Stochastic Control of Drawdowns via Reinsurance under Random Inspection

Abstract

We consider a diffusion risk model where proportional reinsurance can be bought. In order to stabilise the surplus process, one tries to keep the drawdown, that is the difference of the surplus to its historical maximum, in an interval . The observation times of the drawdowns form a renewal process. The retention levels can only be changed at the observation times either. We show that an optimal strategy exists and how it is determined. We illustrate the findings in the case of Poissonian observation times and deterministic inter-observation times.

Keywords: drawdown; diffusion approximation; optimal proportional reinsurance; Bellman equation; random observations

Classification: MSC: Primary 91B05; secondary 60G42, 93E20, 91G05; JEL: C61, G22

1 Introduction

1.1 Problem Formulation

In order to appear reliable, insurance companies are interested in stabilising their surplus process and avoiding large losses. An object of interest is therefore the size of the drawdown, that is, the distance of the surplus to the last historical maximum. In [1], the time, in which the drawdown process of an insurer exceeds a critical level , was considered and an optimal proportional reinsurance strategy for minimising this time was determined. In reality, one can only observe the process and adapt the strategy at discrete time points. In this paper, we implement this idea by inspecting the process at the arrival times of an ordinary renewal process. Our aim is to minimise the number of time points at which a critical drawdown level is observed. We state a dynamic programming equation and show that the value function is the unique increasing and bounded solution. Moreover, we calculate the distribution of the drawdown under constant strategies explicitly. The dynamic programming equation can be solved numerically, which we do explicitly in the case of exponentially distributed and deterministic interarrival times, respectively.

We work on a complete probability space containing all the stochastic objects defined below. The surplus process of an insurance portfolio is given by the diffusion approximation with reinsurance

where is a standard Brownian motion, , and is the surplus level at the beginning of the observation period . That is, we consider proportional reinsurance. The parameters and can be interpreted as the safety loading of the insurer and reinsurer, respectively. In order that is not an optimal strategy, we assume , so reinsurance is more expensive than first insurance. is the reinsurance strategy specified below. The surplus is not monitored continuously but is only observed at the times . We model the observation times by a renewal process and denote the distribution of the interarrival times by and its Laplace transform by . We assume that and are independent. The filtration is the natural filtration generated by and , that is the smallest right continuous filtration such that and are adapted.

The insurer has the possibility to buy proportional reinsurance. But the reinsurance treaty can only be changed at the observation times , too. That means

where are -measurable random variables with values in for all . The set of all such strategies is denoted by . For a chosen strategy , the (controlled) running maximum and the (controlled) drawdown are given by

Remark 1.1.

Note that the distribution of the drawdown process depends on the difference only. It therefore makes sense to write instead.

Our aim is to stabilise the drawdown process in the what we call non-critical area , that is, the drawdown size should not exceed the level . If we nevertheless enter the critical area , what cannot be prevented for all times, then we prefer to leave it before it is observed at the inspection times . We therefore consider

where we count the number of observations in the critical area and is the initial drawdown. Note that we include the present observation. We additionally include a preference factor , such that the present observation has a higher weight than an observation far in the future. Since we want to minimise the number of observations, the value function is given by

The paper is organised as follows. We start by giving some basic properties of , including the dynamic programming equation and uniqueness of its solution. In Section 3 we determine the distribution of the drawdown at the next observation time. Two specific examples are considered in Section 4. Some technical details are given in the appendix.

2 Dynamic Programming

2.1 First Results and Dynamic Programming

We start with the following

Lemma 2.1.

The value function is non-negative, increasing and bounded by .

Proof.

It is clear that takes non-negative values only. For the upper bound we observe

Moreover, note that is (pathwise) increasing for every and . It is then easy to see that for we get for every . By taking the infimum over on the right hand side, we conclude that is increasing. The limit as follows from Bellman’s equation below, see Corollary 2.5. ∎

We can look at the observation times as regeneration times. Thus, for us the process up to time is of interest in which the chosen strategy is constant. We therefore consider now processes with a constant strategy.

Notation 2.2.

For we write , and for the constant strategy .

The following result is crucial for the characterisation of the value function.

Theorem 2.3.

The value function fulfils the dynamic programming equation

| (2.1) |

Proof.

Let be an admissible strategy with for and let . We observe

where for and for . Taking the infimum over on the left hand side yields

| (2.2) |

Choose and . Since the image of is bounded, there are only finitely many jumps larger than . Thus, we can choose and , such that . Moreover, for every we can choose , such that , and for . We define

For every we can choose a strategy , such that . Moreover, for every we can choose , such that . We define

Now let be arbitrary and consider the strategy . Analogously to above we find

By letting , and by taking the infimum over , we conclude

Together with (2.2), this proves the assertion. ∎

Lemma 2.4.

For a fixed retention level , the distribution of the drawdown at time is given by the distribution function

| (2.3) |

The density is of the form

| (2.4) | |||||

We postpone the proof to Section 3.

Corollary 2.5.

We have .

Proof.

Let and fix and . Then there is , such that for any Next, we show that there is , such that for and any . Note that we can find with . Choose

We can assume that , i.e. . By using (2.3), this yields for , and :

We conclude

Thus, for

Letting , and because and are arbitrary, . Thus, . ∎

Next, we show that the value function is the unique solution to the dynamic programming equation (2.1).

2.2 Existence and Uniqueness of a Solution

Denote by the space of all bounded functions with values in . Then, is a Banach space.

Theorem 2.6.

The value function is the unique solution to the dynamic programming equation (2.1).

Proof.

We define the operator by

| (2.5) |

and let . We first note that

and therefore for . Let , and . We have

Maximising over gives . Analogously, , yielding . By taking the supremum over on the left hand side, we conclude . This proves that is a contraction. By Banach’s fixed point theorem, there exists a unique solution to (2.1) which, according to Theorem 2.3, has to be the value function. ∎

Remark 2.7.

Banach’s fixed point theorem also provides an approach for determining the value function numerically. For define for all . This series converges to the fixpoint exponentially fast, which is the value function. We will exploit this in order to calculate numerically.

Theorem 2.8.

There exists a measurable function such that for all

| (2.6) |

Proof.

We claim that the continuous function

can be extended to a continuous function by

For we consider the three terms in (2.4) separately. That is, we calculate the limits of as . In the following we assume that . We start with . The expression can be written as

where is a standard normally distributed random variable. Splitting the expression in and , we get that the limit is

| (2.7) |

Next, consider . Note that tends to . Using as , yields

Thus, the terms connected to can be written as

Note that in the integration area. It now follows for that the expression considered tends to zero if and also if . This shows that exists.

Now there exists a minimiser such that . By [3], we can choose the function measurably. Note that by (2.7) and the observations above. This yields

if is left-continuous. In this case, the minimiser

| (2.8) |

fulfils (2.6). Suppose that is not left-continuous. Choose , such that is maximal. This is possible because is bounded. Due to the continuity of for and the dynamic programming equation, can only be true if

and

But this implies that

Since would violate , we find

which contradicts that was maximal. We conclude that is left-continuous. This shows that defined in (2.8) is a minimiser. ∎

Theorem 2.9.

The strategy given by

is optimal, in the sense that for all .

Proof.

Consider the process

Then,

where we used (2.1) in the last but one equality. Thus, is a martingale. This gives

where we used monotone convergence and bounded convergence, respectively. This shows that is the value of the proposed strategy. ∎

3 Distribution of the Drawdown

The dynamic programming equation (2.1) will be essential for the numerical calculation of the value function and the optimal strategy. We would therefore like to rewrite the equation to

| (3.1) |

where denotes the distribution function of . Thus, we need to determine the distribution of . If , we immediately see that the drawdown process is deterministic and . In the following, we calculate the distribution of for . We start with the case where the initial drawdown is zero.

Lemma 3.1.

The density of is

| (3.2) |

Proof.

The joint density of a Brownian motion with drift and its running maximum is given by

see for example [2, Equation (13.10)]. This yields for

By change of variable we get for the joint density of

which is the assertion. ∎

Proof of Lemma 2.4.

The initial drawdown is given by and let . If the process reaches the maximum in , that is , then is the drawdown in . The corresponding density on is then obtained by integrating the joint density over with respect to

If the maximum in is not reached, then the drawdown is . Integrating over with respect to yields the density of on

This gives the density for the drawdown on

Adding the two densities yields the density (2.4) of . By integrating with respect to we find the distribution function of :

∎

4 Two Different Scenarios for the Renewal Process

4.1 Poissonian Observations

In this section, we assume that the renewal process is given by a Poisson process with Poisson parameter . The inspection of the process therefore occurs at random time points.

4.1.1 Rewriting the Dynamic Programming Equation

First, we note that, according to Lemma 2.1, the value function is bounded from above by . We rewrite the dynamic programming equation (2.1) into an equation of the form

| (4.1) |

and develop an algorithm in order to calculate in a numerical way. If , we have

| (4.2) | |||||

giving

We need the following result for the calculations in the case .

Lemma 4.1.

Let , and . We have the following identities:

where

The proof is given in the appendix.

Now we note that for and , there exists a density function given by (2.4) for the distribution of . We can therefore write

Let . By using Lemma 4.1 we find

Finally, we need the following result for developing an algorithm to solve equation (4.1).

Lemma 4.2.

For it holds

and for

∎

4.1.2 Description of the Algorithm

In order to calculate the value function numerically, we note that, due to the Riemann integrability of and , equation (4.1) takes the form

where

is the set of partitions of the interval for . Moreover, if is the set of partitions of the interval , we find

We conclude for :

if we choose the partitions and sufficiently dense and large enough. We will now apply the idea from Remark 2.7: We fix and partitions and . Choose and define via

We stop the iteration as soon as we find such that for small.

4.1.3 Numerical Results

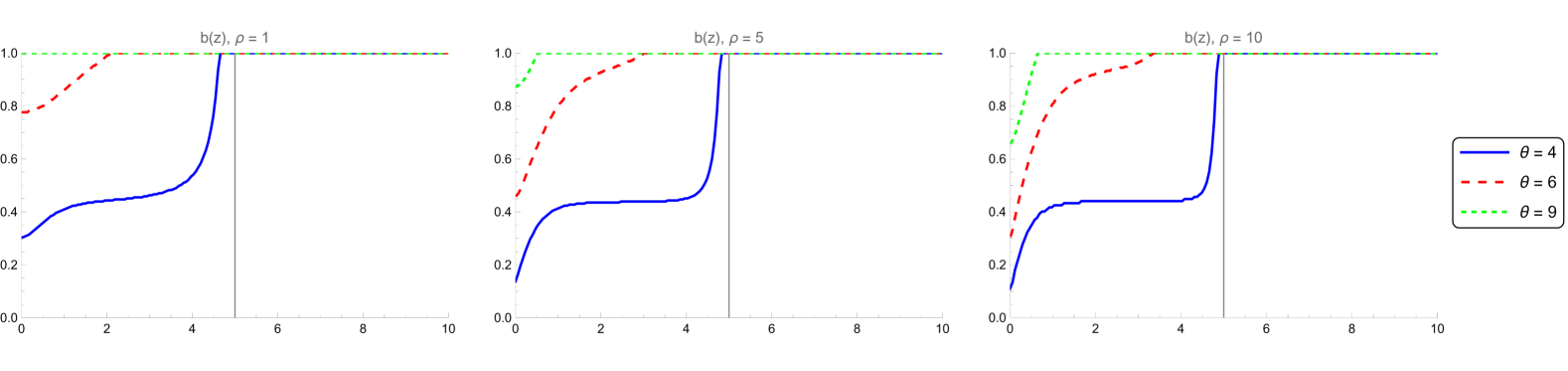

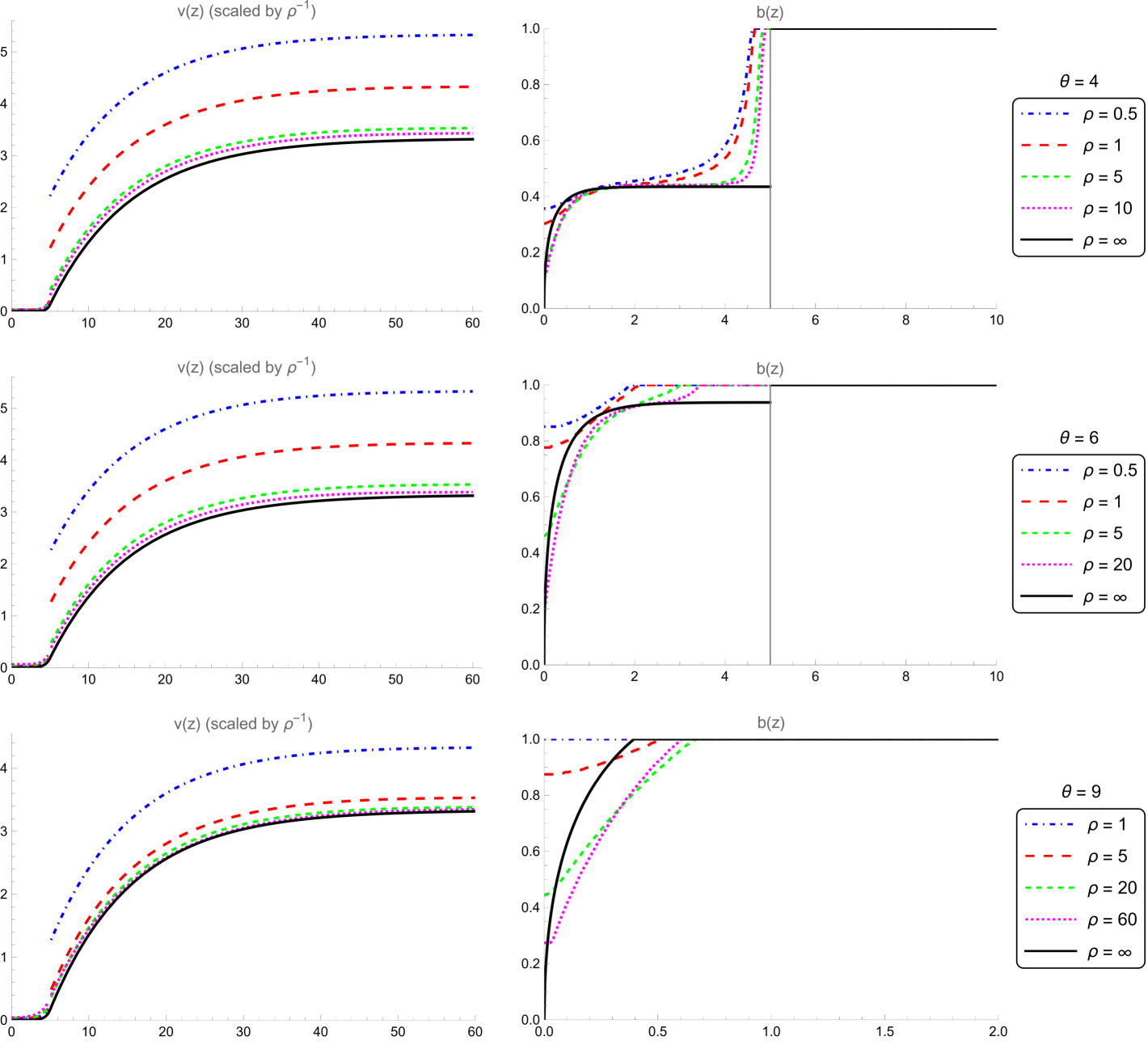

In the following, the results of the numerical analysis are illustrated and discussed. In Figure 1 and 2 we compare the value functions and corresponding retention levels for different prices of reinsurance and different Poisson parameters . The selected parameter values are listed in Table 1.

In general we can see, as observed in Lemma 2.1, that the value function is increasing and has a jump at the critical drawdown size . In Figure 1 we perceive that the retention level increases with the cost of reinsurance. Moreover, the retention level increases as the drawdown becomes larger until it constantly equals . We observe that this point is reached sooner, when reinsurance is more expensive. We can compare these observations to the results of [1], since the continuous time model considered there can be interpreted as a limiting case . In [1] the optimal strategy is given by a feedback strategy , where the minimiser takes the form

Here, is the Lambert W function and and are constants. In particular, it holds for all , which means that we choose the strategy with maximal drift in the critical area in order to reenter the non-critical area as quickly as possible. Comparing this with the results in Figures 1 and 2, we can see that in our model there is also a certain drawdown size above which it is not optimal to buy reinsurance, but this level is smaller than in the examples considered. Since we can only change the retention level at the observation times, i.e. in particular not at the moment when we enter the critical area, we will take countermeasures in advance when the drawdown approaches the critical drawdown level . The second difference we observe is the behaviour of the strategy for close to : In [1] it holds as . Since the drift becomes negative for close to , this means that the maximum value is never exceeded. In our model here, we can see that in all scenarios considered. However, in Figure 2 we observe that this value decreases in . This behaviour can be explained in a similar way as above: In [1] the strategy can be adjusted at any time, so that we can take immediate countermeasures if the drawdown becomes too large. As mentioned before, in our model we have to wait for the random times , such that a negative drift could lead to excessive growth in the drawdown if the expected interarrival time is large. All in all, we can see in Figure 2 that the optimal retention level and the corresponding value function converge to the continuous time case of [1] as the expected interarrival time becomes smaller. Therefore the differences mentioned above disappear for .

| Parameter | ||||

|---|---|---|---|---|

| Value | 3 | 2 | 0.3 | 5 |

4.2 Deterministic Observations

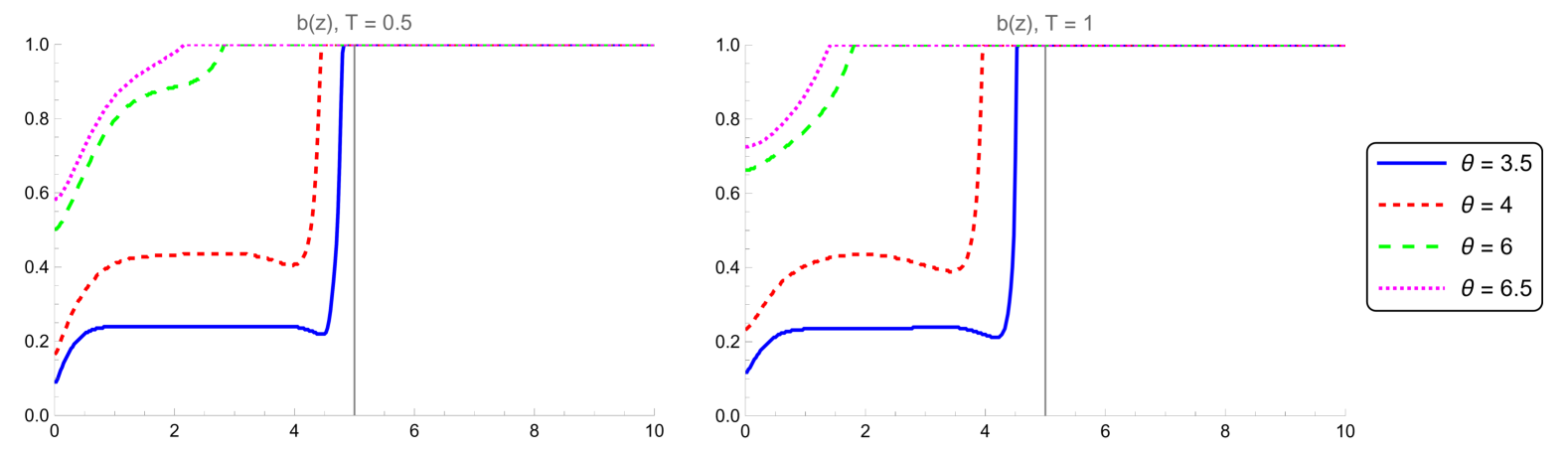

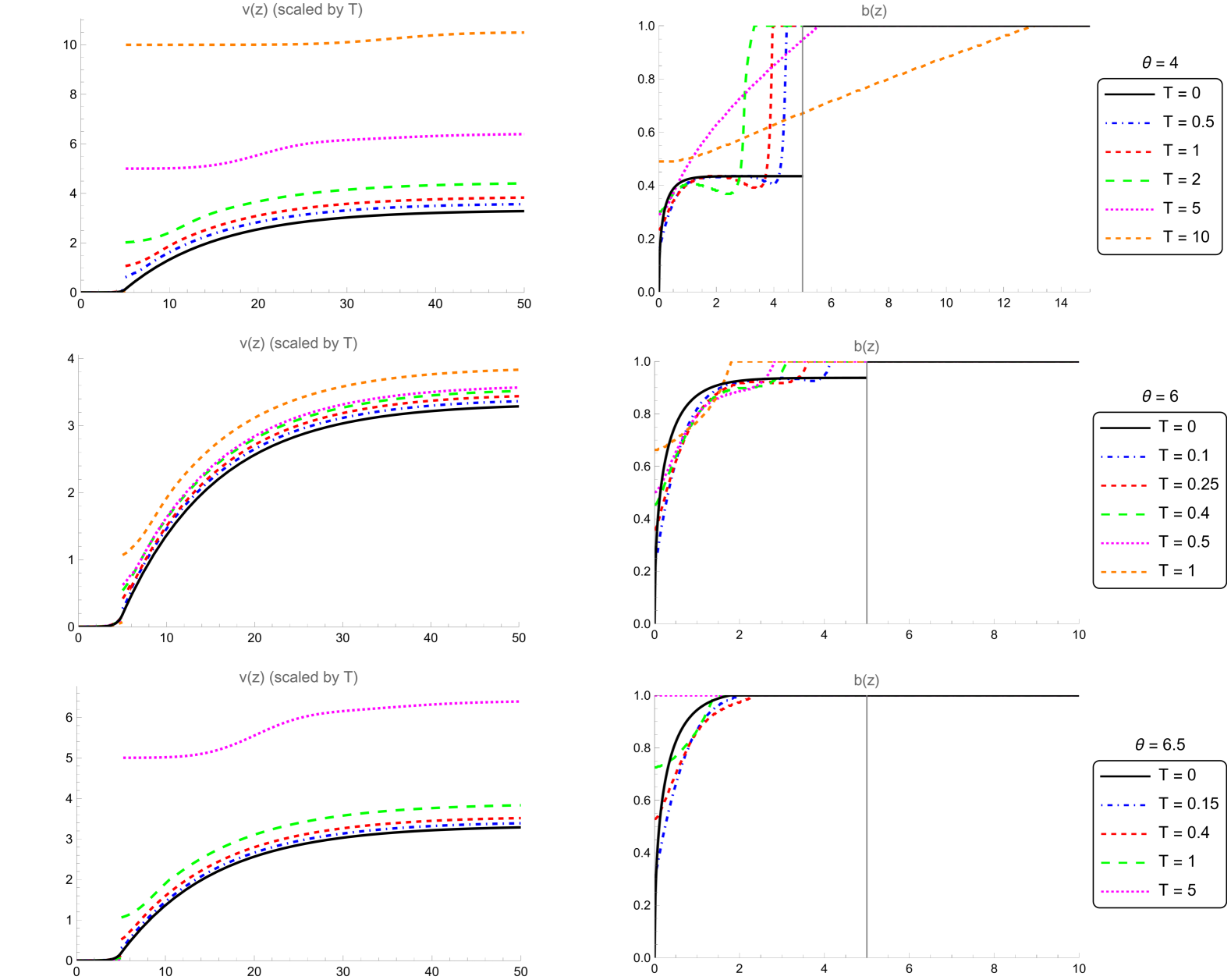

In this case, the drawdown process is inspected at time points for a fixed interarrival time . This is the most intuitive case, where the insurer checks the size of the drawdown at regular intervals (daily, weekly or quarterly, for example).

4.2.1 Rewriting the Dynamic Programming Equation

4.2.2 Description of the Algorithm

We follow a similar approach as in the Poisson case. Let be a sufficiently dense partition of the interval for and one for the interval . Then the approximated version of the dynamic programming equation becomes

for . Note that we need to make sure that is again a grid point or large enough that we can approximate the value function with the upper bound . We therefore construct the grid in the following way: Choose and with . For and set Thus, the sequence forms a grid on the interval . For large enough we can set for . Now one can numerically determine for analogously to the Poisson case.

4.2.3 Numerical Results

The results of the numerical study are illustrated in Figures 3 and 4. As in the Poisson case, we can see in Figure 4 that the value function and the optimal strategy converge to the continuous time case of [1]. Moreover, the retention level is again increasing in the cost of reinsurance (see Figure 3). However, it is not longer increasing in the drawdown size in every scenario considered and the behaviour of the strategy changes significantly for large interarrival times. In particular, buying reinsurance in the critical area is optimal in some cases. This can be explained as follows: In the model considered here, a critical drawdown is only penalized, when it is observed at the deterministic times . If is large, there is more time to reenter the critical area, since we know the next observation time for sure. We can therefore choose a less risky strategy in order to increase the chance reaching the non-critical area before the next observation.

Appendix

Proof of Lemma 4.1.

We can rewrite the exponent as

where

The function

is the density function of the inverse Gaussian distribution with parameters and . The expected value of a random variable is given by . We therefore conclude

and

Since

the third identity follows from the calculations above. ∎

References

- [1] L. V. Brinker and H. Schmidli. Optimal discounted drawdowns in a diffusion approximation under proportional reinsurance. J. Appl. Probab., 59(2):527–540, 2022.

- [2] L. C. G. Rogers and D. Williams. Diffusions, Markov Processes and Martingales, volume 1. Cambridge University Press, Cambridge, 2nd edition, 2000.

- [3] D. Wagner. Survey of measurable selection theorems. SIAM Journal on Control and Optimization, 15:859–903, 1977.