captionlabel \addtokomafontcaption

Exploring Competitive and Collusive Behaviors in Algorithmic Pricing with Deep Reinforcement Learning

Abstract

Nowadays, a significant share of the business-to-consumer sector is based on online platforms like Amazon and Alibaba and uses Artificial Intelligence (AI) for pricing strategies. This has sparked debate on whether pricing algorithms may tacitly collude to set supra-competitive prices without being explicitly designed to do so. Our study addresses these concerns by examining the risk of collusion when Reinforcement Learning (RL) algorithms are used to decide on pricing strategies in competitive markets. Prior research in this field focused on Tabular Q-learning (TQL) and led to opposing views on whether learning-based algorithms can result in supra-competitive prices. Building on this, our work contributes to this ongoing discussion by providing a more nuanced numerical study that goes beyond TQL, additionally capturing off- and on-policy Deep Reinforcement Learning (DRL) algorithms, two distinct families of DRL algorithms that recently gained attention for algorithmic pricing. We study multiple Bertrand oligopoly variants and show that algorithmic collusion depends on the algorithm used. In our experiments, we observed that TQL tends to exhibit higher collusion and price dispersion. Moreover, it suffers from instability and disparity, as agents with higher learning rates consistently achieve higher profits, and it lacks robustness in state representation, with pricing dynamics varying significantly based on information access. In contrast, DRL algorithms, such as PPO and Deep Q-Networks (DQN), generally converge to lower prices closer to the Nash equilibrium. Additionally, we show that when pre-trained TQL agents interact with DRL agents, the latter quickly outperforms the former, highlighting the advantages of DRL in pricing competition. Lastly, we find that competition between heterogeneous DRL algorithms, such as PPO and DQN, tends to reduce the likelihood of supra-competitive pricing.

Keywords: Algorithmic Pricing, Tacit Collusion, Reinforcement Learning, Market Competition

1 Introduction

During the past two decades, a significant share of the B2C business has transitioned towards leading online retailers such as Amazon and Alibaba. With the rise of Artificial Intelligence (AI) and big data, sellers on these platforms increasingly rely on pricing algorithms to explore market dynamics and demand elasticity. In practice, algorithms help businesses adapt to market changes, find optimal strategies, and improve decision-making efficiency. However, some real-world cases have provided evidence that algorithmic decision-making can lead to collusive outcomes, resulting in supra-competitive pricing and sustained collusion (Assad et al. 2020, Brown & MacKay 2021). In this context, algorithmic collusion refers to a phenomenon where independently operating pricing algorithms learn to agree on setting prices above the Nash equilibrium, leading to supra-competitive results, even though the algorithms were not explicitly designed for collusion.

While such tacitly collusive outcomes remain problematic from a market perspective, independently operating pricing algorithms cannot be held responsible for collusion due to their lack of communication and mutual understanding capabilities (Harrington 2018). This creates significant challenges for regulatory bodies in enforcing competition law and antitrust policies (Mehra 2015). Accordingly, automated pricing algorithms pose a potential risk of tacit collusion in modern markets, drawing widespread attention and concern from scientists, antitrust authorities, and practitioners (Ezrachi & Stucke 2017b, Varian 2018, Agrawal et al. 2019). In this paper, we focus on supra-competitive outcomes higher than the Nash equilibrium and refer to the phenomenon as algorithmic collusion or collusive prices.

These concerns go beyond deliberately designed price-manipulating algorithms, and hold particularly for hypothetical or experimental self-learning algorithms that aim to maximize profits. Among such algorithms, Reinforcement Learning (RL) serves as a widely studied example, enabling autonomous learning of pricing strategies through self-play without prior knowledge or explicit guidance from developers. Based on the observed pricing history, algorithms can communicate and coordinate collusive behaviors to maintain an off-equilibrium state. However, in most practical settings, the length of pricing history considered in the state representation is limited, as including longer histories significantly increases the state space, making it computationally challenging. Nevertheless, we analyze this aspect in our study. If such pricing dynamics exist, they pose a serious threat to markets, potentially leading to inefficiencies that benefit companies at the expense of consumers. Although many prices today are still established by human salespeople and subjective judgments, these pricing algorithms may become widespread in retail markets in the near future (OECD 2017). Detecting these issues early is crucial to preventing their widespread adoption, which may lead to unintended consequences such as market distortions and reduced competition regarding algorithmic decision-making.

So far, there is no consensus on whether algorithmic collusion exists or whether it leads to supra-competitive prices that negatively impact social welfare. This lack of consensus highlights the theoretical and practical challenges of analyzing tacit collusion between algorithms. On the one hand, there are no clear standards for detecting algorithmic collusion in real markets, and data or information gaps, often exacerbated by confidentiality, complicate rigorous analyses even further. On the other hand, studying algorithmic collusion through stylized market models can detect tacit collusion by comparing results to analytically derived equilibria, but existing analyses have often been limited to single, simple algorithms, which has led to concerns about their generalizability. In fact, most existing studies focus on Tabular Q-learning (TQL) and argue that if simple algorithms can learn to collude, more complex algorithms, including those that adopt deep learning, will pose even greater risks of tacit collusion (Calvano et al. 2020, Klein 2021). Several studies have explored the use of Deep Reinforcement Learning (DRL) in algorithmic pricing (Liu et al. 2019, Chen et al. 2021), highlighting its potential for strategic pricing decisions. While most existing analyses remain academic, the increasing interest in DRL makes these algorithms strong candidates for real-world pricing applications. However, details of such implementations are rarely disclosed, as firms withhold information about proprietary algorithms to prevent exploitation. In this context, our study aims to provide more nuanced numerical analyses, capturing DRL algorithms beyond RL to reveal the risks of collusion in algorithmic pricing.

Contribution This paper advances the study of algorithmic collusion by systematically analyzing the pricing behavior of DRL algorithms in competitive settings. Building upon prior research focused on TQL, we extend the analysis to more sophisticated on-policy and off-policy DRL methods, including Proximal Policy Optimization (PPO) and Deep Q-Networks (DQN). Using a numerical simulation framework based on Bertrand competition models with various demand specifications, we compare pricing strategies, the emergence of supra-competitive prices, and market stability across these learning paradigms.

Our results provide several key insights. First, we demonstrate that TQL exhibits a higher propensity for collusion, leading to supra-competitive pricing and instability in competitive environments. Agents with higher learning rates systematically outperform slower-learning counterparts, creating unfair market dynamics. Second, DRL agents, particularly PPO and DQN, exhibit stronger competitive behavior, consistently converging to prices closer to the Nash equilibrium. When competing against pre-trained TQL agents, DRL agents rapidly outperform them, suggesting that advanced RL approaches mitigate collusion risks. Lastly, we find that interactions between heterogeneous DRL agents, such as PPO and DQN, further reduce the likelihood of collusive behavior, reinforcing the notion that algorithmic diversity fosters competition. Our study provides a in-depth evaluation of algorithmic collusion risks in DRL-based pricing and highlights the potential for competitive pricing dynamics in algorithmically governed markets. By advancing our understanding of RL in pricing competition, we contribute to the ongoing efforts to design fairer and more competitive digital marketplaces.

The following sections provide a detailed exploration of our approach and findings. Section 2 reviews the state of the art. Section 3 defines the problem setting, outlining key assumptions and market dynamics. Section 4 presents the algorithmic framework, describing the RL algorithms used. Section 5 details the experimental design, specifying key parameters and settings. In Section 6, we present the results, followed by a discussion of their significance. Finally, Section 7 concludes with a summary of contributions and suggestions for future research.

2 State of the art

Our work is closely related to two key research directions: the application of RL algorithms in pricing markets and the discussion surrounding whether automated pricing algorithms may lead to collusion. In the following, we review both research streams concisely.

Application of RL Algorithms in Pricing Markets Research on the application of RL algorithms in pricing markets has evolved significantly over time. Early studies primarily focused on basic RL algorithms, particularly the application of TQL in pricing problems. Kephart & Tesauro (2000) demonstrated that TQL could converge to equilibrium in a simulated market environment where two competing pricebots repeatedly interacted, while Kutschinski et al. (2003) showed its ability to find near-optimal strategies in multi-agent markets, though constrained by a zero discount factor. Rana & Oliveira (2014) proposed using TQL for pricing multiple products with interdependent demand, addressing scenarios where users lack precise knowledge of product relationships. Similarly, Kim et al. (2015) applied TQL in energy markets to optimize pricing strategies through specific model adjustments. Collectively, these studies demonstrate the flexibility of TQL across diverse market settings but also reveal inherent limitations in handling complex and dynamic environments.

Building on the foundations laid by basic RL algorithms, recent advancements in AI and big data have shifted the focus toward DRL algorithms in pricing research. These advanced methods address many of the scalability and adaptability challenges faced by TQL, enabling applications in increasingly complex and dynamic market environments. Notably, their potential has been validated through practical implementations in real-world settings. For instance, Liu et al. (2019) pioneered the application of DRL for discrete and continuous dynamic pricing on real-world e-commerce platforms, demonstrating its significant superiority over manual pricing through large-scale field experiments at Alibaba. Beyond e-commerce, Qiu et al. (2020) proposed a deep deterministic policy gradient method for pricing electric vehicles with discrete charging levels. Similarly, Chen et al. (2021) explored spatial-temporal pricing for ride-hailing platforms using PPO. Meanwhile, Yan et al. (2022) developed a hierarchical RL-based community energy trading scheme using historical data. Overall, these studies highlight the versatility of DRL algorithms in addressing diverse pricing challenges, underscoring their potential to enhance decision-making efficiency and adaptability across various industries.

Automated Pricing Algorithms and Collusion The second research stream examines how automated pricing algorithms may facilitate collusion, resulting in supra-competitive pricing and reduced consumer welfare. This phenomenon has drawn significant attention to antitrust laws, with numerous studies emphasizing the urgent need for policies to address this growing challenge (Werner 2023, Constantine & Quitaz 2018, Capobianco & Gonzaga 2020). Existing research on algorithm-driven collusion primarily focuses on two directions: empirical studies and simulation-based approaches.

Empirical studies on algorithmic collusion are limited but provide valuable insights into its real-world risks. For instance, Assad et al. (2020) investigated the German retail gasoline market and found that since 2017, algorithmic pricing has increased average station profit margins by 9%. Similarly, Brown & MacKay (2021) analyzed the U.S. retail market, showing that algorithmic pricing increased price dispersion and resulted in supra-competitive pricing. However, no direct evidence has proven that algorithms autonomously collude, prompting researchers to explore simulation-based analysis in synthetic environments. Claims about the ability of TQL to sustain supra-competitive prices are often grounded in academic studies (Azzutti et al. 2021, Buckmann et al. 2021), and the most influential simulations supporting algorithmic collusion thereby primarily focus on TQL. For example, Klein (2021) simulated sequential pricing scenarios using TQL and demonstrated that algorithms can autonomously learn collusive behaviors even without explicit human intervention. Calvano et al. (2020) applied TQL to the Bertrand competition with logit demand and showed that the algorithm could sustain supra-competitive prices through reward-punishment strategies. Similarly, Abada & Lambin (2023) simulated the electricity market using a Cournot framework and observed comparable collusive behaviors. However, as Calvano et al. (2020) highlighted, a key limitation of TQL is its slow learning speed, often requiring hundreds of thousands of cycles to form collusion.

Although TQL has shown potential for collusion in simulations, its limitations have sparked academic debate regarding the validity of these findings. In particular, some studies question whether the observed collusive behaviors truly reflect the algorithm’s inherent properties or are artifacts of specific experimental setups. For example, Abada et al. (2024) criticized the single-period price reduction reward-punishment scheme used by Calvano et al. (2020), arguing that insufficient exploration was a key driver of their collusion results. Asker et al. (2022) emphasized that supra-competitive pricing heavily depends on the learning protocol, and synchronous learning where algorithms account for competitors’ behavior may lead to more competitive pricing outcomes. At the same time, Meylahn & V. den Boer (2022) and Epivent & Lambin (2022) stressed the need for further research and comprehensive analysis to validate these collusive findings. To date, most existing studies focus on basic RL algorithms (e.g., TQL)(Brero et al. 2022, Dolgopolov 2022, Sanchez-Cartas & Katsamakas 2022, Bichler et al. 2024), while research on DRL in pricing collusion has gained increasing attention. Recent studies, in particular, have more frequently explored DQN and PPO (Friedrich et al. 2024, Kastius & Schlosser 2022, Schlechtinger et al. 2023), supporting our algorithm choices. However, these works primarily focus on specific or single-industry models. In contrast, our study examines DRL across multiple Bertrand oligopoly variants, providing a broader perspective on algorithmic collusion.

3 Problem Setting

We study the Bertrand model (Bertrand 1883), which describes oligopolistic price competition among firms producing homogeneous products. In this context, each firm employs an independent pricing algorithm. Our analysis focuses on duopoly markets, consisting of two firms, indexed as . Each firm produces a product with a given quality and incurs a marginal cost . The Bertrand model primarily examines the interaction between firms, which set product prices , and consumers, who choose products based on these prices. This interaction directly determines the demand for each firm’s product, and the profit for firm is given by . Firms set prices simultaneously, aiming to maximize their profits. This interaction between firms and consumers creates a dynamic relationship between prices and demand, repeated over multiple rounds. At the start of each round, the two firms simultaneously decide on the prices for their products. Based on these prices, consumers determine the demand for each product, and the interaction proceeds to the next round.

We explore various extensions of the Bertrand model, differing in assumptions about product capacity, product quality, and the form of the demand function. In the remainder of this section, we first discuss the characteristics of these market models (Section 3.1), before we elaborate on the respective Nash and monopoly prices (Section 3.2).

3.1 Market Models

We consider three market models: the Standard Bertrand model, the Bertrand-Edgeworth model in which firms face production capacity constraints, and the Logit Bertrand model.

In the Standard Bertrand Model, products are homogeneous, and consumers choose the product with the lower price. The demand function is given by . For two firms with prices and , demand is allocated as follows:

| (3.1) |

This implies that the firm with the lower price captures all demand, while equal prices result in an equal demand split, assuming unlimited production capacity for both firms.

In the Bertrand-Edgeworth Model, firms face production capacity constraints (Edgeworth 1925), which can lead to market prices above marginal cost if their capacity is fully utilized. While this extension adds a realistic constraint to the standard Bertrand model, it complicates the closed-form equilibrium analysis. To ensure well-defined and unique Nash and monopoly prices, we focus on a specific case where two competing firms have identical production capacities , restrict their pricing strategies to the interval , and face a demand function of the form . In this scenario, the demand allocation results in:

| (3.2) |

In the Logit Bertrand Model, we extend the Standard Bertrand model by relaxing the assumption that consumers always purchase from the firm offering the lowest price. Instead, we incorporate demand variation, product substitutability, and the allocation of consumer expenditure among firms, reflecting a more complex market behavior. Following Calvano et al. (2020), we consider a logit demand model where marginal costs remain constant, and each firm sells a single product. In this model, consumers allocate their expenditure across firms based on pricing rather than solely choosing the lowest-priced product, allowing for a more nuanced modeling of substitution effects and competitive dynamics. In this case, the demand for firm ’s product is given by:

| (3.3) |

where the term reflects the utility consumers derive from purchasing product . The parameter captures the degree of horizontal differentiation or substitutability between products. As , products become perfect substitutes, while larger values correspond to increasing product differentiation and lower substitutability.

Figure 1 visualizes the profit functions for all three market models, assuming the demand to behave as described in Equations (3.1)–(3.3). In the Standard Bertrand model, the profit surface exhibits a symmetric and concave shape, reflecting the homogeneous nature of the products and the fierce characterization of the resulting competition, which leads to an all-or-nothing outcome for the players. In the Bertrand-Edgeworth model, the profit function retains a similar structure but shows the influence of capacity constraints,

particularly when demand exceeds the capacity limit. Lastly, the Logit Bertrand model introduces greater asymmetry and smoother transitions in the profit function, capturing the effects of product differentiation and consumer preference heterogeneity.

3.2 Nash Price & Monopoly Price

In the previous subsection, we introduced three distinct demand models, each capturing the effects of product homogeneity, capacity constraints, and differences in consumer demand distribution on firm competition. These models not only differ in terms of demand and competitive behavior but also exhibit significant variations in key pricing strategies, which leads to different Nash prices and monopoly prices. To characterize the competitive dynamics of the market models introduced in Section 3.1, we provide a detailed discussion of the definitions and economic implications of the Nash prices and monopoly prices in the following. These analyses lay the theoretical foundation for studying the evolution of pricing behavior and the potential for collusion.

The Nash price represents a price at which all firms, while seeking to maximize their profits, have no incentive to unilaterally deviate from their pricing strategies. A key characteristic of this price is its stability, as all participants’ strategies are balanced at the Nash equilibrium point, such that deviating from this price yields no additional benefit to any firm. The computation of varies across different demand models.

In the Standard Bertrand model, where firms produce homogeneous products and consumers always choose the cheaper option, firms continuously undercut each other’s prices to capture the market until prices fall to the marginal cost . At this point, any further price reduction becomes unprofitable, making the unique Nash price (Bertrand 1883).

In the Bertrand-Edgeworth model, considering limited production capacities , the price-cutting competition between firms still drives prices toward the marginal cost . As a result, the Nash price remains , similar to the Standard Bertrand model (Levitan & Shubik 1972).

In the Logit Bertrand Model, products are no longer perfectly homogeneous, and consumers choose with a probabilistic preference, leading to a Nash price that no longer equals the marginal cost. In this case, firms determine by optimizing their profit functions with respect to price, solving the following equation:

| (3.4) |

Accordingly, we obtain the Nash price by solving Equation 3.4 simultaneously for all firms. In practice, iterative search methods can be employed, such as scanning over a range of prices and verifying whether any firm can increase its profit by deviating. The price at which no firm benefits from deviation is identified as the Nash price .

The monopoly price is the price that maximizes collective profits when firms coordinate their pricing strategies as if they were a single entity. By reducing output and increasing prices, firms exploit market demand to achieve higher joint profits. This price is typically higher than the Nash price , as it reflects the absence of competition and the pursuit of monopolistic gains.

In the Standard Bertrand Model, given a total demand of and a marginal cost of , the profit function is . Taking the derivative, , and setting it to zero, the profit-maximizing price is . At this price, each firm captures an equal share of the market demand, , and earns a profit of .

In the Bertrand-Edgeworth Model, the introduction of capacity constraints significantly affects how demand is allocated between firms. When the production capacity is limited, neither firm can fully satisfy the total market demand on its own. This creates a setting where firms may benefit from tacit or explicit collusion to coordinate prices and avoid aggressive competition that would otherwise drive prices to marginal cost. When , the monopoly price is derived as in the standard Bertrand case. Given and , the profit function is maximized at .

In the Logit Bertrand Model, the non-linear nature of demand makes calculating the monopoly price more complex. The total profit is given by . To determine the monopoly price, partial derivatives of with respect to and are set to zero. Numerical methods or iterative algorithms approximate the solution by evaluating and over a discretized range of prices, iteratively refining estimates until convergence criteria are met.

The monopoly price is generally higher than the Nash price , as firms, acting as monopolists, exploit market demand to maximize collective profits. Comparing the Nash price with the monopoly price provides insights into whether and to which extent firms engage in collusive behavior.

4 Algorithmic Framework

This section formalizes the algorithmic framework underpinning our study. We first define the agent’s learning behavior within an Markov decision process (MDP) framework. Following this, we describe RL algorithms in our study.

4.1 Markov Decision Process

We analyze the dynamics of algorithmic collusion in pricing decisions involving RL agents. Each agent represents a firm engaging in pricing competitions to maximize profits. The decision-making process is modeled as an infinite-horizon MDP, which captures the ongoing interaction and competition among firms. An MDP provides a mathematical framework for decision-making in stochastic environments, defined by states, actions, transition dynamics, and rewards. In this context, the market serves as the system, the firms act as agents, and demand response functions driven by pricing decisions determine the transition dynamics. Below, we detail the components of the MDP.

State space: At time , the state for each agent consists of a historical set of pricing decisions with a memory length , capturing the agent’s and its competitor’s pricing decisions. Formally, the state space is , where determines the history length. For simplicity, when , the state reduces to , relying only on the most recent pricing decisions.

Action space: At each time step , an agent chooses a price from the action space , which is constrained by a price range . For Standard Bertrand and Bertrand-Edgeworth models, this range is . For the Logit Bertrand model, we follow Calvano et al. (2020) and set these bounds to and , where controls pricing flexibility. When considering a discretized action space, we divide this range into equidistant values, and when , the state space grows quadratically with .

Transition dynamics: Agents’ pricing decisions determine the transition to the next state . Each agent receives a reward , calculated as , where is the marginal cost and represents the demand for agent ’s product based on its own price and the competitor’s pricing decisions .

Objective: Each agent maximizes discounted future rewards, given by

| (4.1) |

where is the discount factor prioritizing immediate rewards.

4.2 Reinforcement Learning Approaches and Algorithm Selection

Building on the introduced MDP framework, we study RL algorithms that enable agents to learn optimal policies through interactions with the environment. RL methods fall into two categories: value-based and policy-based approaches.

Value-based methods estimate value functions, such as the state-value function or the action-value function , and guide decision-making by selecting actions that maximize the expected return based on these value functions. The Bellman optimality equation for value functions underpins these methods:

| (4.2) |

Here, represents the expected utility of starting in state and following the optimal policy , while is the expected utility of taking action in state and then following the optimal policy. The discount factor balances immediate and future rewards. The essence of value-based methods lies in selecting actions that maximize the value, guiding decision-making towards maximizing long-term returns.

Policy-based methods directly optimize a (stochastic) policy , representing the probability of taking action in state . These methods use gradient ascent to adjust policy parameters , maximizing the expected return:

| (4.3) |

where represents a trajectory generated by the policy . By performing gradient ascent on the policy parameters, the agent progressively improves its policy, increasing the probability of selecting better actions, maximizing long-term total returns by converging to an optimal policy.

Value-based RL algorithms can be implemented in a traditional tabular setting, while both value-based and policy-based methods can be realized in a DRL fashion. Traditional tabular RL often struggles with high-dimensional state spaces and complex tasks. DRL overcomes these limitations by leveraging deep neural networks to enhance representation learning, significantly broadening the applicability of the RL framework. Unlike tabular methods or simple function approximations, DRL employs neural networks to approximate value functions, policies, or state representations, making it well-suited for continuous, high-dimensional, and nonlinear problems. Despite challenges such as training instability and sample inefficiency, its strong generalization capabilities establish DRL as a powerful tool for solving complex decision-making problems.

In this study, we aim for a comprehensive analysis of algorithm dynamics, which is why we consider both tabular RL and DRL algorithms in our experiments. Alongside the basic TQL algorithm, we selected DQN and PPO as representative value-based and policy-based DRL methods, respectively. DQN is well-suited for discrete action spaces, that arise in competitive pricing scenarios. By approximating Q-values with deep neural networks, it effectively handles large state spaces and mitigates the curse of dimensionality. Its extensive use in discrete-action tasks, such as games and market bidding (Mnih et al. 2015, Ye et al. 2019), further supports its selection. PPO was chosen for its flexibility in handling both continuous and discrete action spaces, making it suitable for a wide range of pricing models. Unlike value-based approaches, policy gradient methods directly optimize policies, improving efficiency in large state-action spaces. PPO enhances stability by constraining policy updates, leading to faster convergence and strong performance in practical applications (Schulman et al. 2017, Berner et al. 2019). To ensure a fair comparison with DQN and TQL, we focus our studies on its discrete-action space variant.

TQL: Tabular Q-Learning (TQL), introduced by Watkins (1989), uses a tabular representation for the Q-function with dimensions , where and are the sizes of the state and action spaces. Agents update Q-values at each step using the Bellman equation:

| (4.4) |

where is the learning rate, is the next state, and is the discount factor. This method works well in small state-action spaces but struggles to scale due to its reliance on explicit storage of Q-tables.

DQN: Deep Q-Networks (DQN), proposed by Mnih et al. (2015), extend TQL by using deep neural networks to approximate the Q-function . This approach overcomes scalability issues by generalizing across state-action pairs. Key techniques include experience replay, which randomizes training samples to reduce correlations, and target networks, which stabilize training by decoupling target Q-value computation from network updates. DQN performs well in discrete action spaces and high-dimensional state representations.

PPO: Proximal Policy Optimization (PPO), developed by Schulman et al. (2017), directly optimizes the policy using neural networks. Unlike value-based methods, PPO explicitly models the policy and updates it with a clipped surrogate objective:

| (4.5) |

where is the probability ratio between new and old policies, is the advantage estimate, and controls the clipping range. PPO excels in both discrete and continuous action spaces. Gradient clipping ensures incremental updates that prevent performance degradation.

For all three algorithms used, we provide a pseudocode, accompanied by a more detailed explanation in Appendix A.

5 Experimental Design

We investigate three variants of the Bertrand competition model to understand how different market structures affect competitive behavior. In the Standard Bertrand and Bertrand-Edgeworth models, all competitive agents have a marginal cost set to zero. In the Logit Bertrand model, we set to one to align with the data from Calvano et al. (2020). For the Bertrand-Edgeworth model, we apply a capacity constraint of to both agents.

In the Logit Bertrand model, we set the product quality to and the inter-product substitutability to . For the Standard Bertrand and Bertrand-Edgeworth models, the Nash price and the monopoly price are 0 and 0.5, respectively, while the Nash profit and monopoly profit are 0 and 0.125, respectively. In the Logit Bertrand model, increases to 1.473, to 1.925, and and increase to 0.223 and 0.337, respectively.

Algorithm and Parameter Consistency We use consistent neural network architectures for all DRL algorithms: a fully connected feedforward network with two hidden layers of 64 nodes each. Each layer employs ReLU activation functions, and we trained the network using the Adam optimizer. Although tuning architectures for specific algorithms could enhance performance, we prioritize uniformity to ensure that performance differences reflect intrinsic algorithm characteristics. To standardize action spaces, we configure PPO to operate within a discrete action space, aligning it with TQL and DQN. The action space includes price options, evenly divided. In the Logit Bertrand model, we set the relaxation parameter . This ensures that observed differences arise from algorithm characteristics rather than action space discrepancies.

Experimental Configuration & Convergence Our design involves two RL agents simulating pricing decisions for two firms, focusing on TQL, DQN, and PPO.

Note that we do not define a unified convergence criterion across the three RL algorithms. Instead, we execute each algorithm over a sufficiently long time horizon , based on empirical observations, to allow for price stabilization. Two factors motivate this choice. First, DRL algorithms like PPO retain an intrinsic level of exploration during training, complicating the identification of stable policies. Unlike tabular methods, which gradually reduce exploration, PPO continues exploring, making convergence to a fixed or low-variance policy unlikely. Second, algorithms using neural networks and replay buffers, such as DQN, are prone to catastrophic forgetting, especially without a learning rate decay. Even with stable rewards, policy adjustments may occur due to replay buffer dynamics, causing shifts from seemingly stable policies. Thus, we select a sufficiently extended time horizon based on observed empirical stability in prices and profits, aligning with the adaptive dynamics of pricing problems and RL algorithms.

Our experiments were run on high-performance hardware featuring an AMD Ryzen 9 7950X CPU (32 cores @ 4.5 GHz), 128 GB of RAM, and an NVIDIA RTX 4090 GPU (24 GB). Each experiment was independently repeated 20 times, with the mean and standard deviation of results calculated to assess stability and robustness.

Evaluation Criteria We analyze individual pricing trends and profit trajectories using two indicators: the Relative Price Deviation Index (RPDI), and the profit metric , which was proposed by Calvano et al. (2020). The RPDI measures an agent’s pricing relative to Nash equilibrium and monopoly pricing, indicating the extent of supra-competitive pricing. The profit metric assesses an agent’s average profit over time, normalized relative to Nash and monopoly profits. Both indicators use the average values from the last 10,000 timesteps to ensure robustness.

The RPDI is defined as:

| (5.1) |

measuring an agent’s pricing relative to Nash and monopoly levels. The profit metric from Calvano et al. (2020) is given by:

| (5.2) |

indicating changes in each firm ’s profits relative to Nash and monopoly profits. Together, these metrics provide a comprehensive view: when RPDI and values approach 0, behavior resembles perfect competition; values near 1 suggest a higher propensity for collusion.

6 Results

To introduce the findings presented in this section, we briefly outline five core results examining different aspects of RL behavior in pricing. These results first investigate how variations in learning rates with TQL can influence market dynamics. We then turn to the dynamics within a homogeneous RL agents’ setting, evaluating how homogeneous agents interact in competitive environments. Subsequently, we analyze the comparative effectiveness of DRL algorithms and TQL in pricing strategies. Next, we explore competition among heterogeneous DRL algorithms, highlighting the distinct influences that each type of algorithm brings to market behavior. We then examine how different state definitions impact pricing strategies. Building on this, we further analyze the underlying factors driving differences in pricing behavior among the RL algorithms studied.

6.1 Impact of Learning Rate on Market Stability in TQL

In the following, we analyze how learning rates affect pricing strategies, focusing on competition between two TQL agents. Each agent adjusts its pricing strategy based on its assigned learning rate , revealing how variations in influence decision-making and profitability. We assign Agent 0 a higher learning rate than Agent 1 to evaluate differences in market adaptation and profit outcomes. Both agents use an exploration strategy with an exponentially decaying rate , where controls decay speed. This strategy encourages early exploration and gradually emphasizes profit maximization as decreases.

Specifically, we select learning rates from , assigning Agent 0 consistently higher rates than Agent 1. This setup creates six unique learning rate combinations. To evaluate performance, we calculate differences in the RPDI and normalized profit indices , using Agent 1 as reference point. Boxplots summarize these results for 20 independent runs, capturing variability across combinations.

Main Findings The experimental results for the Logit Bertrand competition show that learning rate variations significantly affect pricing strategies and profitability. Figure 2 demonstrates that agents with higher adjust pricing strategies more aggressively and often outperform competitors. For instance, when Agent 0’s is much higher than Agent 1’s (e.g., in 0.5_0.05 and 0.5_0.01 combinations), Agent 0 sets lower prices, capturing more market share. Agents with aggressive pricing strategies frequently achieve higher profitability, especially with significant learning rate disparities. In the 0.5_0.01 combination, for example, Agent 0’s profit surpasses Agent 1’s by a wide margin. Faster adaptation enables Agent 0 to leverage lower prices for sustained profitability. This trend persists across combinations, showing that faster-learning agents dominate by setting lower prices and achieving higher profit margins.

When learning rates are similar, pricing and profitability differences diminish. For example, in the 0.5_0.1 combination, similar learning rates produce minimal differences,

reflecting a balanced competitive environment. Accordingly, similar learning rates encourage convergence in strategies and outcomes, fostering fairer competition.

In the Standard Bertrand and Edgeworth Bertrand models, results align with these trends. As shown in Appendix A, agents with higher learning rates adopt lower pricing strategies in both models. However, this effect is less pronounced compared to the Logit Bertrand model. Pricing and profitability differences exhibit greater volatility in the Edgeworth Bertrand model due to its dynamic nature. Nevertheless, agents with higher learning rates consistently achieve higher profitability, particularly in cases with significant disparities (e.g., 0.5_0.01 and 0.1_0.01).

Implications These findings highlight critical considerations for companies using TQL as a pricing algorithm. Higher learning rates allow companies to adapt quickly to market dynamics, gaining advantages in pricing agility and profitability. However, these advantages create structural biases that disadvantage companies with lower learning rates, regardless of other strategic capabilities. Companies face challenges in mitigating these biases due to TQL’s reliance on fixed learning rates. This rigidity creates risks of volatile market outcomes when firms compete with optimized learning rates. Over time, such imbalances may destabilize markets, enabling high-learning-rate firms to dominate by undercutting competitors, reducing market diversity, and fostering monopolistic behavior. These biases make TQL unsuitable for companies seeking equitable and stable market positions.

Insight 1. Higher learning rates in TQL lead to aggressive pricing, giving faster-learning agents significant advantages in achieving lower prices and higher profits, particularly in scenarios with large learning rate disparities. This creates structural biases favoring faster-learning agents and risks destabilizing the market, making TQL unsuitable for fair competition.

6.2 Pricing behavior of Identical RL Agents

Previous works claim that agents employing identical strategies often exhibit predictable pricing behaviors, which can increase the likelihood of collusion (Ezrachi & Stucke 2017a, Beneke & Mackenrodt 2019).

A real-world manifestation of this phenomenon can be observed in hub-and-spoke scenarios, where multiple firms utilize similar algorithmic pricing tools provided by third-party platforms. For example, many sellers on Amazon and eBay adopt third-party pricing software instead of developing their own (Chen et al. 2016). Likewise, online travel agencies (OTAs) such as Expedia and Booking.com provide hotels with algorithmic pricing solutions (Wang et al. 2023).

To explore this hypothesis, we analyze interactions between two homogeneous RL agents. Homogeneous agents share identical algorithmic parameters and training configurations, operate in the same market environment, and follow identical training protocols. Despite these shared settings, each agent updates its strategies independently, with learning trajectories diverging due to variations in data sampling paths. This setup reflects real-world scenarios where competing firms use standardized pricing software configurations.

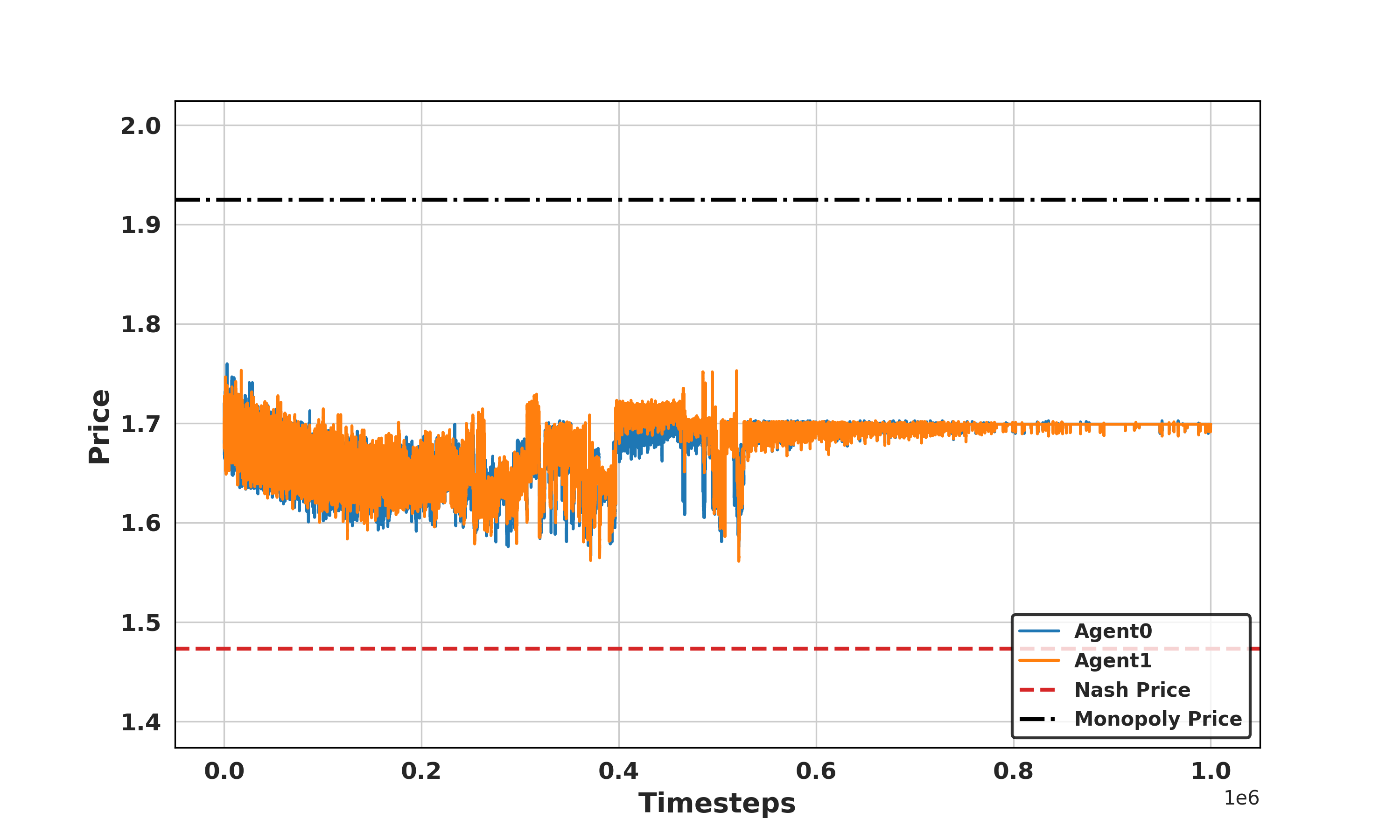

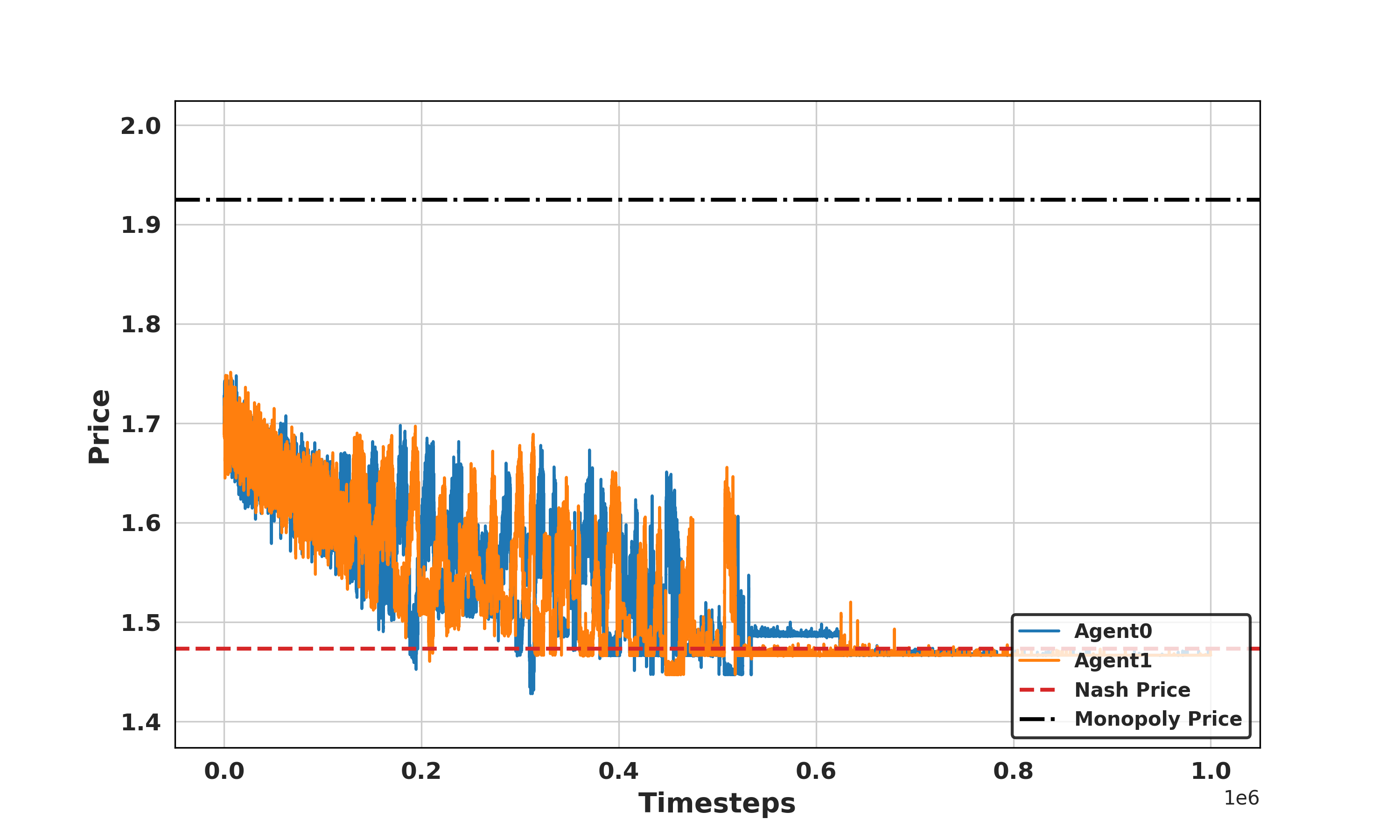

Specifically, we perform experiments with two homogeneous TQL agents to establish a baseline, even though earlier results suggest TQL offers limited advantages compared to DRL. This baseline allows us to quantify the performance of identical TQL agents and compare it with DRL algorithms. Simulations with DRL agents run for 100,000 timesteps due to their faster convergence in dynamic environments. TQL agents interact over 1,000,000 timesteps to achieve stable pricing strategies. We conduct each experiment over 20 independent random seeds to ensure robust and reproducible results.

Main Findings In the Logit Bertrand model, pricing behaviors differ significantly across DQN, PPO, and TQL agents, as shown in Figure 3(a).

PPO agents tightly cluster their pricing distributions around the Nash price, demonstrating strong competitiveness and minimal dispersion. Similarly, DQN agents primarily select prices near the Nash price, with symmetric distributions reflecting coordinated and fair competition. In contrast, TQL agents exhibit broader and more asymmetric price distributions, with some prices approaching the Nash price but many skewing toward higher levels near monopoly pricing. These results highlight TQL’s tendency to favor high-price strategies without achieving pricing consistency.

Normalized profit values , as shown in Figure4(a), further emphasize these trends. DQN agents achieve values centered around 0.1, reflecting stable pricing near Nash equilibrium. PPO agents maintain values near 0, indicating negligible collusion and strong competitiveness. By contrast, TQL agents achieve significantly higher values around 0.6, with greater variability, indicating higher profits but reduced stability.

In the Standard and Edgeworth Bertrand models, DQN and PPO agents show more dispersed pricing behaviors, as depicted in Figure 3(b) and Figure 3(c), though their prices still cluster around the Nash price. This dispersion reflects reduced pricing stability in these environments compared to Logit Bertrand. TQL agents, in contrast, display concentrated pricing distributions near monopoly prices, with lower variability, highlighting their consistent preference for high-price strategies.

Figure 4 show results across the models. In the Standard and Edgeworth Bertrand models, DQN agents achieve values around 0.3, reflecting a higher tendency toward supra-competitive pricing compared to Logit Bertrand. PPO agents maintain values near 0 in the Standard model and around 0.34 in the Edgeworth model, demonstrating strong competitive behavior and stability. TQL agents achieve values near 0.5 in both models, slightly lower than their 0.6 in Logit Bertrand, suggesting marginally reduced collusion and variability.

Implications These findings highlight the adaptability of DRL agents, which consistently converge to competitive pricing strategies near the Nash price, especially in the Logit Bertrand model. However, DRL agents show reduced pricing stability in the Standard and Edgeworth Bertrand models, with greater dispersion in their pricing strategies. In contrast, TQL agents maintain consistent high-price strategies across all models, favoring collusion but sacrificing stability and competitiveness.

Insight 3. Homogeneous DRL agents (DQN, PPO) adapt their strategies across demand models, showing strong competitiveness near Nash price in Logit Bertrand but reduced stability in Standard and Edgeworth Bertrand. TQL agents consistently favor pricing strategies close to the monopoly price and hence benefit collusion.

6.3 Comparing DRL and TQL in Competitive Pricing

While traditional research on algorithmic pricing has primarily focused on TQL, recent studies increasingly consider advanced DRL algorithms such as DQN and PPO. Against this background, this section evaluates DRL algorithms in a competitive pricing environment to determine whether they outperform TQL in achieving superior pricing strategies and profitability.

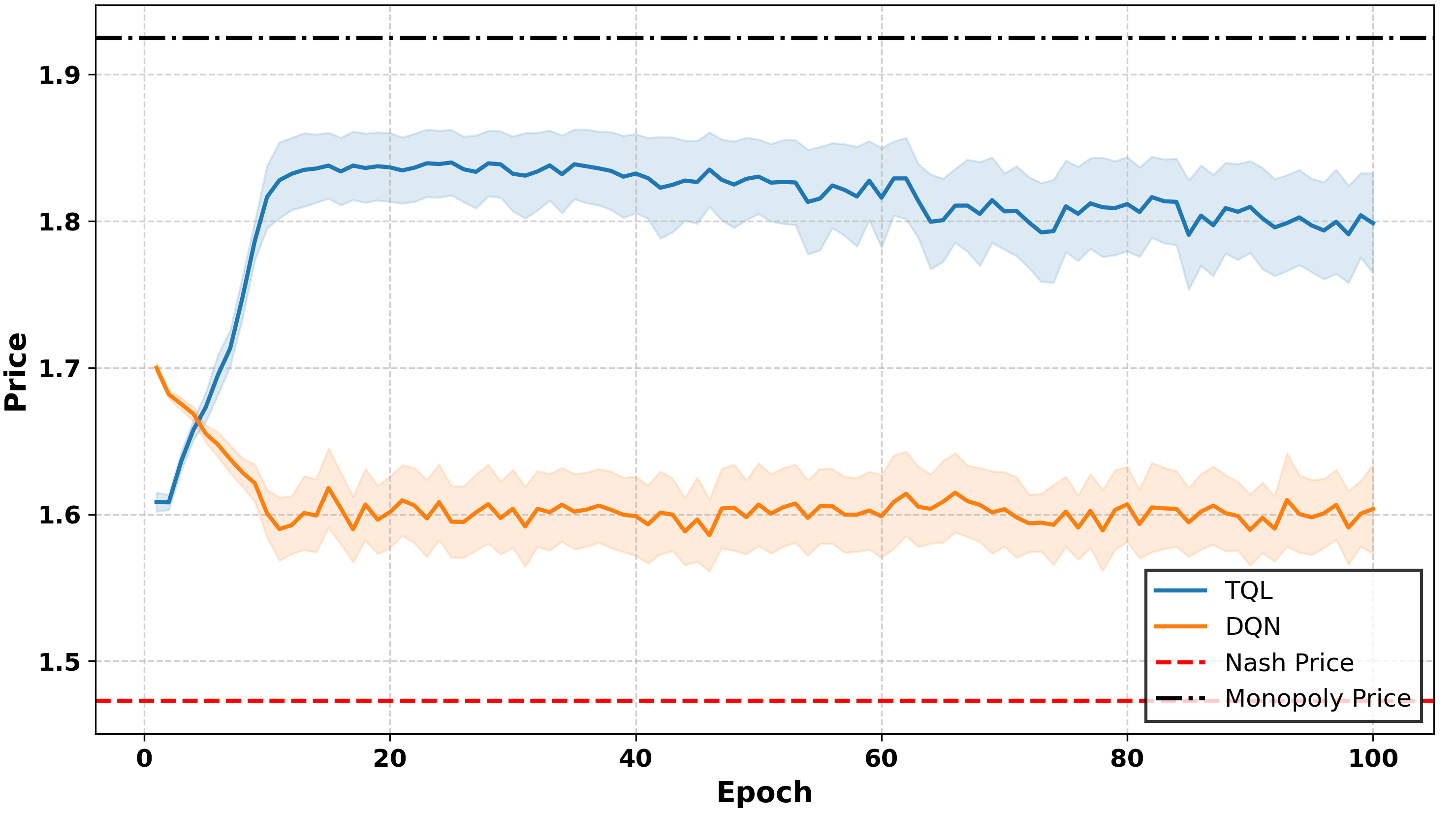

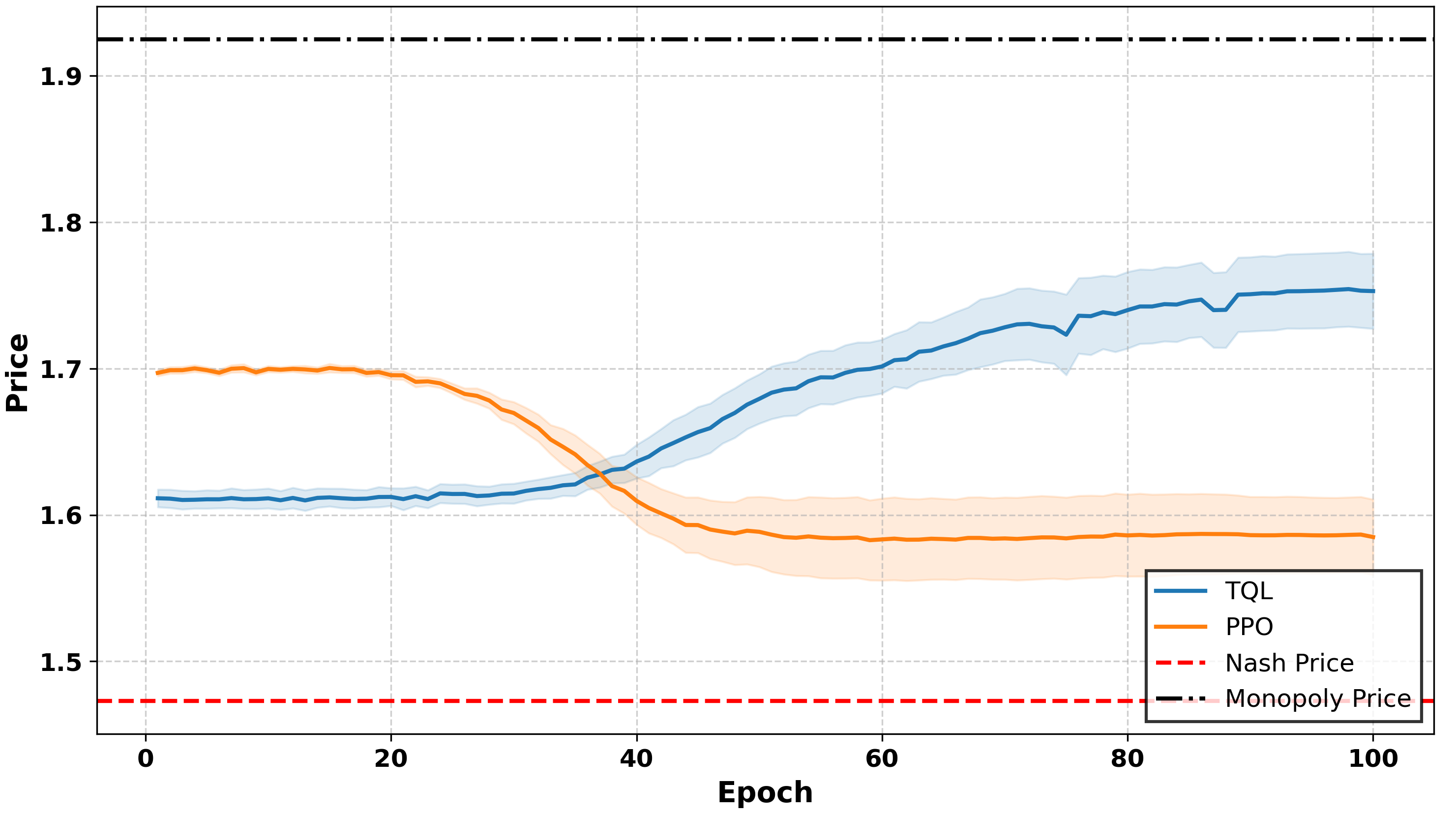

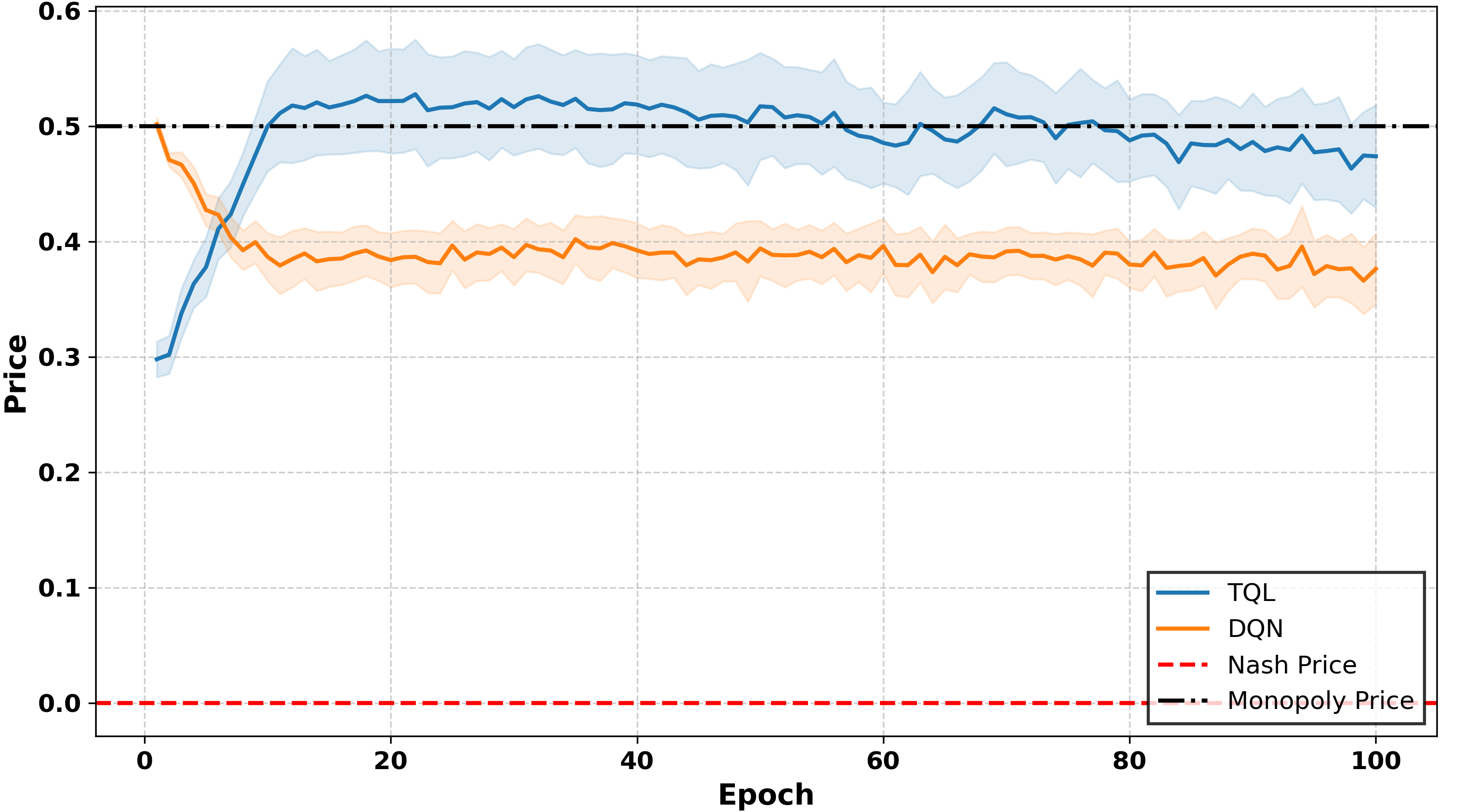

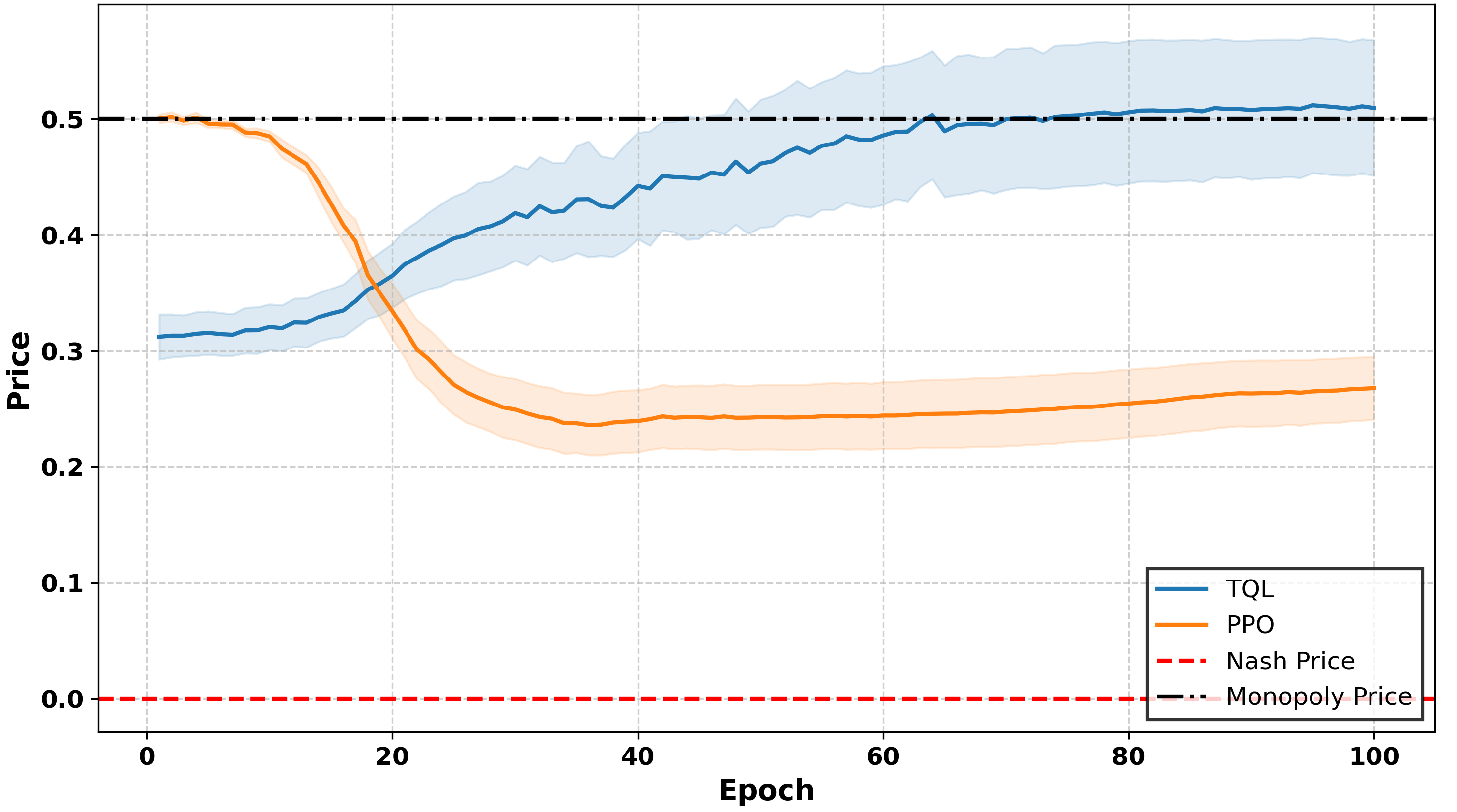

To ensure a fair comparison, the TQL agent is pretrained before interacting with a DRL competitor. This design choice accounts for fundamental differences in how these algorithms learn: TQL updates its strategy at every timestep from the start, whereas DQN first collects data for its replay buffer before batch learning. As a result, their learning rhythms are inherently misaligned, and once DQN begins updating, it benefits from using more data per step. Furthermore, our setup reflects a realistic market dynamic where an incumbent firm relies on a well-established TQL-based strategy, while a newcomer leverages DRL to adapt dynamically and compete effectively. Specifically, we simulate a duopoly where one firm employs a pretrained TQL strategy, and the other adopts a dynamically learning DRL algorithm (DQN or PPO). The TQL strategy, pretrained over 1,000,000 timesteps with two homogeneous agents, converges to a stable pricing strategy. During interactions, TQL operates without further updates, ensuring a consistent baseline. The interaction phase spans 100,000 timesteps, divided into 100 epochs of 1,000 timesteps each. DRL agents start without prior knowledge and adapt their strategies based on TQL’s behavior. Results include price trajectories for TQL vs. PPO and TQL vs. DQN, along with normalized profit distributions over the final 10,000 timesteps.

Main Findings In the Logit Bertrand setting, TQL’s prices remain stable, clustering around 1.8 for TQL vs. DQN (Figure 5(a)) and 1.75 for TQL vs. PPO (Figure 5(b)). These prices align closely with the monopoly price, reflecting TQL’s preference for high-price strategies. In contrast, DQN and PPO gradually reduce their prices, stabilizing around a price of 1.6. DQN exhibits minimal fluctuations by the end, showcasing a learned competitive low-price strategy. PPO, while initially volatile, converges to a similarly aggressive low-price strategy. Both DRL algorithms demonstrate superior adaptability by consistently underpricing TQL. The profit differences further highlight DRL’s advantages. Figure 6 shows that DQN and PPO achieve values predominantly above 1.0, reflecting stable and higher profitability compared to TQL, whose values cluster around 0 with high variability.

The results in the Standard Bertrand and Edgeworth Bertrand models, shown in Appendix A, confirm these observations: in the Standard Bertrand model, TQL again consistently maintains a high-price strategy near the monopoly price. Contrarily, DQN and PPO converge to competitive low-price strategies, achieving superior profitability.

The Edgeworth Bertrand model

exhibits slightly higher volatility in pricing and profit trends, but DRL algorithms still outperform TQL, further demonstrating their robustness across different market conditions.

Implications These results highlight the limitations of TQL, stemming from its static nature and inability to dynamically adapt to competitors’ strategies. By contrast, DRL algorithms excel in dynamic environments, learning competitive strategies that result in lower prices and higher profitability. The consistent performance of DQN and PPO across different Bertrand models underscores their adaptability and effectiveness in automated pricing.

For practitioners, our findings emphasize the importance of transitioning from traditional TQL to advanced DRL techniques to achieve competitive pricing. The DRL algorithm’s ability to outperform TQL in both pricing and profit stability demonstrates its practicality for modern markets.

Insight 2. The studied DRL algorithms (DQN, PPO) consistently outperform TQL by converging to lower prices and achieving higher, more stable profits. This highlights the superior adaptability of DRL methods over TQL, making them better suited to achieve competitive pricing.

6.4 Pricing behavior of heterogeneous DRL Agents

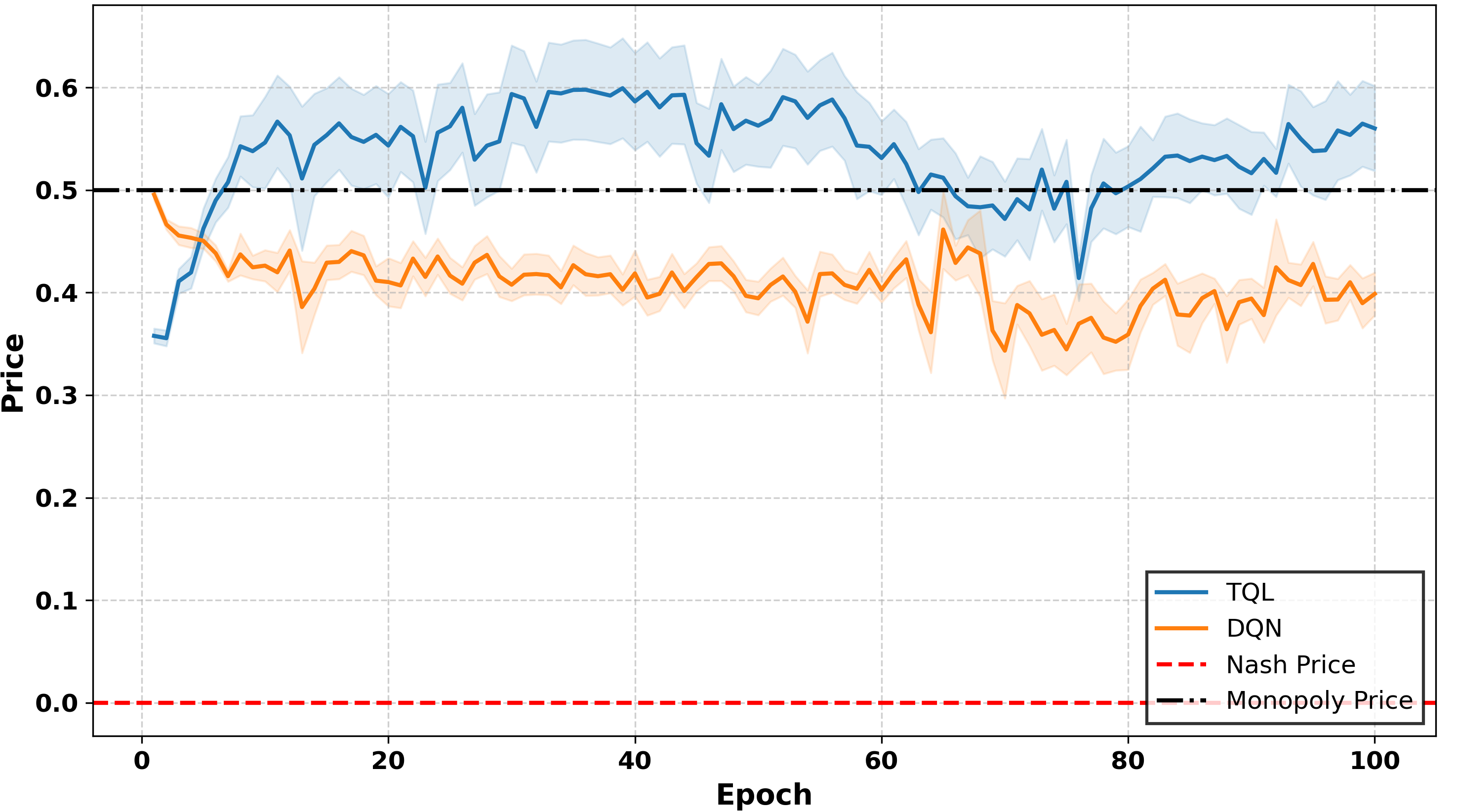

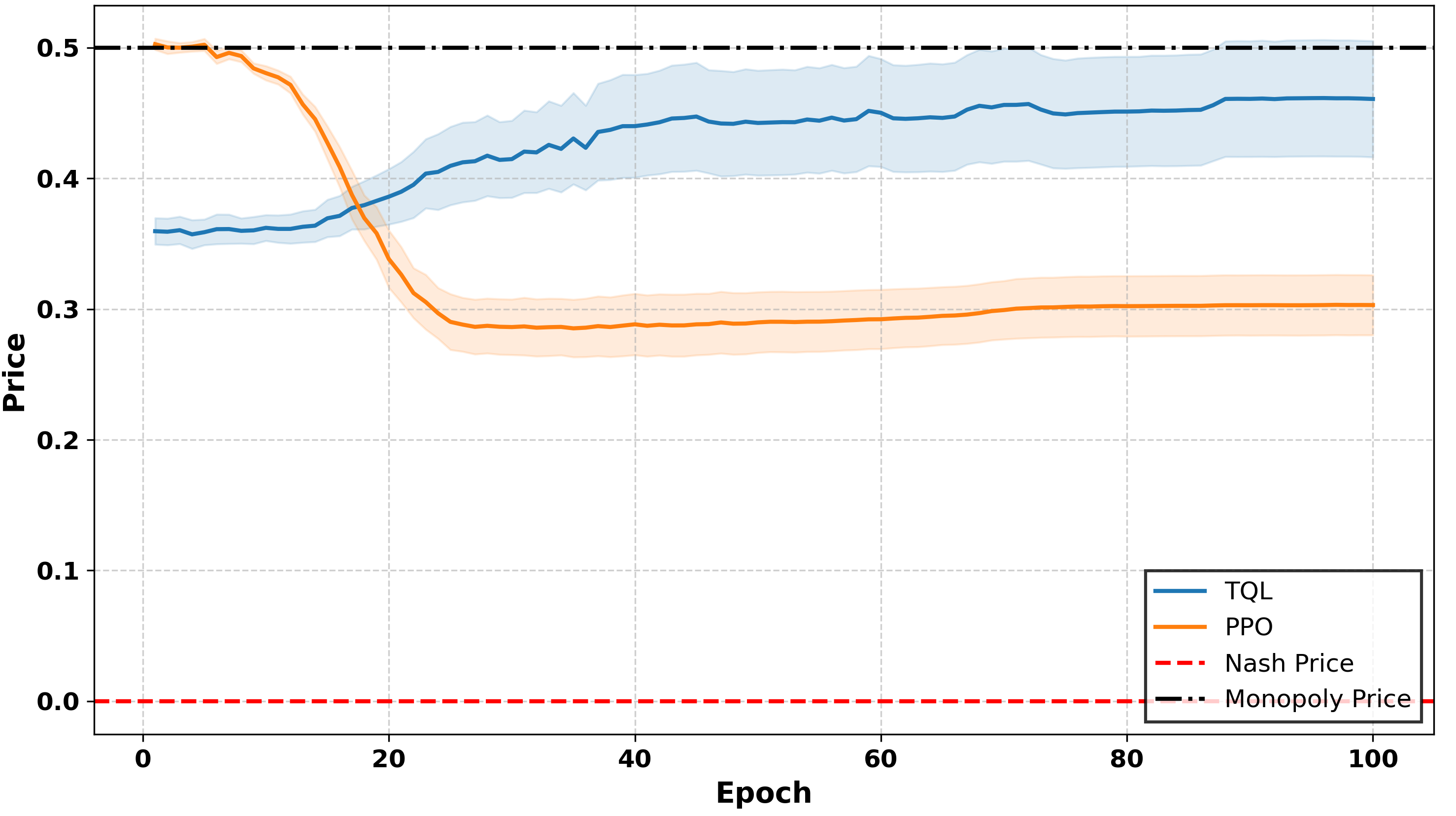

Understanding how different DRL algorithms interact in competitive markets provides valuable insights into their strategic adaptability and market influence. Against this background, we analyze interactions between two heterogeneous agents: one using DQN and the other employing PPO, within the Bertrand competition model. By studying algorithmic diversity, we assess its impact on pricing strategies, profitability, and competitive dynamics.

Specifically, our experiment features two parallel market environments, each designed to focus on a specific algorithm’s learning process. In the DQN environment, Agent 0 employs PPO, while Agent 1 uses DQN. In the PPO environment, Agent 0 uses PPO, and Agent 1 adopts DQN. Policy weights are exchanged every 1,000 timesteps between the two environments to enhance adaptability. For example, updated PPO policy weights from the PPO environment transfer to Agent 0 in the DQN environment, while DQN weights from the DQN environment transfer to Agent 1 in the PPO environment. This exchange allows agents to integrate complementary strategies learned in the alternate environment.

One comment on this experimental design is in order. We intentionally separate the learning of DQN and PPO into independent environments to avoid conflicts arising from their distinct learning mechanisms. DQN, as an off-policy algorithm, performs frequent updates via experience replay, enabling continuous strategy refinement. PPO, an on-policy algorithm, requires complete trajectory collection for updates, leading to less frequent but larger adjustments. Mixing the algorithms in a single environment could disrupt PPO’s stability due to DQN’s frequent updates. This setup replicates real-world market conditions, where companies adapt their algorithms gradually based on long-term strategies rather than immediate competitor reactions.

Main Findings In the PPO environment, as shown in Figure 7(a), the PPO agent stabilizes near the Nash price, adopting a competitive low-price strategy. Meanwhile, the DQN agent gradually increases its price toward the monopoly price. Figure 7(b) reveals that PPO achieves profits near the monopoly level, while DQN’s profits decrease and stabilize near the Nash level.

In the DQN environment (Figure 8), both agents converge to similar mean prices, but PPO exhibits more stable pricing. Initially, DQN achieves slightly higher profits, but PPO matches this performance in later iterations while maintaining lower variance.

Results in the Standard and Edgeworth Bertrand models, presented in Appendix A, align with Logit Bertrand findings, with some variations. In the PPO environment, PPO consistently adopts a low-price strategy, stabilizing around 0.4 and achieving profits near the monopoly level. DQN, by contrast, converges to higher prices and lower profits near the Nash level. In the DQN environment, DQN stabilizes at slightly lower prices than PPO in the Standard Bertrand model, achieving higher profits. This role reversal highlights the influence of the learning environment on competitive dynamics. In the Edgeworth Bertrand model, the profit gap between PPO and DQN narrows significantly, showing overlapping profit curves. Increased market complexity in the Edgeworth Bertrand model diminishes algorithmic performance differences, fostering more balanced competition.

Implications These results demonstrate PPO’s consistent advantage in adopting competitive low-price strategies and achieving higher profits across most scenarios. DQN, while less consistent, shows environment-specific strengths, particularly in the DQN environment within the Standard Bertrand model. The narrowing profit gap in the Edgeworth Bertrand model suggests that greater market complexity reduces algorithmic differences, creating more balanced competitive outcomes. These findings highlight the need to consider market dynamics when deploying DRL algorithms in real-world settings.

Insight 4. Across the three Bertrand demand models, PPO consistently adopts lower pricing strategies and achieves higher profits, while DQN’s performance varies by environment. In more dynamic settings like the Edgeworth Bertrand model, the profit gap between the two algorithms narrows, reflecting the impact of market complexity on their competitiveness.

6.5 Impact of State-Space Design on RL Pricing Strategies

In the following, we analyze how state-space definitions affect homogeneous RL agents, specifically TQL, DQN, and PPO. While DQN and PPO exhibit minimal differences compared to the complete information setting, TQL is more sensitive to state definitions. Therefore, this subsection focuses on how state-space design influences TQL’s convergence behavior, particularly regarding the availability of opponent information.

State-space design plays a crucial role in pricing strategies. In a complete information setting, each agent’s state at time includes a finite memory of past pricing decisions over steps, capturing both its own and its opponent’s historical prices. Formally,

where denotes the memory length, yielding a state-space dimensionality of . This setting reflects a scenario where agents have full awareness of market dynamics.

However, in real-world competitive environments, access to competitor pricing data is often restricted. To model such conditions, we define a limited information setting, where each agent observes only its own past prices:

Here, the state space reduces to a dimensionality of , limiting the agent’s ability to infer competitor strategies. Comparing these two settings allows us to assess how information richness affects learning dynamics and competitive behavior.

We evaluate three memory lengths () under both complete and limited information settings, yielding six unique configurations. Each configuration involves two homogeneous TQL agents interacting over 1,000,000 timesteps per run, with results averaged over 20 random seeds. To assess long-term behavior, we focus on the final 10,000 timesteps, analyzing RPDI and , specifically the normalized price and normalized profit. This setup enables a systematic evaluation of how state-space definitions influence learning and market dynamics.

Main Findings For the Logit Bertrand model, Figures 9 reveal distinct pricing and profit behaviors across state-space definitions. When agents observe both their own and opponent pricing histories (, , ), normalized prices decrease as memory length increases. However, despite this decline, prices remain above Nash equilibrium, indicating supra-competitive behavior.

Conversely, when agents rely solely on self-observed pricing histories (, , ), prices increase with memory length. Notably, under shorter memory settings ( and ), prices converge near Nash equilibrium, suggesting that limited information leads to more competitive pricing strategies (see Figure 10).

These trends hold across alternative Bertrand models (Standard and Edgeworth), with minor variations (See Appendix A). The consistency across different pricing models reinforces the generalizability of these findings.

Implications The results indicate that the availability of opponent information plays a crucial role in shaping pricing behavior among homogeneous TQL agents. When agents can observe both their own and their opponent’s past prices, supra-competitive pricing persists, though it gradually declines with increasing memory length.

In contrast,

when agents rely solely on their own pricing history, they tend to adopt more competitive strategies, with prices converging near the Nash equilibrium.

Insight 5. When TQL agents have access to opponent pricing information, prices decrease with memory length but remain above Nash equilibrium, sustaining supra-competitive behavior. Without opponent information, prices increase with memory but tend to converge near Nash equilibrium for shorter memory lengths. This suggests that richer state definitions can sustain higher, less competitive prices, while limited-information settings encourage more competitive pricing strategies.

6.6 Discussion

In the following, we analyze the factors driving differences in pricing behavior among the RL algorithms studied. Specifically, we address two key questions: (1) why DRL algorithms, particularly DQN and PPO, resist collusion compared to the more collusion-prone TQL; and (2) why PPO consistently achieves lower prices than DQN under similar competitive conditions.

Collusion Propensity: TQL vs. DRL TQL fosters collusion due to strong temporal correlations in its learning process, which enable it to identify and stabilize high-profit focal points. Since TQL updates its Q-values immediately after each experience, it quickly recognizes strategies leading to supra-competitive pricing. When states and actions remain relatively unchanged, the non-stationarity in learning decreases, allowing the algorithm to maintain these high-price strategies over time. This characteristic makes TQL prone to tacit collusion in price competition, as firms can repeatedly adjust strategies without explicit coordination.

In contrast, DRL algorithms, such as DQN and PPO, are less susceptible to collusion due to their more dynamic training mechanisms. DQN utilizes experience replay, where updates are applied to randomly sampled experiences rather than immediate observations. This process disrupts temporal correlations, making it difficult to stabilize collusive pricing. Similarly, PPO updates its strategy incrementally and avoids rapid convergence to high-price strategies. While PPO does not introduce as much randomness as DQN, its update mechanism still prevents the rapid locking of high-price strategies, promoting continuous adaptation.

Additionally, non-stationarity in multi-agent learning environments further limits collusion in DRL. Unlike TQL, which relies on consistent pricing patterns, DRL algorithms prioritize adapting to evolving competitor strategies rather than settling on fixed price agreements. Since deep neural networks update policies using randomly sampled past experiences, their ability to establish supra-competitive pricing strategies is restricted. The continuous disruption of temporal correlations between states prevents DRL from stabilizing on collusive pricing strategies, making competitive behavior more prevalent in multi-agent pricing environments.

In summary, TQL encourages collusion through strong temporal correlation and immediate updates, while DRL algorithms, with their dynamic learning mechanisms and exploratory behaviors, maintain a competitive equilibrium and reduce collusion tendencies.

Pricing Strategies: Why PPO Undercuts DQN In Bertrand competition, PPO tends to set lower prices than DQN, ultimately achieving higher profits. This outcome stems from differences in the algorithms’ learning mechanisms and convergence properties.

Policy gradient methods, such as PPO, naturally favor competitive pricing. Although multi-agent policy gradient convergence remains an open research question, prior studies (Hambly et al. 2023, Shi & Zhang 2020) suggest that such methods can reach Nash equilibria under certain conditions. This theoretical foundation supports PPO’s ability to converge toward aggressive pricing strategies in competitive markets.

In contrast, DQN, an off-policy algorithm relies on -greedy exploration and experience replay. This approach limits DQN’s ability to fully explore the strategy space, increasing the risk of overfitting to local optima such as supra-competitive pricing. Unlike PPO, which continuously refines its policy via gradient updates, DQN may fail to adequately explore lower-pricing strategies due to its reliance on past experiences, leading to higher price outcomes in some scenarios.

Moreover, PPO incorporates policy clipping, which prevents overly large updates and ensures stable learning. This stability allows PPO to steadily refine its pricing strategy without abrupt fluctuations. In contrast, DQN, which relies on experience replay, may suffer from outdated experiences, causing convergence instability and occasional strategy oscillation. These factors make it harder for DQN to consistently achieve the lower-price strategies found by PPO.

Thus, PPO’s robust policy optimization and efficient exploration enable it to identify more competitive pricing strategies, while DQN’s reliance on past experiences and limited exploration can lead to higher pricing levels. These differences highlight PPO’s advantage in competitive pricing environments, reinforcing its ability to achieve lower prices compared to DQN.

7 Conclusion

This study contributes to the growing discourse on algorithmic pricing by examining the competitive and collusive behavior of different RL algorithms in oligopolistic markets. Through extensive simulations based on Bertrand competition models, we compare the pricing behaviors of TQL, DQN, and PPO, offering a nuanced perspective on the risks of algorithmic collusion.

Our findings reveal critical distinctions between traditional and DRL methods. TQL consistently exhibits a strong tendency for supra-competitive pricing, with agents learning to sustain collusion when provided with opponent information. Moreover, variations in learning rates within TQL agents lead to an inherent asymmetry, as faster-learning agents systematically achieve higher profits. In contrast, DRL agents–particularly PPO and DQN–demonstrate more competitive behavior, consistently stabilizing at lower price levels closer to the Nash equilibrium. Notably, when pre-trained TQL agents compete against DRL agents, the latter quickly dominate, reinforcing the advantages of deep learning-based pricing strategies. Furthermore, when heterogeneous DRL agents interact, we observe a further reduction in collusive outcomes, highlighting the role of algorithmic diversity in fostering competition.

These results have significant implications for businesses, regulators, and researchers. From a business perspective, the findings underscore the importance of selecting the right algorithmic pricing strategies, as DRL-based methods yield more competitive and stable outcomes. For regulators, our work suggests that fostering diversity in pricing algorithms may serve as a natural countermeasure against tacit collusion, potentially informing future antitrust policies.

For future research, several promising research directions emerge. First, future studies could explore more complex market structures, including multi-product competition and multi-agent reinforcement learning (MARL) frameworks with dynamic entry and exit of firms. Second, investigating how algorithmic pricing strategies evolve under different regulatory interventions–such as pricing caps or transparency mandates–would provide further insights into policy implications. Finally, studying the sensitivity and dynamics of learning-based pricing strategies with respect to varying demand elasiticity models and preference heterogeneity remains an open question, warranting empirical validation through field experiments or real-world data.

Acknowledgements

This work was funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) - Projektnummer 277991500.

Declaration of generative AI and AI-assisted technologies in the writing process

During the preparation of this work the author(s) used ChatGPT4o in order to improve the paper’s writing style and grammar. After using this tool, the authors reviewed and edited the content as needed and take full responsibility for the content of the publication.

References

- Abada & Lambin (2023) Abada, I., & Lambin, X. (2023). Artificial intelligence: Can seemingly collusive outcomes be avoided? Management Science, .

- Abada et al. (2024) Abada, I., Lambin, X., & Tchakarov, N. (2024). Collusion by mistake: Does algorithmic sophistication drive supra-competitive profits? European Journal of Operational Research, .

- Agrawal et al. (2019) Agrawal, A., Gans, J., & Goldfarb, A. (2019). The economics of artificial intelligence: an agenda. University of Chicago Press.

- Asker et al. (2022) Asker, J., Fershtman, C., & Pakes, A. (2022). Artificial intelligence, algorithm design, and pricing. In AEA Papers and Proceedings (pp. 452–56). volume 112.

- Assad et al. (2020) Assad, S., Clark, R., Ershov, D., & Xu, L. (2020). Algorithmic pricing and competition: Empirical evidence from the german retail gasoline market, .

- Azzutti et al. (2021) Azzutti, A., Ringe, W.-G., & Stiehl, H. S. (2021). Machine learning, market manipulation, and collusion on capital markets: Why the" black box" matters. U. Pa. J. Int’l L., 43, 79.

- Beneke & Mackenrodt (2019) Beneke, F., & Mackenrodt, M.-O. (2019). Artificial intelligence and collusion. IIC-international review of intellectual property and competition law, 50, 109–134.

- Berner et al. (2019) Berner, C., Brockman, G., Chan, B., Cheung, V., Dębiak, P., Dennison, C., Farhi, D., Fischer, Q., Hashme, S., Hesse, C. et al. (2019). Dota 2 with large scale deep reinforcement learning. arXiv preprint arXiv:1912.06680, .

- Bertrand (1883) Bertrand, J. (1883). Review of “theorie mathematique de la richesse sociale” and of “recherches sur les principles mathematiques de la theorie des richesses.”. Journal de savants, 67, 499.

- Bichler et al. (2024) Bichler, M., Durmann, J., & Oberlechner, M. (2024). Online optimization algorithms in repeated price competition: Equilibrium learning and algorithmic collusion. arXiv preprint arXiv:2412.15707, .

- Brero et al. (2022) Brero, G., Mibuari, E., Lepore, N., & Parkes, D. C. (2022). Learning to mitigate ai collusion on economic platforms. Advances in Neural Information Processing Systems, 35, 37892–37904.

- Brown & MacKay (2021) Brown, Z. Y., & MacKay, A. (2021). Competition in pricing algorithms. Technical Report National Bureau of Economic Research.

- Buckmann et al. (2021) Buckmann, M., Haldane, A., & Hüser, A.-C. (2021). Comparing minds and machines: implications for financial stability. Oxford Review of Economic Policy, 37, 479–508.

- Calvano et al. (2020) Calvano, E., Calzolari, G., Denicolo, V., & Pastorello, S. (2020). Artificial intelligence, algorithmic pricing, and collusion. American Economic Review, 110, 3267–3297.

- Capobianco & Gonzaga (2020) Capobianco, A., & Gonzaga, P. (2020). Competition challenges of big data: Algorithmic collusion, personalised pricing and privacy. In Legal Challenges of Big Data (pp. 46–63). Edward Elgar Publishing.

- Chen et al. (2021) Chen, C., Yao, F., Mo, D., Zhu, J., & Chen, X. M. (2021). Spatial-temporal pricing for ride-sourcing platform with reinforcement learning. Transportation Research Part C: Emerging Technologies, 130, 103272.

- Chen et al. (2016) Chen, L., Mislove, A., & Wilson, C. (2016). An empirical analysis of algorithmic pricing on amazon marketplace. In Proceedings of the 25th international conference on World Wide Web (pp. 1339–1349).

- Constantine & Quitaz (2018) Constantine, S., & Quitaz, V. (2018). Oecd competition committee best practice roundtable–algorithms and collusion: United kingdom submission. Competition Law Journal, 17, 41–48.

- Dolgopolov (2022) Dolgopolov, A. (2022). Reinforcement learning in a prisoner’s dilemma. Available at SSRN 4240842, .

- Edgeworth (1925) Edgeworth, F. Y. (1925). Papers relating to political economy volume 2. Royal Economic Society by Macmillan and Company, limited.

- Epivent & Lambin (2022) Epivent, A., & Lambin, X. (2022). On algorithmic collusion and reward-punishment schemes. Available at SSRN 4227229, .

- Ezrachi & Stucke (2017a) Ezrachi, A., & Stucke, M. E. (2017a). Artificial intelligence & collusion: When computers inhibit competition. U. Ill. L. Rev., (p. 1775).

- Ezrachi & Stucke (2017b) Ezrachi, A., & Stucke, M. E. (2017b). Two artificial neural networks meet in an online hub and change the future (of competition, market dynamics and society), .

- Friedrich et al. (2024) Friedrich, P., PĂĄsztor, B., & Ramponi, G. (2024). Learning collusion in episodic, inventory-constrained markets. arXiv preprint arXiv:2410.18871, .

- Hambly et al. (2023) Hambly, B., Xu, R., & Yang, H. (2023). Policy gradient methods find the nash equilibrium in n-player general-sum linear-quadratic games. Journal of Machine Learning Research, 24, 1–56.

- Harrington (2018) Harrington, J. E. (2018). Developing competition law for collusion by autonomous artificial agents. Journal of Competition Law & Economics, 14, 331–363.

- Kastius & Schlosser (2022) Kastius, A., & Schlosser, R. (2022). Dynamic pricing under competition using reinforcement learning. Journal of Revenue and Pricing Management, 21, 50–63.

- Kephart & Tesauro (2000) Kephart, J. O., & Tesauro, G. (2000). Pseudo-convergent q-learning by competitive pricebots. In Proceedings of the Seventeenth International Conference on Machine Learning (pp. 463–470).

- Kim et al. (2015) Kim, B.-G., Zhang, Y., Van Der Schaar, M., & Lee, J.-W. (2015). Dynamic pricing and energy consumption scheduling with reinforcement learning. IEEE Transactions on smart grid, 7, 2187–2198.

- Klein (2021) Klein, T. (2021). Autonomous algorithmic collusion: Q-learning under sequential pricing. The RAND Journal of Economics, 52, 538–558.

- Kutschinski et al. (2003) Kutschinski, E., Uthmann, T., & Polani, D. (2003). Learning competitive pricing strategies by multi-agent reinforcement learning. Journal of Economic Dynamics and Control, 27, 2207–2218.

- Levitan & Shubik (1972) Levitan, R., & Shubik, M. (1972). Price duopoly and capacity constraints. International Economic Review, (pp. 111–122).

- Liu et al. (2019) Liu, J., Zhang, Y., Wang, X., Deng, Y., & Wu, X. (2019). Dynamic pricing on e-commerce platform with deep reinforcement learning: A field experiment. arXiv preprint arXiv:1912.02572, .

- Mehra (2015) Mehra, S. K. (2015). Antitrust and the robo-seller: Competition in the time of algorithms. Minn. L. Rev., 100, 1323.

- Meylahn & V. den Boer (2022) Meylahn, J. M., & V. den Boer, A. (2022). Learning to collude in a pricing duopoly. Manufacturing & Service Operations Management, 24, 2577–2594.

- Mnih et al. (2015) Mnih, V., Kavukcuoglu, K., Silver, D., Rusu, A. A., Veness, J., Bellemare, M. G., Graves, A., Riedmiller, M., Fidjeland, A. K., Ostrovski, G. et al. (2015). Human-level control through deep reinforcement learning. nature, 518, 529–533.

- OECD (2017) OECD (2017). Algorithms and collusion: competition policy in the digital age. OECD, .

- Qiu et al. (2020) Qiu, D., Ye, Y., Papadaskalopoulos, D., & Strbac, G. (2020). A deep reinforcement learning method for pricing electric vehicles with discrete charging levels. IEEE Transactions on Industry Applications, 56, 5901–5912.

- Rana & Oliveira (2014) Rana, R., & Oliveira, F. S. (2014). Real-time dynamic pricing in a non-stationary environment using model-free reinforcement learning. Omega, 47, 116–126.

- Sanchez-Cartas & Katsamakas (2022) Sanchez-Cartas, J. M., & Katsamakas, E. (2022). Artificial intelligence, algorithmic competition and market structures. IEEE Access, 10, 10575–10584.

- Schlechtinger et al. (2023) Schlechtinger, M., Kosack, D., Paulheim, H., Fetzer, T., & Krause, F. (2023). The price of algorithmic pricing: Investigating collusion in a market simulation with ai agents. In AAMAS (pp. 2748–2750).

- Schulman et al. (2017) Schulman, J., Wolski, F., Dhariwal, P., Radford, A., & Klimov, O. (2017). Proximal policy optimization algorithms. arXiv preprint arXiv:1707.06347, .

- Shi & Zhang (2020) Shi, Y., & Zhang, B. (2020). Multi-agent reinforcement learning in cournot games. In 2020 59th IEEE Conference on Decision and Control (CDC) (pp. 3561–3566). IEEE.

- Varian (2018) Varian, H. R. (2018). Artificial intelligence, economics, and industrial organization volume 24839. National Bureau of Economic Research Cambridge, MA, USA:.

- Wang et al. (2023) Wang, Q., Huang, Y., Singh, P. V., & Srinivasan, K. (2023). Algorithms, artificial intelligence and simple rule based pricing. Available at SSRN 4144905, .

- Watkins (1989) Watkins, C. J. C. H. (1989). Learning from delayed rewards, .

- Werner (2023) Werner, T. (2023). Algorithmic and human collusion. Available at SSRN 3960738, .

- Yan et al. (2022) Yan, L., Chen, X., Chen, Y., & Wen, J. (2022). A hierarchical deep reinforcement learning-based community energy trading scheme for a neighborhood of smart households. IEEE Transactions on Smart Grid, 13, 4747–4758.

- Ye et al. (2019) Ye, Y., Qiu, D., Sun, M., Papadaskalopoulos, D., & Strbac, G. (2019). Deep reinforcement learning for strategic bidding in electricity markets. IEEE Transactions on Smart Grid, 11, 1343–1355.

Appendix A Supplementary results

A.1 Learning Rate-Induced Market Imbalances in Tabular Q-Learning

In both the Standard Bertrand and Edgeworth Bertrand models, the observed results align with these established trends. As illustrated in Figures 11 and 12, agents with higher learning rates tend to adopt lower pricing strategies. However, this effect is less pronounced compared to the Logit Bertrand model. The Edgeworth Bertrand model exhibits greater volatility in pricing and profitability differences due to its inherently dynamic nature. Despite this, agents with higher learning rates consistently attain greater profitability, particularly in scenarios with substantial learning rate disparities (e.g., 0.5_0.01 and 0.1_0.01).

A.2 DRL vs TQL: Superior Pricing Strategies

The experimental results from the Standard Bertrand and Edgeworth Bertrand models (Figures 13 -16) further support the main findings from the Logit Bertrand model. In the Standard Bertrand model, TQL consistently adopts high-price strategies near the monopoly price, while DQN and PPO converge to more competitive low-price strategies, achieving higher and more stable profits. In the Edgeworth Bertrand model, pricing dynamics are less smooth, but final price and profit distributions are more stable. DRL algorithms still outperform TQL, demonstrating robustness across different market conditions.

A.3 Heterogeneous DRL Interaction

Figures 17-18 in the Standard Bertrand model show that, PPO consistently adopts a low-price strategy in the PPO environment, stabilizing near 0.4 and achieving profits close to the monopoly level. Meanwhile, DQN converges to higher prices with profits near the Nash level. In the DQN environment, PPO still sets slightly lower prices and earns slightly higher profits than DQN, suggesting that the learned strategies remain consistent across environments.

Figures 19-20 in the Edgeworth Bertrand model show that, increased market complexity narrows the profit gap between the two algorithms. In the PPO environment, PPO maintains its low-price strategy with higher profits. However, in the DQN environment, the profit curves of DQN and PPO overlap, reflecting more balanced competition in this model.

A.4 Impact of State Definitions on TQL Agent Behavior

In the Standard Bertrand model (Figure 21), when state definitions exclude opponent information (e.g., ), pricing remains competitive and stabilizes near the Nash price. As memory length increases (e.g., and ), prices gradually rise, reflecting higher pricing strategies. Conversely, when state definitions include complete opponent information (e.g., , , ), greater state information leads to lower prices, highlighting the influence of memory length on pricing behavior.

In the Edgeworth Bertrand model (Figure 22), under complete opponent information (e.g., , , ), increasing memory length leads to lower prices and lower profits. In contrast, under limited information (self_k1, self_k2, self_k3), this trend is less pronounced.

Appendix A Pseudocodes of Algorithms Selection

This section introduces the RL algorithms used in our experiments, including TQL, DQN, and PPO. We briefly overview their algorithmic steps, highlighting their advantages and applicability in complex decision-making.

A.1 TQL