Data-driven Distributionally Robust Control Based on Sinkhorn Ambiguity Sets

Abstract

As the complexity of modern control systems increases, it becomes challenging to derive an accurate model of the uncertainty that affects their dynamics. Wasserstein Distributionally Robust Optimization (DRO) provides a powerful framework for decision-making under distributional uncertainty only using noise samples. However, while the resulting policies inherit strong probabilistic guarantees when the number of samples is sufficiently high, their performance may significantly degrade when only a few data are available. Inspired by recent results from the machine learning community, we introduce an entropic regularization to penalize deviations from a given reference distribution and study data-driven DR control over Sinkhorn ambiguity sets. We show that for finite-horizon control problems, the optimal DR linear policy can be computed via convex programming. By analyzing the relation between the ambiguity set defined in terms of Wasserstein and Sinkhorn discrepancies, we reveal that, as the regularization parameter increases, this optimal policy interpolates between the solution of the Wasserstein DR problem and that of the stochastic problem under the reference distribution. We validate our theoretical findings and the effectiveness of our approach when only scarce data are available on a numerical example.

I Introduction

Standard stochastic optimal control theory relies on the assumption that a precise statistical description of the noise is available. However, in practice, its probability distribution is often observable only through a finite collection of noise samples. While these can be used to approximate the true distribution, such an estimate can be unsatisfactory for control design as it is heavily based on the quality of the collected data and the available prior knowledge of the unknown variables. When poor statistical information about the uncertainty is used to design controllers, one might face unexpected system behaviors with possible catastrophic out-of-sample performance [1, 2, 3].

Motivated by this observation, Distributionally Robust Optimization (DRO) has emerged as a promising paradigm to deal with uncertainty. It considers a minimax stochastic optimization problem over a neighborhood of the nominal distribution defined in terms of a distance in the space of probabilities. In this way, the solution can be robustified against the most averse distribution which is close in some sense to a nominal one, while the degree of conservatism of the underlying optimization can be modulated by adjusting how far the worst distribution can be from the nominal one.

For choosing a proper ambiguity set, one needs to strike a balance between computational tractability and expressivity. In particular, the ambiguity set should be rich enough to cover all relevant distributions, while avoiding pathological distributions that could result in overly conservative decisions.

Several methods have been explored for quantifying the similarity between probability distributions, such as the Kullback–Leibler divergence and the total variation distance [4]. Another possibility is to define the ambiguity set with distributions sharing moment information [5]. Among these, recent literature has highlighted the advantages of using metrics related to optimal transport (OT). In particular, ambiguity sets based on the Wasserstein metric [6] provide great expressiveness along with strong statistical out-of-sample guarantees. Thanks to these properties, Wasserstein ambiguity sets have been employed for designing DR control policies. In [7] the authors introduced a generalization of the finite-horizon LQG problem with noise belonging to a Wasserstein ball centered at a Gaussian nominal distribution. Other works focused on the infinite-horizon of the same problem when the nominal distribution is Gaussian [8] while [9, 10] consider an empirical center. Among other contributions that exploit the Wasserstein metric, [11, 12, 13, 14], and [15] consider the design of tube-based predictive control schemes. More fundamentally, [16] provides exact characterizations of how Wasserstein ambiguity sets propagate through the system dynamics.

Despite such encouraging results, the current Wasserstein DRO framework suffers from the following limitations. First, guaranteeing that the true distribution lies within the Wasserstein ambiguity set with high probability requires choosing a radius that is inversely proportional to the number of available data. If only a few noise samples are available, the corresponding radius may become too large, resulting in overly conservative policies. Second, from a modeling perspective, when the true distribution is continuous, Wasserstein DRO might not capture its nature. In fact, [17] showed that when the nominal distribution has finite support, the worst-case distribution will also be finitely supported.

Motivated by these challenges, this paper makes the following three contributions. First, inspired by recent results in the machine learning and optimization community [18, 19, 20], we use the Sinkhorn discrepancy [21] to define ambiguity sets and accordingly formulate a Sinkhorn DR finite-horizon control problem. Differently from the Wasserstein metric, this allows us to penalize deviations from a reference distribution and thus combine data with prior information about the true distribution. Second, we prove that, despite the additional entropic regularization term in the discrepancy, the Sinkhorn DR linear-quadratic control problem can be expressed as a finite-dimensional convex program when the prior is Gaussian. To do so, we specialize the strong duality result of [22] to the case of quadratic loss function and transportation cost given by the Euclidean norm, and leverage the system level parametrization of linear dynamic controllers [23].

Last, we derive relations between Sinkhorn and Wasserstein ambiguity sets, showing that the Sinkhorn policy interpolates between the solution of the Wasserstein DR optimal control problem and the stochastic problem under the reference distribution. These extremes are recovered when the regularization term vanishes or grows unbounded, respectively. These findings are validated with numerical examples.

Notation. Throughout the paper, given a measurable set , we will denote by the set of probability distributions supported on . We write to denote that a measure is absolutely continuous with respect to . If are two measures, represents the product measure.

Let be the set of indices . The space of all positive semidefinite matrices of size is denoted by . We denote by the Euclidean norm. Given a positive definite matrix , we denote the weighted norm as . The Frobenius norm of a matrix is . The determinant of a square matrix is denoted by . Finally, the notation is short for .

II Problem Formulation and Preliminaries

We consider the discrete-time linear time-varying system

| (1) |

where , for all , where denotes the length of the control horizon. The evolution of (1), starting from the initial condition , is characterized by the vectors , , and . With this notation in place, (1) becomes

| (2) |

where is the block downshift operator, that is, a block matrix with identity matrices in its first block sub-diagonal and zeros elsewhere, , , and .

We denote the cost incurred applying the input sequence in response to the disturbance realization by

| (3) |

where . We also assume that the underlying true noise distribution of denoted by is unknown. Instead, we have access to i.i.d. samples of noise trajectories of length , .

Consequently, following the DRO literature, we formulate a worst-case cost over a family of probability distributions, and we seek to find the best control action to minimize such a cost. This can be explicitly stated as

| (4) |

where is the control objective defined in (3), and is called ambiguity set. It consists of probability distributions that are related in terms of distance or other suitable properties (e.g. moments) to a reference distribution. In this paper, we use as reference distribution the empirical one induced by the collected noise trajectories, that is, .

For tractability of our formulation and motivated by recent works on DR control [7], [24], which showed global optimality of linear policies when the nominal distribution is normal and the Wasserstein distance is used, we restrict ourselves to linear time-varying policies. Thus, we consider control actions given by

or, in a more compact form,

| (5) |

with being a lower block-triangular feedback matrix.

Remark 1 (Initial conditions):

In the paper we consider to be uncertain. This is for example the case of the LQG theory where the initial condition is uncertain and only its mean and covariance are known, see, e.g., [25, Section 5.3]. However, one can also consider the case where the initial state is given. In this setup the maximization in (4) is carried out only with respect to the disturbance sequence as terms related to a constant can be factored out of the expectation.

II-A System level synthesis (SLS)

In this section, we provide the necessary background on the SLS approach to optimal controller synthesis by referring the reader to [23] and [26] for a complete discussion. SLS shifts the synthesis problem from the direct design of the controller to the shaping of closed-loop maps from the exogenous disturbance to the state and input signals.

Using (2) and (5), the closed-loop behavior of the system is characterized by the following noise-to-input and noise-to-state maps:

| (6) | ||||

| (7) |

The maps and are the system responses induced by the controller . We highlight that these operators inherit a block-triangular causal structure. Although (6) and (7) are non-convex in , they are linear functions of . Therefore, the idea is to optimize directly over these maps: to do so, one must show that there exists a controller such that and . From [26, Theorem 3.1] this is true if and only if

| (8) |

we call pairs that satisfy (8) achievable. Moreover, any block-lower-triangular matrices satisfying (8) are achieved by the corresponding controller .

II-B Characterization of the uncertainty

In this section we will describe the types of ambiguity set that are used in the remainder of the paper. We start by presenting some useful definitions.

Definition 1 (Transportation Cost Function):

A lower semi-continuous function that satisfies the identity of indiscernibles (i.e. if and only if ) is a transportation cost function.

Definition 2 (OT discrepancy):

The optimal transport discrepancy associated with any given transportation cost function is defined through

| (9) |

where represents the set of all couplings between and , that is, all joint probability distributions with marginals and .

By adding a regularizer to the previous formulation, one obtains the so-called entropy-regularized OT or Sinkhorn discrepancy.

Definition 3 (Sinkhorn discrepancy):

Consider the probability distributions , and let be reference probability measures over such that and . For a given transport cost and regularization parameter the Sinkhorn discrepancy between and is defined as

| (10) |

where represents the KL divergence of with respect to the product measure :

We note that any possible choice of in (10) is equivalent up to a constant. Since in DRO applications the nominal distribution is known and fixed, without loss of generality, we will choose in the sequel. Note also that the discrepancy coincides with the OT discrepancy in (9). Consequently, if the cost function is defined as the -th power of some metric in the space we retrieve the well-known -th power of the Wasserstein distance between and , e.g. [6, Definition 6.1]. Intuitively, in (10) when the regularization parameter increases there is an additional constraint on how the mass can be transported from to based on the reference measure . In [22], the authors suggest selecting the reference measure as the Gaussian measure if the underlying true distribution is expected to be continuous, while the counting measure if it is discrete.

Inherently, the quantities and measure how different the probability distributions and are. They also naturally provide a definition of uncertainty in the space of probability distributions. Specifically, we define the Sinkhorn ambiguity set, denoted as -set for brevity, of radius and centered at by

Analogously, we can denote the OT ambiguity set with . In words, contains all probability distributions that are close to in the Sinkhorn discrepancy.

III Sinkhorn Distributionally Robust Control

In the following section, we address the finite-horizon DR control problem using the Sinkhorn discrepancy presented in the previous section. We first prove key properties of -sets. Then, we present the main theorem of our work and conclude the section with its proof.

The next proposition relates -sets with different radii, as well as with OT-sets. We defer its proof to Appendix A-A.

Proposition 1:

Let and fix the radius . Then, the following relationships hold:

-

1.

;

-

2.

;

-

3.

If then is the singleton otherwise it is the empty set.

As hinted by point 3 of the above proposition, the -set can be empty. As a consequence, the stochastic program in (4) with -set can become unfeasible. Intuitively, for a large enough regularization parameter the uncertainty set will only contain distributions that are close to the reference while the first term of the distance will tend to have distributions that are close to the center. Therefore, it might be that for some combinations of radius and regularizer the ambiguity set is empty. See Lemma 1 for an exact characterization of these conditions. This is in contrast to the Wasserstein worst-case cost, for which feasibility of (4) is always guaranteed. Indeed, when the radius of the Wasserstein ball diminishes, it eventually shrinks to a singleton containing only the center distribution.

We now shift our attention to the DR control design with Sinkhorn discrepancy. Using the SLS framework presented in the preliminary section, the control cost we seek to minimize is

with being the column concatenation between and . In the setup where the uncertainty set in (4) is , and the objective function is , the problem we want to solve is finding the optimal map given by

| (11) |

while satisfying the achievability constraints in (8). The inner maximization in (11) is computationally difficult to solve, since it involves an optimization over a possibly infinite number of distributions. The following theorem reformulates this problem into a finite convex program that can be solved with off-the-shelf numerical optimization solvers. Our result explicitly accounts for the entropic regularization term introduced by the Sinkhorn discrepancy in (10) and recovers previously known results for Wasserstein DR control [9] when .

Theorem 1:

Assume and . Let and the reference measure be a multidimensional Gaussian distribution111Our results can in principle be extended to any reference distribution satisfying Assumption LABEL:*assumption (i)-(ii). Exact reformulations of (11), however, require case-by-case computations. with mean vector and covariance matrix , that is

with the usual -dimensional Lebesgue measure and . Then, problem (11) is feasible if and only if

| (12) |

Moreover, the optimal closed-loop map in (11) is given by the minimizer of

| (13a) | |||

| (13b) | |||

| (13c) | |||

| (13d) | |||

Before presenting the proof, we formulate a proposition stating that the optimization problem in (13) is convex. In fact, the objective function is linear in the optimization variables; therefore, (13) is a convex program if and only if its feasible set is convex. We report the proof of this proposition in Appendix A-B.

Proposition 2:

Consider the optimization problem in (13). The constraints are convex sets in the optimization variables .

Note that (13), due to the nonlinear constraint (13b), is a conic problem when . This is in contrast with the Wasserstein counterpart of (13), which is a tractable semidefinite program [1]. This additional complexity is needed to incorporate priors in the synthesis process through an entropic regularization with respect to a reference distribution.

III-A Auxiliary results and proof of the main theorem

Next, we present the technical results that will allow us to give the proof of the main theorem at the end of this section. We start by recalling a strong duality result first proved in [22]. Given a loss function , the following worst-case risk

| (14) |

admits the strong dual reformulation

| (15) |

under the following assumption:

Assumption 1:

The reference measure , the transport cost , the function , and the joint distribution satisfy:

-

(i)

for -almost every ;

-

(ii)

for -almost every ;

-

(iii)

the function is measurable;

-

(iv)

For every joint distribution on with first marginal distribution , it has a regular conditional distribution222We refer to [27, Chapter 5] for the concept of regular conditional distribution. given the value of the first marginal equals .

Remark 2:

It can be shown that the worst-case distribution shares the same support as the measure . When the true distribution is known to be continuous, choosing as a continuous measure in can reduce conservatism with respect to Wasserstein DR control. This is because the worst-case distribution in Wasserstein DRO problems is always finitely supported on at most points when the center is the empirical distribution over points [17].

Motivated by control applications, the following lemma tailors (15) to the case of quadratic transport costs and loss functions. The proof can be found in Appendix A-C.

Lemma 1 (Strong dual reformulation for quadratic loss and transport cost):

Remark 3 (Comparison with Wasserstein DRO):

Finally, we present the proof of Theorem 1.

-

Proof:

We apply Lemma 1 with and . The feasibility condition (12) was already proved in Lemma 1. We then focus on deriving (13). We first introduce the auxiliary variables , for to upper bound the linear part of the constraint in (16). This directly yields the constraint (13b). We then consider the remaining linear part of the constraint

Applying the Schur’s complement to the constraint above we obtain (13c). We are left with enforcing . The inequality

can be equivalently reformulated as in (13d) via Schur’s complement. In contrast, the reverse inequality

does not yield a convex constraint on . Importantly, we show that imposing this reverse inequality is not necessary to ensure the optimality of the resulting closed-loop map . To show this, let us define the optimization problem in (13) as and the same problem with the additional constraint as . Since has a larger feasible set, its solution can be smaller than that of . We show that this is not the case.

Assume to be optimal for with the optimal cost given by . We can construct a candidate solution for as . This satisfies the equality constraint by design. Note also that it has the same cost since the latter depends only on and . Therefore, if such a candidate point is feasible, it is also optimal.

To show feasibility, let us further define . By construction, . We proceed to verify that (13b) and (13c) are satisfied also with . Since the logarithm is a monotone function and given that implies , we deduce thatHence, (13b) is verified when using . By using a similar reasoning for the term one obtains , which implies that (13c) is also verified. Hence, is a feasible solution and the proof is concluded. ∎

IV Numerical Results

We now numerically validate the theoretical results of Proposition 1 and showcase the effectiveness of using the Sinkhorn discrepancy when only a few uncertainty samples are available for control design. In the experiments, we consider a discrete-time stochastic mass–spring-damper system described by the linear dynamics:

with mass , spring and damping constants and , respectively, and sampling time .333All our experiments were run on a M3 Pro CPU machine with 36GB RAM. All SDP problems are modeled in Matlab 2023a using Yalmip and solved with MOSEK, [28]. Our source code is publicly available at https://github.com/DecodEPFL/Sinkhorn_DRC.git.

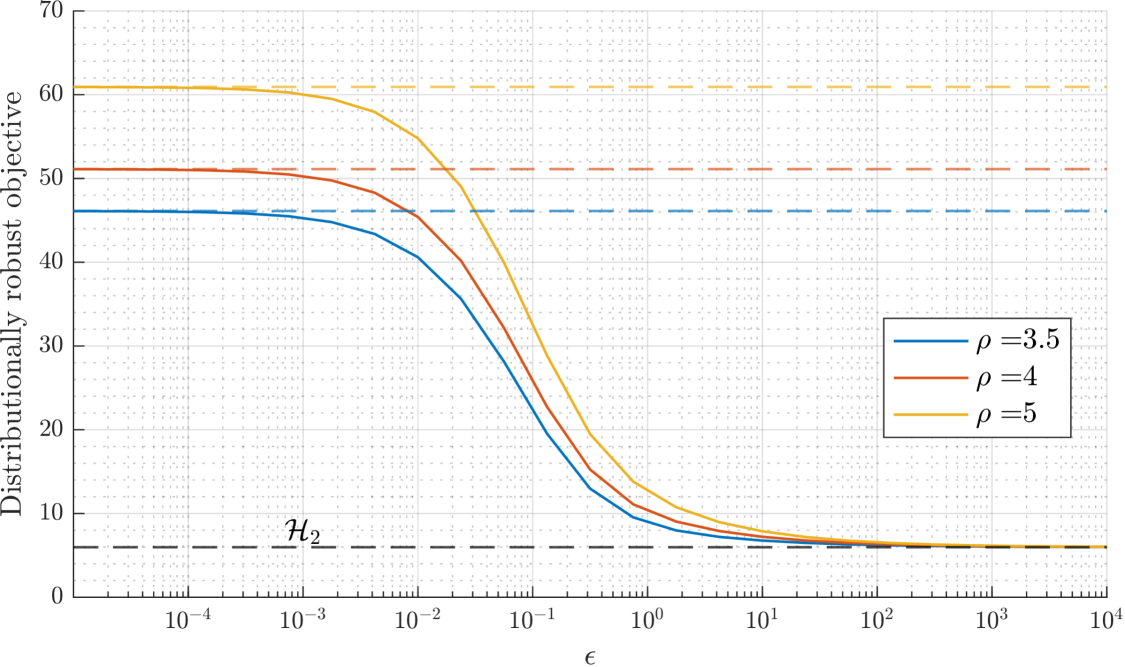

1) Validity of points 1-3 of Proposition 1. In our first test, we synthesize robust controllers starting from a batch of sampled noise trajectories, and we verify the relationships of the proposition. Specifically, we select different values of regularizer and corresponding values of radii ensuring the feasibility of the problem. We compare the behavior of the Sinkhorn worst-case cost with the Wasserstein counterpart. The noise samples are taken from a Gaussian distribution with zero mean and covariance matrix . The considered horizon length is . The selected radii ensuring feasibility are . The reference measure in Theorem 1 was chosen as a multidimensional normal with zero mean and covariance matrix .

In Figure 1 we can see that, as expected, the worst-case costs between Wasserstein and Sinkhorn coincide when the regularization parameter tends to zero. Indeed, we can see that for each value of radius the solid and dashed lines overlap for small regularizer. Furthermore, we also see that the Sinkhorn worst-case cost is a monotonically decreasing function of . Again, this is expected from the proposition, since the -set shrinks with and the worst-case cost can be just smaller or equal over a smaller ball. Finally, also the third point of the Lemma is verified given that for each possible value of radius the Sinkhorn worst-case cost converges to a value that corresponds to the controller cost. Indeed, if the problem is feasible, the Sinkhorn ambiguity set converges to a singleton containing only the reference measure which is Gaussian.

2) Advantages of Sinkhorn DR control. In this second test, we show the advantages of using the Sinkhorn discrepancy to describe the uncertainty in the samples. In particular, we envision our approach to be beneficial when the number of samples to build the ambiguity set is limited. Indeed, in such scenarios, the introduction of the regularizer represents a sort of prior on the true distribution. To show this, we consider only noise trajectories extracted from a Gaussian distribution with zero mean and covariance matrix, horizon , and radii . The selected regularization parameters are . We also consider the reference measure used in the previous experiment. In this setup, we compute the optimal maps by solving DR optimal control problems with Wasserstein and Sinkhorn ambiguity sets for the different radii and regularizers along with the nominal and maps. We then compare the performance of such control schemes when the noise is generated by the true distribution. To do so, we compute which, since the control objective is quadratic, is equivalent to with being the variance of the noise under . The results obtained are reported in Table I for radii and . We can see that DR approaches are beneficial since both Sinkhorn and Wasserstein obtain a cost which is smaller than the nominal one of which exploits only the limited number of samples. In addition, Sinkhorn performs better than Wasserstein since it exploits the prior information encapsulated in the reference and not just the noise samples. This is the case even though the prior was chosen not exactly as the underlying true distribution. For completeness, we also computed the cost we would have incurred if the distribution were known, i.e. the controller cost, which is . This value is obviously smaller than those appearing in Table I since it assumes perfect knowledge of the disturbance distribution. However, the value is not significantly smaller than those obtained with the robust approaches.

| Controller type |

|

|

|

Wasserstein | ||||||

| Cost, | 10.91 | 10.87 | 10.18 | 11.03 | ||||||

| Cost, | 10.77 | 10.76 | 10.67 | 10.80 |

V Conclusion

We have presented a novel method to design DR policies for finite-horizon control using the Sinkhorn discrepancy. To do so, we first leveraged a strong duality result and combined it with the SLS framework. We have shown that the optimization problem to find the optimal map is convex and can be solved with standard tools. We have also framed our approach in the literature of DR control, showing the relationship between ambiguity sets. The numerical results show the validity of our findings. Future work encompasses extensions to infinite-horizon control problems, as well as optimal control with state and input constraints.

References

- [1] D. Kuhn, P. M. Esfahani, V. A. Nguyen, and S. Shafieezadeh-Abadeh, “Wasserstein distributionally robust optimization: Theory and applications in machine learning,” in Operations research & management science in the age of analytics. Informs, 2019, pp. 130–166.

- [2] P. Mohajerin Esfahani and D. Kuhn, “Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations,” Mathematical Programming, vol. 171, no. 1, pp. 115–166, 2018.

- [3] S. Shafieezadeh-Abadeh, L. Aolaritei, F. Dörfler, and D. Kuhn, “New perspectives on regularization and computation in optimal transport-based distributionally robust optimization,” arXiv preprint arXiv:2303.03900, 2023.

- [4] A. L. Gibbs and F. E. Su, “On choosing and bounding probability metrics,” International statistical review, vol. 70, no. 3, pp. 419–435, 2002.

- [5] B. P. Van Parys, D. Kuhn, P. J. Goulart, and M. Morari, “Distributionally robust control of constrained stochastic systems,” IEEE Transactions on Automatic Control, vol. 61, no. 2, pp. 430–442, 2015.

- [6] C. Villani et al., Optimal transport: old and new. Springer, 2009, vol. 338.

- [7] B. Taskesen, D. Iancu, Ç. Koçyiğit, and D. Kuhn, “Distributionally robust linear quadratic control,” Advances in Neural Information Processing Systems, vol. 36, 2024.

- [8] J. Hajar, T. Kargin, V. Malik, and B. Hassibi, “The distributionally robust infinite-horizon LQR,” arXiv preprint arXiv:2408.06230, 2024.

- [9] J.-S. Brouillon, A. Martin, J. Lygeros, F. Dörfler, and G. F. Trecate, “Distributionally robust infinite-horizon control: from a pool of samples to the design of dependable controllers,” arXiv preprint arXiv:2312.07324, 2023.

- [10] K. Kim and I. Yang, “Distributional robustness in minimax linear quadratic control with Wasserstein distance,” SIAM Journal on Control and Optimization, vol. 61, no. 2, pp. 458–483, 2023.

- [11] L. Aolaritei, M. Fochesato, J. Lygeros, and F. Dörfler, “Wasserstein tube MPC with exact uncertainty propagation,” in 2023 62nd IEEE Conference on Decision and Control (CDC). IEEE, 2023, pp. 2036–2041.

- [12] M. Fochesato and J. Lygeros, “Data-driven distributionally robust bounds for stochastic model predictive control,” in 2022 IEEE 61st Conference on Decision and Control (CDC). IEEE, 2022, pp. 3611–3616.

- [13] C. Mark and S. Liu, “Stochastic MPC with distributionally robust chance constraints,” IFAC-PapersOnLine, vol. 53, no. 2, pp. 7136–7141, 2020.

- [14] F. Micheli, T. Summers, and J. Lygeros, “Data-driven distributionally robust MPC for systems with uncertain dynamics,” in 2022 IEEE 61st Conference on Decision and Control (CDC). IEEE, 2022, pp. 4788–4793.

- [15] J. Coulson, J. Lygeros, and F. Dörfler, “Distributionally robust chance constrained data-enabled predictive control,” IEEE Transactions on Automatic Control, vol. 67, no. 7, pp. 3289–3304, 2021.

- [16] L. Aolaritei, N. Lanzetti, H. Chen, and F. Dörfler, “Distributional uncertainty propagation via optimal transport,” arXiv preprint arXiv:2205.00343, 2022.

- [17] R. Gao and A. Kleywegt, “Distributionally robust stochastic optimization with Wasserstein distance,” Mathematics of Operations Research, vol. 48, no. 2, pp. 603–655, 2023.

- [18] W. Azizian, F. Iutzeler, and J. Malick, “Regularization for Wasserstein distributionally robust optimization,” ESAIM: Control, Optimisation and Calculus of Variations, vol. 29, p. 33, 2023.

- [19] J. Blanchet, D. Kuhn, J. Li, and B. Taskesen, “Unifying distributionally robust optimization via optimal transport theory,” arXiv preprint arXiv:2308.05414, 2023.

- [20] C. Dapogny, F. Iutzeler, A. Meda, and B. Thibert, “Entropy-regularized Wasserstein distributionally robust shape and topology optimization,” Structural and Multidisciplinary Optimization, vol. 66, no. 3, p. 42, 2023.

- [21] M. Cuturi, “Sinkhorn distances: Lightspeed computation of optimal transport,” Advances in neural information processing systems, vol. 26, 2013.

- [22] J. Wang, R. Gao, and Y. Xie, “Sinkhorn Distributionally Robust Optimization,” arXiv preprint arXiv:2109.11926, 2021.

- [23] Y.-S. Wang, N. Matni, and J. C. Doyle, “A system-level approach to controller synthesis,” IEEE Transactions on Automatic Control, vol. 64, no. 10, pp. 4079–4093, 2019.

- [24] N. Lanzetti, A. Terpin, and F. Dörfler, “Optimality of linear policies for distributionally robust linear quadratic gaussian regulator with stationary distributions,” arXiv preprint arXiv:2410.22826, 2024.

- [25] R. F. Stengel, Optimal control and estimation. Courier Corporation, 1994.

- [26] J. Anderson, J. C. Doyle, S. H. Low, and N. Matni, “System level synthesis,” Annual Reviews in Control, vol. 47, pp. 364–393, 2019.

- [27] O. Kallenberg, Foundations of modern probability, 2nd ed. Springer-Verlag, New York, 2002.

- [28] M. ApS, The MOSEK optimization toolbox for MATLAB manual. Version 10.2., 2024. [Online]. Available: http://docs.mosek.com/10.2/toolbox/index.html

- [29] S. Boyd and L. Vandenberghe, Convex optimization. Cambridge university press, 2004.

Appendix A Proofs

A-A Proof of Proposition 1

We start by proving the first point of the lemma.

where in (A-A) we have rewritten the logarithm by inverting its argument; the logarithm is concave therefore inequality (A-A) comes from a trivial generalization of Jensen’s inequality, i.e. given with convex it holds ; finally (A-A) follows since and are probability measures and therefore they integrate to one.

Then, for , given any such that it holds that . This in turn implies .

We continue showing the second point. Consider the Sinkhorn discrepancy in (10) and notice that the KL divergence is nonnegative. Therefore

Since the infimum preserves monoticity, we can conclude that for all . This in turn implies .

Finally, for the third point, when the regularization parameter tends to infinity, is finite if and only if the KL divergence term is identically zero. Therefore,

and the last expression is zero if and only if both terms are zero given that they are KL divergences, hence non-negative. Therefore, from the second one we get that and from the first one that . We can conclude that is either the singleton or the empty set. This depends on whether the condition is satisfied or not.

A-B Proof of Proposition 2

Since (13a), (13c) , and (13d) are linear matrix inequalities and the achievability constraint on is affine, they are all convex constraints. We therefore focus only on the non-linear constraint (13b). This constraint is linear in and . We proceed to show that the non-linear part of (13b) is jointly convex in for every . To do so, we define the functions and as follows:

Since the log-determinant of a matrix is a concave function [29], is convex in . Similarly, is affine and therefore convex in . Hence, the function given by

is convex, since it represents the composition of an affine and a convex function. We then note that the non-linear part of (13b) can be rewritten as

and that is the perspective of the function , see [29, Section 3.2.6]. Since the perspective of a convex function is also convex, we conclude the proof.

A-C Proof of Lemma 1

For compactness, we denote by the random variable and by each realization of it. We first verify that our setup satisfies Assumption 1. Assumption LABEL:*assumption (i) follows since the set of points in whose norm is unbounded is a null set. Assumption LABEL:*assumption (ii) holds since the involved expectation is a Gaussian integral which is convergent for any . Since any continuous function is also measurable and is quadratic, we have that is measurable as per Assumption LABEL:*assumption (iii). Finally, we argue that Assumption LABEL:*assumption 2 holds in data-driven scenarios as a regular conditional distribution can be constructed as follows. By the law of total probability, any joint probability distribution of can be constructed from the marginal of and the conditional distribution of given , that is, we may write . We can now prove the lemma starting with the first point. The feasibility condition in [22, Theorem 3.1] is

We compute the inner expectation as

where the last equality follows from the standard Gaussian integral result

|

|

To conclude the proof of the first point we consider the logarithm of the previous expression scaled by and take the expectation with respect to . In this way, we obtain

Next, we provide the proof for the second point. From (15) we have the expression for the strong dual for a generic loss function . We now focus on the inner expectation. With a quadratic loss function and transport cost, we have

with

where we require for the integral to converge.

Then, considering the logarithm of this expression scaled by and taking the expectation with respect to the empirical distribution we obtain

To conclude, we can simply introduce epigraphical variables leading to the final optimization program (16).