Time After Time: Deep-Q Effect Estimation for Interventions on When and What to do††thanks: accepted for presentation at the International Conference on Learning Representations (ICLR) 2025

Abstract

Problems in fields such as healthcare, robotics, and finance requires reasoning about the value both of what decision or action to take and when to take it. The prevailing hope is that artificial intelligence will support such decisions by estimating the causal effect of policies such as how to treat patients or how to allocate resources over time. However, existing methods for estimating the effect of a policy struggle with irregular time. They either discretize time, or disregard the effect of timing policies. We present a new deep-Q algorithm that estimates the effect of both when and what to do called Earliest Disagreement Q-Evaluation (EDQ). EDQ makes use of recursion for the Q-function that is compatible with flexible sequence models, such as transformers. EDQ provides accurate estimates under standard assumptions. We validate the approach through experiments on survival time and tumor growth tasks.

1 Introduction

Sequential decision-making is common in healthcare, finance, and beyond [7, 50]. In hospitals, medical professionals administer treatments at different times based on the evolving observations of a patient’s condition; in financial markets, traders execute orders based on sequential information flows. Algorithmic decision support systems can optimize these processes by evaluating different policies with respect to their expected outcomes. Estimating the difference in expected outcomes between various policies is a causal effect estimation question [19, 51, 7]. This question involves several future treatment decisions taken at varying time points, hence it is a sequential decision-making problem.

Formally, this problem falls within the framework of off-policy evaluation [49, 12]. A defining feature is that timings of observations and treatments are irregularly spaced, represented by a stochastic point process with intensity , whereas the type of the treatments at those times are specified as the marks of this process, governed by a distribution . Unlike traditional formulations of off-policy evaluation that focus on action types, here the times must be accounted for, as they have a large effect on the outcome. This formulation is relevant to many decision-making scenarios, for example, in transplants, where it is often desirable to delay treatment as much as possible to lower the risk of complications. However, delaying too much can result in a deterioration in the patient’s condition. Here, the type of treatment is fixed and what matters is the timing.

Estimating the effect of intervention on treatment timing is a crucial part of evaluating sequential policies. With irregular times, frameworks for sequential decision-making that discretize time can be problematic, as discretization can be inaccurate or inefficient and requires choosing appropriate time scales. Further, length scales for decision-making within a single trajectory can vary dramatically. Consider for example a patient with heart failure; such a patient may be stable for months or years with occasional treatment adjustments made during visits to the cardiologist. However, at some point, they may experience acute decompensation [11], which requires rapid treatment and intensive monitoring during hospitalization. Existing methods for continuous-time causal inference do not scale gracefully, since they solve complex estimation problems, such as integrating importance weights across time [40]. Those methods that scale to high-capacity models and large datasets do not handle dynamic policies (i.e., policies that take past states into account) and are implemented with differential equation solvers [46], restricting architectural choices.

In this work, we give two methods for off-policy evaluation with irregularly sampled data. Our contributions are as follows:

-

•

We define off-policy evaluation with decision point processes and develop Earliest Disagreement Q-Evaluation (EDQ), a model-free solution to the problem. While other methods are intractable in high dimensions or are limited to static treatments, EDQ eliminates these restrictions. EDQ is based on direct regressions and dynamic programming, which makes it easily applicable to flexible architectures including sequence models such as transformers.

- •

-

•

We validate the efficacy of EDQ through an experimental demonstration on time-to-failure prediction and tumor growth simulation tasks. For these tasks, we implement a transformer-based solution. The results show EDQ’s advantage relative to baselines that rely on discretization.

We define the estimation problem, develop a solution, discuss related work and validate empirically.

2 Off-Policy Evaluation with Decision Point Processes

Consider a decision process defined by a marked point process [3, 47] over observations (which take values in ), treatments (in respectively) and real outcomes. We are interested in estimating an overall quantity that is a function of a sequence of observed rewards. For convenience, we let , where is an index for observed outcomes along the trajectory.111We define for an event where is larger than the number of outcomes in the trajectory. Though, the methods extend to other outcome functions like discounted future outcomes. We assume the number of rewards in the segment is finite.

Marked point processes.

A marked point process is a distribution over event times, along with distributions over marks, or details of the events at each time (i.e. treatment times and which treatment was given). We consider multivariate counting processes on the time interval . For a univariate process, e.g. , is the number of events of type until time . A trajectory of event times and their marks is a set . We denote events up to time by and for events in the interval . We use to refer to events of type on the trajectory and for events of all types other than .

Finally, we assume intensity functions for processes exist, is almost surely finite for any , and that the process can depend on its own history. That is, the filtration is the -algebra generated by random variables and their marks [1].

2.1 Problem Definition

We follow notation from the RL literature [50]. We begin with the data generating process and then summarize our goal of inferring causal effects. This involves off-policy evaluation under a distribution , while observing samples from .

Definition 1.

A marked decision point process is a marked point process with observed components for that have corresponding intensity functions , and mark spaces , and a multivariate unobserved process with intensity . By default, we omit unobserved events from the trajectories , hence where . The intensity function and mark distribution are called the policy. The mark distributions for are denoted by .

Off-policy evaluation.

We are given a dataset of trajectories, where trajectory has observations: . These are sampled from an observed decision process with policy . Treatment times are samples from a counting process with intensity and treatments at those times are sampled from . We reason about outcomes when is replaced with a target policy ), with other processes in fixed. The resulting decision process is denoted , and our goal is to estimate the expected future outcome for all and in the natural filtration associated with the point process.

When to treat.

To simplify notation, we omit the marks and focus on intensities . That is, we explore interventions on when to treat (medicine weekly or monthly?) instead of how to treat (which medication?). Technically, “when" is the more challenging and underexplored part of the problem, and solutions can be easily extended to incorporate interventions on using existing methods [6, 22]. In the ASCVD example, this corresponds to reasoning about questions like: “Consider prescribing statins to patients with characteristics , whose LDL cholesterol is below 180 mg/dl up to time . What would be the expected change in 10-year ASCVD risk if going forward, we prescribe a daily dose of statins for patients whose LDL cholesterol goes above 180 mg/dL, instead of the existing policy followed in the population?".

2.2 Roadmap to identifiability via Local Independences

The goal of this section is

to elucidate the conditions under which the algorithm we present in section˜3 estimates valid causal effects. We briefly summarize the essential conditions and supplement this summary in appendix˜D.

Our assumptions to ensure identifiability of causal estimands follow Røysland, [40], Røysland et al., [42], Didelez, [10], who study graphical models for point processes.

In this setting,

where the goal is to intervene on and estimate under rather than , in the presence of unobserved processes ,

[41] define and analyze the following notions:

-

•

A graphical condition called causal validity ensures that changing the treatment intensity from to the interventional , while changing no other intensities, changes the joint distribution from to . A graph may not be causally valid when it contains unobserved variables .

- •

-

•

A certain set of local independences together are referred to as eliminability (a generalization of the backdoor criterion), which implies casual validity, even with unobserved variables .

Consider the graph in Figure˜2, where an edge means that the history of the source node affects the future of the target node [10]. It is possible to show that it satisfies eliminability (see appendix˜D). To understand this condition, we start with the basic local independence requirements.

Definition 2.

For a multivariate process on variables we say that is locally independent of given , or , if . A graphical local independence model is a class of processes on and directed graph , such that holds for all .

This condition means that the intensity of a process only makes use of certain information from other processes. [42] package together the set of local independences that imply causal validity under the name eliminability, defined below. They use a graphical criterion that is akin to using d-separation in graphical models, while we state the conditions in terms of the implied functional independencies of intensities. We expand on this in appendix˜D.

Definition 3.

Let be the set of unobserved variables. Suppose can be written as a sequence such that for each , either

-

•

is locally independent of given , or

-

•

is locally independent of given .

Then the graph is said to satisfy Eliminability. Here, for sets and variable we say is locally independent of given if each is locally independent of given .

We summarize that causal validity holds under the local independences that satisfy eliminability. We assume the graph in Figure˜2, which satisfies these assumptions. We also assume mutual independence of increments of all processes at a one time to rule out instantaneous effects. We refer to validity and this independence together as ignorability, in accordance with existing terminology on confounding.

Assumption 1.

Ignorability (in continuous time) is satisfied when:

-

1.

the graph satisfies causal validity,

-

2.

the increments of features, treatments, and outcome are mutually independent given the history, i.e., .

In addition to ignorability, we require a second, standard assumption, overlap, for the conditional expectations we estimate to be well-defined. Recall that the interventional distribution is defined by replacing the treatment distribution in , i.e., replacing with .

Assumption 2.

Overlap is said to hold between the observational and interventional distributions, and , if is absolutely continuous with respect to , denoted by .

Ignorability and overlap are the core assumptions that allow identification in our setting. Under these assumptions, we can now present algorithms for estimating causal effects in continuous time.

3 Model Free Off-Policy Evaluation for Decision Point Processes

To estimate for times and that overlap with , we express the expectation recursively as a function of expectations for some and trajectory . Then, assuming that expectations at times larger than have been learned correctly, this recursive expression allows us to propagate information for conditioning on earlier histories. Let us describe this solution in more detail, as applied in the context of -evaluation.

Fitted Q evaluation (FQE) in discrete time. Q-evaluation relies on the tower property of conditional expectations, given below in eq.˜1. In discrete time decision processes, where we consider , the property suggests a dynamic programming solution that we lay out in algorithm˜1 [20, 55]. Here, includes all treatments and observations up to and including time , and since they occur simultaneously, there are exactly of each. is defined in the same manner, except that it includes sampled from the target policy .

| (1) |

An attractive property of this algorithm is that it is model-free. That is, to form the label we only need to sample from our target policy , while a model of is not necessary.

With accurate optimization over a sufficiently expressive hypothesis class and arbitrarily large datasets, algorithm˜1 returns correct estimates. This is because if we fix and assume that it accurately estimates , then the minimizer of the regression is the conditional expectation, equal to according to eq.˜1. The model-free solution is enabled by the equality , which validates the use of to form . In practice, we take gradient steps on randomly drawn times and training samples instead of walking backward from to . Crucially, for , e.g. , we have . Hence, an algorithm using eq.˜1 must either be model-based, or resort to solutions such as importance weights that suffer high variance [37, 14], or restrict the problem, e.g., by discounting rewards [29, 15, 37].

Challenges in application to continuous time. Moving to continuous time, the tower property turns into a differential equation, and solving it requires tools that go beyond common FQE (e.g., Jia and Zhou, [17]). Regressing to an outcome that is arbitrarily close to the observation at time is ill-defined. While we may work under a fine discretization of time, this approach is wasteful, as a single update in the minimization for estimating takes into account the development of the process in the interval , and for small values of this will usually yield a very small change to the estimate. Hence, intuitively, when updating , we would like to use estimates of for a large . As explained above, this is seemingly difficult to achieve in a model-free fashion. However, for point processes, since the number of decisions over is countable, it seems plausible that a simple and efficient dynamic programming solution can be devised. In what follows, this is what we present.

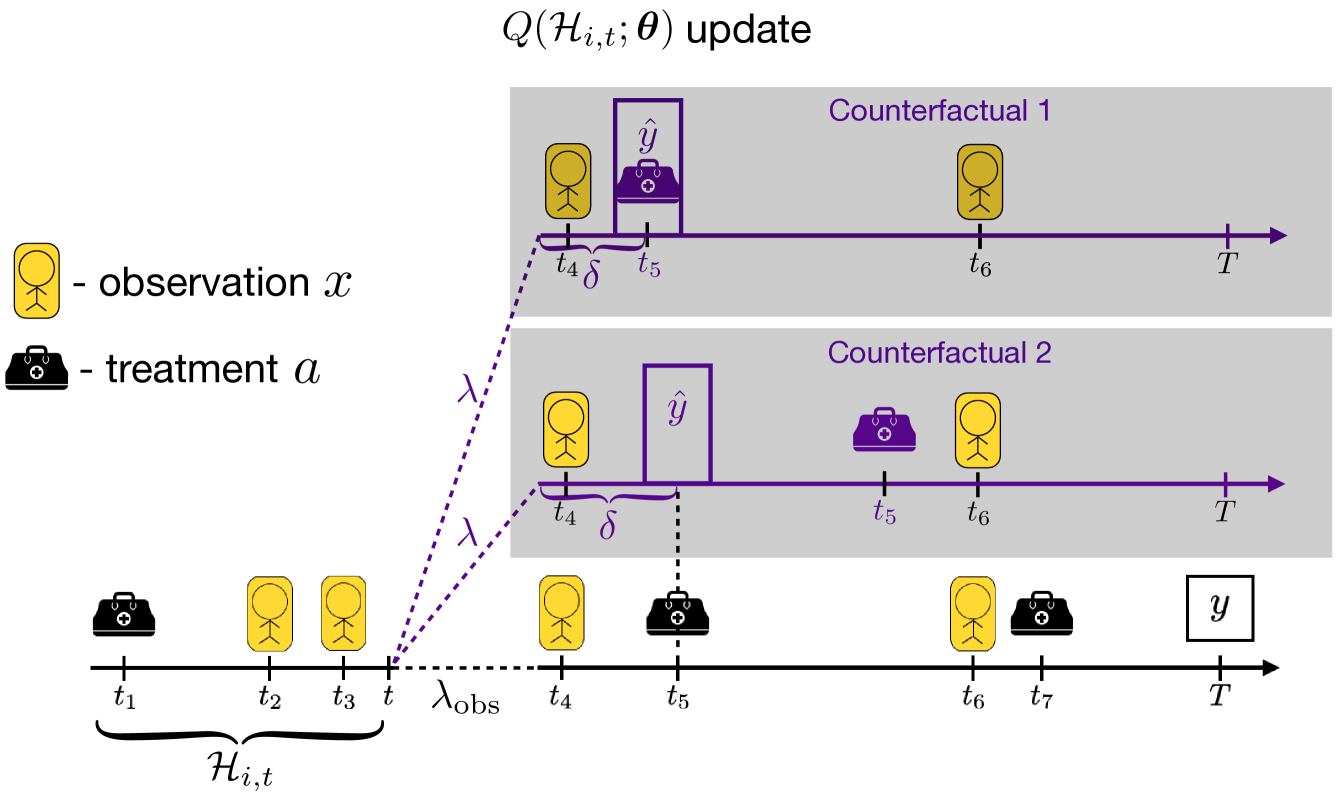

3.1 EDQ: Fitted Q-Evaluation for Decision Point Processes via Earliest Disagreement Times

We wish to reason about what the outcome would have been for an observed trajectory sampled under policy , had we treated it with policy from time onward. Intuitively, it seems plausible that we can use a similar approach to FQE, but instead of going one time unit forward, we can move to the first time where the two policies differ in their treatments. That is, we will sample alternative treatment trajectories, asking what the target policy would have done at each time, given the observed history up until that time and find the earliest disagreement. The resulting algorithm is rather simple, and we summarize it graphically in fig.˜1. The attractive property of this approach is that the “lookahead" time is adaptive. It will likely be short when applied in parts of trajectories where many treatments are applied, and longer when treatments are scarce.

To formalize the method, we present some additional notation, prove an appropriate variation of the tower property, and explain how it is operationalized by the implementation in algorithm˜2.

Definition 4.

For process and policy , define an augmented process where intensities are independent of the history of : (1) the intensity of is , i.e. where history of treatments is given by , 222Note that this is a slight abuse of notation, since is not a random variable. and (2) for . For a trajectory and time , define , where when the set is empty.

The augmented process maintains an additional treatment trajectory, , as an alternative to , the one observed under . From definition˜4, we observe that the intensities of the augmented process do not depend on ’s history. It follows that the marginal over is , while has a similar role to the alternative treatment in algorithm˜1. This notation is helpful for denoting sampled alternative trajectories over time intervals. Finally, denotes the earliest disagreement between observed and target treatments after time .333The minimum treatment time is also the earliest disagreement, since under some regularity conditions, the processes and have probability of jumping simultaneously. Our model-free evaluation method is based on the following result, which expresses our estimand as an expectation over trajectories .

Theorem 1.

Let be a marked decision point processes, the process obtained by replacing the policy with , and the augmented process obtained from in definition˜4. Further, let , and measurable w.r.t . Under Assumption 2, we have that

| (2) |

Takeaways from ˜1 and derivation of EDQ. Equation˜2 suggests a method to calculate expectations , similar to how FQE follows from eq.˜1. The practical version of the resulting method, EDQ, is given in algorithm˜2. To arrive at the method from eq.˜2, let us examine the regressions solved in algorithm˜2. Taking a random variable which is the sum of all outcomes after some time , eq.˜2 can be rewritten as follows (see Appendix˜A for a detailed derivation).

| (3) |

Algorithm˜2 uses gradient descent to fit functions that, at optimality, satisfy a self-consistency condition that appears in the equation above, . To this end, it solves regression problems where is fitted to a label . This label is defined in line and coincides with the term in the expectation above. To conclude that the algorithm estimates the effect of interest, two simple arguments suffice: (1) a uniqueness argument showing that the self-consistency equation holds only when matches , and (2) that despite ignoring the unobserved process , the estimation yields the desired causal effect due to the ignorability assumption. We summarize the conclusion below and provide detailed steps in appendix˜D.

Corollary 1.

An analogue of eq.˜2 holds for discrete-time decision processes, where EDQ bears some resemblance to the eligibility traces approach of Precup et al., [37]. We provide this result in section˜B.3 for completeness but focus here on the point process case, as this is our main motivation and where the earliest disagreement approach is most fruitful.

4 Related Work

Our coverage of related work is divided into an overview of works that solve adjacent tasks to ours, before transitioning into a detailed discussion in section˜4.1 about techniques more closely aligned with our goal of large scale causal inference in sequential decision making.

Causal inference with sequential decisions. Causal effect estimation for sequential treatments is usually studied in discrete time under the sequential exchangeability assumption [39, 16]. Addressing unobserved confounders is of interest [48, 32], but this is beyond our scope here. As described in section˜2.2, the framework of Røysland et al., [42] draws a parallel to sequential exchangeability for continuous time, which we adopt here. For estimation in these continuous-time problems, several methods have been explored [25, 24, 43, 40, 57]. Most do not scale to large and high-dimensional datasets. For instance, Røysland, [40] requires estimating an integral of propensity weights over time; Rytgaard et al., [43] propose a targeted estimator that fits each process in , but it is limited to interventions at fixed times (i.e. no interventions on treatment schedules) and it is unclear how to implement it with expressive models. Nie et al., [33] study the effect of timing when applying a fixed policy from time onward. However, they do not discuss interventions on all treatment timings, as we do here.

Reinforcement learning (RL) techniques. As discussed in section˜3, EDQ is related to FQE and Q-learning [20, 55, 30], and to -step methods from RL [29, 9, 37]. In the causality literature, Q-learning often appears in the context of dynamic treatment regimes [6, 5], where discrete-time policies are learned off-policy. All these methods are not applicable to irregularly sampled times. Works in RL that consider irregularly sampled times, either do not intervene on treatment times, or operate in the on-policy setting [38, 50], or incorporate continuous-time positional embeddings into decision transformers [8]. The latter facilitates the recommendation of sets of actions to arrive at a desired outcome [58] rather than evaluating a policy of interest. Recent work suggests that goal-conditioned imitation learning methods such as decision transformers may fail to estimate the causal effect of actions [26] in some scenarios where there are no unobserved confounders, whereas -learning methods produce correct estimates.

We next discuss scalable causal estimation methods for sequential treatments. We delineate assumptions, implementation choices, and subsequent properties of solutions from recent work.

4.1 Large Scale Estimation Approaches for Sequential Treatments

| Properties | Estimation Method | |||||||||||||||||||

|

|

|

|

|

|

|

||||||||||||||

| CGP | ✗ | ✗ | ✓ | |||||||||||||||||

| CRN , CT | ✗ | ✓ | ✗ | |||||||||||||||||

| R-MSN | ✗ | ✓ | ✗ | |||||||||||||||||

| TE-CDE | ✓ | ✗444We mark TE-CDE with as non-scalable, since the algorithm relies on differential equation solvers which limits the scalability of methods one can use. | ✗ | |||||||||||||||||

| G-Net | ✗ | ✓ | ✓ | |||||||||||||||||

| FQE | ✗ | ✓ | ✓ | |||||||||||||||||

| EDQ | ✓ | ✓ | ✓ | |||||||||||||||||

Notable early work on machine learning for estimating counterfactual quantities related to treatment timelines, Schulam and Saria, [44], used Gaussian Processes for estimation. Limitations such as scalability and incorporating various features prompted the development of deep learning approaches.

Large scale models. One family of solutions [23, 4, 28] took an important step forward by using RNNs and transformers for estimation. All of these methods build on the idea of learning balancing representations [18]. Roughly, these are representations under which the treatment is randomly assigned. This facilitates the training of high-capacity effect estimators on large datasets, but these works are restricted to discrete times.

Dynamic policies. The above methods can only estimate effects of static treatments, meaning the treatment plan cannot dynamically depend on future observations. For instance, consider a policy that prescribes a daily dose of statins, and if the patient develops side effects in the future, switches to another medication. This policy depends on possible future states, which the above methods do not accommodate. G-Net [22, 56] takes a model-based approach, where models are fit for both , and . Then at inference time, a dynamic policy is estimated when is replaced with the desired policy and conditional expectations of are estimated with Monte-Carlo simulations.

Irregular times. None of the above solutions address irregular observation and action times, a key focus of this paper. Some steps in this direction have been taken by Seedat et al., [46], Vanderschueren et al., [53]. Past work on irregular times includes Seedat et al., [46], who combine balanced representations with a neural controlled differential equation architecture suited for irregular sampling, while Vanderschueren et al., [53] use reweighting to adjust for sampling times that are informative of the outcome. However, these methods mitigate sampling-induced bias rather than estimate outcomes under interventions on treatment times. We further discuss them in appendix˜C.

Table˜1 summarizes the above techniques, along with FQE and EDQ. Notably, EDQ possesses the desirable qualities mentioned here and handles interventions on , which other solutions do not.

5 Implementation and Experiments

To implement EDQ for experimentation we use the GPT-2 architecture. Each token is a concatenation of embeddings of time , value and event type . The event types correspond to actions, features, and outcomes, while is introduced for convenience to represent cases where time passes but no events occur. Both absolute times and time gaps use continuous time positional embeddings: the -th dimension is for even , and for odd . Here and is the embedding dimension. We also keep a target network and update it with soft-Q updates, as is common in Deep Q-Networks, e.g., Van Hasselt et al., [52].

5.1 Baselines

We are unaware of baselines for effect estimation on treatment timing with high-dimensional or long-sequence data. Thus, we implement two baselines that let us glean important aspects of EDQ.

ERM / MC is an Empirical Risk Minimizer (ERM) trained to predict observed outcomes, which, also known as Monte-Carlo (MC) prediction in RL and policy evaluation. We use the same GPT-2 architecture and data representation as EDQ, but instead of running algorithm˜2, we train by minimizing prediction loss on observed data. Given each training trajectory with an outcome label , we solve , where is the squared loss. This method estimates outcomes under , therefore we expect it to perform as well as or better than off-policy evaluation methods, including EDQ, when , and to suffer a drop otherwise.

FQE is implemented following section˜3, but with discretized time and Q-updates using one timestep forward. At each iteration, we draw training example and time , define ), and take a gradient step on loss . Similarly, we define discrete-time approximations of our policies of interest, described later. The positional embeddings correspond to discrete times, and the representations of actions, features and outcomes at each time are concatenated. Other than this, we use the same architecture and hyperparameters of EDQ. This baseline examines the effects of time discretization on estimation and optimization.

Computational complexity: The per-iteration runtime of EDQ is similar to FQE, which is a common tool for large-scale offline RL problems, e.g. Paine et al., [36], Voloshin et al., [54]. EDQ and FQE differ in computation times due to sampling methods from the target policy used to draw the treatments used in the -update. We discuss this in appendix˜A.

5.2 Simulations on Time to Failure and Cancer Tumor Growth Prediction

To validate our method, we construct two settings. The first is to predict the effect of treatment timing policies on patients’ time-to-event. The second uses a cancer tumor growth simulator from Geng et al., [13] to form a policy evaluation problem on applications of chemotherapy and radiotherapy.

Simulators. We use two simulators. (i) Time-to-failure: In this setting, each data point simulates the vital of a patient measured regularly at a frequency of one time unit, and treatments are assigned irregularly in time according to an observational policy. Without treatment, the vital drops linearly where and is a noise term drawn at each time unit. Upon receiving treatment, the vital rises by an amount inversely proportional to the number of treatments, , applied up until that time, where is the maximal number of treatments that a patient can receive. That is, the efficacy of treatment reduces with repeated applications. We also inject small noise terms into the treatment dosage that a patient receives, which further affect the vital and add randomness to the problem. Figure˜3 shows an example simulated patient trajectory. (ii) Tumor growth: We use the experimental setting from Bica et al., [4], which other works use to study irregular sampling [46, 53]. As this is a commonly used simulator, we defer its details to appendix˜A and focus on the type of irregular sampling and policies we use. The simulator works in discrete time , and irregular sampling is induced by the features being unobserved at certain times. Namely, the covariate which represents tumor volume is observed with probability , where is the average tumor volume over the last timesteps, and is the maximum considered volume.

| ERM / MC | FQE | EDQ | |

Outcomes and policies. For (i) time-to-failure, our outcome of interest is failure time , where a patient dies if the vital drops to a value of . 555Note that the vital changes outside measurement times, hence death time does not generally coincide with vital measurement times. We focus on effect estimation for interventions on a rate parameter that controls the timing of treatment. At each time where the observed vital crosses a threshold, i.e. for some predetermined , a random time is drawn from an exponential distribution and treatment is applied at . The threshold and the dosage of treatment given are also part of the policy , yet to focus on the effects of timing we do not intervene on them in this experiment. At each experiment we observe patients treated under a policy with and aim to reason about the expected failure times under the interventional . In (ii) tumor-growth, the goal is to predict , where , under a policy that at time assigns treatment from four possible options: no-treatment, radiotherapy, chemotherapy, or combined therapy. Therefore, the estimation here is both on “when" and “what" to do. Policies are determined by two parameters and assign each type of treatment with probability . Here, is the last observed volume and is an intercept controlling how often treatments are applied, while controls the dependence of treatment assignment on tumor volume. Finally is the time of the last treatment, and the term induces a lag between consecutive treatments.

| ERM / MC | FQE | EDQ | |

| ERM / MC | FQE | EDQ | |

Experiments. We perform two sets of experiments for time-to-failure. In the first set, trajectory lengths range in , and there are treaments. In the second set (results in Figure˜4, right), we change the parameters of the problem by taking a high slope and capping at one treatment. This creates short trajectories of length between and . To evaluate the performance of the estimator, we sample trajectories under the target policy and treat every as a labeled data point. We then evaluate normalized RMSE between and the true labels . For tumor growth, we evaluate a policy that increases the likelihood of treatments (i.e increases ) and reduces , the correlation to the observed volume. Error is also calculated with normalized RMSE.

Results. The tables in fig.˜3 and fig.˜4 present results. They show that for time-to-failure, EDQ solves the estimation problem both when (blue rows, no intervention performed), and when (red rows). This is evident by comparing to ERM under the setting where , where ERM should be nearly optimal. 666this is up to numerical optimization issues, as we see FQE can outperform it in certain cases ERM takes a significant performance drop when , as expected. For FQE, while in the first set of experiments (fig.˜3), discretization should not result in significant information loss, it does create a more difficult optimization problem. This is because the updates to need to propagate backwards and most updates get noisy gradient signals by fitting to the value of a trajectory sampled one time step ahead, . This challenge for FQE is most evident in Figure˜3, where and FQE incurs a significant loss both when and when . The results in Figure˜4 (right) demonstrate the potential effects of information loss due to discretization. Here, since trajectories are short, the optimization problem of losses propagating is likely less pronounced. However, we see that there is still a significant drop when and (approximating a high rate of treatment when data was sampled under low rates). Taken together, these two experiments demonstrate two possible drawbacks of discretization. For tumor-growth, EDQ still outperforms the alternatives but suffers a decrease in performance due to distribution shift between observational and interventional distributions.

6 Limitations and Future Work

We have developed a method for off-policy evaluation with irregular treatment and observation times, which facilitates interventions on treatment intensities. We connected the setting to identifiability results from causal inference to highlight the conditions under which the estimates are meaningful, and proved the estimator’s correctness. EDQ is a “direct" method based on regression and, as demonstrated in experiments, is readily applicable to high-capacity sequence modeling architectures. To the best of our knowledge, it is the first available solution to this estimation problem that is applied with such architectures. Several limitations motivate exciting future research. Empirically, we plan to apply the method to large real-world datasets and additional simulators [34, 32]. The method does not handle censoring, which is required for reliable application in survival analysis and real trial data. Further developements include policy optimization in the setting we studied here and deriving bounds on errors due to unobserved confounding.

Acknowledgments

We thank Stefan Groha for helpful discussion in early stages of the project. This work was supported by National Science Foundation Award 1922658, NIH/NHLBI Award R01HL148248, NSF CAREER Award 2145542, NSF Award 2404476, ONR N00014-23-1-2634, IITP with a grant from ROK-MSIT in connection with the Global AI Frontier Lab International Collaborative Research, Apple, and Optum.

References

- Aalen et al., [2008] Aalen, O., Borgan, O., and Gjessing, H. (2008). Survival and event history analysis: a process point of view. Springer Science & Business Media.

- Aalen, [1987] Aalen, O. O. (1987). Dynamic modelling and causality. Scandinavian Actuarial Journal, 1987(3-4):177–190.

- Andersen et al., [2012] Andersen, P. K., Borgan, O., Gill, R. D., and Keiding, N. (2012). Statistical models based on counting processes. Springer Science & Business Media.

- Bica et al., [2020] Bica, I., Alaa, A. M., Jordon, J., and van der Schaar, M. (2020). Estimating counterfactual treatment outcomes over time through adversarially balanced representations. In International Conference on Learning Representations.

- Chakraborty and Moodie, [2013] Chakraborty, B. and Moodie, E. E. (2013). Statistical methods for dynamic treatment regimes. Springer-Verlag. doi, 10(978-1):4–1.

- Chakraborty and Murphy, [2014] Chakraborty, B. and Murphy, S. A. (2014). Dynamic treatment regimes. Annual review of statistics and its application, 1:447–464.

- [7] Chen, I. Y., Joshi, S., Ghassemi, M., and Ranganath, R. (2021a). Probabilistic machine learning for healthcare. Annual review of biomedical data science, 4(1):393–415.

- [8] Chen, L., Lu, K., Rajeswaran, A., Lee, K., Grover, A., Laskin, M., Abbeel, P., Srinivas, A., and Mordatch, I. (2021b). Decision transformer: Reinforcement learning via sequence modeling. Advances in neural information processing systems, 34:15084–15097.

- De Asis et al., [2018] De Asis, K., Hernandez-Garcia, J., Holland, G., and Sutton, R. (2018). Multi-step reinforcement learning: A unifying algorithm. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 32.

- Didelez, [2008] Didelez, V. (2008). Graphical models for marked point processes based on local independence. Journal of the Royal Statistical Society Series B: Statistical Methodology, 70(1):245–264.

- Felker et al., [2011] Felker, G. M., Lee, K. L., Bull, D. A., Redfield, M. M., Stevenson, L. W., Goldsmith, S. R., LeWinter, M. M., Deswal, A., Rouleau, J. L., Ofili, E. O., et al. (2011). Diuretic strategies in patients with acute decompensated heart failure. New England Journal of Medicine, 364(9):797–805.

- Fu et al., [2021] Fu, J., Norouzi, M., Nachum, O., Tucker, G., Wang, Z., Novikov, A., Yang, M., Zhang, M. R., Chen, Y., Kumar, A., et al. (2021). Benchmarks for deep off-policy evaluation. arXiv preprint arXiv:2103.16596.

- Geng et al., [2017] Geng, C., Paganetti, H., and Grassberger, C. (2017). Prediction of treatment response for combined chemo-and radiation therapy for non-small cell lung cancer patients using a bio-mathematical model. Scientific reports, 7(1):13542.

- Hallak et al., [2016] Hallak, A., Tamar, A., Munos, R., and Mannor, S. (2016). Generalized emphatic temporal difference learning: Bias-variance analysis. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 30.

- Harutyunyan et al., [2016] Harutyunyan, A., Bellemare, M. G., Stepleton, T., and Munos, R. (2016). Q () with off-policy corrections. In International Conference on Algorithmic Learning Theory, pages 305–320. Springer.

- Hernan and Robins, [2023] Hernan, M. and Robins, J. (2023). Causal Inference: What If. Chapman & Hall/CRC Monographs on Statistics & Applied Probab. CRC Press.

- Jia and Zhou, [2023] Jia, Y. and Zhou, X. Y. (2023). q-learning in continuous time. Journal of Machine Learning Research, 24(161):1–61.

- Johansson et al., [2016] Johansson, F., Shalit, U., and Sontag, D. (2016). Learning representations for counterfactual inference. In International conference on machine learning, pages 3020–3029. PMLR.

- Joshi et al., [2025] Joshi, S., Urteaga, I., van Amsterdam, W. A., Hripcsak, G., Elias, P., Recht, B., Elhadad, N., Fackler, J., Sendak, M. P., Wiens, J., et al. (2025). Ai as an intervention: improving clinical outcomes relies on a causal approach to ai development and validation. Journal of the American Medical Informatics Association, page ocae301.

- Le et al., [2019] Le, H., Voloshin, C., and Yue, Y. (2019). Batch policy learning under constraints. In International Conference on Machine Learning, pages 3703–3712. PMLR.

- Lewis and Shedler, [1979] Lewis, P. W. and Shedler, G. S. (1979). Simulation of nonhomogeneous poisson processes by thinning. Naval research logistics quarterly, 26(3):403–413.

- Li et al., [2021] Li, R., Hu, S., Lu, M., Utsumi, Y., Chakraborty, P., Sow, D. M., Madan, P., Li, J., Ghalwash, M., Shahn, Z., and Lehman, L.-w. (2021). G-net: a recurrent network approach to g-computation for counterfactual prediction under a dynamic treatment regime. In Roy, S., Pfohl, S., Rocheteau, E., Tadesse, G. A., Oala, L., Falck, F., Zhou, Y., Shen, L., Zamzmi, G., Mugambi, P., Zirikly, A., McDermott, M. B. A., and Alsentzer, E., editors, Proceedings of Machine Learning for Health, volume 158 of Proceedings of Machine Learning Research, pages 282–299. PMLR.

- Lim, [2018] Lim, B. (2018). Forecasting treatment responses over time using recurrent marginal structural networks. Advances in neural information processing systems, 31.

- Lin et al., [2004] Lin, H., Scharfstein, D. O., and Rosenheck, R. A. (2004). Analysis of longitudinal data with irregular, outcome-dependent follow-up. Journal of the Royal Statistical Society Series B: Statistical Methodology, 66(3):791–813.

- Lok, [2008] Lok, J. J. (2008). Statistical modeling of causal effects in continuous time. The Annals of Statistics, pages 1464–1507.

- Malenica and Murphy, [2023] Malenica, I. and Murphy, S. (2023). Causality in goal conditioned rl: Return to no future? In NeurIPS 2023 Workshop on Goal-Conditioned Reinforcement Learning.

- McDermott et al., [2023] McDermott, M., Nestor, B., Argaw, P., and Kohane, I. (2023). Event stream gpt: A data pre-processing and modeling library for generative, pre-trained transformers over continuous-time sequences of complex events. arXiv preprint arXiv:2306.11547.

- Melnychuk et al., [2022] Melnychuk, V., Frauen, D., and Feuerriegel, S. (2022). Causal transformer for estimating counterfactual outcomes. In International Conference on Machine Learning, pages 15293–15329. PMLR.

- Munos et al., [2016] Munos, R., Stepleton, T., Harutyunyan, A., and Bellemare, M. (2016). Safe and efficient off-policy reinforcement learning. Advances in neural information processing systems, 29.

- Murphy, [2005] Murphy, S. A. (2005). A generalization error for q-learning. Journal of Machine Learning Research.

- Nagpal et al., [2021] Nagpal, C., Jeanselme, V., and Dubrawski, A. (2021). Deep parametric time-to-event regression with time-varying covariates. In Survival Prediction-Algorithms, Challenges and Applications, pages 184–193. PMLR.

- Namkoong et al., [2020] Namkoong, H., Keramati, R., Yadlowsky, S., and Brunskill, E. (2020). Off-policy policy evaluation for sequential decisions under unobserved confounding. Advances in Neural Information Processing Systems, 33:18819–18831.

- Nie et al., [2021] Nie, X., Brunskill, E., and Wager, S. (2021). Learning when-to-treat policies. Journal of the American Statistical Association, 116(533):392–409.

- Oberst and Sontag, [2019] Oberst, M. and Sontag, D. (2019). Counterfactual off-policy evaluation with gumbel-max structural causal models. In International Conference on Machine Learning, pages 4881–4890. PMLR.

- Ogata, [1981] Ogata, Y. (1981). On lewis’ simulation method for point processes. IEEE transactions on information theory, 27(1):23–31.

- Paine et al., [2020] Paine, T. L., Paduraru, C., Michi, A., Gulcehre, C., Zolna, K., Novikov, A., Wang, Z., and de Freitas, N. (2020). Hyperparameter selection for offline reinforcement learning. arXiv preprint arXiv:2007.09055.

- Precup et al., [2000] Precup, D., Sutton, R. S., and Singh, S. P. (2000). Eligibility traces for off-policy policy evaluation. In Proceedings of the Seventeenth International Conference on Machine Learning, pages 759–766.

- Qu et al., [2023] Qu, C., Tan, X., Xue, S., Shi, X., Zhang, J., and Mei, H. (2023). Bellman meets hawkes: Model-based reinforcement learning via temporal point processes. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 37, pages 9543–9551.

- Robins, [1986] Robins, J. (1986). A new approach to causal inference in mortality studies with a sustained exposure period—application to control of the healthy worker survivor effect. Mathematical modelling, 7(9-12):1393–1512.

- Røysland, [2011] Røysland, K. (2011). A martingale approach to continuous-time marginal structural models. Bernoulli, 17(3):895 – 915.

- Røysland, [2012] Røysland, K. (2012). Counterfactual analyses with graphical models based on local independence. The Annals of Statistics, 40(4):2162 – 2194.

- Røysland et al., [2022] Røysland, K., Ryalen, P., Nygaard, M., and Didelez, V. (2022). Graphical criteria for the identification of marginal causal effects in continuous-time survival and event-history analyses. arXiv preprint arXiv:2202.02311.

- Rytgaard et al., [2022] Rytgaard, H. C., Gerds, T. A., and van der Laan, M. J. (2022). Continuous-time targeted minimum loss-based estimation of intervention-specific mean outcomes. The Annals of Statistics, 50(5):2469–2491.

- Schulam and Saria, [2017] Schulam, P. and Saria, S. (2017). Reliable decision support using counterfactual models. Advances in neural information processing systems, 30.

- Schweder, [1970] Schweder, T. (1970). Composable markov processes. Journal of applied probability, 7(2):400–410.

- Seedat et al., [2022] Seedat, N., Imrie, F., Bellot, A., Qian, Z., and van der Schaar, M. (2022). Continuous-time modeling of counterfactual outcomes using neural controlled differential equations. arXiv preprint arXiv:2206.08311.

- Snyder and Miller, [2012] Snyder, D. L. and Miller, M. I. (2012). Random point processes in time and space. Springer Science & Business Media.

- Tennenholtz et al., [2020] Tennenholtz, G., Shalit, U., and Mannor, S. (2020). Off-policy evaluation in partially observable environments. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 10276–10283.

- Uehara et al., [2022] Uehara, M., Shi, C., and Kallus, N. (2022). A review of off-policy evaluation in reinforcement learning. arXiv preprint arXiv:2212.06355.

- Upadhyay et al., [2018] Upadhyay, U., De, A., and Gomez Rodriguez, M. (2018). Deep reinforcement learning of marked temporal point processes. Advances in neural information processing systems, 31.

- van Amsterdam et al., [2024] van Amsterdam, W. A., de Jong, P. A., Verhoeff, J. J., Leiner, T., and Ranganath, R. (2024). From algorithms to action: improving patient care requires causality. BMC Medical Informatics and Decision Making, 24(1):111.

- Van Hasselt et al., [2016] Van Hasselt, H., Guez, A., and Silver, D. (2016). Deep reinforcement learning with double q-learning. In Proceedings of the AAAI conference on artificial intelligence, volume 30.

- Vanderschueren et al., [2023] Vanderschueren, T., Curth, A., Verbeke, W., and van der Schaar, M. (2023). Accounting for informative sampling when learning to forecast treatment outcomes over time. arXiv preprint arXiv:2306.04255.

- Voloshin et al., [2021] Voloshin, C., Le, H. M., Jiang, N., and Yue, Y. (2021). Empirical study of off-policy policy evaluation for reinforcement learning. In Thirty-fifth Conference on Neural Information Processing Systems Datasets and Benchmarks Track (Round 1).

- Watkins and Dayan, [1992] Watkins, C. J. and Dayan, P. (1992). Q-learning. Machine learning, 8:279–292.

- Xiong et al., [2024] Xiong, H., Wu, F., Deng, L., Su, M., and Lehman, L.-w. H. (2024). G-transformer: Counterfactual outcome prediction under dynamic and time-varying treatment regimes. arXiv preprint arXiv:2406.05504.

- Zhang et al., [2011] Zhang, M., Joffe, M. M., and Small, D. S. (2011). Causal inference for continuous-time processes when covariates are observed only at discrete times. Annals of statistics, 39(1).

- Zhang et al., [2023] Zhang, Z., Mei, H., and Xu, Y. (2023). Continuous-time decision transformer for healthcare applications. In International Conference on Artificial Intelligence and Statistics, pages 6245–6262. PMLR.

Appendix A Additional Comments on Experimental Aspects

Here we slightly expand on the comment about computational complexity in the main text, and give more details about the cancer simulation we use from Geng et al., [13], Bica et al., [4], Seedat et al., [46], Vanderschueren et al., [53].

A comment on computational complexity: As commented in the main text, the per-iteration runtime of EDQ is similar to that of FQE, which is a common tool in large-scale offline RL problems; for example, Paine et al., [36], Voloshin et al., [54] use it in benchmarks and evaluations. The difference in computation times between EDQ and FQE is due to sampling from the target policy, or more accurately , in order to draw the treatments used in the -update, i.e., and in algorithm˜2. In most applications, the added complexity due to this difference is small relative to the cost of evaluating the -function and its gradients. In turn, the cost of function evaluation is the same for FQE and EDQ. The computational complexity of sampling from depends on how it is represented and implemented. For instance, we may specify policies by allowing evaluations of , and sample using the thinning algorithm [21, 35]; with neural networks that allow sampling the time-to-next-event (e.g., see [31, 27] for examples of event time prediction); or with closed-form decision rules. For example, in the time-to-failure simulation, to determine treatment times we sample exponential variables every times the vital feature crosses a certain threshold.

Cancer simulator: The tumor growth simulation we use is adapted from Bica et al., [4], Seedat et al., [46], Melnychuk et al., [28] and is based on the work of Geng et al., [13]. Tumor volumes are simulated as finite differences from the following differential equation,

Here is the chemotherapy concentration, represents the level of radiothearpy. are effect parameters drawn for each patient from a prior distribution described in Geng et al., [13], and is a noise term. To create irregularly sampled observations of the tumor volume, at each time step we draw a value from a Bernoulli distribution to decide whether the trajectory contains the tumor volume at this time step or not. The success probability is a function of the average tumor volume over the most recent volumes (both observed and unobserved). If we denote a missing value by and the observation at timestep by (which equals if there is no sample at this timestep and otherwise), then sampling times are drawn according to the following probabilities:

The policies we use to decide on treatments draw binary decisions of whether or not to apply chemotherapy and radiotherapy at each timestep. Denoting these decisions by random variables and , they are drawn according to , where is the last observed volume before time and is the last time that treatment was applied before . The same probabilities are applied for . For more details on the specifics of the simulation, see the code implementation.

Appendix B Proofs

We begin with some notation and additional definitions, in section˜B.2 we prove the consistency result for our method, and in section˜B.3 we give its discrete-time version. To avoid cluttered notation and longer proof, we will give the proof of ˜1 for unmarked processes. Adding a distribution of marks is a trivial extension that does not alter the main steps of the derivation.

B.1 Notation and Definitions

For a multivariate point process we use the following notations:

-

•

is the sum , in our case this will include the components .

-

•

For any and any distribution or intensity, e.g. , we will use the conditioning to denote the event where jumps until time are those that appear in . That is, no events occur in the interval .

-

•

is the event in which jumps until time are those that appear in , and the next jump after that happens at time and is of type (i.e. and for ).

-

•

Given a trajectory and time , we define as the time gap from time to the first jump of process in trajectory after , that is for .

Note: This is a slight abuse of notation from the main paper, where we defined : dependence on is omitted and will be included whenever the trajectory is not clear from context, and we add a superscript (e.g. ) to specify the type of event we look for. -

•

Since the processes play a similar role throughout the derivation, as the parts of the process whose intensities are invariant under the intervention, we will shorten notation to

and .

We assume that all processes have well-defined densities and intensity functions, and that is absolutely continuous w.r.t. , . This means that the conditional expectations taken w.r.t. , which we use in our derivation, are well defined. We also adopt the convention where is almost surely finite for any and [3]. This means that the number of events in the interval is countable. We also use the notation for the indicator function that returns if the condition inside it is satisfied and otherwise.

B.2 Proof of Formal Results

Below we prove ˜1 where the result, eq.˜2, implies that performing dynamic programming using the -function from the earliest disagreement time between observed data, and the data sampled from the target distribution, results in a correct estimator. We derive that equation from the lemma below, which is similar to a tower property of conditional expectations with respect to the first jump that occurs in any component of the process.

Lemma 1.

Let be multivariate marked decision point processes, the corresponding augmented process, , and a history of events that is measurable w.r.t . It holds that

| (4) |

Proof.

Note that all the conditional expectations in the above expression exist since . Denoting the next jump time with a variable and its type by , when conditioning on some history , the law of total probability suggests that . In point processes, likelihoods of the form are given by . Expanding with the law of total probability and these likelihoods, while accounting for the option that no jump occurs in , we obtain the following expression.

| (5) |

Next we write down each item in lemma˜1,

| (6) |

The first equality simply expands the expectation as an integration over all possible stopping times for (according to the definition of , see definition˜4). The second equality holds since the intensities are equal to respectively. Then finally we simply add and subtract from the last item. Similarly, for the second item in lemma˜1

| (7) |

The last item in lemma˜1 is

| (8) |

Adding up section˜B.2, section˜B.2 and section˜B.2 while pulling out all the items multiplied by to the last brackets in the bottom expression, we get,

The items in the last brackets equal the right-hand-side of eq.˜5. Plugging this in we rewrite,

| (9) |

Note that we have,

| (10) |

because the left-hand-side is minus the probability that does not jump in the interval , and the integration on the right hand side is the probability that the process jumps at least once (where the first jump is at time ).

Next, we write the third item of lemma˜1 to see that it cancels the residual above in eq.˜9.

| (11) |

We expand again by towering expectations w.r.t to the first jump after ,

Multiplying the left hand side by we get a similar item where the integration on starts from instead of ,

Let us denote the gray item by , and multiply by the observed part in eq.˜11. In the first equality we will pull the integration on outside, then we will change the order of integration, change variables by a constant shift (), and push one integration back inside.

Plugging everything back into eq.˜11, we color in red the same item colored red above, where we change the name of variables back from to for convenience. The remaining item in the equation is obtained by collecting all the items that multiply in the obtained expression.

In the last equality we plugged in section˜B.2. Now it can be seen that the above expression cancels with the residual of eq.˜9, which means that lemma˜1 holds as claimed. ∎

As we explain in the sequel, ˜1 follows directly from the lemma below.

Lemma 2.

For any and , define such that is the time of the -th event after in a trajectory , where as an edge case.777as explained in section B.1, the full notation should be , but will be clear from context. That is, assuming then . Analogously, we define as , which is the -th event of type . For all we have that

| (12) | ||||

Now let us recall ˜1 and prove it, assuming that lemma˜2 holds. Then we will prove lemma˜2, which completes the proofs of our claims. See 1

Proof of ˜1.

Examine eq.˜12 when , because we assume the number of events is finite it holds that

That is because otherwise, the next treatments should occur after an infinite number of events, and we need to have infinitely many observations before time . By convention, we define whenever there fewer than events of type in the interval . Therefore, also due to the finite amount of events in , it holds that

Then we have,

Note that the limit when exists since from lemma˜2 the expectation has the same value for any value of . Next we make two observations:

-

•

The conditioning in the terms can be rewritten as for all items. This is because by definition of as , or when the set is empty,

In the next step we will replace these times with for all items.

-

•

All the events in the indicators are mutually exclusive, and exactly one of them occurs for each . This is since either occurs between the and -th event of type for some value of , or .

Combining these observations into the expressions we developed for , we conclude the proof,

∎

Next, let us complete the proof of the required lemma that we assumed to hold.

Proof of lemma˜2.

For , eq.˜12 is exactly lemma˜1 which we already proved in lemma˜1, and we will proceed by induction. Assume for some that eq.˜12 holds, this hypothesis is written below,

| (13) | ||||

Using the notation for shorthand, we may rewrite the last summand as

The first equality above used the law of total probability, while the second holds since the event and expectation only depend on events up to time . Next we expand the latter term, according to lemma˜1 and plug-in to the equation above.

Next we pull out the expectation over , and then use the law of total probability to turn this into a single expectation over a trajectory drawn from . Each occurrence of will then be changed to accordingly.

| (14) |

Let us simplify the multiples of all the indicators that appear in section˜B.2, while dropping the subscripts since they are clear from context.

| (15) |

Switching these equalities from B.2 into section˜B.2, we get

Then it is easy to deduce that the conditioning sets can be simplified as follows,

Plugging this back into eq.˜13 and using the linearity of expectation gives us exactly the equality in eq.˜12 and concludes the proof. ∎

B.3 Discrete Time Version

For the discrete-time version we keep a similar notation, but take time increments of and call the target policy , which takes a history of the process and outputs a distribution over possible treatments. The trajectory now simplifies to the form and similarly for the history . The analogous claim to ˜1 for these decision processes follows from the lemma we prove below by setting .

Lemma 3.

For any , and such that is measurable w.r.t we have that

| (16) |

Note that for , we define .

Proof.

Throughout the proof we will use conditioning on (where ) as a shorthand for conditioning on , as the meaning is clear from context. We will prove the claim by induction on . The base case for follows simply from observing that the value drawn for does not change the items inside the expectation . Let us write this down in detail.

| (17) |

The first equality, as we argued earlier is due to the conditioning set not depending on (as we defined earlier, it refers to ). Intuitively, this is true because we only expand the expectation one step forward in time. In the identity we wish to prove, lemma˜3, the treatments do change the item within since they determine the earliest disagreement time. The second equality is obtained by marginalizing over the sampled trajectories after time , as they are also not included in . Then the third equality writes the sampling of explicitly, and the fourth marginalizes over as we already mentioned it does not appear in the expectation. Then we use the equality , to write the expectation as sampling from . Finally, we use the tower property of conditional expectation and arrive at the desired expression. Next, assume that the claim holds for some . We write down the induction hypothesis and then marginalize over all the event after time in , as they do not appear in the arguments of the expectation.

| (18) |

As in the base case, we can expand the expectation one time step forward,

| (19) | ||||

Now plug this in section˜B.3 to obtain

The equality between the first and last item is exactly the expression we wish to prove. The first transition plugs eq.˜19 into section˜B.3, the second pushes the expectation over outside, the third uses the law of total expectation. Then we rearrange

and push the first item into the summation over . ∎

To obtain the identity with the earliest disagreement time, set in the statement we proved, and note that for any value of in the expectation above, exactly one of the following items equals ,

and the value of for which the above item equals is (and when ), hence is the earliest disagreement time, and lemma˜3 reduces to eq.˜2 as claimed.

Appendix C Additional Discussion on Related Work

As outlined in section˜4, several techniques have been proposed for scalable estimation of causal effects in sequential decision-making, with more limited development in the case of irregular observation times. One set of approaches [4, 28, 23], that only apply to discrete time processes and static policies, can be roughly characterized as follows. A prediction model for the outcome is learned, where is the observed history of events and is the set of future treatments we would like to reason about. That is, in our notation we would like to estimate , where assigns the treatments in w.p. . In potential outcomes notation, this corresponds to , where is a random variable that outputs the outcome under a set of static future treatments . All methods involve learning a representation of history , and combine two important elements for achieving correct estimates.

-

1.

To yield correct causal estimates under an observational distribution that is not sequentially randomized, methods either estimate products of propensity weights [23], or add a loss to make non-predictive of the treatment , is then called a balancing representation.

-

2.

To facilitate prediction of under a set of future treatments in the interval , either is taken as a sequence model, or a separate “decoder" network is learned [23, 4]. A sequence model is trained with inputs where , i.e. the covariates in a projection interval are masked, while the decoder takes and as inputs. Both are trained to predict the outcome and serve as an estimator for , which recovers the correct causal effect under sequential exchangeability. Notice that these techniques preclude estimation with dynamic treatments, i.e. policies.

For irregular sampling, Seedat et al., [46] follow the same recipe but choose a neural CDE architecture. This interpolates the latent path in intervals between jump times of the processes, and is shown empirically to be more suitable when working with data that is subsampled from a complete trajectory of features in continuous time. The solution is not equipped to estimate interventions on continuous treatment times (in our notation, ). As mentioned earlier, Vanderschueren et al., [53] handle informative sampling times with inverse weighting based on the intensity . However, this is a different problem setting from ours, as they do not seek to intervene on sampling times but wish to solve a case where outcomes, features and treatments always jump simultaneously. In our setting, intervening on with such simultaneous jumps would result in , which is not the focus of our work. Finally, we also note the required assumption for causal validity that is claimed in these works is roughly . The assumption is unreasonable since includes future factual outcomes that depend on the taken action, instead of the more standard exchangeability assumption that posits independence of potential outcomes.

The G-estimation solution of [22] for discrete time decision processes fits models for both , and . Then at inference time, they replace with the desired policy and estimate trajectories or conditional expectations of with monte-carlo simulations. A straightforward generalization of this approach to decision point processes can be devised by fitting the intensities and replacing for inference. While we believe that this is an interesting direction for future work, we do not pursue it further in our experiments, since developing architectures and methods for learning generative models under irregular sampling deserves a dedicated and in-depth exploration.

Appendix D Additional Discussion on Identifiability

To make the discussion on identifiability from section˜2.2 more concise, we refer here to terms and results from Røysland et al., [42], and explain how they apply to our setting. Then we prove ˜1

D.1 Causal Identification Terminology

Filtrations and restrictions.

In our notation, we condition on past events , while in most formal treatments of stochastic processes conditioning is performed on a filtration of a -algbera . is the full set of information generated by the processes . The notation is used for the -algebra generated by the process alone, hence to a reduced set of information with regards to . Note that here we use the index instead of which we used in the main paper. This is to avoid confusion with the notation for edges in a graph . In the notation of Røysland et al., [42], there are also corresponding filtrations of . Finally the restriction is used to denote the restriction of probability measure to the sub -algebra . Intuitively, is the measure that ignores all the information generated by the unobserved processes by marginalizing them. Outside this section, appendix˜D, the notation is used to refer directly to as we work under the ignorability assumption, which means inference under the restricted probability distribution yields valid causal effects. In the rest of this section we explain why this validity holds, hence refers to the full process with the unobserved information included.

Following the above discussion on filtrations, expressions such as should be read as conditioning on a subset of the sample space where the events in the time interval coincide with .

Interventions and causal validity.

Under the assumption on independent increments, item in Assumption 1, we have that densities for a trajectory take on the form:

Interventions on then mean we replace the intensity (which may depend on ) with an intensity that only depends on (formally, this means it is predictable). The densities change accordingly

The question of causal validity is then whether calculating statistics under , e.g. , results in the same estimation as calculating them under . The difference being that intervenes on instead of on .888Røysland et al., [42] also mention the assumption that itself is causally valid, i.e. that calculating effects under the distribution with the unobserved variables indeed yields valid causal effects. Here we take this assumption as a given. The condition of eliminability, along with overlap, ensures that this validity holds.

Eliminability, local independence, and the assumed graph.

We will local independence graph is a directed graph where each node We now recall the definition of eliminability and the result we use from Røysland et al., [42].

is the distribution that performs the intervention on and then restricts information to the observable information, which admits the causal effect we wish to estimate. We then denote as the distribution obtained by the same intervention on (i.e. where we marginalize over before the intervention). We rephrase the theorem of Røysland et al., [42] to make it more compatible and specialized to our notation and case, it is strongly advised to review the results in their paper for a full formal treatment.

Theorem 1 (special case of Røysland et al., [42]).

Let be a local independence model and the nodes be partitioned as in definition˜3. Consider and a distribution obtained by an intervention on the process in , replacing its -intensity by a -intensity . Further consider that is obtained by performing the intervention on .

If satisfies eliminability, then the intensities of coincide with the intensities of .

To finish this overview, we explain in detail why the graph we assume in this work satisfies eliminability, and hence under the additional assumption of overlap, i.e. Assumption 2, we conclude the correctness of our estimation technique.

Definition 5.

A trail from to in is a unique set vertices and edges such that either or for every .

The trail is blocked by if either (i) contains a vertex on the trail that is not a collieder (i.e. there is no such that both and ), or (ii) is a collider for some , while and for any which is a descendant of .

The trail is allowed if . We say that is separated from by if for any , blocks all allowed trails from to .

Didelez, [10] gives results that tie -separation to local independence, namely that under some regularity conditions if is -separated from by , then is locally independent of given . Local independence in turn is a condition on the intensities of the process, namely that the intensity of is indistinguishable from its -intensity. Intuitively, the -intensity is the intensity that does not include information from the past of . Formally, it may be obtained using the innovation theorem [3, II.4.2]. Then to show that the graph we assumed in our derivation satisfies eliminability and conclude our claims, we will explain why the appropriate -separation properties hold.

Claim 1.

The graph in fig.˜2 satisfies eliminability.

Proof.

Consider , it is easy to verify that is locally independent of given (the second option from definition˜3). This is because blocks all directed paths between and on the graph, and in paths where one of these nodes is a collider, the other is not. Next we consider , and claim that are locally independent of given , which means the first bullet in definition˜3 is satisfied. To see this local independence holds, consider any allowed path in from to or . Since allowed trails must end with incoming edges to the last node, then either must be a non-collider on such an allowed trail (e.g. in the trail ), or either or must be a non-collider (e.g. in the trail ). In both cases, these non-colliders are in the conditioning set, and thus is -separated from by . The required local-independence follows from this.999the condition also includes the independence of , but in our case . ∎

D.2 Proof of ˜1

Equipped with the proper definitions of identifiability, we can now conclude our discussion on EDQ. Let us recall ˜1. See 1

Following our discussion on identifiability, we see that assumption 1 guarantees that calculating conditional expectations w.r.t a distribution where we replace by in , yields a correct causal effect. For the rest of this section we will call the resulting distribution . This is a slight abuse of notation, since was used to refer to the interventional distribution under on , but we use it here to avoid clutter.

To finish the proof of this corollary, we need to show that any -function that satisfies the self-consistency equation in eq.˜3 (which is what algorithm˜2 seeks to produce) must also satisfy for every measurable . We first derive the self-consistency condition from eq.˜2. Then we show that the only function that satisfies this condition is the conditional expectation we wish to estimate, . Equation˜2 is rewritten below,

We write as the sum of rewards that have been observed in the trajectory and a random variable that is the sum of future rewards.

Then we subtract the rewards until time , from both sides of the equation.

This is exactly eq.˜3, which we can simplify slightly to

Next we show that if there is a unique function that satisfies both: (1) , i.e. the estimator returns the correct outcome when it is given a full trajectory (notice the outcome is deterministic in this case), and (2) satisfies the recursion in the above equation, namely

| (20) |

Due to this uniqueness, we will gather that must coincide with for all measurable and conclude the proof.

Lemma 4.

Assume are functions that satisfy both eq.˜20 and for all . Then for all measurable .

Proof.

Since both satisfy eq.˜20, it holds that

Applying eq.˜20 repeatedly to and so on, for say times, we get that

where we denote the -th disagreement under the nested sampling above by . Notice that again there is slight abuse of notation here, since we reused the notation in the expectations above, where the different appearing above may not be identical trajectories. It holds that with probability , since the number of events in a trajectory is finite with probability . Hence we have , and may conclude that because for full trajectories , the functions and must coincide,

∎