A Deep Learning Framework for Medium-Term Covariance Forecasting in Multi-Asset Portfolios††thanks: This work was carried out within the scope of the research project funded by Fundação para a Ciência e a Tecnologia, grant number 2023.01070.BD.

Abstract

Accurate covariance forecasting is central to portfolio allocation, risk management, and asset pricing, yet many existing methods struggle at medium-term horizons, where shifting market regimes and slower dynamics predominate. We propose a deep learning framework that combines three-dimensional convolutional neural networks, bidirectional long short-term memory layers, and multi-head attention to capture complex spatio-temporal dependencies. Using daily data on 14 exchange-traded funds from 2017 through 2023, we find that our model reduces Euclidean and Frobenius distance metrics by up to 20% relative to classical benchmarks (e.g., shrinkage and GARCH approaches) and remains robust across distinct market regimes. Our portfolio experiments demonstrate significant economic value through lower volatility and moderate turnover. These findings highlight the potential of advanced deep learning architectures to improve medium-term covariance forecasts, offering practical benefits for institutional investors and risk managers.

Keywords: Covariance Matrix Forecasting, Deep Learning, Portfolio Optimisation, Medium-Term Horizons, Financial Markets.

JEL codes: C45, G11, G17.

1 Introduction

Covariance matrix estimation is central in modern finance. It influences portfolio construction, risk management, and asset pricing models. Markowitz, (1952) introduced mean-variance optimisation, highlighting how correlation among assets shapes the risk-return trade-off. Beyond portfolio choice, covariance estimation underpins factor-based models, hedging strategies, and even debates on market efficiency, where accurate correlation forecasts can drive risk control and potential outperformance.

Early studies found that even simple correlation structures could improve capital allocation. For instance, Elton and Gruber, (1973) suggested using constant-correlation estimates over historical windows for a decade. Their work showed that stable or slowly changing correlation patterns can help avoid distortions caused by transient market fluctuations.

Over time, multiple research strands have focused on short-horizon covariance forecasts. High-frequency datasets, such as intraday prices, enable detailed volatility analyses, often using generalised autoregressive conditional heteroskedasticity (GARCH) based models. Constant (Bollerslev,, 1990) and dynamic conditional correlation (Engle,, 2002) specifications remain common benchmarks, although Symitsi et al., (2018) argue that little fundamental progress has been made recently. Extensions include applying the heterogeneous autoregressive model (Corsi,, 2009) in a multivariate setting through Cholesky decomposition111Cholesky decomposition is a method that breaks down a positive definite matrix into the product of a lower triangular matrix and its transpose. (Chiriac and Voev,, 2011). However, the Cholesky decomposition models outperform DRD-based222Dynamic Relationship/Dependence (DRD) models refer to time-varying models that separate covariance into volatility and correlation components forecasts. (Bollerslev et al.,, 2018).

However, GARCH-type approaches struggle with large cross-sections, falling prey to the curse of dimensionality (Robert F. Engle and Wolf,, 2019). Tools like principal component analysis and random matrix theory (Ledoit and Wolf,, 2003; Laloux et al.,, 2000) have been effective for large datasets. Recent advances, such as dynamic conditional correlation with nonlinear shrinkage (Robert F. Engle and Wolf,, 2019), perform well overall, as per De Nard et al., (2024). Still, most of these methods focus on very short-term horizons, often just one step ahead or one day ahead, and rely on high-frequency data.

Long-horizon forecasts matter for institutional investors like pension funds and endowments, which rebalance portfolios over weeks or months. Moreover, high-frequency data are not always public or cost-effective, making the short-horizon focus less relevant for these institutions. Furthermore, slow-moving trends, such as equity–bond correlation shifts, can be overlooked if one relies solely on high-frequency econometric models. Sandoval and Franca, (2012) highlights how regime shifts or significant structural changes often go undetected in classical specifications, raising the risk of large drawdowns and poor capital allocation.

For longer-term horizons, naive, shrinkage, and factor models are more common (Ledoit and Wolf,, 2004; De Nard et al.,, 2022). Naive approaches assume that recent covariance estimates strongly predict future covariances as they follow a Markov process. At the same time, shrinkage techniques blend the sample covariance matrix with structured targets to reduce noise, particularly when the cross-section of assets is large (Ledoit and Wolf,, 2022). Factor models can provide more insight but may not generalise well across diverse portfolios, especially when markets are affected by many different factors. These methods are typically stable but can underperform when major shifts occur.

In recent years, there has been a surge in machine learning methods that can handle non-linearities and high dimensionality. Gu et al., (2020) and Kim et al., (2023) use techniques like random forests, support vector machines, and generative adversarial networks, while Zhang et al., (2024) applies graph neural networks to capture volatility spillovers for covariance matrix forecast. However, most of these solutions still emphasise short-term horizons.

Attention mechanisms (Vaswani et al.,, 2017) offer a promising direction by weighting key observations more heavily. Some studies apply these techniques in finance but still focus on short-horizon tasks (Nazareth and Ramana Reddy,, 2023; Olorunnimbe and Viktor,, 2023). In principle, attention-based models could capture the slow-moving, cyclical factors and abrupt shifts that define medium- and long-horizon covariance forecasts, realising this potential. However, it requires integrating sophisticated data-driven architectures with the economic logic of excess returns.

Recent efforts to extend these approaches to multi-asset portfolios have been limited. While many studies handle large cross-sections of stocks or focus on single-asset classes such as equities (Reis et al.,, 2024), fewer examine the combined dynamics across multiple asset classes in an integrated framework. However, institutional investors routinely diversify across equities, bonds, alternatives, and derivatives, underscoring the need for robust, multi-asset covariance forecasting models. In particular, capturing time-varying cross-asset correlations over medium-term horizons is a non-trivial challenge that remains under-explored in much of the existing literature.

Two key research gaps remain. First, most existing studies focus on short- or long-term horizons, leaving a relative void in medium-term covariance forecasting. This gap is particularly salient for multi-asset portfolios, where cross-asset correlations over multi-week or multi-month windows can significantly influence asset allocation and risk management (De Nard et al.,, 2021). Second, there is limited empirical evidence on whether using raw returns versus excess returns leads to systematically different covariance forecasts, especially over these medium-term horizons. Economic theory suggests that risk premiums and the underlying drivers of asset co-movements could be more accurately captured through excess returns. However, most machine learning and econometric approaches mostly default to raw returns.

Our study addresses these gaps by focusing on medium-term covariance forecasts in a multi-asset setting. Specifically, we propose a novel deep learning (DL) model that captures spatio-temporal correlations while remaining robust to structural changes. We benchmark against classical methods (naive, shrinkage, GARCH, and dimensional reduction) and demonstrate consistent gains in forecast accuracy under diverse market environments from 2017 to 2023. Our main contributions are as follows:

-

•

We present an integrated 3D-convolution neural network (CNN) and bidirectional long-short-term memory (LSTM) architecture with multi-head attention that improves medium-term forecasting accuracy.

-

•

We compare different return-processing specifications (including the treatment or omission of risk-free rates) and show that the proposed approach preserves its predictive edge.

-

•

We evaluate the economic value of our forecasts in a global minimum-variance (GMV) portfolio, demonstrating significant variance reduction and stable turnover.

2 Methodology

Let denote the -dimensional row vector of excess daily returns for assets at time . Assuming time-varying mean excess returns, can be expressed as follows:

| (1) |

where is the -dimensional vector of rolling means of the excess daily returns, and is the i.i.d. error terms with a normal distribution within each rolling window:

| (2) |

Although empirical evidence suggests financial returns often exhibit heavy tails and non-zero skewness (Cont,, 2001), we adopt the normality assumption because it is standard in many benchmark models (e.g., GARCH-based correlation models and Ledoit–Wolf shrinkage). However, we acknowledge that alternative distributions (e.g., Student- innovations, mixture models, or those explicitly modelling tail dependence) may better capture extreme events and skewness in practice333Extending our DL framework to accommodate such heavy-tailed or asymmetric distributions is an area for future research. Nevertheless, our empirical results in subsequent sections suggest that even a normality-based design can significantly enhance covariance forecasts, given the robustness of the data-driven layers in handling complex, nonlinear dependencies. (Hansen,, 1994; Harvey,, 1997).

The rolling mean and rolling standard deviation at time are calculated using a window of size as follows:

| (3) |

| (4) |

where denotes the element-wise product. Therefore, the realised covariance matrix () is an matrix with each element calculated as:

| (5) |

Our goal is to estimate the conditional covariance matrix of the asset returns for the next days based on the information available at time :

| (6) |

where is the sigma-algebra representing all the information available at time .

To estimate , we compare naive and other benchmark models found in the literature alongside our proposed model. A description of each model is shown below.

2.1 Naïve ()

A naive covariance forecasting approach is based on the lagged realised covariance. This model assumes that covariance is a Markov process, so the covariance matrix of the previous period is highly informative about the future covariance matrix. Under this model:

| (7) |

This forecasting method is as simple as possible as it requires no optimisation.

2.2 Naïve full sample()

Another naïve technique is to use the full sample instead of the rolling covariance matrix as our estimator.

| (8) |

where is the covariance matrix of our sample up until .

2.3 Exponential Weighted Moving Average ()

The EWMA employs exponentially decaying weights for the covariance matrix. The covariance matrix in the EWMA model is recursively computed as follows:

| (9) |

where is the N-dimensional vector of the error terms of all assets from Eq. (1), at time , and acts as a decay factor, confined within the range [0,1], dictating the rate at which the weights on past observations decrease. This factor has been approximated to be around 0.94 (J.P.Morgan,, 1996).

2.4 Ledoit and Wolf ()

The LW shrinkage (Ledoit and Wolf,, 2004) is a robust statistical model that combines the sample covariance matrix with a structured target matrix, improving estimation accuracy by reducing the impact of estimation error due to high dimensionality and limited sample size. The LW shrinkage estimator is given by:

| (10) |

where is the target matrix, with being the identity matrix and representing the sum of the diagonal elements of the sample covariance matrix. The shrinkage coefficient is optimally determined to minimise the mean squared error between the estimated and true covariance matrices:

| (11) |

where are the elements of the sample covariance matrix and are the elements of the target matrix .

2.5 Ledoit and Wolf full sample ()

Similarly to the model, we employed a full sample of Ledoit and Wolf, (2004) as a shrinkage model.

| (12) |

2.6 Constant Conditional Correlations ()

The model, introduced by Bollerslev, (1990), assumes that asset correlations remain constant over time while variances evolve dynamically according to a GARCH process based on a one-step forecast. However, since investment funds and risk managers typically rebalance portfolios over extended horizons, such as monthly or quarterly, a one-step forecast is insufficient for practical decision-making (De Nard et al.,, 2022).

To extend the model to a multi-step forecasting framework, we follow the methodology of Baillie and Bollerslev, (1992), defining the -step ahead conditional covariance forecast as:

| (13) |

where is the diagonal matrix of forecasted conditional volatilities for horizon and the conditional correlation matrix. The multi-step averaging approach used in Eq. (13) was introduced by De Nard et al., (2021) to provide a more stable covariance forecast over the rebalancing period. The series is modelled using univariate GARCH(1,1) processes:

| (14) |

where are the estimated GARCH parameters.

The conditional correlation matrix is assumed to be constant over time calculated through the standardised residuals, which are defined as:

| (15) |

where are the residuals of the return series, which are used to estimate the conditional correlation matrix.

2.7 Dynamic Conditional Correlations ()

The model of Engle, (2002) extends the model by allowing correlations to vary over time while retaining the GARCH framework for variances. This is achieved by replacing the constant correlation matrix in Eq. (13) with a dynamic correlation matrix .

To accommodate multi-step forecasting for practical portfolio management, we follow the methodology of Engle and Sheppard, (2001). The -step ahead conditional covariance forecast is:

| (16) |

where is defined as in Eq. (13), and is the -step ahead forecast of the dynamic conditional correlation matrix. The multi-step forecast for the correlation matrix is computed as follows:

| (17) |

where is the unconditional correlation matrix, and ensures stationarity. The parameters and control the persistence of the dynamic correlations.

The conditional correlation matrix evolves over time according to:

| (18) |

| (19) |

where ensures that remains a proper correlation matrix. The standardised residuals are defined as in Eq. (15), and is estimated from historical standardised residuals.

2.8 Nonlinear Shrinkage Dynamic Conditional Correlations ()

One recent extension is the model from De Nard et al., (2022). The covariance forecast in the model follows the same structure as in Eq. (16), but now with a shrinkage-improved correlation matrix (). They apply the nonlinear shrinkage method of Ledoit and Wolf, (2020), which optimally shrinks the eigenvalues of the sample covariance matrix towards a better-conditioned target matrix. This procedure ensures that the estimated correlation matrix remains positive, definite, and well-conditioned, even in high-dimensional settings.

Given a sample correlation matrix , the optimal nonlinear shrinkage estimator adjusts its eigenvalues as follows. Let have the eigendecomposition:

| (20) |

where is the matrix of eigenvectors and is the diagonal matrix of eigenvalues. The nonlinear shrinkage transformation replaces with a shrinkage-transformed version :

| (21) |

where the optimally shrunk eigenvalues are computed using the oracle nonlinear shrinkage function:

| (22) |

where is the sample spectral density estimator, is the Hilbert transform of the spectral density, and is the limiting concentration ratio of the covariance matrix.

The sample spectral density function is estimated using a kernel-based density estimator, ensuring uniform consistency. The Hilbert transform is computed using the principal value integral, which corrects for eigenvalue bias induced by sampling variability.

The shrunk correlation matrix () is then used as the input for the process in Eq. (18).

2.9 Principal Component Analysis ()

As noted by Ledoit and Wolf, (2003), empirical results show the usefulness of PCA in covariance matrix estimation. The PCA is computed as follows:

| (23) |

To ensure we capture most of the information, we retain only the first principal components that account for at least 95% of the total variance. This is mathematically expressed as:

| (24) |

The final forecasted covariance matrix is then approximated as:

| (25) |

2.10 Random Matrix Theory ()

(Laloux et al.,, 2000) is built upon the where the upper () and lower () bound of the eigenvalues are calculated using the Marchenko-Pastur distribution. These bounds are calculated as:

| (26) |

where is the ratio of the window size to the number of assets. Eigenvalues within these bounds are dominated by noise, while eigenvalues outside the bounds represent meaningful information.

| (27) |

This filtering process removes noise and retains only the significant components of the covariance matrix. The cleaned covariance matrix is reconstructed by multiplying the filtered eigenvalues with their corresponding eigenvectors:

| (28) |

2.11 CNN with A-BiLSTM ()

In our proposed model, each batch of input data is processed sequentially through all six stages, as described below.

2.11.1 Data Preprocessing

Let be the time series data, where each represents the rolling covariance matrix, normalised, of assets at time ).

It is essential to standardise the input features to facilitate efficient training and convergence of the model. This transformation ensures that each feature has zero mean and unit variance, which is crucial for stabilising the training dynamics of neural networks.

We transform the data into overlapping sequences using a rolling window approach to capture temporal dependencies. Specifically, for a given lookback period , the sequence creation process, at time , can be expressed as:

| (29) |

The input to the model consists of sequences of scaled covariance matrices. Formally, let denote the -th sequence.

2.11.2 3D Convolutional Layer

Next, each sequence of covariance matrices is processed through a three-dimensional layer (Lecun et al.,, 1998). We use a 3D CNN to capture local spatio-temporal features, given that each rolling covariance matrix is an () grid, and the temporal dimension arises from stacking these grids over time. The 3D CNN filters can identify how subsets of assets interact and evolve over multiple past windows, offering a more flexible approach than linear assumptions.

By applying a convolution operation with a kernel size of (), the same padding, and a stride equal to one, the CNN layer captures patterns within the data across different time steps and different dimensions of the covariance matrices. The transformation performed by the 3D convolutional layer on the input sequence of covariance matrices can be expressed as:

| (30) |

where is the kernel size of the 3D Convolution, determining the dimensions of the receptive field across the temporal and spatial axes. represents the kernel weights, a learnable parameter of size , where is the number of input channels, and is the number of output channels. The input covariance matrices are reshaped to include a single channel, so . Additionally, the model outputs a single channel, meaning . Consequently, the weight tensor simplifies to . is the input sequence of covariance matrices reshaped to dimensions . The term denotes the bias added to the convolution result, which, with , is a single scalar, i.e., . The indices , , and iterate over all whole integers within the range , centered around , to compute local features. Finally, zero-padding is applied to ensure that the output dimensions match the input dimensions, preserving the temporal and spatial resolution of the covariance matrices.

Subsequently, the convolutional output is flattened () to transition from spatial to feature dimensions suitable for the LSTM layer. This reshaping consolidates the covariance matrices into -dimensional feature vectors for each time step within the sequence.

2.11.3 Bidirectional LSTM (BiLSTM) Layer

Following the CNN, the flattened transformed sequences are fed into a layer configured with layers and hidden dimension. To understand the BiLSTM, it is essential first to grasp the fundamentals of a standard LSTM network (Hochreiter,, 1997). Appendix A.1 provides more detailed information on how each LSTM cell works.

The BiLSTM enhances the standard LSTM by adding another layer that processes the input sequence in the reverse order. This bidirectional approach allows the model to have both forward and backward information about the sequence, making it more effective in capturing the context from past and future data points. Each sequence goes through layers, i.e. the output of layer one serves as input for layer 2.

In our model, the BiLSTM first transforms the input sequence of dimension into an output sequence of dimension . The BiLSTM uses learnable parameters to map the features at each time step into a lower-dimensional hidden representation of size . This transformation is achieved through linear transformations, where weights and biases are optimised during training. Then, the hidden states from both forward and backward pass across all layers, and time steps are concatenated to form a comprehensive hidden state matrix. This matrix captures information from all directions and spans the entire sequence of inputs. Each BiLSTM layer can be expressed as:

| (31) |

where represents the BiLSTM layer, for , and each for is defined as:

| (32) |

The hidden dimension for each LSTM direction, denoted as , results in a concatenated hidden state dimension of at each time step.

The traditional BiLSTM outputs the last time step of the last layer. However, in our model, we use a similar approach to Liu and Guo, (2019) methodology, meaning all time steps from the last layer () are used as an input to our following steps. To mitigate overfitting and enhance the model’s generalisation capabilities, a Dropout Layer is applied to the BiLSTM output. This operation randomly zeroes a fraction of the elements in with a probability of 20%, effectively regularising the model by preventing reliance on specific neurons during training. During our testing phase, this feature will be skipped.

2.11.4 Multi-Head Self-Attention Layer

Our next step is to apply a multi-head attention mechanism (Vaswani et al.,, 2017) to each hidden state of the last layer. The multi-head attention mechanism to refine the temporal dependencies captured in the sequence. For attention heads, the input is used to compute the queries (), keys (), and values (): , , and , where are learnable parameters. The attention weights for each head are computed as follows:

| (33) |

where scales the dot product to stabilise gradients and splits the features. Each head processes its respective portion of the features, which are concatenated to produce . The concatenated output is projected back to using a linear transformation.

The attention output is mean-pooled along the sequence dimension to condense the temporal information into a fixed-length representation:

| (34) |

where is the -th row of . This averaged context vector encapsulates the overall information from the entire sequence. We then pass through a fully connected layer to map it back to the covariance matrix space:

This averaged context vector encapsulates the overall information from the entire sequence. We then pass through a fully connected layer to map it back to the covariance matrix space:

| (35) |

where and are receptively the weight matrix and bias vector of the fully connected layer.

Because our pipeline stacks 3D Convolution, BiLSTM, and attention in succession, the final latent representation becomes highly abstract, making interpretability at each layer difficult. Consequently, we do not attempt to interpret the hidden states or attention weights in a domain sense.

2.11.5 Enforcing Symmetry and Positive Semi-Definiteness

The output vector is reshaped into a square matrix () to form the predicted covariance matrix.

The output matrix may not necessarily be symmetric, a key property of covariance matrices. To enforce symmetry, we average the matrix with its transpose:

| (36) |

Then, we rescale the normalised output back to the original scale of the data, using the reverse process of Section 2.11.1 resulting in .

Symmetry alone does not guarantee that is positive semi-definite, which is another requisite property of covariance matrices. To ensure positive semi-definiteness, we perform eigenvalue decomposition:

| (37) |

We then modify by setting all negative eigenvalues to zero:

| (38) |

The positive semi-definite matrix is reconstructed as:

| (39) |

2.11.6 Shrinkage

While DL-based forecasts can learn intricate patterns, historical covariance may still convey valuable stability and continuity, particularly when the model is tested on data different from training. Therefore, our model’s final step is incorporating a linear shrinkage from historical values in our predictions.

| (40) |

where CAB is the final matrix output, and is the shrinkage factor.

2.12 Evaluation metrics

We will use performance metrics consistent with previous literature (Symitsi et al.,, 2018; Bollerslev et al.,, 2018; Zhang et al.,, 2024) to check the models’ performance. We consider the following loss functions to measure the average distance between predicted covariances and realised covariances matrices for the model comparisons:

| (41) |

| (42) |

where represents the Euclidean distance between the dimensional vectorised version of the upper triangular of forecast covariances and ex-post realised covariances. is the Frobenius distance between the two matrices, and is the trace of a square matrix. All these functions measure losses. Therefore, lower values are preferred.

3 Empirical Results

We obtain our sample data from the Refinitiv Database, covering daily adjusted closing prices of 14 major ETFs that reflect equity and bond markets across diverse global sectors. These ETFs were selected to construct a multi-asset environment that includes equity sectors (e.g. technology, financials, industrials, consumer staples) and fixed-income exposures. Table 1 details the ETF’s information. To compute excess returns, we also retrieve from the Federal Reserve Economic Data the 1-month U.S. Treasury yield, treating it as a daily risk-free rate. Our sample runs from 1 January 2017 to 31 December 2023, totalling 1,760 trading days.

| Name | Ticker | ISIN | Asset Class |

|---|---|---|---|

| iShares Global Tech ETF | IXN | US4642872919 | Equity |

| iShares Global Financials ETF | IXG | US4642873339 | Equity |

| iShares Global Consumer Discretionary ETF | RXI | US4642887453 | Equity |

| iShares Global Industrials ETF | EXI | US4642887297 | Equity |

| iShares Global Healthcare ETF | IXJ | US4642873255 | Equity |

| iShares Global Consumer Staples ETF | KXI | US4642887370 | Equity |

| iShares U.S. Real Estate ETF | IYR | US4642877397 | Real Estate |

| iShares International Developed Real Estate ETF | IFGL | US4642884898 | Real Estate |

| iShares Global Materials ETF | MXI | US4642886950 | Equity |

| iShares Global Energy ETF | IXC | US4642873412 | Equity |

| iShares Global Comm Services ETF | IXP | US4642872752 | Equity |

| iShares Global Utilities ETF | JXI | US4642887115 | Equity |

| iShares Core U.S. Aggregate Bond ETF | AGG | US4642872265 | Fixed Income |

| iShares Core International Aggregate Bond ETF | IAGG | US46435G6724 | Fixed Income |

We split our dataset into a training period from 1 January 2017 to 31 December 2020 and a testing period covering 1 January 2021 to 31 December 2023. The testing sample thus comprises 753 trading days, encompassing a wide range of economic and market conditions. We identify three distinct market regimes within this testing window to examine whether our model responds robustly to varying interest-rate and equity-market environments. We designate the interval between 1 January 2021 and 2 January 2022 as the First Bull Period (Bull-1), typified by low yields on the risk-free asset and a generally stable equity market. We label the interval from 3 January 2022 to 12 June 2022 as the Bear Period (Bear), characterised by a steady rise in the risk-free rate and a drop of 20% or more in the S&P 500 from its last peak. Lastly, we classify the interval from 13 June 2022 to 31 December 2023 as the Second Bull Period (Bull-2), featuring persistently high interest rates but a renewed upswing in equity prices. This subdivision ensures that our out-of-sample evaluations capture both low- and high-rate market phases and a bear-market regime, offering a comprehensive test of the model’s ability to adapt to evolving financial landscapes.

During the training period, we minimise the Frobenius distance (Eq. 42) to select hyperparameters. We use Optuna (Akiba et al.,, 2019) for hyperparameter selection. Appendix A.2 shows the grid search table. Specifically, we split the training dataset into a model-fitting subset (80%) and a validation subset (20%) to identify optimal settings under a forecast horizon () of 20 days. We adopt the Adam optimiser over 100 epochs, using a batch size of 128 and a learning rate of . For the neural-network-based model, we use a lookback window () of 100 days. We set the 3D convolution kernel size () to five; the BiLSTM has 128 hidden dimensions () across seven stacked layers (), and the multi-head attention uses 16 heads (). Finally, we apply a shrinkage factor of 0.8 () when combining the DL output with the most recent historical covariance.

We conduct a rolling estimation procedure to simulate live conditions. Each new trading day in the test set triggers an online update of our DL model, incorporating all data up through day . This design ensures that the forecasts mimic a real-world trading environment, where only up-to-date historical data is available at each decision point.

Table 2 reports the average Euclidean () and Frobenius () distances between forecasted and realised covariance matrices for all models over the entire testing period (2021–2023)444Bold and underlined numbers represent the lowest and the second lowest values, respectively.. GARCH models ( and ) and perform relatively well as they adapt faster to structural changes in the covariance matrices. However, our model () yields the lowest errors in both metrics, outperforming classical benchmarks. Dimensional reduction models perform inadequately as we only use 14 assets.

| 53.526 | 82.020 | |

| 52.713 | 80.987 | |

| 49.111 | 75.349 | |

| 49.772 | 76.514 | |

| 68.136 | 103.363 | |

| 48.568 | 75.198 | |

| 48.268 | 74.716 | |

| 51.621 | 79.079 | |

| 54.348 | 83.154 | |

| 54.145 | 82.915 | |

| 38.312 | 58.923 |

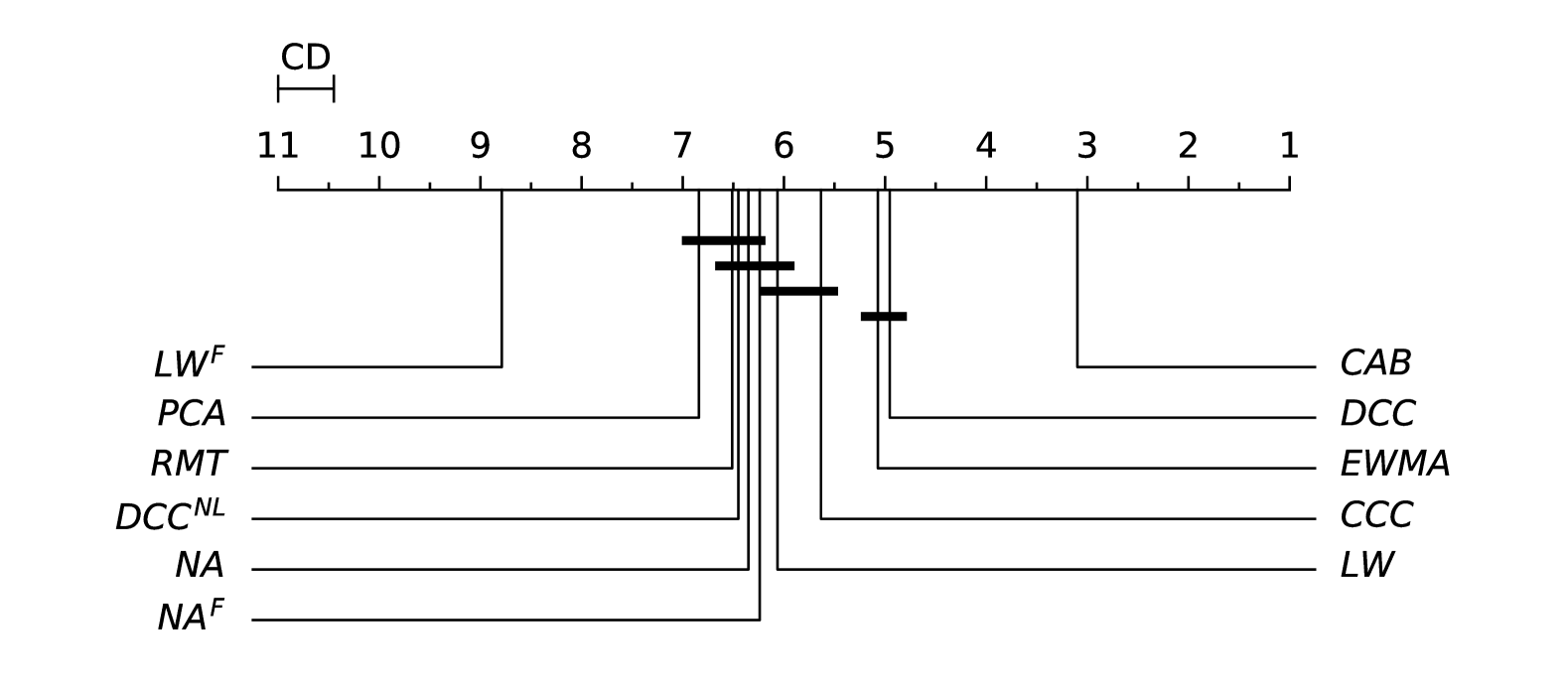

To solidify our findings, we analysed the 10 models with 753 paired samples for the Euclidean and Frobenius distances following Demsar, (2006) frequentist methodology. The significance level is for all tests here forward. We rejected the null hypothesis that the population is normal for all the populations ( for all models in both distances). Therefore, we assume that not all populations are normal.

Because we have more than two populations and the populations are not normal, we use the non-parametric Friedman test as an omnibus test to determine if there are any significant differences between the median values of the populations. We use the post-hoc Nemenyi test to infer which differences are significant. Differences between populations are significant if the difference in the mean rank is greater than the critical distance CD=0.494 of the Nemenyi test.

We reject the Friedman test’s null hypothesis, which states that there is no difference in the central tendency of the populations. Therefore, we assume that there is a statistically significant difference between the central tendencies of the populations. Figure 1 shows the post-hoc Nemenyi test critical distance between groups. Our model reports statistically better results than the benchmark models.

Table 3 presents the average distance metrics for the testing period across three market regimes: Bull-1, Bear, and Bull-2. Overall, the model consistently outperforms all benchmarks.

| Bull-1 | Bear | Bull-2 | ||||||

|---|---|---|---|---|---|---|---|---|

| 36.937 | 56.621 | 89.891 | 137.868 | 53.709 | 82.252 | |||

| 35.680 | 54.992 | 98.002 | 150.780 | 50.586 | 77.545 | |||

| 31.754 | 48.973 | 82.799 | 126.614 | 50.574 | 77.549 | |||

| 34.126 | 52.599 | 90.441 | 138.173 | 48.089 | 74.088 | |||

| 63.288 | 94.759 | 93.189 | 143.636 | 63.989 | 97.222 | |||

| 31.688 | 49.784 | 88.106 | 134.902 | 48.017 | 74.316 | |||

| 33.516 | 52.166 | 84.745 | 130.345 | 47.227 | 73.161 | |||

| 36.779 | 56.449 | 87.650 | 134.167 | 50.767 | 77.734 | |||

| 37.424 | 57.281 | 90.720 | 139.116 | 54.747 | 83.660 | |||

| 37.246 | 57.083 | 90.638 | 138.821 | 54.493 | 83.411 | |||

| 24.276 | 37.643 | 66.381 | 102.252 | 39.253 | 60.126 | |||

While all models experience a decrease in accuracy during the turbulent Bear regime, the approach exhibits notable robustness. In particular, during the Bull-2 period, characterised by elevated interest rates and dynamic shifts in cross-asset relationships, integrating DL techniques with classical shrinkage enables to adapt effectively to changing market conditions, thereby maintaining lower distance metrics.

Supplementary Nemenyi post-hoc tests confirm that the performance improvements observed with are statistically significant. These tests provide further evidence that the model’s superior performance is not merely a result of sample-specific idiosyncrasies but reflects a robust ability to handle varying market regimes.

Moreover, these findings contribute to the literature on hybrid forecasting methods by demonstrating that blending modern DL with traditional econometric techniques can offer substantial gains in predictive accuracy, especially in periods of market stress. This robust performance under diverse macroeconomic conditions highlights the practical relevance of the approach for risk management and strategic asset allocation.

4 Robustness analysis

4.1 Impact of Using Raw Returns vs. Excess Returns

One potential criticism of our model is that it may be overly tailored to excess returns, even though some classic optimisation frameworks (Markowitz,, 1952) often use raw returns. We re-estimate our model without subtracting the risk-free rate to address this concern. All other model parameters remain identical to those described in Section 2, with the sole difference being that now represents the -dimensional row vector of raw daily returns for assets at time .

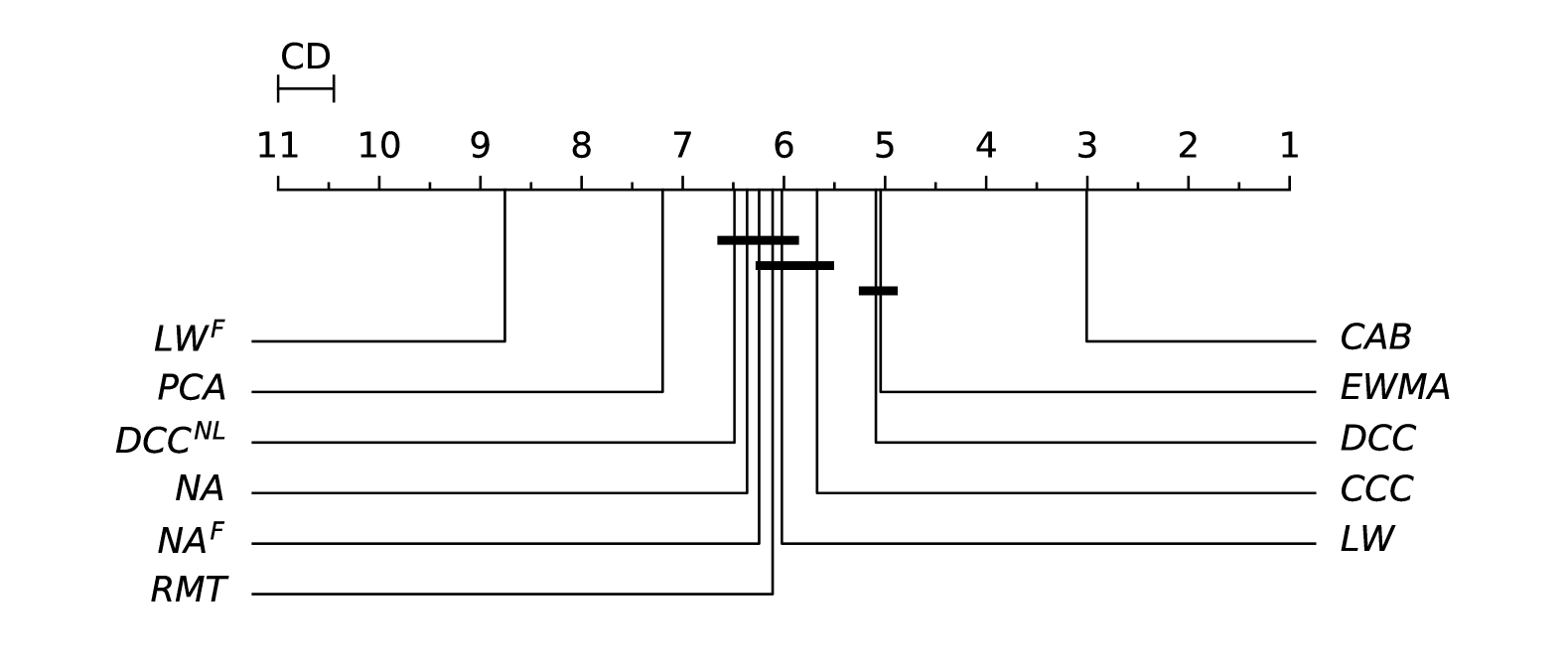

Table 4 reports the performance of the various models under these raw returns assumptions. Our approach () continues outperforming all benchmarks across the entire sample and within individual market regimes, with statistically significant results based on the same post-hoc Nemenyi criteria used earlier. This finding directly informs our second research question about whether raw vs. excess returns lead to materially different covariance forecasts. When comparing Table 4 (raw returns) to Tables 2 and 3 (excess returns), the numerical magnitudes change slightly, but the rank order remains the same: still produces the most accurate forecasts overall.

Our findings indicate that the advantage of our framework is not contingent on the choice between excess or raw returns, reaffirming its robustness to the presence or absence of the risk-free rate. Moreover, this consistency suggests that subtracting the risk-free rate over the medium-term horizon does not significantly alter the core structure of asset co-movements. Hence, even though economic theory posits that excess returns better capture risk premiums, our empirical results show that the forecasting edge of holds across both raw and excess return specifications. In other words, our method retains its superior performance even when modelling raw returns, suggesting that its effectiveness does not hinge on subtracting the risk-free rate.

| Overall | Bull-1 | Bear | Bull-2 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 53.525 | 82.020 | 36.936 | 56.620 | 89.895 | 137.875 | 53.707 | 82.249 | ||||

| 52.486 | 80.668 | 34.913 | 53.883 | 98.623 | 151.717 | 50.462 | 77.372 | ||||

| 49.174 | 75.441 | 31.753 | 48.972 | 82.798 | 126.613 | 50.697 | 77.730 | ||||

| 49.771 | 76.512 | 34.125 | 52.598 | 90.442 | 138.174 | 48.087 | 74.085 | ||||

| 68.130 | 103.353 | 63.273 | 94.736 | 93.190 | 143.636 | 63.985 | 97.217 | ||||

| 48.508 | 75.106 | 31.599 | 49.634 | 88.139 | 135.038 | 47.948 | 74.196 | ||||

| 48.232 | 74.661 | 33.445 | 52.045 | 84.884 | 130.630 | 47.161 | 73.050 | ||||

| 51.604 | 79.051 | 36.691 | 56.305 | 87.856 | 134.535 | 50.731 | 77.664 | ||||

| 54.348 | 83.153 | 37.423 | 57.280 | 90.724 | 139.123 | 54.745 | 83.657 | ||||

| 54.144 | 82.914 | 37.245 | 57.081 | 90.643 | 138.829 | 54.491 | 83.408 | ||||

| 36.663 | 56.518 | 22.807 | 35.673 | 62.036 | 96.406 | 38.273 | 58.441 | ||||

4.2 Varying Forecast Horizons

We also examine our model’s behaviour as the forecast horizon () varies. In the baseline analysis, days are medium-term, but many institutional investors face different time horizons for risk management or asset allocation decisions. In line with our first research question regarding underexplored medium-term horizons, we extend from 10 to 250 days, thus covering short, medium, and long horizons. To explore model performance across this range of settings, we evaluate both excess (Table LABEL:tab:diffhorizonsexc) and raw returns (Table LABEL:tab:diffhorizonsraw).

Table LABEL:tab:diffhorizonsexc shows that our model consistently achieves the lowest average distance metrics across most forecast horizons. remains among the top performers for shorter horizons (). However, it does not outperform GARCH-based models ( and ) and . These differences are not statistically different in the overall period, Bull-1 and Bull-2. During Bull-2, our model outperformed the benchmarks, and the results were statistically significant based on the post-hoc Nemenyi test.

For mid-term forecasting () for both distances, the differences are statistically significant in all periods. Thus, our model consistently outperforms the benchmarks. Please note that GARCH models tend to underperform as the forecast horizon increases, while full data models ( and ) tend to diminish forecasting errors. Please note, while the was more recently designed for high dimensional matrices, it provides more stable forecasts based on eigenvalues than the classical .

At the longest horizon (), again excels in most periods. Besides showing a large difference between distances during the Bear period and Bull-1, the post-hoc Nemenyi test shows no statistical difference between our model and and , respectively. These results suggest that more complex models capture slower-moving cross-asset dynamics effectively, while classical estimators remain competitive in certain regime-specific conditions. As anticipated, naive and shrinkage methods perform relatively well at the longer horizon. These patterns reinforce our first research question’s premise that medium-term horizons can benefit from sophisticated models and highlight instances where simpler approaches hold their own.

Turning to Table LABEL:tab:diffhorizonsraw, we link our findings to the second research question: whether using raw or excess returns makes a systematic difference. Results show that the top-performing models remain consistent across all forecast horizons.

Once again, tends to yield the strongest overall performance. Although it does not dominate at shorter horizons, it consistently ranks near the top, showing no statistical difference between our model and the top performers. All other differences are statistically significant. These results mirror the trends seen under excess returns, indicating that the performance edge of does not hinge on subtracting the risk-free rate. Therefore, our DL approach remains robust even if practitioners opt for raw returns, common in certain classical optimisation frameworks. Our model performs better than the benchmarks for longer horizons (). However, the results are not statistically different from the second-performing models ( and ) for the Bull-1 and Bear periods, respectively.

These findings indicate that DL-based models can adapt effectively across different forecast windows. Across both dimensions, shows a stable advantage, with only minor variations in extreme horizons.

5 Economic Value in Portfolio Management

Next, we investigate the economic importance of accurate covariance forecasts in a practical asset allocation framework. Specifically, we consider an investor allocating wealth among the ETFs specified in section 3, subject to a no-short-selling constraint. Such a constraint is common among regulated institutional investors (e.g., pension funds, mutual funds) that may face limits on leverage or short positions. We adopt daily, weekly, and monthly rebalancing intervals (Symitsi et al.,, 2018).

At each rebalancing date, the investor solves the GMV problem:

| (43) |

where is an vector of GMV portfolio weights, is the forecast covariance from each model, and is an vector of ones. Excluding expected returns from the optimisation allows us to isolate the impact of covariance forecasts (DeMiguel et al.,, 2009; Kourtis et al.,, 2012).

Using a rolling estimation window, we generate 11 portfolio strategies (one for each forecast model) plus an equally weighted (1/) benchmark. After estimating , we compute the GMV weights and hold them until the next rebalancing date. We then record the ex-post average portfolio return for each model () as:

| (44) |

where is an vector of realised asset returns, is the total out-of-sample length, and are the portfolio weights at the start of period for model .

We focus on two main metrics to compare forecast models: out-of-sample portfolio variance and turnover. The variance of daily returns by a portfolio constructed by model is:

| (45) |

where is the ex-post return of model in period , and is its mean and number of observations over the out-of-sample window. Meanwhile, the average turnover reflects how often the portfolio adjusts its weights:

| (46) |

where are the portfolio weights of model immediately before rebalancing at , and is the 1-norm. A higher turnover implies more frequent portfolio adjustments, potentially incurring greater trading costs (Kourtis,, 2014).

We also include an equally weighted (1/) portfolio, often cited for its simplicity and historically strong performance (DeMiguel et al.,, 2009). Although avoids estimation risk and typically maintains low turnover, it cannot adapt to shifting market correlations.

From Table 5, it is evident that the covariance forecasts provided by the model strike a competitive balance between risk reduction and turnover across all rebalancing horizons. Across daily, weekly, and monthly rebalancing horizons, slightly trails the top daily performer, approaches the leading weekly method, and matches or surpasses most other approaches monthly, thus consistently ranking among the best-performing models. This robust performance does not come at the cost of excessive turnover, as CAB’s turnover measures remain moderate compared to methods that may obtain marginally lower variances only at the expense of frequent portfolio rebalancing (e.g., , , ).

| Daily | Weekly | Monthly | ||||||

|---|---|---|---|---|---|---|---|---|

| 0.018132 | 0.005733 | 0.018115 | 0.002567 | 0.018060 | 0.001282 | |||

| 0.001991 | 0.125568 | 0.002527 | 0.055395 | 0.002631 | 0.025707 | |||

| 0.002451 | 0.001445 | 0.002453 | 0.000653 | 0.002461 | 0.000369 | |||

| 0.002475 | 0.079388 | 0.002482 | 0.037928 | 0.002554 | 0.016088 | |||

| 0.002655 | 0.098020 | 0.003373 | 0.047089 | 0.003598 | 0.022957 | |||

| 0.002774 | 0.001816 | 0.002777 | 0.000956 | 0.002784 | 0.000620 | |||

| 0.002281 | 0.126519 | 0.002580 | 0.049839 | 0.002713 | 0.014816 | |||

| 0.002075 | 0.116446 | 0.002388 | 0.051710 | 0.002524 | 0.017159 | |||

| 0.002048 | 0.129453 | 0.002448 | 0.056173 | 0.002618 | 0.023470 | |||

| 0.002680 | 0.197322 | 0.002722 | 0.072903 | 0.002657 | 0.023108 | |||

| 0.002647 | 0.125512 | 0.002689 | 0.055954 | 0.002733 | 0.024767 | |||

| 0.002293 | 0.078799 | 0.002428 | 0.048383 | 0.002579 | 0.023807 | |||

When compared to the benchmark, please note that all models present a statistically significant lower annual variance, based on the one-side F-Test of equalities of variance.

Examining the same metrics across distinct market regimes (Table LABEL:tab:portfoliovariancesmr) reveals that remains a robust contender under varying conditions: in Bull-1, it consistently competes for the lowest variance, even attaining the best performance in weekly and monthly rebalancing; in the Bear regime, ranks near the top in daily and weekly horizons, balancing lower turnover against marginally higher volatility than a few dynamic methods; and while Bull-2 sees other estimators occasionally surpass , it still demonstrates stable risk control with moderate trading activity, indicating that its effectiveness persists across both tranquil and turbulent market environments.

Comparisons to the benchmark further highlight the importance of adaptivity. While offers minimal turnover, it endures noticeably higher variance in all market conditions, reflecting its inability to exploit up-to-date correlation information. Indeed, the difference in annualised variances between and can reach 80-90 basis points in certain scenarios, a gap that can substantially affect risk-adjusted returns and capital preservation.

Overall, tends to exhibit moderate turnover, balancing the need to adjust to changing correlations without incurring unnecessary trades. This stability benefits investors who must limit transaction costs or adhere to regulatory constraints on turnover. These results underscore that advanced covariance estimation can yield economically meaningful improvements in risk control, particularly over the medium-term horizons favoured by many institutional investors. The model stands out by combining strong variance reduction with stable rebalancing behaviour, balancing responsiveness to market changes and turnover efficiency.

6 Conclusion

We propose a novel DL framework for medium-term covariance forecasting in multi-asset portfolios, combining 3D convolutions, bidirectional LSTMs, and multi-head attention. Empirical tests on various ETFs from 2017 to 2023 reveal that this model, enhanced by a final shrinkage step, consistently outperforms classical benchmarks across different forecast horizons and market regimes.

Notably, its performance advantage remains robust whether one subtracts a risk-free rate from returns, suggesting broad applicability in diverse portfolio management practices.

In portfolio experiments, the proposed method enables global minimum-variance (GMV) strategies to achieve lower out-of-sample volatility with moderate turnover, underlining the tangible economic value of improved covariance estimation. By bridging cutting-edge DL techniques with established financial principles, our work highlights the promise of sophisticated spatiotemporal modelling for risk management and allocation decisions, especially at horizons where structural shifts and evolving correlations pose unique forecasting challenges.

Still, several research avenues warrant further exploration. First, extending the network architecture to accommodate skewed or heavy-tailed distributions could better capture tail risk in times of market stress. Second, explicitly incorporating transaction costs or liquidity constraints within the optimisation process might yield more realistic and implementable trading strategies. Finally, evaluating the model in larger cross-sectional settings or applied to alternative asset classes (e.g., commodities, crypto assets) would illuminate its scalability and robustness.

We hope these findings encourage the finance community to explore and adapt advanced neural architectures for medium-term and long-horizon applications, strengthening the link between machine learning innovation and effective real-world asset allocation.

References

- Akiba et al., (2019) Akiba, T., Sano, S., Yanase, T., Ohta, T., and Koyama, M. (2019). Optuna: A next-generation hyperparameter optimization framework. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 2623–2631. ACM.

- Baillie and Bollerslev, (1992) Baillie, R. T. and Bollerslev, T. (1992). Prediction in dynamic models with time-dependent conditional variances. Journal of Econometrics, 52(1):91–113.

- Bollerslev, (1990) Bollerslev, T. (1990). Modelling the coherence in short-run nominal exchange rates: A multivariate generalized arch model. The Review of Economics and Statistics, 72(3):498–505.

- Bollerslev et al., (2018) Bollerslev, T., Patton, A. J., and Quaedvlieg, R. (2018). Modeling and forecasting (un)reliable realized covariances for more reliable financial decisions. Journal of Econometrics, 207(1):71–91.

- Chiriac and Voev, (2011) Chiriac, R. and Voev, V. (2011). Modelling and forecasting multivariate realized volatility. Journal of Applied Econometrics, 26(6):922–947.

- Cont, (2001) Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2):223.

- Corsi, (2009) Corsi, F. (2009). A simple approximate long-memory model of realized volatility. Journal of Financial Econometrics, 7(2):174–196.

- De Nard et al., (2022) De Nard, G., Engle, R. F., Ledoit, O., and Wolf, M. (2022). Large dynamic covariance matrices: Enhancements based on intraday data. Journal of Banking & Finance, 138:106426.

- De Nard et al., (2021) De Nard, G., Ledoit, O., and Wolf, M. (2021). Factor models for portfolio selection in large dimensions: The good, the better and the ugly. Journal of Financial Econometrics, 19(2):236–257.

- De Nard et al., (2024) De Nard, G., Ledoit, O., and Wolf, M. (2024). Improved tracking-error management for active and passive investing. Available at SSRN 4898624.

- DeMiguel et al., (2009) DeMiguel, V., Garlappi, L., Nogales, F. J., and Uppal, R. (2009). A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management Science, 55:798–812.

- Demsar, (2006) Demsar, J. (2006). Statistical comparisons of classifiers over multiple data sets. J. Mach. Learn. Res., 7:1–30.

- Elton and Gruber, (1973) Elton, E. J. and Gruber, M. J. (1973). Estimating the dependence structure of share prices–implications for portfolio selection. The Journal of Finance, 28(5):1203–1232.

- Engle, (2002) Engle, R. (2002). Dynamic conditional correlation. Journal of Business & Economic Statistics, 20(3):339–350.

- Engle and Sheppard, (2001) Engle, R. F. and Sheppard, K. (2001). Theoretical and empirical properties of dynamic conditional correlation multivariate garch. Working Paper 8554, National Bureau of Economic Research.

- Gu et al., (2020) Gu, S., Kelly, B., and Xiu, D. (2020). Empirical asset pricing via machine learning. The Review of Financial Studies, 33:2223–2273.

- Hansen, (1994) Hansen, B. E. (1994). Autoregressive conditional density estimation. International Economic Review, 35(3):705–730.

- Harvey, (1997) Harvey, A. (1997). Trends, cycles and autoregressions. The Economic Journal, 107(440):192–201.

- Hochreiter, (1997) Hochreiter, S. (1997). Long short-term memory. Neural Computation MIT-Press.

- J.P.Morgan, (1996) J.P.Morgan (1996). Riskmetrics technical document. Morgan Guaranty Trust Company of New York.

- Kim et al., (2023) Kim, I., Lee, M., and Seok, J. (2023). Icegan: inverse covariance estimating generative adversarial network. Machine Learning: Science and Technology, 4:025008.

- Kourtis, (2014) Kourtis, A. (2014). On the distribution and estimation of trading costs. Journal of Empirical Finance, 28:104–117.

- Kourtis et al., (2012) Kourtis, A., Dotsis, G., and Markellos, R. N. (2012). Parameter uncertainty in portfolio selection: Shrinking the inverse covariance matrix. Journal of Banking & Finance, 36(9):2522–2531.

- Laloux et al., (2000) Laloux, L., Cizeau, P., Potters, M., and Bouchaud, J.-P. (2000). Random matrix theory and financial correlations. International Journal of Theoretical and Applied Finance, 03:391–397.

- Lecun et al., (1998) Lecun, Y., Bottou, L., Bengio, Y., and Haffner, P. (1998). Gradient-based learning applied to document recognition. Proceedings of the IEEE, 86(11):2278–2324.

- Ledoit and Wolf, (2003) Ledoit, O. and Wolf, M. (2003). Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of Empirical Finance, 10(5):603–621.

- Ledoit and Wolf, (2004) Ledoit, O. and Wolf, M. (2004). A well-conditioned estimator for large-dimensional covariance matrices. Journal of Multivariate Analysis, 88(2):365–411.

- Ledoit and Wolf, (2020) Ledoit, O. and Wolf, M. (2020). Analytical nonlinear shrinkage of large-dimensional covariance matrices. The Annals of Statistics, 48(5):3043 – 3065.

- Ledoit and Wolf, (2022) Ledoit, O. and Wolf, M. (2022). The power of (non-)linear shrinking: A review and guide to covariance matrix estimation. Journal of Financial Econometrics, 20:187–218.

- Liu and Guo, (2019) Liu, G. and Guo, J. (2019). Bidirectional lstm with attention mechanism and convolutional layer for text classification. Neurocomputing, 337:325–338.

- Markowitz, (1952) Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7:77–91.

- Nazareth and Ramana Reddy, (2023) Nazareth, N. and Ramana Reddy, Y. V. (2023). Financial applications of machine learning: A literature review. Expert Systems with Applications, 219:119640.

- Olorunnimbe and Viktor, (2023) Olorunnimbe, K. and Viktor, H. (2023). Deep learning in the stock market—a systematic survey of practice, backtesting, and applications. Artificial Intelligence Review, 56(3):2057–2109.

- Reis et al., (2024) Reis, P., Serra, A. P., and Gama, J. (2024). The role of deep learning in financial asset management: A systematic review. Authorea, Inc.

- Robert F. Engle and Wolf, (2019) Robert F. Engle, O. L. and Wolf, M. (2019). Large dynamic covariance matrices. Journal of Business & Economic Statistics, 37(2):363–375.

- Sandoval and Franca, (2012) Sandoval, L. and Franca, I. D. P. (2012). Correlation of financial markets in times of crisis. Physica A: Statistical Mechanics and its Applications, 391(1):187–208.

- Symitsi et al., (2018) Symitsi, E., Symeonidis, L., Kourtis, A., and Markellos, R. (2018). Covariance forecasting in equity markets. Journal of Banking & Finance, 96:153–168.

- Vaswani et al., (2017) Vaswani, A., Shazeer, N. M., Parmar, N., Uszkoreit, J., Jones, L., Gomez, A. N., Kaiser, L., and Polosukhin, I. (2017). Attention is all you need. In Neural Information Processing Systems.

- Zhang et al., (2024) Zhang, C., Pu, X., Cucuringu, M., and Dong, X. (2024). Graph-based methods for forecasting realized covariances. Journal of Financial Econometrics, page nbae026.

Appendix A Appendix

A.1 LSTM cell detailed explanation

An LSTM (Hochreiter,, 1997) cell consists of three main gates: the forget gate (), the input gate (), and the output gate (). They are respectively calculated as:

| (A.1) |

| (A.2) |

| (A.3) |

where is the vector input at time , is the hidden vector state, , and are weight matrices, and , and are bias vectors. The sigmoid function ensures that the output values are between 0 and 1, representing how much each component should be forgotten.

The forget gate decides what information should be discarded from the cell state. Next, the input gate determines what new information should be added to the cell state. This process involves two steps: calculating the input gate Eq. (A.2) and creating new candidate values:

| (A.4) |

where is the weight matrix, and is a bias vector. The input gate modulates the extent to which new information is added to the cell state. The cell state update combines the forget gate and input gate operations to update the cell state:

| (A.5) |

This equation ensures that the cell state retains essential information over long periods.

Finally, the output gate controls what information should be outputted from the cell. This involves two steps: calculating the output gate Eq. (A.3) and determining the hidden state:

| (A.6) |

A.2 Hyperparameter Grid Search

| Hyperparameter | Range |

|---|---|

| Optimiser | Adam, SGD |

| Batch size | 32, 64, 128, 256 |

| Learning rate | , , |

| Lookback window () | 20, 40, 60, 80, 100, 120, 250 |

| 3D convolution kernel size () | 3, 5, 7 |

| BiLSTM hidden dimensions () | 32, 64, 128, 256 |

| BiLSTM stacked layers () | 3, 4, 5, 6, 7 |

| Number of heads ()a | 2, 4, 6, 8, 16, 32 |

| Shrinkage factor () | 0.00, 0.20, 0.40, 0.60, 0.80, 1.00 |

A.3 Extended Data Tables

| Overall | Bull-1 | Bear | Bull-2 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

70.309 | 107.739 | 54.194 | 82.600 | 107.447 | 165.092 | 69.960 | 107.363 | ||||

| 62.260 | 95.586 | 46.956 | 71.921 | 106.652 | 163.471 | 59.271 | 91.185 | |||||

| 58.851 | 90.253 | 42.125 | 64.612 | 94.704 | 145.253 | 59.272 | 90.889 | |||||

| 63.548 | 97.681 | 47.376 | 72.757 | 104.804 | 160.926 | 62.036 | 95.449 | |||||

| 75.861 | 115.370 | 69.194 | 104.027 | 105.832 | 162.356 | 71.461 | 109.054 | |||||

| 58.111 | 89.824 | 42.451 | 65.818 | 95.819 | 147.003 | 57.301 | 88.763 | |||||

| 62.210 | 95.018 | 48.557 | 73.797 | 96.913 | 147.989 | 60.972 | 93.374 | |||||

| 65.361 | 99.154 | 51.461 | 77.640 | 100.48 | 152.649 | 64.160 | 97.548 | |||||

| 71.266 | 109.164 | 54.984 | 83.752 | 110.811 | 170.301 | 70.323 | 107.864 | |||||

| 71.064 | 108.951 | 54.819 | 83.588 | 110.623 | 170.011 | 70.094 | 107.641 | |||||

| 56.954 | 87.317 | 44.134 | 67.401 | 94.689 | 145.287 | 54.291 | 83.369 | |||||

|

|

45.872 | 70.272 | 24.755 | 38.850 | 72.135 | 108.838 | 51.939 | 79.449 | ||||

| 47.436 | 72.906 | 31.056 | 47.811 | 90.540 | 139.813 | 45.522 | 69.719 | |||||

| 44.734 | 68.528 | 26.175 | 40.546 | 74.009 | 112.405 | 48.262 | 73.923 | |||||

| 43.441 | 66.728 | 23.834 | 37.275 | 76.162 | 114.702 | 46.645 | 71.886 | |||||

| 63.848 | 96.730 | 62.374 | 93.125 | 78.628 | 122.264 | 60.501 | 91.635 | |||||

| 43.434 | 67.183 | 27.608 | 43.493 | 75.190 | 114.891 | 44.465 | 68.675 | |||||

| 42.622 | 66.124 | 27.194 | 42.996 | 73.983 | 113.348 | 43.509 | 67.391 | |||||

| 43.764 | 67.604 | 28.135 | 44.201 | 75.173 | 114.919 | 44.767 | 69.024 | |||||

| 46.390 | 71.007 | 24.934 | 39.238 | 72.294 | 109.567 | 52.781 | 80.410 | |||||

| 46.177 | 70.771 | 24.796 | 39.028 | 72.411 | 109.269 | 52.424 | 80.176 | |||||

| 22.851 | 35.411 | 13.091 | 20.268 | 42.372 | 65.754 | 23.505 | 36.408 | |||||

|

|

44.053 | 68.114 | 26.115 | 42.593 | 72.110 | 109.681 | 47.531 | 72.584 | ||||

| 45.519 | 69.961 | 30.907 | 47.659 | 83.084 | 128.667 | 44.068 | 67.348 | |||||

| 44.704 | 68.490 | 26.626 | 41.728 | 74.557 | 112.995 | 47.751 | 72.910 | |||||

| 42.035 | 65.084 | 24.836 | 40.385 | 75.018 | 113.948 | 43.600 | 66.895 | |||||

| 62.001 | 93.989 | 62.649 | 93.590 | 69.286 | 108.383 | 59.458 | 90.055 | |||||

| 42.647 | 66.037 | 29.089 | 45.917 | 68.525 | 105.242 | 43.916 | 67.686 | |||||

| 40.986 | 63.934 | 26.426 | 42.585 | 69.459 | 106.517 | 42.150 | 65.398 | |||||

| 42.268 | 65.595 | 27.106 | 43.443 | 71.582 | 109.283 | 43.579 | 67.259 | |||||

| 44.550 | 68.801 | 26.466 | 43.142 | 72.705 | 111.010 | 48.096 | 73.173 | |||||

| 44.334 | 68.575 | 26.291 | 42.936 | 72.803 | 110.768 | 47.761 | 72.940 | |||||

| 22.305 | 34.990 | 12.842 | 20.226 | 39.166 | 62.879 | 23.540 | 36.458 | |||||

|

|

43.972 | 68.530 | 30.179 | 49.646 | 76.424 | 117.032 | 43.479 | 66.670 | ||||

| 43.572 | 67.004 | 30.527 | 47.207 | 83.143 | 128.419 | 40.520 | 61.975 | |||||

| 44.720 | 68.781 | 28.925 | 45.742 | 73.402 | 111.890 | 46.624 | 71.190 | |||||

| 42.446 | 66.204 | 28.694 | 47.283 | 79.704 | 121.665 | 40.527 | 62.340 | |||||

| 60.006 | 91.073 | 61.704 | 92.289 | 64.055 | 100.713 | 57.724 | 87.477 | |||||

| 43.390 | 67.342 | 32.735 | 51.757 | 68.495 | 105.076 | 42.999 | 66.475 | |||||

|

|

40.234 | 63.342 | 29.961 | 48.303 | 65.688 | 101.473 | 39.492 | 62.005 | ||||

| 42.615 | 66.462 | 29.762 | 48.148 | 71.380 | 108.855 | 42.584 | 66.011 | |||||

| 44.464 | 69.171 | 30.520 | 50.091 | 76.867 | 118.267 | 44.085 | 67.265 | |||||

| 44.239 | 68.951 | 30.343 | 49.925 | 77.105 | 118.060 | 43.693 | 67.005 | |||||

| 13.977 | 21.752 | 10.080 | 16.184 | 20.742 | 32.133 | 14.538 | 22.346 | |||||

|

|

48.590 | 75.398 | 36.397 | 59.019 | 84.342 | 128.425 | 46.097 | 70.593 | ||||

| 41.909 | 64.465 | 31.713 | 49.127 | 84.615 | 129.958 | 36.093 | 55.352 | |||||

| 45.330 | 69.861 | 33.556 | 53.195 | 71.953 | 109.497 | 45.222 | 69.142 | |||||

| 47.098 | 73.175 | 34.956 | 56.786 | 87.296 | 132.635 | 43.277 | 66.502 | |||||

| 58.216 | 88.420 | 60.114 | 90.286 | 64.569 | 100.736 | 55.133 | 83.621 | |||||

| 44.163 | 68.631 | 36.440 | 57.692 | 71.518 | 108.718 | 41.212 | 64.060 | |||||

| 40.946 | 64.563 | 33.741 | 54.358 | 68.094 | 104.261 | 37.719 | 59.629 | |||||

| 44.082 | 68.671 | 34.120 | 54.937 | 74.174 | 112.239 | 41.789 | 64.902 | |||||

| 49.115 | 76.015 | 36.715 | 59.374 | 84.740 | 129.651 | 46.794 | 71.202 | |||||

| 48.867 | 75.827 | 36.519 | 59.220 | 85.041 | 129.486 | 46.352 | 70.985 | |||||

| 12.635 | 19.816 | 10.718 | 17.319 | 18.659 | 29.190 | 12.125 | 18.707 | |||||

|

|

57.475 | 88.882 | 50.083 | 79.438 | 92.682 | 140.191 | 52.022 | 80.073 | ||||

| 38.460 | 59.180 | 32.171 | 49.910 | 82.117 | 124.805 | 29.829 | 46.088 | |||||

| 50.035 | 77.019 | 43.437 | 68.307 | 76.903 | 116.122 | 46.487 | 71.288 | |||||

| 56.137 | 86.937 | 49.005 | 77.757 | 94.604 | 142.932 | 49.567 | 76.591 | |||||

| 54.308 | 82.570 | 54.261 | 81.972 | 45.646 | 95.111 | 52.187 | 79.306 | |||||

| 44.949 | 70.232 | 40.531 | 64.242 | 72.901 | 110.150 | 39.678 | 62.498 | |||||

| 46.528 | 72.381 | 41.217 | 65.244 | 75.945 | 114.305 | 41.410 | 64.807 | |||||

| 46.532 | 72.386 | 41.220 | 65.248 | 75.950 | 114.312 | 41.414 | 64.812 | |||||

| 58.026 | 89.446 | 50.494 | 79.976 | 92.884 | 141.079 | 52.765 | 80.559 | |||||

| 57.744 | 89.294 | 50.351 | 79.843 | 93.189 | 140.964 | 52.223 | 80.384 | |||||

| 12.356 | 19.146 | 11.116 | 17.602 | 18.159 | 27.468 | 11.472 | 17.726 | |||||

|

|

76.850 | 117.44 | 107.237 | 163.541 | 79.505 | 120.16 | 56.341 | 86.706 | ||||

| 34.002 | 52.367 | 33.076 | 51.123 | 64.126 | 97.309 | 25.830 | 40.087 | |||||

| 53.737 | 82.720 | 53.030 | 82.554 | 72.648 | 109.762 | 48.689 | 74.953 | |||||

| 74.903 | 114.697 | 103.984 | 158.986 | 80.825 | 122.029 | 54.291 | 83.797 | |||||

| 49.653 | 75.499 | 47.293 | 71.542 | 45.646 | 70.522 | 52.353 | 79.519 | |||||

| 43.487 | 68.479 | 42.628 | 67.459 | 58.966 | 89.895 | 39.537 | 62.904 | |||||

| 40.299 | 64.494 | 38.892 | 62.869 | 53.375 | 82.622 | 37.405 | 60.269 | |||||

| 40.223 | 66.604 | 49.514 | 77.717 | 81.610 | 120.697 | 22.135 | 43.633 | |||||

| 77.628 | 118.284 | 108.476 | 165.211 | 79.544 | 120.791 | 57.035 | 87.075 | |||||

| 77.315 | 118.139 | 108.26 | 165.074 | 79.841 | 120.668 | 56.481 | 86.919 | |||||

| 16.116 | 24.758 | 22.511 | 34.543 | 16.201 | 24.572 | 11.938 | 18.457 | |||||

| Overall | Bull-1 | Bear | Bull-2 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

70.309 | 107.739 | 54.193 | 82.599 | 107.449 | 165.094 | 69.959 | 107.362 | ||||

| 62.057 | 95.297 | 46.340 | 71.028 | 107.068 | 164.102 | 59.155 | 91.020 | |||||

| 58.908 | 90.338 | 42.125 | 64.612 | 94.704 | 145.253 | 59.384 | 91.053 | |||||

| 63.547 | 97.680 | 47.376 | 72.755 | 104.804 | 160.927 | 62.035 | 95.448 | |||||

| 75.854 | 115.361 | 69.181 | 104.007 | 105.831 | 162.355 | 71.457 | 109.048 | |||||

| 58.092 | 89.783 | 42.384 | 65.733 | 95.843 | 147.035 | 57.300 | 88.730 | |||||

| 62.186 | 94.973 | 48.470 | 73.686 | 96.894 | 147.968 | 60.986 | 93.364 | |||||

| 65.338 | 99.111 | 51.367 | 77.516 | 100.447 | 152.608 | 64.186 | 97.557 | |||||

| 71.265 | 109.164 | 54.983 | 83.750 | 110.813 | 170.304 | 70.322 | 107.863 | |||||

| 71.064 | 108.951 | 54.818 | 83.587 | 110.625 | 170.014 | 70.093 | 107.640 | |||||

| 58.272 | 89.475 | 43.967 | 67.109 | 94.554 | 145.032 | 56.996 | 87.822 | |||||

|

|

45.876 | 70.278 | 24.754 | 38.850 | 72.131 | 108.833 | 51.948 | 79.462 | ||||

| 47.200 | 72.577 | 30.161 | 46.526 | 91.426 | 141.121 | 45.386 | 69.534 | |||||

| 44.796 | 68.618 | 26.174 | 40.545 | 74.005 | 112.399 | 48.383 | 74.100 | |||||

| 43.444 | 66.733 | 23.834 | 37.275 | 76.161 | 114.700 | 46.652 | 71.896 | |||||

| 63.845 | 96.725 | 62.359 | 93.102 | 78.638 | 122.279 | 60.502 | 91.636 | |||||

| 43.321 | 67.023 | 27.469 | 43.276 | 75.123 | 114.858 | 44.354 | 68.515 | |||||

| 42.585 | 66.060 | 27.081 | 42.811 | 74.082 | 113.527 | 43.481 | 67.335 | |||||

| 43.739 | 67.556 | 28.016 | 44.008 | 75.278 | 115.106 | 44.766 | 69.003 | |||||

| 46.394 | 71.012 | 24.934 | 39.237 | 72.291 | 109.562 | 52.789 | 80.423 | |||||

| 46.181 | 70.777 | 24.796 | 39.027 | 72.408 | 109.265 | 52.432 | 80.188 | |||||

| 26.619 | 41.417 | 13.427 | 20.765 | 45.197 | 69.510 | 29.777 | 46.649 | |||||

|

|

44.060 | 68.125 | 26.115 | 42.593 | 72.109 | 109.679 | 47.545 | 72.605 | ||||

| 45.268 | 69.612 | 30.016 | 46.385 | 84.049 | 130.081 | 43.879 | 67.086 | |||||

| 44.759 | 68.570 | 26.625 | 41.727 | 74.548 | 112.981 | 47.861 | 73.069 | |||||

| 42.043 | 65.095 | 24.836 | 40.385 | 75.020 | 113.951 | 43.615 | 66.916 | |||||

| 62.000 | 93.988 | 62.634 | 93.568 | 69.301 | 108.405 | 59.462 | 90.061 | |||||

| 42.543 | 65.895 | 28.943 | 45.693 | 68.234 | 104.807 | 43.895 | 67.683 | |||||

| 39.404 | 61.909 | 26.764 | 42.978 | 64.589 | 100.135 | 40.279 | 63.072 | |||||

| 42.240 | 65.544 | 27.015 | 43.295 | 71.326 | 108.855 | 43.658 | 67.380 | |||||

| 44.557 | 68.811 | 26.466 | 43.142 | 72.705 | 111.009 | 48.109 | 73.194 | |||||

| 44.341 | 68.586 | 26.291 | 42.935 | 72.803 | 110.767 | 47.775 | 72.961 | |||||

| 24.079 | 37.328 | 13.698 | 21.649 | 43.977 | 68.513 | 25.026 | 38.428 | |||||

|

|

43.982 | 68.545 | 30.179 | 49.646 | 76.435 | 117.049 | 43.496 | 66.694 | ||||

| 43.314 | 66.645 | 29.713 | 46.043 | 84.231 | 130.003 | 40.232 | 61.574 | |||||

| 44.761 | 68.841 | 28.925 | 45.742 | 73.405 | 111.893 | 46.704 | 71.306 | |||||

| 42.457 | 66.219 | 28.694 | 47.283 | 79.715 | 121.682 | 40.544 | 62.365 | |||||

| 60.007 | 91.075 | 61.690 | 92.268 | 64.073 | 100.740 | 57.731 | 87.486 | |||||

| 43.276 | 67.199 | 32.551 | 51.513 | 68.021 | 104.421 | 43.036 | 66.546 | |||||

| 40.134 | 63.219 | 29.870 | 48.186 | 65.191 | 100.793 | 39.503 | 62.039 | |||||

| 42.532 | 66.357 | 29.680 | 48.045 | 70.880 | 108.147 | 42.622 | 66.080 | |||||

| 44.474 | 69.186 | 30.520 | 50.092 | 76.878 | 118.284 | 44.100 | 67.288 | |||||

| 44.249 | 68.966 | 30.343 | 49.925 | 77.116 | 118.077 | 43.709 | 67.029 | |||||

| 14.661 | 23.076 | 10.115 | 16.203 | 22.040 | 34.086 | 15.465 | 24.333 | |||||

|

|

48.604 | 75.417 | 36.397 | 59.018 | 84.366 | 128.460 | 46.116 | 70.620 | ||||

| 41.664 | 64.124 | 31.048 | 48.181 | 85.754 | 131.620 | 35.717 | 54.821 | |||||

| 45.361 | 69.908 | 33.555 | 53.194 | 71.959 | 109.504 | 45.282 | 69.232 | |||||

| 47.111 | 73.194 | 34.955 | 56.785 | 87.320 | 132.670 | 43.296 | 66.530 | |||||

| 58.219 | 88.425 | 60.101 | 90.267 | 64.599 | 100.781 | 55.138 | 83.629 | |||||

| 44.126 | 68.610 | 36.335 | 57.587 | 71.120 | 108.182 | 41.325 | 64.245 | |||||

|

|

43.988 | 68.569 | 34.032 | 54.862 | 73.636 | 111.512 | 41.819 | 64.965 | ||||

| 44.025 | 68.619 | 34.051 | 54.887 | 73.690 | 111.582 | 41.864 | 65.025 | |||||

| 49.129 | 76.034 | 36.715 | 59.373 | 84.764 | 129.686 | 46.813 | 71.230 | |||||

| 48.881 | 75.846 | 36.519 | 59.219 | 85.065 | 129.521 | 46.371 | 71.013 | |||||

| 12.118 | 18.831 | 9.496 | 15.248 | 17.864 | 27.435 | 12.147 | 18.653 | |||||

|

|

57.494 | 88.910 | 50.085 | 79.441 | 92.730 | 140.261 | 52.044 | 80.105 | ||||

| 38.294 | 58.953 | 31.839 | 49.444 | 83.328 | 126.577 | 29.370 | 45.434 | |||||

| 50.062 | 77.060 | 43.438 | 68.309 | 76.943 | 116.140 | 46.536 | 71.363 | |||||

| 56.156 | 86.964 | 49.007 | 77.759 | 94.651 | 143.001 | 49.589 | 76.623 | |||||

| 54.314 | 82.579 | 54.255 | 81.962 | 61.748 | 95.188 | 52.188 | 79.307 | |||||

| 44.844 | 70.073 | 40.368 | 64.069 | 72.299 | 109.109 | 39.755 | 62.603 | |||||

| 46.364 | 72.137 | 41.041 | 65.057 | 75.312 | 113.195 | 41.391 | 64.777 | |||||

| 46.406 | 72.191 | 41.077 | 65.104 | 75.366 | 113.267 | 41.432 | 64.830 | |||||

| 58.045 | 89.474 | 50.496 | 79.979 | 92.932 | 141.148 | 52.787 | 80.592 | |||||

| 57.763 | 89.322 | 50.352 | 79.846 | 93.237 | 141.034 | 52.245 | 80.416 | |||||

| 12.828 | 19.854 | 11.180 | 17.728 | 20.372 | 30.851 | 11.702 | 18.031 | |||||

|

|

76.900 | 117.511 | 107.237 | 163.540 | 79.568 | 120.252 | 56.420 | 86.818 | ||||

| 34.000 | 52.376 | 33.222 | 51.351 | 65.353 | 99.107 | 25.373 | 39.432 | |||||

| 53.792 | 82.799 | 53.034 | 82.561 | 72.673 | 109.796 | 48.785 | 75.090 | |||||

| 74.952 | 114.767 | 103.983 | 158.985 | 80.888 | 122.122 | 54.369 | 83.906 | |||||

| 49.692 | 75.555 | 47.295 | 71.544 | 45.710 | 70.616 | 52.408 | 79.599 | |||||

| 43.349 | 68.233 | 42.431 | 67.189 | 58.278 | 88.611 | 39.597 | 62.977 | |||||

| 40.167 | 64.257 | 38.751 | 62.682 | 52.667 | 81.284 | 37.446 | 60.321 | |||||

| 40.261 | 66.455 | 49.351 | 77.363 | 80.796 | 119.188 | 22.552 | 44.012 | |||||

| 77.678 | 118.355 | 108.475 | 165.210 | 79.607 | 120.884 | 57.115 | 87.187 | |||||

| 77.365 | 118.210 | 108.260 | 165.073 | 79.904 | 120.760 | 56.560 | 87.032 | |||||

| 18.246 | 27.828 | 29.049 | 44.148 | 14.976 | 22.681 | 12.182 | 18.727 | |||||

| Daily | Weekly | Monthly | |||||||

|---|---|---|---|---|---|---|---|---|---|

|

Bull-1 |

0.009883 | 0.005169 | 0.009873 | 0.002335 | 0.009907 | 0.001103 | |||

| 0.000543 | 0.150112 | 0.000794 | 0.060372 | 0.000834 | 0.026885 | ||||

| 0.000731 | 0.001378 | 0.000732 | 0.000607 | 0.000736 | 0.000327 | ||||

| 0.000735 | 0.088541 | 0.000748 | 0.043884 | 0.000754 | 0.015613 | ||||

| 0.001054 | 0.091979 | 0.001572 | 0.044883 | 0.001692 | 0.022283 | ||||

| 0.000780 | 0.001228 | 0.000781 | 0.000610 | 0.000783 | 0.000349 | ||||

| 0.000620 | 0.119486 | 0.000681 | 0.053221 | 0.000728 | 0.013605 | ||||

| 0.000529 | 0.207262 | 0.000698 | 0.093558 | 0.000781 | 0.024324 | ||||

| 0.000522 | 0.217432 | 0.000784 | 0.097809 | 0.000875 | 0.034673 | ||||

| 0.000850 | 0.236835 | 0.000827 | 0.090803 | 0.000795 | 0.020906 | ||||

| 0.000856 | 0.150601 | 0.000860 | 0.067402 | 0.000826 | 0.025859 | ||||

| 0.000634 | 0.086489 | 0.000656 | 0.055931 | 0.000707 | 0.023736 | ||||

|

Bear |

0.029939 | 0.007221 | 0.029940 | 0.003443 | 0.029793 | 0.001599 | |||

| 0.002207 | 0.092111 | 0.002682 | 0.032018 | 0.002959 | 0.018142 | ||||

| 0.002891 | 0.001650 | 0.002892 | 0.000935 | 0.002906 | 0.000436 | ||||

| 0.002908 | 0.079065 | 0.002843 | 0.036314 | 0.003120 | 0.019997 | ||||

| 0.003118 | 0.095723 | 0.003970 | 0.041663 | 0.004754 | 0.021610 | ||||

| 0.003196 | 0.002035 | 0.003197 | 0.001043 | 0.003201 | 0.000570 | ||||

| 0.002497 | 0.129487 | 0.002646 | 0.043843 | 0.002590 | 0.012451 | ||||

| 0.002355 | 0.067768 | 0.002639 | 0.015372 | 0.002636 | 0.005911 | ||||

| 0.002269 | 0.083567 | 0.002652 | 0.024277 | 0.002730 | 0.010308 | ||||

| 0.002800 | 0.114256 | 0.002792 | 0.043637 | 0.002864 | 0.011111 | ||||

| 0.002983 | 0.094396 | 0.002896 | 0.037508 | 0.003153 | 0.023308 | ||||

| 0.002273 | 0.030506 | 0.002464 | 0.022686 | 0.002656 | 0.016836 | ||||

|

Bull-2 |

0.019967 | 0.005666 | 0.019956 | 0.002382 | 0.019933 | 0.001334 | |||

| 0.002823 | 0.118997 | 0.003526 | 0.053457 | 0.003667 | 0.029686 | ||||

| 0.003398 | 0.001426 | 0.003400 | 0.000577 | 0.003406 | 0.000261 | ||||

| 0.003432 | 0.073812 | 0.003433 | 0.034460 | 0.003630 | 0.016887 | ||||

| 0.003512 | 0.102531 | 0.004274 | 0.048313 | 0.004245 | 0.020765 | ||||

| 0.003874 | 0.002113 | 0.003879 | 0.001123 | 0.003889 | 0.000788 | ||||

| 0.003233 | 0.129874 | 0.003635 | 0.047812 | 0.003671 | 0.015276 | ||||

| 0.002947 | 0.071444 | 0.003294 | 0.026871 | 0.003364 | 0.009476 | ||||

| 0.002924 | 0.085242 | 0.003318 | 0.034070 | 0.003365 | 0.012661 | ||||

| 0.003793 | 0.194898 | 0.003678 | 0.063899 | 0.003597 | 0.024379 | ||||

| 0.003668 | 0.118539 | 0.003720 | 0.055498 | 0.003762 | 0.029837 | ||||

| 0.003323 | 0.087821 | 0.003547 | 0.052596 | 0.003885 | 0.029487 | ||||