign of the corresponding LAML gradient element, while avoiding the assumption.

The next section focusses on the efficient computation of the log-likelihood derivatives w.r.t. , under either the logM or MCD parametrisation.

3 Efficient Computation of Parametrisation-Specific log-Likelihood Derivatives

If we define , then the -th log-likelihood contribution is

| (8) |

up to an additive constant. In the following, we omit the subscript to lighten the notation (e.g., is simply ) and denote the Hadamard product with , while and represent, respectively, the -th row and the -th column of a matrix .

3.1 Log-Likelihood Derivatives under the logM Parametrisation

chiu1996 consider an unconstrained parametrisation matrix defined by , where is the matrix exponential such that, if is the eigendecomposition of , then . Hence, is the matrix logarithm of , and the positive-definiteness of the latter is guaranteed. Given that , the log-likelihood given in (8) is now

| (9) |

where and . Although the cost of evaluating the log-likelihood by eigen-decomposing is , the main bottleneck during model fitting is the computation of the log-likelihood derivatives w.r.t. (i.e., the elements of ), which are required by the methods described in Section 2.2.

To the best of our knowledge, analytic expressions for such derivatives can be obtained in two main ways. The first relies on the chain rule for the matrix exponential (see e.g. mathias1996chain), where the derivatives are obtained as functions of augmented matrices. This approach requires computing the exponential of block-triangular matrices via a scaling and squaring algorithm based on a Padé approximation (see e.g. higham2008functions, Section 10.3), which is expensive. For example, obtaining , for , involves building a matrix and then computing its matrix exponential. The second approach involves expressing the directional derivatives of the matrix exponential via an integral and solving it using the spectral decomposition (see e.g. najfeld1995). This is the approach taken by chiu1996, which we improve below to obtain derivative expressions that are much more computationally efficient.

Let and be two lower triangular matrices such that and . Denoting with the row-wise half-vectorisation operator, that is , we define and . Then, log-likelihood gradient, , is

| (10) | ||||

| (11) | ||||

| (12) |

where with and is a matrix such that and , with . See SM A.2 for the derivation of (10 - 12).

Remark 1.

Computing , for , requires two matrix-vector multiplications, while computing , for , requires computing , which is of order , and then simply accessing its elements. Hence, the total cost is , which is of the same order as computing the log-likelihood itself by eigen-decomposing . In contrast, the first-order derivative formulas provided by chiu1996, have an cost because they involve computing, for each of the elements of the gradient, a sum over terms (see formulas (16) and (A.1) therein).

The first rows of the Hessian matrix are given by

| (13) | ||||

| (14) | ||||

| (15) |

for . Here and the -th entry of , for , is given by

Remark 2.

While (13) requires no extra computation, if the eigen-decomposition of is available, (14) and (15) use the matrix , which implies a cost. Further, for each and , (14) and (15) require vector-vector operations, leading to an total cost. Note that the mixed derivatives blocks in (14) and (15) are not required by the fitting procedure of chiu1996, which updates the linear predictors controlling and in separate steps, rather than via a joint Newton update. Further, mixed derivatives are required here for smoothing parameter selection via the FS and EFS updates.

Denoting with , , and , the elements of the last rows of the Hessian matrix are

| (16) | ||||

| (17) |

for , while for , and , they take the form

| (18) |

where is a array, with elements

Here, is a matrix given by , where is such that if and 0 otherwise; is a array given by , where is a matrix whose -th row, , is given by ; and is a array given by , where if and , and 0 otherwise. SM A.2 provides details that lead to (16 - 18).

Remark 3.

Computing , for , and , requires computing the arrays , and at cost . Then, for each and , we need to compute the sum of terms involving the elements of and , which implies an cost. Instead, the expressions in chiu1996 (see formulas (17) and (A.2) therein), involve a sum over terms for each and , leading to a total cost of .

In summary, the expressions for the first and second log-likelihood derivatives w.r.t. provided above save, respectively, and computation, relative to the formulas provided by chiu1996. Recall that such derivatives are required by the model fitting methods of Section 2.2 and that the EFS iteration requires also the third-order derivatives. However, as demonstrated by SM A.2, obtaining efficient formulas for the third-order derivatives would be very tedious. Further, the results discussed in Section 3.3 show that they would be expensive to compute due to the lack of sparsity, which makes the EFS iteration unattractive under the logM parametrisation. As explained in Section 4 the lack of sparsity can lead to a large memory footprint even when third-order derivatives are not computed, but the block-based strategy proposed therein alleviates the issue.

3.2 Log-Likelihood Derivatives under the MCD Parametrisation

The MCD parametrisation of pourahmadi1999 is defined as follows. Let be the lower-triangular Cholesky factor of , such that . Then the MCD of is

| (19) |

where is a diagonal matrix such that , , and . Note that the non-zero elements of and are unconstrained, hence they can be modelled via the linear predictors , . In terms of the general parametrisation matrix , defined in (1), we have and .

An important advantage of the MCD parametrisation is the interpretability of the decomposition elements, which can be obtained by regressing the response vector elements on their predecessors. In particular, pourahmadi1999 shows that a random vector such that can be generated by the process

where , for , and , for . Hence, the lower-triangular elements of can be interpreted as the negative regression coefficients of an element of on its predecessors, while the elements of are related to the variance of the regression residuals.

Note the interpretation of the MCD elements depends on the order of the response vector elements, which can aid model selection when the elements of have some natural ordering. In particular, see pourahmadi1999 and gioia2022additive for examples where the response elements have, respectively, a temporal and a spatial order. When the elements of do not have a natural ordering, the dependence of the MCD on the ordering is undesirable, hence kang2020variable has proposed a strategy to mitigate the ordering effect. However, note that muschinski2024 and barratt2022covariance found the covariance model fit to be insensitive to random permutations of the variables, which suggests that ordering should be checked but might be not a problem in practice.

From a computational perspective, fitting MCD-based multivariate Gaussian additive models is very efficient, relative to logM. Indeed, by using the property within (8), we obtain that a log-likelihood contribution is

| (20) |

which, in contrast with the logM case, can be directly expressed in terms of the linear predictors, thus facilitating the model fitting procedures (see SM A.3 for details). Evaluating (20) takes operations, lower than the required under the logM parametrisation. Further, the derivatives of (20) w.r.t. are easier to obtain, relative to the logM case, hence they are reported in SM A.3. More importantly, they become increasingly sparse as the order of differentiation increases, and this greatly speeds up computation.

Remark 4.

The log-likelihood gradient w.r.t. is dense and requires computations, as for the logM parametrisation. The Hessian is sparse, with a ratio of non-zero to total unique elements of . Most of these elements cost , leading to a total cost of , which should be compared with under the logM model. The third-order derivatives are even sparser, the ratio of non-zero to the total unique elements being . Most of these elements cost , leading to an total cost. See SM A.3 for MCD derivative expressions and SM A.3.1 for an analysis of their sparsity patterns.

Recall from Section 2.2 that the first two log-likelihood derivatives w.r.t. are needed for model fitting, while the third-order derivatives are required for smoothing parameter optimisation via the EFS iteration. The sparsity of the third-order derivatives makes the EFS iteration a feasible option under the MCD parametrisation, hence Section 5 compares the FS and the EFS iteration in a simulation-based scenario.

3.3 Comparison between the logM and MCD Parametrisations

The analytical results provided so far show that the computational cost for evaluating , , is of the same order for the logM and MCD parametrisations, while evaluating , , under the logM parametrisation cost times more than for the MCD. Here we empirically assess the computational time needed to evaluate the second-order derivatives under each model, by considering and . To provide a benchmark, we compare the timings obtained using the derivative expressions provided here (henceforth called Efficient) with those obtained by using automatic differentiation (henceforth AD) via TMB package (tmbPackage).

Figure 1 shows the results obtained over ten runs. By comparing the -axes scales it is clear that the MCD is more scalable than the logM model as grows. Further, the relative performance of AD deteriorates as increases, particularly under the MCD model. A tentative explanation is that, under the logM parametrisation, the evaluation of the derivatives via AD is less optimised than the expressions provided in Section 3.1, which required considerable analytical work aimed at efficient evaluation (see SM A.2). Under the MCD model, AD is not, to our best knowledge, automatically detecting the sparsity pattern of the Hessian, hence it is computing more elements than necessary.

We also compare the logM and the MCD parametrisations in the context of additive covariance matrix model fitting, using the FS iteration described in Section 2.2. To do this, we generate the data from , , where is obtained from via either the MCD or the logM parametrisation. In particular, the true mean vector and the lower triangular entries of , are simulated according to

where , and are generated from the standard uniform , , , , , , and .

We fit the model , for , and , for , where the ’s are smooth functions built using thin-plate spline bases of dimension , under both the MCD and logM parametrisation. The simulation study is replicated ten times, with and over the grid .

Figure 2 shows the model fitting times and the total number of Newton’s iterations used to obtain (a MAP estimate of must be computed at each FS optimisation step), for both the logM- and MCD-based models, when the true covariance matrix is related to via the MCD model. The results confirm that the MCD is more scalable than the logM parametrisation as increases. The plot on the right shows that the number of iterations is similar between the two parametrisations, hence the lower fitting time of the MCD-based model is not due to faster convergence. Instead, the MCD model is faster to fit because computing the Hessian w.r.t. , which is the dominant computation cost of model fitting via the FS iteration, is more scalable under this model. This is due to the second-order derivatives w.r.t. being increasingly sparse as increases which leads to a sparse Hessian w.r.t. . Similar fitting times are obtained when the true covariance of the simulated responses is related to via the logM parametrisation; see SM B.2 for details.

4 Limiting Memory Requirements

The previous section focussed on the computation of the log-likelihood derivatives w.r.t. , under either the MCD or the logM parametrisation. This section is concerned with the memory footprint required during model fitting and proposes strategies to mitigate its size.

4.1 Block-based Derivatives Computation

Fitting multivariate Gaussian additive models using the methods described in Section 2.2 can require a considerable amount of memory. In particular, recall that obtaining MAP estimates, , via Newton’s methods requires the gradient and Hessian of the log-posterior w.r.t. and assume, for simplicity, that all the model matrices , , have columns. Then, computing the gradient and the Hessian via (4) requires storage for the design matrices. However, the memory footprint can be reduced by an factor if and are discarded immediately after being used to compute and . Doing so for each and has an cost, but the matrix-matrix products in (4) cost operations, hence the leading cost of computation is not altered. Under the MCD parametrisation, the cost of computing all the blocks is reduced by an factor, due to the sparsity of , but this does not affect the memory required to store the model matrices, hence discarding and re-evaluating them can still be advantageous.

In contexts where is large and is moderate, storing even a single model matrix can still require a considerable amount of memory. However, in such scenarios the memory footprint can be limited by adopting block-oriented methods for computing (4). In particular, assume that the observations have been divided into blocks and that, for simplicity, is a multiple of . Indicate with the number of observations in each block, and with the -th row-wise block of . Analogously, let and , for , be sub-vectors of and , respectively. Then, (4) can be written as

| (21) |

If and are discarded after being used to compute a term in (21), then memory requirements are reduced by an factor, relative to stardard evaluation via (4).

Block-oriented GAM fitting methods that do not require storing the full model matrix have been considered by wood2015generalized, while wood2017generalized focus on speeding up GAM computation via a covariate discretisation scheme. However, such methods apply to GAMs with only one linear predictor (i.e., ). Here is , which leads to additional computational challenges. In particular, storing and for , and , requires, respectively, and memory, which can be considerable even for moderate . For example, gioia2022additive consider a regional electricity net-demand data set where and , which they model using a multivariate Gaussian additive model comprising linear predictors. Under the logM parametrisation, storing requires nearly 6 GBytes of memory, whereas under the MCD this is reduced to approximately 1 GB due to sparsity. By computing and and discarding them as soon as the -th accumulation term in (21) has been computed, the memory requirements are reduced to , without incurring any additional computational cost.

4.2 Exploiting Parsimonious Model Structures

In principle, the block-oriented strategy just described solves any memory requirement issue when computing because, given , we can choose to obtain blocks of the desired size. But, as increases, limiting the memory needed to store the vectors , requires to increase at an rate. Hence, the number of rows, , of decreases rapidly with , which is detrimental from a computational point of view. In particular, the matrix multiplications required to compute are level-3 (i.e. matrix-matrix) BLAS routines, optimized by numerical linear algebra libraries such as ATLAS or OpenBLAS. Such libraries provide implementations of level-3 routines designed to speed up computation by making optimal use of cache memory and other processor-dependent features, provided that they are multiplying matrices of sufficiently large size. Hence, reducing the size of the matrix blocks that are being passed to such routines, can lead to slower computation of .

While, under a simple setting where is an matrix for every , keeping a small memory footprint as increases requires smaller and smaller blocks, there are practically relevant modelling settings that lead to more efficient computation. Here we focus on parsimoniuous scenarios, where a significant proportion of the linear predictors do not depend on the covariates, but are fixed to an intercept. Examples are provided by gioia2022additive, who consider models where over 60% of the linear predictors controlling an MCD-based covariance matrix parametrisation are modelled only via intercepts. More generally, in cases where the elements of the response variable are related in space and/or time, as in the example considered in Section 6, one might expect parsimonious model structures to emerge as increases. For instance, as explained in Section 3.2, under the MCD model the elements of the factor can interpreted as regression coefficients between elements of and, if the distance between such elements increases with , it seems sensible to keep constant the elements of that quantify the dependence between distant responses.

When dealing with parsimonious model structures, it is possible to rearrange the computation of to use larger matrix blocks, which leads to a more efficient use of level-3 BLAS routines. Recall that the derivatives should be computed and stored jointly, for all values of and , so that they can be used to compute the -th term in the accumulation appearing in (21). However, when both and are modelled only via intercepts, the corresponding design matrices are simply vectors of ones and is a scalar equal to the sum of the elements of . Hence, the elements of the latter can be accumulated as soon as they are computed, as detailed in Algorithm 1.

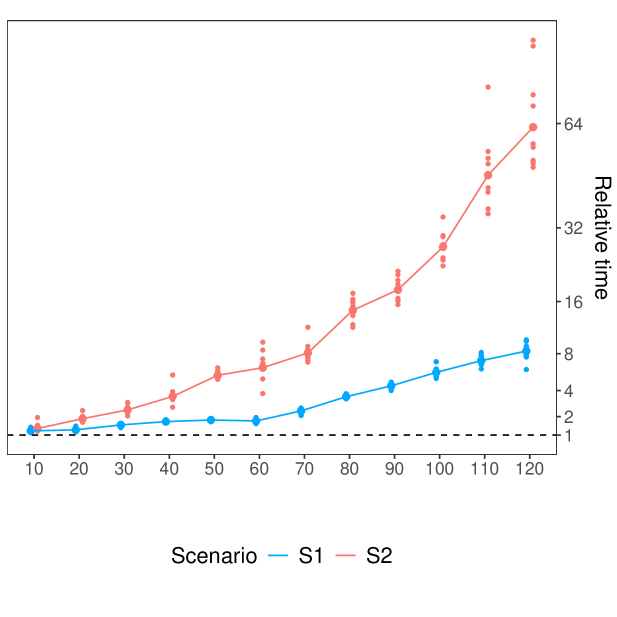

To quantify the effect of parsimony on the size of the matrix blocks, assume that a fraction of the linear predictors is controlled only via an intercept. Then, using Algorithm 1, the storage required by is . Hence, taking into account the structure of parsimonious models permits expanding by an factor, while fulfilling the same memory requirements. To assess how larger blocks translate into more efficiency during level-3 BLAS computations, we consider a numerical study where we simulate multivariate Gaussian responses in dimensions, from a model where the mean vector elements are , , while the linear predictors controlling the covariance matrix are

| (22) |

where , indicates one of two scenarios. In particular and which, considering that , implies that the number of modelled (i.e., non-constant) linear predictors grows, respectively, at a and rate. These parsimonious regimes are shown on the left of Figure 3. Note that the second scenario is highly parsimonious but still realistic as it includes, for example, MCD-based banded models where only the elements of and of the first few sub-diagonals of depend on covariates. Under both scenarios, we evaluate using either the standard block-oriented computation as in (21) (Standard) or Algorithm 1 (Parsimonious). In both cases, the number of blocks, , is such that storing requires at most 1 GByte.

The plot on the right of Figure 3 shows the time required to evaluate using the Standard approach relative to the Parsimonious method, based on ten runs under the logM parametrisation. Clearly, the performance gains of the Parsimonious approach are proportional to , particularly in the second scenario. Under the MCD model, the gains are marginal due to the sparsity of the derivatives w.r.t. . See SM B.3 for further details.

Let , for , be sets of indices such that if , and otherwise. Let be the indices of the fixed linear predictors, that is for , where is a vector of ones. Define if and otherwise. Let be the indices of the observations belonging to the -th block. Let be either scalars, initialised a zero if , or vectors with elements, otherwise. Finally, let be matrices of appropriate size, with elements initialised at zero. For :

-

1.

For , and , compute and then either store it or accumulate it, that is

-

2.

For and , compute via

5 Efficient Computation of the Fellner-Schall Update

Recall that the smoothing parameter vector, , is selected by maximising the LAML (5), via either the approximate FS update or its exact version (EFS). Here we provide efficient methods for computing the latter, which allow us to check whether the FS update leads to a poorer model fit and to compare the computational cost of the two methods.

As explained in Section 2.2, the FS update assumes that in (7) is zero. This simplifies computation, because is obtained by evaluating the third-order log-likelihood derivatives w.r.t. , rendering the EFS update unattractive under the logM parametrisation. However, under the MCD-based model, the third- and second-order derivatives incur the same cost due to sparsity, which, in combination with the methods described below, makes the adoption of the EFS update feasible.

In particular, the block of corresponding to the -th and -th linear predictor is

| (23) |

where and can computed by implicit differentiation (see wood2016, for details). Using (23), we can now write

| (24) |

where , the latter being the -th block of . However, a more computationally efficient expression for computing is

| (25) |

where , with a p-dimensional vector of ones, and is the matrix-to-vector diagonal operator.

Remark 5.

Assume, for simplicity, that each model matrix has columns. Then, computing involves an , which is the leading cost under the FS update. Under an MCD-based model, the EFS update involves a further cost, if is evaluated via (24). However, the cost of computing can be reduced to by adopting (25). This implies that the additional cost of EFS, relative to FS, is moderate unless .

To compare the FS and EFS methods, we consider the simulation setting of Section 3.3, with , , and ten runs for each value of . We include in the comparison the back-fitting (BF) methods provided by the bamlss R package (umlauf2021jss). The times reported in Table 1 shows that EFS is slightly slower than FS, due to the cost of computing the term in (25) and of the third-order log-likelihood derivatives w.r.t. (see SM A.3). Note that BF leads to model fits that are very similar to those obtained via either FS or EFS (the relative differences in log-likelihood at convergence, not shown here, are less than ), which highlights the scalability of the proposed methods.

| Value | Method | 2 | 5 | 10 | 15 | 20 |

| Time (min) | FS | 0.2 (0.2) | 1.2 (1.3) | 6.8 (7.3) | 27.0 (32.9) | 109.1 (155.1) |

| Rel. time | EFS | 1.1 (1.2) | 1.1 (1.2) | 1.2 (1.3) | 1.5 (1.8) | 1.5 (1.8) |

| BF | 5.0 (6.1) | 17.1 (28.4) | 58.5 (91.0) | - (-) | - (-) |

Finally, recall that both the EFS update and its approximate FS version aim to select the smoothing parameters by minimising the LAML. Interestingly, in the simulation study conducted here, the two updates converge to the same LAML score, within a relative difference of less than . Hence the approximation error induced by the simpler FS update is minimal, which motivates its adoption in the following section.

6 Application to Electricity Load Modelling

Here we compare the performance of the logM- and MCD-based models in a realistic setting. We consider data from the electricity load forecasting track of the GEFCom2014 challenge (hong2016). The response vector consists of hourly electricity loads (), where , indicates the hour and , is the index of the day, spanning the period from the 2nd of January 2005 to the 30th of November 2011. Hence, we have and . The covariates are progressive time (), day of the year (), day of the week (), hourly loads of the previous day (), hourly temperatures ( and exponential smoothed temperatures (, with ).

We consider the model , where is parametrised via either the logM or the MCD. The joint mean and covariance matrix model has linear predictors, which entails a challenging model selection problem. For the mean vector, we use the model

for , where and are parametric linear effects, while to are smooth effects, with superscripts denoting the spline bases dimensions. To model the linear predictor controlling , we consider a full model where

under either the MCD or the logM parametrisation. Having 3000 parameters controlling , the full model is over-parametrised, hence we simplify by backward stepwise effect selection. In particular, we fit the full model on data from up to 2010, and then we remove the five effects with the largest p-values. We iterate this procedure until we get to a model where for , are all constant, that is they are modelled only via intercepts.

The number of effects to be retained in the model is determined by optimising the out-of-sample predictive performance on 2011 data. To evaluate such performance, we adopt a 1-month block rolling origin forecasting procedure. In particular, having fitted each model to data up to the 31st of December 2010, we produce predictions of and for the next month. We then update each model by fitting it to data up to the 31st of January 2011, and obtain a new set of predictions. By repeating the process over the whole of 2011, we obtain a full year of predictions, which we use to compute the log-score (LS), that is the negative log-likelihood of the out-of-sample data.

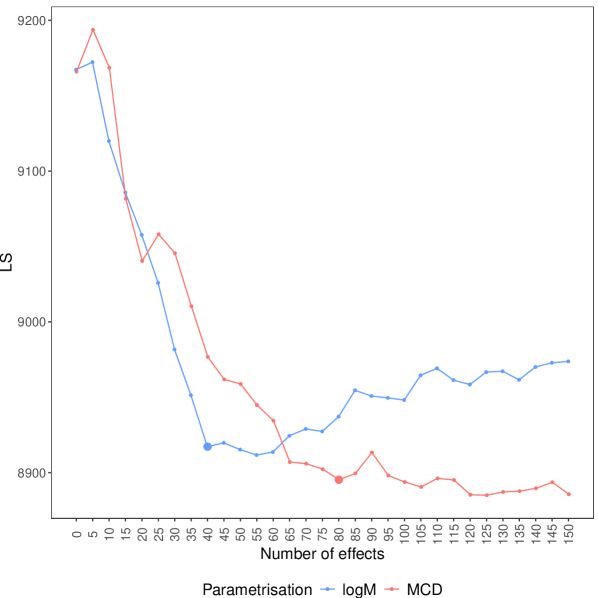

While the fitting times on the training data are reported in SM B.4, the plot on the left of Figure 4 shows the LS metric for models ranging from 0 to 150 effects to model . Considering the shape of the two curves, we sped up computation by not evaluating the performance of models containing more than 150 effects. Indeed, under the logM model, predictive performance has a well-defined minimum between 40 and 60 effects while, under the MCD model, the gains are diminishing for models containing more than 80 effects. Hence, the logM parametrisation leads to more parsimonious models for this data, but their predictive performance is inferior to that of more complex MCD-based models.

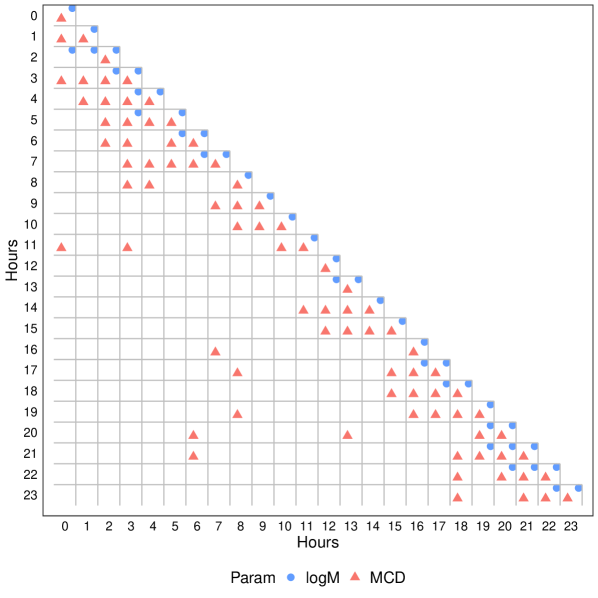

On the right of Figure 4, we show which elements of the logM and MCD parametrisation matrices have been modelled via smooth effects of , when using respectively 40 and 80 such effects. Considering the interpretation of the MCD parametrisation presented in Section 3.2, it is not surprising to see that all the diagonal elements of and many of the elements on the first few leading sub-diagonal are being modelled. This suggests that the residual correlation between consecutive hours, and the residual variance after having conditioned on previous hours, vary significantly with . Under the logM model, all diagonal elements of are allowed to vary with , with the remaining effects appearing on the first or second leading subdiagonal. Although the elements of the logM model do not have any direct interpretation in general, our understanding is that, for the data considered here, the logM model allows the variances to vary strongly with , while the correlation structure is kept relatively constant. See SM B.4 for more details.

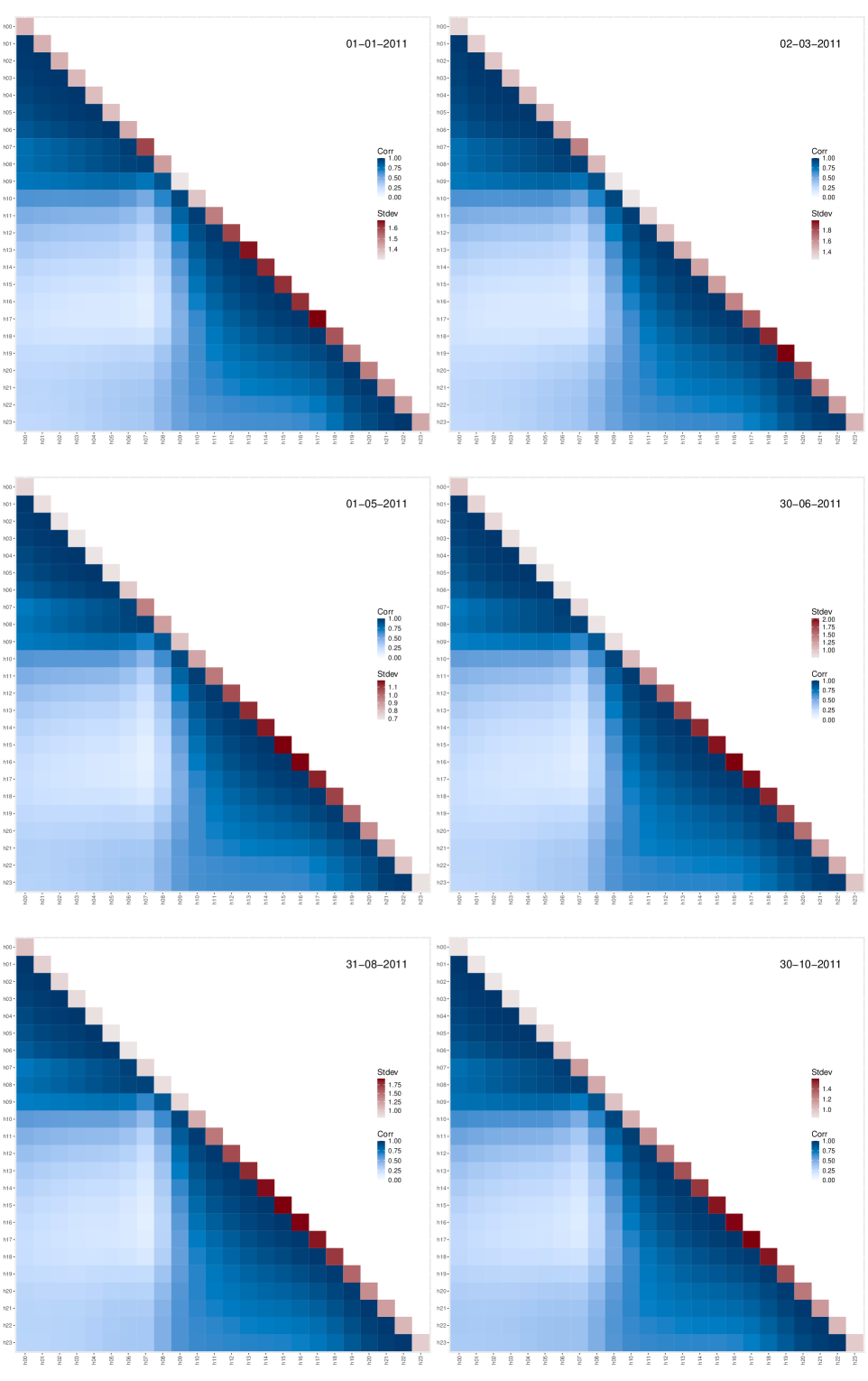

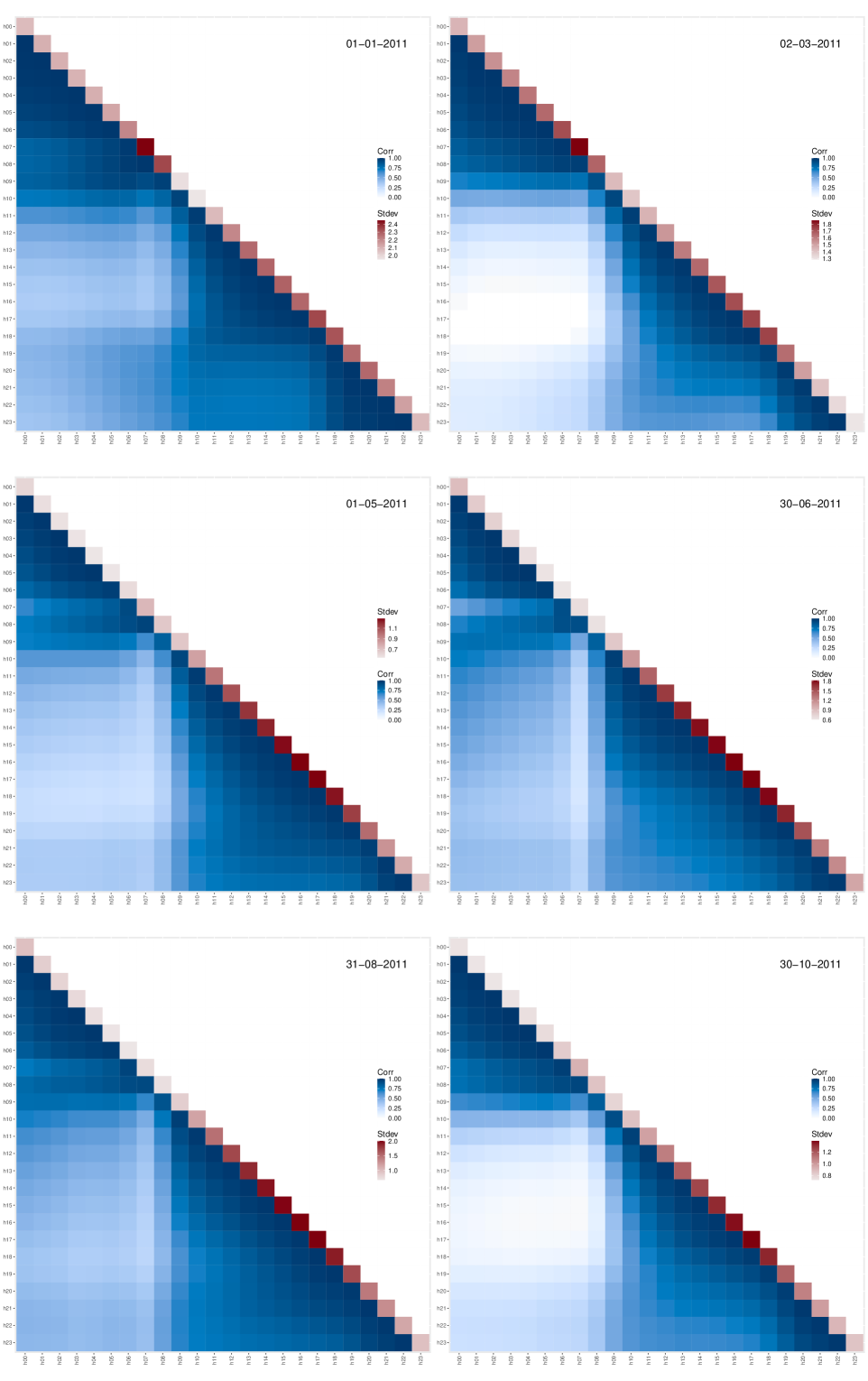

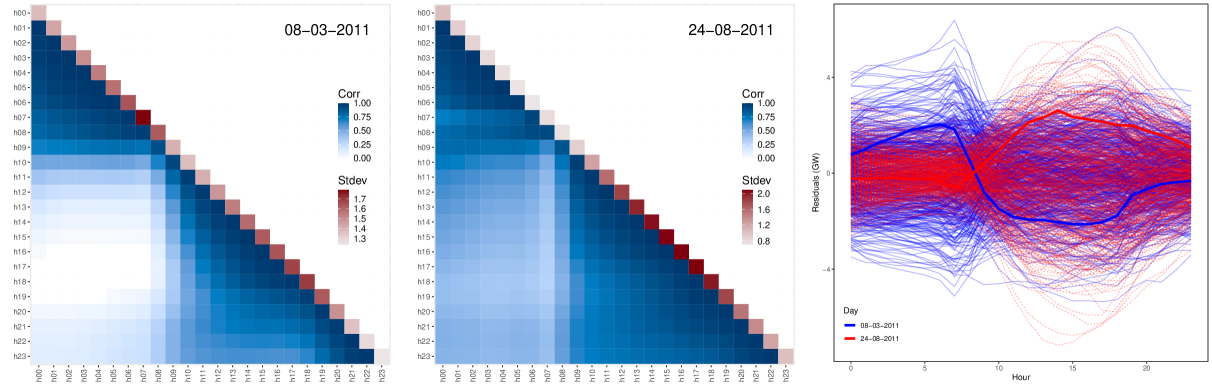

The heatmaps in Figure 5 represent the covariance matrices predicted by the MCD-based model with 80 effects on two different days, demonstrating the importance of a dynamic covariance matrix model in this context. In particular, note that in March the residual variance is largest at 7 am and 6 pm, which correspond to the morning and evening demand ramps (the times at which demand increases at the fastest rate). In August, the variance has a wider peak around 4 pm, indicating that load prediction errors are expected to be largest at this time. Note also that the correlation structure changes with the time of year, with the correlation between morning and evening residuals being much weaker in March than in August. The plot on the right of Figure 5 shows the observed residuals on the two days, together with 500 residual trajectories simulated from the model. The shape of the simulated trajectories is coherent with that of the observed curve, meaning that the model could be used to generate realistic demand curves, which could serve as inputs for decision-making under uncertainty in the power industry (e.g., to inform trading strategies or stochastic power-production scheduling).

7 Conclusion

This work provides computationally efficient methods for fitting multivariate Gaussian additive models with covariate-dependent covariance matrices, with a particular focus on the widely used MCD and logM unconstrained parametrisations. Under the model fitting framework proposed here, computational efficiency requires fast evaluation of the log-likelihood derivatives. Hence, we show how this can be achieved by exploiting sparsity in the MCD case or by employing highly optimised derivative expressions under the logM model. Further, we provide computational methods for exploiting parsimonious modelling scenarios and show that doing so can greatly speed up computation, especially under the logM model and in high dimensions. We also enable efficient computation of the exact FS update to maximise the LAML. While the results provided here support the use of the original FS update, which is cheaper to compute, more theoretical work is needed to verify whether the approximation error implied by this update is negligible in general.

Future work could also focus on developing covariance matrix models that better exploit known structures in the data. For example, in the application considered here, the MCD elements can be interpreted as the parameters of an autoregressive model on the residuals. Here, we do not exploit this interpretation and choose the model via an expensive backward effect selection routine to fairly compare the MCD and logM models. But it would be interesting to integrate the computational methods proposed here with the models considered by huang2007estimation, who exploit the MCD interpretation to control the whole covariance matrix via a few parameters.

References

Supplementary Material to “Scalable Fitting Methods for Multivariate Gaussian Additive Models with

Covariate-dependent Covariance Matrices”

Appendix A Parametrisation Specific Quantities Needed for Model Fitting

A.1 Notation and Useful Quantities

Recall the following notation. The operator is the vector-to-matrix diagonal operator, while is the matrix-to-vector diagonal operator. The matrix exponential operator is denoted with , the Hadamard product with , and is the indicator function. Further, and represent, respectively, the -th row and the -th column of a matrix . Finally, the derivatives w.r.t. are denoted with , , and , corresponding to the vectors with -th elements

where refers to the element () of the matrix including the linear predictors, , and is a scalar-valued function.

Then, let a lower triangular matrix such that

with , and let and two lower triangular matrices such that and . Denoting with the row-wise half-vectorisation operator, that is , we define and . In the following, the subscript is omitted to lighten the notation.

A.2 Derivatives for the logM Parametrisation

This section reports the formulation of the likelihood quantities needed for implementing the logM-based multivariate Gaussian model. Some quantities, already introduced in Section 3.1, are recalled for clarity. Let , where is the orthonormal matrix of the eigenvectors and is the diagonal matrix of the log-eigenvalues, resulting from eigen-decomposing , that is , for . Then, with . The Gaussian log-density, up to an additive constant and omitting the subscript , is

| (A.1) |

where and .

In addition, recall that and the relation , where the ’s are basis matrices; that is, if they take the form

Gradient

The log-likelihood gradient is given by

| (A.2) | ||||

| (A.3) |

where and are vectors of indices defined in SM A.1, while with and is a matrix such that

While the derivatives , , are trivial to obtain, those for , are derived from

| (A.4) |

Leveraging najfeld1995, the following expression can be obtained via

| (A.5) |

where , . By exploiting the property , the derivatives , , take the form

Then, the result is obtained by substituting in , and noticing that is the element of accessed by the indices given in (A.2) and (A.3).

First Rows of the Hessian Matrix

Denoting with , the second-order derivatives of (A.1), for , are

| (A.6) | ||||

| (A.7) | ||||

| (A.8) |

where the -th element of , for , is

Expression (A.6) is trivial to obtain, while the derivatives , for , and , are derived from

| (A.9) |

By using the property , it is possible to obtain the form

Then, for , the expression (A.7) is obtained by observing that , for , and , for , which implies that

Finally, for , to obtain (A.8) note that , with , and , with which leads to

Last Rows of the Hessian Matrix

Denote with , , , and , and recall from Section 3.1 the following quantities; is a matrix obtained as , where is such that if and 0 otherwise; is a array given by , where is a matrix whose -th row, , is given by ; in indicial form it is

then, is a array given by , where if and and 0 otherwise; in indicial form it is

finally, is the array, whose elements are of the form

Then, the second-order derivatives of (A.1), for , are

| (A.10) | ||||

| (A.11) |

and, for and , take the form

| (A.12) |

The second derivatives , for and , are obtained via

whose solution require computing . To simplify, is carried out because the final result is simply obtained by changing the sign of the eigenvalues. Similarly to najfeld1995, can be obtained via directional derivatives (w.r.t. to the direction and ) of , denoted with , that are solution of the integral

| (A.13) |

Only one of the two integrals in (A.2) must be solved, the other is simply obtained by permuting the indices and . Instead of solving directly (A.2), an efficient formulation is carried out by considering , which allows using the property . Then, the first inner integral of (A.2) takes the form

with and (note that , after changing the sign of the eigenvalues), and consider that , with a matrix such that , for . Denote with the -th column of , , and consider the identity matrix . Thus, it is possible to obtain

| (A.14) |

where . Then, for simplicity distinguish three cases

-

1)

For , and

-

2)

For , and

-

3)

For and ,

Then, replacing the above case-expressions into (A.2) and developing the integral, the expressions of the arrays , and are obtained after some algebraic arrangements, including the change of sign for the ’s. Hence the solutions (A.10), (A.11), and (A.12).

A.3 Derivatives for the MCD Parametrisation

The MCD parametrisation is expressed as , where is a diagonal matrix, such that , and

Omitting the constants that do not depend on and denoting with the -th element , the -th log-likelihood contribution is

| (A.15) |

after using and implicitly assuming that the sum should not be computed when (the same convention is used in several places below). Similarly, below the sum will not be computed when . Here the derivatives of w.r.t. up to the third order are obtained, both in compact matrix form and indicial form, the latter being more useful for efficient numerical implementation. Finally, the following matrices are introduced, being largely used in the matrix form expression of the likelihood derivatives reported below, that is , for , and , for , such that and , while all other elements are equal to zero.

Score Vector

The elements of are

for ,

for , and

for .

Hessian Matrix

The elements forming the upper triangle of (here ), are

for and ,

for and ,

for and ,

for and ,

for and , and finally

for and .

Third Derivatives Array

The elements forming the third derivatives array (here ), are

for

for

for

for

for

for

for

for

for

for .

A.3.1 Sparsity of Derivatives for the MCD Parametrisation

The sparsity of the second- and third-order derivatives is directly related to the dimension of the outcome . Consider the following notation. Let , , the subset of corresponding to the predictors involved in modelling the vector (), the matrix () and the matrix (). Then, , , and . Hence, for the Hessian matrix, denotes the number of non-redundant elements forming the block , , and denotes the number of non-zero elements of such blocks. For instance, is the number of non-redundant elements forming the upper triangular block of , , and, thus, is the number of non-redundant elements different from zero forming such triangular block, while is the number of non-redundant elements forming the square block , , , and is the number of non-redundant elements different from zero forming such square block, and so on. Similarly, for the third derivatives array, we denote with the number of non-redundant elements forming the block , , and with the number of non-zero elements of such blocks. It is easy to obtain the total number of elements for each block and the number of elements different from zero within them. To obtain such closed forms the identity is massively used. In Table A.1, the number of non-redundant elements different from zero and the total number of non-redundant elements for each block is reported for the Hessian matrix and the third derivative array, respectively, while the last row considers all the blocks. Instead, in Figure A.1 we report the ratio between the total number of elements different from zero and the total number of elements, by varying the dimension of the outcome .

| (1,1) | 1 | ||

| (1,2) | 1 | ||

| (1,3) | |||

| (2,2) | |||

| (2,3) | |||

| (3,3) | |||

| Total | |||

| (1,1,1) | 0 | ||

| (1,1,2) | 1 | ||

| (1,1,3) | |||

| (1,2,2) | |||

| (1,2,3) | |||

| (1,3,3) | |||

| (2,2,2) | |||

| (2,2,3) | |||

| (2,3,3) | |||

| (3,3,3) | 0 | ||

| Total |

Appendix B Further Details and Results

B.1 Computer System and Software Details

The log-likelihood derivatives w.r.t. and , as well as auxiliary parametrisation-specific quantities, are written using the C++ language and interfaced with the R (Rsoftware) statistical software by means of Rcpp (RcppPackage) and RcppArmadillo (eddelbuettel2014rcpparmadillo). Further, methods for building and fitting the multivariate Gaussian additive models are implemented by the SCM R package, which is available at https://github.com/VinGioia90/SCM and leverage the model fitting routines of the mgcv package (wood2011fast, wood2016). At the time of writing, being not yet on CRAN, a developer package version of mgcv is used. The code for reproducing the results in this article is available at https://github.com/VinGioia90/SACM. All the computations are done by using a 12-core Intel Xeon Gold 6130 2.10GHz CPU and 256GBytes of RAM.

B.2 Simulation Results

Figure B.1 shows the model fitting times and the total number of Newton’s iterations used to obtain , for both the logM- and MCD-based models, when true covariance matrix is related to via the logM model.

It is interesting to compare the MCD and logM models also in terms of goodness-of-fit. Hence, here we consider each model’s log-score (LS), that is the negative log-likelihood, as a performance metric. In agreement with intuition, Figure B.2 shows that the MCD (logM) model leads to a better fit when the true covariance matrix is related to via the MCD (logM) model. That is, fitting the true covariance model leads to a better fit, and the goodness-of-fit gains increase with .

B.3 Further Simulation Results under Parsimonious Models

Here we present further results using the simulation setting described in Section 4.2. In particular, the plot on the left-hand side of Figure B.3 shows the time needed to compute under the Standard approach, relative to that required under the Parsimonious methods for the MCD-based model. Clearly, the gains obtained by using the latter are very marginal.

To understand why this is the case consider that, under a logM model where each linear predictor is controlled via parameters (hence not a parsimonious setting), computing , for each and , requires operations. Hence, when , the Hessian w.r.t. determines the leading cost of computation, as computing involves operations. Under the MCD-based model, both derivatives cost less, due to sparsity, but their relative cost is unchanged. However, the number of blocks required to keep memory usage constant as increases is , rather than , hence the computational slowdown due to small blocks is less severe than under the logM model.

To assess the impact of sparsity on this issue, it is useful to consider a simulation setting in which the linear predictors controlling the mean vector are fixed to their intercepts, i.e. for . The corresponding relative computational times are shown on the right-hand side of Figure B.3. In this scenario, the Parsimonious methods scale better with , particularly in the second, more parsimonious, case. Note that fixing the mean vector to intercepts does not significantly affect the results under the logM model, as demonstrated by Figure B.4, which is consistent with the right-hand plot of Figure 3.

In summary, under the MCD model, the sparsity of the second-order log-likelihood derivatives with respect to for means that storing these derivatives requires little memory compared with the dense logM case. Consequently, adopting Parsimonious computational methods does not yield substantial gains, as most of the memory is allocated to storing the (dense) second-order derivatives associated with the mean vector, for . This implies that Parsimonious computational methods are effective for MCD models only when many of the linear predictors controlling the mean vector are fixed to their intercepts. By contrast, under the logM parametrisation, the second-order derivatives with respect to are non-zero for , so that Parsimonious computational methods lead to a speed-up regardless of whether the unmodelled linear predictors (i.e. those fixed to intercepts) control the mean vector or the covariance matrix.

B.4 Further Details on the Application

Figure B.5 illustrates the time required to fit the models described in Section 6. Under both parametrisations, model fitting was performed using the FS update for selecting the smoothing parameter and the computational methods detailed in Section 4, which are designed to exploit parsimonious modelling settings. Note that the MCD models are considerably faster than the logM models when only a few effects are used to model , for . This is because computing the second-order log-likelihood derivatives with respect to is much less computationally expensive under the MCD model, and this cost becomes dominant in highly parsimonious scenarios.

Recall from Section 6 that backward effect selection leads to a logM model where almost all the effects fall on the main diagonal or on the first subdiagonal. The reason for this is not immediately obvious because, in contrast with the MCD model, the element of the logM parametrisation to not have, to our best knowledge, a clear interpretation. However, Figure B.6 suggests that the logM elements that are being modelled as functions of the time of year () mostly control the conditional variances. In fact, the plots show that the conditional variances of electricity load vary strongly with , while the correlation structure is roughly constant through the year. In contrast, the selected MCD model allows both the variance and the correlation to vary through the year, as shown by B.7.