Towards turnpike-based performance analysis of risk-averse stochastic predictive control

Abstract

In this paper, we present performance estimates for stochastic economic MPC schemes with risk-averse cost formulations. For MPC algorithms with costs given by the expectation of stage cost evaluated in random variables, it was recently shown that the guaranteed near-optimal performance of abstract MPC in random variables coincides with its implementable variant coincide using measure path-wise feedback. In general, this property does not extend to costs formulated in terms of risk measures. However, through a turnpike-based analysis, this paper demonstrates that for a particular class of risk measures, this result can still be leveraged to formulate an implementable risk-averse MPC scheme, resulting in near-optimal averaged performance.

I Introduction

In optimal control and model predictive control (MPC), risk can be considered in two fundamentally different ways: by relaxing inequality constraints to hold with a given probability or by ensuring that unlikely outcomes do not lead to arbitrary bad performance. While both risk concepts appears in stochastic MPC, this paper is concerned with the latter, i.e., we focus on risk-averse objective transformations in stochastic MPC.

When formulating stochastic optimal control problems, one cannot simply evaluate the deterministic objective function with random variable arguments as this will give a random variable. Instead, one has to map random variables to real numbers. The most frequently, used approach is optimization in expectation. However, it is known that risk measures such as, e.g., the averaged value-at-risk, also known as conditional value-at-risk or expected shortfall, are better suited to avoiding rare outcomes with bad performance [12, 18].

Hence, the consideration of risk aware objective transformations has been considered in stochastic optimal control [7, 8, 10, 2]. Moreover, [19] considers stochastic uncertainty of linear systems and an MPC framework employing coherent measures of risk [12, 18], while [20] considers a similar but nonlinear setting.

Considering expected value objectives, we have recently extended dissipativity notions for optimal control problems to the stochastic setting, and we analyzed different kinds of stochastic turnpike notions and their relation to each other [15, 13, 14]. The underlying motivation is that turnpike and dissipativity properties play a crucial role in the analysis of deterministic MPC schemes [6]. Moreover, in [16] we have given novel performance estimates for stochastic MPC. Yet, all of our above works do not take into account risk aware objective formulations.

Hence, in this work, we analyze the performance of risk-aware stochastic MPC. In particular, we derive conditions under which a risk-aware abstract MPC in random variables delivers performance close to the optimal performance of a stationary process. To this end and similar to [3, 17, 7] we rely on parametrized risk measures.

II Setting and preliminaries

II-A Problem formulation

We consider discrete-time stochastic system

| (1) |

defined by a continuous function

Here , , and are Borel spaces and the initial condition , the states , the controls as well as the noise are random variables on the probability space for all , where

Furthermore, is independent of and for all and the sequence is i.i.d. with known distribution .

Additionally, we assume that the control process is measurable with respect to the natural filtration , i.e.

| (2) |

for all . This condition can be seen as a causality requirement, formalizing that we do not use information about the future noise and only the information contained in about the past noise when deciding about our control values. For more details on stochastic filtrations we refer to [5, 11].

We call a control sequence that satisfies (2) admissible and denote the set of all admissible control sequences for the initial value on horizon by . For a given initial value and control sequence , we denote the solution of system (1) by , or short by if the initial value and the control are unambiguous. Note, that the solution also depends on the disturbance . However, for the sake of readability, we do not highlight this in our notation and assume in the following that is an arbitrary but fixed stochastic process.

Moving from the stochastic dynamics (1) to optimal control problem, we consider the stage cost

where is a continuous function bounded from below and is a mapping of random variables from a linear space to the real values.

Then, the stochastic optimal control problem under consideration reads

| (3) |

By we denote the optimal value function of the optimal control problem (3) and if a minimizer of this problem exists we will denote it by or if we want to emphasize the dependence on the initial condition.

Moreover, in order to guarantee well-posedness of problem (3) and finiteness of the optimal value function for finite , we assume the initial values — and thus the whole optimal trajectory — to lie in the constraint set

For instance, if we consider the generalized linear-quadratic problem from [14] with we get .

II-B Fundamentals of risk-measures

A common choice for the mapping in (3) is the expected value . However, as risk measures are widely used as optimization criteria in various risk-averse applications (see the references in the introduction), in this paper we consider more general mappings , as defined next.

Definition 1 (Risk measures)

Let be a linear space of measurable functions , where is a probability space. A function is called risk measure if it is

-

(i)

monotone, i.e. for all it holds that

-

(ii)

translative, i.e. for all and it holds that

Remark 2

In our definition of a risk measure we associate high values of the random variable with a high risk . While in insurance mathematics the same concept is used, in financial mathematics the common choice would be to associate low values of with a high risk . However, the two definitions are easily transformed into each other as .

While an arbitrary risk measure only has to satisfy the conditions of Definition 3, there are several additional properties for risk measures, which can be useful under certain circumstances. Especially, law-invariance will be necessary for our later investigations.

Definition 3

A risk measure satisfying Definition 1 is called

-

(i)

convex if for all , ;

-

(ii)

positive homogeneous if for all and ;

-

(iii)

coherent if it is convex and positive homogeneous;

-

(iv)

law-invariant if holds for all with .

For coherent risk measures, the robust representation theorem, cf. [4], can be used to represent them in terms of expectations as

| (4) |

for some set of probability measures which are absolutely continuous to . However, using this representation can be challenging in applications since one has to take the supremum over probability measures. Thus, for our approach, we consider another special class of risk measures which have been considered in [3, 17] and [7] in an optimal control contexts and which can be written in parametric form.

Definition 4 (parameterized risk measures)

A risk measure according to Definition 1 is called parameterized if there exists a set , and a function such that

| (5) |

Note that for every proper, closed and monotone non-decreasing function , the function

| (6) |

defines a risk measure according to Definition 1 given in parametric form (5). Moreover, if is additionally convex the risk measure (6) is also convex. However, it is in general not positive homogeneous, and thus, not coherent. Several risk measures that are used in practice can be represented in the parametric form (5), as shown in the following examples.

Example 5 (Averaged value-at-risk)

The averaged value-at-risk (also called expected shortfall or conditional value-at-risk, cf. Remark 7 (i)) with confidence-level is a coherent risk measure and can be parametrized as

| (7) |

Example 6 (-divergence risk measures)

Let be the space of probability density functions on and define the -divergence ambiguity set

| (8) |

where is a convex lower semicontinuous function with and for . Then, the coherent risk measure corresponding to with constraint-level is given by and by duality arguments this risk measure can be written in parametric form (5) as

| (9) |

where is the Legendre-Fenchel conjugate of . In particular, by choosing as the Kullback-Leibler-divergence for and for we obtain the risk measure

| (10) |

Remark 7

-

(i)

While expected shortfall is used as a synonym for averaged value-at-risk, the term conditional value-at-risk is used ambiguously in the literature. Depending on the reference, it is either used again as a synonym for averaged value-at-risk, cf. [12], or as another name for tail conditional expectation. While these two concepts coincide for continuous random variables, this is in general not the case for discrete ones, cf. [1].

- (ii)

II-C Turnpike properties in stochastic optimal control

Our analysis in Section III will be based on recently developed turnpike properties for stochastic optimal control problems, see [15, 13, 14], which we recall in the following. While in deterministic settings the turnpike is usually an equilibrium of the system, in stochastic settings this is not possible due to the persistent excitation of the system (1) by the noise. Thus, we make the following definition of a stationary solution of system (3).

Definition 8 (Stationary stochastic processes)

A pair of the stochastic processes given by

| (11) |

with is called stationary for system (1) if there exist probability distributions , , and with

for all .

The next definition formalizes the turnpike property of stochastic optimal control problem (3) where the turnpike is defined as a stationary solution from Definition 8. Note that this definition is equivalent to the definition used in [13], if we set and considering only optimal trajectories instead of near stationary solutions.

Definition 9 (Random variable turnpike)

Consider a stationary pair , a pseudometric on the space and a set . We say that the optimal control problem (3) has

-

(i)

a stochastic finite horizon turnpike property on if there exists such that for each optimal trajectory with and all there is a set with elements and

for all ;

-

(ii)

a stochastic infinite horizon turnpike property on if there exists and such that for each optimal trajectory with and all there is a set with elements and

for all .

Definition 10 (Types of stochastic turnpike properties)

Assume that the optimal control problem has a stochastic turnpike property according to definition 9. Then we say that it has

-

(i)

the turnpike property if is the -norm, i.e.

-

(ii)

the pathwise-in-probability turnpike property if is the Ky-Fan metric, i.e.

-

(iii)

the distributional turnpike property if is a metric on the space of probability measures , or more precisely

-

(a)

the Wasserstein turnpike property of order if is the Wasserstein distance of order , i.e

-

(b)

the weak distributional turnpike property if is the Lévy-Prokhorov metric, i.e.

-

(a)

-

(iv)

the -th moment turnpike property if

Example 11

Consider the stochastic optimal control problem

| (12) |

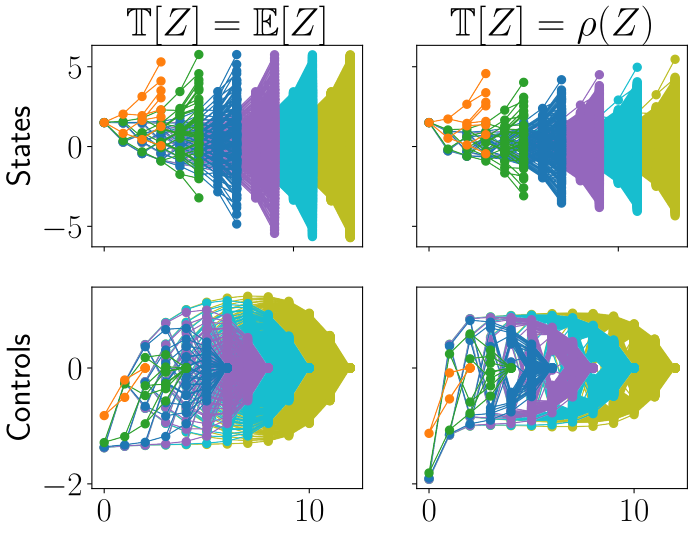

where follows a two-point distribution such that with probability and with probability . For this corresponds to a standard stochastic linear-quadratic problem and for this problem it was already shown analytically and numerically that the problem exhibits stochastic turnpike properties in various forms, cf. [16, 9]. The optimal trajectories of problem (12) with for horizons and are shown in the left column of Figure 1. If, instead, we consider a risk measure as the mapping , then we can still observe stochastic turnpike properties as shown in the right column of Figure 1 for the averaged value-at-risk from equation (8) of Example 5 with confidence-level . Here, for numerical purpose we used the softplus function in the simulations instead of the function in (8). Note that usage of the softplus leads to an approximation of the averaged value-at-risk but can also be interpreted as a risk measure on its own sake due to equation (6) with . The results from Figure 1 show that although we can observe the same qualitative behavior for the expectation and the risk measure used in the cost, the overall width of the possible paths for the state trajectories is smaller if we use the risk-averse formulation rather than the expectation.

Example 12

Consider the stochastic optimal control problem

| (13) |

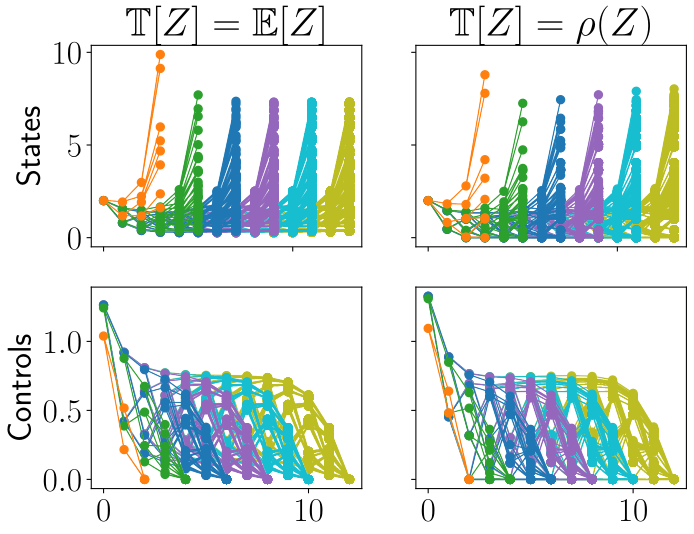

where is a regularization parameter and follows a two-point distribution such that with probability and with probability . For this is a slight modification of the example in Section V of [16], where it was shown numerically that the problem exhibits stochastic turnpike phenomena for . Moreover, for it was shown analytically in [13] that the problem has all the stochastic turnpike properties in Definition 10. For and , where is the Kullback-Leibler divergence from equation (10) of Example 6 with constraint level , the state and control trajectories on horizons with and are shown in Figure 2. We can again observe stochastic turnpike properties if we chose a risk measure as the mapping in (13). Moreover, we can observe that the qualitative behavior of the solutions remains the same for or . However, the usage of the risk measure in the costs seems to lead to a consolidation of the paths such that high values for the states are less likely.

III Risk-averse stochastic MPC

In this section, we aim to derive a risk-averse stochastic MPC algorithm that can also be implemented using measurements from a real plant. To this end, we start with Algorithm 1, which implements a deterministic MPC algorithm for the stochastic problem formulated as a deterministic problem on the space of random variables .

Algorithm 1 is useful for theoretical analysis, since we can transfer the proof ideas from the deterministic setting to the stochastic one. Yet, it requires knowledge of the complete random variables, or at least their distributions. However, in an implementation with a real plant, one cannot measure the random variable , but only a realization thereof, i.e. a step of a single path drawn randomly from all possible paths. Thus, an implementable version of Algorithm 1, which is given by Algorithm 2, would use the measured realization as initialization in each iteration instead of the random variable.

The following Theorem, which is [16, Corollary 7], shows that the closed-loop performance

coincides for the two algorithms if one uses the expected value as the mapping in (3).

Theorem 13

Unfortunately, if we choose a mapping in (3) that is different from the expected value, the result of Theorem 13 is, in general, no longer valid. The reason for this is that a general map will in general not fulfill the tower property of conditional expectations, which is crucial for proving Theorem 13. Therefore, although for general we can still analyze the performance of the abstract Algorithm 1, we cannot transfer these performance bounds to the implementable Algorithm 2. However, if we consider a parameterized risk measure, cf. Definition 4, we can fix the parameter and consider the stage costs , for which by optimality we get

for all and to which we can apply Theorem 13. To formalize this, we make the following assumption.

Assumption 14

The mapping from (3) is a law-invariant parameterized risk measure with such that is bounded from below for all and is continuous in uniformly in , i.e. for all there exists such that holds for all and .

Under Assumption 14 we can replace the original optimal control problem (3) by the optimal control problem

| (14) |

in each iteration of Algorithm 2. This way we obtain Algorithm 3, where in Step 2.) an upper bound of the original problem is minimized and the performance again coincides with the abstract version of this algorithm.

Since the cost in (14) does now satisfies the assumptions from [16] we can use the results from there to bound the performance of the MPC Algorithm 3. For this, we have to make the following assumptions, where we define the distributional ball around a stationary process with respect to a metric on the space of probability measures as in Definition 10 (iii) as

Note that we use the notation since implies for all since holds for all . Furthermore, due to the stationarity of we also write instead of for law-invariant stage costs and to ensure that in addition to the stage costs also the costs are finite we consider the constraint set

Assumption 15

Consider the stochastic optimal control problem (14) for some fixed , a metric on the space of probability measures and a stationary pair with . Then, we assume that the following properties hold:

-

(i)

There exists a set and some such that for the closed-loop trajectory generated by Algorithm 3 it holds that for all , , and .

-

(ii)

The optimal control problem is optimally operated at according to [16, Definition 10].

-

(iii)

The optimal control problem has the finite and infinite distributional turnpike property from Definition 10 (iii) at on with respect to the metric .

- (iv)

However, since these performance bounds are computed with respect to the new cost , it is not immediately clear how well the closed-loop solution of Algorithm 3 performs with respect to the original cost . So in the following we will analyze the performance of Algorithm 3 with respect to the original cost and show how we can achieve averaged performance optimality by making an appropriate choice of the parameter in problem (14). In order to this, we make the following additional assumption on the original stochastic optimal control problem (3).

Assumption 16

The original stochastic optimal control problem (3) is optimally operated at a stationary pair , i.e.

holds for all and .

Now we can show the following result regarding the averaged closed-loop performance with respect to the original cost for the solution from Algorithm 3

for arbitrary satisfying Assumption 15.

Theorem 17

Proof:

Since is constant it follows immediately by Assumption 16 that

holds for all and , and thus, in particular . Moreover, by [16, Theorem 20] we know that

holds for all with . Moreover, by the optimal operation from Assumption 15 (ii) and the continuity of we get there is an such that

which shows the claim since holds due to the choice of from (15). ∎

Remark 18

- 1.

- 2.

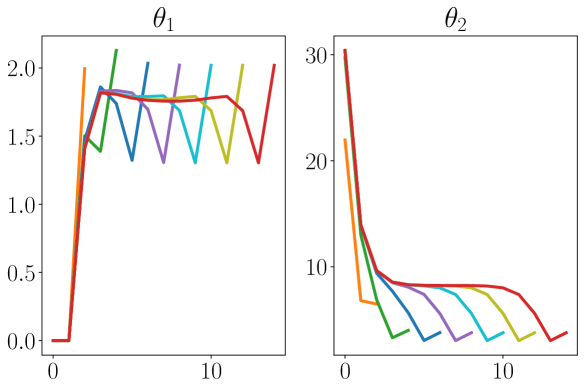

Theorem 17 shows that we can achieve near-optimality of averaged performance for the original cost criterion using Algorithm 3, and that the distance to optimality is determined by the optimization horizon and by how well the fixed parameter fits the optimal stationary one from equation (15). Thus, our results show that switching from the expectation-based setting in [16] to the risk-averse setting considered in this paper extends the problem by a parameter-fitting component. In the following we will illustrate this result numerically. For this purpose we first consider the risk-averse setting from Example 12. Since equation (15) is difficult to solve, both analytically and numerically, we use the observations from Figure 3 to approximate the optimal stationary parameter . Here, we can clearly see that in addition to the optimal states and controls, cf. Figure 1, also the parameters realizing the optimal cost exhibit a turnpike property. Thus, we can approximate and the optimal stage cost by the values at the middle of the horizon where we are near the turnpike.

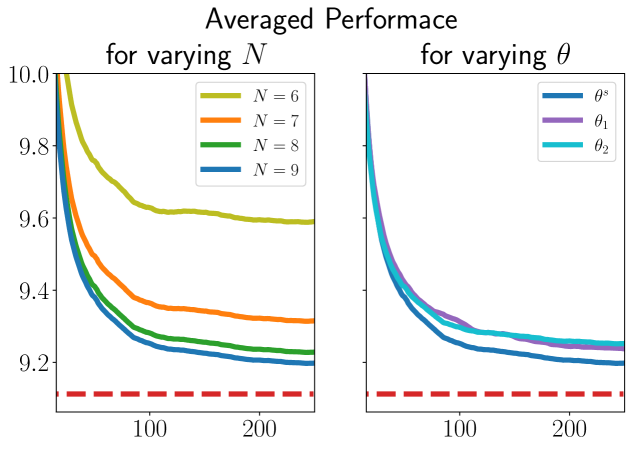

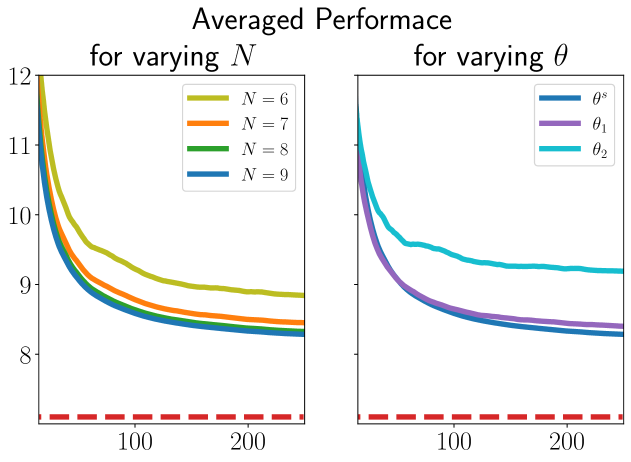

The averaged performance results for different time horizons and parameter in Algorithm 3 are shown in Figure 4. In addition, Figure 4 also shows the performance results for fixed horizon and different choices of the parameter with and . It is clearly observable that an increasing time horizon leads to a better average performance and that a deviation from the optimal stationary parameter leads to a poorer performance, which is in line with Theorem 17. Moreover, we can see that the time horizon seems to have a much larger impact on the performance than the parameter , which suggests that our approach is not too sensitive regarding a error in the parameter estimation, at least for this example.

To further illustrate our theoretical findings, we implemented the MPC Algorithm 3 for the setting of Example 11. Again, we approximated the stationary optimal parameter and the corresponding optimal stationary cost by the turnpike. The obtained averaged performance results for varying horizons with fixed parameter and varying with , and fixed are shown in Figure 5. We can observe that an increasing horizon leads to a better performance and a deviation from the parameter worsens the performance. However, in contrast to Figure 4, we can see that for a too large deviation from the optimal parameter the performance significantly deteriorates. This shows that the parameter estimation is not negligible, although the sensitivity with respect to the parameter is again not too large.

IV Conclusion

We presented a risk-averse stochastic MPC algorithm with near-optimal averaged performance guarantees. Our results are based on the observation that for parameterized risk measures, we can transfer results for stochastic MPC schemes with expected costs by fixing a certain parameter in the cost formulation. The upper bound on the averaged performance then depends on how well this parameter matches an optimal one. Further research should focus on analyzing the non-averaged performance and stability properties of the proposed algorithm. Furthermore, a useful extension for our algorithm would be to develop an adaptivity such that the fixed parameter is tuned automatically during the MPC loop and does not need to be calculated offline in advance.

References

- [1] C. Acerbi. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking & Finance, 26(7):1505–1518, 2002.

- [2] M. Ahmadi, U. Rosolia, M. D. Ingham, R. M. Murray, and A. D. Ames. Risk-averse decision making under uncertainty. IEEE Transactions on Automatic Control, 69(1):55–68, 2023.

- [3] A. Ben-Tal and M. Teboulle. Penalty functions and duality in stochastic programming via -divergence functionals. Mathematics of Operations Research, 12(2):224–240, 1987.

- [4] H. Föllmer and A. Schied. Stochastic finance: an introduction in discrete time. Walter de Gruyter, 2011.

- [5] B. Fristedt and L. Gray. A Modern Approach to Probability Theory. Birkhäuser Boston, 1997.

- [6] L. Grüne. Dissipativity and optimal control: Examining the turnpike phenomenon. IEEE Control Systems Magazine, 42(2):74–87, 2022.

- [7] V. Guigues, A. Shapiro, and Y. Cheng. Risk-averse stochastic optimal control: An efficiently computable statistical upper bound. Operations Research Letters, 51(4):393–400, 2023.

- [8] J. Isohätälä and W. B. Haskell. Risk aware minimum principle for optimal control of stochastic differential equations. IEEE Transactions on Automatic Control, 67(10):5102–5117, 2021.

- [9] R. Ou, M. H. Baumann, L. Grüne, and T. Faulwasser. A simulation study on turnpikes in stochastic LQ optimal control. IFAC-PapersOnLine, 54(3):516–521, 2021.

- [10] A. Pichler and R. Schlotter. Risk-averse optimal control in continuous time by nesting risk measures. Mathematics of Operations Research, 48(3):1657–1678, 2023.

- [11] P. E. Protter. Stochastic Integration and Differential Equations. Springer Berlin Heidelberg, 2005.

- [12] R. T. Rockafellar. Coherent approaches to risk in optimization under uncertainty. In OR Tools and Applications: Glimpses of Future Technologies, pages 38–61. Informs, 2007.

- [13] J. Schießl, M. H. Baumann, T. Faulwasser, and L. Grüne. On the relationship between stochastic turnpike and dissipativity notions. IEEE Transactions on Automatic Control, 2024.

- [14] J. Schießl, R. Ou, T. Faulwasser, M. H. Baumann, and L. Grüne. Turnpike and dissipativity in generalized discrete-time stochastic linear-quadratic optimal control. SIAM Journal on Control and Optimization (accepted), 2024.

- [15] J. Schießl, R. Ou, T. Faulwasser, M. H. Baumann, and L. Grüne. Pathwise turnpike and dissipativity results for discrete-time stochastic linear-quadratic optimal control problems. In Proceedings of the 62nd IEEE Conference on Decision and Control (CDC 2023), pages 2790–2795, 2023.

- [16] J. Schießl, R. Ou, T. Faulwasser, M. H. Baumann, and L. Grüne. Near-optimal performance of stochastic econimic mpc. In Proceedings of the 63rd IEEE Conference on Decision and Control (CDC 2024), pages 2565–2571, 2024.

- [17] A. Shapiro. Distributionally robust stochastic programming. SIAM Journal on Optimization, 27(4):2258–2275, 2017.

- [18] A. Shapiro, D. Dentcheva, and A. Ruszczynski. Lectures on stochastic programming: modeling and theory. SIAM, 2021.

- [19] S. Singh, Y. Chow, A. Majumdar, and M. Pavone. A framework for time-consistent, risk-sensitive model predictive control: Theory and algorithms. IEEE Transactions on Automatic Control, 64(7):2905–2912, 2018.

- [20] P. Sopasakis, D. Herceg, A. Bemporad, and P. Patrinos. Risk-averse model predictive control. Automatica, 100:281–288, 2019.