Optimal Nonlinear Online Learning under Sequential Price Competition via -Concavity

Abstract

We consider price competition among multiple sellers over a selling horizon of periods. In each period, sellers simultaneously offer their prices and subsequently observe their respective demand that is unobservable to competitors. The demand function for each seller depends on all sellers’ prices through a private, unknown, and nonlinear relationship. To address this challenge, we propose a semi-parametric least-squares estimation of the nonlinear mean function, which does not require sellers to communicate demand information. We show that when all sellers employ our policy, their prices converge at a rate of to the Nash equilibrium prices that sellers would reach if they were fully informed. Each seller incurs a regret of relative to a dynamic benchmark policy. A theoretical contribution of our work is proving the existence of equilibrium under shape-constrained demand functions via the concept of -concavity and establishing regret bounds of our proposed policy. Technically, we also establish new concentration results for the least squares estimator under shape constraints. Our findings offer significant insights into dynamic competition-aware pricing and contribute to the broader study of non-parametric learning in strategic decision-making.

1 Introduction

Pricing plays a central role in competitive markets, where firms continuously adjust prices in response to demand fluctuations and rival strategies. With the rise of algorithmic pricing, companies are increasingly using data-driven methods to optimize pricing decisions. However, many existing pricing algorithms still operate under monopolistic assumptions (Fan et al., 2024; Javanmard & Nazerzadeh, 2019; Golrezaei et al., 2019; Bracale et al., 2025), treating demand as independent of competitors’ actions. This oversimplifies the strategic nature of pricing, where firms dynamically respond to each other in a competitive environment. In reality, pricing is not an isolated decision but an interactive process that requires firms to anticipate and react to competitors’ actions. As highlighted by Li et al. (2024), a major challenge in competition-aware pricing lies in inferring rivals’ pricing behavior from limited observations. Firms cannot easily estimate price sensitivity through controlled experiments since competitors do not coordinate to hold prices constant while one firm tests different price points. Also, designing models that effectively capture competitive effects remains difficult. Although numerous sequential pricing algorithms yield low regret and converge toward Nash equilibrium, they often rely on a linear demand framework (Li et al., 2024). Even approaches that incorporate nonlinear demand typically confine themselves to a specific parametric family with a predetermined nonlinear transformation (Goyal et al., 2023), thereby reducing their applicability.

Motivated by the fact that nonlinear demand models are more realistic and widely studied in various pricing applications (Gallego et al., 2006; Wan et al., 2022; 2023), we extend beyond these limitations by considering a more flexible semi-parametric model where both the parametric and nonparametric components are unknown. We propose a tuning-free algorithm, that achieves sublinear regret with respect to a dynamic benchmark.

In our work, we extend the conventional multi-period pricing framework by incorporating a nonlinear demand model. Here, sellers simultaneously set prices over periods, and each seller’s observed demand results from a complex interplay of their own pricing and that of their competitors – a feature that becomes even more pronounced when departing from linearity. Sellers are able to review the pricing history of their rivals, yet they remain unaware of the actual demand those competitors face. We assess performance by comparing the revenue outcomes of our policy against an idealized benchmark where full information is available.

Our study examines pricing policies with two key objectives: (1) assessing whether sellers maximize their revenue over time and (2) analyzing whether seller prices converge to the Nash equilibrium that would arise under full information. To evaluate performance, we measure cumulative regret, defined as the worst-case gap between a seller’s average revenue under our proposed pricing policy (where neither model parameters nor competitor demand is known) and an optimal policy in hindsight (which assumes fixed competitor prices and full knowledge of the demand model).

2 Related Literature and Contributions

2.1 Sequential Price Competition with Demand Learning

Over the past two decades, significant advancements have been made in demand learning within competitive pricing environments. A substantial body of literature exists on price competition under known demand, beginning with the early works of Cournot (1838) and Bertrand (1883), which introduced the classic static models for competition in production output and market price respectively; to different variations such as multinomial logit models (Gallego et al., 2006; Aksoy-Pierson et al., 2013; Gallego & Wang, 2014); fixed-point based methods for mixed-logit demands Morrow & Skerlos (2011); and price competition across multiple decision epochs (Gallego & Hu, 2014; Federgruen & Hu, 2015; Chen & Chen, 2021).

In this paper, we will instead focus on sequential price competition with demand learning. Early foundational work in this area by Kirman (1975) examined a symmetric two-seller competition with linear demand, focusing on unknown demand structures using a model where the expected demands of two firms, given their prices and , are , ; and symmetric means that the parameters and, are shared for the two firms. The case of asymmetric sellers under noisy linear demand was first studied by Cooper et al. (2015) who allowed each seller to learn independently, as if operating like a monopolist. Equilibrium was shown to be attained assuming sellers knew individual price sensitivity, though this is rarely true in practice. In contrast, Li et al. (2024) addressed dynamic pricing with unknown price sensitivities, achieving the optimal regret rate , under a linear demand model: specifically, firm ’s expected demand is , where , is the number of firms in the market, , and are unknown for each .

However, nonlinear demand models are more realistic and have been used and studied in several models and applications (see e.g. Gallego et al. (2006); Wan et al. (2022; 2023)). For example Gallego et al. (2006) considered the mean demand function for some known increasing functions and real value . In contrast to prior studies (Li et al., 2024; Kachani et al., 2007; Gallego et al., 2006), we analyze the more general unknown monotone single index expected demand model

for where and is a vector of dimension with -th entry equals to and the rest of the entries are the values of ordered. Here the parameters are unknown. This model generalizes the linear demand model by Li et al. (2024); specifically, setting recovers their formulation. Differently from Kachani et al. (2007), the sellers do not share demand information to accomplish the estimation step. We analyze the existence and uniqueness of the Nash Equilibrium (NE) and we prove the convergence of the pricing policy to the NE as well as the rate of convergence of the regret of every single firm relative to a dynamic benchmark policy in our sequential price competition with an arbitrary number of sellers.

2.2 Monotone Single Index Models

Our work is related to the monotone single index model. Specifically, Section˜2.1 describes monotone single index models , with unknown -dimensional parameters and unknown non-decreasing functions . Unlike generalized linear models (GLMs), which assume that is known in advance, the single index model, where is more general a nonlinear function non-necessarily monotone, requires learning non-parametrically, offering additional flexibility while avoiding the “curse of dimensionality” of fully non-parametric models in high-dimensional settings Zhao (2008). In our setting, we add the requirement that be non-decreasing. The monotonicity assumption of here arises naturally: as seen in Section˜2.1, it ensures that demand is non-increasing in uniformly in . This assumption – namely, that the mean demand for a firm decreases with its own price – is common in economics (see e.g. Birge et al. (2024); Li et al. (2024)). Moreover, the monotonicity assumption of has a great advantage. Estimators based only on smoothness conditions on the ridge function typically depend on a tuning parameter that has to be chosen by the practitioner. The monotonicity assumption allows non-parametric estimators that are completely data-driven and do not involve any tuning parameters.

The monotone single index model has been studied intensively by Balabdaoui et al. (2019). They proved that the model is identifiable if, for example, is increasing and , as long as has a density with respect to Lebesgue measure which is strictly positive on its domain (see Balabdaoui et al. (2019, Proposition 5.1)), a condition that we will rely on in this work (see ˜4.1 and discussion in Section˜6.2). They also proposed a (joint) estimator based on i.i.d. data points , for which has rate of order in the norm. Additionally, they analyze the well-known linear estimator , where

| (1) |

The linear estimator , which dates back to Brillinger (2012), coincides with what one would use under a purely linear model and remains consistent if is drawn from an elliptical distribution.

In this work, we utilize an exploration-exploitation algorithm, where the exploration phase is used to collect data to obtain consistent estimators for . Since the data in the exploration phase has a different distribution from the data in the exploitation phase, it typically is not sufficient to have a convergence in of to derive an upper bound on the total regret, while a supremum norm converge is sufficient for this scope. For this reason, we propose to split the exploration phase into two sub-phases for which we separately learn and , and derive a supremum norm convergence. Concretely, in the first part, we estimate using the linear estimator in Equation˜1, for which we prove a concentration inequality (see Proposition 6.3), differently from Balabdaoui et al. (2019) that primarily studies convergence in probability and in distribution. In the second part of the exploration phase, we estimate . While a natural choice would be the isotonic estimator (which enforces monotonicity), we impose the additional constraint that must be -concave for some . This extra condition is sufficient for the existence of a Nash Equilibrium in our setting, as discussed below.

2.3 Connection with the Existence of NE, Virtual Valuation Function, and -Concavity

In Lemma˜4.5 we establish the existence of an NE for model in Section˜2.1 under the condition that

| (2) |

(aka virtual valuation function) is increasing with derivative bounded away from zero, that is that for some . The same assumption found in several works with , for example, Assumption 2.1 in Fan et al. (2024), Assumption 1 in Chen & Farias (2018), Equation 1 in Cole & Roughgarden (2014) and Golrezaei et al. (2019); Javanmard (2017); Javanmard & Nazerzadeh (2019) which assume and to be log-concave (which implies specifically ), where here is bounded in , i.e. it represents a survival function.

While log-concavity is a natural shape restriction, recent work in non-parametric shape-constrained inference has explored natural generalizations to classes of functions that exhibit concavity under transformation by a fixed function. Of particular interest is the notion of -concavity, where the transforming function is driven by the real parameter and yields log-concavity as goes to 0 (see Section˜2.4 for more details). Our main observation to establish the existence of a NE in terms of shape constraints on is that for some is equivalent to requiring that is -concave (Lemma˜4.5 and Proposition˜4.3). This observation allows us to leverage the shape-constrained statistical inference for estimating , and then a tuning-parameter-free algorithm. Specifically, we use non-parametric least squares estimation (NPLSE) to estimate under -concavity. As must be clear from the above discussion but worth restating: this shape-constrained assumption is not an artificial imposition by us; rather, it is implicit in the work of previous researchers. A key advantage of our shape-constrained approach compared to common non-parametric approaches lies in that our estimate can be computed without needing to specify any tuning parameter and is entirely data-driven.

2.4 -Concavity

A technical contribution of this work is the study of the uniform rate of convergence of the least-squares estimator of an -concave regression function. This class of functions includes both concave functions () and log-concave functions (). As defined in Han & Wellner (2016), a function is said to be -concave for some and we write if

for all and , where

This notion generalizes log-concavity which holds for , in the sense that . The class of log-concave densities has been extensively studied: see Bobkov & Madiman (2011); Dümbgen & Rufibach (2009); Cule & Samworth (2010); Borzadaran & Borzadaran (2011); Bagnoli & Bergstrom (2006); Doss & Wellner (2016); Brascamp & Lieb (1976); while Han & Wellner (2016); Doss & Wellner (2016); Chandrasekaran et al. (2009); Koenker & Mizera (2010) deal with general -concavity. It’s easy to see that such functions have the form for some concave function if , where , for some concave function if , and for some convex function if . These classes are nested since , if . In this paper, we consider the unidimensional case, where represents a mean demand function on a set of prices that is positive and strictly increasing, and then has the form where is concave and

| (3) |

More precisely, we study the more general class that contains functions of the form , where is a known increasing twice differentiable function and is an unknown concave function. Differently from previous results, we focus on regression problems with mean function in . More precisely, in Appendix˜F, we consider i.i.d. observations for where are noisy versions of the mean function and for some unknown concave and a known increasing twice differentiable transformation (i.e. ), where is an interval containing . We study the uniform convergence rate of , where is the LSE

The uniform convergence of to plays a crucial role in establishing the convergence of our proposed pricing strategy to the Nash Equilibrium, as we will see later in the paper.

2.5 Summary of Key Contributions

We now provide a brief summary of our key contributions as follows.

A novel semiparametric pricing policy for nonlinear mean demand. We extend the standard approach to estimating the mean demand function of a firm by introducing a monotone single index model , where is increasing, providing substantially more flexibility than previous parametric models (Li et al. (2024); Kachani et al. (2007); Gallego et al. (2006)). Similar to Li et al. (2024) the (randomized) demand values are kept private, making it impossible for a given seller to anticipate any other seller’s strategy, or even to estimate their model parameters.

Existence of the NE in terms of shape constraints on the mean demand functions. To guarantee the existence of a Nash-equilibrium, many existing works implicitly assume that the virtual valuation function defined in Equation˜2 is increasing; often by invoking log-concavity or similar conditions as we discuss in Section˜2.3. We show how all such assumptions can be cast under the more general framework of -concavity (Lemma˜4.5 and Proposition˜4.3), thereby providing a unified perspective on the existence of a Nash-Equilibrium (NE). This reformulation allows the development of a fully data-driven, tuning-parameter-free algorithm using shape constraints.

Regret upper bound and convergence to equilibrium. We establish an upper bound on the total expected regret and analyze the convergence to the Nash equilibrium (NE) for a general exploration length of for (Theorem˜6.9). Our results reveal the existence of an optimal choice of that minimizes the total expected regret for each seller, leading to a regret of order , where excludes log factors. Moreover, we show that by the end of the selling horizon, the joint prices set by sellers converge to Nash equilibrium prices at a rate of (Corollary˜6.10).

Concentration inequality for -concave regression function in the supremum norm. Our work involves establishing a concentration inequality for the LSE, under the supremum norm, for a large class of shape constraints that includes -concavity (Appendix˜F). As a minor contribution, we derive a concentration inequality for the parametric component of the monotone single index model (Proposition˜6.3), while previous results show convergence in probability or distribution (Balabdaoui et al., 2019).

3 General Notation

We use , and to denote the norm, the Euclidean norm, and the supremum norm, respectively. We denote the dimensional sphere as . The notation omits any logarithmic factors in . A function is -Hölder, for some , if there exists a constant such that for all in the domain; is Lipschitz if is -Hölder. We use and to denote the gradient vector and the Hessian matrix of at . We denote by the set of -th continuously differentiable function on . We denote by the Lipschitz constant of a Lipschitz function . A vector field is a contraction if for some . Following the definition in Delmas et al. (2024, Pag 86), a -dimensional random variable is distributed according to an elliptically symmetric distribution with density generator , location vector and a positive-definite scale matrix , and we denote if the density of has the form (up to a constant) .

4 Problem Formulation

We adopt a problem setup similar to that of Li et al. (2024). We consider sellers, each selling a single type of product with unlimited inventories and aiming to maximize individual cumulative revenue over a selling horizon of periods. We use to index time periods and to index sellers. At the beginning of each period, each seller simultaneously selects their price. For seller , denotes the price that seller offers in period , with price bounds and . Let denote the competitor prices at time , denote the joint prices, and denote the support of joint prices. We define the set

| (4) |

The demand of seller in period depends on the offered prices of all sellers, , following a nonlinear model:

| (5) |

where are (zero mean) sub-gaussian demand noises following independent and identical distributions ( and can be correlated with , ), and is a vector of dimension with -th entry equal to and the rest of the entries are the values of , ordered. The parameter vector measures how seller ’s demand is affected by competitor prices. We assume that the parameter space is such that the average demand is non-negative and among all values of ; a similar assumption is found in Birge et al. (2024); Li et al. (2024). The above conditions hold if and , which are explicitly assumed in ˜4.1.

Assumption 4.1.

For every , is an unknown function in such that and on for some and . We also assume

where is an unknown constant.

The condition and the monotonicity of guarantees the identifiability of the monotone single index model (Chmielewski, 1981; Balabdaoui et al., 2019). Note that Section˜4 is well defined, that is , indeed from ˜4.1 we get that for every , and then . Seller aims to maximize the individual (cumulative) revenue, which can be expressed as

Each seller’s offered prices are public but their demand history is private; that is, when seller decides price in period , they can utilize the information of joint price history and individual demand history .

Maximizing a seller’s revenue can be reframed as minimizing their regret. Each seller competes with a dynamic optimal sequence of prices in hindsight while assuming that the other sellers would not have responded differently if this sequence of prices had been offered. Under such a dynamic benchmark, the objective of each learner is to minimize the following regret metric in hindsight:

| (6) |

where ,

where . In addition to individual regret minimization, we also investigate whether sellers converge to equilibrium if each of them employs a regret-minimizing policy.

4.1 Nash Equilibrium (NE)

Our equilibrium prices are defined based on the static (one-shot) price competition. Consider a single period , wherein superscript is omitted. The Nash equilibrium prices are defined as a price vector under which unilateral deviation is not profitable for any seller. Specifically, is a solution to the following balance equation (or fixed point equation):

| (7) |

Under certain conditions, the map has a closed form expression given by

(see the proof of Lemma˜4.5 for the derivation) where is the virtual valuation function of firm as defined in Equation˜2. First, we guarantee the existence of , i.e. of , with ˜4.2, which states that the ’s are increasing, and then invertible.

Assumption 4.2 (Existence of NE).

For every , there exist constants such that . Moreover, falls in the interior of for all .

The second part of ˜4.2, is a mild assumption and is guaranteed if each boundary action is dominated by some other action; see, e.g. Hsieh et al. (2021); Besbes et al. (2015); Chen et al. (2019).We now present an equivalent formulation of ˜4.2—or, equivalently, a sufficient condition for the existence of a Nash equilibrium—in terms of -concavity. The proof is provided in Appendix˜A.

Proposition 4.3.

For every , iff is -concave.

For the uniqueness of the Nash equilibrium (i.e., the fixed-point equation in Equation˜7), a sufficient condition is to ensure that the Lipschitz constant of is strictly less than in . The following condition guarantees the uniqueness of the Nash equilibrium:

Assumption 4.4.

.

Lemma 4.5 (Existence and Uniqueness of NE).

Suppose that ˜4.2 and ˜4.4 hold. Then, there exists a unique price vector in the interior of satisfying the balance equations in Equation˜7.

This result is based on the contraction mapping theorem. The proof is relegated to Appendix˜B.

Remark 4.6 (Special case for ).

Remark 4.7.

Note that ˜4.4 coincides with Assumption 2 in Li et al. (2024) (with which is greater than as in their definition) which guarantees the uniqueness of the NE as well. Similar assumptions are found in Kachani et al. (2007). Moreover, a market that does not satisfy ˜4.4 can yield impractical outcomes. For instance, consider the scenario where for some (i.e. the mean demand function is log-concave), and for some . In this case would become excessively large, driving the -th seller’s demand close to the market size. However, such a situation is infeasible when is sufficiently large, as it would exceed the natural upper bound of . Indeed, -concave functions are inherently bounded over any finite domain, making this scenario unrealistic.

5 Proposed Algorithm

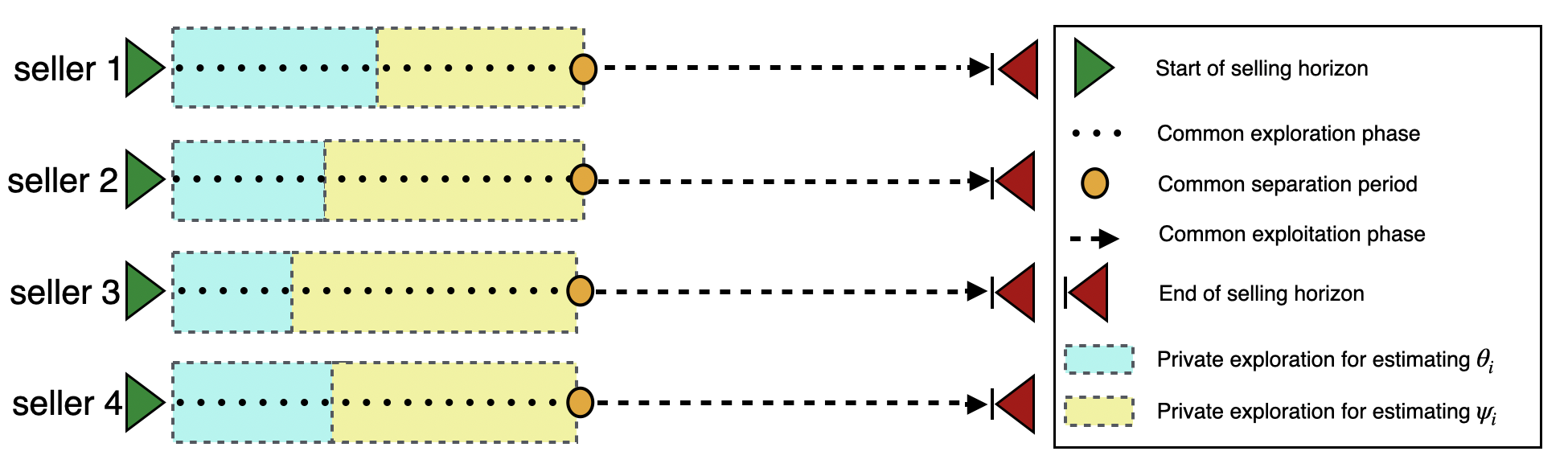

Our Algorithm˜1 consists of an initial exploration phase for parameter estimation, followed by an exploitation phase where sellers set prices based on the learned demand model. For , seller samples iid prices from a distribution , and for , where is the common exploration length for some that will be specified later (Corollary˜6.10). The random prices charged by different sellers in the exploration phase are not necessarily independent, and we will use from now on to denote the joint distribution of the price vector in the exploration phase. At every time , each firm observes their own (random) demand value while the prices are made public. At the end of the exploration phase, firm estimates using data . More precisely, each firm chooses a proportion of initial data points in the exploration phase to estimate , and subsequent time points to estimate (a scheme in presented in Figure˜1). For simplicity of notation we define and .

-

(1)

Exploration phase part 1: . In this first part of the exploration phase, seller considers the estimator

where

(8) The linear estimator goes back to Brillinger (2012) and it is exactly what one would use if the regression model were known to be linear.

-

(2)

Exploration phase part 2: . For the second part define for , and define the estimator:

(9) where is the class of -concave functions , where is defined in Equation˜4.

During the exploitation phase, every firm will obtain an estimated revenue function by plugging in its estimators from the exploration phase:

| (10) |

where are the prices of all the other firms at time , that are made public. A price is then offered by firm as a maximizer of Equation˜10. We present the full algorithm in Algorithm˜1 and a scheme in Figure˜1.

Remark 5.1 (The common exploration phase).

To highlight the importance of a common exploration phase, we demonstrate that no seller has an incentive to extend or shorten the exploration phase. If firm prolongs its exploration phase, it risks incomplete learning of its model parameters (Keskin & Zeevi, 2018), leading to inaccurate parameter estimation and, consequently, a loss in revenue. Conversely, if firm shortens its exploration phase, it may achieve consistent estimation but at the cost of higher regret due to insufficient exploratory data. For a better illustration, consider a scenario where firm extends its exploration phase to while all other firms use a phase of length . When firm estimates its parameters using data , the data from times to are no longer iid. In this later period, all other firms have already started their exploration, causing the prices to be dependent on the earlier data . This dependency can result in inconsistent parameter estimation and a loss of efficiency for firm . Conversely, if firm opts for a shorter exploration phase than , it may achieve consistent estimation, but the reduced amount of exploratory data could lead to lower efficiency compared to firms that adhere to the full exploration phase.

Remark 5.2 (Need for two different phases for model estimation).

In principle, one could estimate jointly using the full exploration phase. For instance, Balabdaoui et al. (2019) employ a profile least squares approach to achieve convergence for the joint LSE of based on the data . However, in our context, convergence alone does not suffice to establish an upper bound on the total expected regret. To elaborate, let denote the joint estimator proposed in Balabdaoui et al. (2019) based on the data . Their result applied to our setting gives the following convergence rate:

Here, the convergence is measured with respect to the measure , which governs the distribution of prices during the exploration phase. Consequently, the distance between and can only be evaluated for prices distributed according to . This is problematic because, in the exploitation phase (), the distribution of prices may differ from . A uniform convergence result, which does not depend on any specific price distribution, is critical to our problem. However, achieving uniform convergence of the form

| (11) |

is challenging when are estimated jointly. To overcome this difficulty, our approach is to first estimate and then, conditional on this estimator, separately estimate using an independent dataset. This two-step procedure ensures conditional independence and yields consistent estimators, addressing the difficulties of the joint estimation strategy.

6 Convergence of NE and Regret Analysis

We first analyze, for every seller , the convergence of the estimators in Section˜6.1 and in Section˜6.2, associated with the exploration phase. Then we analyze the convergence of the NE and the upper bound on the total regret in Section˜6.3.

6.1 Estimation of the Parametric Component

In a single-index model, the linear estimator in Equation˜8 converges to the true at a rate and is asymptotically Gaussian (Chmielewski, 1981), provided that the covariates (in this case, the joint prices ) follow an elliptical distribution (Balabdaoui et al., 2019; Brillinger, 2012). We adopt the same elliptical assumption to ensure the consistency of the estimator in Equation˜8. More specifically, and in contrast to earlier work, we establish a concentration inequality for this estimator (Proposition˜6.3), which serves as a key tool in deriving our regret upper bound.

We assume that in the exploration phase the distribution of the covariates is elliptically symmetric with density generator supported on , location vector , and a positive definite scale matrix , i.e.

and we denote the above distribution by . We denote by , which is proportional to .

Remark 6.1.

It should be noted that from a purely theoretical stand-point we do not restrict the domain of the price vector in the exploration phase to , but this has essentially no implication for the application of the pricing algorithm in practice. To ensure that the ’th seller’s exploration prices can, realistically, never lie outside , all they need is to take be a normal distribution (for example) centered at the midpoint of this interval with variance taken to be an adequately small fraction of the length of . If the sellers function independently, as is generally the case, the joint distribution is certainly elliptically symmetric. More generally, view the parameters , , and as concentrating the mass of in with overwhelmingly high probability. Theoretically, some proposed price in many thousands of time steps could lie outside , but realistically the procedure entails no financial consequence for them. Letting belong to an infinitely supported elliptical distribution allows the implementation of a simple linear regression-based approach to learn which satisfies the useful concentration inequality proved in Proposition 6.3 below, and is also important for certain conditioning arguments involved in estimating appropriate surrogates for in the following subsection, while compromising nothing in terms of the core conceptual underpinnings of the problem.

Assumption 6.2.

, where for some and the density generator is such that for all .

˜6.2 holds for a wide range of distributions, including Gaussian distributions and, more generally, all elliptically symmetric distributions for which , for and . This assumption on is instrumental in estimating since it guarantees that the sampled points are sub-Gaussian, a property that is essential for deriving the concentration inequality in Proposition˜6.3. Moreover, as we will discuss in Section˜6.2, this assumption is also beneficial for the estimation of because it ensures that (defined in Equation˜12) depends on solely through the argument of rather than that of , and this decoupling guarantees that inherits key properties from , such as smoothness and adherence to the prescribed shape constraints, as highlighted in Proposition˜6.5.

Since the covariance matrix of an elliptically symmetric distribution is proportional to , then there exists such that , where , . These constant will appear in Proposition˜6.3, which proof is provided in Appendix˜C.

Proposition 6.3.

Under ˜6.2, there exist positive constants and (that depend solely on and the variance proxies of the sub-Gaussian random variables and ) such that, for sufficiently large, with probability at least , the estimator in Equation˜8 satisfies

6.2 Estimation of the Link Function via s-Concavity

This section provides a uniform convergence result of to for any fixed . In this section, all the results must be considered as conditioned on estimated using data in independent of data in . For simplicity of notation, we re-index as . To estimate we would need to know in advance, indeed we remind that . However, our knowledge is limited to an approximation of , and the observable design points are . This implies that, with data , we are only able to estimate

| (12) |

We will now construct an estimator of , and we will prove, in Theorem˜6.6, a uniform convergence result in the (bounded) set (where defined on Equation˜4), however, the result holds for any bounded set . Indeed, from Mösching & Dümbgen (2020) we have that if the density of the design points is bounded away from on a set , then are “asymptotically dense” within each interval contained in , which condition is sufficient to produce a uniform convergence result of our estimator of on any interval contained in . In our case, is supported on all , and hence is bounded away from on any bounded set , therefore the convergence result holds uniformly on any bounded set .

Remark 6.4.

Note that, since the NE falls in the interior of , our algorithm will be able to converge to it if is sufficiently small to guarantee for all .

A closed-form expression for and some of its properties are proved in Proposition˜6.5.

Proposition 6.5.

Under ˜4.1 and ˜6.2 we have the following properties:

-

(1)

, , , where is independent of , is defined in Equation˜21, and is such that .

-

(2)

is bounded uniformly in .

-

(3)

and is bounded from above uniformly in .

-

(4)

for all and .

-

(5)

If also ˜4.2 holds (i.e. is -concave for some as it arises from Proposition˜4.3) then is -concave for any .

Proposition˜6.5 is crucial because it tells us that if we had a (uniform) consistent estimate of , then by point (4), is close to as long as is close to , which will be used to prove the regret upper bound. Moreover, guided by point (5) in Proposition˜6.5 we estimate using LSE under -concavity restriction, denoted as

| (13) |

where is the set of concave functions . We are now prepared to demonstrate the convergence of to , where

Theorem 6.6.

Let ˜6.2 and ˜4.2 hold. Then, by Proposition˜4.3 and Proposition˜6.5, is -concave for some . Let , where is the proportion of data points lying in the set as . For every there exists , a constant and depending only on constants in the assumptions such that

where , with .

Theorem˜6.6 is an application of our more general Theorem˜F.5 (and following Remark˜F.6). We defer to Appendix˜G for the proof.

6.3 NE and Regret

Recall that . Before stating our main theorem, we need the following assumption.

Assumption 6.7.

There exists such that for all and .

Remark 6.8.

˜6.7 informally states that the revenue functions are smooth around the NE. ˜6.7 is satisfied in several scenarios, for example when for all for some independent of . Indeed, in this case, since we have that . Examples where the condition for all for some independent of is satisfied are: the linear demand models (Li et al., 2024), the concave demand models, and the -concave demand functions for some . For a more detailed description of these and more examples, we defer to Appendix˜H.

In Theorem˜6.9, we present our main result for a fixed value , which, we recall, represents the proportion of (common) exploration length .

Theorem 6.9.

In Corollary˜6.10, we provide the exploration-exploitation trade off for our Algorithm˜1. More specifically, we provide the optimal choice of that minimizes the expected regrets. Corollary˜6.10 follows immediately from Theorem˜6.9 by equalizing the exponents of in the regret upper bound (ignoring logarithmic factors)

which yields the value of that minimizes the total expected regret.

Corollary 6.10.

Suppose that the same assumption in Theorem˜6.9 holds. Then, the value of that minimizes the expected regrets is . With this choice, we get that for each :

-

(1)

Individual sub-linear regret: .

-

(2)

Convergence to NE: .

7 Numerical Experiments

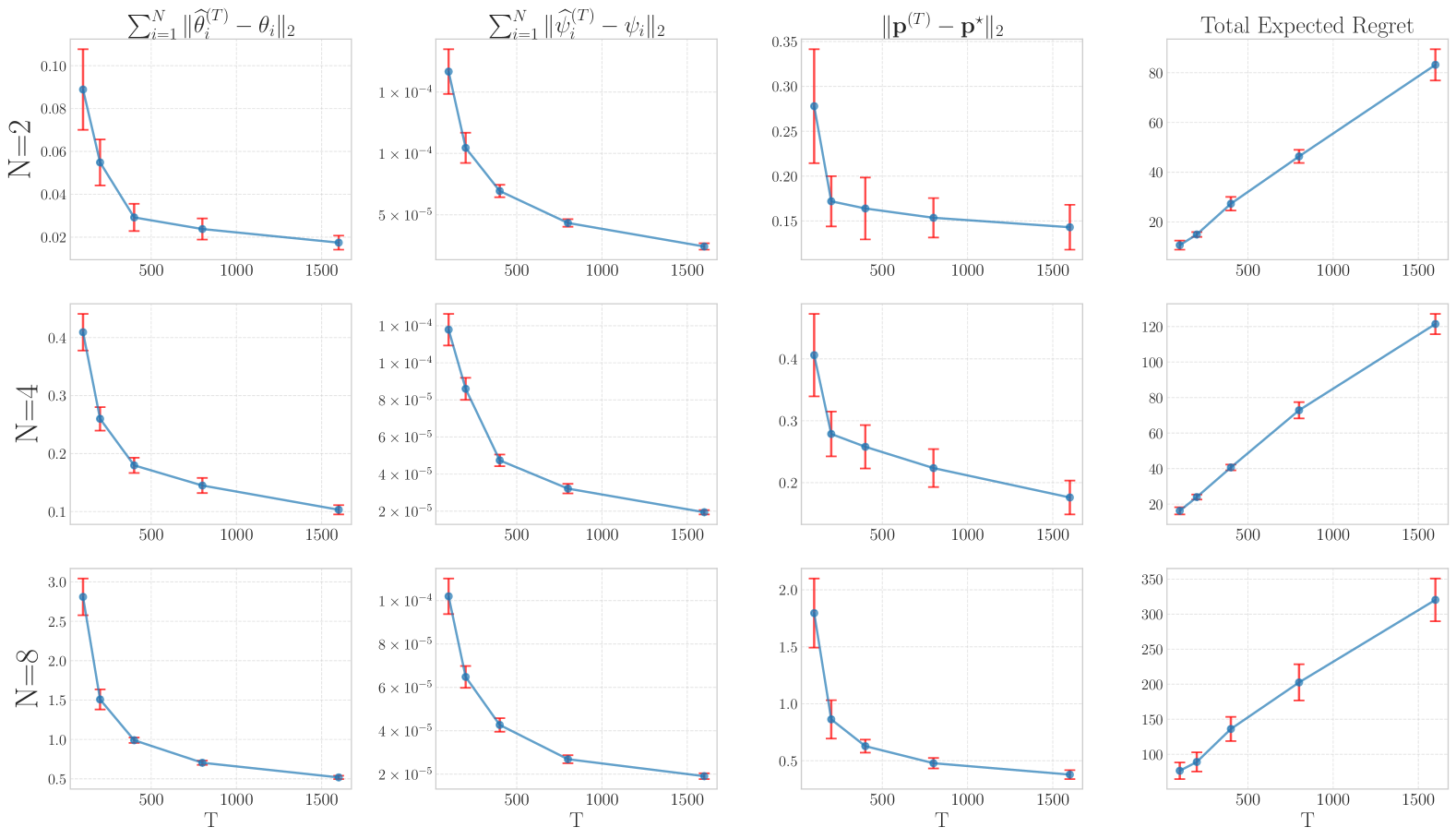

We test the performance of our Algorithm˜1 in the sequential price competition with sellers. For each seller , the price is supported on . The link functions are defined as where is the cumulative distribution function of a standard Gaussian random variable which is log-concave and therefore -concave. Their price sensitivities and are such that has unitary -norm and satisfy ˜4.4, because, by Remark˜4.6, . A fixed point exists and is unique by Lemma˜4.5 and is evaluated using Picard’s iteration, and we check that the fixed point falls in the interior of . The demand noise of firm follows a uniform distribution on . For every , we apply Algorithm˜1. We independently repeat the simulation times to obtain average performances and of confidence intervals. In Figure˜2 we report the results: we display the convergence of the estimators and , as well as the convergence to the Nash equilibrium , and the expected cumulative regret.

8 Conclusions

In this paper, we introduced an innovative online learning algorithm for sequential price competition, where each seller’s mean demand is modeled as a nonlinear function of joint prices. This departure from standard parametric models (Li et al. (2024); Kachani et al. (2007); Gallego et al. (2006)) not only broadens the scope of demand modeling but also enhances the realism of market interactions. Leveraging shape constraints on the mean demand function that arise naturally in the literature, we demonstrated the existence of the NE, provided an upper bound on the algorithm’s regret, and established a convergence rate for the joint prices to the Nash Equilibrium.

Future research directions. There are several promising avenues for further research. One direction is to design an algorithm that permits each seller to independently determine the length of their exploration phase, which is difficult in our setting for reasons elaborated in Remark˜5.1.

On the theoretical front, an important research direction is achieving uniform convergence of the joint estimator . While this does not affect the theoretical convergence rate of the regret or the Nash equilibrium – since it influences only a constant factor (given that is estimated using data points and using , where is the length of the exploration phase, whereas a joint estimator would treat as a single sample size rather than splitting it) – it may yield practical improvements. Two existing theoretical results are relevant to the joint estimator: Balabdaoui et al. (2019) and Kuchibhotla et al. (2021). The former establishes convergence for the joint estimator, which is insufficient for deriving an upper bound on the expected regret. Notably, while Balabdaoui et al. (2019) imposes only a monotonicity constraint on , our framework requires -concavity to guarantee the existence of an equilibrium. The latter work, Kuchibhotla et al. (2021), provides a uniform convergence result for , but under the assumption that is convex (or concave, i.e., ). Moreover, their result offers only an rate rather than a concentration inequality, making it insufficient for establishing a regret bound in expectation. Differently from these works, our framework would require a concentration inequality in the supremum norm of the joint estimator, i.e., deriving a probability tail bound of the event in Equation˜11.

Another theoretical challenge lies in estimating the ’s. In this work, we assume is known, but in practice, its true value may be uncertain. While our algorithms can be extended to estimating and simultaneously, the theoretical foundations for such an approach are a challenge in their own right and remain to be explored.

Finally, a compelling direction for future exploration is to develop an algorithm that foregoes the traditional exploration-exploitation trade-off. In a more realistic framework, each seller would utilize all past (public) price observations and corresponding (private) demand data to set the price at every time , such that converges to the Nash Equilibrium as . A key challenge in this setting is to prevent incomplete learning of the model parameters (Keskin & Zeevi, 2018), which can lead to suboptimal parameter estimates and a consequential loss in revenue, manifested as higher regret.

References

- Aksoy-Pierson et al. (2013) Margaret Aksoy-Pierson, Gad Allon, and Awi Federgruen. Price competition under mixed multinomial logit demand functions. Management Science, 59(8):1817–1835, 2013.

- Bagnoli & Bergstrom (2006) Mark Bagnoli and Ted Bergstrom. Log-concave probability and its applications. In Rationality and Equilibrium: A Symposium in Honor of Marcel K. Richter, pp. 217–241. Springer, 2006.

- Balabdaoui et al. (2019) Fadoua Balabdaoui, Cécile Durot, and Hanna Jankowski. Least squares estimation in the monotone single index model. Bernoulli, 25(4B):3276–3310, 2019.

- Bertrand (1883) Joseph Bertrand. Review of “theorie mathematique de la richesse sociale” and of “recherches sur les principles mathematiques de la theorie des richesses.”. Journal de savants, 67:499, 1883.

- Besbes et al. (2015) Omar Besbes, Yonatan Gur, and Assaf Zeevi. Non-stationary stochastic optimization. Operations research, 63(5):1227–1244, 2015.

- Birge et al. (2024) John R Birge, Hongfan Chen, N Bora Keskin, and Amy Ward. To interfere or not to interfere: Information revelation and price-setting incentives in a multiagent learning environment. Operations Research, 2024.

- Bobkov & Madiman (2011) Sergey Bobkov and Mokshay Madiman. Concentration of the information in data with log-concave distributions. The Annals of Probability, 39(4):1528–1543, 2011.

- Borzadaran & Borzadaran (2011) GR Mohtashami Borzadaran and HA Mohtashami Borzadaran. Log-concavity property for some well-known distributions. Surveys in Mathematics and its Applications, 6:203–219, 2011.

- Bracale et al. (2025) Daniele Bracale, Moulinath Banerjee, Yuekai Sun, Kevin Stoll, and Salam Turki. Dynamic pricing in the linear valuation model using shape constraints. arXiv preprint arXiv:2502.05776, 2025.

- Brascamp & Lieb (1976) Herm Jan Brascamp and Elliott H Lieb. On extensions of the brunn-minkowski and prékopa-leindler theorems, including inequalities for log concave functions, and with an application to the diffusion equation. Journal of functional analysis, 22(4):366–389, 1976.

- Brillinger (2012) David R Brillinger. A generalized linear model with “gaussian” regressor variables. Selected Works of David Brillinger, pp. 589–606, 2012.

- Chandrasekaran et al. (2009) Karthekeyan Chandrasekaran, Amit Deshpande, and Santosh Vempala. Sampling s-concave functions: The limit of convexity based isoperimetry. In International Workshop on Approximation Algorithms for Combinatorial Optimization, pp. 420–433. Springer, 2009.

- Chen & Chen (2021) Ningyuan Chen and Ying-Ju Chen. Duopoly competition with network effects in discrete choice models. Operations Research, 69(2):545–559, 2021.

- Chen et al. (2019) Xi Chen, Yining Wang, and Yu-Xiang Wang. Nonstationary stochastic optimization under l p, q-variation measures. Operations Research, 67(6):1752–1765, 2019.

- Chen & Farias (2018) Yiwei Chen and Vivek F Farias. Robust dynamic pricing with strategic customers. Mathematics of Operations Research, 43(4):1119–1142, 2018.

- Chmielewski (1981) Margaret Ann Chmielewski. Elliptically symmetric distributions: A review and bibliography. International Statistical Review/Revue Internationale de Statistique, pp. 67–74, 1981.

- Cole & Roughgarden (2014) Richard Cole and Tim Roughgarden. The sample complexity of revenue maximization. In Proceedings of the forty-sixth annual ACM symposium on Theory of computing, pp. 243–252, 2014.

- Cooper et al. (2015) William L Cooper, Tito Homem-de Mello, and Anton J Kleywegt. Learning and pricing with models that do not explicitly incorporate competition. Operations research, 63(1):86–103, 2015.

- Cournot (1838) AA Cournot. Recherches sur les principes mathématiques de la théorie des richesses par augustin cournot (paris, france: chez l. hachette). 1838.

- Cule & Samworth (2010) Madeleine Cule and Richard Samworth. Theoretical properties of the log-concave maximum likelihood estimator of a multidimensional density. Electronic Journal of Statistics, 4:254–270, 2010.

- Delmas et al. (2024) Jean-Pierre Delmas, Mohammed Nabil El Korso, Stefano Fortunati, and Frédéric Pascal. Elliptically symmetric distributions in signal processing and machine learning. Springer, 2024.

- Doss & Wellner (2016) Charles R Doss and Jon A Wellner. Global rates of convergence of the mles of log-concave and s-concave densities. Annals of statistics, 44(3):954, 2016.

- Dümbgen & Rufibach (2009) Lutz Dümbgen and Kaspar Rufibach. Maximum likelihood estimation of a log-concave density and its distribution function: Basic properties and uniform consistency. Bernoulli, 15(1):40–68, 2009.

- Dümbgen et al. (2004) Lutz Dümbgen, Sandra Freitag, and Geurt Jongbloed. Consistency of concave regression with an application to current-status data. Mathematical methods of statistics, 13:69–81, 2004.

- Fan et al. (2024) Jianqing Fan, Yongyi Guo, and Mengxin Yu. Policy optimization using semiparametric models for dynamic pricing. Journal of the American Statistical Association, 119(545):552–564, 2024.

- Federgruen & Hu (2015) Awi Federgruen and Ming Hu. Multi-product price and assortment competition. Operations Research, 63(3):572–584, 2015.

- Gallego & Hu (2014) Guillermo Gallego and Ming Hu. Dynamic pricing of perishable assets under competition. Management Science, 60(5):1241–1259, 2014.

- Gallego & Wang (2014) Guillermo Gallego and Ruxian Wang. Multiproduct price optimization and competition under the nested logit model with product-differentiated price sensitivities. Operations Research, 62(2):450–461, 2014.

- Gallego et al. (2006) Guillermo Gallego, Woonghee Tim Huh, Wanmo Kang, and Robert Phillips. Price competition with the attraction demand model: Existence of unique equilibrium and its stability. Manufacturing & Service Operations Management, 8(4):359–375, 2006.

- Golrezaei et al. (2019) Negin Golrezaei, Adel Javanmard, and Vahab Mirrokni. Dynamic incentive-aware learning: Robust pricing in contextual auctions. Advances in Neural Information Processing Systems, 32, 2019.

- Goyal et al. (2023) Vineet Goyal, Shukai Li, and Sanjay Mehrotra. Learning to price under competition for multinomial logit demand. Available at SSRN 4572453, 2023.

- Groeneboom & Hendrickx (2018) Piet Groeneboom and Kim Hendrickx. Current status linear regression. The Annals of Statistics, 46(4):1415–1444, 2018.

- Han & Wellner (2016) Qiyang Han and Jon A Wellner. Approximation and estimation of s-concave densities via rényi divergences. Annals of statistics, 44(3):1332, 2016.

- Hsieh et al. (2021) Yu-Guan Hsieh, Kimon Antonakopoulos, and Panayotis Mertikopoulos. Adaptive learning in continuous games: Optimal regret bounds and convergence to nash equilibrium. In Conference on Learning Theory, pp. 2388–2422. PMLR, 2021.

- Javanmard (2017) Adel Javanmard. Perishability of data: dynamic pricing under varying-coefficient models. Journal of Machine Learning Research, 18(53):1–31, 2017.

- Javanmard & Nazerzadeh (2019) Adel Javanmard and Hamid Nazerzadeh. Dynamic pricing in high-dimensions. Journal of Machine Learning Research, 20(9):1–49, 2019.

- Kachani et al. (2007) Soulaymane Kachani, Georgia Perakis, and Carine Simon. Modeling the transient nature of dynamic pricing with demand learning in a competitive environment. Network science, nonlinear science and infrastructure systems, pp. 223–267, 2007.

- Keskin & Zeevi (2018) N Bora Keskin and Assaf Zeevi. On incomplete learning and certainty-equivalence control. Operations Research, 66(4):1136–1167, 2018.

- Kirman (1975) Alan P Kirman. Learning by firms about demand conditions. In Adaptive economic models, pp. 137–156. Elsevier, 1975.

- Koenker & Mizera (2010) Roger Koenker and Ivan Mizera. Quasi-concave density estimation. 2010.

- Kuchibhotla et al. (2021) Arun K Kuchibhotla, Rohit K Patra, and Bodhisattva Sen. Semiparametric efficiency in convexity constrained single-index model. Journal of the American Statistical Association, pp. 1–15, 2021.

- Li (1991) Ker-Chau Li. Sliced inverse regression for dimension reduction. Journal of the American Statistical Association, 86(414):316–327, 1991.

- Li et al. (2024) Shukai Li, Cong Shi, and Sanjay Mehrotra. LEGO: Optimal online learning under sequential price competition. Major Revision at Operations Research. Available at SSRN 4803002, 2024.

- Morrow & Skerlos (2011) W Ross Morrow and Steven J Skerlos. Fixed-point approaches to computing bertrand-nash equilibrium prices under mixed-logit demand. Operations research, 59(2):328–345, 2011.

- Mösching & Dümbgen (2020) Alexandre Mösching and Lutz Dümbgen. Monotone least squares and isotonic quantiles. 2020.

- Niculescu & Persson (2006) Constantin Niculescu and Lars-Erik Persson. Convex functions and their applications, volume 23. Springer, 2006.

- Vershynin (2010) Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- Wan et al. (2022) Yi Wan, Tom Kober, and Martin Densing. Nonlinear inverse demand curves in electricity market modeling. Energy Economics, 107:105809, 2022.

- Wan et al. (2023) Yi Wan, Tom Kober, Tilman Schildhauer, Thomas J Schmidt, Russell McKenna, and Martin Densing. Conditions for profitable operation of p2x energy hubs to meet local demand with energy market access. Advances in Applied Energy, 10:100127, 2023.

- Zhao (2008) Zhibiao Zhao. Parametric and nonparametric models and methods in financial econometrics. 2008.

Acronymous

| Acronym | Full Form |

| NE | Nash Equilibrium |

| LSE | Least Squares Estimator |

| NPLSE | Non-Parametric Least Squares Estimator |

| NPLS | Non-Parametric Least Squares |

| GLM | Generalized Linear Model |

| MLE | Maximum Likelihood Estimator |

| UCB | Upper Confidence Bound |

| SPE-BR | Semi-Parametric Estimation then Best Response |

Appendix Contents

Appendix A Proof of Proposition˜4.3

iff with . The statement follows by Proposition˜A.1.

Proposition A.1.

Let , a twice differentiable function. Then is -concave iff in .

A.1 Proof of Proposition˜A.1

As for is a known result, we prove it for . A function is -concave if and only if is concave, where is defined in Equation˜3. Then is -concave if and only if

Appendix B Proof of Lemma˜4.5

We first find an explicit solution of . We have , where . By ˜4.2, the first order condition of Equation˜7 is

or equivalently

| (14) |

In other words, are a fixed point for the map on the compact space ; i.e., . To show that Nash equilibrium prices exist and are unique, we only need to prove that is a contraction mapping. For any , we have

where

which is strictly less than by ˜4.4.

Appendix C Proof of Proposition˜6.3

For simplicity, we redefine as , . The loss function is defined as

Then the gradient and Hessian of is given by

Let be the global minimizer of . We do a Taylor expansion of around , with to be determined:

As is the global minimizer of loss , we have , that is

which implies

By Lemma˜C.1, the LHS satisfies

w.p. at least (as long as ) for certain constants and that depend only on the variance proxy of the sub-Gaussian random variable and, and by Lemma˜C.2 the RHS satisfies

with probability at least (as long as ), where is a constant that depends solely on and the variance proxies of the sub-Gaussian random variables and . Putting the two inequalities together we get with probability at least that, for sufficiently large

where . Now we conclude. Recall that from Equation˜15 we have that . Let

Let be large enough so that : this guarantees that any is such that , which come from the fact that . Then for we can write

and, as with probability at least , for sufficiently large, this implies that with the same probability bound

where which concludes the proof.

Lemma C.1.

There exist such that with probability at least we have , where

Proof.

To get a lower bound of the minimum eigenvalue of we use the following remark 5.40 of Vershynin (2010): let be a matrix whose rows are independent sub-gaussian random vectors in with second moment matrix (non necessarily isotropic), then there exist depending only on the sub-gaussian norm, such that for every we have with probability at least , where . In our case, since is an average of i.i.d. random matrices with mean and that are sub-Gaussian random vectors (recall that is sub-gaussian because the generator satisfies for all ), then there exist such that for each with probability at least ,

Here are both constants that are only related to sub-Gaussian norm of . Now, choosing , then as long as we have . Thus with probability at least we have

and since we get , and considering the first and last term we get

and since we get . ∎

Lemma C.2.

With probability at least , for sufficiently large, we have , where is a constant that depends solely on and the variance proxies of the sub-Gaussian random variables and .

We first prove that for all ,

Using the known property of elliptically symmetric random variables (see, e.g. Li (1991, page 319, comment following Condition 3.1) or Balabdaoui et al. (2019, Section 9.1)) we have that

where is a vector that has to satisfy or equivalently (using ), . We have

which is equal to as long as we choose

Note that : indeed, as is increasing, it implies that, given independent copy of

| (15) |

Thus, , then every entry of is mean zero, i.e.

Now, since is sub-gaussian (because is sub-gaussian) with variance proxy denoted as and is sub-gaussian (because the generator satisfies for all ) with variance proxy denoted as , is sub-gaussian, and given that is sub-gaussian, the product is sub-exponential. More specifically

| (16) |

where is the Orlicz norm associated to , with . For , is equivalent to belonging to the class of sub-exponential distributions, while with , is equivalent to belonging to the class of sub-gaussian distributions. Then for , that is

Now, using that are independent for all , with we get

By taking , for sufficiently large we have that

and then

with probability at least .

Appendix D Proof of Proposition˜6.5

We start by proving point (1). We have be an elliptically symmetric random vector with density

where is the location vector, is a positive-definite scatter matrix, is the density generator, and is a normalizing constant. We wish to find the conditional density of given , where is a fixed vector. The constraint defines a hyperplane:

The conditional density satisfies:

that is,

where is the normalizing constant. Define the transformation:

where satisfies . Then, since , the density becomes:

The constraint transforms as:

Define , so that the constraint simplifies to:

| (17) |

Decomposing into components parallel and perpendicular to , we write:

| (18) |

Then . From the constraint in Equation˜17:

Since the original density in the -space is

when conditioning on , the conditional density on the -dimensional space of is:

Now, using the assumption that we have that

| (19) |

Now, recall that

| (20) |

where we defined the conditional center (the "shift")

| (21) |

Thus,

| (22) |

This completes the proof of (1). We now prove point (2). By Appendix˜D we have

where is independent of . We note that is bounded, because is bounded, proving point (2). Now we prove point (3). We first define

| (23) |

where we recall from Equation˜21 that . Note that

Assume that for some , then

and if is -Hölder we have

where we used that

Moreover . Now we proove point (4). We can write

Note that

for some , where we used that and that , which is a bounded set. We then have

where we have used that

is finite because since , then has exponential decay. Now we prove point (5). Recall that

where

First note that if , we have , since , and then . Now suppose . More generally, we will prove that for non-negative functions integrable in that satisfy

then

where

where is a probability measure.

Lemma D.1.

Let , , and , and let nonnegative be integrable functions on satisfying

For every fixed define and as

where for a non zero vector , a nonzero real value and a constant , and is a probability measure, then

where we have defined

Proof.

We have

We can write

and by assumption on we have that

and then

where in we used that for the map

is convex on , and then we can apply Niculescu & Persson (2006, Theorem 3.5.3), which is an extension of the Jensen’s inequality for in variables. ∎

Appendix E Proof of Theorem˜6.9

Now we compute the regret upper bound of a single firm . Recall the definitions

so that , where

By first order condition, we have that

| (24) |

where in the first inequality we used that

for some in the segment between the points and , and then, since , we have and for some , which implies

Lemma E.1.

If Assumptions in the Theorem hold, for sufficiently large we have for any .

Lemma E.2.

If Assumptions in the Theorem hold, for sufficiently large, implies for every .

By Lemma˜E.1, Lemma˜E.2 have that for with sufficiently large,

and as a consequence, give that , for every

Then we get

and for

E.1 Proof of Lemma˜E.1

Let be the minimum exploration phase among the firms and . Let be the length of the exploration phase to estimate and the remaining length for estimating the link function . Define the event where as defined in Proposition˜6.3, and

We can write

Analyzing the :

By Proposition˜6.3 we have .

Analyzing the :

Analyzing on : Define the event . For sufficiently large, by Theorem˜6.6 we have that

where we chose .

Analyzing on : By Proposition˜6.5, is Lipschitz, then .

Analyzing on : By Proposition˜6.5 we have .

Combining the terms and : Given that and that carries the factor, the dominating term turns out to be .

E.2 Proof of Lemma˜E.2

Recall the definition

and

We have

Then we have that for every ,

that implies

Appendix F NPLS for -concave regression

Inspired by the work of Dümbgen et al. (2004), we prove a uniform convergence result for the NPLSE of a mean function that can be written as an increasing function composed with a concave function . Suppose that we observe with fixed numbers and independent random variables with

for unknown function , where is an known interval containing . Assume that

| (25) |

for some known increasing twice differentiable function and unknown concave function . We denote the class of functions that can be written as with , which includes log-concave functions () and more generally -concave functions for every real ( if and if ).

Now we go back to general transformation . We assume that for some , so that . Let such that . Then on for some , where and depend on and . Note that are well defined, indeed, by Weierstrass theorem, is locally bounded, that is for every compact set there exists such that in . Then we can write

| (26) |

where is the set of all concave functions . When (or equivalently for -concave functions), Equation˜26 was studied by Dümbgen et al. (2004), for which exists and is unique and doesn’t need restrictions on the codomain of , that is can be the whole . Proposition˜F.1, which is followed by Lemma˜F.7, shows the constraints on the codomain of when is -concave for .

Proposition F.1 (Constraints for -concave transformations).

Suppose that is -concave, that is for some , where as defined in Equation˜3. Then

By Weierstrass’ theorem, a solution of Equation˜26 exists, but might not be unique. Let be a solution of Equation˜26. We consider a triangular scheme of observations and but suppress the additional subscript for notation simplicity. Let be the empirical distribution of the design points , i.e.

We analyze the asymptotic behavior of on a fixed compact interval

under certain conditions on , the probability measure of the design points, and the errors

Assumption F.2.

The probability measure of the design points satisfies for some and for all with .

Assumption F.3.

For some constant ,

Assumption F.4.

There exists a and such that for all

| (27) |

˜F.2 holds if the density of the measure is bounded away from zero, that is , which is a standard assumption for uniform convergence of non-parametric functions (see e.g. Dümbgen et al. (2004); Mösching & Dümbgen (2020)) as well as for convergence (see e.g. Groeneboom & Hendrickx (2018); Balabdaoui et al. (2019)).

Theorem F.5.

Suppose that ˜F.2, ˜F.3 and ˜F.4 are satisfied. Let be a solution of Equation˜26, and let . Then, for all there exists a integer and a real value such that

where depends on , , , , , and , and for some .

Remark F.6.

F.1 Tecnical Lemma 1

Lemma F.7.

Recall the definition

Then it holds

where

| (28) |

for and for . As a consequence, for every real , the function is increasing on with the following bounds

Proof.

Case 1. . Then is increasing and is increasing for , for and is decreasing for .

Case 2. . Then and .

Case 3. . Then is decreasing and increasing.

Conclusion. If , then we

and specifically

where

for and for . ∎

F.2 Technical Lemma 2

˜F.2 implies the following Lemma˜F.8 that will be used to prove the uniform convergence consistency in Theorem˜F.5.

Lemma F.8.

Let and stands for Lebesgue measure and i.i.d. points with probability measure that satisfies ˜F.2, then for a given constant , and for any there exists and a sequence , such that

where is the event

This result immediately follos from the proof of the more general result by Mösching & Dümbgen (2020, Section 4.3) which can be stated as follows:

Lemma F.9.

Let such that while (as ). Then for every , there exists and , such that

where are respectively the probability measure and the empirical probability measure of the design points , that is

and

where . The value is the smallest integer that satisfies .

F.3 Proof of Theorem˜F.5

First note that for every , since , then . By assumption we also have for some . Let be a solution of Equation˜26, i.e. the LS estimate of . Then, being a minimizer, we have that for any direction such that for sufficiently small, . Hence the directional derivative at along direction satisfies

Fix such a direction that will be selected later. We have

Adding and subtracting we get

| (29) |

In what follows we apply Equation˜29 to a special class of perturbation functions and write

The next Lemma˜F.10 is proved in Section˜F.4

Lemma F.10.

For an integer , let be the family of all continuous, piece-wise linear functions on with at most knots. Then for any fixed ,

with probability at least .

The next ingredient for our proof is a result concerning the difference of two concave functions, which can be found in Dümbgen et al. (2004, Lemma 5.2) and we report the proof in Section˜F.5 for completeness.

Lemma F.11.

Let satisfy ˜F.4. There is a universal constant with the following property: for any , let . Then, for any concave function

implies

for some . More specifically we have .

Now, we have to show that one of our classes does indeed contain useful perturbation functions . We denote with the unique continuous and piecewise linear function with knots in such that on . Thus is one particular LS estimator for . The following technical Lemma˜F.12 can be found in Dümbgen et al. (2004, Lemma 3).

Lemma F.12.

For let

Suppose that on some interval with length . Then there is a function such that

| (30) |

Now we prove the theorem. Consider the event

for some (random) that we aim to prove to be . Then we have . It follows that

From Lemma˜F.11, replacing

there is a (random) interval on which , provided that

-

•

is sufficiently large to guarantee that , so that .

-

•

. This condition comes from the fact that that is .

Because is a sub-interval of on length , Lemma˜F.8 (which holds by ˜F.2) guarantees that this interval contains at least one observation . This implies Lemma˜F.12. For any define . Define also . Using that with (which comes from Lemma˜F.7) we have that

and as a consequence, using that we have

| (31) |

Recall that . By the definition of and Lemma˜F.12, there is a (random) function such that

Consequently,

Now consider the event in Lemma˜F.10 and the event in Lemma˜F.8. For define

which holds with probability at least . In we have

where we used that is a positive quantity appearing in the denominator. More precisely we have that

then with probability less than we have provided (by Lemma˜F.10)

More precisely, the condition on is that , where .

F.4 Proof of Lemma˜F.10

˜F.3 implies the following inequality

| (32) |

for any function with and arbitrary . Indeed, since , we have

| (33) |

where and . We get

where we used that is maximized at . Equivalently we get

and

For , let

if . Otherwise let and .

This defines a collection of at most different nonzero functions . Then for any fixed , Equation˜32 implies

where

For let . Then by Equation˜32,

| (34) | ||||

because . Recall that is the family of all continuous, piecewise linear functions on with at most knots. For any , there are disjoint intervals on which is either linear and non-negative, or linear and non-positive. For one such interval with let . Then

This shows that there are real coefficients and functions in such that on , and for all pairs . Consequently,

The last inequality is due to Cauchy-Schwarz inequality

Thus by Equation˜34 we have that

Setting we get the result.

F.5 Proof of Lemma˜F.11

We divide the proof in 2 parts. Part A: for some . Part B: for some .

Part A

Suppose that for some . Without loss of generality let . Define the linear function

where . Define the concave function . Now, note that by ˜F.4 we have

| (35) |

Now, since by assumption we have

| (36) |

Now let .

-

•

Step 1.A. Since is concave, it follows that if then, joint with Equation˜36, on .

-

•

Step 2.A. Now assume . By concavity of we have

Consequently, for

-

•

Step 1.A + 2.A: or on some interval with length . Using this fact and Equation˜35, we have that

is greater or equal than

which is greater or equal than provided that .

Part B

Now suppose that for some and , where . By ˜F.4 and concavity of both there exist numbers such that

and

Thus

for all in the interval or , depending on the sign of . Moreover, , provided that .

Appendix G Proof of Theorem˜6.6

Let be the asymptotic fraction of points lying in , where is the sample size and . Define the empirical fraction of points in as the random quantity

By Lemma˜F.9, the event

holds with probability at least for some , provided that is sufficiently large and as . Now, we apply Theorem˜F.5, using Remark˜F.6, with the following substitutions:

where is defined in Equation˜3. Intersecting with the high-probability event in Theorem˜F.5 yields the desired result. The only remaining step is to verify that the assumptions of Theorem˜6.6 imply those of Theorem˜F.5.

-

(1)

is -concave for some . According to Proposition˜6.5, this condition is satisfied provided is -concave for some , which holds by Proposition˜4.3 and ˜4.2.

-

(2)

˜F.2 holds uniformly in because the design points are drawn from an i.i.d. truncated elliptically symmetric distribution with density generator and then on any bounded interval, then for some .

-

(3)

˜F.3 holds because are sub-gaussian (indeed is bounded and are sub-gaussian) and is bounded uniformly in by point (2) of Proposition˜6.5.

-

(4)

˜F.4 holds uniformly in because by point (3) of Proposition˜6.5, which implies where , defined in Equation˜3.

Appendix H Remark on ˜6.7

˜6.7 informally states that the revenue functions are smooth around the NE. ˜6.7 is satisfied in several scenarios, for example when for all for some independent of . Indeed, in this case, since we have that . Now we give some examples where the condition for all for some independent of is satisfied:

-

(1)

Linear demand models (Li et al., 2024). In this case , and .

- (2)

-

(3)

s-concave demand functions. Suppose that satisfies ˜4.1 and ˜4.2. Then, by Proposition˜4.3, is -concave for some , and by Proposition˜A.1 this is equivalent to . This implies that

and since a sufficient condition is that

for some constant . Note that since is non-negative, for the condition is trivially satisfied with , indeed this condition coincides with the case studied before for concave demand functions. When the condition becomes

where we set . Note that the left-hand side is always negative, then the inequality makes sense if the right-hand side is negative too, i.e. if , or . For example, suppose that is -concave (i.e. log-concave), that is for some increasing concave function , where needs to be increasing in order to guarantee that is increasing. The condition becomes

and it’s easy to see that any for sufficiently small, indeed the condition becomes which holds in as long as , or . Another example is for sufficiently large, indeed the condition becomes or for some , and mast by such that .

-

(4)

General condition on derivatives. The condition is satisfied if and , indeed we have