Paper Title

Linear programming approach to partially identified econometric models††thanks: I am grateful to Andres Santos, Denis Chetverikov, Rosa Matzkin, Jinyong Hahn, Bulat Gafarov, Tim Armstrong, Kirill Ponomarev, Manu Navjeevan, Zhipeng Liao, Estefanía Saravia, Bohdan Salahub, Shuyang Sheng, as well as to all the participants of the 2024 California Econometrics Conference and the 2024 European Winter Meeting of the Econometric Society for the valuable discussions and criticisms. Earlier versions of this paper were circulated under the title ‘Identification and Inference under Affine Inequalities over Conditional Moments’. First draft: May 30, 2024.

\vskip-12.0pt

Sharp bounds on partially identified parameters are often given by the values of linear programs (LPs). This paper introduces a novel estimator of the LP value. Unlike existing procedures, our estimator is -consistent, pointwise in the probability measure, whenever the population LP is feasible and finite. Our estimator is valid under point-identification, over-identifying constraints, and solution multiplicity. Turning to uniformity properties, we prove that the LP value cannot be uniformly consistently estimated without restricting the set of possible distributions. We then show that our estimator achieves uniform consistency under a condition that is minimal for the existence of any such estimator. We obtain computationally efficient, asymptotically normal inference procedure with exact asymptotic coverage at any fixed probability measure. To complement our estimation results, we derive LP sharp bounds in a general identification setting. We apply our findings to estimating returns to education. To that end, we propose the conditionally monotone IV assumption (cMIV) that tightens the classical monotone IV (MIV) bounds and is testable under a mild regularity condition. Under cMIV, university education in Colombia is shown to increase the average wage by at least , whereas classical conditions fail to yield an informative bound.

Keywords: partial identification, linear programming, bounds estimation, stochastic programming, uniform estimation, returns to education.

1. Introduction

In many partially identified models, the sharp bounds on parameters correspond to the values of linear programs (LPs) that depend on identified functionals of the underlying probability measure. Examples include conditional moment inequalities Andrews et al. (2023), generalized IV models Mogstad et al. (2018), revealed preference restrictions Kline and Tartari (2016), intersection bounds Honoré and Lleras-Muney (2006), dynamic discrete choice panels Honoré and Tamer (2006) and shape restrictions Manski and Pepper (2000).

In these settings, the bounds take the form , where

| (1) |

and is the true value of parameter , estimated via a -consistent estimator . However, optimization problem (1) exhibits non-regular behavior, particularly when the underlying model is rich enough that some linear functionals of are nearly or exactly point-identified over . In such cases, existing estimators of the LP value are either inconsistent or rate-conservative, creating an undesirable tradeoff in empirical work: richer models provide tighter bounds but complicate their estimation.

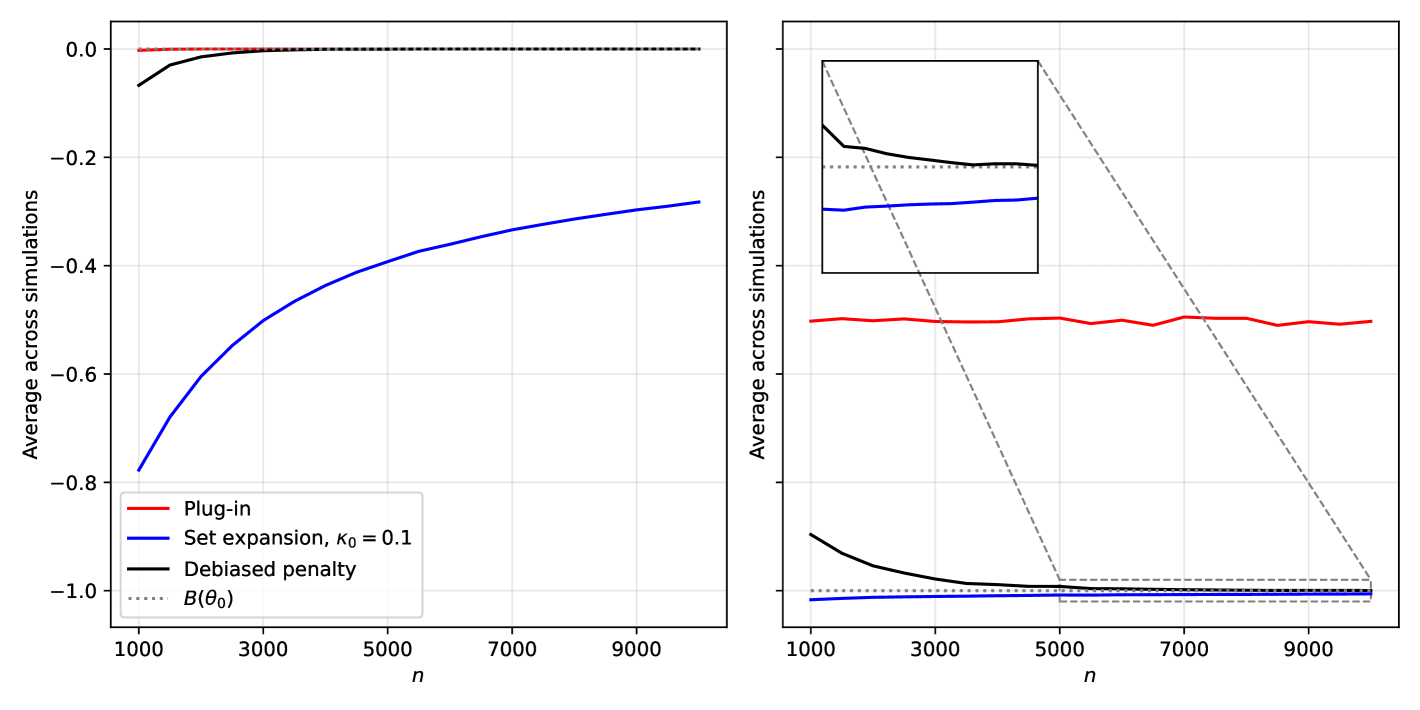

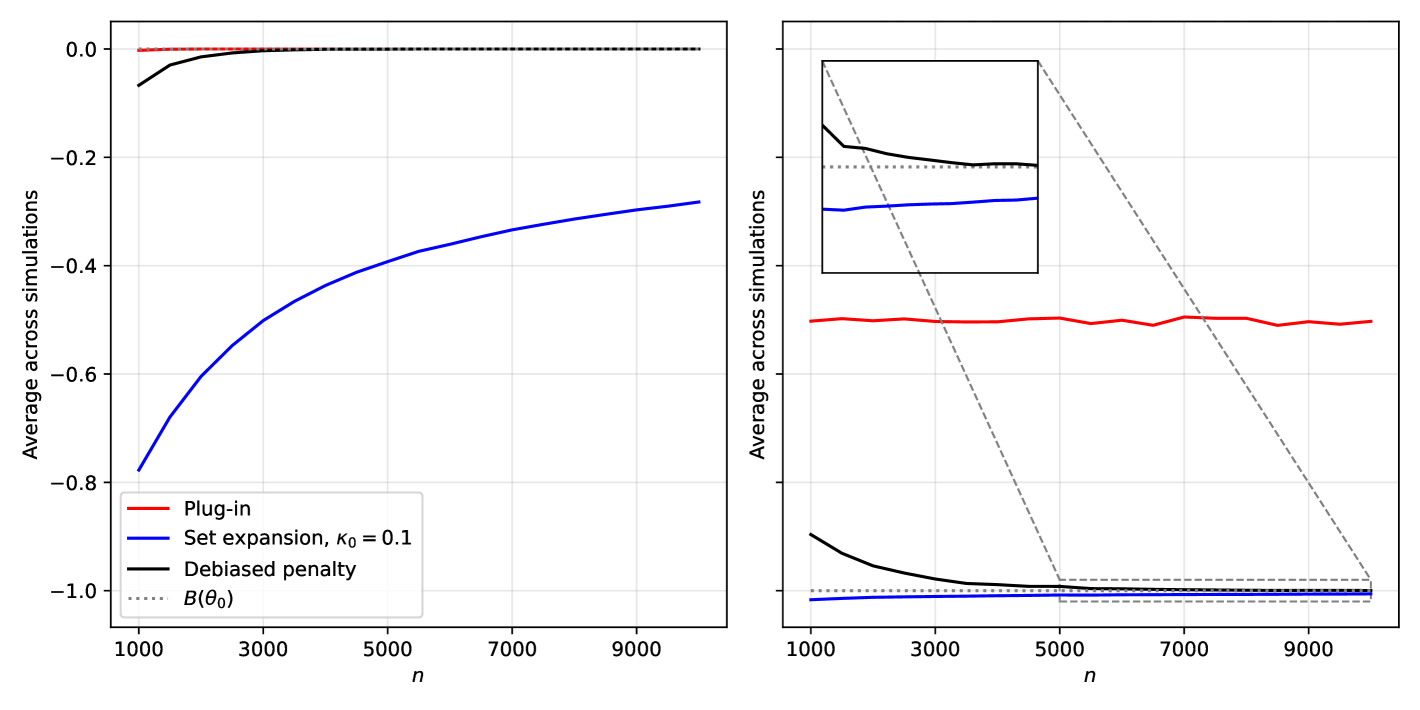

To address this issue, we develop a novel debiased penalty function estimator of . Only assuming that the true polytope is non-empty and contained in a known compact set, we show that our estimator is consistent, pointwise in the probability measure. In contrast, the plug-in estimator is not generally consistent and may fail to exist with non-vanishing probability, while the alternative set-expansion estimator based on Chernozhukov et al. (2007) is rate-conservative and may fail to exist in finite samples. Figure 1 gives a preview of the comparative performance of these estimators.

We obtain an asymptotically normal version of our estimator via sample-splitting and construct confidence regions with exact asymptotic coverage at any fixed probability measure. By comparison, existing procedures either rely on further conditions Gafarov (2024), or result in asymptotically conservative inference Cho and Russell (2023). Notably, the approach most commonly used in applied research—combining plug-in estimation with bootstrap (De Haan (2017), Cygan-Rehm et al. (2017), Siddique (2013), Kreider et al. (2012), Gundersen et al. (2012), Blundell et al. (2007))—may not provide valid confidence intervals even when the underlying model is far from point-identification. In addition, our procedure is the most computationally efficient in the existing literature111Both Gafarov (2024) (BG) and Cho and Russell (2023) (CR) rely on resampling methods, which require to compute one or multiple LPs at each bootstrap iteration. Computing a confidence interval for a LP with 32 variables takes 16.81 seconds with the approach of BG and 40.65 seconds with the approach of CR, according to the latter work. Our approach requires solving a LP once, which takes around 0.0022 seconds on average. The LPs in our application have 160 variables..

Turning to uniform asymptotic theory, we first establish a general impossibility result: using Le Cam’s binary testing method, we show that no uniformly consistent estimator exists when the estimated functional is discontinuous in the total variation norm. This result implies that the LP value cannot be uniformly consistently estimated over the unrestricted set of distributions . To make progress, we introduce the ‘condition’ that parametrizes by restricting it to the measures at which the smallest singular value of some full-rank submatrix of constraints binding at an optimal vertex is lower-bounded by a . This condition is minimal in the sense that any measure from satisfies it for some , ensuring the family of restricted measures’ sets covers as grows small. Unlike the conditions in Gafarov (2024), it does not exclude economically relevant problematic cases, such as point-identification and over-identification, nor does it preclude solution multiplicity. Under the condition, our estimator is shown to be uniformly consistent.

To complement our estimation procedure, we derive sharp (and novel) LP bounds for a broad class of causal parameters under affine inequalities over conditional moments222Including ATE and CATE, among other typically studied parameters, see Section 3. (AICM), potentially augmented with affine almost sure restrictions and missing data conditions. In the simplest case, AICM identifying restrictions have the form

| (2) |

where are continuous potential outcomes corresponding to the legs of treatment and are other covariates. Identified matrices and vectors are chosen by the researcher. In AICM models, from (1) is usually a function of identified conditional moments and the identified joint distribution of , while collects relevant unobserved conditional moments. Our approach accommodates arbitrary combinations of existing ‘nonparametric bounds’ restrictions, allows to conduct sensitivity analysis, and extends to more complex conditions where sharp bounds were previously unavailable333For example, cMIV and the mixture of all classical Manski and Pepper (2000) conditions, see below..

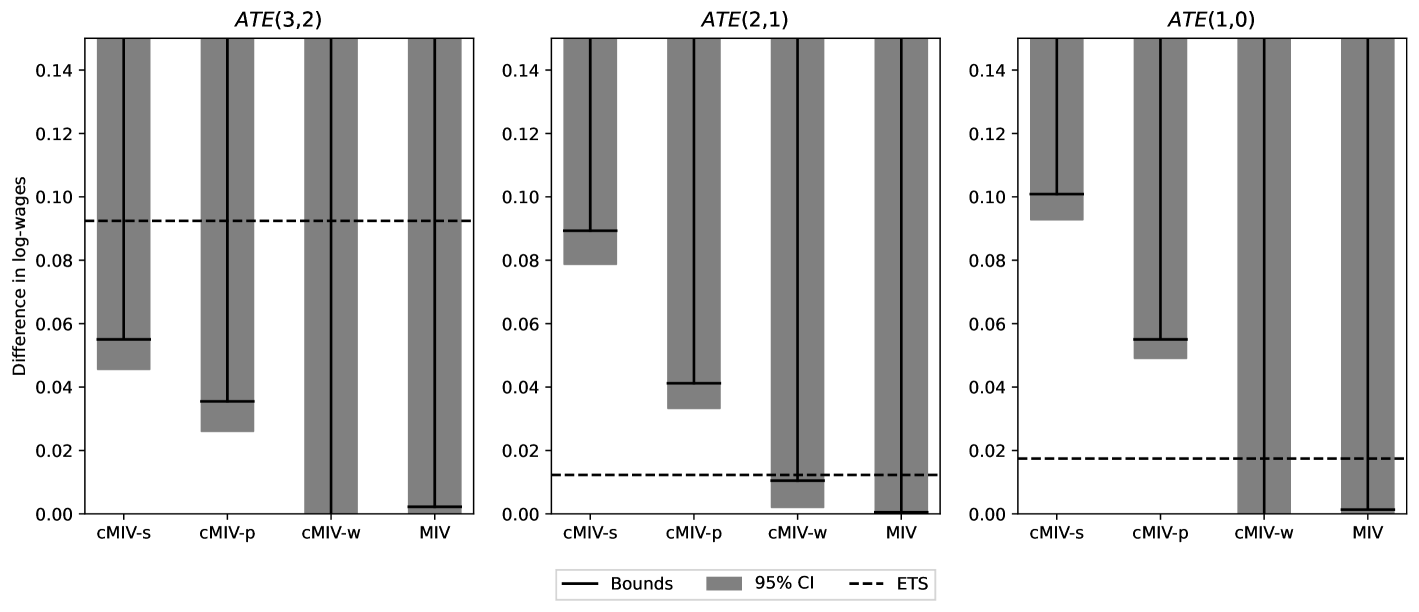

Finally, we apply our approach to estimating returns to education in Colombia. To that end, we first introduce a family of conditionally monotone instrumental variables assumptions (cMIV), which are nested within (2). A variable is a cMIV if the potential outcomes are mean-monotone in it both unconditionally and within selected treatment subgroups444The collection of treatment subgroups over which monotonicity is assumed is chosen by the researcher, see Section 4 for details.. While an explicit form for the sharp bounds under cMIV may not be feasible, their LP representation follows from our general identification result for (2). The cMIV conditions yield tighter bounds than the classical MIV assumption of Manski and Pepper (2000). We argue, however, that they remain unrestrictive in many applications, including ours. While empirical studies (e.g., De Haan (2017)) have assessed the monotonicity of observed conditional moments to justify applying MIV, such monotonicity is instead equivalent to a particular form of cMIV given that MIV holds and under a mild regularity condition. The formal test of cMIV is obtained as an extension of Chetverikov (2019). Using Saber test scores as a cMIV, we find that earning a university degree increases average wages by at least in Colombia. In contrast, the classical conditions fail to produce an informative bound.

This paper also contributes two auxiliary results. The first one is concerned with an important special case of (2) - the combination of all classical Manski and Pepper (2000) conditions. Since this combination has the strongest identifying power among classical restrictions, it has been used in empirical work even without a formal justification, sometimes leading to incorrect bounds (see Lafférs (2013)). We provide sharp bounds under continuous outcomes in this setting. Another auxiliary contribution is a novel lower bound on the -deviation from a non-empty bounded polytope in terms of Euclidean distance from the polytope. It may offer insights into the behavior of -penalized solutions of systems of linear inequalities studied in the control theory literature (e.g. Pinar and Chen (1999)).

We briefly note the limitations of our approach. On the identification side, the absence of restrictions on treatment selection prevents us from studying more granular parameters, such as marginal treatment responses. Furthermore, our identification results are given for discrete treatment and instrument. An extension to the continuous case is feasible, but is outside the scope of this paper555Even when continuous identification results are available, in practice estimation is still carried out with discretized covariates. This is true for all empirical work referenced below.. On the estimation side, while our estimator is pointwise consistent in general, we only establish -uniform consistency666We show, however, that one side of the convergence happens at the uniform rate , see Section 2.5. for a slowly diverging sequence 777Theoretically, can diverge arbitrarily slowly. We use , see Section 2.6 and Appendix H.. We provide further evidence on the uniform rate of consistency in Appendix E. A theoretically uniformly consistent estimator follows from our analysis, but it depends on an unobserved parameter that is difficult to estimate, so we do not recommend using it in practice. Finally, while our inference procedure naturally extends to uniform setup under sufficient regularity conditions, exploring this is left for future work.

The strand of literature relevant to the estimation of (1) is concerned with statistical inference in the LP estimation framework. Semenova (2023) considers a LP with an estimated constraint vector but known and , while Bhattacharya (2009) considers LPs with an estimated and known . Methods developed under a known assumption do not easily extend to the setting when is estimated. Mogstad et al. (2018) construct a set-expansion estimator and prove its consistency. Gafarov (2024) develops uniform inference for a LP described by affine inequalities over unconditional moments, provided uniform Linear Independence Constraint Qualification (LICQ) and Slater’s condition (SC) hold. Gafarov’s conditions may be restrictive in some applications - for example, under AICM, see Section 2. Cho and Russell (2023) obtain uniformly valid, yet conservative inference for the case when is affine in unconditional moments. Their practical procedure implicitly assumes that the SC holds888We discuss this in more detail in Section 2.6.. Andrews et al. (2023) develop an inference procedure for the LP value in a special case in which SC holds. Syrgkanis et al. (2021) develop a testing procedure for the failure of LP feasibility. We conduct Monte Carlo simulations to compare our approach with relevant existing methods in Section 2.6.

Despite the similar name, AICM approach is unrelated to the model in Andrews et al. (2023) beyond producing LP bounds. Instead, it generalizes the nonparametric bounds analysis of Manski and Pepper (2000, 2009). The LP sharp bounds in Theorem 3.2 coincide with or tighten the bounds in Blundell et al. (2007), Boes (2009), Siddique (2013), Kreider et al. (2012), De Haan (2017) and Cygan-Rehm et al. (2017). These studies combine the plug-in estimator with bootstrap for inference, an approach that relies on strong assumptions (see Section 2.2.b). The exact inference procedure in Algorithm 1 could be used instead. AICM also complements the findings of Mogstad et al. (2018), who develop identification theory for generalized IV estimators and obtain bounds in the form (1). Their method imposes a Heckman and Vytlacil (1999, 2005) selection mechanism in the binary treatment case and thus restricts them to valid IVs999Additive separability in treatment selection is equivalent to the Imbens and Angrist (1994) IV conditions under instrument exogeneity Vytlacil (2002)., but allows to accommodate arbitrary a.s. restrictions on the marginal treatment response functions and derive bounds for potentially more granular causal parameters. Even though (2) nests mean-independence conditions, AICM approach is most useful when a valid IV is not available101010Thus, if one is faced with i) a binary treatment setup, ii) has a valid IV and iii) no outcomes’ data is missing, the method of Mogstad et al. (2018) may be used. If any of these conditions fail, AICM is an alternative..

Notation

All vectors are column vectors, and denotes the transpose of . If is a set, stands for its complement. A collection is a column vector. denotes the powerset of set , and is the collection of integers from to . is a Cartesian product of sets, while is the Kronecker product. The sign denotes a disjoint union. Signs and stand for logical ‘and’ and ‘or’ operators respectively. For and , is the submatrix of the rows of with indices in . If , write . stands for the range of , while denotes its rank. is the th largest singular value of , and denotes the Moore-Penrose pseudoinverse of . In a normed space , the distance between and is written as , and is the Hausdorff distance between . For the open expansion is . and are the interior and closure of , while is its conical hull. If is a matrix, is the conical hull of its columns. for a compact and is a support function. For , define . For vector inequalities and mean and respectively. is a vector of ones, is the identity matrix, and the subscript is dropped occasionally. Operator is the expectation under a measure , and the subscript is dropped whenever it does not cause confusion. The statement w.p.a.1 means that . We adopt the convention , and .

2. LP estimation framework

In many partial identification settings, bounds on the parameters of interest can be characterized as the values of linear programs (see Kline and Tamer (2023) for a review). Readers who prefer to first see an identification framework leading to such bounds may refer to Section 3, where LP sharp bounds are derived for a general class of AICM models. This section focuses on the estimation theory for such problems. The LP value function is given by

| (3) |

where , and . The vector collects parameters of the LP. The estimable value of these parameters at a fixed true measure is denoted by , with . The value of interest is therefore . Note that (3) does not rule out equality constraints, as .

We denote the constraint set by and omit the argument when is concerned. In the context of Section 3 and other existing applications (e.g. Mogstad et al. (2018)), the set is the identified set for an unobserved feature of the underlying distribution. Under Assumption A0.i-ii, the set is a convex polytope.

Assumption A0 (Pointwise setup).

Suppose that at the fixed true parameter : i) The identified set is non-empty, ; ii) for a known compact and iii) There is an estimator :

Assumption A0 is maintained throughout this section, while other conditions are stated explicitly. A0.i ensures feasibility of the population LP. In partially identified models it means that there exists a distribution consistent with the identifying restrictions, which does not imply correct model specification. A0.ii is a mild restriction111111For a polytope to be bounded, it must be that , see Chapters 2 and 3 in Grünbaum et al. (1967) that usually holds in applications, for example under bounded outcomes in AICM models (see Section 3). The estimator in A0.iii is typically warranted by CLT and the Delta-Method. We focus on the case in which is estimable for expositional simplicity, but our results generalize to any rate .

The following primal and dual solution sets will prove useful in our discussion:

Assumption A0 implies that a finite is attained as a minimum in (3), and are non-empty compact sets, and is non-empty. We now briefly discuss the typically imposed regularity conditions.

Definition.

Slater’s condition (SC) is the assertion that .121212We give simplified versions of assumptions here for simplicity of exposition. In the presence of ‘true’ equalities , SC should be stated in terms of relative interior, allowing for point-identification along ‘true’ equalities. LICQ should similarly be restated to account for equalities, as in Gafarov (2024).

SC rules out point-identification of any linear functional of . In particular, it precludes exact point-identification of the target and point-identification of , i.e. the case when . Most existing methods rely on SC explicitly (Gafarov (2024)) or implicitly (Cho and Russell (2023), Andrews et al. (2023)). Even an ‘approximate’ failure of SC, when the true identified set becomes ‘thin’, can be problematic for the existing methods in finite samples. Our simulation evidence illustrates this, see Section 2.6. This creates an undesirable tradeoff in applications: higher identification power comes with poorer estimation quality.

Definition.

Linear independence constraint qualification (LICQ) is the assertion that the submatrix of binding inequality constraints at any is full-rank.

LICQ precludes the existence of overidentifying constraints at the optimum. It may be hard to justify in ‘bigger’ models, like the one we develop and apply in Sections 4 and 5. These feature a larger number of inequality constraints that may have similar identifying power, so it is not ex-ante clear why there must not be overidentification at the optimum. LICQ also rules out parameters-on-the-boundary, as the following remark clarifies.

Remark 2.1.

Definition.

No flat faces condition (NFF) is the assertion that .

The notion of flat faces thus corresponds to , i.e. the situation in which the bound on the target parameter is achieved at multiple partially identified features .

Assumption A0 does not impose LICQ or SC, nor does it rule out flat faces. Estimating without these conditions is challenging due to the irregular behavior of . If SC fails, may be discontinuous at , and the plug-in estimator may not be pointwise consistent.

Fix any . Then, i) for any , there exist and satisfying Assumption A0, with and for all surely; and ii) for any , there exist and satisfying Assumption A0, with and with non-vanishing probability. The proposition above can be illustrated using two simple examples.

Example 2.1.

Example 2.2.

To illustrate the second part of Proposition 2, consider

where is estimated via with i.i.d. Suppose . If , the sample LP is infeasible, so . This occurs w.p. for any .

In some special cases (e.g., Honoré and Tamer (2006)), SC may be argued to hold, ensuring the continuity of 131313Under SC and A0, is continuous at , see Appendix F.1.. However, an additional challenge arises: is not necessarily Hadamard differentiable unless further regularity conditions hold. This complicates inference, as Proposition 2.2.b in Section 2.2 illustrates.

This section addresses Propositions 2 and 2.2.b. Section 2.1 introduces the penalty function estimator and its debiased version, which we show to be -pointwise consistent under A0. Section 2.2 develops a computationally efficient inference procedure with exact asymptotic coverage under A0. Turning to uniform properties, Section 2.3 presents a general impossibility result for discontinuous functionals. It implies that the LP value cannot be uniformly consistently estimated under a uniform version of A0 alone. We then characterize a broad class of measures over which a uniformly consistent estimator exists. Sections 2.4 and 2.5 establish the uniform rates of the penalty function estimators over this class. Section 2.6 provides simulation evidence.

2.1. Consistency

2.1.a. Penalty function estimator

We now develop a consistent estimator that is inspired by the theory of exact penalty functions. The idea is to restate (3) as an unconstrained penalized problem. Define the penalized version of the LP objective as

and consider the unconstrained problem

| (5) |

We use to obtain a preliminary estimator of the LP value, which we term the penalty function estimator. Note that at any , i.e. the penalized objective function is equal to the LP objective function whenever the constraints in (3) are satisfied.

Assumption A1 (Penalty parameter).

The penalty vector and the true parameter are such that in the problem (3) evaluated at there exists a KKT vector , such that .

Note that Assumption A1 does not require to be component-wise larger than all KKT vectors. In any finite and feasible LP there exists at least one , so at any fixed there always exists a large enough that satisfies A1.

Remark 2.2.

If it is known that i) for some , and ii) for some known , Assumption A1 is satisfied by and known by duality.

The following Lemma is key to understanding the penalty function approach. It asserts that under Assumption A1 the penalty function is exact for the LP in (3). {lemma} For any , and , if , then

| (6) |

Moreover, if and satisfy Assumption A1, then: i) (6) holds with an equality at , and ii) solutions coincide, . The deterministic result in Lemma 2.1.a, combined with the observation that the objective function converges in probability uniformly in under A0, establish that the penalty function estimator with a fixed is consistent under A1. {prop} Under Assumption A1,

For ease of notation, from now on we treat as a scalar penalty that induces the penalty vector . Our results extend immediately to the case when the coordinates of the penalty vector differ. Based on Lemma 2.1.a and Proposition 2.1.a, it might seem that should be selected to be as large as possible. This, however, yields a generally inconsistent estimator if SC fails.

Example 2.1 (cont’d).

Consider (4) with and suppose . If , there exists a sample KKT vector , whose largest coordinate is . So, if also , the penalty estimator selects an incorrect optimum in light of Lemma 2.1.a. Since , at a large enough sample size will exceed any fixed with high probability and the correct minimum of will be estimated. However, that logic fails in finite samples if is ‘large’.

This observation justifies the need to study asymptotic theory. We show that the penalty parameter can be allowed to diverge at the rate dominated by . {theor} For any w.p.a.1 with , we have

Observe that the estimator in Theorem 2.1.a does not rely on Assumption A1, as the latter is always satisfied at a fixed measure for a large enough when .

2.1.b. Debiased penalty estimator

The rate of convergence in Theorem 2.1.a is determined by the slowly vanishing penalty term. This term is a product of the deviation from the true polytope, that vanishes at , and an exploding sequence . It is thus reasonable to ask whether the rate could be restored by dropping the penalty term, i.e. debiasing the penalty function. We show that this can be done. Before we proceed, let us make the following simplification. Without loss of generality, suppose that

| (7) |

To see why (7) can be assumed w.l.g., note that one can set and add an auxiliary variable for the value of the problem in the first position of (see Gafarov (2024)).

We define the debiased penalty function estimator as

The following theorem establihes its rate, and is one of the main contributions of this paper.

Suppose . For any w.p.a.1 with ,

Remark 2.3.

The result in Theorem 2.1.b is uniform over the argmin set, so one may use any measurable selection from to obtain a consistent estimator. In the context of lower/upper bound estimation, respectively yield the tightest bound.

Remark 2.4.

The argmin set of the penalty function estimator can be computed by solving a LP with variables and constraints. Specifically, in Appendix A.3 we show that, w.p.a.1, .

Remark 2.5.

An alternative estimator can be constructed using a set-expansion argument: . In Appendix G, we show that the results from Chernozhukov et al. (2007) and the geometry of polytopes imply that with an appropriately chosen, diverging , is consistent for . However, it can be rate-conservative, converging at . It appears to perform worse than the debiased penalty function estimator in our simulations, see Section 2.6.

We now outline the main ideas behind Theorem 2.1.b. For , let denote the set of constraints that bind at when evaluated at . For ease of notation, from now on we write . Let us introduce the following terminology.

Definition (Vertex).

We call a vertex-solution if the corresponding matrix of binding constraints, , has full column rank.

Definition (Nice face).

We say that a nonempty set corresponds to a nice face141414It should be noted that a nice face is not necessarily a valid face of the true polytope . if for any .

Intuitively, the proof of Theorem 2.1.b proceeds in two steps. First, by anti-concentration arguments we establish that with high probability asymptotically the penalty function estimator manages to select a vertex-solution such that the set of constraints that bind at it, , corresponds to a nice face . Once a nice face has been selected, the convergence of to obtains as a consequence of converging to at this rate for a fixed .

2.2. Inference

This section develops an inference procedure for a general LP estimator, in which all parameters are inferred from the data. This procedure nests special cases in which some parameters remain fixed, as in Semenova (2023) or Bhattacharya (2009).

Assumption B0 (Random sample).

Suppose is a measurable function of the sample , where are i.i.d. random vectors.

We suppose that Assumption B0 holds throughout Section 2.2, whereas the rest of the conditions are imposed explicitly.

Assumption B1 (Asymptotic normality).

The estimator is such that, for ,

Assumption B1 is typically warranted by reference to CLT and the Delta Method when for some smooth , as in the AICM models (2), see Section 3.

2.2.a. Exact inference on a debiased estimator

We construct a method for statistical inference on that achieves exact asymptotic coverage under minimal regularity conditions. Our approach is based on an asymptotically normal version of the debiased penalty estimator with w.p.a.1 and is outlined in Algorithm 1. Before stating the main result, we introduce key auxiliary constructions and discuss our assumptions.

Given data , estimators and , penalty vector and constants , , follow the steps below to obtain confidence intervals for .

Step 1 (Split the sample):

Step 2 (Find the vertex):

Step 3 (Construct the C.I.)

For the true and some subset of indices , consider conditions

| (8) | |||

| (9) |

Equation (8) is satisfied if constraints may bind simultaneously at some solutions of the original LP, while (9) holds if the objective function’s gradient is a linear combination of the gradients of inequalities from . For example, if is a set of all binding constraints at some , equation (9) follows from KKT conditions.

Continuing the discussion in Section 2.1.b, we note that subsets that satisfy (8) and (9) correspond to the nice faces.

If satisfies (8) and (9), then is a nice face,

Define the set . It is non-empty in any feasible finite LP. With probability approaching , the penalty function estimator manages to select a vertex-solution , determined by the binding constraints that satisfy (8) and (9) and thus correspond to a nice face by Lemma 2.2.a.

The debiased estimator may hence be understood as a two-stage procedure: one first finds the set of binding inequalities , and then estimates as . Performing inference on that object directly would require working with the complex joint distribution of , and , and would likely result in an asymptotically non-normal estimator.

We address this by ‘disentangling’ the variation in and via sample splitting. Intuitively, a vertex is estimated on one part of the sample, while the noise in the parameter estimation comes from the other. We now state our assumptions and present the main result.

Assumption B2 (Variance estimator).

B1 holds, and there exists an estimator .

Assumption B2 requires the researcher to possess a consistent estimator of the asymptotic variance of . If for some smooth and known , such estimator can typically be obtained from the estimated covariance matrix of via Delta-method. In more complicated scenarios, bootstrap on may be employed.

Define the set and note that (9) is equivalent to .

Assumption B3.

For a constant , .

Assumption B3 is a technical condition ensuring that we can find a sequence approaching asymptotically, i.e. for defined in (10). Practical guidance on choosing is provided in Appendix E.2. Simulation evidence in Figure 16 in Appendix E.2 suggests that the specific value of has no impact on inference, as long as it is sufficiently large.

Definition (Optimal triplet).

We call an optimal triplet if i) , ii) , iii) , iv) , and v) .

We randomly split into two disjoint, collectively exhaustive folds of size for , with and for some fixed . Our inference procedure uses the data from to estimate an optimal triplet . The vertex151515While we assume that is estimated precisely, the results do not change if one is only able to estimate a single optimum. This may occur if numerical errors do not allow the LP-solver to find all of the LP solutions. Such optimum will satisfy by definition, and so will be a valid vertex-solution. is estimated as

the set of binding constraints that define it is denoted by , and

| (10) |

Finally, we define so that and for .

Assumption B4 (Non-degeneracy).

B1 holds, and for any optimal triplet .

An inspection of the proof of Theorem 2.2.a below reveals that Assumption B4 rules out the scenarios when finding an determines the value , even though is noisy. This may occur, for example, if the corresponding are deterministic. In this case, if is also unique, meaning , the debiased estimator has asymptotic variance, because and therefore are correctly estimated with probability approaching .

Suppose and Assumptions B1, B3, B4 hold. Moreover,

for any optimal triplet with , which holds for under Assumption B2. Then, for any , and any w.p.a.1 such that ,

Remark 2.6.

Remark 2.7.

If an estimator is not available and is not obtained via bootstrap on , one may alternatively construct confidence intervals using the quantiles of . These can be computed via bootstrap on , where remain fixed, while and are bootstrapped over the second fold data .

2.2.b. Bootstrapping the plug-in fails even under SC

To further justify the need for our inferential procedure, we examine the properties of the approach that combines bootstrap on with the plug-in estimator . This method is widely used in empirical literature applying AICM conditions (Blundell et al. (2007), Kreider et al. (2012), Gundersen et al. (2012), Siddique (2013), De Haan (2017), and Cygan-Rehm et al. (2017)). In light of Proposition 2, this approach is inapplicable when SC fails. In practice, researchers attempting to apply it to a LP with a small or empty interior of may encounter frequent LP infeasibility in the bootstrap draws.

In some cases, SC may be established. This is true, for example, if the bound of interest can be expessed as an intersection bound , where (as in Chernozhukov et al. (2013)). Yet, even if SC holds, we demonstrate that bootstrap inference based on the plug-in estimator is not valid, unless further regularity conditions hold. This observation can be viewed as a generalization of the parameter-on-the-boundary problem of Andrews (1999, 2000).

Definition.

Let and be Banach spaces, and . The map is said to be Hadamard directionally differentiable (H.d.d.) at tangentially to , if there is a continuous map , such that

for all sequences and such that , as and for all . If, moreover, is linear in , the map is said to be fully Hadamard differentiable at .

For simplicity of exposition, we abstract from the case of ‘true equalities’ in . The results extend trivially to this case if SC is defined in terms of relative interior. {lemma}[Duan et al. (2020)] Under SC, is Hadamard directionally differentiable at . The directional derivative is given by

| (11) |

where is the direction of the increment in . Hadamard directional differentiability of is sufficient for convergence in law. {prop} Under SC and Assumption B1, it follows that

Proof.

Fang and Santos (2018) Theorem 2.1. combined with Lemma Definition. ∎

Gaussianity of is a necessary condition for bootstrap consistency Fang and Santos (2018). Consequently, the empirical literature using bootstrap with the plug-in estimator has implicitly relied on this assumption. However, is not normal unless full Hadamard differentiability holds, i.e. is linear in . As (11) suggests, this is not generally the case. Theorem 3.1 in Fang and Santos (2018) establishes that bootstrap is inconsistent for the distribution when fails to be linear. The typically applied plug-in and bootstrap combination is then only valid under further restrictive assumptions161616The full-support condition in Proposition 2.2.b is imposed for expositional purposes. Sufficiency of conditions i, ii holds generally, whereas necessity obtains whenever the derivative is not linear over when are not singletons, see Lemma F.3 in Appendix.: {prop} If SC and Assumption B1 hold, and satisfies Assumption 3 in Fang and Santos (2018), bootstrap is consistent in the sense that

where , if and only if i) NFF and ii) SMFCQ also hold at .

Remark 2.8.

Strict Mangasarian-Fromovitz Constraint Qualification (SMFCQ) that we define in Appendix F.3 is equivalent to , which is necessary for bootstrap consistency. However, it depends on both the vector and on . In Appendix F.4, we show that uniformly over all objective functions minimized at some if and only if (pointwise) LICQ holds at . Both SMFCQ and LICQ are high-level and may be restrictive in models with potentially overidentifying constraints, as in Sections 4 and 5.

Remark 2.9.

A consistent estimator for the distribution of under SC can be obtained by combining the Functional Delta Method (FDM) of Fang and Santos (2018) with the Numerical Delta Method (NDM) given in Hong and Li (2015), see Appendix F.1. In Appendix F.2, we also show that the penalty function estimator is H.d.d. in , so FDM + NDM combination yields exact inference for it. This approach relies on an arbitrarily selected NDM step size and a fixed , and so does not appear satisfactory. Finally, the set-expansion estimator enforces SC and has a Lipschitz-bounded bias (see Appendix F.1). A conservative inference procedure based on it can then also be obtained via FDM and NDM.

2.3. Impossibility result

The optimization problem (1) is challenging to study under no further assumptions, as it may exhibit instability under arbitrary perturbations of parameters. We now show that this not only leads the plug-in to fail pointwise, but also precludes the existence of a uniformly consistent LP estimator over the unrestricted set of measures.

We first establish a new impossibility result that complements the findings of Hirano and Porter (2012). Specifically, we show that no uniformly consistent estimator exists for any discontinuous functional from the space of probability measures endowed with the total variation norm to an arbitrary metric space .

Suppose a functional is discontinuous at . Then, there exists no uniformly consistent estimator , which is a sequence of measurable functions of the data . Moreover, if is a lower bound on the discontinuity, i.e. for any there exists such that and , then

where infinum is taken over all measurable functions of the data.

In this section, we treat the parameter as a functional of the underlying probability measure . We then make the following assumption on the pair :

Assumption U0 (Uniform setup).

The functional and the set of probability measures are such that: i) is continuous; ii) for a known and fixed compact

Assumption U0 formalizes the notion of the unrestricted set of measures. U0.i demands that the true parameter be continuous in , which holds, for example, in AICM models (see Example 2.4). U0.ii assumes that has full support over , meaning that any corresponding to a consistent model with is attained at some . {theor} Under U0, there exists no uniformly consistent estimator of .

Given this negative result, it is natural to seek a minimal restriction on for which a uniformly consistent estimator may exist. We now show that the condition ensuring uniform consistency of the penalty function approach can be considered minimal in the sense to be made precise in Proposition 2.3 .

Our examination of Example 2.1 has shown that cannot be allowed to diverge faster than , as otherwise the penalty approach may fail at measures where SC fails. At the same time, if all KKT vectors grow large, an arbitrarily large is needed for Assumption A1 to hold. This occurs when optimal vertices become ‘sharp’, i.e. all relevant full-rank submatrices of binding inequality constraints grow closer to being degenerate. The condition that ensures uniform consistency of the penalty function approach should therefore bound such ‘sharpness’.

We begin our construction with an existence result based on the Caratheodory’s Conical Hull Theorem.

The problem (3) admits a solution and the associated KKT vector such that for some index subset with , is invertible and:

Proposition 2.3 asserts that any finite and feasible LP has an optimal vertex at which there is a subset of binding constraints, such that i) the corresponding gradients form a full-rank square matrix, and ii) the objective function gradient belongs to the conical hull formed by the gradients of the constraints from .

Assumption U1 (-condition).

The class of measures satisfies the condition for a given , if

| (12) |

where collects all defined in Proposition 2.3 at a given .

The -condition does not rule out the failure of LICQ, SC or NFF, and is weaker than the conditions under which uniform consistency of LP estimators has been established. To formalize this, let us introduce three families of measures. Firstly, denote the family of measures satisfying U1 for a given by . A measure satisfies the Slater’s condition if . Similarly, a measure satisfies a uniform -LICQ condition (as in Gafarov (2024)) if , where

where the set consists of sets of indices of binding inequalities that define vertices of the polytope .

The following hold:

-

(i)

, where the inclusion is strict

-

(ii)

for any , where the inclusion is strict

Proof.

Intuitively, the in Assumption U1 merely parametrizes the degree of irregularity that the researcher is willing to allow for the identified polytope over the considered set of measures. The resulting family of sets ‘covers’ the unconstrained set of measures asymptotically as decreases to . Uniform LICQ and SC, on the contrary, both restrict the set of measures. That is because measures like the one in Figure 2(b) do not belong to either for any , or .

Example 2.1 (cont’d).

Figure 4 plots the range of values that correspond to the measures satisfying the condition for a given in (4). The condition cuts off an interval of along which the optimal vertex becomes ‘too sharp’. Recall that the case leads to the failure of SC. However, it satisfies the condition for a relatively large , because at the optimum there is a set from Proposition 2.3 such that the relevant matrix of binding constraints has the smallest singular value .

Example 2.3.

There are LPs in which SC, LICQ and NFF all fail, but the condition is satisfied for a relatively large . One example is the problem

where the condition is satisfied for . It is large relative to the values of , for which the penalty vector suggested in Appendix H is valid for small . There are flat faces, as any pair with and is a solution, SC fails, as , and LICQ fails, as at an optimal there are three binding constraints.

2.4. Uniform consistency of penalty function estimator

The penalty function estimator converges to the LP value a.s. at rate , uniformly over the set of distributions that satisfy the condition for some . {theor} Suppose that i) converges to a.s. uniformly over at rate , i.e. for all with and any ,

| (13) |

and ii) w.p.a.1 a.s. uniformly over , i.e. for any ,

Then, for all with and any ,

In applications, condition i) in Theorem 2.4 can usually be established with rate by reference to the uniform LLN, provided is uniformly continuous in population moments.

Example 2.4.

In the AICM models (2), is linear in moments of interactions of with treatment indicators and linear or hyperbolic in probabilities of (see Section 3). Thus, condition i) in Theorem 2.4 is established by, firstly, imposing integrability

which holds whenever bounded outcomes are assumed. If also a full-support condition holds,

for some , then is uniformly continuous in population moments. Combining this with the LLN uniform in probability measure (see Proposition A.5.1 on p. 456 of Van Der Vaart and Wellner (1996)) yields condition (ii). If one additionally assumes that

the rate in (13) is (see Proposition A.5.2 on p. 457 of Van Der Vaart and Wellner (1996)).

Remark 2.10.

The existence of a uniformly consistent estimator over implies that is continuous over . However, as Example 2.1 illustrates, it is not necessarilly continuous over the support of . It is straightforward to see that the case in (4) satisfies the -condition for a relatively large , but the plug-in estimator is still pointwise inconsistent at such measure.

2.5. Uniform consistency of the debiased estimator

This subsection provides a variation of the condition under which the debiased penalty estimator is shown to be uniformly consistent. Intuitively, the debiased estimator achieves uniform consistency whenever for all considered measures it is true that if the distance of from the polytope is large, then the constraint violation is also large. To develop that notion formally, we introduce the following two terms.

Definition (Face condition number).

For a proper -face171717See Chapters 2 and 3 in Grünbaum et al. (1967) for the definition. We call a face proper if . A face is a vertex. of a polytope , given by and described by binding constraints with such that , define the face condition number to be

Definition (Polytope condition number).

For a polytope , define the polytope condition number as

The following proposition simplifies the interpretation of . It asserts that in the definition of it suffices to only consider the vertices of , {prop}For any polytope , , and

We are now ready to define the polytope condition.

Assumption U2 (Polytope -condition).

The class of measures satisfies the polytope condition for a given , if

The polytope condition lower bounds the smallest singular values of all full-rank matrices that can be constructed from the vertices of the polytope. Similarly to Assumption U1, it parametrizes the unconstrained set of probability measures, since at any fixed we have by definition. Proposition 2.3 continues to hold for U2, if one substitutes with - the family of measures satisfying U2 for a given .

The following Lemma provides a minorization of the deviation from a polytope, and appears to be mathematically novel. Intuitively, determines ‘sharpness’ of the vertices of a polytope. The less sharp is a vertex, the greater the polytope constraints’ violations need to be in terms of the distance from the polytope. Figure 5 illustrates that point.

For any non-empty and bounded polytope :

By Theorem 2.4, the biased penalty estimator is uniformly consistent at rate under the -condition. The following Theorem asserts that the debiased estimator converges at least at the same rate.

Suppose that the hypotheses i) and ii) of Theorem 2.4 are satisfied. Then, for all with and any ,

Moreover, for all with and any ,

Remark 2.11.

Theorem 2.5 establishes that under the polytope condition the debiased estimator converges at least at the rate for some slowly growing . Moreover, it converges from below at the rate uniformly.

Remark 2.12.

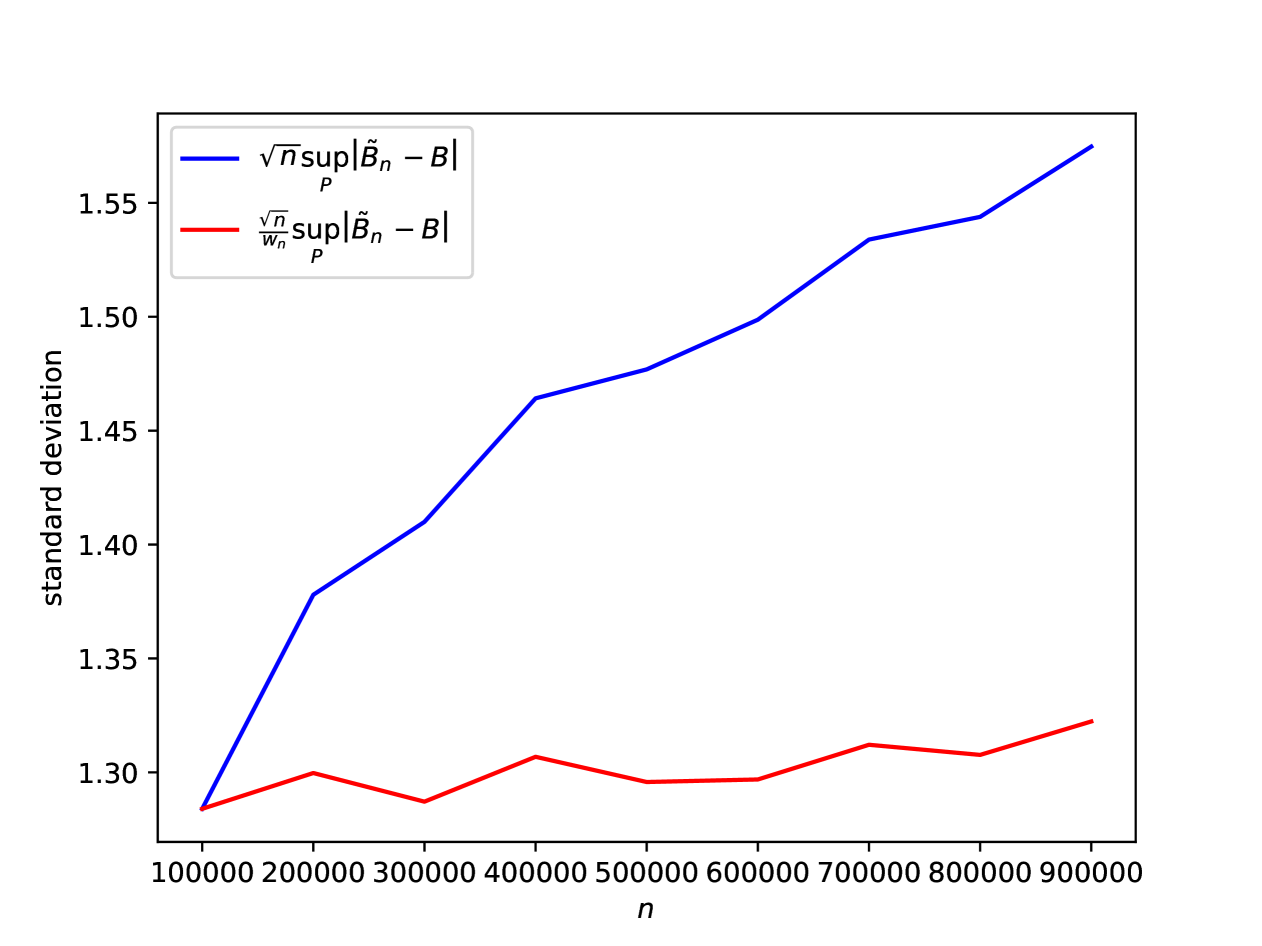

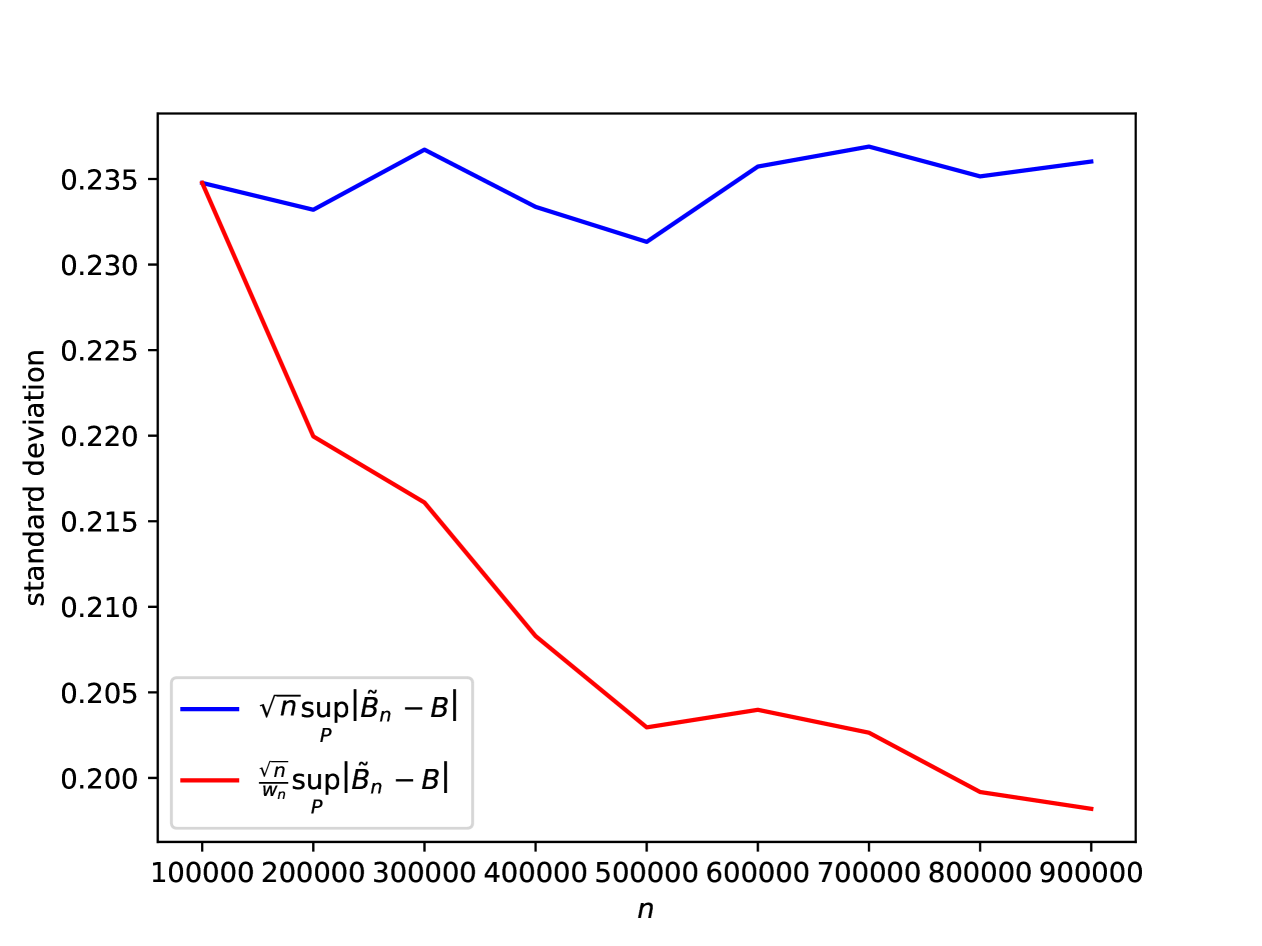

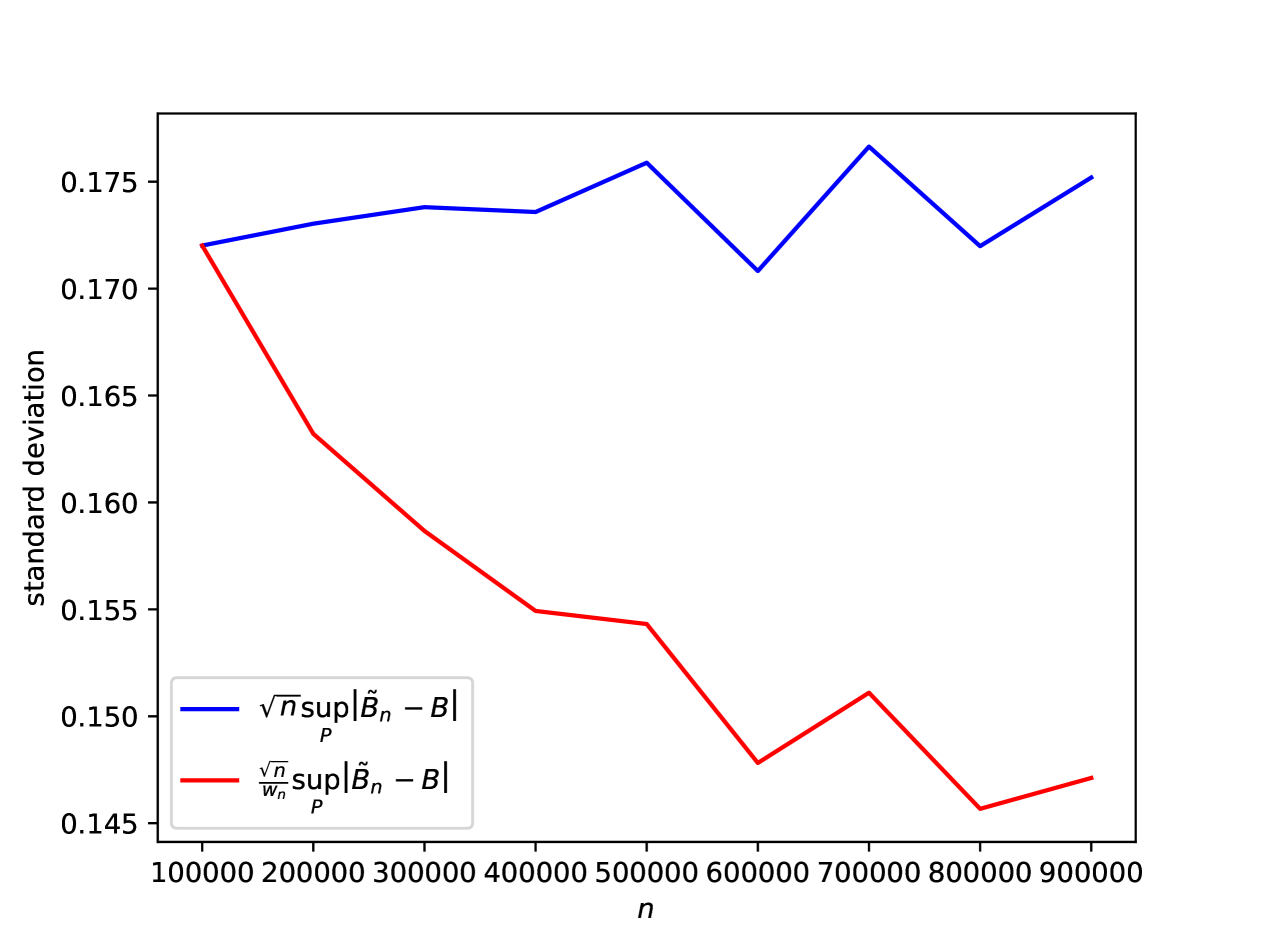

It is unclear if the uniform rate is sharp. The simulation evidence in Appendix E suggests that this may be the case, but only along the sequences of measures , for which SC, LICQ and NFF all fail in the limit. Once such sequences are ruled out, the rate of appears to be restored uniformly.

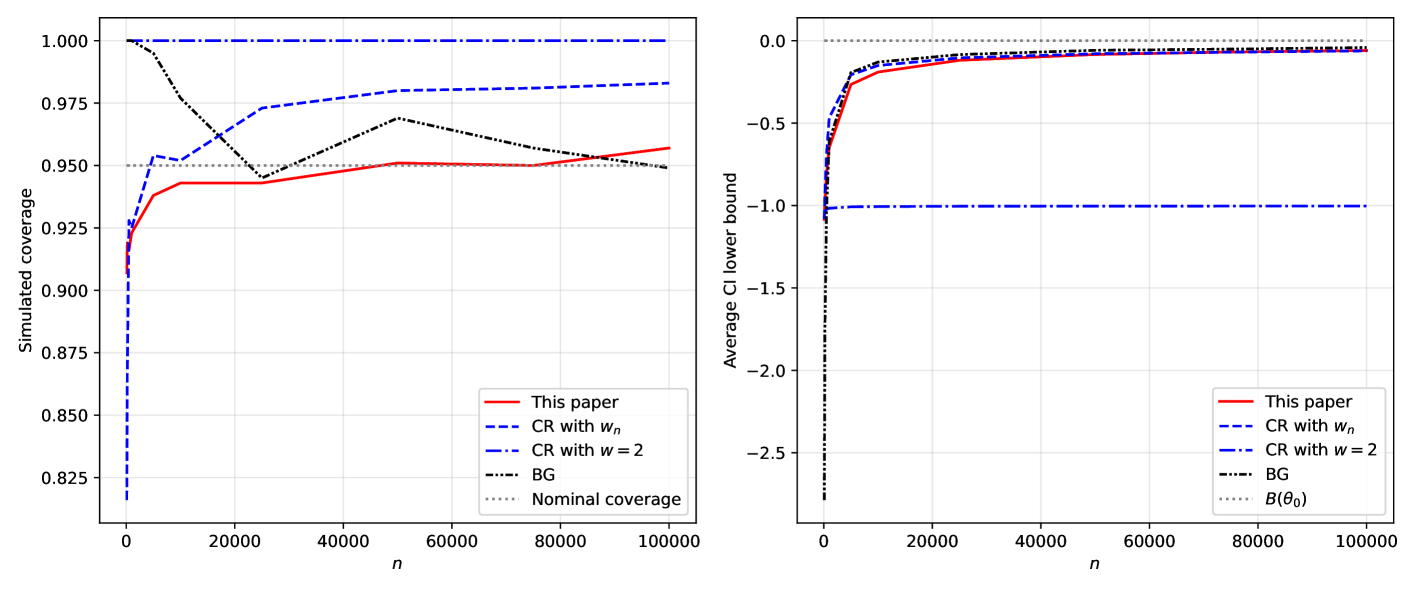

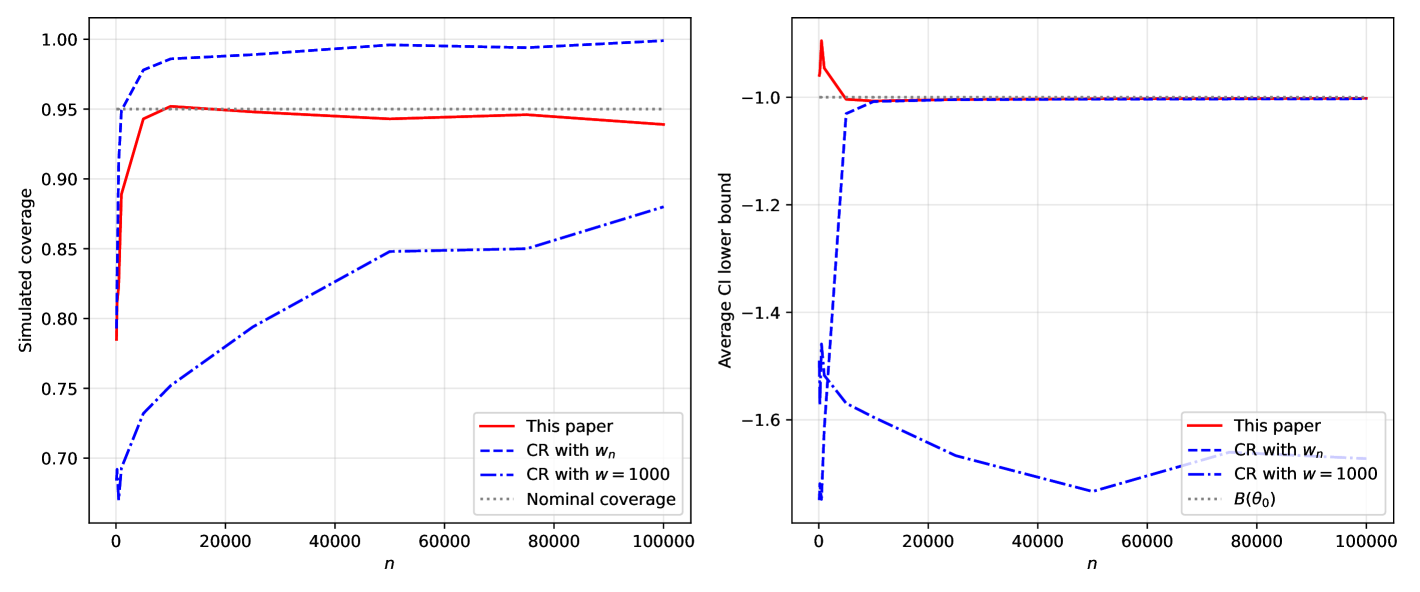

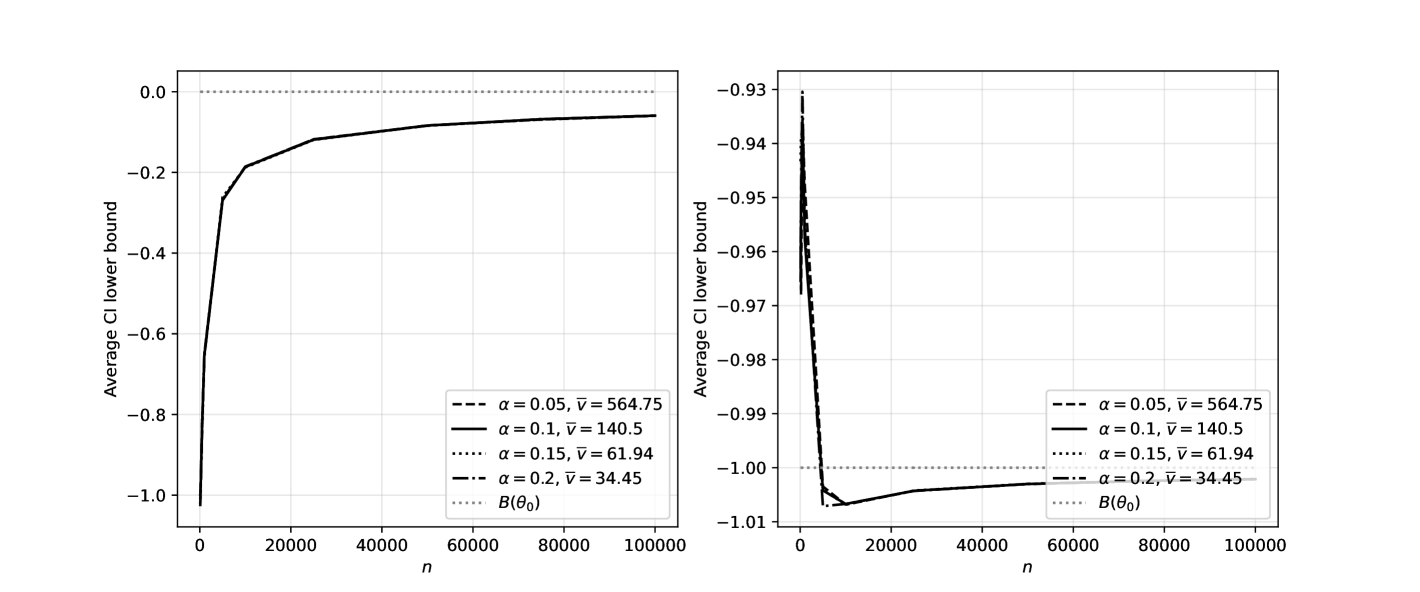

2.6. Monte Carlo

Consistency and inference simulations use and repetitions respectively.

2.6.a. Consistency

We first describe Example 2.1 in more detail. Consider a setup with variables and constraints. Recall that . In this case, the parameters are defined as

| (14) |

The sample analogues of parameters in (14) are obtained by substituting with its estimator . In our simulation study, that estimator is given by , where for are i.i.d.

The true parameter is in one-to-one correspondence with the underlying measure, and is completely described by it: . Consequently, it is sufficient to index the parameter , the identified polytope and the program’s value by only.

Observe that the example (14) is so engineered that would never be empty or unbounded, ensuring the existence of the plug-in estimator . A slight modification to that setup, that we consider in the next subsection, would lead the identified polytope to be empty with a potentially non-vanishing probability.

Measures

We consider two values of : and . At , SC fails, because has an empty interior. LICQ also fails at , as at the optimum , inequalities are binding. There are no flat faces at . At , SC, LICQ and NFF all hold. The values and result in the smallest singular values of matrices that correspond to the th and the th percentiles of the Tao-Vu distribution given in Theorem H in the Online Appendix.

If , the norm of the ‘smallest’ KKT vector in the true LP corresponding to (14) is proportional to . So, for a small negative , the -condition is only satisfied for a small value of . In this case the ‘optimal’ is large. By that logic, the plug-in estimator, which in this case obtains as the limit , should perform well at such , and potentially outperform the debiased penalty estimator. This is partly an artifact of the setup in (14): additional noise in one of the slated lines’ intercepts would render the problem infeasible with positive probability, which would worsen the performance of the plug-in estimator in finite samples (see Figure 9).

At , the -condition is satisfied with a relatively large , and so the ‘optimal’ is relatively small. If , in 50% of the cases, is estimated. If, moreover, , the debiased penalty estimator would select the incorrect maximum of in such cases. A larger at thus hampers the performance of the debiased penalty estimator.

Parameters

We set , where is the quantile of the dimensional Tao-Vu distribution given in Theorem H in Appendix H. To ensure the same expansion rate for the set-expansion estimator, we set . There is no guidance as to the selection of . Our baseline is , and we explore other values in Figure 8.

Discussion

Consider the right panel of Figure 6, corresponding to . The plug-in estimator is inconsistent, while the set-expansion estimator performs well, approaching from below for larger . The debiased penalty-function estimator is slightly upward-biased for smaller , but yields the value of almost exactly in larger samples. In contrast, the set-expansion estimator has a conservative rate, and remains slightly downward-biased even in larger samples.

The case of is depicted in the left panel of Figure 6. The plug-in estimator is consistent and appears to be the best estimator out of the three. The set-expansion estimator is severely downward-biased. This is because when the optimal vertex has a ‘sharp’ angle, a small expansion of the inequalities’ RHS may lead to a large shift of the vertex. To see that, consider shifting both inequalities outwards in Figure 2 for a small and a large absolute value of , when is negative. Once the expansion grows smaller, the set-expansion estimator slowly converges to the true value of from below. While selecting a smaller parameter would improve the performance of the set-expansion estimator at , in the next part of our analysis we demonstrate that in this example is close to being optimal in the uniform sense, because smaller worsens the estimator’s performance at . The debiased penalty estimator, in contrast, converges rather quickly. It is slightly conservative at smaller , as it selects the incorrect vertex of whenever and , i.e. when the penalty parameter is not large enough.

Robustness of the debiased penalty estimator

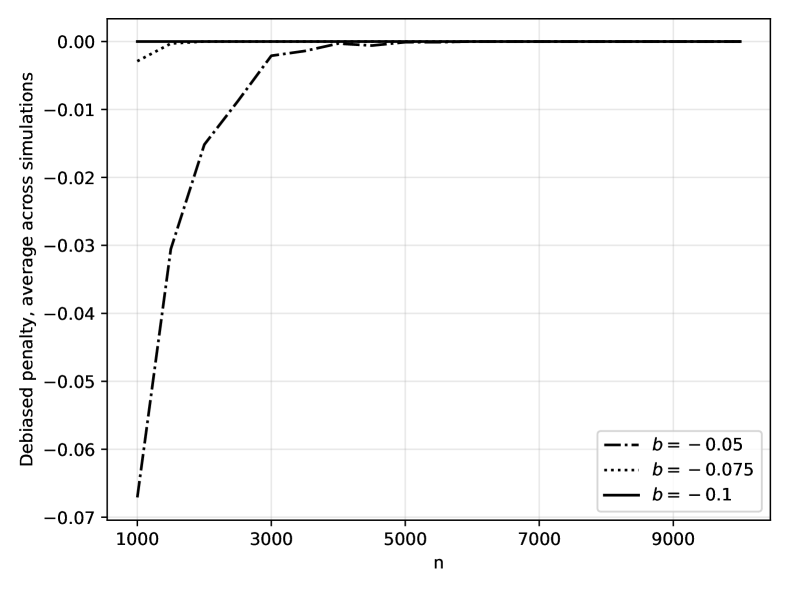

For , the debiased estimator may be expected to perform better at measures with a larger . Figure 8 illustrates that point:

Researchers applying any LP estimator should exercise caution when operating in smaller samples due to irregularity inherent in 3. In example (14), the debiased penalty estimator exhibits desirable behavior even along highly irregular measures for sample sizes of order . Such sample sizes are not uncommon in partially identified settings. In our application, estimation is performed on observations.

Alternative

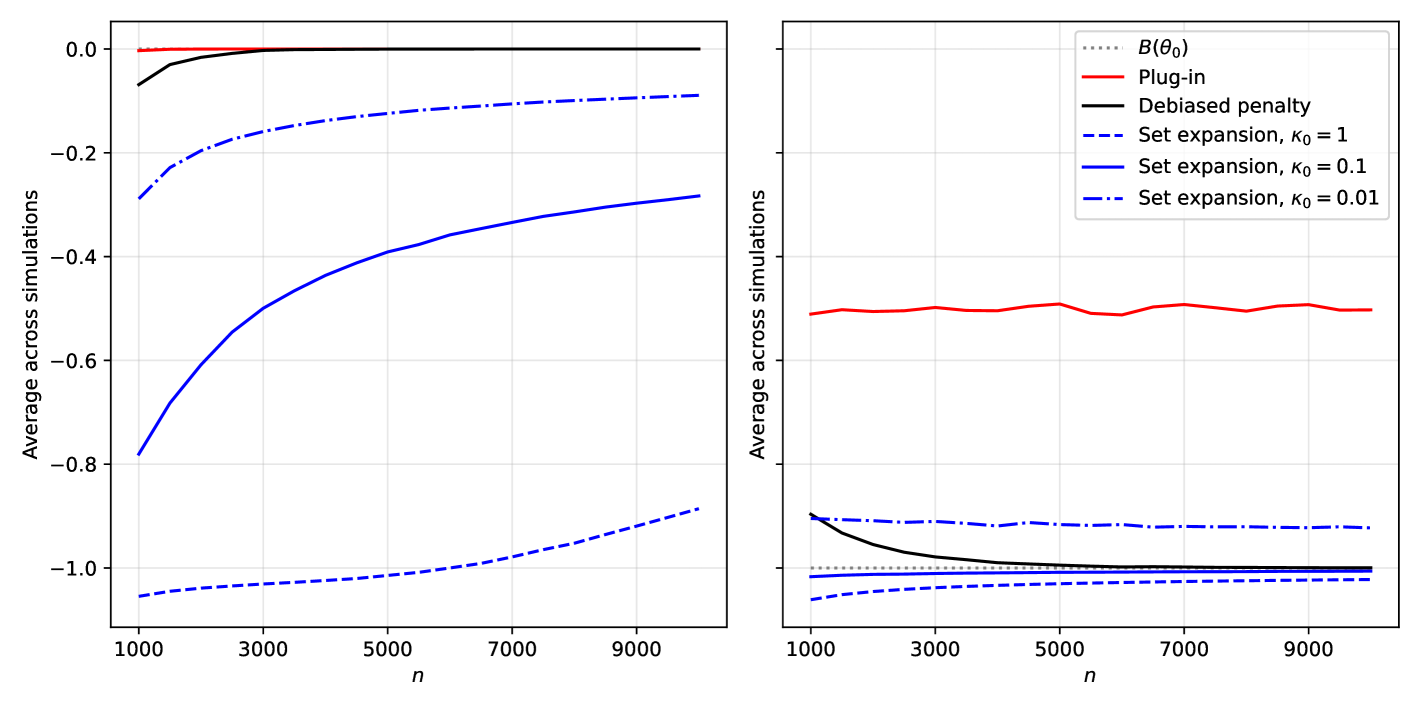

We now investigate to which extent the behavior of the set-expansion estimator can be improved by selecting an alternative parameter. Clearly, a larger makes the set-expansion estimator more conservative. However, cannot be selected as small as possible. If the expansion is too small, it may be insufficient to counteract the noise involved in estimating , leading to poor performance of the estimator at measures where SC fails to hold.

That tradeoff is very clear in Figure 8. Compare the performance of the estimator with to the baseline of . Decreasing down to makes the estimator less conservative at , but results in an upward bias at . This occurs, because at the resulting set-expansion sequence is too small to counteract the estimation noise for the considered sample sizes. This logic is ‘monotone’, meaning that selecting an even smaller would worsen the performance at further. Even at , the set-expansion estimator is quite conservative for the measure , and the parameter can clearly not be reduced any further without affecting the validity of the estimator at . It appears that the baseline choice of is close to being optimal in our example. Therefore, the conservative behavior of the set-expansion estimator at is not explained by a poor choice of the tuning parameter, but rather is a feature of the estimator itself.

Noise in

We also report the result of consistency simulations for the DGP described in (15). This DGP features noise on the right-hand-side of the inequalities that describe the polytope, which allows the estimated polytope to be empty.

In Figure 9, the plug-in and the debiased penalty estimators perform equally well at . The rest of the conclusions are qualitatively unchanged.

2.6.b. Inference

In this section, we assess the performance of our inferential procedure. We compare it to the performance of two recently developed methods, Cho and Russell (2023) (CR) and Gafarov (2024) (BG). We consider a slightly modified version of example (14):

| (15) |

The sample analogues of parameters in (15) are obtained by substituting with their estimators:

where , i.i.d. across and . We consider measures, for which the true values of , whereas we still vary as in the example before. As before, we mainly consider and .

Note that in (15) the plug-in estimator of the polytope may be empty for some realizations of . That is the case, for example, if and .

Other methods

In case SC fails, the BG estimator is not applicable. It fails to exist in around 25% of cases at . The CR estimator in the main text of the paper also relies on and is not applicable if SC fails. The procedure described on p.47 of the Supplementary Appendix in Cho and Russell (2023) would not be practically applicable without the results contained in the present paper. It can be shown that the CR augmented procedure combines a random, non-vanishing set expansion and objective function perturbation with the penalty function approach181818Because the penalty function estimator can be rewritten in the form of an equivalent problem w.p.a.1.. The authors, however, treat the analogue of the penalty parameter as ‘some [fixed] large value’. They proceed to argue that the inequalities, which establish the size of their inference procedure, hold for any value of , which appears to suggest that its selection is unimportant. There is no practical guidance on selection, and CR do not implement the augmented estimator in their simulations. In this paper, we studied penalized estimation in great detail, and our results suggest that the appropriate choice of is critical. Both our previous findings and simulations in Figure 10 demonstrate that for different values of the performance of the CR procedure ranges from highly conservative to invalid. Selecting ‘a large value’ of does not yield a valid procedure in finite samples. Our simulations also suggest that CR augmented approach can perform relatively well if combined with our results on the rate and level of . Unlike our approach, however, it remains asymptotically conservative due to the use of non-vanishing random expansions.

Implementation details

As mentioned in Section 2.2, one can obtain an estimator for the asymptotic covariance matrix of via resampling. One then plugs it into the expression for to obtain the required s.e. An even simpler approach is to obtain an estimator for directly by bootstrapping the quantities estimated on the second fold, while keeping the first fold quantities fixed. We have verified that the performance of the two approaches is similar to using the closed-form estimator for , namely , where and is the sample covariance matrix of . We employ the latter estimator in our simulations. When implementing the procedure in Cho and Russell (2023) (CR), we use uniform noise with the support size of , as recommended in the paper. Note that we refer to their parameter as . The estimator in Gafarov (2024) (BG) was implemented using the code kindly provided by the author.

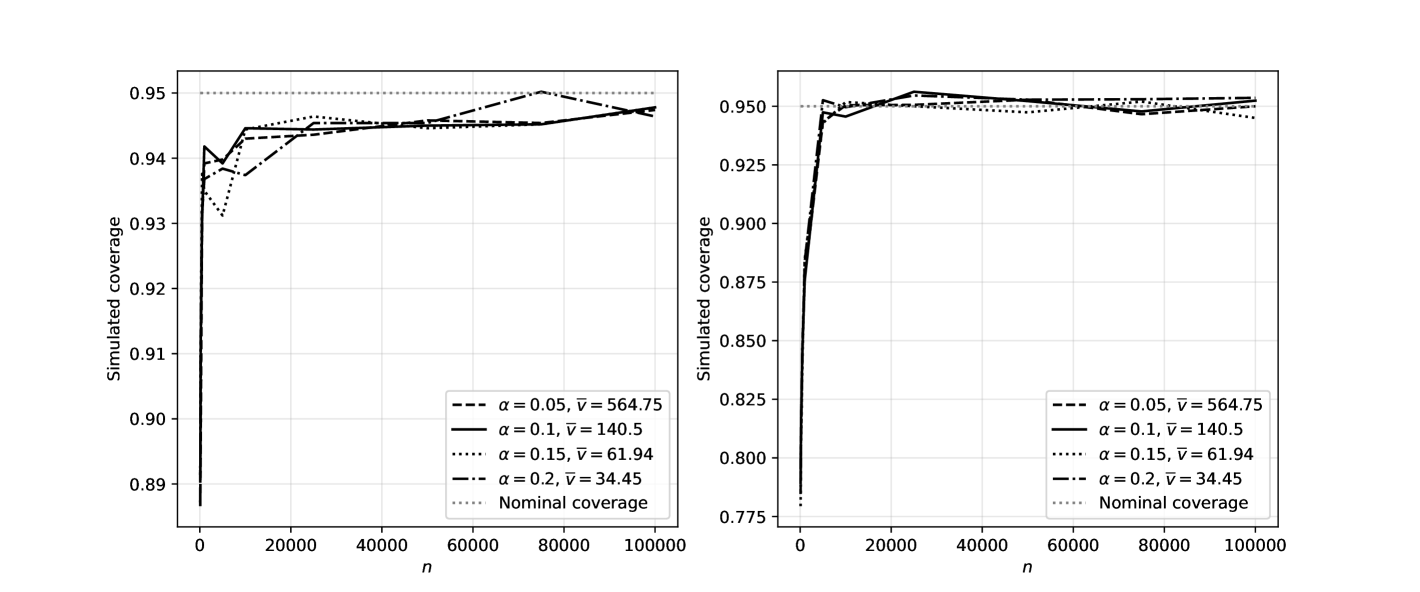

Discussion

Results of our simulations are given in Figure 10. Overall, it appears that our estimator has the correct nominal level even at smaller sample sizes, whereas the CR with penalty overcovers asymptotically. BG estimator achieves nominal coverage asymptotically, although it over-covers in smaller samples and may yield a very conservative left confidence bound, as is evident from the right panel. It fails at , because the SC fails191919We have still run the corresponding simulations, but are not displaying them. BG fails to exist in around 25% of cases, while the remaining simulations result in highly conservative bounds with incorrect coverage. For different fixed values of the Cho-Russell procedure’s performance may range from highly conservative to invalid. We illustrate this by adding lines with and to the figures corresponding to and , respectively.

3. Special case of LP bounds

Let denote the outcome of interest202020Univariate case is considered for simplicity of exposition, but the extension to multivariate outcomes is immediate., stand for the treatment, and be the candidate instrument. Here treatment is any variable which effect on we attempt to infer, whereas the term instrument refers to an auxiliary variable that allows us to partially identify the causal effect of interest. Our approach nests the case when is the usual IV. The reader seeking an economic intuition may refer to Section 5, where is the log-wage, is the level of education, and is a proxy for the level of ability.

Denote the supports as , and respectively. Throughout this section we consider the case of continuous outcome and discrete treatment and instrument, namely is a (possibly infinite) interval212121We focus on the uncountable case for concreteness. Inclusion (20) in Theorem 3.2 holds generally, while sharpness also holds for the case of arbitrary if there are no almost sure inequalities., while and . In non-parametric bounds literature it is rather conventional to employ a discrete instrument at the estimation stage (see Manski and Pepper (2009)). While our main identification result may be extended to continuous , estimation in such settings is left for future research.

Our setup accommodates missing observations of the dependent variable. Namely, we split the set of treatments into two disjoint subsets . Whenever , the researcher observes , whereas if , only the covariates are observed. For example, in Blundell et al. (2007) the wage is observed only if an individual is employed. Corresponding to the legs of the treatment are the potential outcomes :

Continuing the wages and education example, the value of for a fixed may then correspond to the potential wage that an individual with the associated random characteristics would get, had she obtained education .

Let us collect the potential outcomes in the vector . Variables are jointly defined on the true probability space and we let denote the considered collection of probability measures on , such that . We impose the following conditions on the set of considered measures throughout this section:

Assumption I0 (Conditions on ).

is such that if: i) generates and ; ii) and iii) for all and

Part i) of the Assumption I0 formalizes the assumed identification pattern. It says that the joint distribution of is always identified and the researcher also observes the joint distribution of whenever . Parts ii) and iii) of I0 ensure that all conditional expectations and probabilities are well-defined and finite222222Similar identification results can still be obtained if one relaxes the full-support condition for some known pairs from . Note that it can also be verified in the data..

Remark 3.1.

Under no missing data, i.e. , condition i) is equivalent to generating the identified joint distribution .

We define the vector collecting all elementary conditional moments as

and suppose that the researcher is interested in the target parameter , given by

| (16) |

where is identified232323By this we mean that for all . and chosen by the researcher. It parametrizes the choice of the outcome of interest, as the following remark clarifies.

Remark 3.2.

The form (16) nests i) , ii) and iii) .

3.1. Affine inequalities over conditional moments

We now introduce the general class of identifying conditions described by affine inequalities over conditional moments, potentially augmented with affine a.s. restrictions. These restrict the set of admissible measures to :

| (17) |

where , , and are identified parameters, chosen by the researcher. These parametrize the choice of identifying inequalities on conditional moments of potential outcomes as well as almost sure inequalities on the potential outcomes. In general, and are functionals of . We omit this dependence whenever it does not cause confusion.

The family of models that can be written in the form (17) is very rich, as illustrated by the following examples.

Example 3.1 (MIV).

Example 3.2 (IV).

is mean-independent of potential outcomes if, for each and , . This assumption is nested in AICM for , , and no a.s. restrictions.

Example 3.3 (MTR).

Monotone treatment response assumption Manski and Pepper (2000) imposes that, for each , if , then a.s. It is nested in AICM for an appropriate choice of matrix with , and no inequalities over conditional moments, .

Example 3.4 (Roy model).

Lafférs (2019) imposes that for each , the individual’s choice is, on average, optimal: . It is nested for an appropriate choice of matrix and , and no a.s. restictions.

Example 3.5 (Missing data).

Blundell et al. (2007) derives bounds on - the cdf of wages evaluated at some , conditional on . The wage is observed if the individual is employed, , and unobserved otherwise (). Introduce and . Let , so that . Our approach allows to accommodate all identifying conditions in the original paper by appropriately choosing and .

Remark 3.3.

Combinations of assumptions are obtained by stacking the respective matrices, as in Example 3.2. Sensitivity analysis can be performed via relaxations , or for some . For example, given some , inequalities for with and yield a relaxation of MIV. In De Haan (2017) the shape of observed moments may suggest a failure of monotonicity near the boundaries of . Selecting positive for values of close to the boundaries could constitute a meaningful robustness check.

3.2. Linear programming bounds

We now provide the general identification result for the models described by . Let us construct that collects unobserved pointwise-conditional moments242424Formally, is a partially identified functional , whereas is point-identified. and the vector of those pointwise-conditional moments that are identified:

For known selector matrices , one can then decompose as

It is also straightforward to observe that a.s. implies

| (18) |

Before we state the main identification result, let us construct the matrix and the vector that combine the conditional restrictions with the implications of the almost sure restrictions in (18), as

| (19) |

Suppose Assumption I0 holds. For any , the sharp identified set for satisfies

| (20) |

where

Reverse inclusion in (20) holds if , or if one of the following is true:

-

(i)

MTR holds, i.e. a.s. s.t. :

-

(ii)

Outcomes are bounded, , a.s. for known :

(21) -

(iii)

MTR holds, outcomes are bounded and can support a r.v.:

(22)

The matrix is defined in Appendix D.3.

Theorem 3.2 postulates that bounds on the target parameter under can be obtained by solving two linear programs. The LP bounds are sharp if there are no a.s. inequalities in the model, or if the a.s. inequalities parametrize three special cases that are typically used in the literature. Otherwise, the LP bounds are valid, but not necessarily sharp, as we show in Appendix D.2. This is because, in general, the entire distribution of is relevant for under a.s. restrictions. The naive approach of searching over such joint distributions, however, would involve infinite-dimensional optimization, because .

Remark 3.4.

Remark 3.5.

The empirical literature has extensively relied on the MIV + MTR + MTS combination of Manski and Pepper (2000) assumptions, as it yields the tightest bounds out of all classical conditions. In the absence of a theoretical justification, this has led to errors Lafférs (2013). Theorem 3.2 provides the first available sharp bounds under this combination when is continuous.

Remark 3.6.

In any of the sharp cases in Theorem 3.2, the polytope gives the sharp identified set for the vector of unobserved pointwise-conditional moments under the corresponding AICM model described by .

4. Conditional monotonicity assumptions

A particular family of identifying conditions that can be written in the form (17) is the conditional monotonicity class of assumptions. These impose that potential outcomes are mean-monotone in the instrument even within some treatment subgroups. While more restrictive than the conventional MIV, conditionally monotone instrumental variables (cMIV) allow to sharpen the bounds on the outcomes of interest. Throughout this section, we assume that outcomes are bounded for known , . We also suppose that there are no missing data252525Although it is hopefully clear from our general approach how cMIV conditions extend to the missing data case., i.e. .

We argue that cMIV assumptions are reasonable in classical applications, discuss the difference between MIV and cMIV and develop a formal testing strategy for a particular version of cMIV. This testing procedure relies on the observed outcomes’ monotonicity, which has been typically used in applied work to justify applying MIV. Our results imply that if such monotonicity is observed and the researcher is comfortable with MIV, the cMIV assumption is inexpensive, and can be applied to sharpen the bounds on the outcomes of interest. In some applications, as is the case in Section 5, cMIV yields informative bounds even when the classical conditions fail to do so.

While we only discuss three variations of cMIV, the class of such assumptions is potentially richer262626One can consider the class of conditional restrictions for all where subcollections are chosen by the researcher. The triplet from Theorem 3.2 under any such restrictions can be constructed by following the procedure in Appendix I.2., and Theorem 3.2 applies in any such framework.

Assumption cMIV-s.

Suppose that for any , and s.t. we have:

i.e. the potential outcomes are, on average, non-decreasing in for any treatment subgroup.

The strong conditional monotonicity assumption possesses the greatest identifying power across all considered cMIV conditions. To see that cMIV-s implies MIV, set in the definition above.

Assumption cMIV-w.

Suppose MIV holds and for any and s.t. we have:

i.e. the potential outcomes are, on average, non-decreasing in for the non-treated and the whole population.

The weak conditional monotonicity assumption allows for closed-form expressions for sharp bounds that are easy to compute and perform inference on.

Assumption cMIV-p.

Suppose MIV holds and for any and s.t. we have:

i.e. the potential outcomes are, on average, non-decreasing in conditional on any counterfactual level of treatment.

The pointwise conditional monotonicity assumption is directly testable under a mild homogeneity condition, see Section 4.2.

Conditional monotonicity restrictions differ in the collection of treatment subsets over which monotonicity in the instrument is assumed. The strong conditionally monotone instruments are such that, among individuals from any given counterfactual treatment subgroup, higher values of are, on average, associated with higher potential outcomes. The weak conditional monotonicity restriction only imposes the same mean-monotonicity on the whole population and on the untreated, whereas the pointwise form assumes it over the entire population as well as conditional on each counterfactual level of treatment.

Remark 4.1.

All cMIV assumptions imply MIV. Moreover, cMIV-w, cMIV-p are implied by cMIV-s. If treatment is binary, cMIV-s, cMIV-w and cMIV-p are equivalent.

While it is possible for the general apporach of form (17), cMIV conditions avoid assuming monotonicity over the observed treatment subset . This is because such monotonicity is identified. If it holds, it should not add any identifying power to our conditions in theory. However, large violations of the observed outcomes’ monotonicity will lead the test developed in Section 4.2 to reject cMIV-p and cMIV-s.

The following observation motivates the use of cMIV assumptions.

Manski and Pepper (2000) MIV bounds are not sharp under either cMIV-s, cMIV-w or cMIV-p.

Proof.

Consider a binary treatment , three levels of the instrument with and . Suppose for a fixed , we have , with , , . The no-assumptions lower bounds on are . MIV ‘irons’ the no-assumptions bounds to , which also implies the lower bounds on : . Under cMIV, one can further ‘iron’ these to improve the lower bound for up to , so that the lower bound on becomes . ∎

Sharp bounds for all versions for cMIV follow from Theorem 3.2. We also show that under cMIV-w the bounds can be characterized explicitly, which is especially convenient if the treatment is binary, so that all cMIV assumptions coincide (see Appendix I.1). For didactic purposes, we also provide detailed guidance on how to construct the triplet from Theorem 3.2 under cMIV-s, cMIV-p and MIV in Appendix I.2.

4.1. Discussion of cMIV

This section illustrates the difference between MIV and cMIV by considering two parametric examples with classical applications.

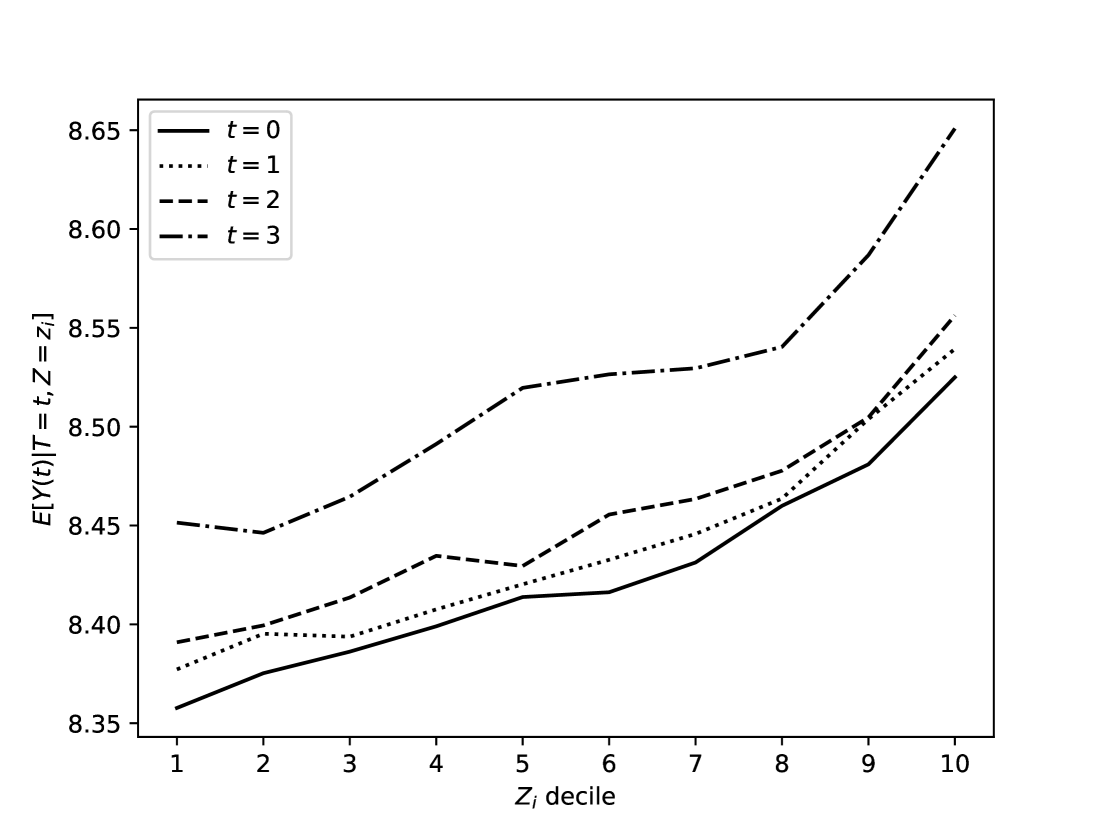

4.1.a. Education selection

Consider the following empirical setup. Suppose is an indicator of whether or not an individual has a university degree, are potential log wages and is an observed indicator of ability.

MIV assumption on implies that more able individuals can do better both with and without a college degree on average: - monotone in . cMIV additionally imposes that: i) among those who have a college degree, a smarter individual could have done relatively better on average than their counterpart if both did not have it: - monotone in ; and ii) among those who do not have a college degree, a smarter individual could have done relatively better on average than their counterpart if both had it: - monotone in .

We now consider a parametric example. Suppose that measures how diligent one is from birth and is ex-ante mean-independent of . While is observed by both the employers and the econometrician (e.g. an IQ score), the employer additionally observes the employee effort level with . Suppose and . Suppose that, on average, employees choose to maximize their expected earnings. This motivates a stylized Roy selection model, with

where is remaining heterogeneity, and . MIV demands that

MIV postulates that the direct effect of ability on potential earnings is positive. It seems reasonable to suppose that , i.e. both effort and ability increase potential wages. Letting and denote the differentials in the effects of ability and effort respectively, the additional requirement of cMIV is that:

| (23) | |||

| (24) |

where .

Notice that if and are of different signs, for example because the jobs that one may apply for with a college degree are more ability-intensive (), whereas those which are available otherwise are more skill-intensive (), the additional conditional monotonicity requirements (23)-(24) are less strict than MIV. This is because, conditional on both having a degree and not having it, ability and effort are positively associated.

Intuitively, among those who do not have a degree (), people of higher ability must have had stronger incentives to forgo college. This should have been because a higher level of diligence gives them a comparative advantage in effort-intensive jobs. Among those with a degree, higher ability implies a comparative advantage in ability-intensive occupations, which explains their willingness to select into this option (). It does not, therefore, signal as low an effort level as it would for a less capable individual.

Now consider the same setup with and ,

This selection mechanism can be explained by the fact that to get a degree one needs to be either hard-working or of high ability. The requirement of MIV is unchanged, and cMIV necessitates that:

| (25) | |||

| (26) |

In this case, conditional on each level of education, effort level and ability are negatively associated, so the conditional selection terms in (25)-(26) make cMIV a stricter assumption than MIV. Intuitively, a more able individual with a college degree did not need to work as hard to get it as her counterpart with a lower ability. Similarly, if an individual is capable, but does not have a degree, she has to be of lower effort as otherwise she would have selected into education.

Even if MIV holds, cMIV can thus fail if employer prefers effort over ability to the extent that the conditional negative association between the two outweighs the direct impact of ability on wages as well as any ex-ante positive correlation between the employer-observed signal of diligence and the ability.

An examination of equations (23) and (24) suggests that cMIV is more likely to hold whenever is small relative to , while is large relative to . This means that should be relatively weak in the parlance of the classical IV models, and strongly monotone.

Overall, it seems reasonable to use a proxy for the level of ability as a conditionally monotone instrument in the estimation of returns to schooling. One would be inclined to think that while does enter selection, it affects the potential outcomes directly and strongly enough, so that there are no subgroups by schooling for which a higher value of ability would correspond to lower potential wages on average.

4.1.b. Simultaneous equations

As some aspects of mathematical intuition may be muted in discrete models, we also consider a simple continuous setup to confirm the insights derived from the previous analysis. For illustrative purposes, we drop the boundedness and discreteness assumptions and consider the supply and demand simultaneous equations,

The observed log-price clears the market in expectation,

| (27) |

where are continuous unobserved and observed random variables respectively, with a.s.272727Mean independence is not restrictive, as it can always be enforced by redefining the d.g.p. in an observationally equivalent way. and with for . Further assume that all functions of are continuous.

Potential price indexes the potential outcomes, giving rise to the demand and supply schedules. Suppose we aim to identify the elasticity of supply, for some , and is a monotone instrument for , while can be interpreted as treatment. is unobserved heterogeneity and are random violations from the market clearing condition or measurement errors independent of the rest of the model. For an individual realization of market clearing an econometrician observes , but does not observe the schedules at other prices , nor disturbances .

Define and similarly for , with . As stated, the model is potentially incomplete or incoherent, as for a given vector equation (27) may have multiple or no solutions. To avoid that, so long as that the support of is full, it is necessary that , be constant. We shall assume that for simplicity. Provided that , which determines the excess supply at fixed , is strictly increasing and has full image, the model is complete and coherent, and

| (28) |

Equation (28) introduces a deterministic linear relationship between and conditional on each given value of . As we saw in the previous example, this constitutes the worst-case scenario for cMIV, if and have the same sign. A noisier selection mechanism would relax the conditional link between and , and would thus weaken the conditional selection channel.

Note that the reduced-form error is and there is a simultaneity bias, as

In this setup, MIV requires that

Whereas cMIV-p additionally imposes that

| (29) |

Suppose that to rule out uninteresting cases. (29) then implies

| (30) |

For concreteness, consider two positive supply shocks, i.e. . Equation (30) means that either and affect the reduced-form equilibrium price in different directions (recall the comparative advantage example), or the effect of on the equilibrium price relative to its effect on the supply schedule is smaller than that of ,

| (31) |

Under , equation (31) once again requires that be strongly monotone and relatively weak for cMIV-p to hold. The logic we described may help the researcher navigate the potential economic forces in a given application to decide whether cMIV-p is a suitable assumption.

For example, consider estimating the supply elasticity in the market for plane tickets in the early days of Covid-19 pandemic. Suppose is an inverse Covid-stringency index for the economy, while may be interpreted as residual cost shocks, defined to be mean-independent of . It is likely that , i.e. residual cost shocks affect mainly the supply in that sector, and not the demand. It is also likely that either supply is less responsive to than demand (so that cMIV is implied by MIV), or the effects are of the same order of magnitude. is therefore likely to be a conditionally monotone instrument.

4.2. Testing cMIV

One could argue against cMIV conditions whenever fail to be monotone in the data. In general, the power and size of that test are unclear. There is, however, a special case when cMIV can be tested directly, provided that the researcher is willing to assume MIV. In some applications one may conjecture that the potential outcomes’ functions , either in the reduced or in the structural form, are such that the relative effects of and the unobserved variable(s) , potentially correlated with , are unchanged across outcome indices .

Researchers often impose even stricter versions of this homogeneity assumption. For example, Manski and Pepper (2009) discuss MIV identification under HLR condition: . Conditions in Proposition 4.2 relax HLR to an arbitrary shape of response of a potential outcome to treatment and allow for a generally heteroscedastic/treatment-specific response to unobserved variables and instrument, so long as the relative effects are unchanged across potential outcomes. All functions in the proposition below are assumed to be measurable.

Suppose that a): i) , for all , with and ii) MIV holds, strictly for some with ; or b): i) for all , with , ii) ; and iii) MIV holds. Then Assumption cMIV-p holds iff are all monotone. Note that whether or not is observable in the data for case and whether or not is also identified for .

Remark 4.2.